The US and Eurozone are showing clear signs of a cyclical slowdown, and this may signal they get closer to the end of the current cycle of rate hikes

US

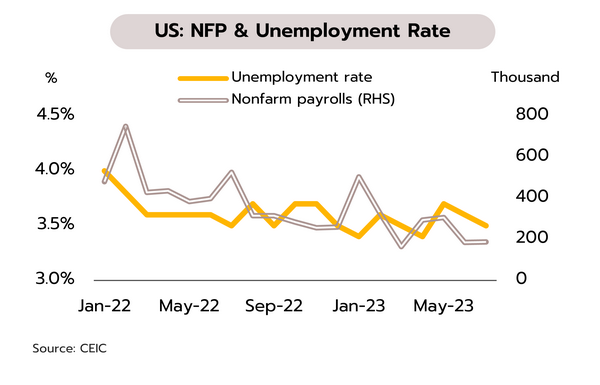

The US economy is softening, and Fitch’s downgrade of the US credit rating from AAA to AA+ may impact financial stability and faith in US Treasuries. In July, non-farm payrolls grew by 187,000, up from June’s 185,000 but below the anticipated 200,000. The unemployment rate also fell from 3.6% to 3.5%, while as expected, average hourly wages rose 0.4% MoM and 4.4% YoY. However, the ISM Manufacturing PMI slipped from 48.1 to 44.4, its 8th month in recessionary territory, while the Services PMI also dropped from 53.9 to 52.7.

Although the risk of a US recession is receding, this round of rate hikes is pushing the economy into a cyclical slowdown. This is then showing up in: (i) the Leading Economic Indicator, which is now at a 15-month low; (ii) the Composite PMI, which has slipped to its lowest in 4 months; and (iii) the ongoing slowdown in the release of new credit. Moreover, the yield curve remains inverted, historically a strong indicator of an approaching recession, while in light of worsening fiscal conditions and rising government debt, Fitch has recently cut the US credit rating from AAA to AA+. The latter may then add to the cost of borrowing for the US public and private sectors, potentially dragging on future growth. Given the above and with real interest rates now positive, we see the Fed likely ending the current cycle of rate rises at its 20 September meeting.

Eurozone

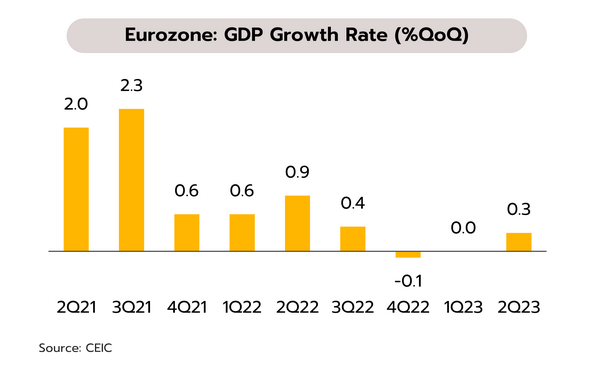

The Eurozone escaped slipping into a recession in Q2, but overall, the bloc’s economy remains weak and this may encourage the ECB to raise rates just once more this year. In Q2, GDP growth came in at 0.6% YoY and 0.3% QoQ, above market expectations of respectively 0.5% and 0.2%, while in July, headline inflation softened from 5.5% to 5.3% YoY, though core inflation remained unchanged at 5.5% YoY. June’s retail sales were also down -1.4% YoY and -0.3% MoM.

Although the Eurozone dodged a recession in Q2, the high cost of living and tight monetary conditions have ensured that European economies remain weak, and this is reflected in major indicators, including: (i) 13 months of contraction in retail sales; (ii) slower release of new credit; (iii) 3 months of negative prints for the ZEW Economic Sentiment Index; and (iv) 3 months during which the Composite PMI has been in recessionary territory. Tight labor markets have helped to slow the softening of inflationary pressures, and so the real interest rate remains negative. We thus believe that although inflation remains some way off the 2% target, the weak overall state of the Eurozone will encourage the ECB to raise rates just once more this year, adding 25bps to the deposit facility rate to 4%. The latter will then likely remain unchanged through to mid-2024.

China

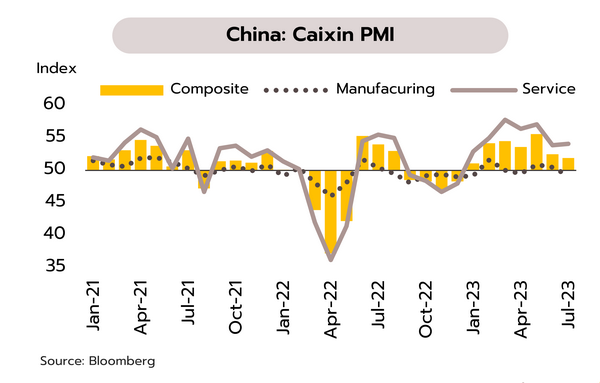

Chinese activity is its weakest since the reopening, and manufacturers are now hoping for stimulus measures. The private-sector Caixin Composite PMI dropped from 52.5 to 51.9 in July, its weakest since January, and although the Services PMI edged up from a 5-month low of 53.9 to 54.1, the manufacturing PMI contracted for the first time in 3 months, sliding from 50.5 to a half-year low of 49.2. This weakness was seen in a number of components, with new orders, export sales, employment, output and sentiment all worsening.

