FED and ECB signal tight monetary policy to continue; Chinese economy shows signs of slowing despite rolling out relief measures

US

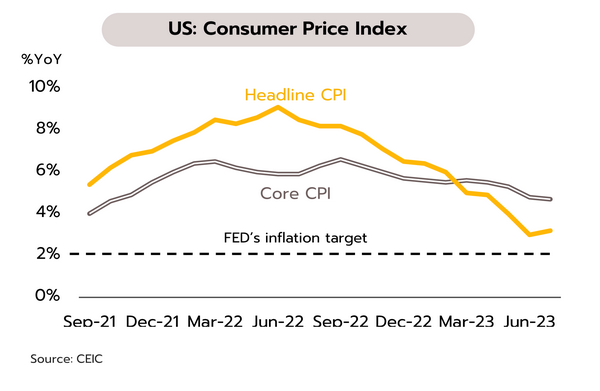

The Fed Chair has indicated that rate hikes may continue, providing greater clarity over the likelihood of a US slowdown. In August, the Consumer Confidence Index slipped from 71.6 to 69.5, while one-year inflation expectations edged down to 3.3% from July’s 3.4%. The Composite PMI was also down, sliding from 52.0 to a 6-month low of 50.4, as were existing-home sales, which softened -2.2% MoM and -16.6% YoY to 4.07m units.

Fed Chair Powell’s speech at the annual central bank meeting in Jackson Hole has increased the likelihood of ‘higher for longer’ interest rates as the Fed looks to maintain pressure on inflation and to keep this within the 2% target over the long run. CME Group’s FedWatch Tool is thus pricing in a 48.6% chance of a 0.25% rate rise being announced in November, up from 33% a week earlier, although this would also imply a heavier risk that a sharper slowdown would follow. Nevertheless, the scope for upward adjustments to inflation is somewhat limited given recent negative readings for a range of economic indicators (including PMIs, private-sector consumption, and growth in credit), and given this and the Fed’s unwillingness to inflict unnecessary pain on the US economy, Krungsri Research sees the Fed will continue to be cautious and not as intense as before. This will help the US economy avoid entering a deep recession.

Eurozone

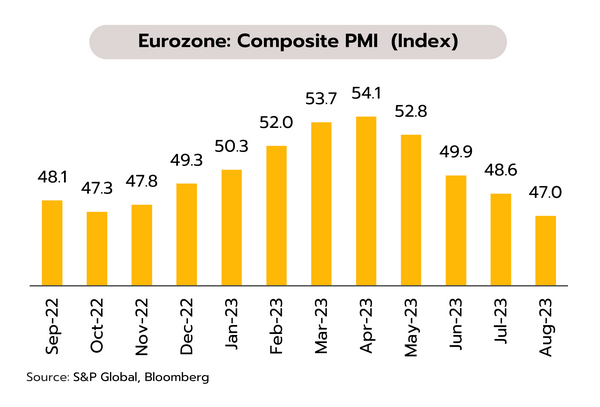

Overall economic weakness in the Eurozone will likely prevent further ECB rate hikes in 2H23. Weak economic data has included August’s drop in the Consumer Confidence Index from -15.1 to -16.0, July’s decline in the Composite PMI from 48.6 to 47.3 (its lowest since November 2020), and the release of the final revision to Q2 data on the German economy, which showed a 0.0% QoQ change but a -0.2% YoY contraction.

The ECB President continues to emphasize the need to maintain tight monetary policy as the authorities strive to keep inflation below the 2% target, but at the start of Q3, the data are indicating an accelerating slowdown across the bloc. Thus, the latest print shows retail sales falling at the sharpest rate in a year, the Economic Sentiment Index is down for 4 months running, and the Composite PMI is at an almost-3-year low, reflecting the elevated risk that the Eurozone will enter recession in 2H23. Given this, we expect that the ECB will likely raise rates only once more, adding 0.25% to the bank’s reference deposit rate to take this to 4.00%. Rates should then remain unchanged through to mid-2024, with the bank preferring to avoid the risk of higher rates triggering a recession, even if inflation remains high.

China

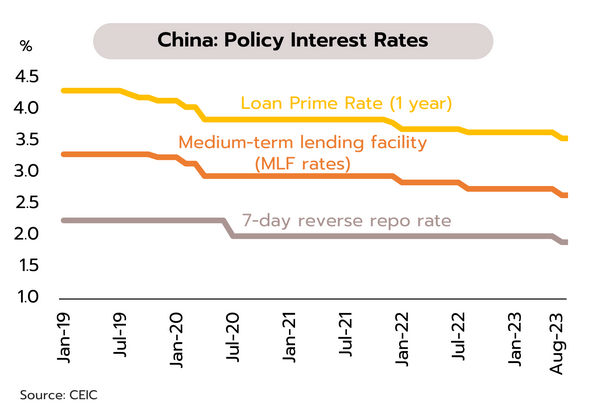

China has cut rates and is trying to aid the real estate market, but their efforts may be insufficient. In the past week, the Chinese authorities have: (i) lifted rules banning those who have had a mortgage (even if fully repaid) from being treated as first-time buyers, potentially boosting property sales in the major cities; (ii) cut the 1-year loan prime rate (LPR) by -0.10% to 3.45%, though the 5-year LPR remains at 4.20%; (iii) allowed local governments to issue bonds worth CNY 1.5 trillion to be used for refinancing; and (iv) reiterated that financial institutions stand ready to help maintain stability in capital markets and to assist with wider economic development, especially after the stock market faced continuous selling pressures.

