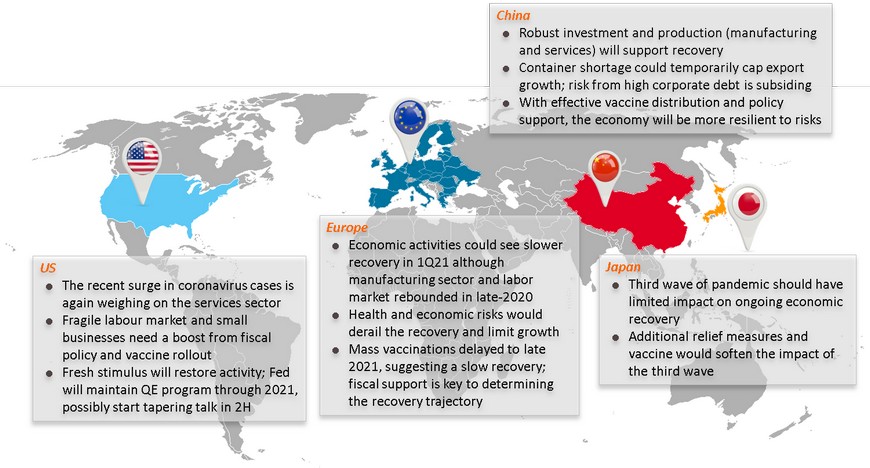

Global: Risk & resilience amid a resurgence in COVID-19

Global daily COVID-19 cases have been rising again since late 2020, delaying the global economic recovery

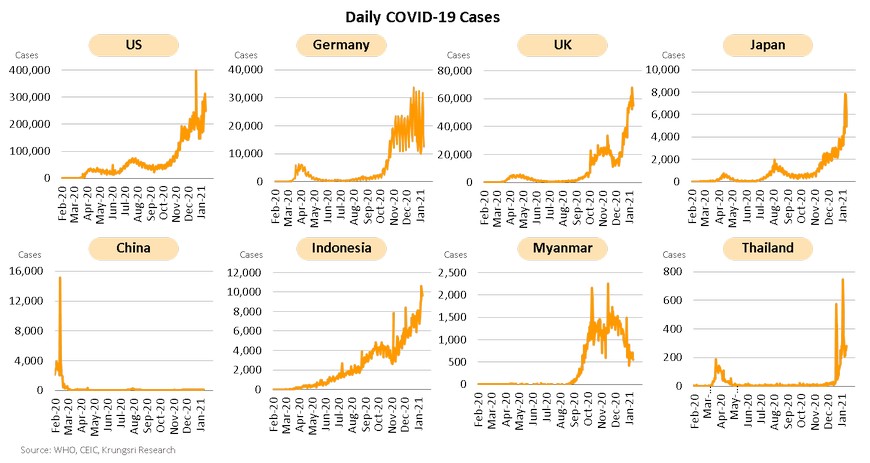

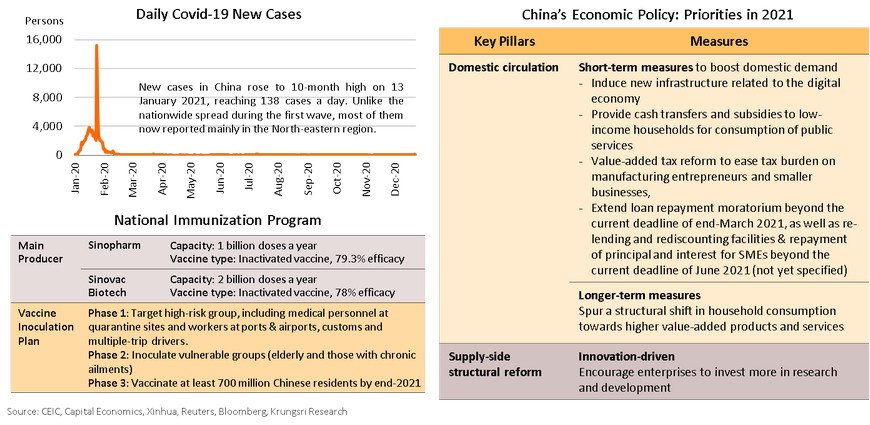

Daily COVID-19 cases in major economies and several other countries have been rising again since late December. New cases have skyrocketed to more than 200,000 in the US, 50,000 in the UK, 30,000 in Germany, and 6,000 in Japan. China also saw the biggest COVID-19 spike in over 10 months, although the number is low relative to most countries. Several Asian countries also experienced a sharp rise in cases. The resurgence of COVID-19 infections has forced governments to impose more restrictions and measures to control the pandemic, which will disrupt economic recovery at least in the first quarter of this year.

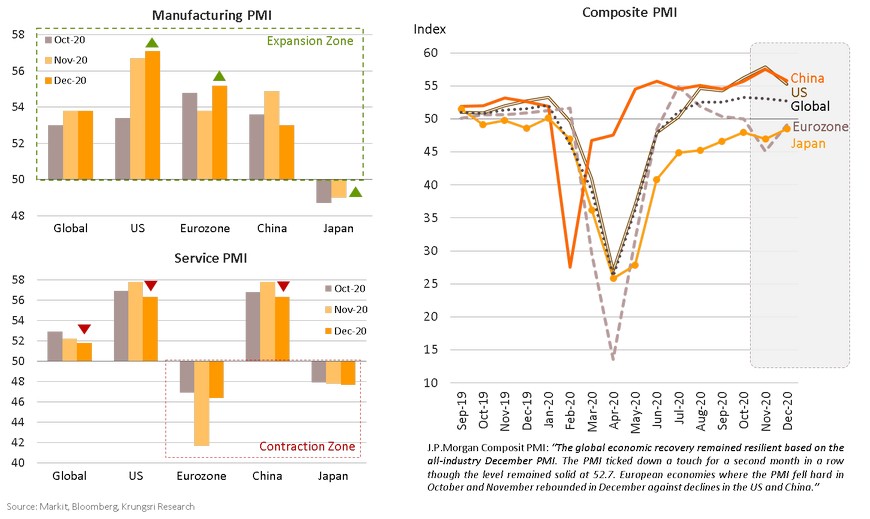

Resurgence heightens risks to services sector, but resilient manufacturing sector will support global growth

US: Resurgence of COVID-19 cases is weighing on services sector again

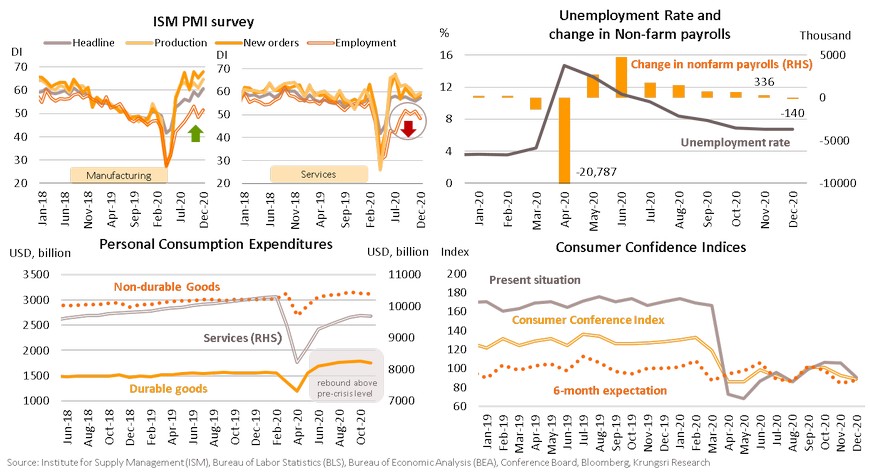

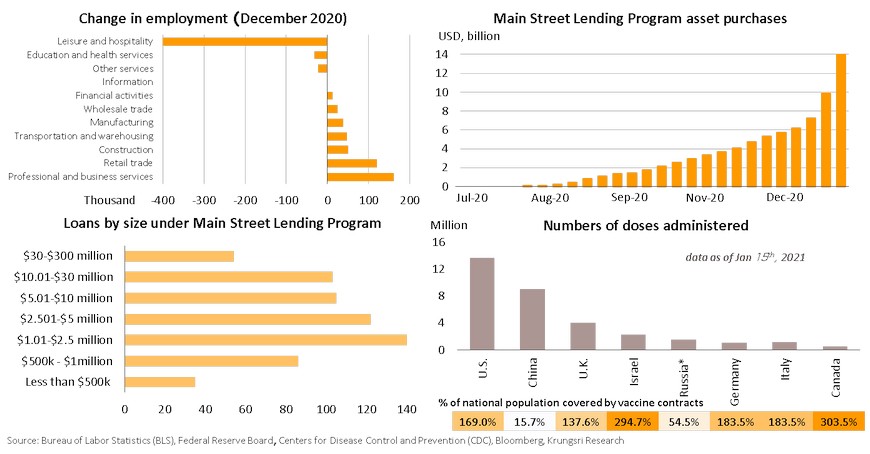

Renewed lockdown in some states revealed visible impact on the services sector but manufacturing and spending continued to rebound. Manufacturing PMI inched up to 60.7 in December 2020 from 57.5 in the previous month, and all sub-indices improved. Services PMI also inched up from 55.9 in November to 57.2 in December, but the Employment Index slid to contraction territory at 48.2. The raging cases also restrained the labour market in December. Non-farm payrolls fell by 140,000 jobs, the first loss since April 2020. Durable goods expenditure has rebounded to pre-crisis path, suggesting consumer demand is recovering. Looking at consumer sentiment, the Present Situation Index dropped to 90.3 due to fears of contracting the virus, while 6-month expectation rose slightly to 87.5 in December following reports of approvals for and distribution of vaccines. Hiring and consumer confidence would be suppressed until the mass population is vaccinated.

