Executive Summary

Thailand has recently been described by some media outlets as the “Sick Man of Asia,” amid concerns over its subdued and below-potential economic growth relative to several countries in the region. However, Thailand’s current economic context differs markedly from that of the Philippines, widely labeled the “Sick Man of Asia” in the 1980s. During that period, the Philippines economy resembled a body so severely afflicted that it was unable to move due to deep-rooted “structural failures”. In contrast, Thailand’s economy remains in motion despite “structural weakness” and continues to be supported by considerably stronger macroeconomic fundamentals. However, Thailand faces its own distinct challenge in the form of rapid population aging, which further constrains the time and resources available for structural transformation. Drawing lessons from the Philippines experience, improving the quality of economic policy, strengthening governance, and building upon existing strengths will help promote investment in high-productivity and innovation-driven sectors. These are critical factors in facilitating the transition toward new engines of growth and mitigating structural risks.

At this juncture, while the country still retains economic potential and sufficient policy space, serious, systematic, and sustained structural reform will be essential to prevent Thailand from drifting toward a “Sick Man” trajectory, as illustrated by the experience of the Philippines.

Introduction

The term "Sick Man of Asia" originated as a reference to the Philippines during the 1980s under the administration of President Ferdinand Marcos, a period when the Philippines economy faced a severe debt crisis and a deep economic recession. Currently, this term has resurfaced in some discussions to describe Thailand, amid economic growth that has been weaker than ASEAN peers. Although Thailand's current economic context differs from that of the Philippines during that era, its persistent growth below potential—particularly in the post-COVID-19 period—may reflect long-standing, accumulated structural issues.

Therefore, drawing lessons from the Philippines case is important, as it helps illuminate shared vulnerabilities that could become obstacles to the long-term growth of the Thai economy. This article aims to analyze economic developments, specifically the root causes of the issues during the period when the Philippines was labeled the "Sick Man of Asia," and compare them with Thailand’s economic context since the post-COVID-19. The analysis focuses on structural factors and offers policy suggestions conducive to elevating Thailand's growth trajectory.

Causes of the Philippines Economic Crisis Preceding the “Sick Man of Asia” Era

The Philippines fell into the status of the "Sick Man of Asia" throughout the 1980–1989 period, amid structural problems that had accumulated over many years. These issues were fundamentally rooted in the 1970s, during which President Ferdinand Marcos declared martial law and institutionalized a patronage economy. When confronted with both external and domestic shocks, these structural weaknesses culminated in a debt crisis in 1983.

External triggers included the second oil crisis of 1979–1980, a significant decline in the prices of key commodity exports, including sugar and coconut decreased, the global economic recession, and the Mexican debt crisis of the early 1980s that caused sudden stops in capital flows to developing countries.

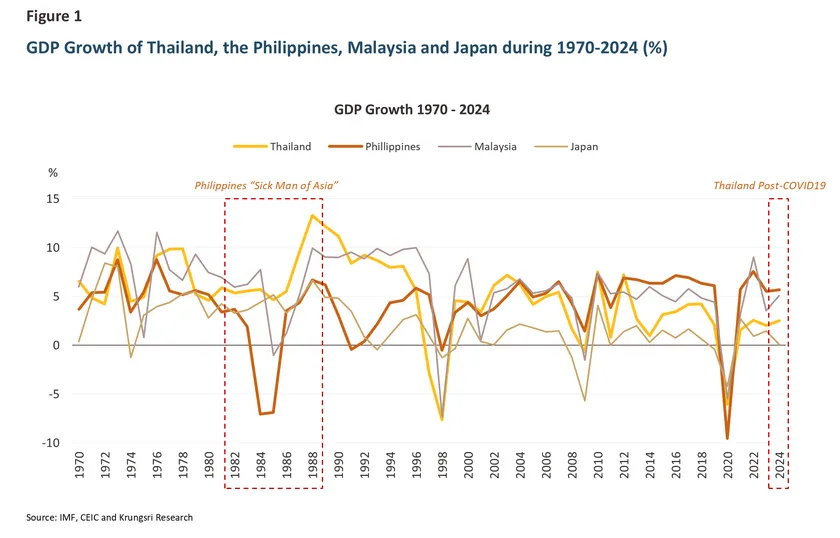

On the domestic front, the assassination of opposition leader Benigno S. Aquino Jr. in August 1983 undermined both domestic and international investor confidence. This led to massive capital outflows and the government’s subsequent debt default in October of the same year. Consequently, the Philippine economy contracted during 1984–1985 (Figure 1) and entered a protracted recession, solidifying its reputation as the "Sick Man of Asia."

