End of rate-hike cycle in the US and Eurozone are facing more challenge while Chinese slowdown may impact other Asian economies

US

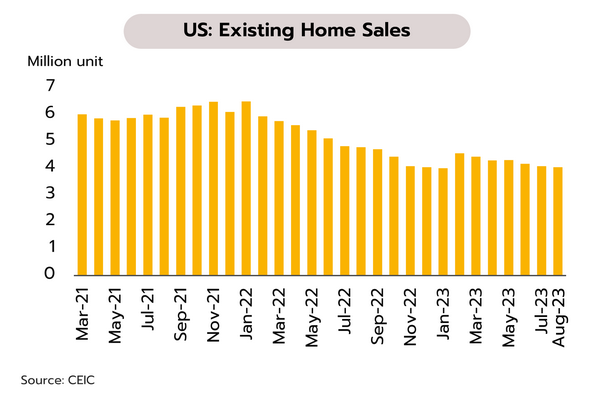

US FOMC opens door for another rate hike this year with upward forecast of 2023 GDP, supporting chance of ongoing ‘Goldilocks’ recovery. The Fed has made a ‘hawkish pause’, holding rates steady at the 22-year high of 5.25-5.50% but indicating that a hike to 5.6% may be made before the year-end, followed by possible cuts to 5.1% at end-2024 and 3.9% at end-2025. Forecast 2023 GDP growth has also been raised from 1.0% to 2.1%. Existing home sales contracted -0.7% MoM to 4.04mn units in August. September’s Flash Services PMI slipped from 50.5 to an 8-month low of 50.2, and the Flash Composite PMI edged down from 50.2 to 50.1.

The US economy is decelerating but the strength of labor markets makes a recession unlikely, and 2023 and 2024 growth should be stronger than expected. Moreover, although inflation remains above the Fed’s 2% target range, it is also cooling. Keeping interest rates elevated over an extended period may drag on the economy, risking extended sluggishness and raising recession risk. At its most recent meeting, the FOMC kept the door open to the possibility of announcing a 0.25% rate rise at its last meeting of 2023, taking policy rates to 5.50-5.75%, where they will remain until clear evidence has emerged that inflation will stay in the 2% target range over the long term.

Eurozone

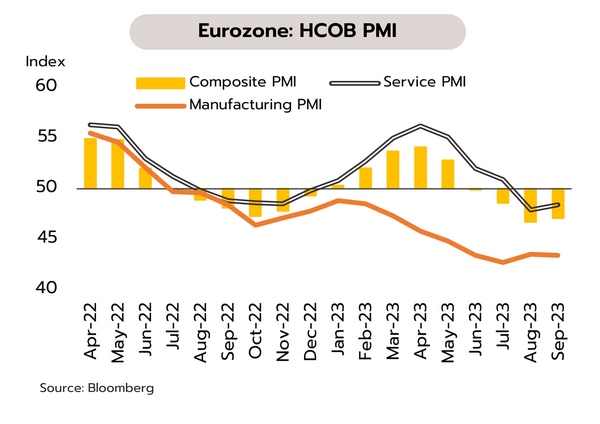

High inflation continues to weigh on the Eurozone economy, but the worsening outlook is increasing uncertainty over the direction of ECB monetary policy. In August, headline inflation inched down from 5.3% to 5.2% YoY, with core inflation also down from 5.5% to 5.3%. However, consumer confidence index slipped from -16.0 to -17.8. Although the Flash Composite PMI strengthened from the 33-month low of 46.7 to 47.1, this is its fourth consecutive month in contractionary territory. Likewise, the Flash Services PMI rose from 47.9 to 48.4, but still below 50 for the second straight month.

The combination of still-high inflation and tight monetary policy is dragging on Eurozone growth, and with economic indicators (e.g., for private-sector consumption and confidence) worsening, there is a significant risk of the slowdown developing into outright recession during 2H23. At its most recent monetary policy meeting, the ECB signaled that the current cycle of rate hikes may be drawing to a close, but with global energy prices at an 11-month high and labor markets still tight, any declines in inflation are likely to be slower than expected, and going forward, this will only add to the challenges faced by the ECB as it tries to decide future monetary policy.

China

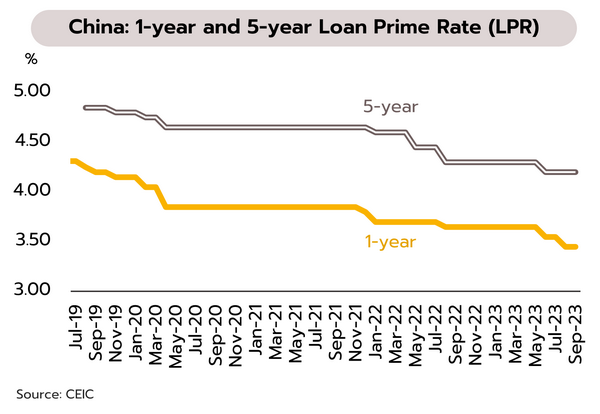

Following a period of dissipating momentum, the Chinese economy is stabilizing and so the PBOC is keeping its benchmark lending rates unchanged. After several months of worsening prints, economic data are improving, such as retail sales (+4.6% YoY in August vs +2.5% in July), industrial output (+4.5% vs +3.7%), unemployment rate and new credit. As of 20 September, the PBOC has therefore kept its 1-year and 5-year loan prime rates (LPR) at 3.45% and 4.20%.

