Introduction

Virtual banks are a new form of commercial bank that operates entirely through digital channels, with business structures built fully on digital systems. Their key advantage lies in lower average operating costs compared to traditional banks, allowing them to offer more competitive products and services. Virtual banks have already launched in many countries around the world, although only a few have managed to achieve profitability. In Thailand, the Ministry of Finance and the Bank of Thailand (BoT) have announced three licensees authorized to establish virtual banks, which are expected to begin operations by mid-2026, marking the country’s entry into this growing global trend.

According to Krungsri Research, Thailand is well-positioned to support this new type of bank. In the first two years, these digital-only banks are likely to focus on expanding their customer base through various strategies, before later diversifying their services to differentiate themselves and generate new revenue streams. However, virtual banks still face major challenges in achieving sustainable growth, such as intense competition with existing players and regulatory constraints.

Although the emergence of virtual banks is unlikely to severely disrupt traditional commercial banks, it will increase market competition in the early stages. Therefore, existing banks should proactively adapt by developing products and services that better meet customer needs, to maintain their competitiveness in a rapidly changing financial landscape.

The Rise of Virtual Banks

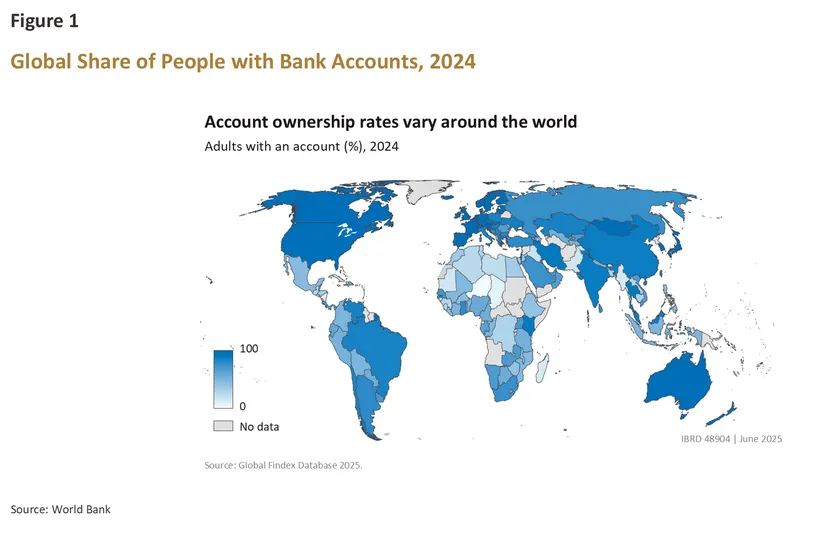

Since the outbreak of COVID-19 in 2020, financial institutions worldwide have accelerated their digital transformation, particularly in service channels that allow customers to access banking services online. However, according to the World Bank,

1/ as of 2024, 21% of the global population still does not have a bank account,2/ which limits their access to financial services. This is especially true for people living in remote areas, low-income groups, and self-employed individuals, who often face difficulties traveling to bank branches or lack sufficient financial documentation. As a result, the concept of “virtual banks” has gained increasing attention as a new alternative for expanding financial inclusion to all segments of society.

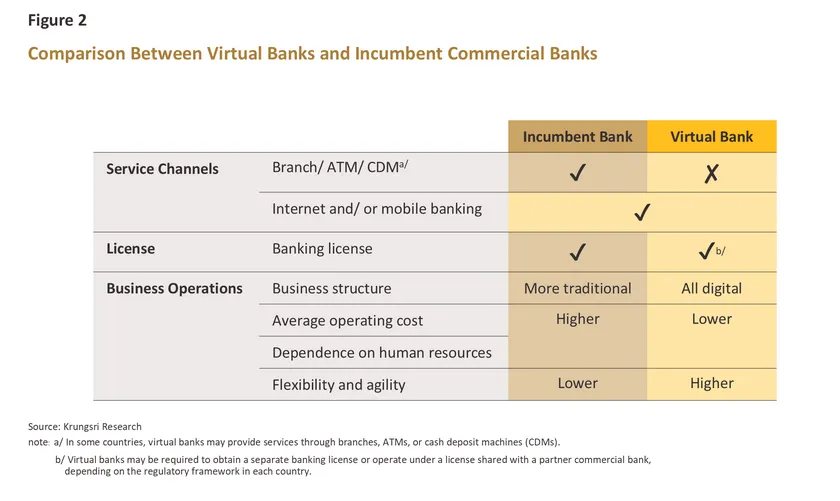

According to the Bank of Thailand (BoT), a virtual bank is a new type of commercial bank that provides financial services—such as opening deposit accounts, applying for loans, and accessing other banking services—entirely through digital channels, without operating its own branches, ATMs, or cash deposit machines (CDMs).3/

Virtual banks are known by different names in various countries, including “virtual bank,” “neobank,” “digital bank,” “challenger bank,” or “internet-only bank,” and are subject to different regulatory frameworks. In some countries, virtual banks must obtain a full banking license just like traditional commercial banks and may also face additional requirements specific to branchless banking. In other countries, virtual banks can operate under a banking license shared with a partner commercial bank. Many virtual banks also originate from financial technology (FinTech) companies or large tech firms. They often start by providing payment, lending, or other financial services and later expand into offering a full suite of banking services.

Key Advantages of Virtual Banks

Virtual banks offer several advantages compared to traditional commercial banks, including lower costs, attractive products, operational efficiency, and easier customer access:

-

Lower operating costs: Virtual banks do not need to invest in physical branches or hire large numbers of staff, allowing them to manage expenses more efficiently.

-

Ability to offer attractive products: The lower operating costs enable virtual banks to design products with higher returns or lower fees, such as offering higher deposit interest rates than traditional banks or reducing or waiving transaction fees.

-

Flexible and agile business structure: Built entirely on digital systems, virtual banks can quickly scale operations according to market conditions and develop innovative products at a faster pace.

