Global: Reflation concern, recovery hope

Economic recovery has pushed up bond yields, but low velocity of money should sooth reflation concerns

US: Fresh COVID-19 relief bill and remarkable progress in vaccination program to boost consumption

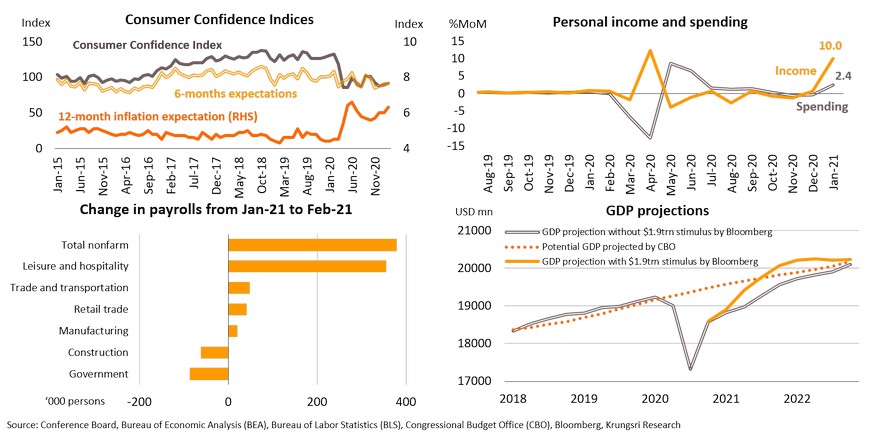

Households are more upbeat about recovery following the approval of additional government aid and fewer COVID-19 new cases. The Consumer Confidence Index improved to 91.3 in February from 88.9 in January as more Americans are vaccinated. Consumer inflation expectation has risen to the highest since June last year, as consumers hope demand for services would return. Personal income rose by 10% MoM in January as the cash aid to eligible recipients supported a 2.4% increase in spending. This suggests consumption, which accounts for 70% of the economy, would be the major driver of recovery. Looking at the labor market, services sectors improved substantially with leisure and hospitality payrolls rising by 355k jobs in February. The latest USD1.9trn relief bill is expected to push the US GDP level back to pre-virus level by mid-year and the legislation could have a positive impact up to end-2022. Moreover, Biden hoped that America can “mark independence” from COVID-19 on 4 July if people get vaccinated. The upcoming fiscal relief and faster-than-peers’ inoculation program will lift sentiment further and accelerate economic recovery for the rest of the year.

Manufacturing sector should continue to recover; several headwinds would be transitory

The Fed is not stressing over rising yields, signals no policy change this year

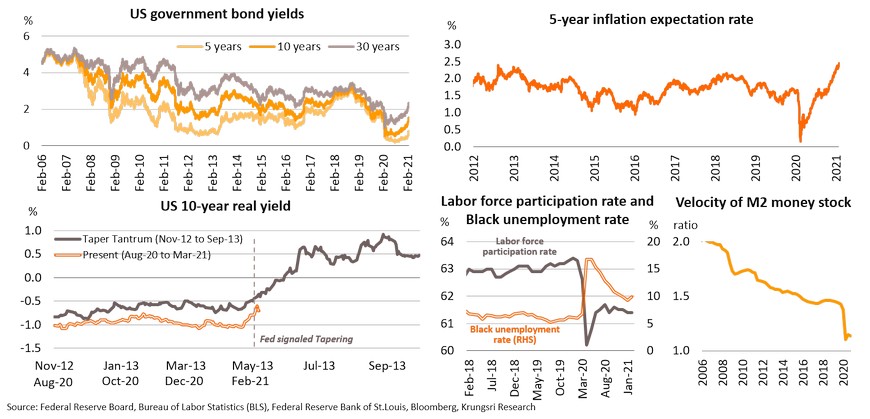

The promising economic outlook and rising inflation have pushed up bond yields recently. 5-year inflation expectation has risen to the highest level since 2008, at 2.35%. Government 10-year bond yield rose to 1.6% in late-February, the highest in more than a year, raising concerns the Fed might hike rates. However, inflation could have risen due to the low-base effect and additional stimulus measures, rather than an overheating economy. Although the current path of 10-year real yield looks similar to that during the 2013-Taper Tantrum period, the latest real yield remains very low and had edged down in the beginning of March. In addition, the recovery in the labor market is far from complete as labor force participation rate remains low at 61.4% compared to 63% in 2019, while Black unemployment is still elevated at 9.9%, suggesting a long way towards inclusive labor market goals. More importantly, money velocity remains at a historical low, implying the economic transactions are very low. Moreover, Powell claimed the rising yields reflect ‘the statement of confidence on recovery’ and stated inflation is still ‘soft’. Thus, the Fed is not stressing over rising yields. We expect the Fed to commit to keep the current size of asset purchases this year and maintain record-low interest rates until the end of 2023.

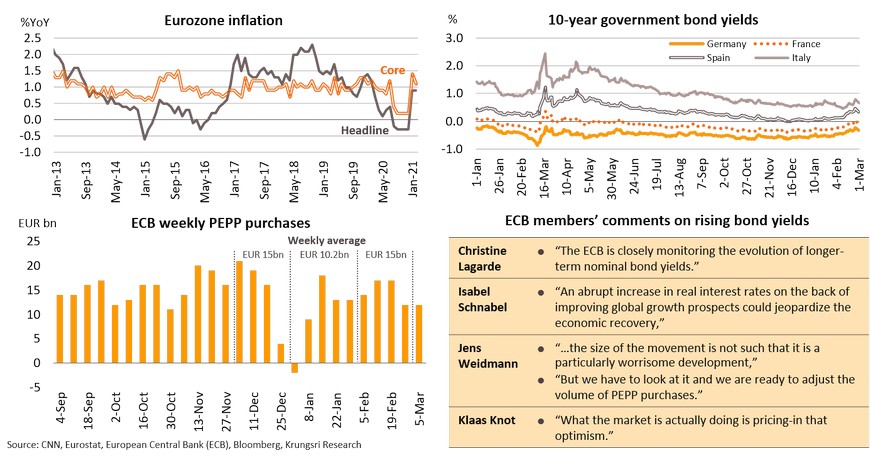

Europe: Economic improvements are challenged by supply shortage, restrictions and slow vaccination