Government actions have stabilized the economy, but troubles in the real estate sector rumble on. The ratings agency Moody’s recently cut its outlook for the property sector from stable to negative and warned of possible downgrades to the credit ratings of property giants China Jinmao Holdings Group and China Vanke, while developer Sunac China Holdings has sought Chapter 15 protection in New York. These troubles will continue to drag on growth, both in China and in the Asia region. The ADB expect Chinese growth to decline from 4.9% in 2023 to 4.5% 2024. The ADB also lowered the GDP growth forecast for developing Asian economies to 4.7%, from 4.8%, warning that unresolved stresses in Chinese property markets have the potential to further hurt growth in China and the region more broadly.

Thailand’s private investment may grow only slightly this year; a possible widening of fiscal deficit may weigh on sentiment

Private investment is expected to see weak growth this year while signs of a recovery in foreign investment remain unclear. The Ministry of Commerce reports that as per the requirements of the 1999 Foreign Business Act, during January-August, 425 foreign companies made investments in Thailand (+14% YoY) worth a total of THB 65.79bn (-21%). The most important sources of investment inflows were Japan (99 companies investing THB 21.98bn), Singapore (72 companies investing THB 13.99bn), the United States (71 companies investing THB 3.07bn), China (31 companies investing THB 11.85bn), and Hong Kong (19 companies investing THB 5.36bn).

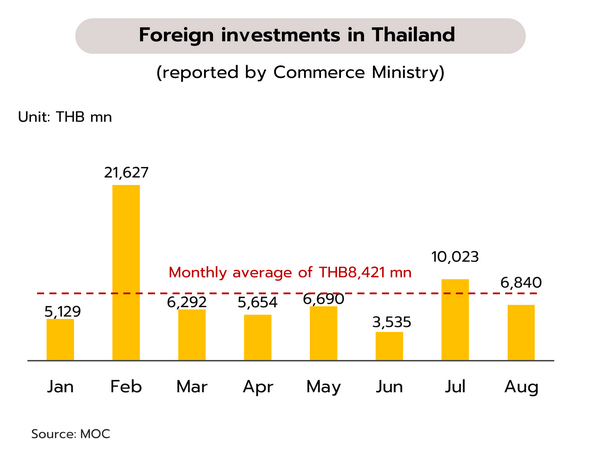

Private investment edged up just 1.8% YoY in the first half of the year, and for the second half of 2023, indicators point to weak recovery. Although the Private Investment Index strengthened in July, this was up just 1.4% YoY. In August, applications for foreign direct investment came to THB 6.84bn, down from THB 10.02bn in July and below the THB 8.42bn averaged over the first 7 months of the year. This weakness has occurred alongside extended uncertainty over investment policy and delays to the FY2024 budget, which will have further consequences for new projects of public investment. Investment is also under ongoing pressure from weakness in the export sector, which has been contracting steadily since the last quarter of 2022. For all of 2023, we therefore see private investment growing by just 2.0%, down significantly from 2022’s 5.1% expansion.

Worries over Thailand’s fiscal stability have intensified. It waits to be seen how the digital wallet policy will shape up. At the 26 September cabinet meeting, Deputy Finance Minister Julapun Amornvivat will present proposals to set up a committee to manage strategy for the rollout of the digital wallet. This will include stakeholders from across the board, including parties involved in operations, spending, auditing, fraud, performance, and assessment. The hope is that the project will be launched on 1 February 2024.

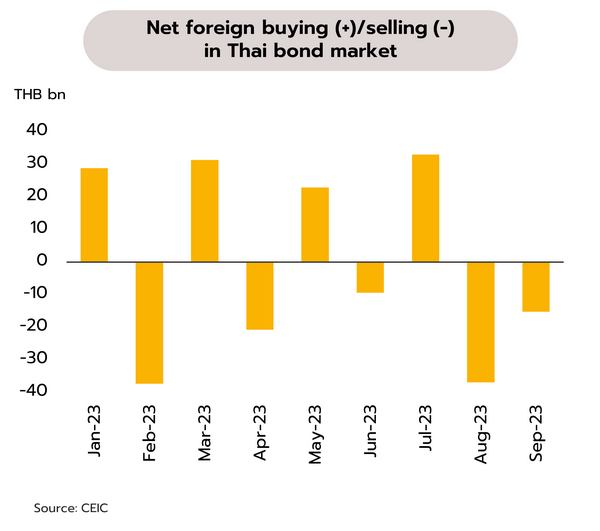

One of the incoming government’s top priorities for supporting economic growth in 2024 is the implementation of their digital wallet scheme, under which the government plans to make payments of THB 10,000 to digital wallets held by all adult Thais. This may need funds worth THB 560bn, and the scale of these commitments is raising worries over increased deficit spending and the possible impacts of this on Thailand’s fiscal stability. The policy may increase risks to Thailand’s credit ratings. Indeed, Fitch Ratings and Moody’s have already warned that the new government’s plans for stimulus spending may add substantially to public debt. In light of this, sentiment has softened, and this is one reason why capital outflows have increased, such that over the first 22 days of September, there was a THB 15bn net selling in Thai bond market by foreigners. This follows on from a THB 36bn net foreign selling in Thai bonds in August. This has then pushed the exchange rate to THB 36.32 against USD, the baht’s weakest in 10 months.