-

Convenient access for customers: Customers can access services anytime and anywhere via smartphone apps or online channels, without needing to visit a physical branch.

The International Landscape of Virtual Banks

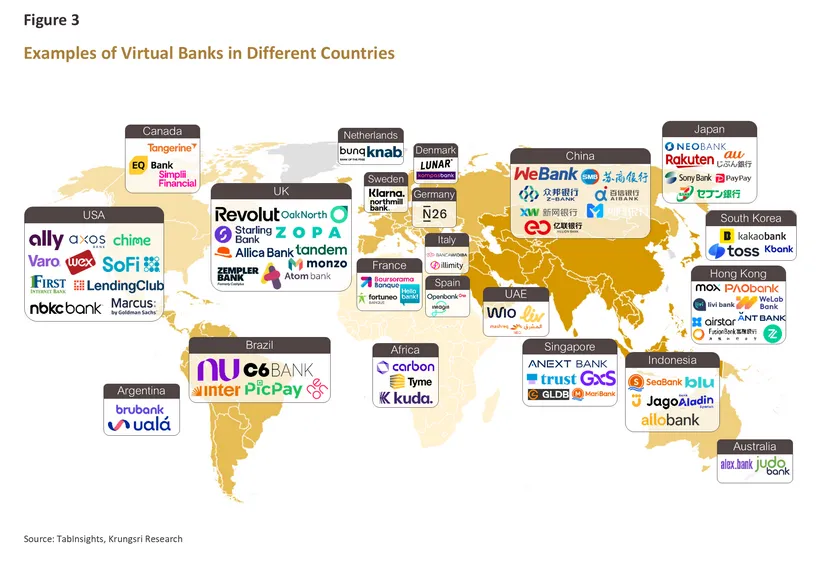

Today, virtual banks are present on every continent, including Europe, the Americas, Africa, Asia, and Oceania. They are particularly numerous in Europe and North America, supported by several factors such as regulatory frameworks that encourage growth and enable competition with traditional banks, widespread internet infrastructure, large populations, and consumers who are familiar with digital financial services. These factors have contributed to the steady growth of virtual banks worldwide in terms of user numbers, assets, and revenue.

However, despite an increasing number of profitable providers and shorter average payback periods, only one in four virtual banks globally is currently profitable.4/ The reasons behind this will be discussed in the next section.

United Kingdom

The United Kingdom and the European Union are considered key global hubs for virtual banking innovation. In the UK, financial regulators5/ view virtual banks—also known as “new banks”—as drivers of innovation in the financial sector. From 2013 to September 1, 2025, the UK has issued licenses to 41 new banks,6/ many of which began as fintech companies before obtaining full banking licenses.

A notable example is Revolut, founded in 2015, which started by offering debit cards for international payments without fees. Revolut’s core strategy has been to expand its customer base globally, and it now serves over 60 million individual customers and supports transactions in more than 36 currencies. Other leading players include OakNorth Bank, which focuses on serving SMEs and began expanding into the U.S. in 2024. Banks that have recently started turning a profit include Zopa, Allica, Monzo, and Atom.

European Union

In the European Union, virtual banks are regulated under the same legal framework as traditional commercial banks. Their strategies often share a common goal: expanding services to other member states in order to reach a broader customer base. This is facilitated by the Single Authorization system, which allows a financial institution licensed in one member state to operate in other member states without obtaining additional licenses. Another key factor is the PSD2 regulation,7/ which enables the sharing of customer data between banks and third-party providers through Open Banking, fostering further financial innovation across Europe.

A common feature of virtual banks in the EU is their product offerings. Many provide multi-currency deposit accounts or debit cards, and several adopt a subscription-based business model similar to other digital services. They offer tiered packages, with higher-level plans providing additional benefits, such as waived ATM withdrawal fees, free travel insurance, or the ability to open supplementary accounts for children.

Leading virtual banks in the EU originate from a variety of member states. For example, the Netherlands is home to bunq, which targets tech-savvy customers and digital nomads. Germany’s N26 has also been notable, and in May 2025, it expanded into the telecommunications market by launching flexible, affordable eSIM services in partnership with Vodafone. These initiatives illustrate how virtual banks differentiate themselves through partnerships and innovative products after years of operation.

United States

In the United States, virtual banks are regulated under the same legal framework as traditional commercial banks, similar to the UK and the European Union. However, due to the strict regulatory environment, some providers that are not bank subsidiaries must operate as fintech companies and rely on banking licenses held by partner financial institutions.

Leading examples include Chime, founded in 2012, which currently serves around 8.6 million users8/ and plans to go public in 2025. Varo is the first fully licensed virtual bank in the U.S., offering comprehensive services with notable features such as high-yield savings accounts and tax filing through its banking app. Other significant providers include Ally, Axos, and SoFi. Despite these successes, most virtual banks in the U.S. still face challenges in achieving sustainable profitability.

Latin America and South America

South America is another market where virtual banks are growing rapidly, both in terms of user numbers and transaction volume. This growth is driven by a large young population and a high proportion of unbanked individuals.

Leading providers are mainly concentrated in Brazil, Argentina, and Mexico. Nubank, founded in 2014 in Brazil, currently serves over 120 million customers across Brazil, Mexico, and Colombia,9/ with plans to expand into the United States. Other notable Brazilian providers include Banco Inter, C6 Bank, PicPay, and Neon. In neighboring countries, prominent players include Uala in Argentina and Albo in Mexico.

These providers focus on strategies that promote financial inclusion, while also expanding their services, such as offering multi-currency accounts, eSIM services, and AI-driven personalized banking experiences. However, virtual banks in South America still face challenges from volatile economic conditions, high inflation, and strict regulatory requirements, especially when expanding operations abroad.

Asia-Pacific

The Asia-Pacific region is another key market for virtual banks and has a history almost as long as Europe or the Americas. Some of the region’s earliest virtual banks were established in Japan, such as Rakuten Bank and Sony Bank, founded in 2001 as internet-only banks, which were more similar to traditional banks than the fully-digital virtual banks of today.