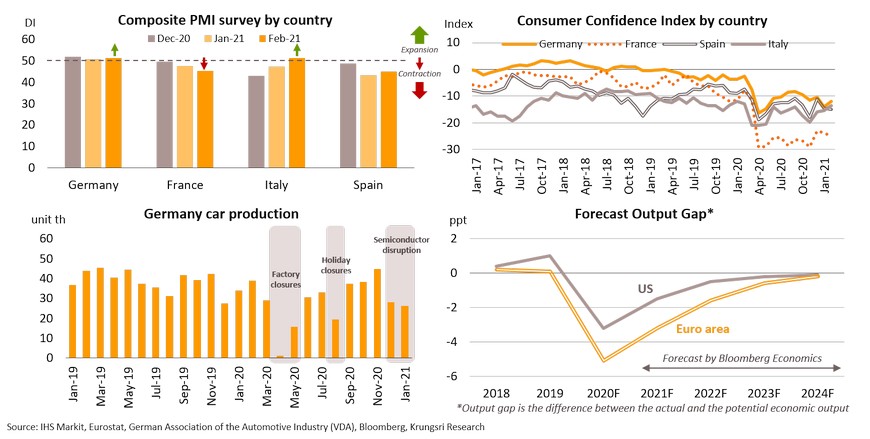

Eurozone economy has improved slightly since mid-February, but several headwinds could send the eurozone economy into contraction territory in 1Q21. The Composite PMI data has inched-up in major countries, especially Italy where it has risen to 51.4 in February from 47.2 in January. The Consumer Confidence Index improved in Germany and Italy. The improving confidence in Italy reflects optimism towards the new Draghi-led government. By contrast, there was broad-based deterioration in France and Spain due to tighter restrictions as well as concerns over another lost summer tourism season. Manufacturing sector has been attacked by the global semiconductor shortages, leading to lower car production since December, especially in Germany. On the pandemic situation, lockdowns have been extended in many economies while vaccination progress has been slow in 1H21 because of smaller-than-expected vaccine deliveries. Coupled with the absence of additional fiscal supports in 1H21, they are holding back economic recovery. Hence, we expect the Eurozone economy to shrink in the first quarter and the output gap is unlikely to be closed until 2024, one year behind the US.

ECB would step up bond purchases in 2Q21 to improve financial conditions

A temporary surge in inflation and spillover-effect from US financial markets have pushed up Eurozone bond yields. Headline inflation continued to register a one-year high of 0.9% YoY in February, while core inflation remained high at 1.1% YoY due to the cancelled winter sales. Looking ahead, higher inflation would be temporary because of the change in inflation component weightings this year and the expiration of Germany VAT cut which impact could disappear by end-1H21. In the bond market, the increment in 10-year yield in the eurozone is smaller than in the US and still below historical level. The ECB board also stated optimism over economic developments have led to the rising yields. However, the ECB promised to ‘closely monitor’ the situation and pledged to ramp up bond purchases in 2Q21. We expect the ECB to speed up weekly bond purchases from the current EUR15bn to up to EUR20bn in the next quarter, close to the level in July last year, and maintain an accommodative policy throughout the year. But, they are unlikely to adjust the purchase ceiling because assuming purchases at current pace, the ECB would reach EUR1.85trn of PEPP envelope by April 2022.

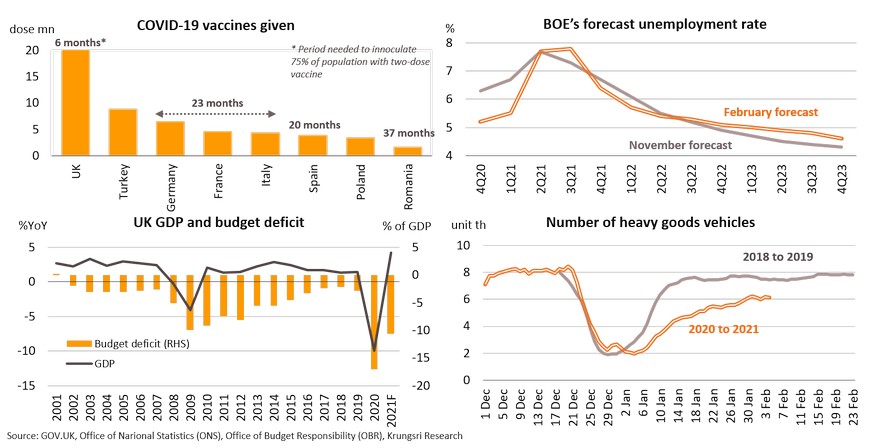

UK: Progress in vaccination program; latest aid would lift growth this year but there are obstacles ahead

The significant progress in vaccine rollout relative to other EU countries suggests the UK would reach herd immunity within 6 months. This optimism allowed Boris Johnson to unveil the road map for lifting lockdowns from March to June. In addition, the UK has extended fiscal aid period to 3Q21, including business tax holiday, VAT reduction, and furlough programs which could reduce unemployment rate in 1H21 compared to the previous forecast. These imply the UK outlook would be preferable this year. However, economic recovery might face big hurdles ahead as the largest GDP slump in its history and much-wider budget deficit would prompt the government to raise corporate income tax from 19% to 25% in 2023 and probably raise personal income tax to tackle the balance sheet, but this would affect company revenues and household income. Additionally, vehicles traffic at port of Dover in late-January fell 19% compared to the same period in 2019, indicating Brexit has pointed partial impact on trade. Manufacturers also reported several difficulties relating to custom checks could delay exports and permanently reduce the EU-UK trade volumes.

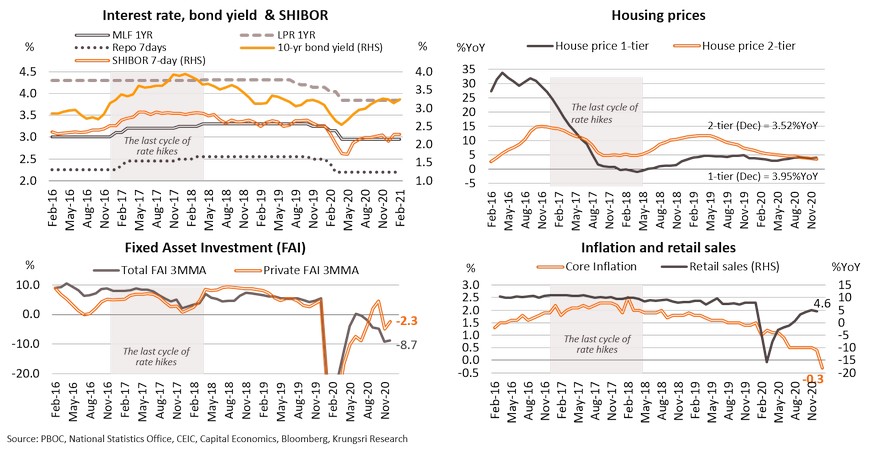

China: Still needs stimulus although impacts of latest outbreak have been limited

At the beginning of 2021, the Chinese economy was affected by a new wave of infections and restrictions during the Lunar New Year, although exports grew favorably during January-February. Recent high-frequency data suggest economic activities are still below pre-pandemic levels despite signs of improvement after the seasonal holidays. In terms of travel, the number of domestic trips and tourism revenues during the spring festival this year were below pre-pandemic levels. Both Manufacturing and Non-manufacturing PMI data for February have dropped to the lowest in 9 and 12 months, respectively, although the notable increase in business expectations (for sub-indices) indicates production will continue to expand. The weaker economic activity underscores the need to continue with fiscal and monetary policy supports to broaden recovery.

