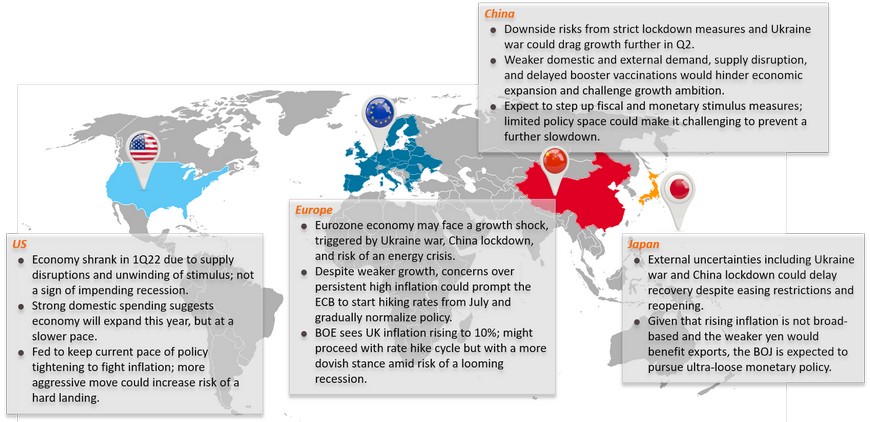

Global: Multi-speed economy

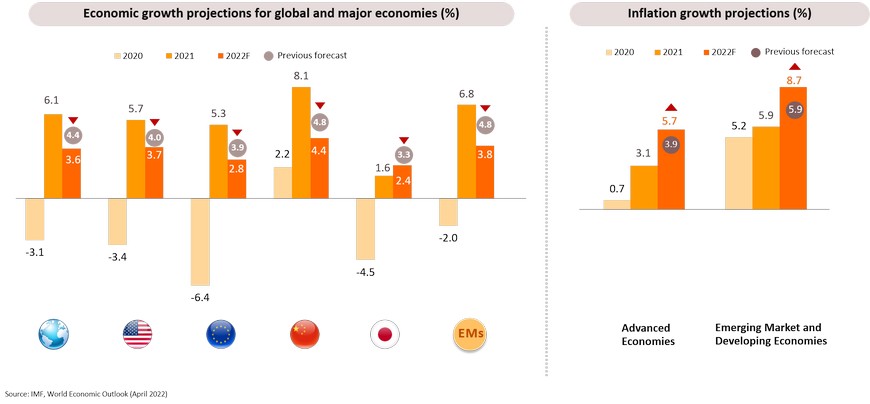

IMF trimmed 2022 global growth forecast because of Ukraine war, but raised inflation outlook due to soaring commodity prices and supply-demand imbalances

Global economic growth is at its weakest since June 2020, amid slowing manufacturing activity, downturn in China, and rising inflationary pressure

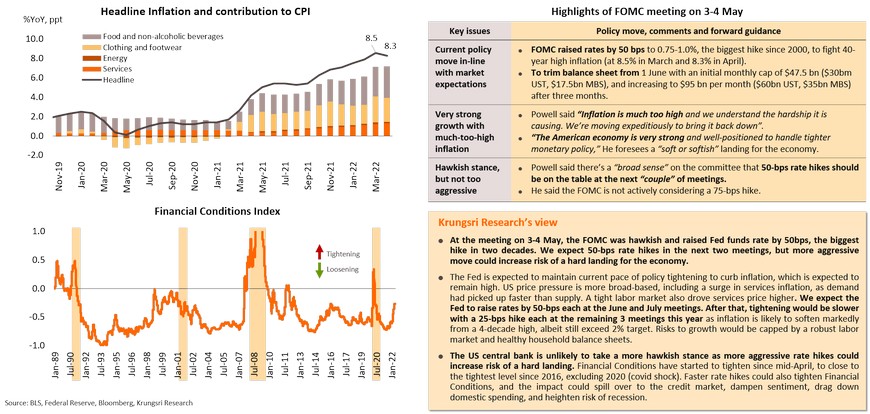

US: Economy shrank in Q1 due to supply disruptions and unwinding of stimulus; not a sign of impending recession

