Executive Summary

Amid ongoing energy concerns stemming from geopolitical tensions, Indonesia and Brazil have responded to the crisis by mandating high-blend biofuels at home, such as B50 (diesel blended with 50% palm oil) in Indonesia, or E100 (100% ethanol) in Brazil. However, if Thailand were to follow suit, it would face several challenges that carry high risks and could affect other industries, particularly the agricultural supply chain and the agro-industrial, food, and energy sectors. This is because Thailand faces structural constraints that differ from those of major energy-crop producing countries in several respects, such as insufficient upstream feedstock supply, the enforcement of emission standards, Thai consumers' growing preference for electric vehicles, as well as the risk that high-blend fuels could damage engine systems. Nevertheless, Thailand could instead redirect its policy toward developing an advanced biorefinery industry to produce Drop-in fuels such as renewable diesel (Hydrogenated Vegetable Oil: HVO) or sustainable aviation fuel (Sustainable Aviation Fuel: SAF) in order to focus on premium export markets and the global aviation industry.

Introduction: The First Step into the Biofuel Era

Recently, geopolitical tensions in the Middle East, flaring up periodically, have kept crude oil prices in the global market volatile and persistently high. Transport and production costs have risen accordingly, leaving consumers to shoulder higher living costs and surging energy bills. In addition, many countries around the world have also grown concerned about energy security, especially those that rely on crude oil imports, including Thailand.

Amid this crisis, Indonesia, the producer and exporter of crude palm oil (Crude Palm Oil: CPO) ranked No. 1 in the world, has announced the mandatory use of B50 diesel, a blend of 50% palm-oil biodiesel with 50% fossil diesel, along with a halt to imports of low-grade diesel1/ effective 1 July 2026 onward2/. Its main goals are to strengthen domestic energy security and to ease the burden of energy subsidies, which have been rising3/ due to tensions in the Middle East.

This news raises an important question: can Thailand follow in the footsteps of Indonesia, which uses high-blend biofuels like B50, or Brazil, which uses E1004/?

In this article, Krungsri Research analyzes Thailand's overall biofuel landscape and assesses the strategic feasibility as well as the constraints, using the PESTEL framework. The analysis covers factors ranging from the security of upstream feedstocks, namely crude palm oil and ethanol, to the impacts on consumers and industry, in order to answer how ready Thailand is to raise the share of biofuels, build resilience against energy crises, and move toward sustainability over the long term.

Understanding Biodiesel and Biogasoline

Biodiesel and biogasoline are the two main groups of biofuels, which can substitute for diesel and gasoline, respectively. Both groups follow the same principle: plant-based fuel is blended with petroleum-based fuel in various proportions, and the number at the end of the name indicates the percentage of biofuel in the blend.

Biodiesel (Biodiesel or Fatty Acid Methyl Ester: FAME)5/, 6/, is a liquid fuel for diesel engines. It is an alternative fuel produced from agricultural raw materials or organic matter, mainly vegetable oil

7/, animal fat, or used cooking oil from households and restaurants. These feedstocks go through a chemical process that converts them into pure biodiesel at 100%, or B100, which burns and lubricates in much the same way as regular diesel refined from crude oil. In everyday use, however, pure biodiesel is not put directly into vehicles; it is blended with base diesel in various proportions. For example, B7 is diesel containing 7% biodiesel, which is the current standard fuel.

Accordingly, B50 is a diesel-engine fuel containing 50% biodiesel blended with 50% conventional diesel.

Biogasoline is a liquid fuel for gasoline engines, made by blending base gasoline with “ethanol” (Ethanol)

8/, a pure alcohol produced from plant feedstocks. In Thailand, molasses, cane juice, and cassava are the main feedstocks. The number after the E indicates the share of ethanol in the blend. For example, E20 is gasoline blended with 20% ethanol; E85 is gasoline blended with ethanol at 85%; and E100 is pure ethanol at 100%, which Brazil uses as a domestic fuel.

For Thailand, both “Gasohol 91” and “Gasohol 95”, the names we all know well, are in fact both E10, meaning they contain the same 10% ethanol. What differs is the octane rating, which measures how well the fuel resists premature ignition, or engine “knock”. The higher the octane rating, the better suited the fuel is to high-performance engines. Gasohol 95

9/ differs from Gasohol 91 only in that it has a higher octane rating.