Despite rising bond yields, PBOC likely to keep policy rate unchanged to accommodate growth in real sector

Recently, markets have been concerned the central bank (PBOC) will tighten monetary policy to curb bubble risks, reflected in higher 7-day SHIBOR and 10-year government bond yields. However, data for the real estate sector indicate it is not overheating like in 2016, and the PBOC has implemented targeted measures to mitigate bubble risks, which subsequently reined-in housing prices in first and second tier cities. Meanwhile, the adverse impact of the pandemic continues to dampen the real sectors, reflected in still-weak private investment. Likewise, retail sales growth is still below pre-outbreak level, which means limited inflationary pressure. Hence, we expect the PBOC to maintain policy interest rate throughout 2021 to accelerate recovery in private consumption and private investment.

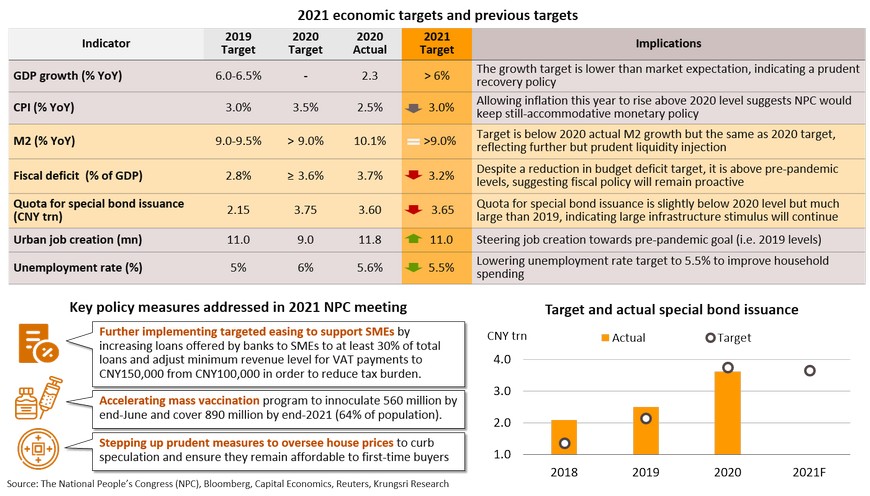

Economic policies still focus on supporting a recovery despite more prudent stance

Economic targets for 2021 set by the National People’s Congress (NPC) imply a more prudent policy stance after the economy shows signs of recovery. However, the NPC’s main goals suggest policies would still focus on boosting economic growth to support a further recovery, as evidenced by (i) allowing inflation this year to rise above 2020 level; (ii) setting 2021 fiscal deficit beyond pre-COVID level; and (iii) plans to increase off-budget spending by increasing quota for special bond issuance to above 2020 actual level and much larger than pre-pandemic target.

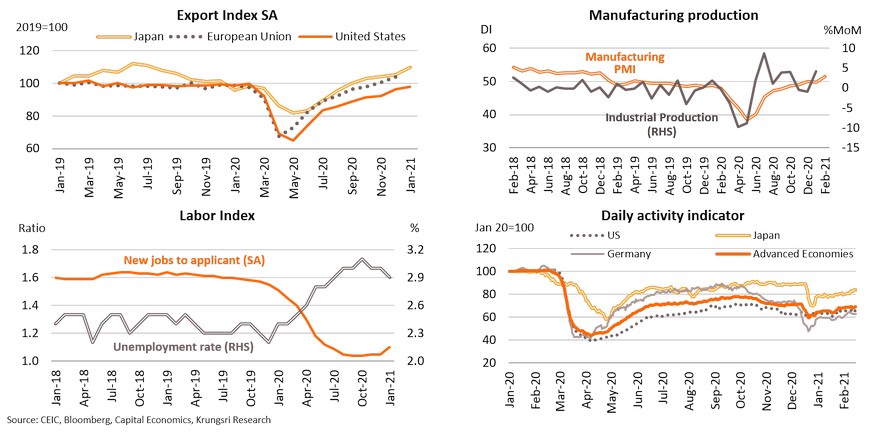

Japan: Positive momentum in exports and easing lockdown measures will help to support economic recovery

Japan’s economy continues to improve as domestic infections remain low. This has prompted the government to lift the state of emergency in 6 of 10 prefectures, and in the remaining prefectures including Tokyo by March 21. The key economic driver is the rebound in Japan’s exports, which have returned to pre-pandemic level and improved more than the US and the European Union. The positive momentum in exports will continue to boost industrial production which reached a 6-month high in January. Likewise, Manufacturing PMI data was positive, entering expansion territory for the first time since December 2018, partly driven by a recovery in the new export orders sub-index. Improving production also contributed to the recent recovery in the labor market, which would boost domestic spending. Looking ahead, the economy should continue to recover following relaxation of lockdown measures and progress in the vaccination program which could revive services activities and domestic demand.

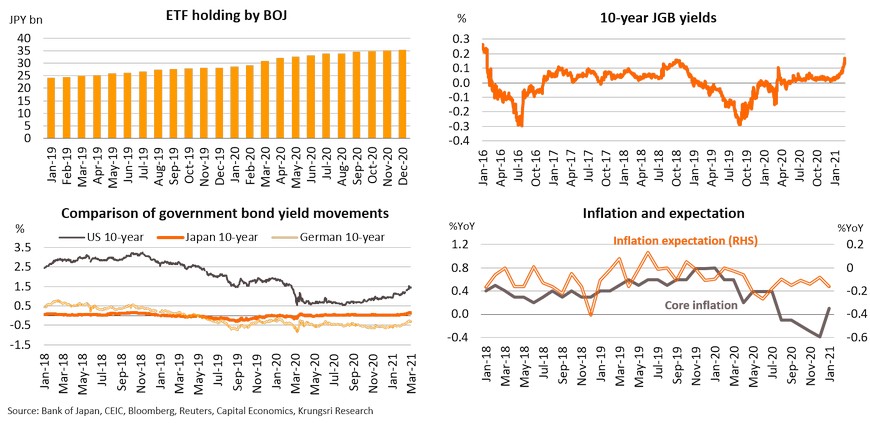

BOJ might tweak policy this year but Japan still needs very-loose policy to support a further recovery