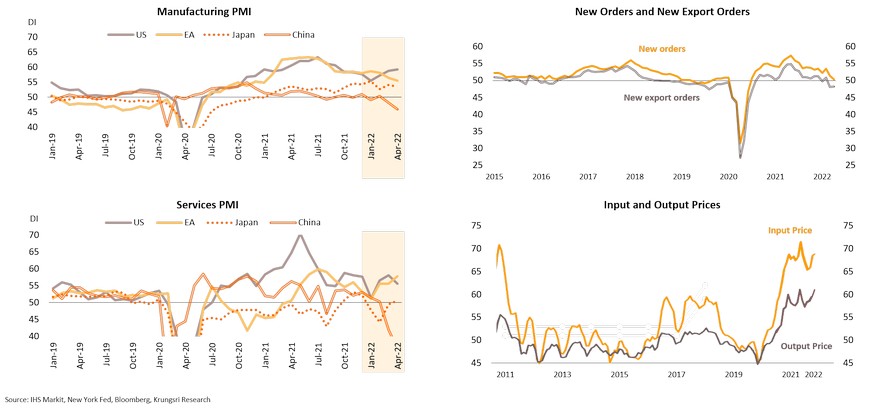

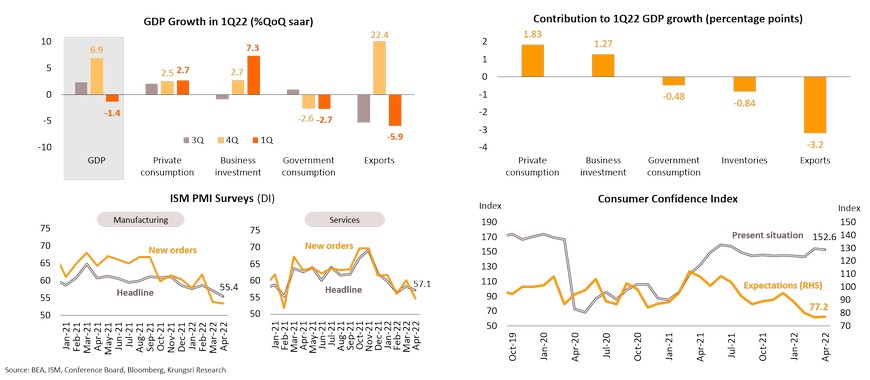

The negative GDP growth in 1Q22 in the US was mainly due to supply disruptions, not a sign of recession. 1Q22 GDP fell by 1.4%, triggered by (i) a wider trade deficit with surging imports and falling exports due to pandemic-related supply-chain constraints; (ii) slower inventory restocking; and (iii) fading impact of government stimulus spending to address the pandemic. In April, ISM Manufacturing PMI dropped for a second straight month to its lowest since July 2020, amid supply disruptions and labor shortage. ISM Services PMI remained strong but growth slowed down in April as a result of high inflation, high material costs, capacity constraints and logistical challenges. For consumer confidence, the Present Situation Index edged down but remains high, with stronger intention to buy big-ticket items like automobiles and appliances. The Consumer Expectation Index had stopped falling amid high oil prices and the war in Ukraine. Despite a potential slowdown in economic activity due to supply constraints and other headwinds, several economic indicators suggest domestic spending would continue to expand in 2Q22.

Strong consumer and business spending suggest US economy will expand this year, but at a slower pace

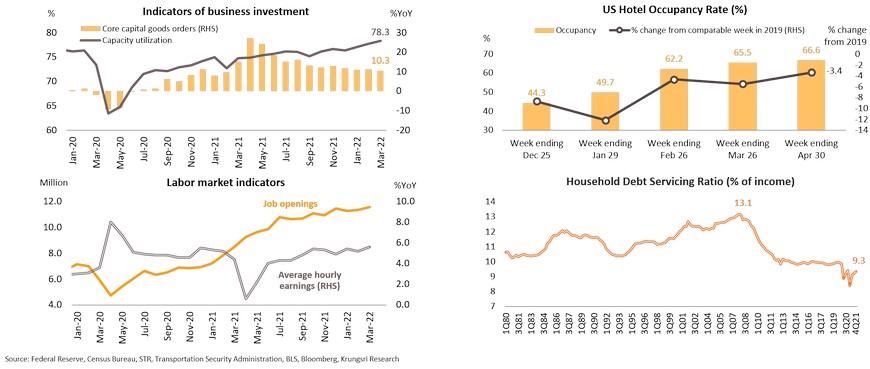

The domestic economy remains resilient with strong growth of consumer and business spending. Business investment had surged, reflected by (i) a 10% YoY increase in Core Capital Goods New Orders (non-defense capital goods used in the production of goods or services, excluding aircraft) in March, and (ii) a rise in Capacity Utilization rate to 78.3%, the highest since January 2019. Consumers are spending more on services following fewer Covid-19 cases and lifting of pandemic restrictions. Travel is a key driver. US hotel occupancy continued to rise to 66.6% for the week ended April 30, only 3.4% below pre-Covid level. About 2.1 mn people passed through airport checkpoints in late April, up from 1.4 mn three months earlier. The strengthening labor market and rising wages suggest consumer spending would continue to improve. Household balance sheets are strong. Buffered by pandemic savings, Household Debt Servicing Ratio (repayment/income) is the lowest in 40 years, which means households would be able to weather high costs by either dipping into savings or expanding borrowing.

Robust domestic spending and high inflation risks suggest Fed would keep pace of policy tightening; more aggressive move could increase risk of a hard landing

Eurozone: Economy could face a growth shock because of Ukraine war, China lockdowns, and risk of an energy crisis