Assessing the Feasibility of High-Blend Biofuels in Thailand through the Lens of PESTEL

In this section, Krungsri Research assesses how ready Thailand is to push high-blend biofuels such as B50 or high-blend biogasoline into mainstream fuels, weighing both opportunities and constraints through the PESTEL framework, a tool for analyzing the macro-level external environment across six dimensions: political (Political; P), economic (Economic; E), social (Social; S), technological (Technological; T), environmental (Environmental; E) and legal (Legal; L), to systematically explain the factors that determine feasibility, as follows:

1. Political Dimension: Policy Feasibility

In the political and policy dimension, if Thailand were to rely mainly on high-blend biofuels, the following issues would need to be considered:

- Risk to the supply of cooking palm oil: In the past, the Thai government has adjusted the biodiesel blending ratio, for example from B5 to B7, as a tool to help absorb surplus output and stabilize cooking oil prices. But if the government pushed all the way to B50, demand for crude palm oil in the energy sector would surge to the point of potentially competing with the volumes used in the food industry. This would push up the price of cooking palm oil and directly raise the cost of living

- Thailand's energy strategy: Thailand has laid out an energy strategy that clearly differs from Indonesia's. Thailand aims to become a Regional Bio-hub, or the region's biofuel hub, and to move up from producing conventional blending-grade biodiesel (FAME)10/ to two types of advanced fuels: renewable diesel (HVO)11/ and sustainable aviation fuel (Sustainable Aviation Fuel: SAF)12/, to capture international airlines and export markets that require the CORSIA13/ standard, which generates higher value per liter than conventional biodiesel. In contrast, Indonesia focuses on producing biodiesel primarily to reduce oil imports. And as the producer and exporter of crude palm oil ranked No. 1 in the world, it holds bargaining power akin to an "OPEC of vegetable oil". Producing high-blend biodiesel therefore helps create large-scale demand for crude palm oil (CPO)14/, allowing Indonesia to control crude palm oil prices and steer price direction in the global market. The differences between the energy strategies of Thailand and Indonesia are summarized in Table 1.

2. Economic Dimension: Investment Worthiness

Looking at the economic dimension and investment worthiness, high-blend biofuels face the following constraints for Thailand:

-

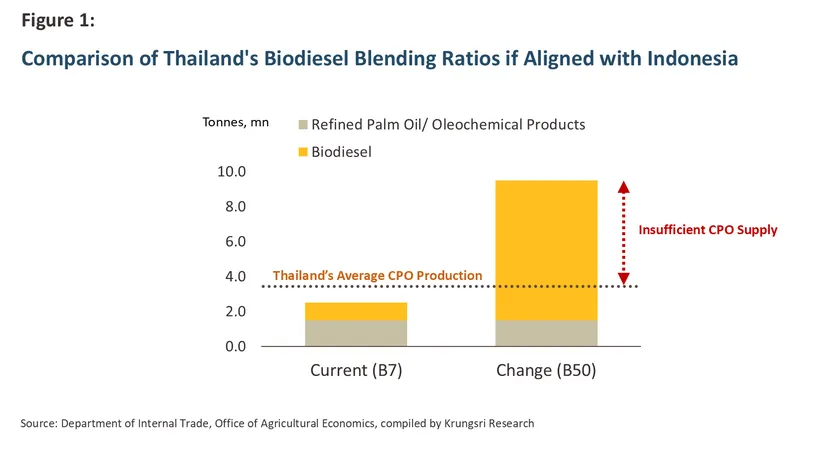

Thailand does not produce enough oil palm: As the producer and exporter of crude palm oil (CPO) ranked No. 1 in the world15/, Indonesia produces well beyond its domestic needs, so it can freely produce B50 biodiesel without affecting its food industry. Thailand, by contrast, is in a very different situation. Currently, Thailand uses CPO to produce biodiesel - about 0.9-1.1 million tonnes per year16/, or roughly 27-29% of total CPO output. If Thailand moved to B50, demand for CPO in the energy sector would jump 7-10-fold17/, exceeding the total CPO Thailand currently produces. In other words, even if all the palm oil used in the food industry were diverted to energy, it might still not be enough (Figure 1)