Given the improving economic outlook, the Bank of Japan (BOJ) may tweak monetary policy this year, including widening the tolerance band for bond yields and reducing purchase volume of exchange-traded funds (ETF). This would allow markets to function more efficiently, improve banks’ earnings, and mitigate market speculation. We expect the policy tweak to be gradual because the economic recovery is in the early stage and a sharp rise in bond yields would affect recovery. Although Japanese bond yields have been relatively flat compared to peers, 10-year JGB yield had recently risen to a two-year high, suggesting the BOJ needs not rush to adjust policy. Krungsri Research views there would be a policy tweak instead of tightening, for the following reasons: (i) core inflation is improving but remains far below the BOJ’s target of 2%. The BOJ forecasts core inflation would reach +0.5% in 2021 and +0.7% in 2022, and (ii) Governor Kuroda said, “the BOJ now won’t hit its goal before 2024”, implying the central bank would continue to pursue very-loose monetary policy for several years to support a sustainable economic recovery.

Thailand: Gradually turns a corner

Latest data point to early signs of economic rebound after recovery stumbled with the resurgence of COVID-19

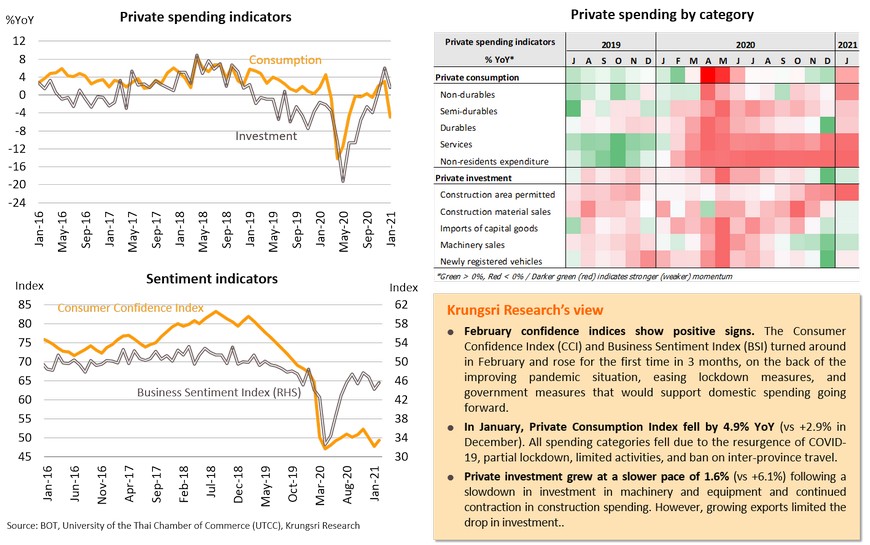

- Exports will be a key driver of the Thai economy, with latest data showing positive momentum. Recovering external demand would help to cushion the COVID-19 impact on manufacturing production. By sector, exports and capacity utilization rates in several categories have recovered beyond pre-pandemic levels. Domestic tourism will recover following easing lockdown measures, although it was hit in January after Thailand experienced a second outbreak. Inbound tourism activity could see substantial improvements in 4Q with the relaxation of COVID-19 travel restrictions and quarantine requirements. Private consumption and investment show signs of picking up after slowing down due to the second outbreak at the beginning of this year.

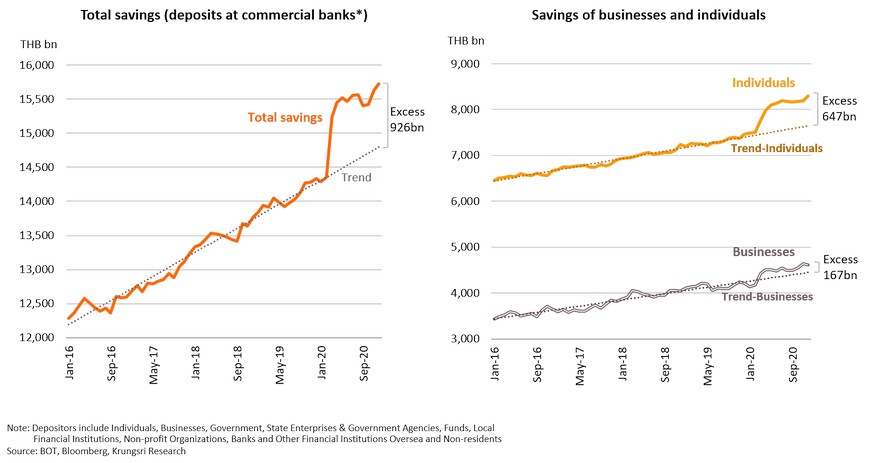

Excess savings suggest large room for domestic spending when pandemic ends

- Excess savings has surged since the COVID-19 pandemic started last year, to THB926bn at the end of 2020, accounting for almost 6% of Thai GDP. This implies large room for spending after the pandemic ends. Excess savings of individuals has surged to THB647bn (or 4% of GDP) and that of businesses has also increased to THB167bn (1% of GDP). These will support growth of private consumption and investment in the periods ahead.

Low velocity of money indicates accommodative policy will continue, while signs of economic recovery suggest no need for more rate cuts

- Despite the recent spike in bond yields and reflation concerns amid rising money supply, there is no sign of tightening monetary policy because the economic recovery is in the early stage and the velocity of money remains near a historical low. Krungsri Research expects the Monetary Policy Committee (MPC) to maintain accommodative monetary policy by keeping policy rate at a record low of 0.50% throughout this year. Meanwhile, the MPC is unlikely to cut policy rate given signs of economic recovery amid further relaxation of lockdown measures.