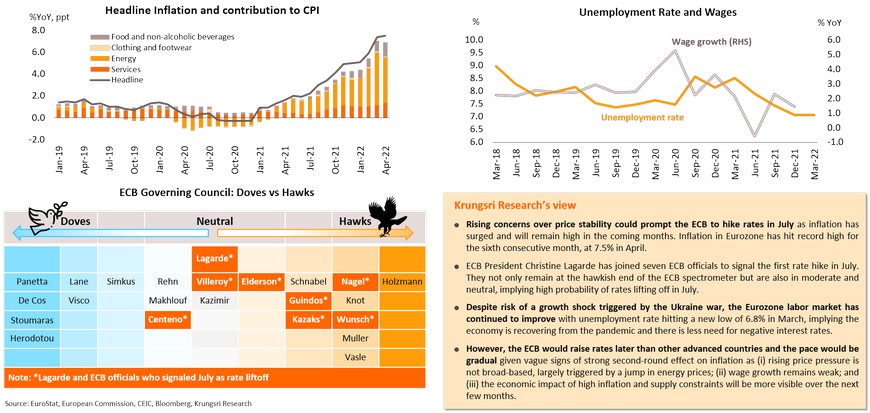

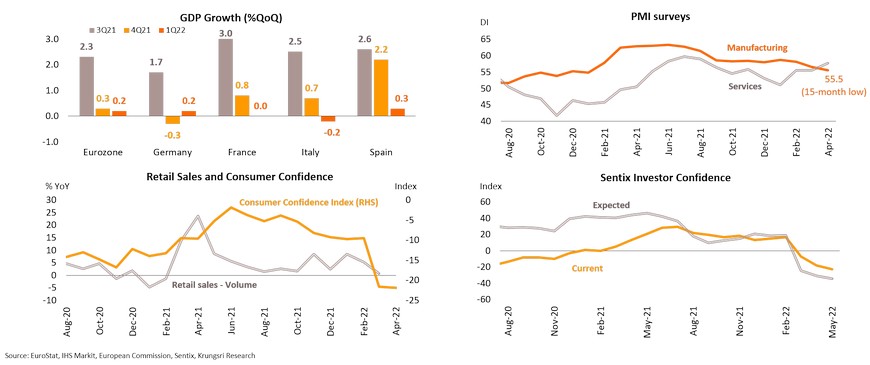

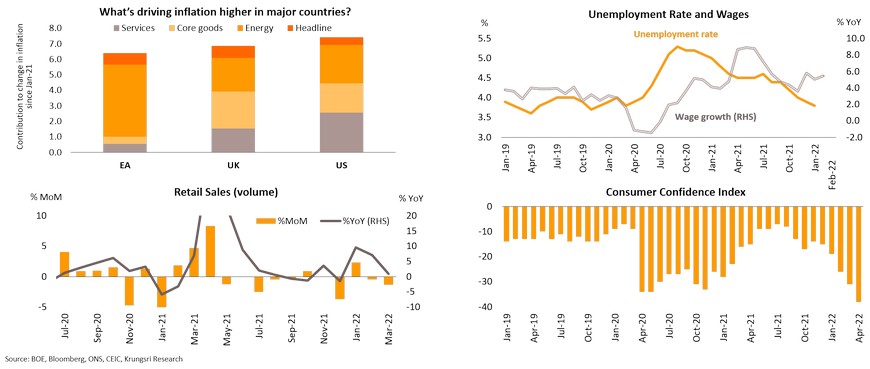

Despite Eurozone recording positive growth in 1Q22, it decelerated to only 0.2% qoq sa driven by weakness in Germany and Spain, stagnation in France, and a contraction in Italy. Eurozone economy could experience stagnation in 2Q22 given greater negative impact from the Ukraine war and extended lockdowns in China which have worsened supply-side issues. Manufacturing PMI hit a 15-month low in April but Services PMI rose following the lifting of Covid-19 restrictions. Surging energy prices are also dampening consumer and business confidence. Soaring inflation is affecting households’ real income and business profit margins. March retail sales volume saw the weakest growth since February 2021 and April Consumer Confidence Index dropped to its lowest in two years. In May, Sentix Investor Confidence continued to decline to an almost two-year low and the Expectation Index is at its lowest since December 2008. And given energy embargo risks, the growth shock would be worse. Russia’s energy firm Gazprom has halted gas flows to two EU nations for not paying for the commodity in rubles. The move sparked fears Russia would also stop supplying gas to other countries. There is rising pressure on Europe as Russia has imposed sanctions on Gazprom Germania, the former Germany-based unit of Russian gas producer Gazprom, a day after Ukraine stopped a major gas transit route.

Despite ripple effect of Ukraine crisis and China lockdowns, rising concerns over persistent high inflation could prompt ECB to hike rates in July and gradually normalize policy

UK: BOE raises rates to 13-year high, sees inflation rising to 10%; will proceed with rate hike cycle but at a more dovish pace amid looming risk of a recession

At the meeting on 5 May, the Bank of England (BOE) voted 6-to-3 to raise base interest rate for the fourth consecutive meeting, by 25 bps to 1%, the highest since 2009. The minority preferred to hike rates by 50bps. The BOE is expected to continue to normalize policy to curb risk of persistent inflation from a tightening labor market. While unemployment rate fell to 3.8% in February, the lowest since the pandemic, inflation hit a 30-year high of 7% in March. The BOE expected inflation to rise to 10% this year. However, we expect the pace of rate hikes to be slower, possibly delivering up to 2 hikes only in 2H22 given slow inflation in the services sector (relative to the US) and looming risk of a recession. Recent indicators suggests a deteriorating growth outlook. UK GDP contracted by 0.1% in March, compared to 0% in February. Retail sales volume dropped for the second straight month in March and Consumer Confidence Index plunged to a near record low in April. The BOE also expects UK GDP to shrink in 4Q22, partly reflecting the projected large hike in household energy bills in October. The BOE projects 2023 economic growth would turn to negative 0.25% (vs previous forecast of +1.25%).

China: Downside risks from strict lockdown measures and Ukraine war could drag growth further in Q2

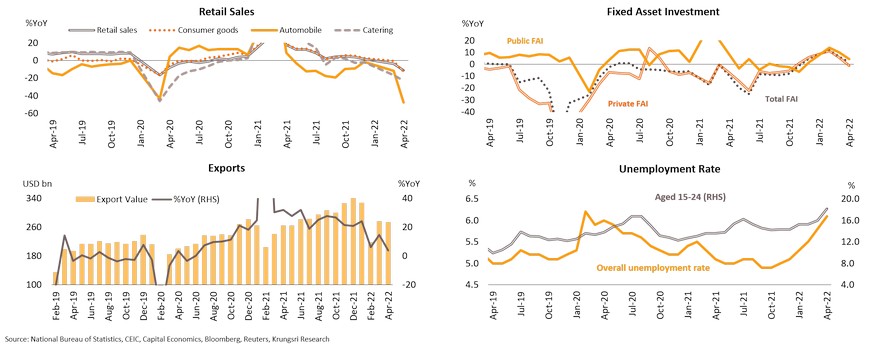

The major economic growth drivers have showed signs of weakening since the beginning of this year. The outbreaks and following lockdowns in parts of Shanghai since mid-March and tighter restrictions in Beijing during April to contain cases have continued to dampen expenditure. April’s retail sales dropped for the second straight month, as spending on consumer goods, automobile and catering services slumped. Fixed asset investment growth slipped to 1.8% YoY in April from 6.6% in March, driven mainly by a contraction private investment for the first time in 5 months, while public investment slowed down further, due to disrupted manpower from stringent restrictions. On the external front, export growth slowed to 3.9% in April, its weakest since June 2020, which underlines weaker global demand and worsening supply chain disruption triggered by the extended Russia-Ukraine war and domestic lockdowns. Looking at 2Q22, economic growth would be dampened further by the following: (i) possibly extended lockdowns in China, which would disrupt supply and economic activity, (ii) prolonged Ukraine war and intensifying sanctions against Russia, which could weigh on exports, and (iii) combined effects of lockdowns and war could pressure economic activities and weaken the labor market, indicated by a more than 2-year high of 6.1% unemployment rate in April, which would further deteriorate household purchasing power.