Officials have responded to slowing growth with a slew of new policies targeted at businesses and households. 28 measures supporting the private sector are thus being rolled out in 5 areas: fair, open and equitable access to markets for the private sector; greater support with regard to finances and land use; strengthened legal protections for private businesses; improved governance; and the development of an attractive business environment. 20 measures aim to boost consumption. These include the promotion of: (i) sales of ‘new energy vehicles’ and the construction of new EV charging points; (ii) the purchase of smart electronics; (iii) tourism; and (iv) affordable rented accommodation. However, it remains unclear whether this will be sufficient to offset the slowing economy and to function as an effective counter-cyclical policy.

With uncertainty high and future impacts on the economy potentially significant, we expect the MPC to hold rates at 2.25% for the remainder of 2023

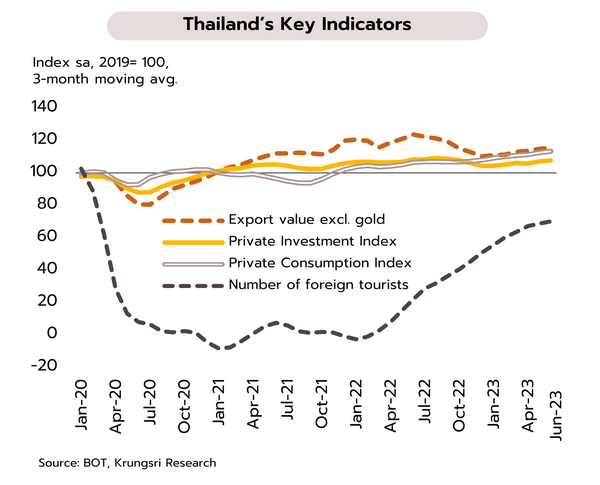

Q2 growth should be close to that of Q1, helped by expansion in the tourism sector and the resilience of private-sector consumption. The BOT reports that overall, the economy continued to expand in June on an improving outlook for the tourism sector (in both the domestic and international segments) and the ongoing strength of private-sector consumption. Although growth in the latter dipped from a month earlier (+6.5% vs. +7.0% YoY), this was due to temporary factors such as the ending of election-related spending, and employment and sentiment have both firmed up further. However, private-sector investment softened (-1.6% vs. +2.7%), with declines seen in spending on plant and machinery and on construction. By value, exports also declined for the 9th month, contracting -5.9%.

A range of economic indicators show that through Q2 (April-June), the economy continued to expand, helped by growth in the tourism sector and in private-sector consumption. We therefore see Q2 GDP growth running to +1.0% QoQ sa, or +2.7% YoY, compared to growth of +1.9% QoQ sa or +2.7% YoY in Q1. However, going forward, the uncertain political situation and the extended delays to installing a new government may hold up the FY2024 budget, which would then undercut sentiment and weigh on growth momentum through the second half of the year.

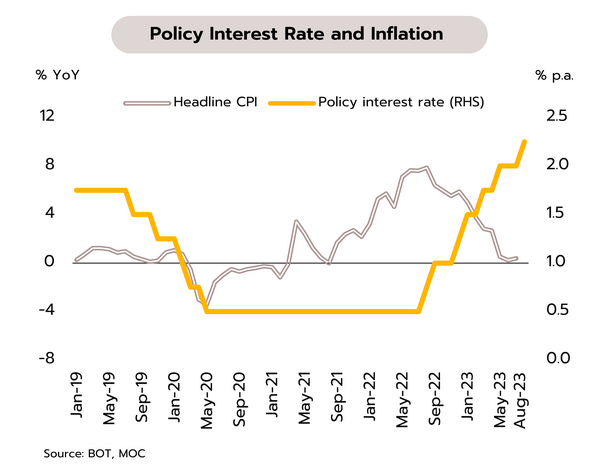

The MPC has raised rates to a 9-year high, but this may be the last hike of 2023. At its 2 August meeting, the Monetary Policy Committee (MPC) voted unanimously to raise policy rate to 2.25% (up 25bps). The MPC has taken the view that the economy is on track to meet its potential and so monetary policy should be focused on bringing inflation back to a sustainable target range and building long-term financial stability. This requires preventing the buildup of the financial imbalances that may accumulate during a period of low interest rates, as well as preserving the authorities’ financial firepower and the policy space required to deploy this, which may well be needed to deal with uncertain future conditions. A 25bps hike was thus deemed appropriate.

The BOT has stated that Thai policy rates are now in a more neutral zone, while the economy is returning to its growth potential, though unlike in some other countries, it is not overheating. Monetary policy should therefore support growth that tracks the economy’s potential amid an uncertain environment. The latter includes: (i) the slowing world economy; (ii) the tense political situation, which may delay the FY2024 budget, affect sentiment and the investment climate; and (iii) the emerging El Niño, with drought likely to start dragging on growth in 2H23. The MPC’s latest meeting thus had a less hawkish coloring, and although the committee sees a risk that the El Niño may push up world food prices and so add to domestic inflation, the correlation between global cost of food and domestic price rises is relatively weak and with demand-pull inflation softening, we see the consequences of this being limited. In addition, since high risk and uncertainty could adversely affect the Thai economy, the BOT is likely to revise down its forecasts for growth and inflation at its September meeting. We therefore expect that the MPC will keep rate at 2.25% for the rest of 2023.