The structural problems of the Philippines can be summarized into two key aspects:

-

First, crony capitalism: Government under the Marcos administration led to distorted resource allocation and caused a decline in the country's Total Factor Productivity (TFP) between 1981 and 1987 (Cororaton and Caesar B., 2002). The regime facilitated rent-seeking behavior by granting monopoly rights in major industries, such as sugar and coconut, to politically connected associates and state-owned enterprises to drive large-scale industrial projects disregarding of economic viability. Consequently, this resulted in chronic losses and became a significant fiscal burden (Dohner and Intal, Jr., 1989).

-

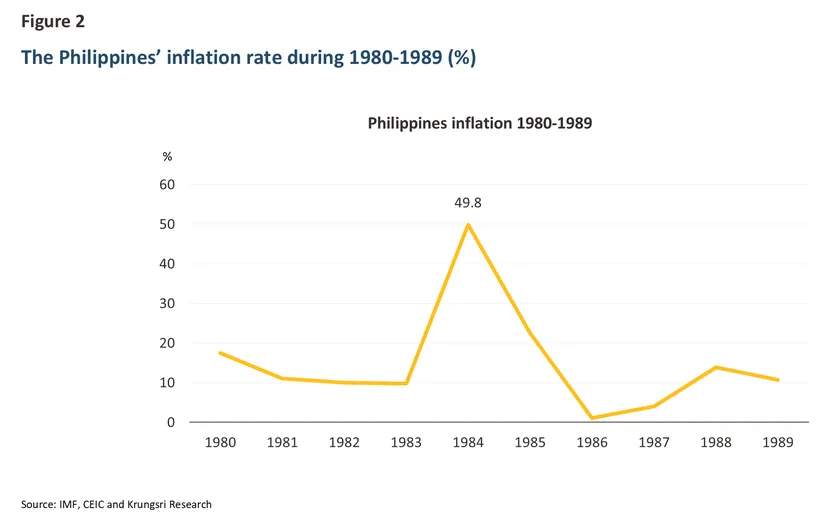

Second, policy mismanagement: The government maintained an overvalued Peso exchange rate—misaligned with fundamentals—to support domestic industries under the Import Substitution Industrialization (ISI) strategy. Concurrently, the Philippines exhibited significant vulnerability due to high external debt, particularly short-term obligations, which accounted for nearly 50% of total external debt in 1982 (Dohner and Intal, Jr., 1989). In the aftermath of the Mexican debt crisis, the Philippines faced a sudden stop in capital inflows and sudden capital outflows, leading to the country’s Balance of Payment crisis. Furthermore, government policy missteps continued by allowing the monetary base to expand by 44% in 1983 (Canlas, 2012). This fueled a surge in inflation, which reached 49.8% the following year, further deepening economic imbalances (Figure 2). As the economy entered a recession, commercial banks that had already accumulated vulnerabilities from their high reliance on foreign funding recorded elevated levels of non-performing loans (NPLs), leading to the insolvency of several financial institutions1/ (Tadem, 2018)

The Philippines’ experience shows how persistent structural issues can escalate into an economic crisis when triggered by an adverse shock. Following the debt crisis, the country underwent debt restructuring and economic reform programs under the framework of the International Monetary Fund (IMF). The severity of the crisis undermined the economy’s growth foundations for decades, and the Philippines continued to be labeled the “Sick Man of Asia” until the early 2000s, where economic recovery began gradually thereafter, with the economy achieving an average growth rate of 6.4% between 2010 and 2019. This rebound reflected anti-corruption initiatives, fiscal and financial sector reforms, and sustained productivity-enhancing efforts after President Ferdinand Marcos Sr. left office in 1986.