Weaker domestic and external demand, supply disruptions, and delayed booster vaccinations could hinder economic expansion and challenge growth ambition

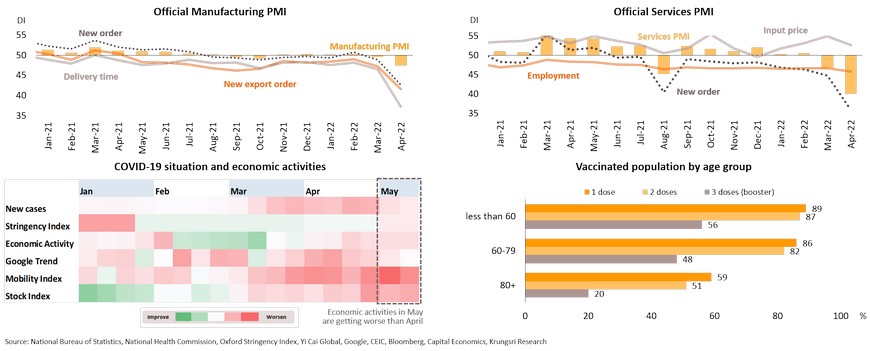

Recent economic indicators show China’s economy has continued to lose momentum. In April, the Composite PMI slipped to 42.7, the lowest since February 2020, led by a contraction in PMI data for Manufacturing (47.4) and Services (40.0) for the second month. This mostly reflected the impact of China’s zero-COVID policy in major areas, especially Shanghai, and exacerbated by the Ukraine war. High-frequency data, which mirror the effect of the lockdown in Beijing since the last week of April, indicates greater economic impact of containment measures although the number of daily cases are trending down. Overall, China’s economy growth for the rest of the year would be dragged by several obstacles, including, (i) simultaneous slowdown in domestic and external demand, reflected by the PMI sub-indices for new orders and new export orders, which have dropped to their lowest since 2020, (ii) supply chain disruptions triggered by China lockdown and the Russia-Ukraine conflict has led to a sharp drop in delivery time sub-index within the Manufacturing PMI to its worst in more than 2 years, and (iii) delays in vaccinating vulnerable people with booster shots, especially the elderly. In March, only half of Chinese residents aged 80 and above had been fully-vaccinated and just one-fifth of these have received a booster shot. In all, the economy is expected to experience a further slowdown and it would be difficult to meet its 5.5% official growth target for 2022.

Expect to step up fiscal and monetary stimulus measures but limited policy space could make it challenging to prevent a further slowdown

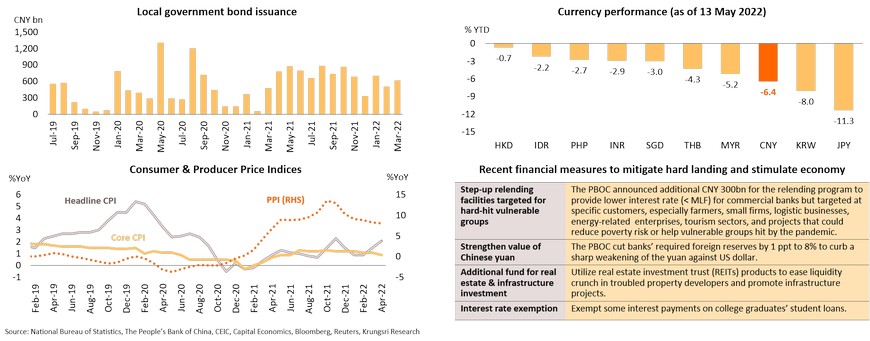

To mitigate a sharp economic slowdown, authorities need to employ more accommodative measures against escalating risks. On the fiscal front, local government bond issuance in the first 3 months of 2022 was more than the same period last year and the government has pledged to step up infrastructure investment. In terms of monetary policy, the People’s Bank of China (PBOC) announced on 15 May to cut interest rates for mortgage loans for first-home buyers by 20 bps to 4.4%. In fact, the PBOC has limited room to cut interest rates due mainly to capital outflows following rate hikes by other major central banks. In early-May, the yuan hit an 18-month low and had depreciated against the US dollar by 6.4% YTD. On the inflation front, headline inflation rose to 2.1% in April, the highest in 4 months, but rising prices were uneven and concentrated in food and energy categories. Looking forward, there is still some space for accommodative monetary policy supported by still-low core inflation and decelerating growth in the Producer Price Index which suggest weak demand-pull pressure and easing production costs. Monetary easing in the next period is expected to be targeted and structural instead of a broad-based interest rate reduction as indicated by the recent PBOC’s measures to ease the adverse impacts particularly on vulnerable groups. Given limited policy space due to risk of capital outflow and risk to economic stability, additional fiscal and monetary measures might not be able to prevent an economic slowdown.

Japan: External uncertainties including Ukraine war and China lockdown could delay recovery despite easing restrictions and reopening

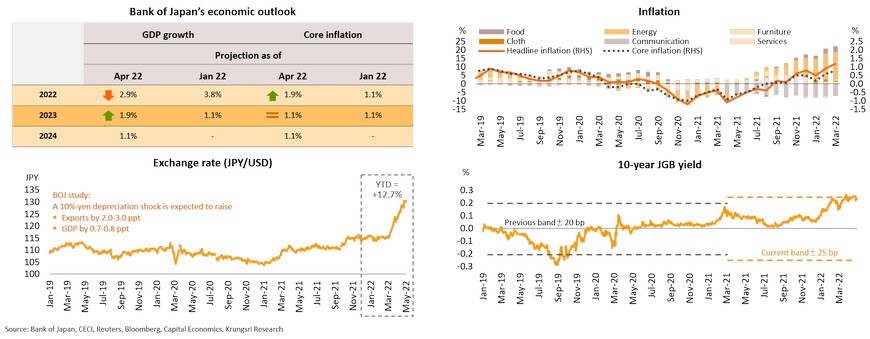

Japan has resumed economic activity following easing omicron fears but the negative impact of the Ukraine war and China lockdown have started to kick-in. Industrial production fell 0.8% YoY in March (vs +0.5% in Feb) because of supply chain disruption. Export volume to China, the largest market at 23% of total exports, shrank partly due to the latest lockdowns there. Manufacturing PMI dropped in April. However, there were several positive factors to cushion the negative external impact. First, easing containment measures have helped economic activity to resume, reflected in high-frequency data in May. In April, Services PMI returned to expansion territory for the first time in 4 months and consumer confidence inched-up for the first time in 6 months. Second, the reopening to foreign travelers from June will support recovery in the tourism sector despite arrivals being capped at 300,000 a month (vs pre-pandemic average of 2.6 mn per month). Third, the labor market has rebounded with unemployment rate falling to a 1-year low of 2.6% in March. In addition, new JPY6.2trn stimulus package funded by reserves under the FY2022 budget, equivalent to 1.2% of GDP, would mitigate the negative impact of rising energy prices and boost domestic demand in 2Q-3Q. However, economic recovery would be delayed by several risks mentioned above, suggesting a need for more accommodative measures.