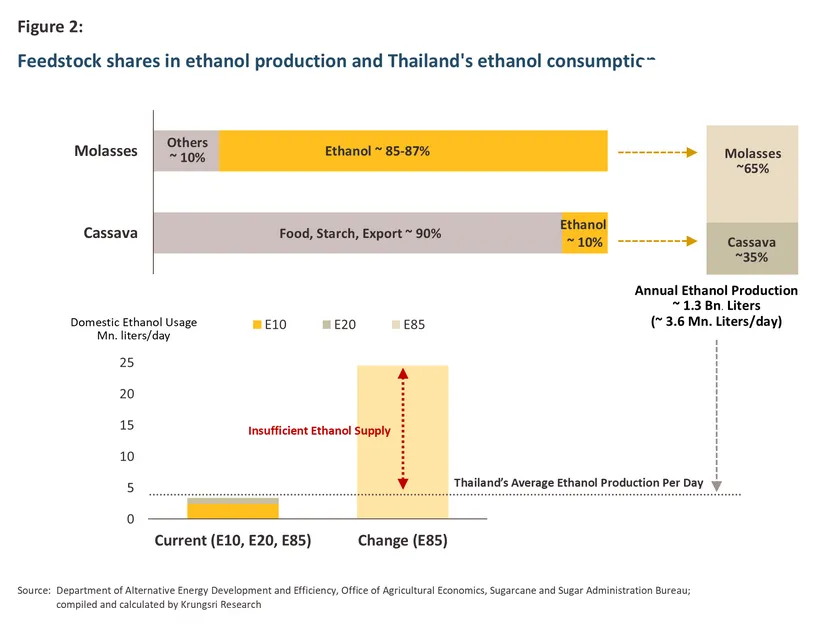

- Feedstocks for producing ethanol are insufficient as well: If Thailand were to push E85 or E100 as the base gasoline18/, the ethanol supply chain would reveal three overlapping weak points, as follows:

-

Plants lack feedstock: Although Thai ethanol plants have a combined installed capacity as high as 7 million liters per day19/, they actually run at only 50-54%, or about 3.5-3.6 million liters per day, because of feedstock shortages

-

Almost all domestically produced molasses is already used up: The ethanol industry consumes nearly all domestic molasses, about 3.6-3.7 million tonnes per year, or 85-87% of the country's total molasses output20/. So to produce more ethanol, producers would have to pull sugarcane out of the sugar industry21/, leaving sugar output short of domestic demand and potentially pushing sugar prices up.

-

Beyond molasses, other feedstocks also face strong demand from the food industry, so shortages could arise: If molasses runs short, ethanol production would have to switch to cassava instead. Currently, the ethanol industry uses about 2.7-3.1 million tonnes of cassava per year, or 9-11% of Thailand's total cassava output. The remaining 90%-plus goes mainly into the cassava starch industry, in which Thailand is the world's No. 1 exporter. Diverting more cassava into ethanol would put the energy sector in direct competition for resources with the food industry and other related industries (Figure 2)

- Volatile feedstock prices: Biodiesel and ethanol producers face cost risks that shift with natural phenomena, crop diseases, and volatile global demand for feedstocks. For example, feedstock shortages caused by El Niño would push up feedstock costs for ethanol and biodiesel, making biofuels less price-competitive compared with fossil fuels.

3. Social Dimension: Impacts on Consumers

If energy policy were to shift toward high-blend biofuels, the social issues to consider are as follows:

-

Consumer acceptance: Whether consumers will accept high-blend biofuels depends on three main factors: 1) price, which is the most decisive. If the retail price per liter is cheaper than alternative fuels, consumers will be more inclined to switch to high-blend biofuels; 2) confidence that the fuel can be used with their engines — if automakers certify compatibility and warranty terms cover high-blend fuels, consumers will be more willing to accept and switch. Conversely, if consumers are not sure whether high-blend fuels will affect their engines or warranty terms, they may turn back to familiar low-blend fuels such as B5 B7 or E10 instead; and 3) ease of access — if service stations selling high-blend fuels are widely available, consumers can change their behavior more easily without adjusting their refueling routines. All three factors remain challenges for high-blend biofuels.

-

Consumers increasingly favor electric vehicles: Thai consumers have taken to battery electric vehicles (BEV) quite quickly. In 2025, new BEV passenger-car registrations in Thailand reached 118,696 units, or around 21.9% of all new passenger-car registrations for the year, up sharply from 2021, when the share was only 0.4%. Support has come from interest in new technology and running costs that are lower than for combustion cars — both from vehicle prices that have fallen considerably as automakers compete on price and from cheaper energy costs per kilometer — as well as their environmental friendliness. As a result, pushing high-blend biofuels may not match what Thai consumers currently want.