Thailand Economic Outlook 2021

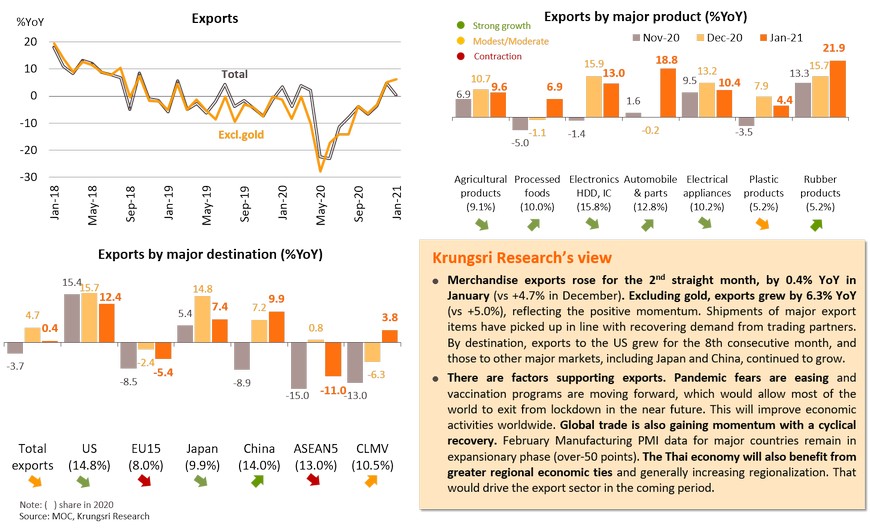

Export sector will be key driver of the Thai economy; latest data show positive momentum

Rising external demand helps to cushion negative impact of COVID-19 on domestic manufacturing production

By sector, exports and capacity utilization in many categories are recovering beyond pre-pandemic levels

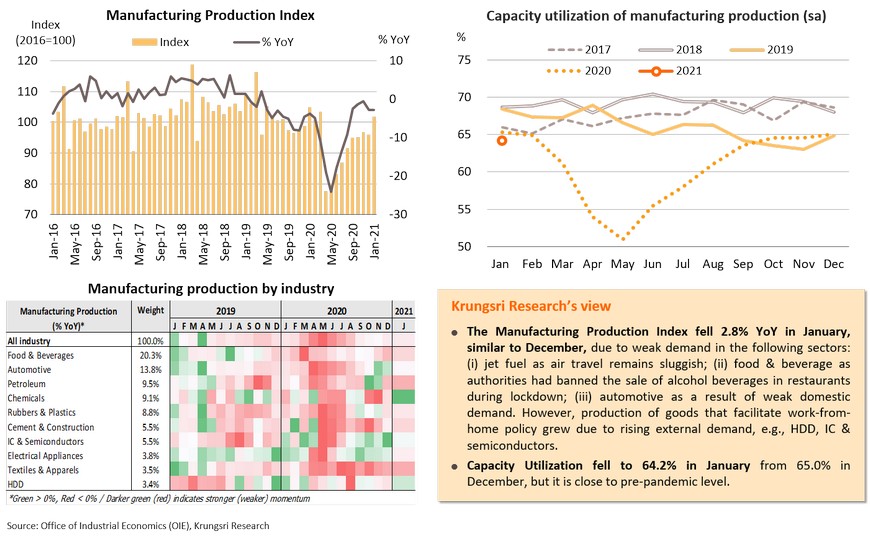

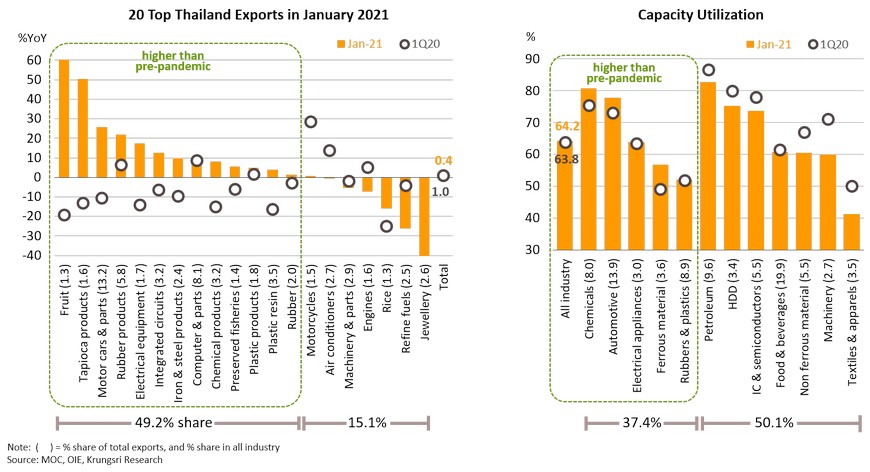

In January, exports in several sectors had expanded faster than pre-pandemic levels (in 1Q20), led by products to facilitate work-from-home policy and to contain the pandemic. 13 out of the top-20 export items saw stronger growth than in 1Q20, led by fruit, tapioca products, cars & parts, rubber products, electrical equipment, and integrated circuits. The stronger exports have had positive spillover effects on domestic production. Capacity utilization rates in several sectors have also risen above pre-COVID-19 levels although domestic demand remained weak and suffered from the second outbreak at the beginning of this year.

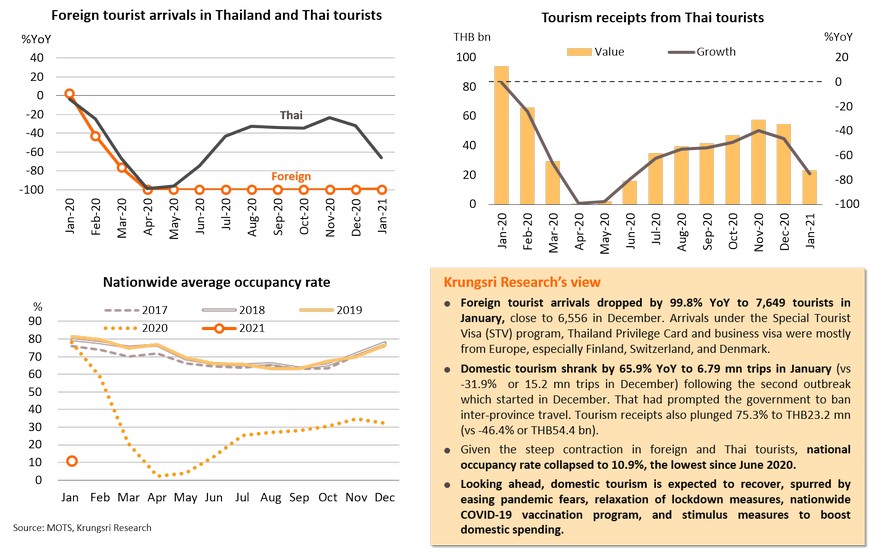

Domestic tourism will recover with easing lockdown measures, through it was hit in January by the second outbreak

Inbound tourism could recover substantially in 4Q; relaxation of COVID-19 restrictions will revive activity