Given that rising inflation is not broad-based and the weaker yen would benefit exports, the BOJ is expected to pursue ultra-loose monetary policy

Although inflation in Japan continues to rise and the yen has weakened sharply, the Bank of Japan (BOJ) is unlikely to rush to adjust monetary policy, for the following reasons. (i) Recovery is still fragile, reflected by lower industrial production and exports because of external factors. The BOJ also revised down its 2022 GDP growth projection to +2.9% from +3.8%. (ii) Rising inflation is not broad-based, mostly due to higher energy prices. In addition, the increment from April onwards would be driven by the low-base effect due to reductions in mobile-phone service fees since April 2021. There is weak demand-pull inflationary pressure with softening real wages. The BOJ projects inflation would drop from 1.9% projected for 2022 to 1.1% in 2023 and 2024. (iii) The weaker yen is expected to drive up exports and economic growth. Based on a BOJ study, a 10% depreciation of the yen would raise exports by 2.0-3.0 ppt and lift GDP growth by 0.7-0.8 ppt. Although a weaker yen could lead to higher inflation, fiscal measures, including subsidies and a reduction in energy tax, would help to mitigate the impact. Meanwhile, although 10-year JGB yield has exceeded the official ceiling of 0.25%, the BOJ is unlikely to tweak policy by widening the tolerance band and would thus wait for a more sustainable recovery, especially reopening effects on the tourism sector. Policy interest rates would be kept at record lows as inflation is projected to stay below target over the next two years.

Thailand: Divergent growth across key drivers amid external headwinds

- Thailand has started to allow quarantine-free entry to fully-vaccinated foreign tourists on expectations a recovery in the tourism sector would drive overall economic growth. While services sector looks set to recover, manufacturing growth is slowing down following external headwinds. On demand side, reopening effects in general should release pent-up demand by middle- to upper-income classes but high inflation would eat into consumers’ real income and businesses’ profit margin. Path of economic recovery will remain uneven with divergent growth across key drivers.

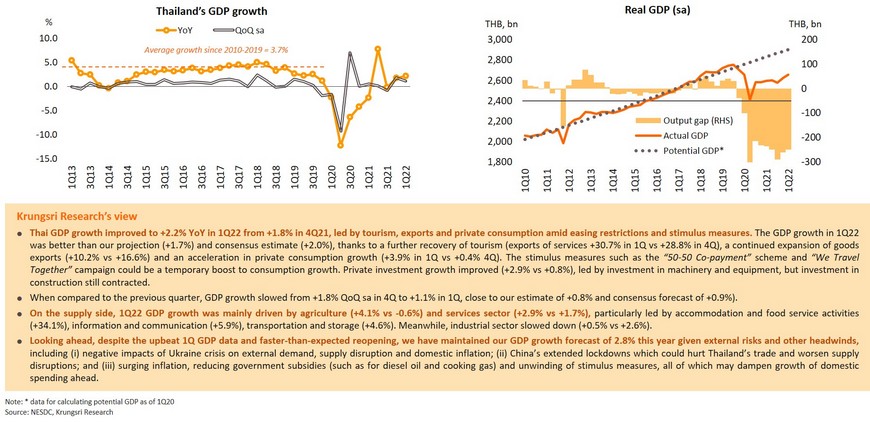

- 1Q22 GDP growth improved to +2.2% YoY in 1Q22 from +1.8% in 4Q21, led by tourism, exports and private consumption amid easing restrictions and stimulus measures. The GDP growth in 1Q22 was slightly better than our projection (+1.7%) and consensus estimate (+2.1%). However, we have maintained our GDP growth forecast of 2.8% this year given negative impacts of Ukraine crisis and China’s extended lockdowns. Also, surging domestic inflation, reducing government subsidies and unwinding of stimulus measures all may dampen growth of domestic spending ahead.

- Thai exports surged in 1Q, which could lift our full-year growth forecast but we expect exports to slow down the rest of this year. Global economic slowdown and supply chain disruption are starting to show in trade data, could hurt Thai exports going forward. Manufacturing could be hurt by global slowdown and lingering supply chain disruptions; consumer demand will shift from goods to services.

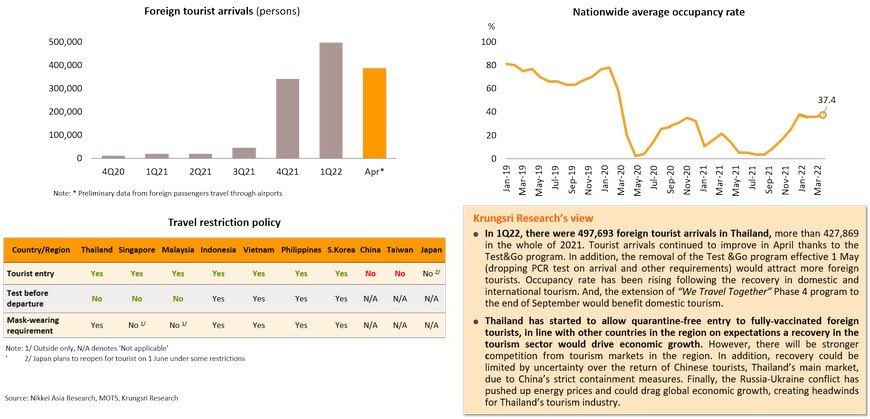

- Tourism sector is improving with the removal of Test & Go program but there could be stronger competition in the region. Following easing Covid-19 cases after the long Songkran holiday, Thailand has downgraded Covid-19 alert level from 4 to 3 effective May 9, allowing more economic activities to resume. Large excess savings since pandemic mostly parked in savings accounts, reflecting middle- and upper-income groups are prepared to spend.