Overall, virtual banks in Asia differ from those in other regions in terms of regulatory frameworks and business models. Financial regulators in many countries issue licenses specifically for virtual banks and set rules to manage operational and financial risks. For example, the Monetary Authority of Singapore (MAS) classifies virtual bank licenses into two types based on the bank’s target customer segment.10/ It also sets initial deposit caps for individual customers, which can be lifted once the bank demonstrates operational stability and effective risk management.

Several countries in the region also limit the number of virtual banking licenses to maintain financial-system stability. Hong Kong, South Korea, Singapore, and Malaysia, for example, either cap the total number of licenses in advance or restrict participation to institutions that meet certain capital and technology requirements.

A highly successful business model in the region links virtual banks with digital platforms that already have large user bases. This approach allows banks to reach break-even points faster than conventional models. For example, KakaoBank in South Korea, founded in 2016 and licensed in 2017, integrates banking services into KakaoTalk, a popular messaging app from the same company, allowing users to conduct transactions on a familiar platform and quickly become the primary bank for many customers. Similarly, WeBank, Tencent’s virtual bank in China, connects its services to WeChat, China’s leading messaging and payment app, creating a comprehensive ecosystem for over 400 million users.11/ WeBank has also developed AI technology to assess loans using alternative data, such as payment behavior, enabling greater access to credit for freelancers and small SMEs.

Thailand’s Journey Toward Virtual Banking

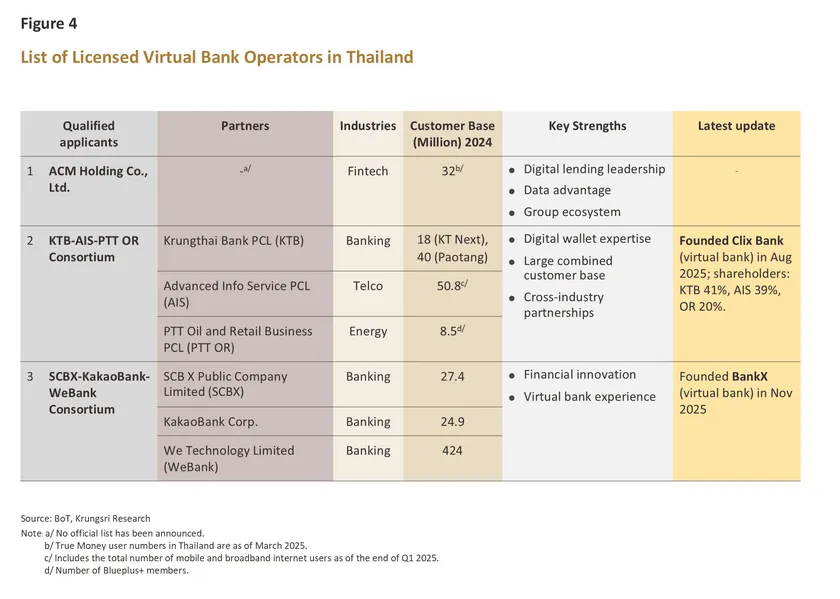

The Bank of Thailand (BoT) has been studying the feasibility of establishing virtual banks for several years. In 2024, the BoT officially opened applications for interested parties to apply for a license to operate. Initially, the number of licenses was limited to three, as this was considered sufficient to stimulate healthy competition without posing risks to financial system stability, while also ensuring effective regulatory oversight.

12/

The BoT has outlined three key objectives for virtual banks in Thailand:

13/ (1) Providing financial services that meet the needs of different customer segments, particularly underserved and unserved groups—such as retail customers and small and medium-sized enterprises (SMEs)—who currently lack adequate access to suitable financial products; (2) Enhancing customer experience in accessing and using financial services; and (3) Fostering appropriate competition within the financial system.

In June 2025, the Ministry of Finance and the BoT announced the three licensees authorized to establish virtual banks, all of which are required to set up their operations and begin offering services within one year. The approved groups are: (1) ACM Holding Co., Ltd.; (2) Krungthai Bank Group, in partnership with Advanced Info Service (AIS) and PTT Oil and Retail Business (OR); and (3) SCBX Group, in partnership with WeTechnology Limited and KakaoBank Corp. All three licensees are joint ventures combining the strengths of existing financial institutions with those of partners that have large customer bases, broad digital ecosystems, and advanced technological expertise—both domestic and international.

Given the unique advantages of virtual banks, traditional commercial banks in Thailand should look closely at international examples, especially in markets with similar characteristics. Doing so will help them anticipate the likely direction of business models and service innovations in Thailand and allow them to adapt proactively to the intensifying competition that is expected in the coming years.

Virtual Bank Trends in Thailand

Virtual banks in each region have developed and evolved in different directions, influenced by various factors such as

regional characteristics — particularly customer needs, infrastructure readiness, and financial regulations — as well as

the business models of service providers, including their competitiveness, ability to diversify revenue streams, and capacity to develop and adopt technology to support operations.

By comparing these international factors with the fundamental characteristics of Thailand’s financial services market and the potential of the license holders, Krungsri Research projects the outlook for virtual banks in Thailand, which are expected to commence operations around mid-2026, as follows:

Infrastructure and Adoption

Thailand is well-positioned to embrace the rise of virtual banking, supported by its robust and extensive digital infrastructure. As of the end of 2024, around 90% of the adult population owned a smartphone,

14/ and approximately 61 million people, or 92% of the population, were internet users.

15/ Moreover,

Thais are highly familiar with digital payment services in their daily lives, as reflected by the continuously increasing number of accounts and transaction volumes in Internet and Mobile Banking each year.

16/

On the regulatory side, Thailand has a strong financial regulatory framework that fosters consumer confidence, encompassing the supervision of financial institutions, lending businesses, interest rate regulations, and the deposit protection system.

Products and Services

Overall, the products and services that virtual banks in Thailand will offer depend on several factors, including the timing of their launch, business strategies, specific customer needs, the technologies employed, and financial regulations.