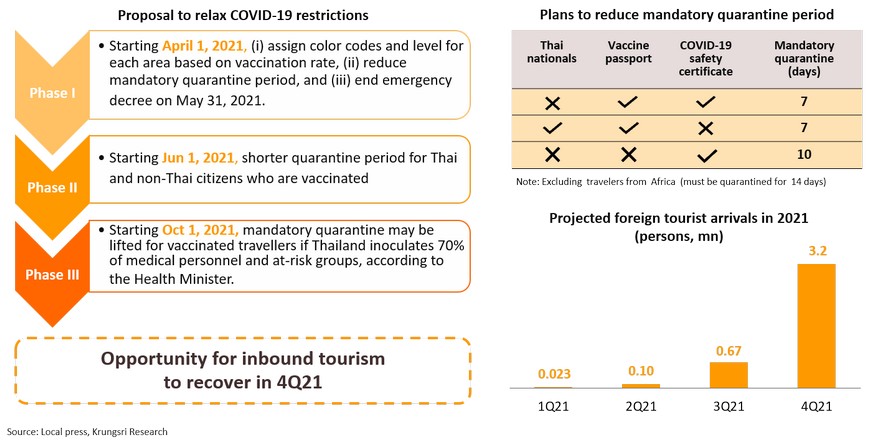

The vaccination programs and easing COVID-19 fears in Thailand and other countries will pave the way for the government to ease inbound travel restrictions. That will be implemented in three phases (see chart). One proposal is to reduce the mandatory quarantine period for incoming travelers. The new quarantine requirement is tentatively scheduled to start on April 1, and would be 7-10 days (instead of 14 days currently) on a case-by-case basis (details in the table), according to the Department of Disease Control. The proposal is pending official approval on March 19. The most important is the proposal to reopen the border to most tourists from October 1, which will improve inbound tourism. Krungsri Research is maintaining forecast for foreign tourist arrivals to recover significantly to 3.2 mn in 4Q21.

Domestic spending show signs of picking up after slowing down early this year following the second outbreak

Excess savings suggest domestic spending would expand when the pandemic ends

Excess savings (defined as the differential between actual savings and its trend) has surged since the pandemic started, to THB926bn at the end of 2020, accounting for almost 6% of Thai GDP. This implies large room for spending after the pandemic ends. Excess savings of individuals has surged to THB647bn (or c.4% of GDP) and that of businesses has increased to THB167bn (c.1% of GDP). These will support growth of private consumption and investment in the periods ahead.

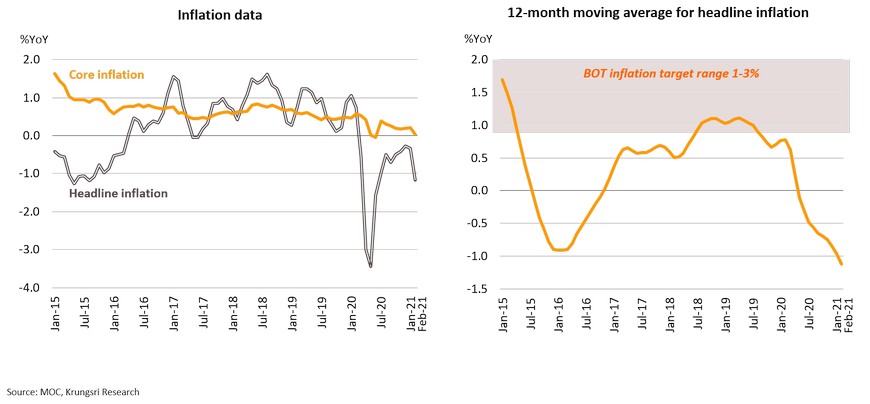

Inflation temporarily slipped into negative territory in February; expect to turn positive in 2Q21

February headline inflation fell to an 8-month low of -1.17% YoY from -0.34% in January, the 12th month in negative territory. This was partly driven by government measures to reduce water and electricity bills in February and March, coupled with lower prices of raw food (-1.38%). Price indices for other goods and services were mostly unchanged, in line with production and consumer demand, except retail gasoline prices which rose for the first time in 13 months following higher global oil prices. Core inflation (excluding volatile raw food and energy components) stood at 0.04% in February, down from 0.21% in January. For 2M21, average headline and core inflation came in at -0.75% and 0.12%, respectively. We expect headline inflation to return to positive territory in 2Q21 as the pandemic situation is improving, lockdowns are being eased, and the vaccination program is moving forward. In addition, government measures to support purchasing power would boost domestic spending, which would slowly push up consumer prices.

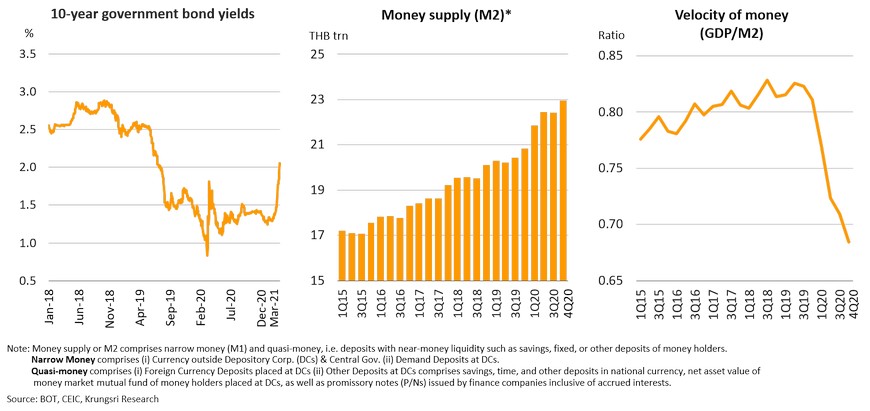

Despite rising bond yields and reflation concerns, MPC will maintain dovish stance given low velocity of money

Despite the recent spike in bond yields (to the highest since July 2019) and growing concerns over reflation amid rising money supply, there is no sign of tightening monetary policy because the economic recovery is in the early stage, and the velocity of money, which indicates frequency of transactions, remains at a historical low (at 0.68 vs a 5-year average of 0.80). Krungsri Research expects that the Monetary Policy Committee (MPC) will maintain accommodative monetary policy by keeping policy rate at a record low of 0.50% throughout this year. Meanwhile, the MPC is unlikely to cut policy rate given signs of economic recovery amid further relaxation of lockdown measures. At its last meeting, the MPC said that since the recovery remained uneven, it would be necessary to implement targeted measures aimed at specific groups. Officials are currently working on a new aid under the ‘asset warehouse scheme’, expected to start in 2Q21. This will be targeted at the hard-hit tourism industry, including hotels and related businesses who are debtors of commercial banks and SFIs. This implies no need of more rate cuts.