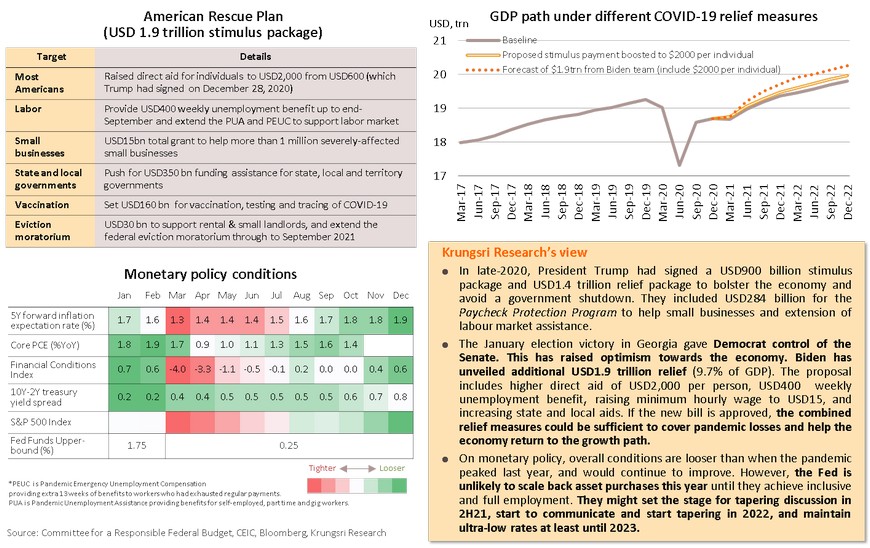

Fragile labour market and small businesses need a boost from fiscal policy and vaccine rollout

The economy is facing downside risks as the labour market is hit again by extended restrictions on bar and restaurants. Leisure and hospitality payrolls fell by 498k jobs in December. Some of the unemployed are shifting to gig work such as driver and delivery, putting pressure on income and employee benefits. Similarly, firms still need liquidity to survive the pandemic. Applications for the Main Street Lending Program had risen sharply ahead of its expiry on December 31 last year. There were more applications from medium-size firms than small firms, because the former have better ability to repay debt. This implies small businesses, which make up 76% of US businesses (in terms of annual sales) and employ 47.5% of Americans, will continue to struggle to access liquidity and require more policy support. Aside from policy, the rollout of vaccines under “Operation Warp Speed” would also help the economy. The US has signed vaccine supply contracts to cover more than 100% of the national population. US President-elect Joe Biden targets to vaccinate 100 million Americans in his first 100 days in office. At this pace, 75%-85% of Americans would be vaccinated by 3Q21, the number required to achieve herd immunity in order to resume normal activities.

Fresh stimulus will restore activity; Fed will maintain QE program through 2021, possibly start tapering talks in 2H

Europe: Slower recovery in 1Q21, although manufacturing sector and labour market rebounded in late-2020

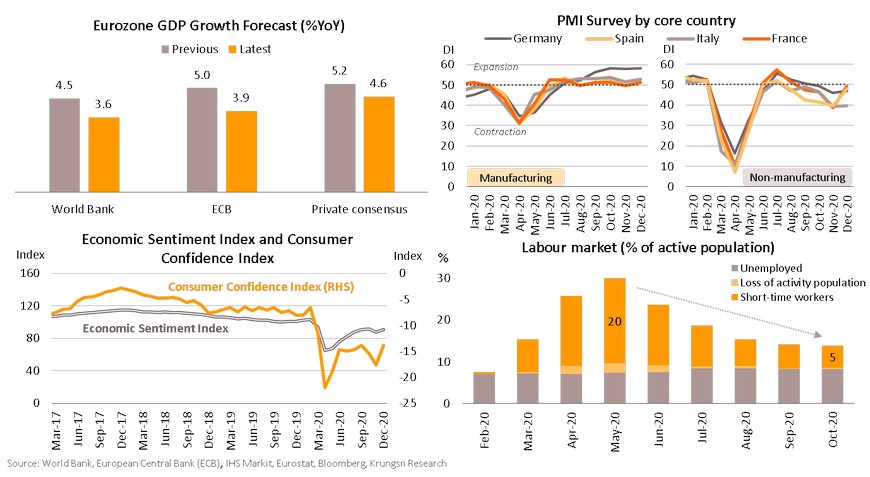

Eurozone economy will experience a slower-than-expected recovery in 2021. The World Bank estimates Eurozone GDP would expand by 3.6% this year instead of 4.5%, due to the resurgence of coronavirus and the overwhelming risks. The severity of lockdown illustrate a different pace of recovery between manufacturing and services sectors. Manufacturing PMI expanded across the region in December 2020, led by Germany, where activity rose to 58.3, the highest since March 2018. In contrast, Services PMI continued to contract, especially in Spain (39.7). The Economic Sentiment Index rose 2.7 points to 90.4 in December. This was driven by higher confidence in the industry sector. Consumer Confidence Index improved from -17.6 in November to -13.9 December, but remained below the pre-crisis path. In the labour market, unemployment rate slightly changed from 7.3% in Feb-20 to 8.3% in Nov-20. In addition, the number of short-time workers fell in 4Q20. These show government support has been able to keep the labour market stable during the pandemic.

Health and economic risks could derail recovery and cap growth

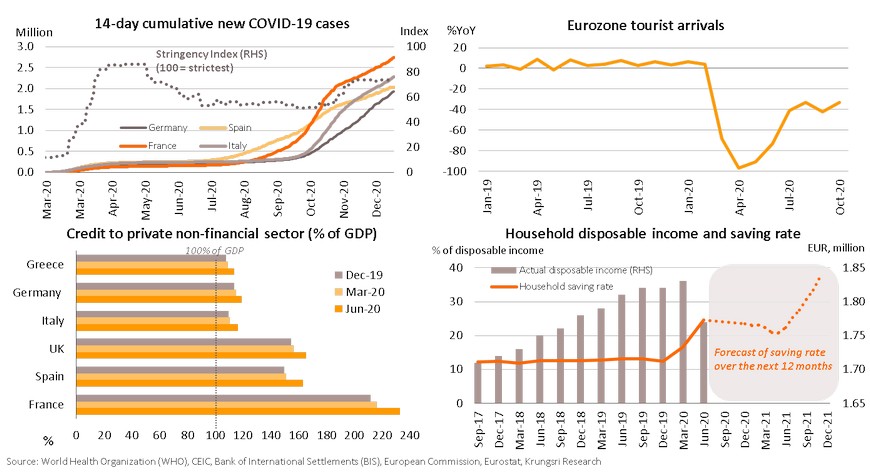

Surging COVID-19 cases and discovery of mutant strains are weighing heavily on the economy. The Stringency Index rose to 73 in December from 54 in November, reflecting the renewed national lockdown to contain the latest outbreak; the lockdown is expected to remain in place at least through January. The restrictions continue to dampen the tourism sector. Although the eurozone is open to international tourists, arrivals fell by 33% YoY in 4Q20, suggesting the sector continues to lose revenues, especially in southern Europe. There are also economic risks, including sharply higher debt in the private non-financial sector in 2Q20 led by France (+16.6% of GDP) and Spain (+12.5%). Rising household saving rate also post challenges to the economy. In early 2020, saving rate rose along with higher disposable income, which could help drive the economy after the outbreak, but latest surveys show household permanent savings is likely to rise. The combined risks could derail recovery and continue to cap economic growth even after the pandemic is under control.