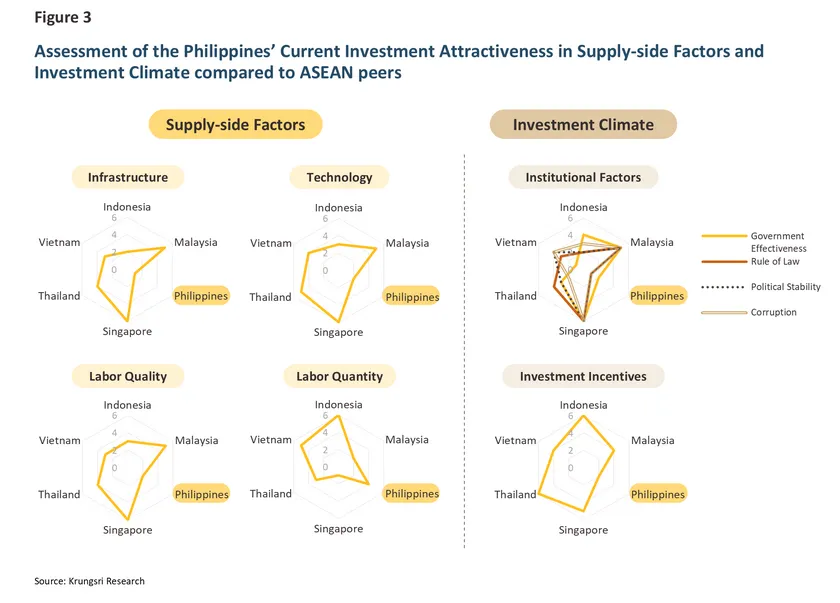

Although the Philippines was able to restructure its economy and restore confidence, recovering from the “Sick Man of Asia”, its current competitiveness remains below than that of other countries in the region (Figure 3). In particular, qualitative factors—such as infrastructure, technology level, labor quality, and institutional factors—continue to weigh on growth momentum. This situation reflects how the legacy of past economic crises remains one of a constraints on enhancing the Philippines’ growth potential at present.

Differences Context Between the Philippines’ “Sick Man of Asia” Then, and Thailand Now