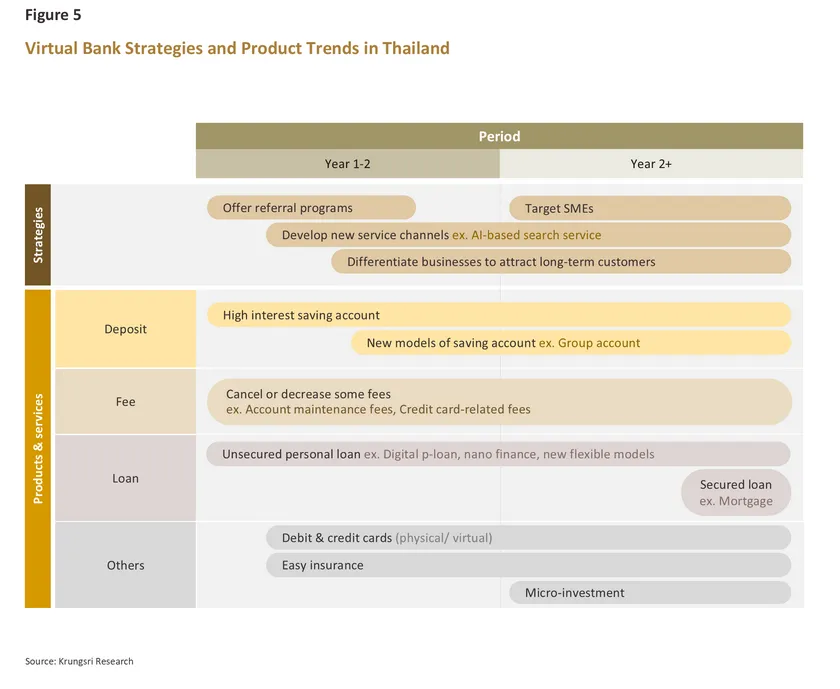

During the first 1–2 years, virtual banks are expected to focus on growing their customer base through various strategies such as offering high-interest rates for new accounts, reducing or waiving certain fees, implementing referral programs to encourage customers to bring in friends and acquaintances, and developing digital ecosystems to access partner networks’ customer bases.

At this stage, virtual banks will focus on offering simple, easy-to-understand products, as services are delivered through digital platforms without direct assistance from bank staff. They will primarily offer deposit products and low-limit loans, along with acting as intermediaries for non-complex insurance products, particularly travel insurance. These offerings allow virtual banks to generate revenue from the outset.

Once they accumulate sufficient capital and customer credit data—typically from the second to third year onward—they may begin expanding into additional services to diversify revenue streams and differentiate themselves from competitors. Examples include low-entry investment services, higher-limit loans with longer repayment terms for customers with good credit histories, virtual credit and debit cards, and expanded services for SME customers.

Deposits

Virtual banks are likely to offer higher interest rates on deposit accounts compared with traditional commercial banks to attract new customers. However, they may impose a cap on the deposit amount eligible for preferential rates, such as applying high interest only to the first THB 100,000—similar to the online deposit products offered by several banks today.

Furthermore, given that the license holders have experience in both domestic and international financial sectors,

Krungsri Research expects digital deposit accounts to incorporate innovative features that make account management more convenient and flexible. One interesting example is the

“group online account”, where multiple members can manage deposits and withdrawals collectively. This type of account has been highly popular in South Korea: since KakaoBank introduced it in 2018, the number of group account users has steadily grown to around 12 million accounts, accounting for 47% of all customers.

17/ This success has prompted other players, including

TossBank and

K Bank, to adopt similar offerings.

Fees

Virtual banks are expected to reduce or waive fees that traditional banks typically charge, particularly fees related to deposit accounts, such as account maintenance charges when there is no activity or when balances fall below a certain threshold. These fees can be a barrier for consumers who are unbanked.

In addition, virtual banks may lower other fees, such as debit card issuance fees, annual card fees (both physical and virtual),

and leverage partner networks to further reduce costs—for example, waiving SMS alert fees for customers on partner telecom networks, or lowering fees for cash deposits and withdrawals via banking agents affiliated with the virtual bank. While reducing or waiving certain fees may lower short-term revenue, it can help attract new customers and strengthen connections between virtual bank customers and partner ecosystems.

Loans

Lending is expected to be one of the key revenue streams for virtual banks. Considering customer demand and financial regulations in Thailand,

Krungsri Research anticipates that virtual banks will primarily offer unsecured personal loans, particularly

digital personal loans. The Bank of Thailand allows financial service providers to assess credit limits using alternative data, such as utility and phone payment histories, fuel purchases, or retail transaction behaviors. Virtual banks may also leverage machine learning to evaluate borrowers’ repayment capacity. Additionally, the

Your Data initiative will help connect alternative data from non-financial service providers with financial institutions, enabling product offerings that better meet customer needs.

Another likely loan type is

nano-finance or microloans for SMEs, providing quick liquidity and higher credit limits. To remain competitive,

these loans are expected to be easily accessible, require minimal documentation, offer fast approval, and allow 24/7 application via mobile banking apps. Initially, virtual banks may approve smaller loan amounts for first-time borrowers and gradually increase limits for customers with good repayment histories

or offer innovative loan models that provide flexibility.

For example,

CIMB Singapore launched a revenue-based loan product for micro-entrepreneurs in August 2025. Repayments are calculated as a fixed percentage (holdback rate) of daily deposits or ‘daily sales revenue,’ meaning borrowers only repay when they generate income. These loans do not charge interest or penalties for early or late repayment, while the bank earns revenue from a one-time upfront fee paid at loan approval.

Once virtual banks have established themselves or become primary banks for users, they may expand their loan offerings to cover more diverse and higher-value credit needs. For instance,

KakaoBank began offering digital home loans in July 2025, roughly eight years after its launch in 2017. These loans are fully processed through digital channels and offer lower interest rates than conventional mortgage products.