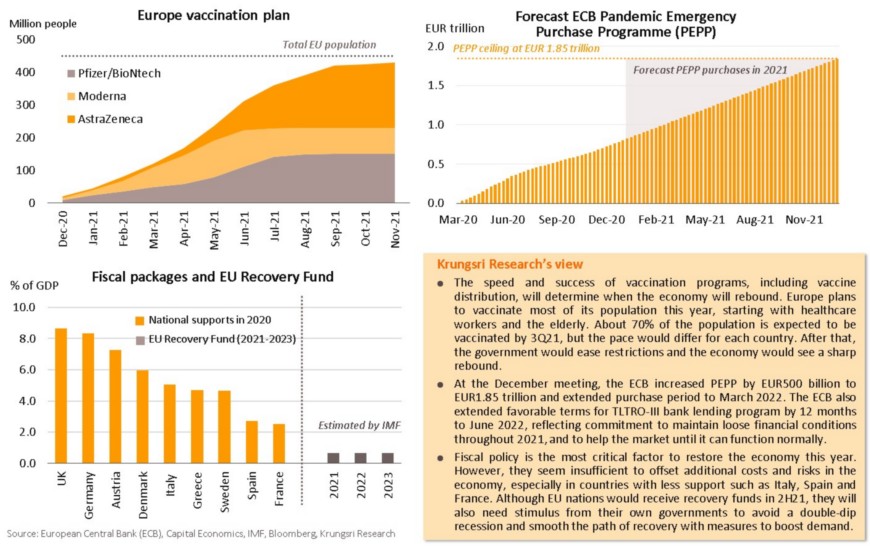

Mass vaccination delayed to late 2021, suggesting slow recovery; fiscal support is key to determine recovery path

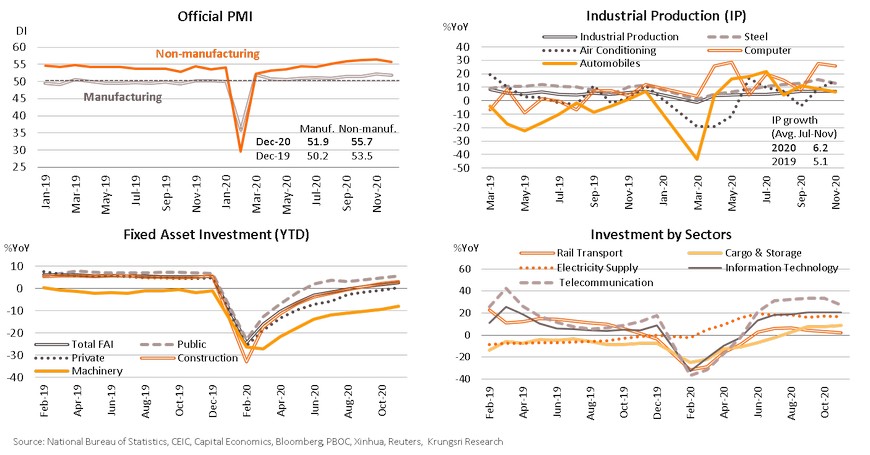

China: Robust investment and production (manufacturing and services) will accelerate recovery

The Chinese economy continues to recover, driven by robust improvements in production activities. In December, both the official Manufacturing and Non-manufacturing PMI remained above-50 for the 10th straight month. Industrial production rose at a faster pace than pre-COVID level. The cyclical recovery in China and major economies could push growth higher. On the demand side, private investment turned positive for the first time in 10 months, which could induce investment in machinery ahead. Recovery was more notable in “new infrastructure”, in line with the digital transformation. Looking forward, recovery in the non-manufacturing sectors, which are more resilient than in other countries, will boost economic activities going forward. Coupled with mass vaccination programs in China and worldwide to end the pandemic, we will see stronger broad-based recovery in China’s economy.

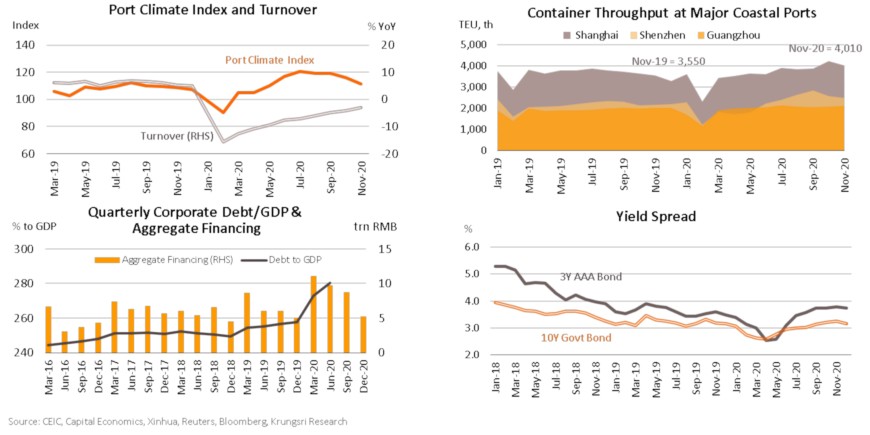

Container shortage could temporarily cap export growth; risk from high corporate debt is subsiding

The ongoing recovery in exports might see a mild hiccup because of container shortage, following a spike in demand for Chinese exports. The shortage has pulled down the Port Climate Index for major coastal ports. Container shipping costs from China to major destinations have surged to record highs. The bottleneck worsened recently as exporters front-load shipments ahead of Chinese New Year festivities. However, container manufacturers in China, which account for 96% of global output, have increased capacity to cope with the spike in demand. Indeed, port turnover has been rising along with higher container throughput. In December, exports grew 18.1%, rising for the seventh straight month. The shortage is expected to be temporary, after the Chinese New Year rush tapers off. Another risk to the economy is corporate sector debt which had reached 272.7% of GDP in 1H20. However, that risk has been subsiding since PBOC introduced more prudent measures, which reined-in broad credit. Corporate credit spread over benchmark government bond yield is stable. Defaults in corporate bonds remain small relative to the total market size. The PBOC is also monitoring the real estate sector to prevent a bubble.

With effective vaccine distribution and policy support, the economy will be more resilient to risks

China is leading ahead of major economies in mass vaccination, on expectations that would end the pandemic soon. China plans to inoculate 50 million citizens by the Lunar New Year in mid-February and increase national vaccine production capacity to 3 billion doses per year and vaccinate at least 700 million Chinese residents, about half the national population, by end-2021. In terms of supporting measures to support ongoing economic recovery, China will maintain policy direction to sustain growth through a proactive fiscal policy and accommodative but prudent monetary policy. The priority for fiscal measures is to boost domestic demand by stimulating infrastructure investment and household consumption. The government also supports SMEs with measures to ease tax and loan repayment burden, which could allow small firms to upgrade to innovative production technology. Meanwhile, the PBOC will continue with monetary easing to support demand-side recovery, especially by providing liquidity to help SMEs and local firms. On long-term economic reform, the Central Economic Work Conference (CEWC) recently identified new infrastructure investment as well as supply-side structural reform that could strengthen the domestic economy under the “dual circulation” strategy. Looking forward, China can accelerate economic recovery given larger fiscal stimulus, still-accommodative monetary policy, and an effective national immunization program to restore confidence and boost overall economic activities.

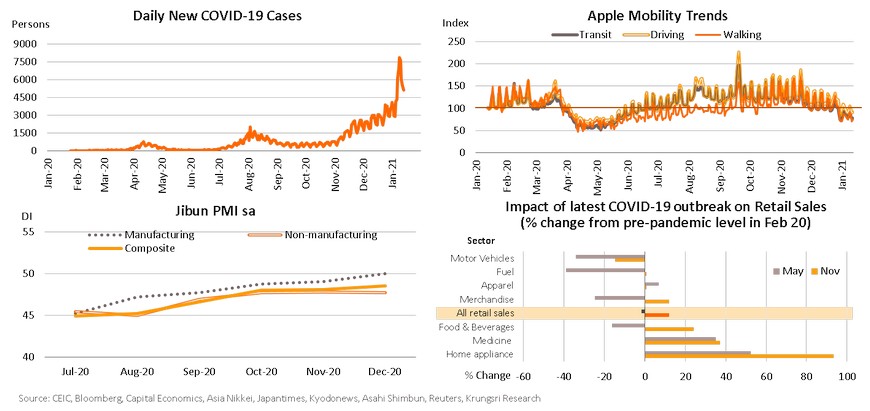

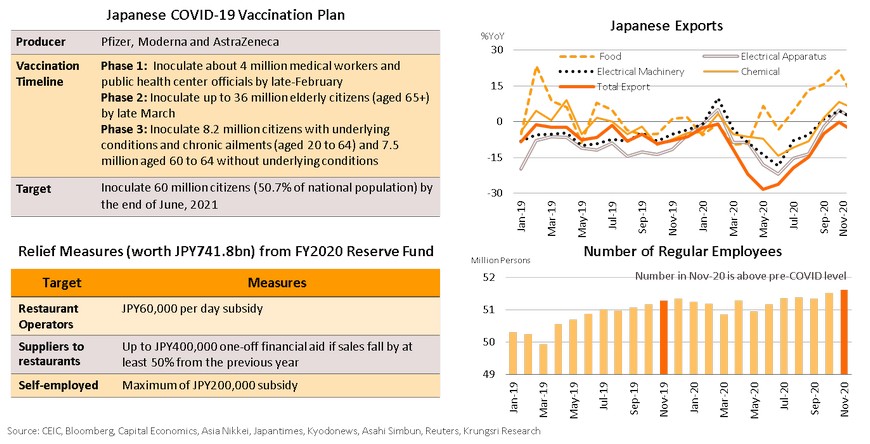

Japan: Third wave of pandemic should have limited impact on ongoing economic recovery