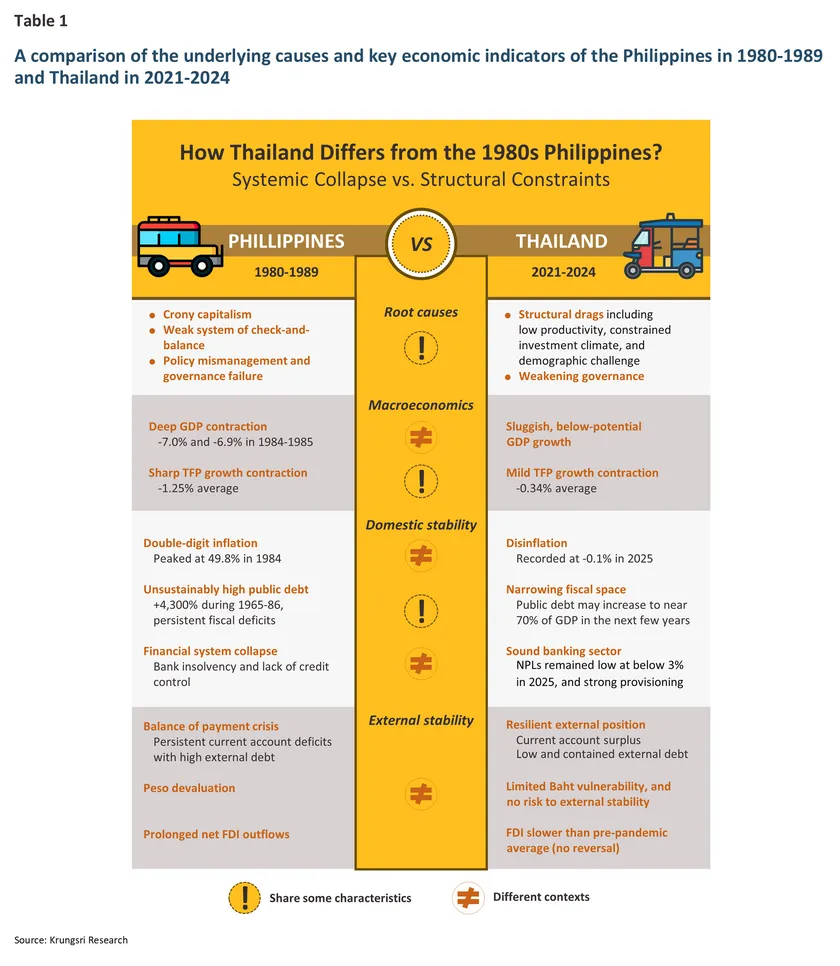

At present, although the Thai economy faces growth below its potential and at a pace slower than that of other countries in the region, the nature of its challenges differs markedly from those experienced by the Philippines in the 1980s. These differences can be categorized across macroeconomic indicators, domestic stability, external stability, and the underlying causes of the problems, as summarized in Table 1.

- Macroeconomics and Domestic Stability

Following the 1983 economic crisis, the Philippines economy experienced a prolonged recession and entered the “Sick Man of Asia” period, during which private investment contracted and foreign capital exited sharply. In contrast, both domestic and foreign investment in Thailand have continued to expand, albeit at a low level. Domestic economic stability also differed significantly. During that period, the Philippines faced high inflation and a fragile financial sector, whereas Thailand currently operates in a low-inflation environment with a sound commercial banking system. Nevertheless, Thailand faces some risks to domestic stability in the household debt of nearly 90% of GDP, which weighs on private consumption.

On the fiscal front, the Philippines government ran persistent fiscal deficits driven by large non-revenue-generating projects, ultimately leading to external debt default. In Thailand’s case, the country is not confronting fiscal crisis, however, fiscal space has been narrowed down due to revenue constraints and long-term obligations associated with an aging population, reflecting a degree of structural vulnerability.

The most pronounced difference lies in external stability. In the 1980s, the Philippines relied heavily on foreign capital, particularly short-term debt, and experienced a balance-of-payments crisis, which led to a sharp depreciation of the Peso. In contrast, Thailand currently maintains a continued current account surplus, with the Baht largely moving in line with global financial market conditions.

- Root Causes of the “Sick Man of Asia”

The causes underlying the Philippines’ economic crisis in the 1980s and Thailand’s current economic weakness may appear largely different, but they share some common characteristics. In the case of the Philippines, the concentration of political power during the presidency of Ferdinand Marcos led to the absence of effective check-and-balance in economic policymaking, resulting in entrenched corruption and a deeply rooted crony capitalism. Thailand, by contrast, continues to maintain a degree of check- and-balance system. However, it shares certain similarities in that regulatory frameworks tend to favor incumbent firms, posing barriers to new entrants (TDRI, 2017). This is consistent with research by the Puey Ungphakorn Institute for Economic Research (PIER) in 2019, which found that Thailand’s economic system exhibits characteristics of economic rent-seeking2/ As a result, resources and skilled labor do not flow toward high-productivity and innovation-driven sectors but instead remain concentrated among established business groups.

Overall, the Philippines during its “Sick Man of Asia” period reflected a “structural failure” that culminated in economic crisis. Although Thailand has not faced such a crisis, it is experiencing “structural weakness”—particularly in institutional factors and the quality of economic policies—which shares some similarities with the Philippines case and constitutes a key structural factor constraining Thailand’s growth potential.

Thailand and the Risk of Becoming the New “Sick Man of Asia”