4. Technological Dimension: Engineering Constraints

Advances in engine technology may create constraints for a high-blend biofuel policy, as follows:

-

Current diesel and gasoline engines do not yet support high-blend biofuels: Automakers and the Thai automotive industry association currently cap diesel-engine warranties at B20 and gasoline engines at E2022/ under the Euro 523/ emission standard, because higher biofuel blends cause sludge or sediment to form in fuel tanks and fuel filters24/ and fuel lines to corrode and fail prematurely25/. Diesel vehicles face even greater damage as diesel particulate filters clog26/ and exhaust after-treatment systems wear out faster27/, giving manufacturers grounds to void the warranty (OEM Warranty Void)

-

High-blend biofuels are highly corrosive, so infrastructure may need a complete overhaul: Because biofuels absorb moisture, which corrodes storage tanks, pipelines, and dispensers, using high-blend biofuels could force logistics operators and service stations to invest in upgrading their infrastructure across the entire system — for example, separating storage tanks, increasing the frequency of corrosion inspections and pipeline cleaning, and adding dispensers for large freight trucks and public transport vehicles.

-

The automotive industry is heading toward ZEV: Global vehicle technology is shifting toward zero-emission vehicles (Zero Emission Vehicle: ZEV)28/, both battery electric vehicles (Battery Electric Vehicle: BEV)29/ and fuel cell electric vehicles (Fuel Cell Electric Vehicle: FCEV)30/ more and more. Automakers are therefore focusing their research and development in this direction, as well as making combustion engines more efficient and environmentally friendly. Developing engines to support high-blend biofuels has thus become a lower priority.

-

Fuel technology may leapfrog to Drop-in31/ fuels instead: Conventional biodiesel remains constrained mainly by engine limitations, whereas Drop-in fuels like HVO and SAF are bio-based feedstocks that have been hydrotreated until their molecular structure matches fossil diesel/gasoline. They can therefore be blended with fossil fuels at high ratios right away. Using Drop-in fuels requires no engine retuning, and they do not cause the sediment or clogging problems in exhaust after-treatment systems that are the main drawbacks of conventional biodiesel.

5. Environmental Dimension: Natural Constraints

Thailand's support for biofuels faces constraints from nature as well as environmental policy, as follows:

-

Feedstock yields fluctuate with the climate: Historical data show that palm and sugarcane yields fluctuate with the climate32/, causing Thailand's biofuel production to fluctuate too. For example, in 2016 and 2020 Thailand faced El Niño events that reduced palm yields, and the government had to cut the biodiesel blending ratio33/.

-

More air pollution: Because high-blend biofuels raise combustion temperatures, they emit more nitrogen oxides (NOx), a precursor of PM2.5 dust.

-

Expanding cultivated areas for more feedstock could lead to forest encroachment and reduced biodiversity: To secure enough feedstock for high-blend biofuel production, Thailand would need to expand palm and sugarcane plantations, which risks leading to encroachment on forest land. In addition, monoculture farming of palm or sugarcane alone further reduces biodiversity.

6. Legal Dimension: Regulatory Hurdles

The legal dimension is one of the constraints on the high-blend biofuel industry, as follows:

-

The legal gap on liability (Liability gap): Current law does not clearly specify who would bear the repair costs34/ if the state made high-blend biofuel the standard fuel and a consumer's engine was damaged by using it — the automaker that voided the warranty, the consumer left to shoulder the burden, or the state that issued the policy.

-

Global trade standards: Thailand's current fuel standards follow international standards so that vehicles made in Thailand can be exported. Setting a country-specific fuel standard (such as B50) would make Thailand's fuel standards diverge from global standards, which could conflict with the Agreement on Technical Barriers to Trade (TBT) under the World Trade Organization, which prohibits member states from setting product standards in ways that obstruct international trade35/.

-

New supporting legislation required: To mandate high-blend biofuels, the Department of Energy Business would have to issue a new notification on fuel specifications and quality, which must go through drafting and a full impact review. So putting the policy into practice would take time.

-

Mismatch between the carbon tax and the Oil Fuel Fund law: On the legal front, the state is switching tools — from subsidizing biofuel prices through the Oil Fuel Fund to levying a carbon tax on fossil fuels. The goals point in the same direction: making biofuels price-competitive with fossil fuels. But technical issues between the two laws have not yet been fully reconciled.

