Global growth is under threat from slowing labor market growth in the US and Japan, combined with risks in China

US

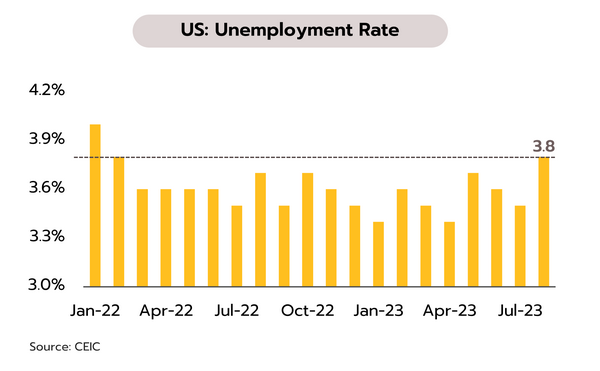

Despite clearer signs that labor markets are softening, services inflation remains sticky, supporting the Fed to keep interest rates high for longer. In July, headline PCE increased 3.3% YoY and 0.2% MoM, compared to rises of 3.0% and 0.2% in June, with core PCE also up 4.2% YoY and 0.2% MoM from rises of 4.1% and 0.2% a month earlier. While August’s non-farm payrolls rose by 187,000, beating market expectations of an increase of 170,000, the JOLTs job openings print fell to its lowest since April 2021 at 8.827m. The unemployment rate rose to 3.8%, its highest since February 2022 and above the 3.5% expected by the market. At 4.3% YoY and 0.2% MoM, rises in average hourly earnings likewise undershot the expected 4.4% and 0.3%. Alongside this, although the ISM manufacturing PMI strengthened from 46.4 to 47.6, it remains in contraction territory (sub-50) for the 10th consecutive month.

August’s weaker data on employment and the continued softening service sector highlight the rising likelihood of a gradual drop in inflation and of a slowdown in the US economy. Nevertheless, persistent inflationary pressure in the service and real estate sectors may encourage the Fed to maintain policy rates at high levels for an extended period, or until there are clearer signs that inflation has sustainably returned to the 2% target range.

Japan

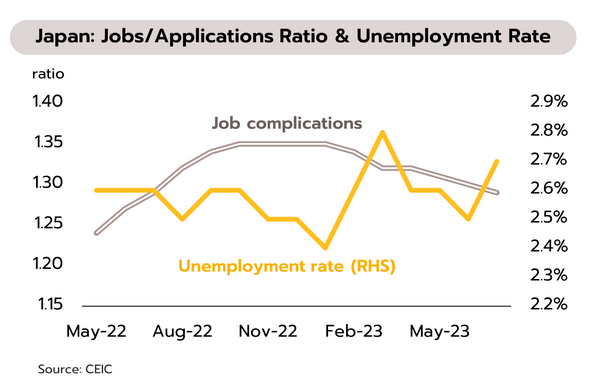

The unemployment rate in Japan has increased, reflecting the slowdown of the economy. However, reopening tailwinds and ultra-loose monetary policy might help to avoid a recession. In July, the unemployment rate edged up from 2.5% to 2.7%, the job-to-application ratio slipped from 1.30 to 1.29, and manufacturing output contracted -2.0% MoM having grown 2.4% a month previously. However, retail sales expanded 6.8% YoY, up from 5.6% a month earlier, and PM Fumio Kishida has promised that following China’s block on imports of Japanese seafood, assistance will be forthcoming for the fishing industry.

The high cost of living and weak demand in export markets are dragging on growth. This is reflected in falling household spending, the negative turn in wage growth, and a contracting export sector. All of these factors are leading to clearer signs of a slowdown in labor markets. However, the revival in foreign arrivals, accommodative monetary policy, and forthcoming wage hikes should help to keep growth positive through 2H23, thus avoiding a recession. Krungsri Research therefore expects that given weakening inflationary pressures and a slowing economy going forward, the Bank of Japan will be in no rush to tighten monetary policy.

China

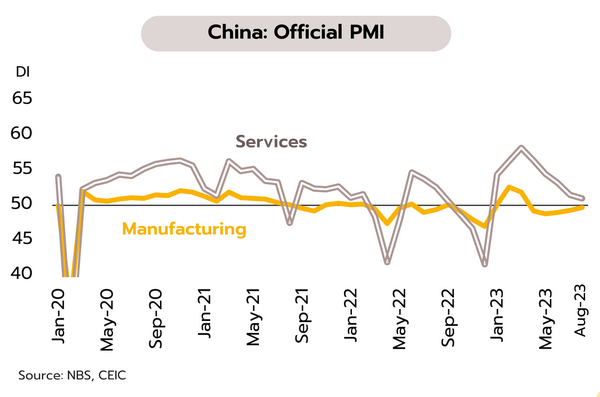

Parts of the manufacturing sector grew in August, and stimulus measures have been announced, but risk remains high. Last week, authorities launched a tranche of measures to support the financial sector and the overall economy, including (i) cuts from 0.1% to 0.05% in stamp duty on securities; (ii) 5-25bps cuts in deposit rates at leading commercial banks from 1 September, and with preparation to reduce mortgage loan rates; and (iii) 2023’s first cut in the foreign currency reserve requirement ratio (RRR) by 200bps to 4%, effective from 15 September. This move aims to increase FX liquidity, mitigate the devaluation of the yuan, and alleviate negative impacts on the economy.