Other Products and Services

Once operations are established, virtual banks are likely to focus on diversifying revenue streams and differentiating themselves from competitors. A key strategy is to introduce

new financial products and services that better meet customer needs, especially in areas that are more complex or underpenetrated in the market, such as investment and insurance. Compared with basic daily services like deposits, transfers, payments, and unsecured loans (excluding credit cards), Thai households still have relatively low adoption of these more sophisticated financial products.

Virtual banks are expected to offer simplified versions of complex products, such as life insurance and unit-linked insurance, with plans tailored to individual customers based on alternative data, particularly transactional data on the bank’s digital platforms.

An example of an accessible investment product with a low entry point is

GXS Bank, which launched an investment service in July 2025 which claimed to

grow your savings faster, requiring a minimum investment of just 1 Singapore dollar.

In addition, virtual banks can offer

debit and credit cards, both physical and digital, for retail and corporate customers, often bundled with benefits linked to partner networks.

Customer Service

Since virtual banks cannot serve customers through physical branches like traditional banks, they must develop innovative digital customer touchpoints, often leveraging AI technology. For example,

KakaoBank launched Conversational AI Search Service in May 2025, allowing customers to ask questions about banking products and general financial knowledge in a conversational format, with answers sourced exclusively from verified bank data. KakaoBank also provides an AI Financial Calculator, helping customers compute interest on deposits, loan repayments, or foreign exchange rates, supporting more informed financial planning.

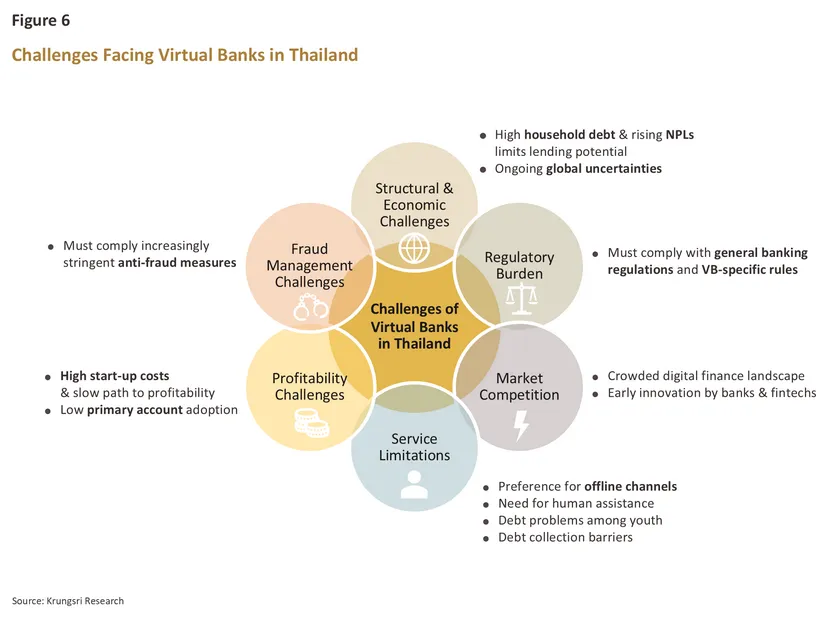

Challenges for Virtual Banks in Thailand

Even though Thailand’s traditional banking system is generally stable, virtual banks face numerous challenges in achieving long-term success. Globally, most virtual banks remain unprofitable, and in worst-case scenarios, they have had to cease operations—such as

Xinja Bank and

Volt Bank in Australia, which closed in December 2020 and June 2022, respectively, due to insufficient funding.

For Thailand, the upcoming virtual banks will confront multiple challenges:

1. Structural and macroeconomic uncertainties: Over the past several years, Thailand’s economy has faced persistent challenges, both from long-standing structural issues—particularly the high level of household debt—and from economic factors affecting trade and investment, such as U.S. trade restrictions, regional conflicts, a still-recovering business sector, and non-performing loans in both corporate and retail segments. These issues collectively have long-term impacts on the lending activities of Thai banks.

2. Stringent financial regulation: Since virtual banks in Thailand are classified as ‘financial institutions’ just like traditional commercial banks, they must comply with strict financial regulatory standards under the Financial Institution Business Act. As a result, virtual banks need to maintain stability and manage risks according to these standards, which limits their ability to rapidly expand revenue-generating operations, especially lending.

Moreover, virtual banks must follow specific regulations that may affect their competitiveness, both among themselves and compared with traditional banks. For example, they are required to provide services exclusively through digital channels, which could restrict certain types of services.

In addition, if a virtual bank operates as a subsidiary of another financial institution, it cannot rely on loans from its parent company after the grace period ends. This may create funding challenges when expanding lending or business operations. Furthermore, virtual banks cannot share deposit, loan, Internet banking, or mobile banking systems with other financial institutions domestically or internationally, meaning they must invest in developing all systems independently during the initial phase. Another key limitation is that virtual banks cannot use names, logos, or symbols similar to those of other financial institutions, which may require additional investment in branding to establish credibility and gain customer trust.

3. Intensifying digital financial competition: Today, Thailand offers a wide range of digital financial services, covering the core offerings that virtual banks typically introduce in their early stages. These include basic transactions through mobile banking, opening digital savings accounts (e-Savings) and electronic wallets (e-Wallets), and applying for digital personal loans based on alternative data. Such products allow customers to access services without visiting a physical branch, making them a direct competitor to virtual banks. In addition, traditional banks and fintech companies that do not hold a virtual banking license are also likely to roll out new services before virtual banks officially start operations, to gain an early advantage. As a result, virtual banks may face significant pressure to differentiate themselves from existing services right from the start.

4. Service limitations: While the core mission of virtual banks is to increase accessibility, they may not fully meet customer needs. According to a 2022 survey by the Bank of Thailand,18/ when it comes to basic financial services, Thai households still prefer using non-digital channels for deposits, loans,19/ and payments over digital alternatives.20/ Moreover, a significant portion of the population has yet to adopt digital financial services, particularly low-income self-employed individuals, the elderly, and residents in the northeastern and northern regions. This suggests that virtual banks, which operate exclusively through digital channels, may not effectively reach unserved or underserved segments as intended.