The third wave of COVID-19 infections has prompted the government to declare a state of emergency for the third time. Daily COVID-19 cases have hit a new-high of over 7,800, almost four times higher than the peak during the second wave in July-August. The government re-imposed a one-month state of emergency, starting from 7th January. The order covers Tokyo, Osaka and 9 other prefectures, which together account for 60% of GDP. However, the latest containment measures are less stringent, such as reducing restaurant & bar opening hours, instead of ordering businesses to close nationwide and restricting domestic travel. To address concerns, Yasutoshi Nishimura, minister in charge of Japan's coronavirus response, has said “there was no immediate plan to expand the state of emergency nationwide”. Based on indicators before the latest wave of infections, Japan’s economy had been recovering. High-frequency data up to early-January indicated economic activity had almost returned to pre-pandemic level. In December, the Composite PMI reached a 10-month high, while Manufacturing PMI returned to expansion territory for the first time since January 2019. Retail sales of merchandise, fuel and apparel had picked up, after contracting during the first state of emergency. Given stronger growth prior to the latest outbreak and less stringent lockdown measures, the resurgence of COVID-19 would have limited impact on the pace of recovery.

Additional relief measures and vaccine would soften the impact of the third wave

Although economic recovery is likely to stumble because of the third wave, the impact would be moderate in 1H21 as policy makers have pledged additional support. The government has launched the third supplementary budget for FY2020, valued at JPY21.835trn (3.9% of GDP) to help severely-hit businesses, particularly restaurant and related businesses, as well as to stimulate domestic demand. Meanwhile, the BOJ governor has pledged to expand monetary stimulus if the pandemic threatens ongoing recovery. Moreover, the latest outbreak would have limited impact because of the following: (i) restrictions are milder than before, i.e., only reduce operating hours for restaurants & bars, instead of forced closure, (ii) exports would improve led by by resilient growth of the Chinese economy, the second largest market for Japan at 19.9% to total exports, and (iii) gradual improvement of the labor market - regular wage-earning growth reached the a 9-month high in November. In 2H21, the Japanese economy would see a stronger recovery, premised on plans to immunize half the national population by June 2021, one of the most ambitious plans in the world.

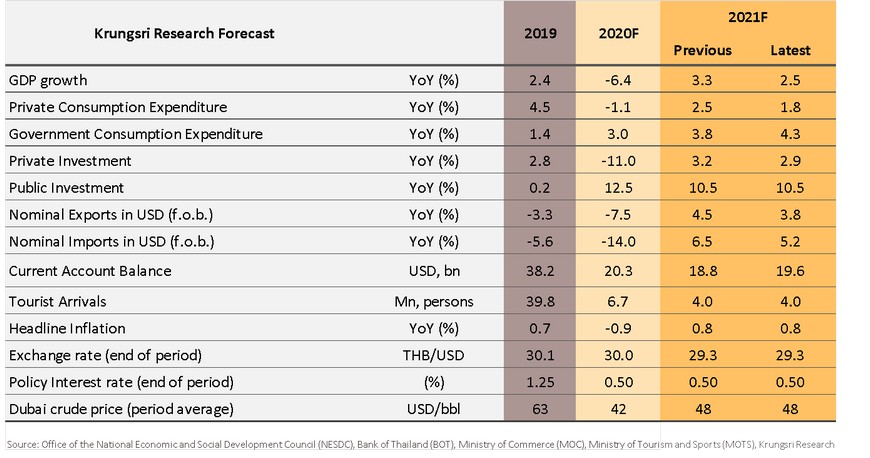

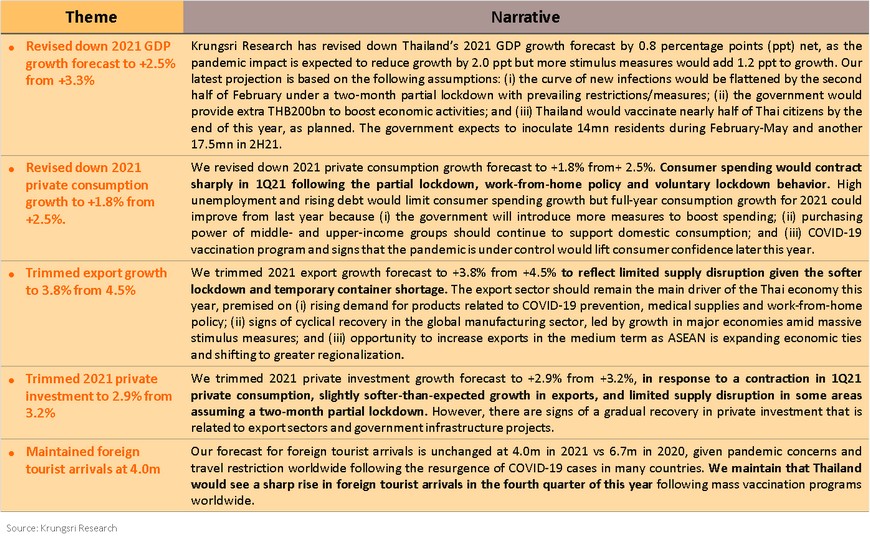

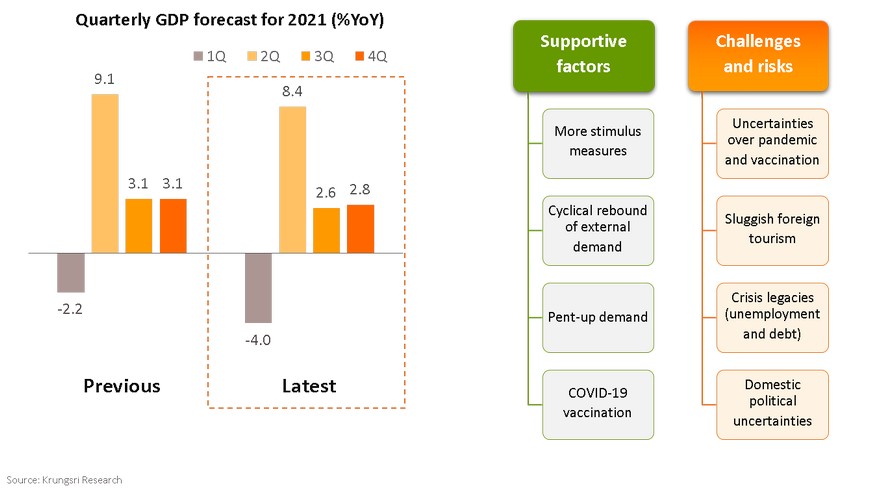

Thailand: Krungsri Research revises down 2021 GDP growth forecast to +2.5% from +3.3%