Unfortunately, these measures are unlikely to be sufficient to counter the headwinds. Although what Beijing calls its ‘new economy’ (green manufacturing and hi-tech production such as microchips) grew by 6.5% in 1H23 to contribute 17% of GDP, contraction in spending on real estate declined by 8%, which together with associated industries accounts for 20% of GDP. This indicates that, while China possesses some growth drivers, these may not be sufficient to fully offset drags on growth from weak global demand, the dissipating effects of China’s reopening, and the effect of property crisis on sentiment and investment.

A recovery in tourism sector will further provide the Thai economy’s primary source of strength this year, while exports are weaker than expected due to slowdowns in trading partner economies

Krungsri Research has revised our forecast for 2023 tourist arrivals upward to 28-29m, though we remain cautious about the level of receipts generated by the sector. The Ministry of Tourism reports that between 1 January and 20 August, 17.03m foreign arrivals were recorded, this generating income worth THB 741.42bn. The 5 most important markets were Malaysia (2.66m arrivals), China (2.11m), South Korea (1.02m), India (0.98m), and Russia (0.90m).

The tourism sector continues to strengthen, and in July, arrivals hit 2.49m, the highest monthly total since Thailand’s post-Covid reopening. The Chinese market has also returned to top spot with total Chinese arrivals breaching the 400,000 mark for the first time in July. China was followed in importance by Malaysia, South Korea, India, and Vietnam. With the number of flights to Thailand increasing and greater clarity over the political situation likely to strengthen confidence in Thailand ahead of the Q4 high season, we now expect combined 2023 arrivals to reach 28-29m, up from our earlier forecast of 27m. However, the impacts of this on sectoral income will be limited since per person spending on tourism has weakened. Compared to the 2019 pre-Covid average of THB 48,000 per person per trip, over the first 7 months of 2023, this dropped to an average of just THB 41,000.

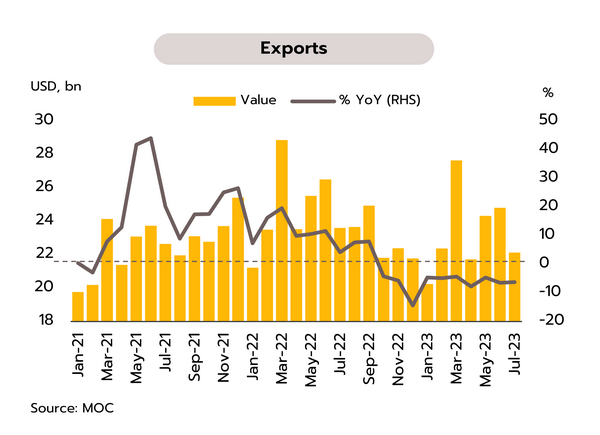

The value of exports was down -6.2% YoY in July, the 10th consecutive month of contraction, and we are now revising our forecast for 2023 exports down to a drop of -1.5%. The Ministry of Commerce reports that in July, exports generated receipts of USD 22.1bn, a decline of -6.2% YoY that was significantly worse than market expectations of a fall of just -0.8%, though excluding oil, gold and weapons reduces the drop to -2.0%. Exports to most of the major overseas markets declined, including those to China, Japan, the EU, the ASEAN-5, and the CLMV countries, while the US returned to minor gains following a decline a month earlier. Exports of agricultural and agro-processing goods slid for the 3rd month and for these a -7.7% drop was reported, with exports of industrial goods also extending the previous month’s decline by softening by a further -3.4%. For the first 7 months of the year (January-July), the total value of exports therefore weakened -5.5%.

With declines in July’s export value down more than 10% from June’s USD 24.8bn and below the 1H23 average of USD 23.5bn per month. This reflects the continued weakness in exports amidst a global economic slowdown, as a result of tight monetary policy in major economies. Moreover, China, an important trade partner for Thailand, is suffering from a slowing economy as the impetus given by the reopening peters out and the rolling real estate crisis drags on spending. The export sector is thus likely to remain fragile through the remainder of the year. Any return to growth on a year-on-year basis that would be seen in 4Q23 will be heavily influenced by the weak data in 4Q22, when China was in lockdown. We have therefore now cut our forecast for 2023 export growth, and in place of our earlier forecast of growth of 0.5%, we now see a contraction of -1.5%.