In addition, a 2025 survey by Accenture21/ found that when customers encounter issues they cannot resolve online, most still want to contact a bank branch. Across all age groups, branches remain symbolic of “stability” and “availability,” which remain key attributes for trusted financial service providers.

On the other hand, while younger generations have greater access to digital channels compared to the elderly, many already carry debt burdens from an early age, limiting their eligibility for loans from virtual banks or additional credit. According to a Bank of Thailand study,22/ half of first jobbers aged 22-29 already have existing debt, with some experiencing non-performing loan issues. Therefore, virtual banks may need to develop programs—particularly debt counseling and refinancing solutions23/—to help this demographic resolve their debt problems and eventually become viable customers.

Additionally, service limitations may pose challenges for debt collection. Virtual banks may need to collaborate with partners for collection activities and develop robust credit analysis systems to minimize NPL risks.

5. Achieving sustainable profitability: Virtual banks around the world often struggle to achieve profitability, even after several years of operation. A key reason is the high initial cost burden, as they must invest heavily in developing their entire system while simultaneously building credibility and attracting new customers through various promotional strategies. For instance, offering high deposit interest rates or special introductory benefits increases customer acquisition costs (CAC), directly affecting financial performance. In addition, during the early stages, limited loan portfolios—due to cautious lending—typically result in low net interest margins (NIM).

These high initial costs mean that virtual banks often operate at a loss for at least the first two years, and on average may take five to six years to reach profitability.24/ Virtual banks that cannot secure sufficient funding during this loss-making period may be forced to shut down.

Even when customer numbers increase, virtual banks in advanced markets such as the United Kingdom and Singapore face a similar challenge: customers initially open accounts to take advantage of introductory benefits, but the banks often fail to become the customer’s primary financial provider. This limits opportunities to expand services and generate sustained revenue from existing customers. Consequently, developing and offering services that encourage customers to designate the virtual bank as their main financial provider remains a crucial challenge for virtual banks in Thailand.

6. Managing financial fraud and cybercrime: Fraud, technology-related crimes, and mule accounts remain major challenges for Thailand’s financial sector. In recent years, the Cybercrime Prevention and Suppression Operation Center has worked closely with the Bank of Thailand (BoT), the Anti-Money Laundering Office (AMLO), the Cyber Crime Investigation Bureau, and financial institutions to continuously strengthen measures to address these issues.

Key measures25/ that directly impact financial institutions include: (1) Managing mule accounts by screening for risk and freezing suspicious accounts; (2) Exchanging lists of suspicious accounts with other financial institutions; (3) Detecting and suspending transactions linked to fraudulent activity; (4) Notifying account holders when transactions are blocked; and (5) Providing urgent contact channels (hotlines) so customers can report incidents both during and outside business hours.

As financial institutions, virtual banks in Thailand are required to comply with these measures. This may involve developing Application Programming Interfaces (APIs) to share or receive information on suspicious accounts and transactions, managing back-end systems, and establishing direct customer communication channels. Since these processes go beyond normal banking operations, managing financial fraud and related risks represents another significant challenge for virtual banks.

Krungsri Research view: Adapting to the Virtual Bank Era

Although Thailand has started later than some neighboring countries, virtual banks in Thailand are likely to “establish themselves” quickly. This is due to the well-prepared financial infrastructure, supported by the Bank of Thailand (BoT), Ministry of Finance, Thai Bankers’ Association, and other relevant agencies. Key enablers include electronic Know Your Customer (E-KYC) systems, which allow customers to open bank accounts without visiting a branch, mechanisms for providers to access customer data (Open Data), and the use of alternative data for credit assessment—critical elements for the virtual banking business.

Krungsri Research expects that, in the long term, virtual banks will have limited impact on the financial performance of traditional banks, because their primary target customers, as defined by the BoT, are underserved and unserved populations—often not current clients of traditional banks. Additionally, most Thai banks already provide comprehensive and fully digital financial services.

However, virtual banks are likely to intensify competition in the early stages, particularly in deposits and digital personal loans. They will initially focus on high-interest online deposit accounts and digital personal loans, which may overlap with existing market offerings. Additionally, as mentioned, virtual banks need to rapidly expand their customer base initially. They will likely target digital-native users already familiar with digital financial services—a segment that largely comprises existing commercial bank customers.

Therefore, traditional banks need to adapt to maintain competitiveness through two key strategies: (1) developing products and services that are easy to access, user-friendly for all customer segments, and closely aligned with customer needs; and

(2) leveraging existing advantages, such as non-digital service channels (ATMs/CDMs and branches) that customers associate with reliability and immediate assistance, enhanced digital services and financial products ensuring 24/7 customer access comparable to virtual banks, and a trustworthy brand image—a key factor influencing customers' choice of financial services that virtual banks will need time to establish in their early years.

Moreover, traditional banks should be

(3) prepared for potential regulatory and legal changes after virtual banks begin operations, which could reduce the competitive edge of traditional banks. For example, in October 2024, the Hong Kong Monetary Authority renamed “Virtual Banks” as “Digital Banks” and allowed them to open limited branches—five years after the first virtual bank license was granted—believing that physical branches would enhance customer confidence and experience.

Although virtual banks in Thailand are still in their early stages and it may take several months before a clear business direction emerges, they have already created pressure on existing market players to accelerate their adaptation—particularly in financial technology and customer service—to maintain competitiveness in a rapidly changing market. This increased competition aligns with one of the key objectives of establishing virtual banks in Thailand and also benefits customers by providing new options, making it easier for people to access loans and financial services, and offering products better suited to their needs.

Beyond business competition, virtual banks also have a crucial mission to expand financial access to those who are currently underserved and those who remain unserved by traditional banks. Measuring success in this area requires well-defined business metrics, which presents a regulatory challenge that will need to be closely monitored going forward.