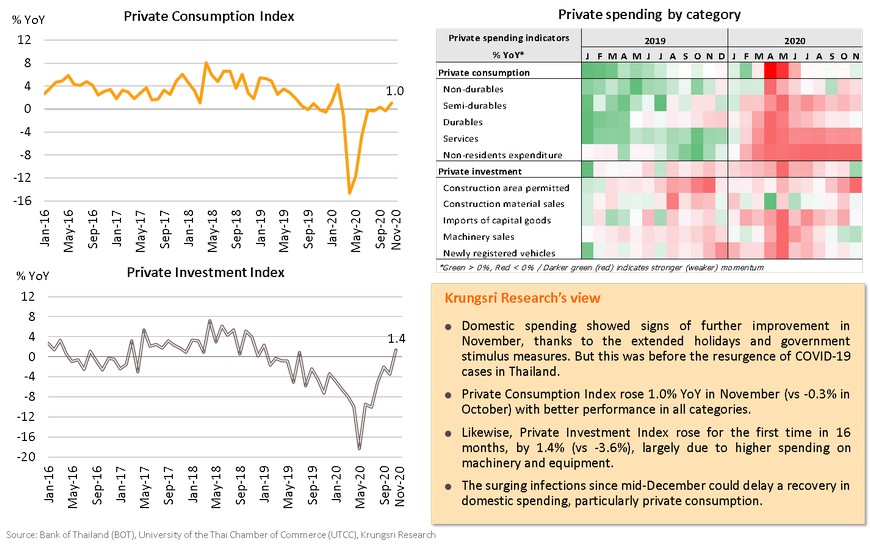

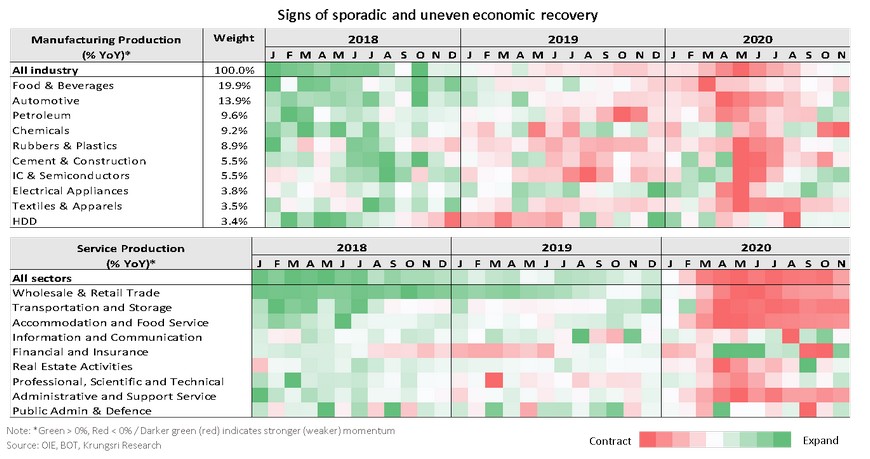

Data for late-2020 point to a positive trend but recovery is stumbling following latest COVID-19 outbreak

- Domestic spending improved in November, thanks to the extended holidays and government stimulus measures. Private Consumption Index rose by 1.0% YoY (vs -0.3% in October). Likewise, Private Investment Index rose for the first time in 16 months (+1.4% vs -3.6%). In addition, the recovery of demand in trading partners’ economies eased the contraction in Thai goods exports. However, there are signs recovery is stumbling following the resurgence in COVID-19 cases since mid-December, with the Consumer Confidence Index and Business Sentiment Index falling in December.

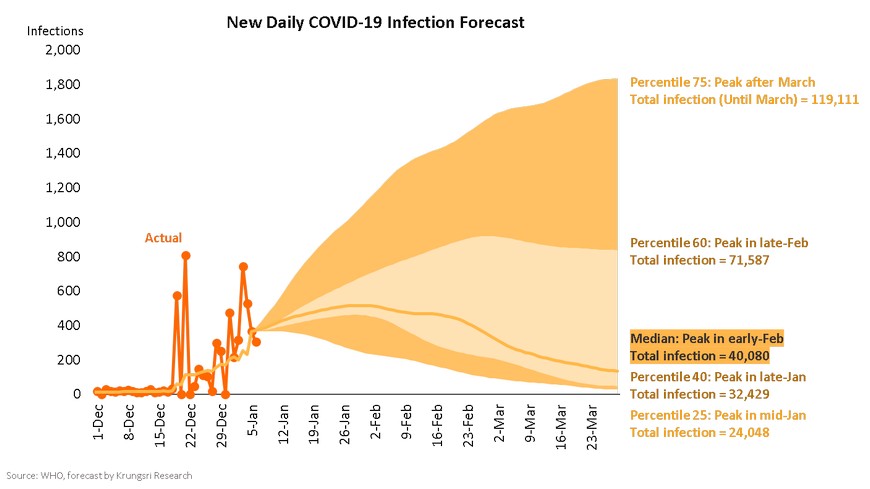

Our model suggests the latest wave would peak in early February

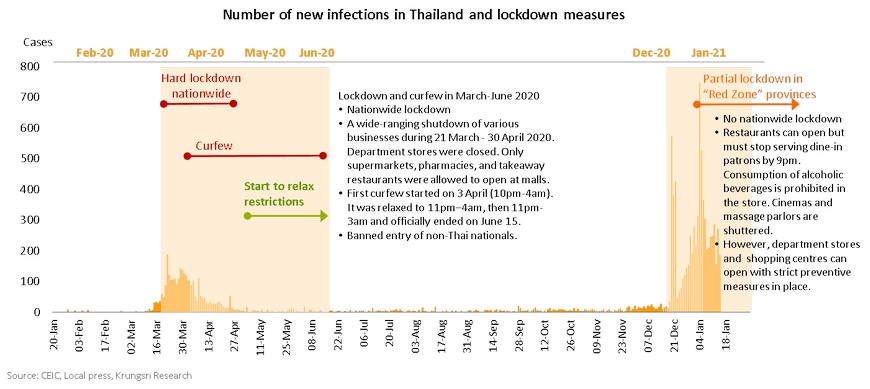

- After a half year of calm, the total number of COVID-19 cases in Thailand have skyrocketed by more than 5,000 since mid-December to over 10,000 in early January. The virus has been spreading much faster than during the initial outbreak in March-April last year. Based on latest coronavirus data, Krungsri Research’s model suggests the median forecast for domestic infections would peak in early February and the curve would flatten in the second half of the month. Hence, the partial lockdown in red-zone provinces could be extended to end-February.

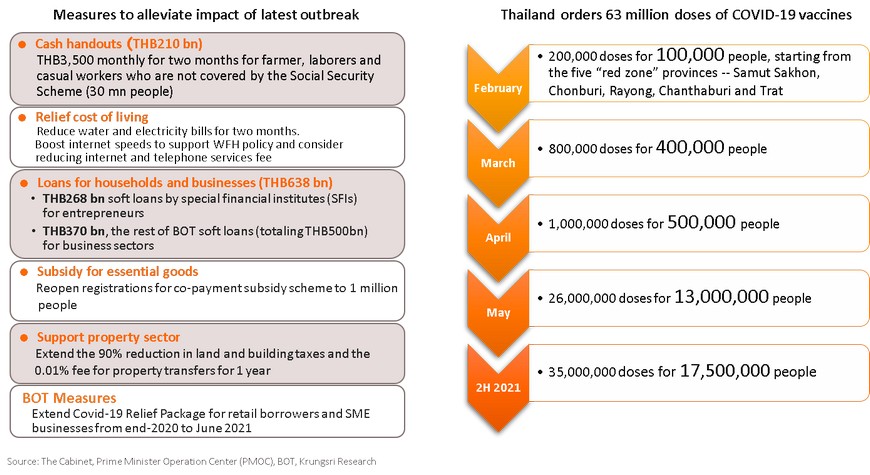

After imputing two-month partial lockdown and more stimulus, we reduced 2021 GDP growth forecast by 0.8 ppt to +2.5%

- Krungsri Research has revised down Thailand’s 2021 GDP growth forecast by 0.8 percentage points (ppt) net, as the pandemic impact is expected to reduce growth by 2.0 ppt but more stimulus measures would add 1.2 ppt to growth. Our latest projection is based on the following assumptions: (i) the curve of new infections would be flattened by the second half of February under a two-month partial lockdown with prevailing restrictions/measures; (ii) the government would provide extra THB200bn to boost economic activities; and (iii) Thailand would vaccinate nearly half of Thai citizens by the end of this year, as planned.

To support the sporadic recovery, fiscal measures and targeted monetary easing would be more appropriate than rate cuts

- The MPC is likely to maintain policy rate at a record low of 0.50% for the following reasons. First, further rate cuts are unlikely to help several affected groups such as small businesses, the self-employed, and low-income earners. Second, since the economic recovery would be uneven and sporadic across economic sectors and areas, fiscal stimulus and targeted monetary easing would be more appropriate to support the recovery than policy rate cuts. This is based on our median forecast for domestic infections. Yet, the distribution in our infection forecast reflects extreme uncertainties surrounding the COVID-19 pandemic and exhibits an upward skew in cases. Hence, we do not rule out rate cuts if the latest outbreak is not contained quickly.