Krungsri Research's View

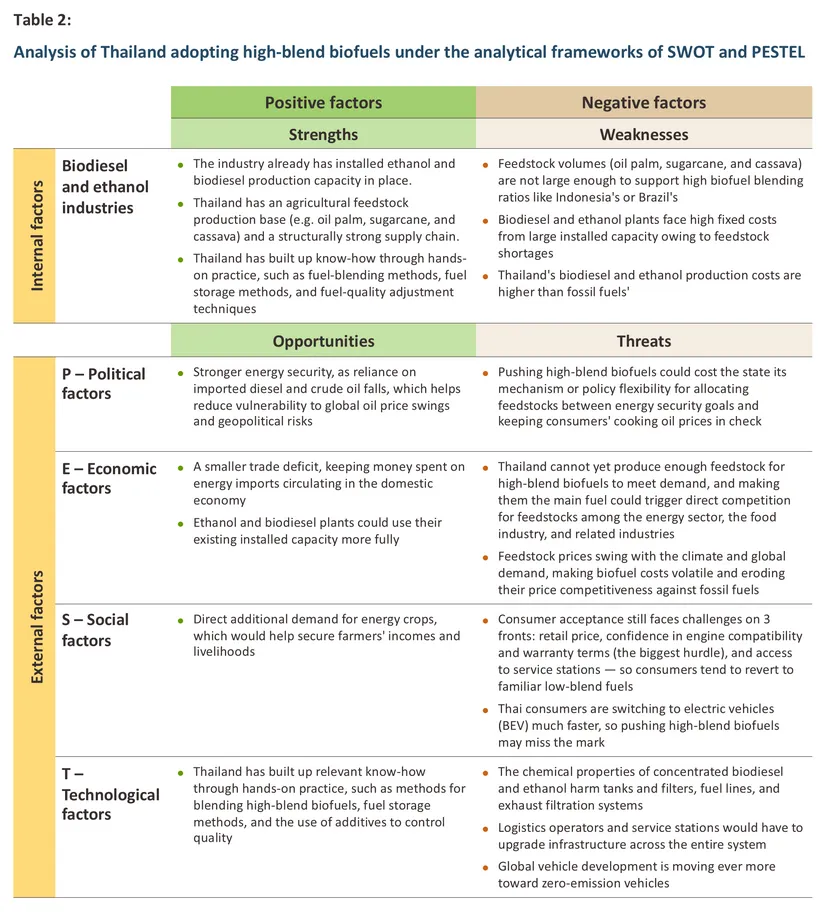

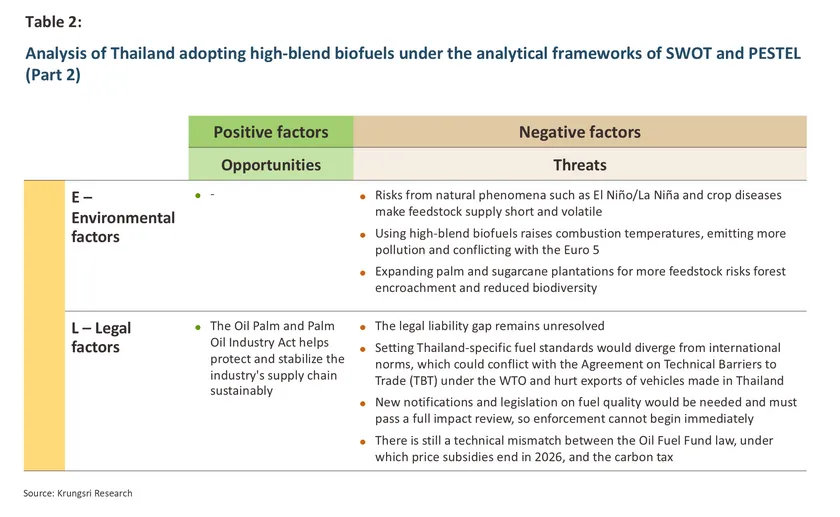

Given that the supply chains and broader contexts of Thailand, Indonesia, and Brazil differ, Krungsri Research analyzes biofuel policy using two tools together: SWOT Analysis to assess Thailand's strengths, weaknesses, opportunities, and threats, together with PESTEL to explore the external factors that pose both opportunities and threats across the political, economic, social, technological, environmental, and legal dimensions. This helps build a well-rounded picture of how Thailand should proceed with this policy. The results are shown in Table 2

From the SWOT and PESTEL analyses above, it is clear that adopting high-blend biofuels such as B50 or E100 as the main fuel, as Indonesia and Brazil have done, may not be a path Thailand can sustain over the long run, given structural obstacles: feedstock constraints, technical limits of engines, and fiscal constraints, since the Oil Fuel Fund is currently still in deficit. Krungsri Research therefore sees a better fit for Thailand's context in moving toward advanced drop-in biofuels such as HVO and SAF, whose advantages directly address the constraints above, as follows:

-

No competition for feedstocks: Producing HVO and SAF can use used cooking oil (UCO) directly as the main feedstock instead, so it avoids the limited-supply problem and does not compete with other industries for raw materials. Thailand already has operators investing in and developing this area36/.