References

ธนาคารแห่งประเทศไทย. (2023). คำถาม-คำตอบ เรื่อง แนวทางการอนุญาตให้จัดตั้งธนาคารพาณิชย์ไร้สาขา (Virtual Bank). BOT. https://www.bot.or.th/content/dam/bot/financial-innovation/digital-finance/virtual-bank/%E0%B8%84%E0%B8%B3%E0%B8%96%E0%B8%B2%E0%B8%A1-%E0%B8%84%E0%B8%B3%E0%B8%95%E0%B8%AD%E0%B8%9A%20Virtual%20Bank.pdf

ธนาคารแห่งประเทศไทย. (2024). คำถามที่พบบ่อย (FAQ) หลักเกณฑ์ วิธีการ และเงื่อนไขในการขอใบอนุญาตและการออกใบอนุญาตประกอบธุรกิจธนาคารพาณิชย์ไร้สาขา (Virtual Bank). BOT. https://www.bot.or.th/content/dam/bot/financial-innovation/digital-finance/virtual-bank/faq-vb.pdf

ธนาคารแห่งประเทศไทย. (2024). ประกาศธนาคารแห่งประเทศไทย ที่ สนส. 6/2567 เรื่อง หลักเกณฑ์การกำกับดูแลธนาคารพาณิชย์ไร้สาขา (Virtual Bank). BOT. https://www.bot.or.th/content/dam/bot/fipcs/documents/FPG/2567/ThaiPDF/25670153.pdf

ธนาคารแห่งประเทศไทย. (n.d.). โครงการ Your Data. BOT. https://www.bot.or.th/th/financial-innovation/digital-finance/open-data/Your_Data_Project.html

ธนาคารแห่งประเทศไทย. (n.d.). สินเชื่อรายย่อย ตัวช่วยสำคัญเมื่อเงินขาดมือ. BOT. https://www.bot.or.th/th/research-and-publications/articles-and-publications/bot-magazine/Phrasiam-67-2/256702_finwis_retail_loan.html

ธนาคารแห่งประเทศไทย. (n.d.). สินเชื่อส่วนบุคคลภายใต้การกำกับ. BOT. https://www.bot.or.th/th/satang-story/managing-debt/personal-loan.html

ฝ่ายกลยุทธ์สถาบันการเงิน ธนาคารแห่งประเทศไทย. (2022). ผลสำรวจการเข้าถึงบริการทางการเงินของคนไทยภาคครัวเรือน. BOT. https://www.bot.or.th/content/dam/bot/documents/th/research-and-publications/reports/financial-access-survey-of-thai-household/fin_access_survey_hh_full_report_2022_th.pdf

สถาบันคุ้มครองเงินฝาก. (2024). ระบบคุ้มครองเงินฝากของไทย. DPA. https://www.dpa.or.th/articles/thailand-deposit-protection-system

Amazon. (n.d.). AI เชิงสนทนาคืออะไร. AWS. https://aws.amazon.com/th/what-is/conversational-ai/

Asian Banking and Finance. (2025). CIMB Singapore unveils FlexiPay loan with flexible SME repayment terms. Asian Banking and Finance. https://asianbankingandfinance.net/retail-banking/news/cimb-singapore-unveils-flexipay-loan-flexible-sme-repayment-terms

Asian Banking and Finance. (2025). SG digital banks expand into investments and loans to boost profits. Asian Banking and Finance. https://asianbankingandfinance.net/news/sg-digital-banks-expand-investments-and-loans-boost-profits

Bank of England. (n.d.). New banks authorised since 2013. Bank of England. https://www.bankofengland.co.uk/prudential-regulation/new-bank-start-up-unit/new-banks-authorised-since-2013

Browne, R. (2025). Inside Revolut’s bid to be the Amazon of banking, and the lessons it’s learned from breakneck growth. CNBC. Retrieved from https://www.cnbc.com/2019/07/05/revolut-ceo-nikolay-storonsky-on-the-fintech-unicorns-journey.html

Caminiti et al. (2025). Banking Consumer Study 2025. Accenture. https://www.accenture.com/content/dam/accenture/final/industry/banking/document/Accenture-Global-Banking-Consumer-Study-2025-Report.pdf

European Banking Authority (EBA). (n.d.). Passporting and supervision of branches. EBA Europa. https://eba.europa.eu/regulation-and-policy/passporting-and-supervision-branches

European Central Bank (ECB). (2016). The revised Payment Services Directive (PSD2) and the transition to stronger payments security [Press release]. ECB Europa. https://www.ecb.europa.eu/press/intro/mip-online/2018/html/1803_revisedpsd.en.html

Financial Conduct Authority. (n.d.). New Bank Start-up Unit launched by the financial regulators [Press release]. FCA. Retrieved from https://www.fca.org.uk/news/press-releases/new-bank-start-unit-launched-financial-regulators

Groenfeldt, T. (2020). Varo Gets A Banking License And Moves Operations To Temenos Transact Platform. Forbes. https://www.forbes.com/sites/tomgroenfeldt/2020/09/16/varo-gets-a-banking-license-and-moves-operations-to-temenos-transact-platform/

Klapper et al. (2025). The Global Findex Database 2025: Connectivity and Financial Inclusion in the Digital Economy. Washington, DC: World Bank. https://doi.org/10.1596/978-1-4648-2204-9.