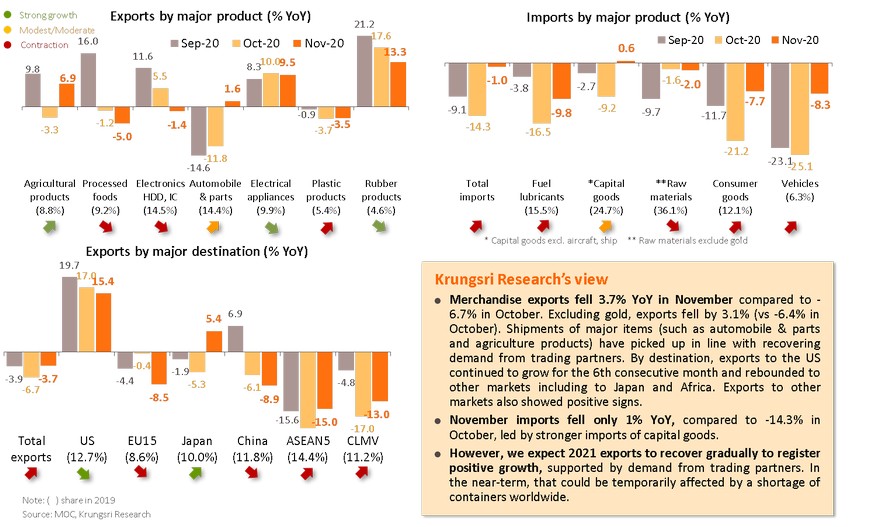

In late 2020, domestic consumption and investment rose year-on-year, before the resurgence of COVID-19

Thai export contraction has been easing, and imports of capital goods rose for first time in several months

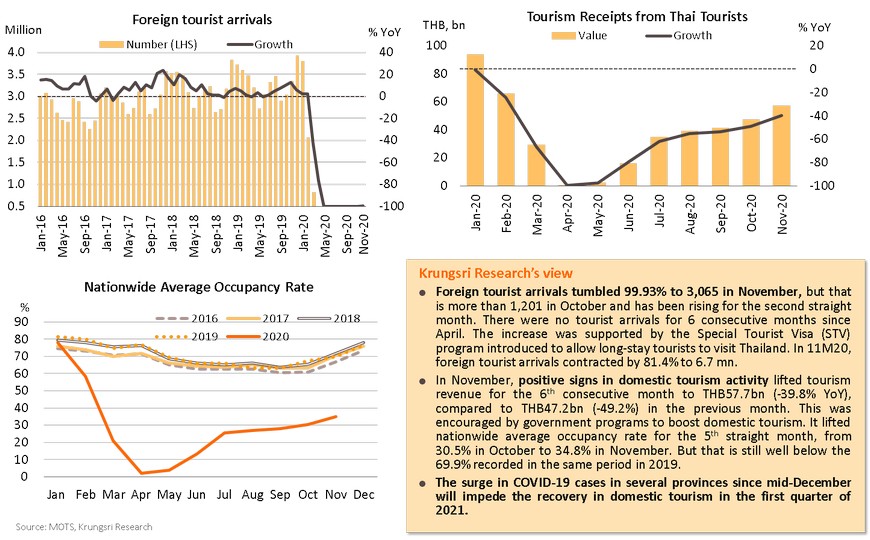

Foreign tourist arrivals still near-zero despite more applications for Special Tourist Visa (STV)

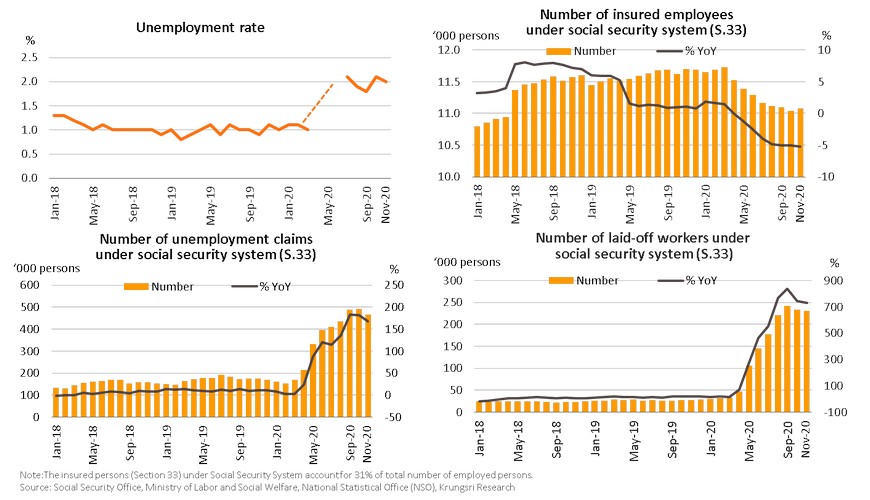

Labor market has been stable since late-2020 but is at risk again following latest outbreak

The National Statistic Office reported that unemployment rate had stabilized at 2.0% in November (vs 2.1% in October) but remained higher than 1.0% in 2019. The number of employees insured under Section 33 contracted for the 7th straight month, by 5.3% YoY to 11.1 mn in November. The number of lay-offs remained high at 231,370 (+730% YoY), as well as jobless claims at 465,465 (+168% YoY). Although the labor market seemed stable in 4Q20, the latest outbreak could rein in the recovery in the labor market.

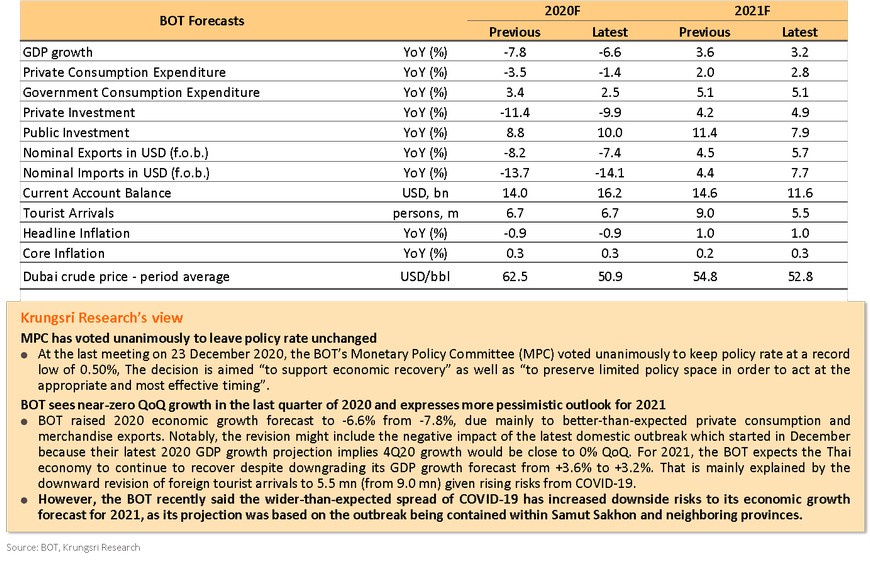

BOT sees downside risk to its forecasts following latest outbreak

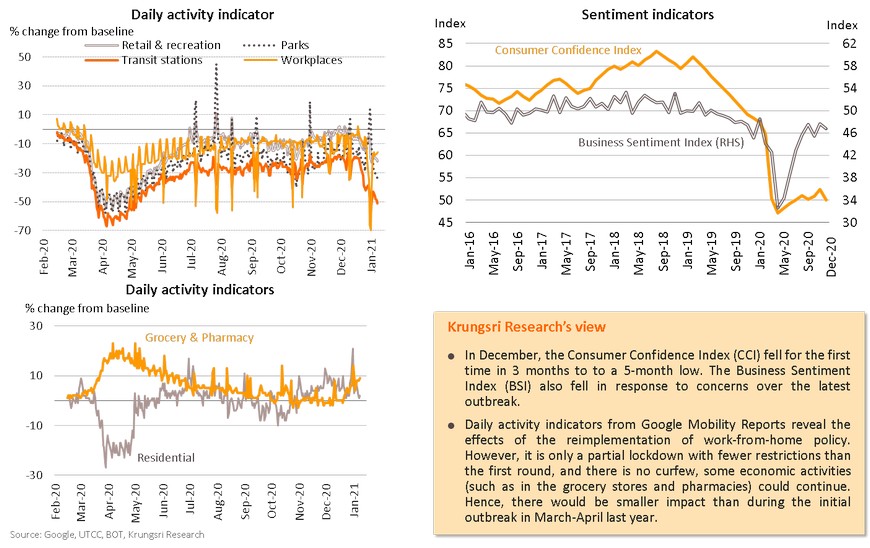

Latest domestic outbreak which started in mid-December will hurt confidence and some economic activities

COVID-19 situation: Our model suggests latest outbreak would peak in early February

After a half year of calm, the total number of COVID-19 cases in Thailand have skyrocketed by more than 5,000 since mid-December to over 10,000 in early January. The virus has been spreading much faster than during the initial outbreak in March-April last year. Based on the latest coronavirus data, Krungsri Research’s model suggests the median forecast for domestic infections would peak in early February and the curve would flatten in the second half of the month. Hence, the partial lockdown in red-zone provinces could be extended to end-February.