Stimulus measures are helping to improve liquidity and parts of the manufacturing sector. The manufacturing PMI for SMEs rose from 49.2 to 51.0 in August, the highest since February. However, the manufacturing PMI for large businesses fell to 49.7, its 5th month of contraction. Importantly, the services PMI fell to 51.0, its lowest since December. The data point to economic weakness amid slowing momentum from the reopening, the effects of the global slowdown, and turmoil in the real estate sector. Country Garden posted a record loss of USD 7bn and is now at risk of default. This could potentially spread contagion to the financial sector and to the broader economy.

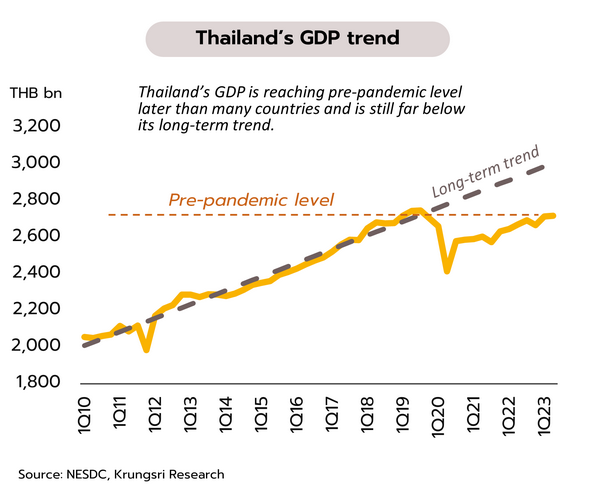

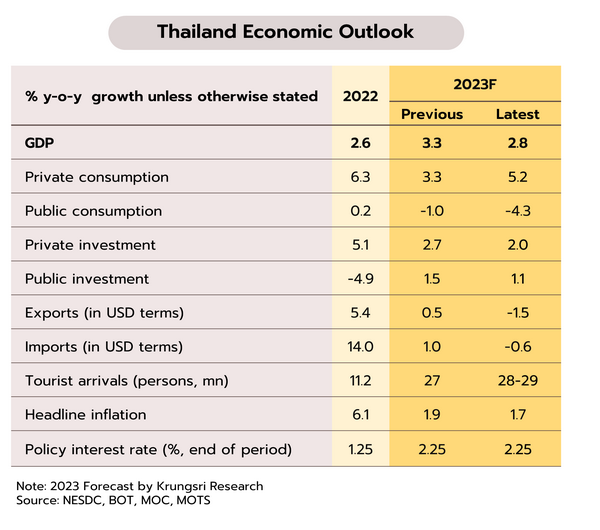

Krungsri Research has cut its 2023 growth forecast from 3.3% to 2.8% on weaker-than-expected exports, investment, and public-sector spending

The rebound in the tourism sector and growth in domestic expenditure are helping to lift the economy at the start of Q3, though exports remain weak. The Bank of Thailand reports that in July, the economy grew on an improving outlook for the tourism sector. 2.5m foreign arrivals were recorded in the month, the highest monthly total since the post-Covid reopening, while domestic tourism also benefited from recent public holidays, and this then boosted spending on services and nondurable goods. In addition, non-farm payrolls also rose, lifting household purchasing power. Private investment has returned to growth on strength in the construction sector. Nevertheless, weak overseas demand meant that the value of exports slipped for the 10th consecutive month.

We expect economic growth to improve to 3.4% in 2H23 from 2.2% in 1H23. This outlook will be supported by: (i) continuing expansion in the tourism sector, especially during the Q4 high season; (ii) the introduction of the new government’s policy agenda, which should improve confidence and encourage domestic spending. Recently, the government stated that it will rollout measures to help reducing cost of electricity and of other utilities, as well as restructuring debts in the agricultural sector; and (iii) the low base last year due to China’s lockdown in 4Q22, undercutting world demand and disrupting global supply chains, should serve as a supporting technical factor for year-on-year growth in the last quarter of this year. However, weak exports, the delay in the FY2024 annual government budget bill, the impacts of drought, and the rising cost of borrowing (alongside high levels of household debt) will all limit the room for economic growth.

We have downgraded our forecast for 2023 economic growth from 3.3% to 2.8%, and we now expect the MPC to keep policy rates unchanged at 2.25% through the rest of 2023. The outlook for the Thai economy has worsened somewhat on 2Q23 GDP growth of just 1.8% YoY (below our forecast of +2.7%) and worse-than-expected performance by the export sector, which we now see contracting -1.5% (rather than our prior forecast of +0.5%) on weak growth in China and soft demand in other major overseas markets. Sluggishness in the export sector will then drag private investment below earlier predictions. Moreover, delays to the FY2024 annual budget will undercut government expenditure. However, the overall economy will still benefit from

(i) a recovery in tourism, especially in Q4 which is the start of the high season, (ii) growing private consumption, and (iii) the government’s stimulus policies, which are expected to rollout towards the end of this year.

The outlook of policy rate will be affected by the easing inflationary pressures, and the likelihood that economic activity (or GDP level) will undershoot its long-term potential. Given that the Bank of Thailand recently indicated a potential downward revision of this year’s economic growth forecast of 3.6%, we therefore see the Monetary Policy Committee (MPC) calling a halt to the current cycle of rate hikes at its September meeting. We expect the MPC to hold rates steady at the 9-year high of 2.25% for the remainder of the year to ensure a further economic recovery.