-

Compatible with existing engines: Drop-in fuels have the same molecular structure as fossil fuels, so they can be blended at high ratios without engine retuning, cause no sediment or clogging problems, and do not affect warranty terms.

-

Higher value added and access to premium export markets: HVO and SAF37/ target international airlines and the European Union market, where laws require set biofuel blending shares — for example, the CORSIA scheme for aviation, the RED III38/ law, and ReFuelEU Aviation39/ of the European Union. This creates assured demand and selling prices per liter above conventional biodiesel, helping lift Thailand into the region's hub for advanced biofuel production (Regional Bio-hub)

References

Bangchak (2026). Bangchak Group Begins Commissioning of Sustainable Aviation Fuel (SAF) Production Unit with Product Delivery Expected for Q2. Retrieved from https://www.bangchak.co.th

Bangchak (2026). Bangchak has commenced the first commercial production of Sustainable Aviation Fuel (SAF) in Thailand, ready for export to the global market. Retrieved from https://www.bangchak.co.th

BioEnergy Times (2026). Thailand to introduce SAF standards and blending from 2026. Retrieved from https://bioenergytimes.com/thailand-to-introduce-sustainable-aviation-fuel-standards-and-blending-from-2026/

Department of Alternative Energy Development and Efficiency (2026). Ethanol Promotion and Utilization Status, March 2026. Retrieved from https://www.dede.go.th/category?id=13

Energy Policy and Planning Office, Ministry of Energy (2026). Fuel Price Structure. Retrieved from https://www.eppo.go.th/index.php/th/petroleum/price/structure-oil-price

GC (2025). GC has successfully moved forward to produce Sustainable Aviation Fuel (SAF) as the first in Thailand, reinforcing its potential as a global leader in low-carbon chemicals. Retrieved from https://www.pttgcgroup.com

Maaai (2026). Indonesia to Halt Diesel Imports and Boost Domestic Alternatives. Retrieved from https://maaal.com/en/news/details/indonesia-to-halt-diesel/

Ministry of Energy (2026). Annual Action Plan for 2026. Retrieved from https://www.energy.go.th

RRI (2026). Indonesia Stops Importing Diesel, Implements B50 Starting July 2026. Retrieved from https://rri.co.id/en/national/2346634/indonesia-stops-importing-diesel-implements-b50-starting-july-2026

The Secretariat of Cabinet (2024). Request for extension of the compensation period for biofuels-blended fuels. Retrieved from https://resolution.soc.go.th/PDF_UPLOAD/2567/P_411810_2.pdf

1/ Diesel of this grade is designed and used mainly for the following vehicle and engine types: 1) trucks and commercial transport vehicles; 2) public buses; 3) older diesel vehicles (Pre-Common Rail or Direct Injection systems) built before strict emission standards took effect (pre-Euro 4); and 4) agricultural machinery and small fishing boats.

2/ The implementation timeline for each grade of low-grade diesel is as follows: 1) diesel grade CN48 (Cetane Number 48), known as Solar, for which Indonesia has now completely ended imports; and 2) diesel grade CN51 (Cetane Number 51), which Indonesia allows to be imported until 30 June 2026. So from 1 July 2026 onward, Indonesia will end all imports of conventional diesel (Source: Indonesian Palm Oil Association, Indonesia's Ministry of Agriculture, Indonesia's Ministry of Energy and Mineral Resources)

3/ A report by the International Institute for Sustainable Development (IISD) states that Indonesia's B30/B35 program saves the country as much as USD 8.0-9.0 billion per year in reduced crude oil imports.

4/ Brazil is the only country in the world with an ecosystem for using E100. More than 80% of small private passenger cars in Brazil are Flexible Fuel Vehicle (FFV) vehicles, developed by automakers to run on pure E100 from dispensers at ordinary service stations. Thailand has FFV vehicles designed by original equipment manufacturers (OEM), but they support only E85; as for E100, use is limited to modified vehicles and research applications.