We trim 2021 GDP growth forecast by 0.8 ppt to +2.5%, based on two-month partial lockdown and more stimulus

Krungsri Research has revised down Thailand’s 2021 GDP growth forecast by 0.8 percentage points (ppt) net, as the pandemic impact is expected to reduce growth by 2.0 ppt but more stimulus measures would add 1.2 ppt to growth. Our latest projection is based on the following assumptions: (i) the curve of new infections would be flattened by the second half of February under a two-month partial lockdown with prevailing restrictions/measures; (ii) the government would provide extra THB200bn to boost economic activities; and (iii) Thailand would vaccinate nearly half of Thai citizens by the end of this year, as planned. The government expects to inoculate 14mn residents during February-May and another 17.5mn in 2H21.

Thailand Economic Outlook 2021

Key revision

2021 supply disruption and demand shock would be less severe than during the initial outbreak last year

The latest COVID-19 outbreak will delay Thailand’s economic recovery. 1Q21 GDP is projected to contract by 4.0% YoY instead of -2.2% YoY. But despite higher numbers this round, the economic impact would be smaller than during the first wave (2Q20 GDP -12.1% YoY) for the following reasons: (i) the government is expected to impose only partial lockdown in certain provinces and no curfew, compared to the hard lockdown with curfews during April to mid-June last year. This suggests less severe disruption to domestic supply chains and demand shock this year; (ii) there is also less severe disruption to worldwide supply chains than last year; and (iii) given the above reasons, the negative income effect (or multiplier effect) should be smaller than last year.

Economic recovery will be patchy this year given challenges ahead

Looking forward, Thailand’s economic growth (year-on-year basis) is expected to turn positive from 2Q21, and would be slightly slower than our previous forecast. This would be supported by not only the low-base effect last year but also more stimulus measures, rising pent-up demand, COVID-19 vaccination program, improving domestic tourism, and a cyclical rebound in external demand. However, economic recovery will be patchy given challenges ahead, including uncertainties over the pandemic and vaccination, weak inbound tourism, high unemployment and rising debt, as well as domestic political uncertainties.

Fiscal measures and targeted monetary easing are more appropriate than rate cuts, to support sporadic recovery

Although we have revised down our economic growth forecast for this year, the MPC is likely to keep policy rate at a record low of 0.50% for the following reasons. First, as parts of the Thai economy continue to recover, there would be no need for broad-based monetary easing (or further rate cuts). Rate cuts are unlikely to help several affected groups such as small businesses, the self-employed, and low-income earners. Second, since the economic recovery would be uneven and sporadic across economic sectors and areas, fiscal stimulus and targeted monetary easing would be more appropriate to support the recovery than policy rate cuts. Our latest view is based on the median forecast for domestic infections. Yet, the distribution in our infection forecast reflects extreme uncertainties surrounding the COVID-19 pandemic and exhibits an upward skew in cases. Hence, we do not rule out rate cuts if the latest outbreak is not contained quickly; that would generate “broad” negative impact on the overall economy via severe supply disruption and demand shock nationwide.

Regional Economic and Policy Developments in January

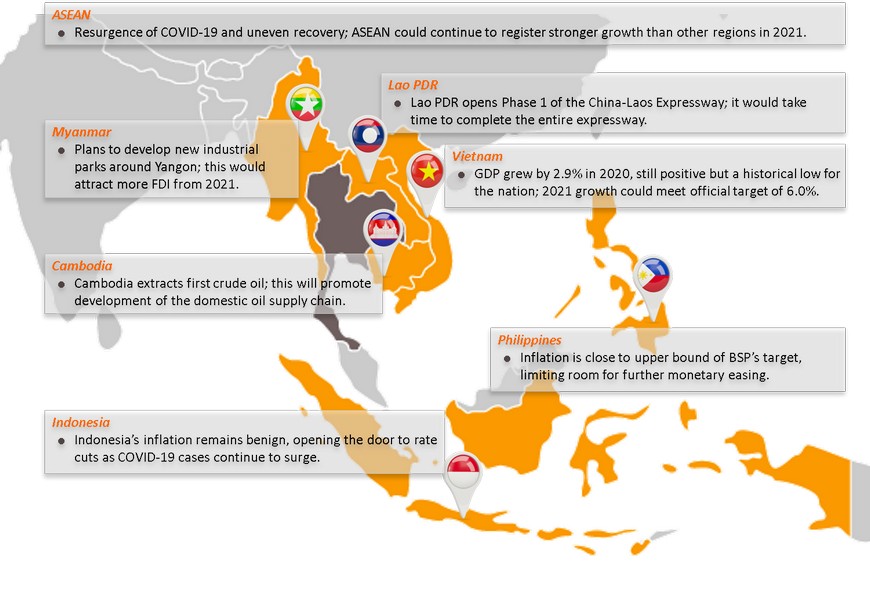

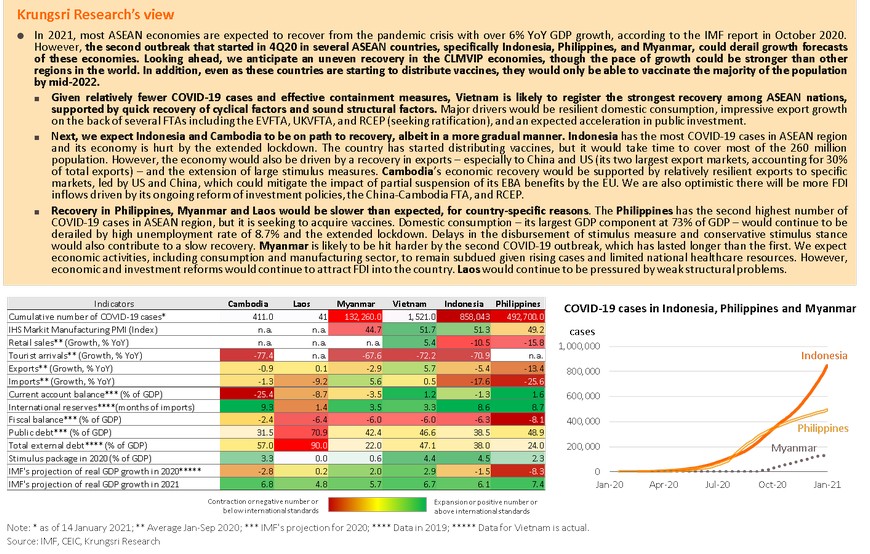

ASEAN: Resurgence of COVID-19 and uneven recovery; continue to see stronger growth than other regions in 2021

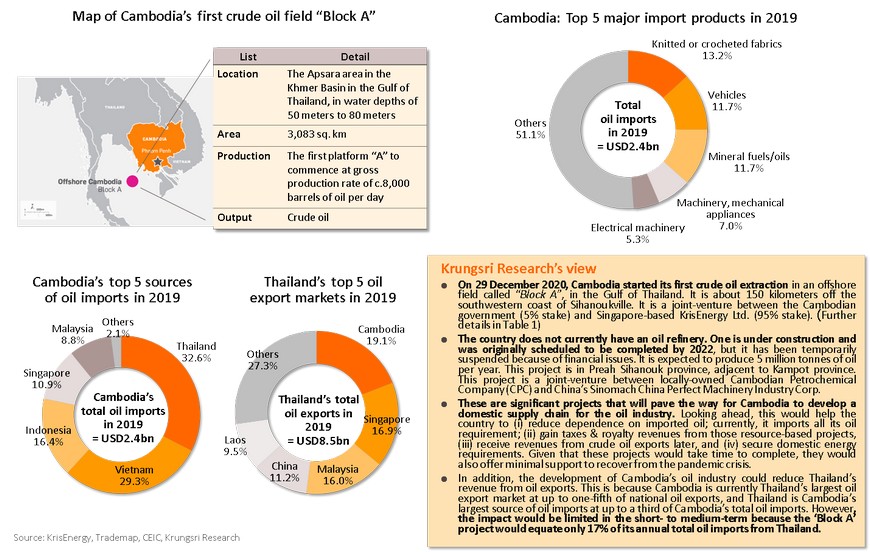

Cambodia extracts first crude; this will promote development of the domestic oil supply chain

