The major economies are slowing, in particular China, where the rolling real estate crisis is further undermining the reopening tailwinds

US

The US service sector continues to soften, while Fitch’s recent warning of potential downgrades to major US banks reflects increased credit risk. In July, retail sales rose 3.17% YoY and 0.7% MoM, up from respectively 1.59% and 0.3% a month earlier. Core retail sales were also up 1.0% MoM compared to June’s increase of 0.2%. Declines in industrial output slowed from -0.78% to -0.23% YoY. Likewise, initial jobless claims came in at 239k in July, down from 250k in June.

Although the risk of recession has fallen on better-than-expected economic data and GDP growth, high interest rates and the elevated cost of living began to drag on expansion in the service sector. Momentum is thus dissipating and overall, the economy is starting to show clearer signs of slowing. This is reflected in: (i) a 3-month slide in the Services PMI and, in July, a fall in the Composite PMI to a 5-month low; (ii) a drop in growth in private consumption from 4.2% QoQ in Q1 to 1.6% in Q2, which coincided with the sharpest slide in core inflation in over 2 years; (iii) the ongoing slowdown in the release of new credit; and (iv) a 16-month contraction in the monthly Leading Economic Indicator Index, its longest run of declines since 2009 and the depths of the global financial crisis. In addition, Fitch’s warning of possible downgrades to the credit ratings of major US banks including JP Morgan, the US’s largest, reflects the increased credit risk emerging within the financial system, and this may push up bond yields, potentially impacting the economy over the longer run. Given rising risk, clearer signs of a slowdown, and the fact that real interest rates are now positive, we expect that at the 20 September meeting, the Fed will signal an end to the current round of rate hikes.

Japan

Although changes to its yield curve control policy surprised markets, weakening inflation and a slowing economy will likely leave the BOJ little room to tighten monetary policy in the remainder of 2023. In Q2, Japan’s economy expanded by 6.0% YoY and 1.5% QoQ, above market expectations of respectively 3.7% and 0.9%. In July, National CPI remained unchanged at 3.3% YoY, Core CPI inched down to 3.1% YoY from 3.3% in June. The household spending remained at -4.2% YoY in June vs -4.1% in May.

Given high inflation, which has now outpaced wage growth for the past 15 months, a decline in household spending is to be expected. In addition, labor markets are also showing signs of slowing, and although the overall unemployment rate remains low, the job-to-applicant ratio has dropped to its lowest in a year. These factors will combine with weakness in the export sector to weigh on overall economic growth through the remainder of 2023. Nevertheless, with tourist arrivals rebounding, monetary policy still accommodative, and wages on an upward track, we see only a limited risk of outright recession this year. On the inflation front, while this remains high, softening energy prices and the overall slowdown in economic activity will likely help to pull prices below the BOJ’s 2% target. In light of this, the surprise move by the BOJ to adjust its YCC policy may increase the probability of the Bank raising short-term policy rate or and adjusting YCC again soon, but the gradual slowdown in inflation and economic activities will convince the Bank to refrain from further policy tightening the rest of this year.

China

Debt crisis in China’s real estate sector is exacerbating the economic slowdown. Following its 2021 default and liquidity problems, developer Evergrande has filed for bankruptcy in the US last week. At end-2022, its total debt came to USD 340bn, or roughly 2% of GDP, coupled with losses of USD 81bn. Country Garden, China’s largest developer (its projects are 4-times the size of Evergrande) faces losses that may amount to USD 7.6bn, and on 7 August the company missed payments on dollar-denominated debts. If these fail to be made within the 30-day grace period, the company will be considered to be in default for the first time.

Crisis in the real estate sector may now trigger a domino effect, amplifying problems for the wider economy. Asset management company Zhongzhi thus reports that since mid-July, its Zhongrong Trust (which has around 11% of its funds in the real estate sector) has halted payments on all its financial products. These developments may worsen the slowdown seen in many parts of the economy, including in retail sales, investment, manufacturing, and exports. As of 15 August, the PBOC announced a 15bp cut in the 1-year medium-term lending facility (MLF) rate to 2.50% and a 10bp cut in the 7-day reverse repurchase rate to 1.8%, but these moves have been insufficient to reverse the combined effects of the worsening troubles in property markets and dissipating overall growth momentum.