Regional Economic and Policy Developments in March

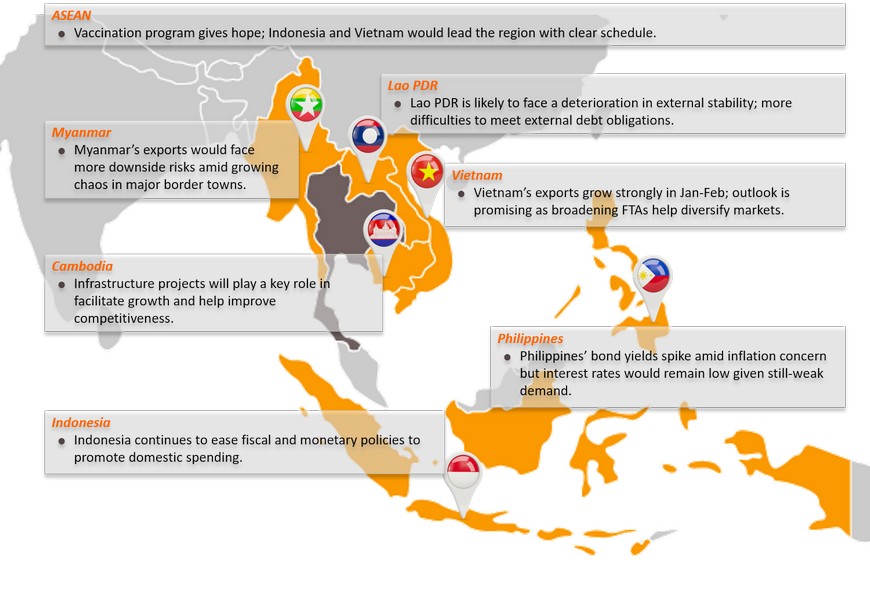

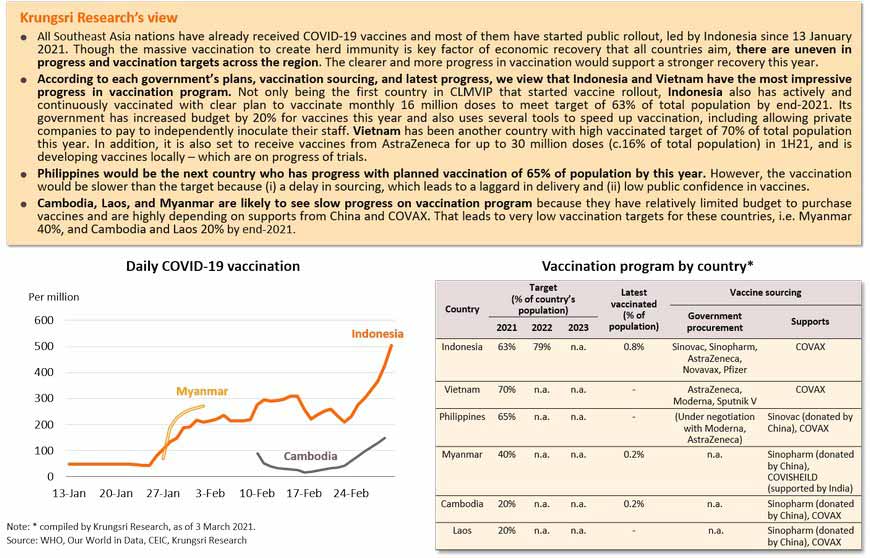

ASEAN’s vaccination program gives hope; Indonesia and Vietnam would lead the region with clear schedule

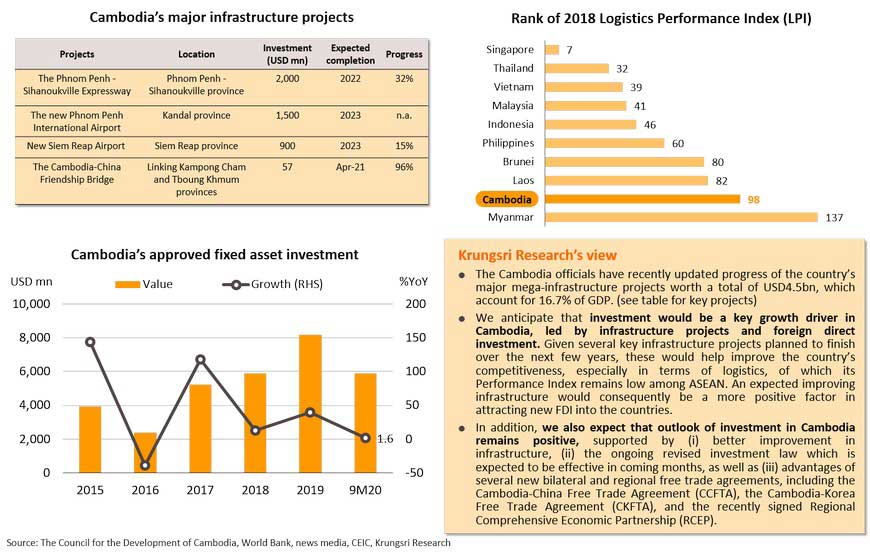

Cambodia: Infrastructure projects will play a key role in facilitate growth and help improve competitiveness

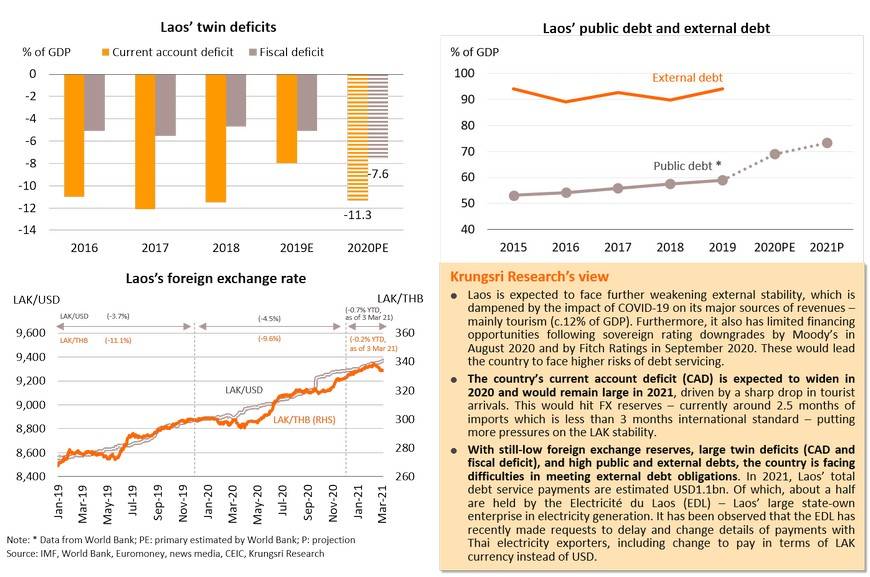

Lao PDR is likely to face a deterioration in external stability; more difficulties to meet external debt obligations