Lee, Y. (2023). Internet banks boost competitive edge with 'group accounts'. Korea Times. https://www.koreatimes.co.kr/business/banking-finance/20230306/internet-banks-boost-competitive-edge-with-group-accounts

Microsift. (2025). KakaoBank Launches Korea’s First Azure OpenAI-Powered Conversational AI Service in the Financial Sector. Microsoft. https://www.microsoft.com/en/customers/story/24967-kakao-bank-azure-openai

Monetary Authority of Singapore (MAS). (n.d.). Eligibility Criteria and Requirements for Digital Banks. MAS. https://www.mas.gov.sg/-/media/Digital-Bank-Licence/Eligibility-Criteria-and-Requirements-for-Digital-Banks.pdf

Mordor Intelligence. (2025). Latin America Neo Banking Market Size & Share Analysis – Growth Trends & Forecasts (2025-2030). Mordor Intelligence. https://www.mordorintelligence.com/industry-reports/latin-america-neo-banking-market

N26. (2025). N26 enters Germany’s telecommunication market with digital mobile plan offer [Press release]. N26. https://n26.com/en-eu/press/press-release/n26-enters-germany-s-telecommunication-market-with-digital-mobile-plan-offer

Office of the Comptroller of the Currency (OCC). (n.d.). Bank Management. OCC. https://www.occ.gov/topics/supervision-and-examination/bank-management/index-bank-management.html

Office of the Comptroller of the Currency (OCC). (n.d.). Financial Technology. OCC. https://www.occ.gov/topics/supervision-and-examination/financial-technology/index-financial-technology.html

PRNewswire. (2025). WeBank Wins Three Awards at The Asian Banker Excellence in Retail Finance Services Awards Ceremony 2025. PRNewswire. https://www.prnewswire.com/apac/news-releases/webank-wins-three-awards-at-the-asian-banker-excellence-in-retail-finance-services-awards-ceremony-2025-302383366.html

Riley, D. (2025). Chime jumps 37% in Nasdaq debut after raising $700M in IPO. Silicon Angle. https://siliconangle.com/2025/06/12/chime-closes-37-nasdaq-debut-raising-700m-ipo/

Romani, A. (2025). Nubank applies for US bank charter in expansion outside Latin America. Reuters. https://www.reuters.com/business/finance/brazils-nubank-applies-us-bank-charter-2025-09-30/

The Asian Banker. (2025). Nubank, ING (Global) and WeBank are the world’s top digital banks, with 61% of the top 100 reporting full-year profitability. The Asian Banker. https://www.theasianbanker.com/press-releases/nubank-ing-global-and-webank-are-the-world-s-top-digital-banks-with-61-of-the-top-100-reporting-full-year-profitability

Tirona, O. (2023). Regulatory caps on neobanks’ operations could stifle growth, expert warns. Asian Banking and Finance. https://asianbankingandfinance.net/banking-technology/exclusive/regulatory-caps-neobanks-operations-could-stifle-growth-expert-warns

1/ The Global Findex 2025 | www.worldbank.org

2/ A bank account refers to an account held with a bank or a financial institution that functions similarly to

a bank, such as a credit union, microfinance institution, post office, or mobile money provider.

3/ ถอดรหัส VIRTUAL BANK ข้อมูลที่ผู้ให้และผู้ใช้บริการควรรู้ | Bank of Thailand

4/ Nubank, ING (Global) and WeBank are the world’s top digital banks, with 61% of the top 100 reporting full-year profitability | The Asain Banker

5/ The regulatory authorities overseeing virtual banks in the United Kingdom are the Prudential Regulation Authority (PRA) and

the Financial Conduct Authority (FCA).

6/ New banks authorised since 2013 | Bank of England

7/ The Payment Services Directive 2 (PSD2) aims to enhance the security of online financial transactions. It requires banks to provide account information to third-party providers (TPPs) and enforces Strong Customer Authentication (SCA) to prevent payment fraud.

8/ As of March 2025

9/ Nubank applies for US bank charter in expansion outside Latin America | Reuters

10/ Licenses are divided into Digital Full Bank (DFB), for virtual banks that primarily serve retail and corporate customers, and Digital Wholesale Bank (DWB), for banks that focus on serving SMEs.

11/ As of June 2024

12/ คำถาม-คำตอบ เรื่อง แนวทางการอนุญาตให้จัดตั้งธนาคารพาณิชย์ไร้สาขา (Virtual Bank) | Bank of Thailand

13/ ประกาศกระทรวงการคลัง เรื่อง หลักเกณฑ์ วิธีการ และเงื่อนไขในการขอใบอนุญาตและการออกใบอนุญาตประกอบธุรกิจธนาคารพาณิชย์ไร้สาขา (Virtual Bank) | Bank of Thailand

14/ The Global Findex 2025 | www.worldbank.org

15/ Based on data at the end of 2024, Thailand had 60.94 million internet users (NBTC)

out of a total population of 65.95 million. (the Department of Provincial Administration, Ministry of Interior)

16/ By the end of 2024, there were 147.3 million Internet and Mobile Banking accounts in Thailand. During the year,

the total number of transactions reached 36.5 billion, with a total value of THB 112.8 trillion. (BoT)

17/ As of 2Q 2025

18/ ผลสำรวจการเข้าถึงบริการทางการเงินภาคครัวเรือน ปี 2565 (Financial Access Survey of Thai Households) | Bank of Thailand

19/ Excluding credit cards

20/ Non-digital channels here include bank branches, CDM/ATM machines, and banking agents,

while digital channels refer to mobile and internet applications.

21/ The Banking Consumer Study 2025 surveyed 49,300 bank customers across 39 countries.

22/ แค่เริ่มทำงานก็เป็นหนี้! แบงก์ชาติเผย First Jobbers ไทย ‘ครึ่งหนึ่ง’ เป็นหนี้แล้ว พบ 1 ใน 4 เริ่มมีปัญหา พร้อมส่องทางออกวิกฤตหนี้ไทย | The Standard

23/ replacing an existing loan with a new one under better terms (e.g., lower interest rates)

24/ Nubank, ING (Global) and WeBank are the world’s top digital banks, with 61% of the top 100 reporting full-year profitability | The Asian Banker

25/ ประกาศธนาคารแห่งประเทศไทย ที่ 19/2568 เรื่อง มาตรฐานและมาตรการเพื่อป้องกันอาชญากรรมทางเทคโนโลยีสำหรับสถาบันการเงิน | Bank of Thailand