5/ FAME (Fatty Acid Methyl Ester) is the chemical name — an ester formed when fatty acids react with methanol— while biodiesel is the commercial or product name.

6/ For more details, see Industry Outlook 2025-2027: Biodiesel Industry.

7/ In Thailand and the ASEAN region (e.g. Indonesia, Malaysia), production is based mainly on palm oil.

8/ For more details, see Industry Outlook 2026-2028: Ethanol Industry.

9/ Gasohol 91 and 95 perform in engines the same way as octane-91 and octane-95 gasoline, respectively.

10/ FAME or Fatty Acid Methyl Ester is conventional biodiesel that is blended with today's diesel.

11/ HVO or Hydrogenated Vegetable Oil is renewable diesel produced from vegetable oil through hydrogenation, with properties very close to petroleum diesel.

12/ SAF or Sustainable Aviation Fuel is sustainable aviation fuel produced from bio-based feedstocks. The Department of Energy Business began applying the sustainable aviation fuel standard on 1 January 2026, designating the Jet A-1 grade to accommodate SAF blending, to stimulate demand in the region.

13/ CORSIA or Carbon Offsetting and Reduction Scheme for International Aviation is the global aviation industry's carbon reduction standard. For more details, see Krungsri Research's Research Intelligence report “CORSIA: Paving the Way for Flying Net Zero”.

14/ CPO or Crude Palm Oil is crude palm oil, the primary palm oil obtained by pressing fresh palm fruit at palm oil extraction plants. CPO is passed on to downstream industries such as refineries producing refined palm oil for consumption (RBD Palm Olein) or the oleochemicals industry (Oleochemicals), and it is the main feedstock for producing biodiesel (B100).

15/ Indonesia is able to push B50 because it is the largest producer and exporter of crude palm oil (CPO) - ranked No. 1 in the world. In 2023-2025, Indonesia produced around CPO 43.0-45.5 million tonnes of CPO per year and exported a CPO surplus of around 23.5-28.1 million tonnes per year (Source: USDA)

16/ In 2023-2025, Thailand produced about CPO 3.3-3.9 million tonnes of CPO per year, while consumption was 2.4-2.5 million tonnes per year - about 1.4-1.6 million tonnes for consumption and the food industry and about 0.9-1.1 million tonnes for biodiesel production - leaving only a small amount for reserve stocks and exports.

17/ Based on the standard biodiesel blends B5 and B7 in force during 2023-2025 (Source: Central Committee on the Prices of Goods and Services).

18/ Under the National Energy Plan 2024, the Thai government is restructuring the fuel lineup, aiming to cut the number of fuel types down to only those that are essential or most used: Gasohol 95 and E20 as the mainstays for gasoline vehicles, and diesel B7 for diesel vehicles, while Gasohol 91 and E85 are the group the plan will gradually withdraw from the market, to simplify the fuel structure, reduce fuel inventory management burdens, cut logistics costs, and make price subsidies more targeted.

19/ In 2025, Thailand had 28 ethanol producers with a combined installed capacity of 7.0 million liters/day: plants using molasses, 2.8 million liters per day; cassava, 2.3 million liters per day; cassava and molasses combined, 1.1 million liters per day; and cane juice, 0.8 million liters per day. For more details, see Industry Outlook 2026-2028: Ethanol Industry (page 7)

20/ Out of average domestic sugarcane output of around 82-94 million tonnes per year.

21/ Brazil can use E100 because it is the producer of sugarcane, ranked No. 1 in the world. In 2023-2025, Brazil produced around 38.1-45.5 million tonnes of sugar per year and exported around 28.2-36.0 million tonnes per year — 3-5 times and 4-8 times more than Thailand, respectively (Source: USDA)

22/ Vehicle owners can check which models automakers certify for B20 diesel or E20 gasohol in the owner's manual and vehicle warranty booklet (vehicle handbook), at each brand's service centers, or with the Department of Energy Business, which compiles the models and engine types certified by automakers for B20 or E20 at the website https://www.doeb.go.th/th

23/ Thailand fully enforced the engine emission control standard, Euro 5 nationwide in 2024-2026

24/ FAME reacts easily with oxygen and absorbs moisture, so sludge or sediment readily forms in fuel tanks and fuel filters.