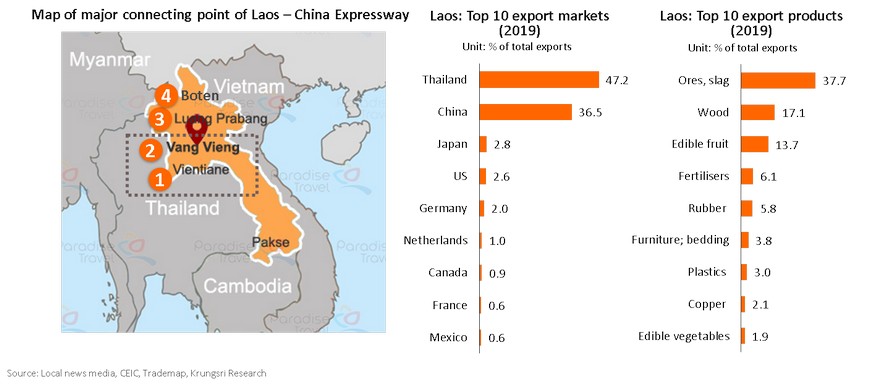

Lao PDR opens Phase 1 of the China-Laos Expressway, but it will take time to complete entire expressway

- On 20 December 2020, Laos opened the Vientiane-Vang Vieng Expressway, linking Vientiane – the country’s capital – and Vang Vieng – one of its most famous tourist destination. The project would reduce land travel time from 3.5 hours to about 1 hour. This is part of the China-Laos Expressway that will start from Vientiane and end at the Laos-China border town of Boten, a 440 km journey that would take about 5 hours. The expressway will operate under the Build-Operate-Transfer (BOT) contract with a 50-year concession.

- We estimate this would help Laos to transition from a land-locked to land-linked country. The expressway would not only expand its road network but also shorten travel time. It will further improve efficiency and competitiveness in the country’s transportation infrastructure. Specifically, it would promote its bilateral trade with China – its second largest export market – through the northern region. Target items include agriculture products, wood & wooden products, and other resources. However, it would be at least 3 years before Laos can enjoy the full benefits, because other sections of the expressway have yet to be constructed.

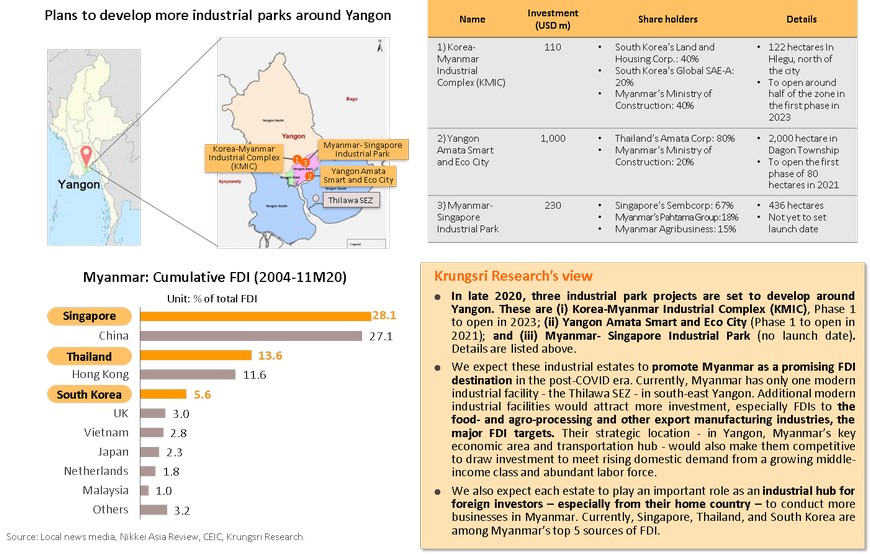

Myanmar plans to develop new industrial parks around Yangon; this would attract more FDI from 2021

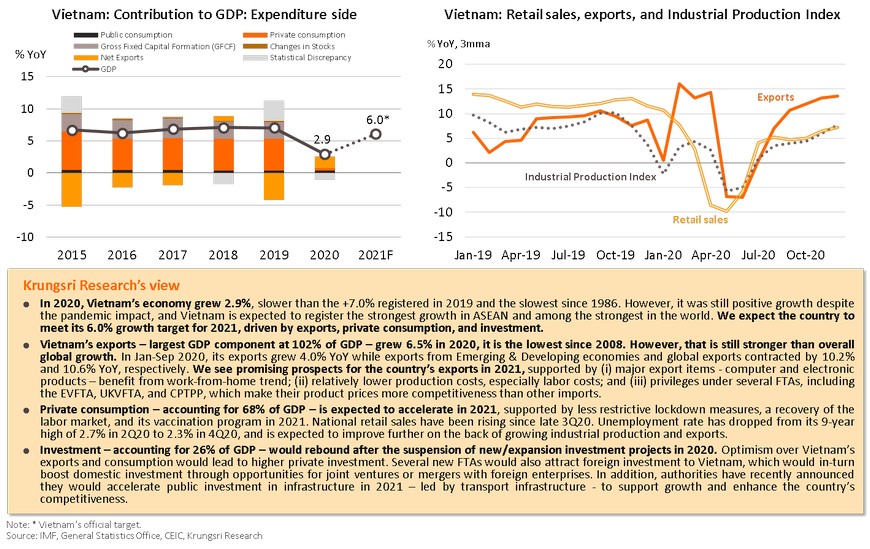

Vietnam’s GDP grew 2.9% in 2020, still positive but a new low; 2021 growth could reach official target of 6.0%

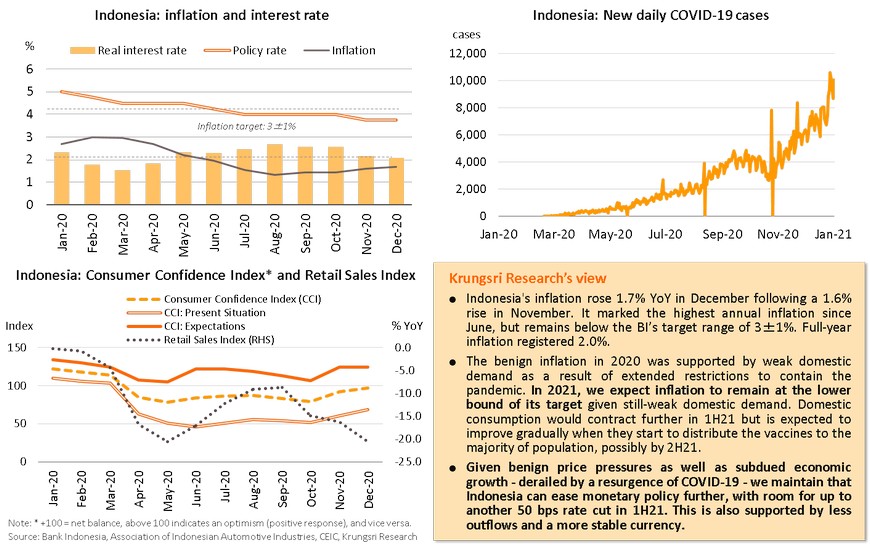

Indonesia’s inflation remains benign, opening the door to rate cuts amid surging COVID-19 cases

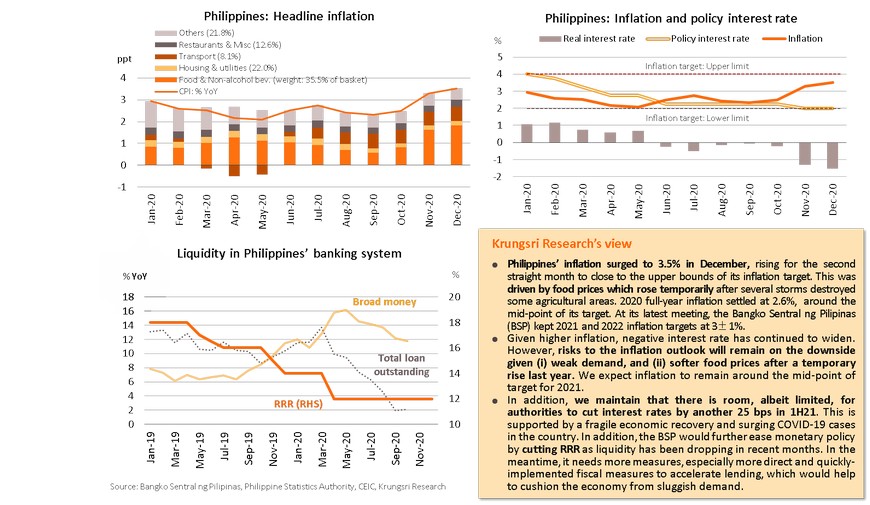

Philippines’ inflation is close to upper bound of BSP’s target, limiting room for more monetary easing