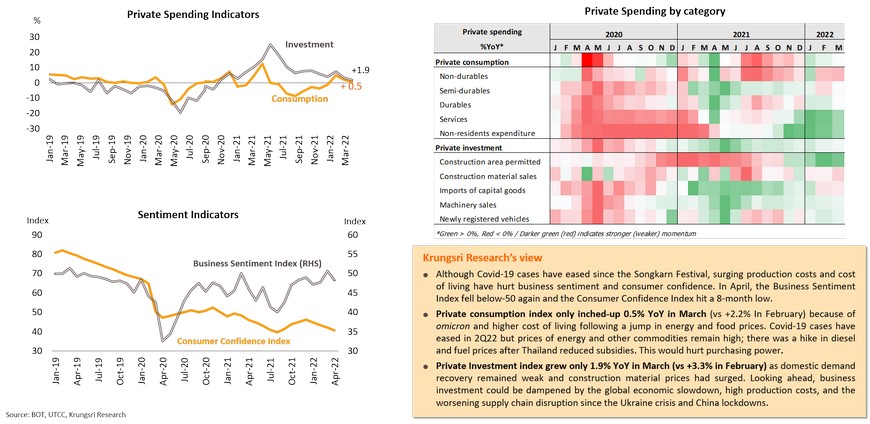

- For private spending, easing pandemic fears is a domestic tailwind but several external headwinds and high inflation could dampen consumer and business spending.

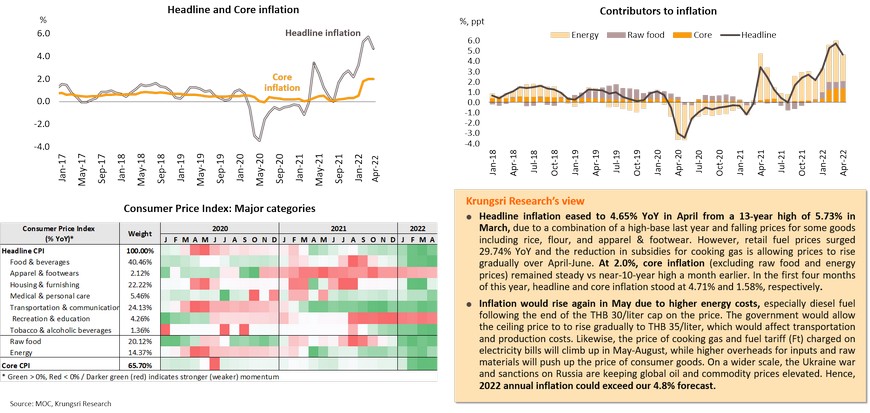

- Inflation rate is expected to rise again in May after easing in April. Given still-high energy prices and smaller-than-expected government subsidies, 2022 annual inflation could exceed our 4.8% forecast.

- Thailand is less vulnerable to external shocks than peers, allowing the MPC to maintain low policy rate this year to support economic activity which remain weaker than peers.

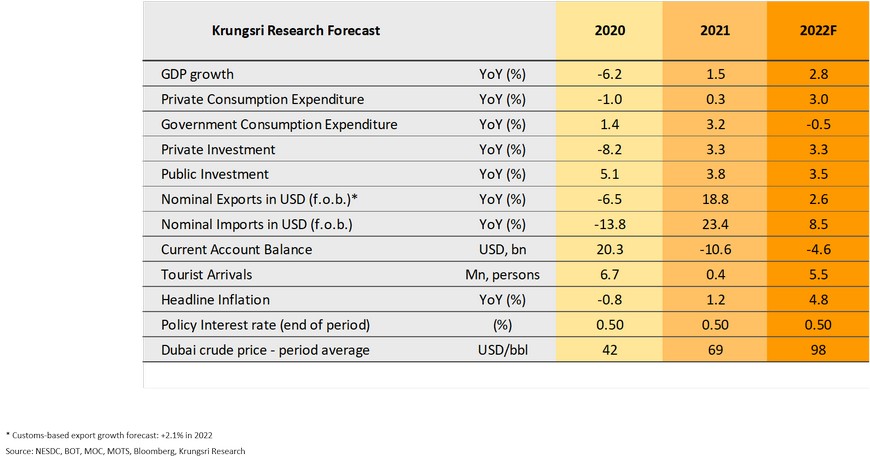

Krungsri Research Forecasts for 2022

1Q22 GDP grew slightly better than expected by +1.1% QoQ sa, +2.2% YoY but our full-year growth forecast maintained at 2.8% given rising downside risk the rest of this year

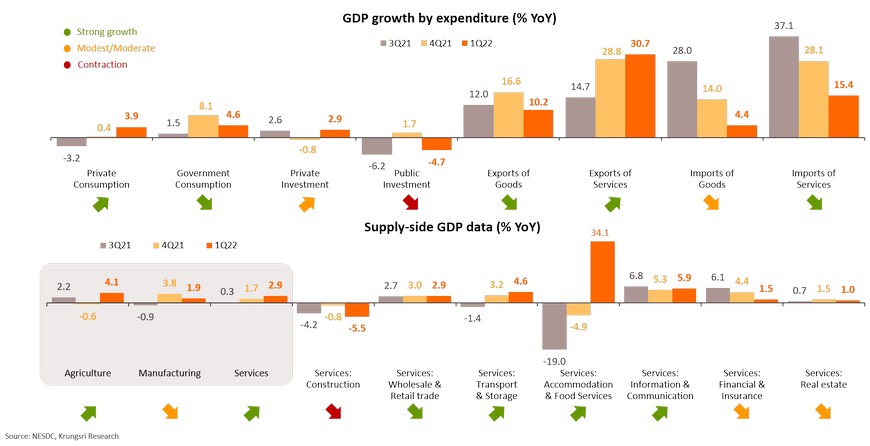

Major drivers for 1Q GDP were improving tourism, growing exports, and a temporary boost on consumption; slowing manufacturing sector limits supply-side growth