25/ The chemical cause: biodiesel and ethanol are strong solvents, readily absorb moisture, and have a lower heating value than fossil fuels, so they corrode rubber parts, gaskets, plastics, and metals in the fuel line system, while also reducing driving range per tank.

26/ FAME has a higher boiling point than fossil diesel. When fuel is injected to burn off soot in the DPF (Diesel Particulate Filter), some FAME may not fully evaporate and can seep into the engine oil (Oil Dilution), reducing lubrication performance and clogging the DPF system.

27/ Using FAME at high blends generates nitrogen oxides (NOx), making the exhaust after-treatment system in diesel vehicles (Selective Catalytic Reduction :SCR) work so hard that it degrades faster, and requiring more urea solution (AdBlue) to keep emissions within the Euro 5 and 6

28/ For more details, see Industry Outlook 2025-2027: Automobile Industry and Industry Outlook 2026-2028: Electric Vehicle Industry.

29/ An electric vehicle powered by a battery (Battery Electric Vehicle: BEV), which must be plugged in to charge and store energy in the battery.

30/ A fuel cell electric vehicle (Fuel Cell Electric Vehicle: FCEV) is driven by an electric motor just like a BEV, but generates its own electricity on board from a chemical reaction between high-pressure hydrogen and oxygen in the air, via a fuel cell that acts like a miniature power plant. It therefore needs no external charging like a BEV or PHEV, but must still refuel with hydrogen at dedicated stations, which takes about as long as filling up with gasoline. The electricity generated by the fuel cell drives the motor and charges the onboard battery. Throughout the driving process, the vehicle emits no pollutants — only water vapor from the tailpipe, which is environmentally safe. For more details, see Hydrogen-Powered Vehicles: A Clean Energy Alternative for a Greener Future.

31/ This technology is the Hydroprocessing or Hydrotreating process: bio-based feedstocks (such as palm oil, animal fat, or used cooking oil) are reacted with hydrogen under high pressure and heat to remove oxygen and rearrange the molecules. The result is a clean fuel, free of sulfur and aromatics, that does not cause moisture, sludge, or clogging problems in modern engine systems.

32/ For more details, see Industry Outlook 2026-2028: Palm Oil Industry (page 14) and Industry Outlook 2026-2028: Sugar Industry (page 14)

33/ For more details, see Industry Outlook 2026-2028: Palm Oil Industry (page 8)

34/ Repair costs depend on the vehicle type and brand. For example, replacing the entire DPF system costs around 30,000 - 200,000 baht; the SCR system around 60,000 - 150,000 baht; and fuel filters 500 - 5,000 baht (Source: authorized service centers and specialist garages)

35/ Indonesia addressed this problem by 1) notifying the measure to the TBT Committee, citing energy security objectives; 2) applying the requirement to every drop of fuel in the domestic market without discrimination, whether locally produced or imported; 3) separating vehicle type approvals to match each market's fuel — vehicles sold domestically support B40/B50, while export vehicles follow the standards of destination countries; and 4) coordinating with automakers on engine compatibility testing and warranty terms for vehicles sold domestically. Source: Ministry of Energy and Mineral Resources of the Republic of Indonesia, compiled by Krungsri Research.

36/ Operators that have already invested include: 1) Bangchak (BCP), which has set up an SAF refinery using used cooking oil (Used Cooking Oil: UCO) as the main feedstock, with a capacity of 1 million liters/day; 2) PTT Global Chemical (GC), which uses Co-processing technology, processing UCO together with fossil crude oil, with a first-phase capacity of 6 million liters per year; and 3) Thai Oil (TOP), which has begun the Clean Fuel Project (CFP) to expand its capacity to refine high-quality fuels and handle bio-based feedstocks; parts of the system are now in test operation, with full commercial operation targeted for Q3 2028. Meanwhile, PTG Energy (PTG) is still testing and conducting further studies.

37/ Refineries upgraded to produce HVO can also switch their process to produce SAF, or bio-jet fuel. SAF commands a higher value than diesel and enjoys demand from the aviation industry worldwide.

38/ RED III is the European Union's legal framework on renewable energy use, covering, for example, setting renewable energy targets the EU must meet, specifying the types of feedstock that must be used to produce biofuels, and banning agricultural feedstocks from biofuel production for the EU market (e.g. sugarcane, soybean, and palm, because of their impact on forests and land-use change)

39/ A special European Union regulation requiring airlines to blend SAF (Sustainable Aviation Fuel) into jet fuel at shares set for each year, and specifying the feedstocks allowed for making SAF