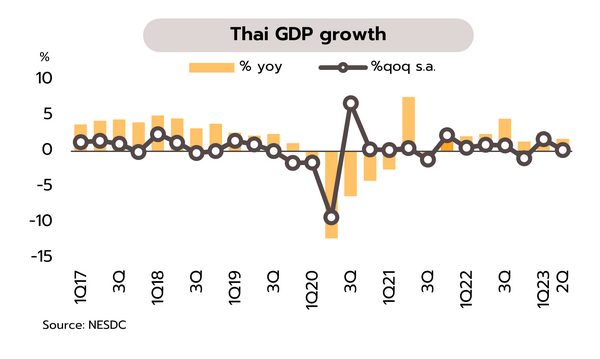

Krungsri Research will trim our 2023 GDP forecast after 1H23 growth became weaker than expected at 2.2%

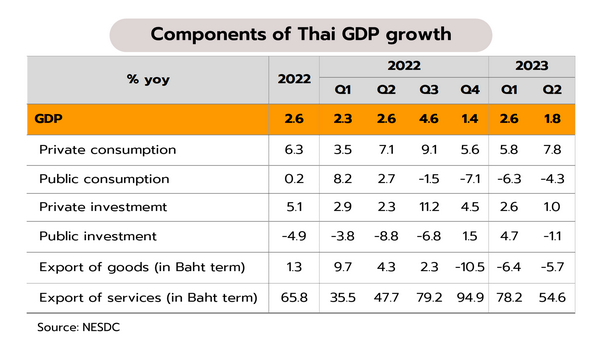

2Q23 Thai GDP growth slowed down to just 1.8% YoY and 0.2% QoQ. Krungsri Research will revise down 2023 GDP forecast. According to the NESDC report, the Thai economy in 2Q23 grew at only 1.8% (lower than consensus and Krungsri Research’s forecasts of 3.1% and 2.7% respectively), down from 2.6% growth in 1Q23. The main reason of disappointing growth came from (i) weaker-than-expected investments; (ii) a contraction in government expenditures due partly to last year’s high base (as a result of large spending for public health and covid-19 policy which occurred in 2022); and (iii) a contraction of merchandised exports. However, private consumption continued to expand, and exports of services grew sharply thanks to the rising number of foreign tourist arrivals. In addition, the NESDC cut 2023 GDP growth forecast from a range of 2.7-3.7% to 2.5-3.0%.

The NESDC reported 2Q23 Thai GDP (seasonally adjusted) increased slightly, by only 0.2% QoQ, below consensus and Krungsri Research’s estimates of 1.2% and 1.0% respectively. In this first half of 2023, GDP expanded by 2.2% YoY, lower than Krungsri Research’s forecast of 2.7%. For the second half of this year, we expect that the Thai economy is likely to recover further, mainly driven by (i) tourism sector, especially during the high season period in 4Q23, and (ii) the formation of the government with expectations of completion by 3Q23. This factor could help to improve investors’ confidence and accelerate the implementation of economic policies in the rest of the year. Nonetheless, Thai exports would remain weak owing to trading partners’ economic slowdown. Overall, we will trim 2023 GDP growth forecast from the current 3.3%. For the exact number of revised growth forecast, we are waiting for the development of domestic political situation later this month as it may indicate the direction of economic policies in the period ahead.

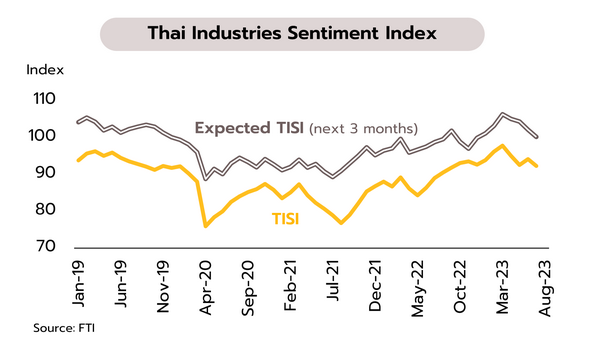

Industrial output remains weak on a combination of softer domestic and external demand and strengthening competition from Chinese goods. In July, the Thailand Industrial Sentiment Index dropped from 94.1 to a 10-month low of 92.3, with declines seen in all areas, including orders, sales, output, operating costs, and turnover. Similarly, sentiment 3 months out also softened from 102.1 to 100.2. These declines were driven by: (i) worries that delays in installing the new government will impact policies helping to sustain economic growth; (ii) fears that more expensive energy, electricity and labor will add to manufacturing costs; and (iii) the uncertain outlook for the global economy, the higher borrowing costs, and the effect of high household debt on domestic purchasing power.

We expect that through the rest of 2023, the continuing global slowdown, especially in the manufacturing industries in the major economies, will undermine the Thai industrial sector, thus extending the -4.6% YoY decline in the Manufacturing Production Index recorded in the first half of the year. The outlook will be further impacted by the worse-than-expected performance of the Chinese economy, and this will significantly affect exports of Thai goods. Moreover, the Federation of Thai Industries states that Thai companies are facing stiffening competition from Chinese exporters fighting for Thai domestic market share, and whereas in the past, this was concentrated in the steel industry, this competition has now spread to include sales of pharmaceuticals, plastics, aluminium goods, and petrochemical products.