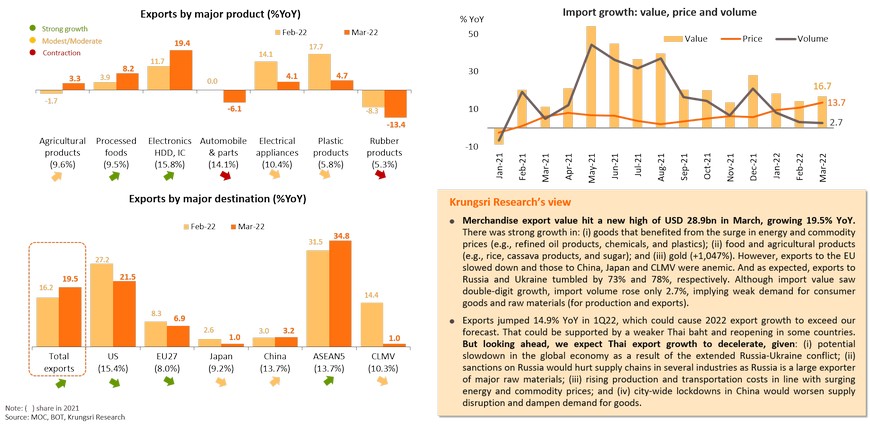

Exports surged in 1Q, which could lift our full-year growth forecast but we expect exports to slow down the rest of this year

Global economic slowdown and supply chain disruption are starting to show in trade data, could hurt Thai exports going forward

Total export value surged nearly 20% YoY, partly boosted by gold exports. Without gold, March export value grew only 9.5%.

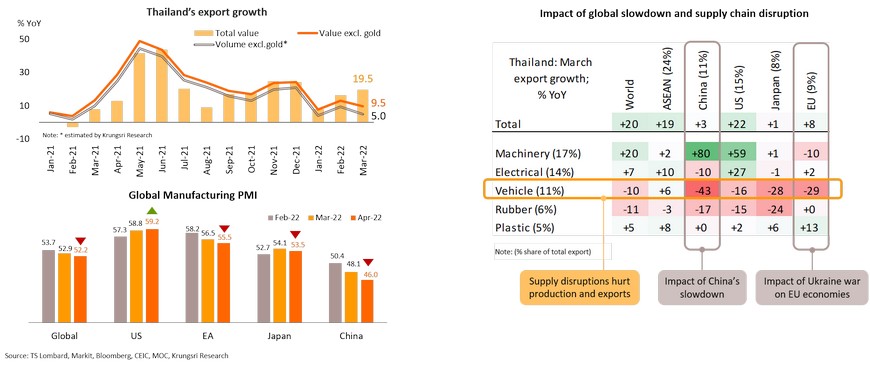

Excluding gold and price effect, exports grew only 5.0% in March, reflecting weaker export volume. The marked slowdown in Thai exports to China and Europe as well as the contraction of automobile exports (as a result of supply chain disruption) reflect the spillover effects from an economic slowdown in China and the Ukraine crisis. Global Manufacturing PMI slowed down in April with weaker growth in key trading partners, including Eurozone, China and Japan. We expect Thailand’s international trade data to weaken further because of the extended Russia-Ukraine conflict and lockdowns since March and stricter containment measures since late-April in China hurting its economy.

Manufacturing could be hurt by global slowdown and lingering supply chain disruptions; consumer demand will shift from goods to services

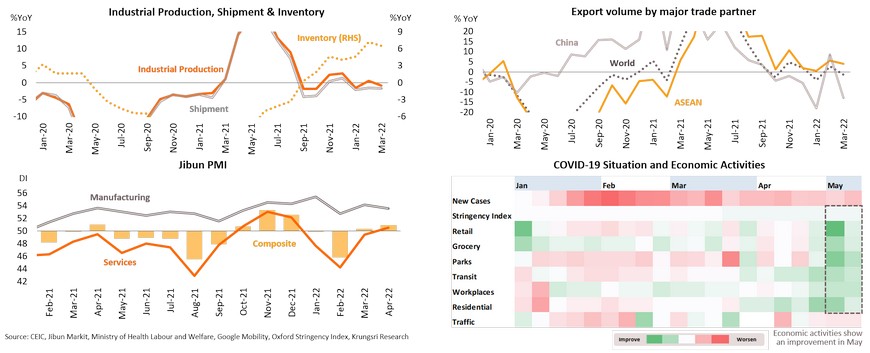

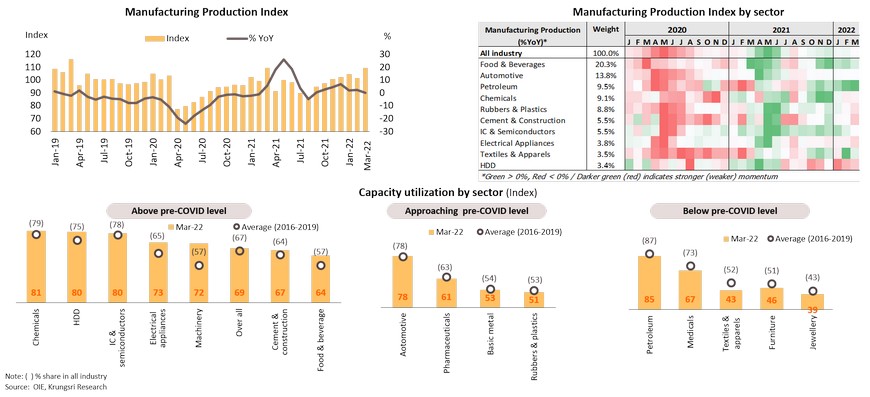

Capacity utilization rate in the manufacturing sector is slightly above pre-COVID level, led by Chemicals, HDD, IC & Semiconductors, Electrical Appliances, and Machinery. Utilization rates in Automobile, Pharmaceutical and basic metal industries are close to pre-COVID level. However, the global economic slowdown and lingering supply chain disruption would drag recovery in the manufacturing sector. The Manufacturing Production Index (MPI) contracted for the first time in 7 months in March, by 0.1% YoY. Some manufacturing industries have been hit by components shortage, such as Electrical Appliances and IC & Semiconductors. In addition, following the relaxation of Covid-19 measures, consumer demand will shift from manufactured goods to services such as travel and recreation.