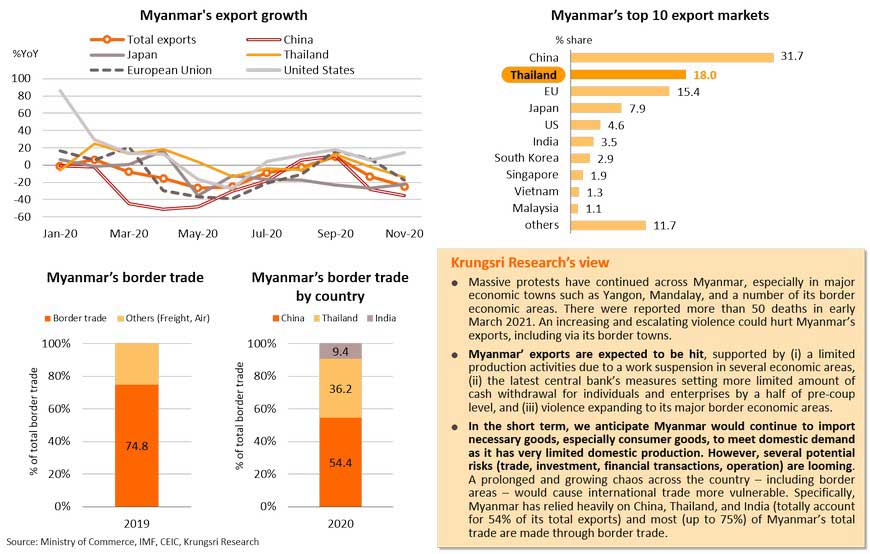

Myanmar’s exports would face more downside risks amid growing chaos in major border towns

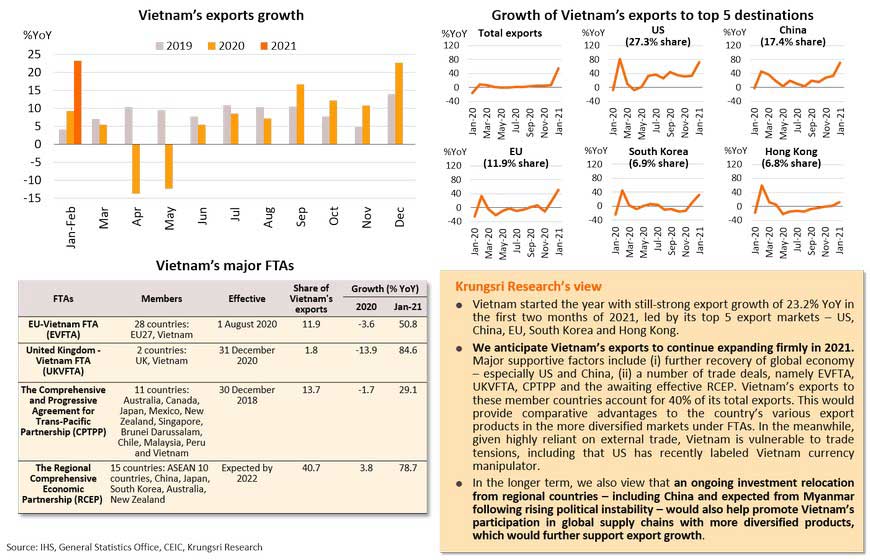

Vietnam’s exports grow strongly in Jan-Feb; outlook is promising as broadening FTAs help diversify markets

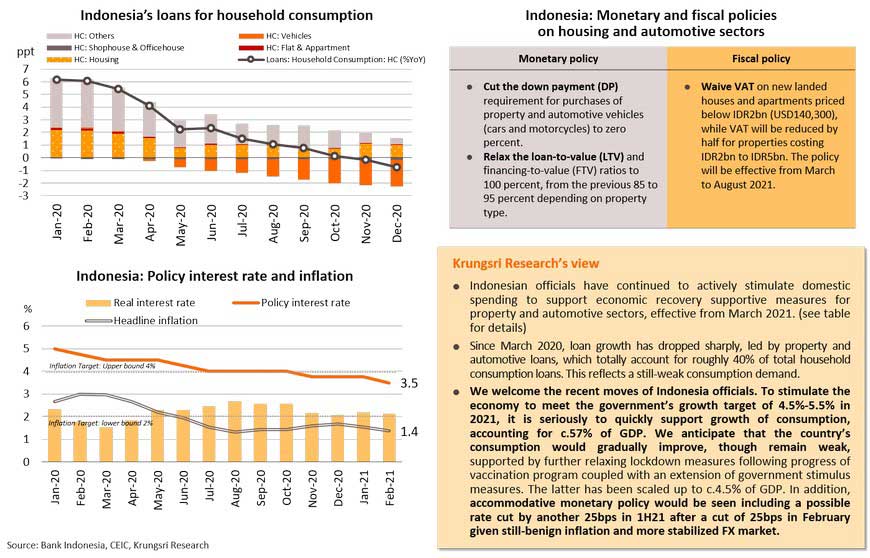

Indonesia continues to ease fiscal and monetary policies to promote domestic spending

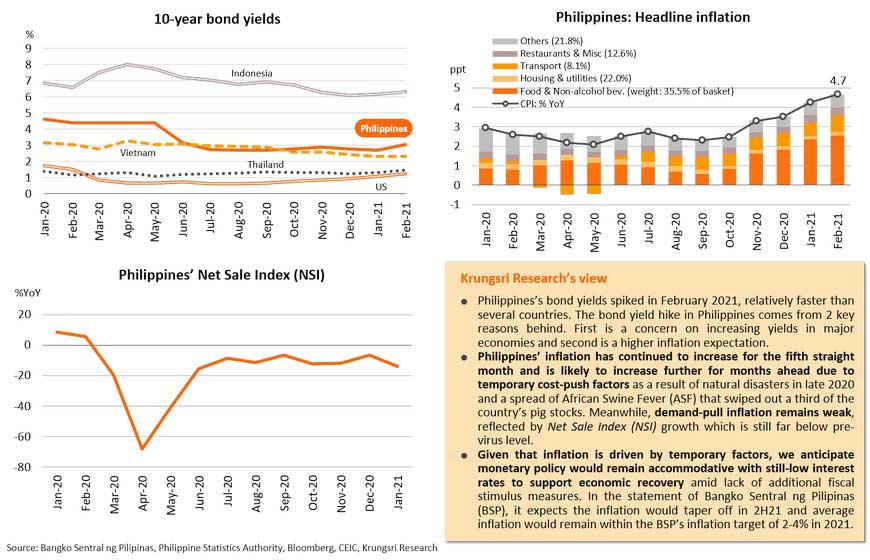

Philippines’ bond yields spike amid inflation concern but interest rates would remain low given still-weak demand