Tourism sector is improving with removal of Test & Go program but there could be stronger competition in the region

Following easing Covid-19 cases after Songkarn festival, Thailand has downgraded Covid-19 alert level from 4 to 3 effective May 9, allowing more economic activities to resume

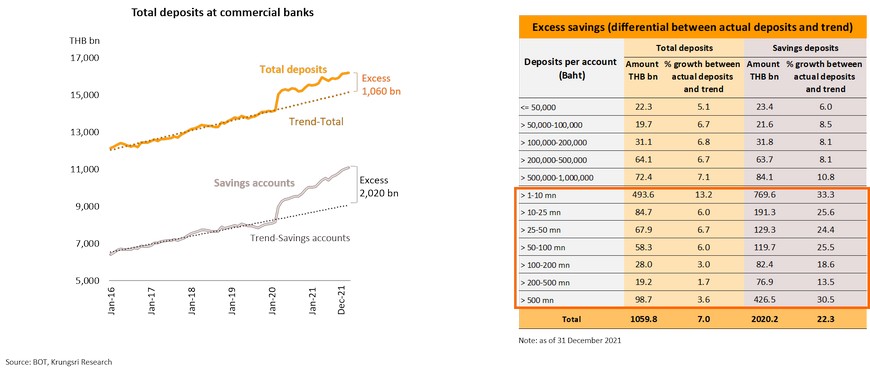

Large excess savings since pandemic mostly parked in savings accounts, reflecting middle- and upper-income groups are prepared to spend

Excess savings (defined as the differential between actual savings and its trend) has surged to THB1060 bn at end-2021, accounting for almost 6.5% of GDP. Excess savings has risen 14% from THB928 bn at the end of 2020, compared to trend of only +3.6% total deposits growth. By type of account (including demand deposits, savings deposits, and time deposits), savings accounts registered THB2,020 bn excess savings, led by accounts with THB1-10mn each which accounted for 34% of total excess savings in savings account. This not only indicates precautionary savings but also means the middle- and upper-income groups are prepared to spend. When the pandemic ends or the government introduces stimulus measures for these groups, their large excess savings would drive domestic spending.

Private spending: Easing pandemic fear is a domestic tailwind but several external headwinds and high inflation could dampen consumer and business spending

Inflation rate eased in April but is expected to rise again in May given higher energy prices and smaller government subsidies

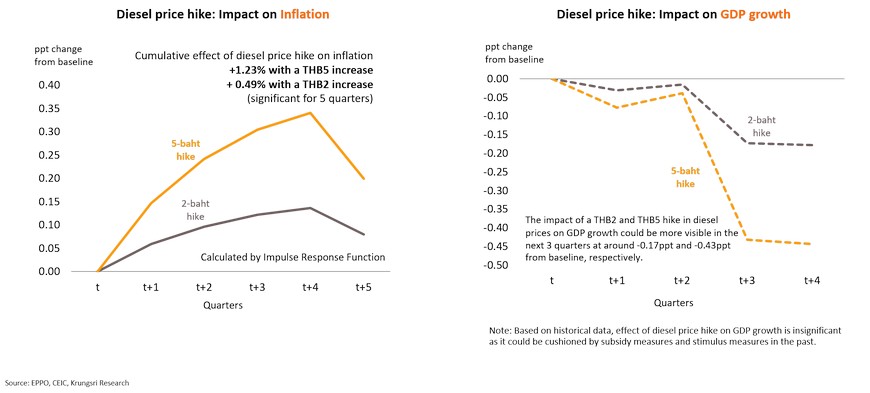

Impact of diesel price hike: A 2-baht and 5-baht hike in domestic diesel prices would lift headline inflation (from baseline) by 0.49 and 1.23 ppt, respectively

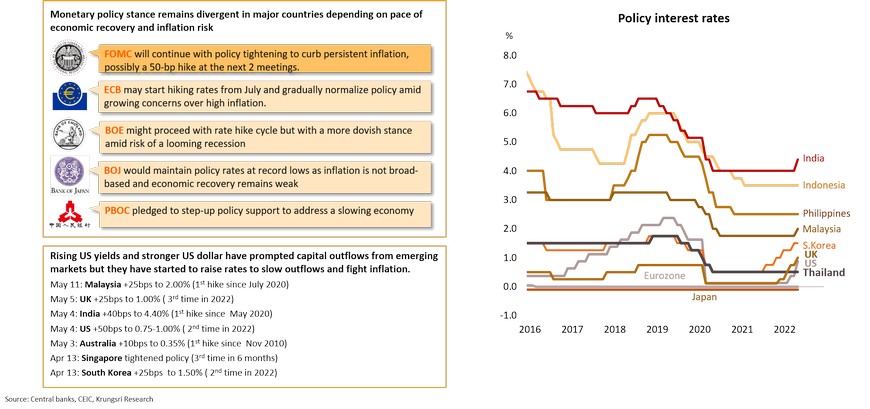

To curb high inflation amid the economic recovery, central banks have started to raise policy rates but at different pace depending on risks to growth and stability

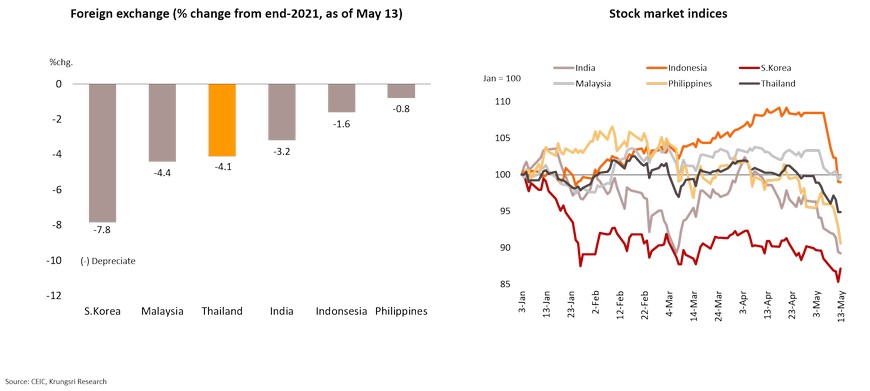

Asian currencies continued to weaken against USD and stock indices have dropped in response to Fed’s aggressive rate hikes and fears of fund outflows

MPC: Thailand is less vulnerable to external shocks than peers, allowing MPC to maintain low policy rate this year to support economic activity which remains weaker than peers