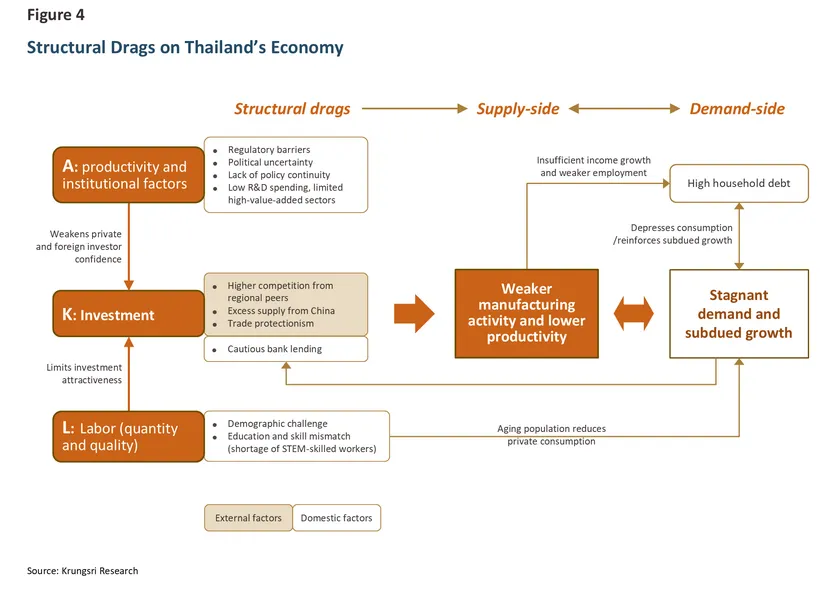

Although some media reports have referred to Thailand as the “Sick Man of Asia,” the preceding analysis suggests that Thailand’s economic challenges differ significantly from those of the Philippines. Nevertheless, Thailand’s below-potential economic growth over nearly the past decade underscores the need for a systematic examination of its underlying causes. This section therefore focuses on analyzing Thailand’s structural constraints from the supply side, which determine long-term growth potential. Specifically, it examines structural limitations across the key factors of production: Total Factor Productivity, institutional factors, and the quality of economic policies (A), capital and investment (K), and labor (L).3/ The main findings are summarized in Figure 4.

As illustrated above, Thailand’s structural limitations on the supply side can be summarized as follows:

-

Productivity, Institutional Factors, and Quality of Economic Policy: Research by TDRI (2017) indicates that uncompetitive regulatory frameworks, policy discontinuity, political uncertainty, as well as low levels of public investment in research and development and limited investment in high value-added manufacturing sectors, constitute major obstacles to enhancing Thailand’s productivity. These factors undermine investor confidence and weaken incentives for long-term investment.

-

Investment, Capital, and Capital Formation: Private sector investment decisions face pressures from both external and domestic factors, including intensifying competition from neighboring countries, excess supply from China, and rising global trade protectionism. At the same time, tighter lending standards based on stricter risk assessments may constrain access to financing. This, in turn, affects investment expansion and capital accumulation within the country.

-

Labor (Quantity and Quality): Thailand faces structural labor constraints in both quantitative and qualitative dimensions. Demographic aging is a significant challenge, alongside declining cost competitiveness in labor. Moreover, the country faces shortages of workers with skills aligned to the needs of the modern economy, particularly in science, technology, engineering, and mathematics (STEM) fields. These limitations constitute a key constraint on investment expansion and the transition toward higher value-added sectors (TDRI, 2017).

-

These structural drags are interconnected and generate a negative feedback loop within economic activity. Weak investment and labor constraints dampen production activity, leading to limited growth in income and employment. Combined with elevated household debt burdens, domestic demand remains subdued, which in turn further suppresses investment and production, reinforcing the cycle of economic weakness.

Is Thailand the Sick Man of Asia?

In comparison, the Philippines economy during its “Sick Man” period resembled a body struck by a sudden and severe illness—triggered by a crisis—leaving it unable to move. In contrast, Thailand’s economy today continues to expand, or at least remains “in motion,” as it is supported by much stronger macroeconomic fundamentals. These include greater financial stability, external economic stability, and a more resilient financial system. This distinction suggests that Thailand still possesses sufficient potential and resources to undertake structural reforms from its current position.

However, Thailand is experiencing a gradual “weakening” due to the accumulation of structural problems. This is compounded by additional challenges distinct from those faced by the Philippines in the past, which is the transition into an aging society amid existing constraints. This reflects a period in which the growth momentum generated by Thailand’s traditional economic model has begun to fade, while the transition toward new growth engines remains unclear. As a result, several economic indicators have shown signs of deceleration.

The key issue, therefore, is not whether Thailand should be labeled the “Sick Man of Asia,” but rather how to understand the structural constraints that are holding back the Thai economy and identify pathways to recalibrate and upgrade its growth model. The priority is to act while the country still has sufficient time and resources to do so, in order to break free from the cycle of low growth in the years ahead.

Krungsri Research View

In recent years, numerous policy proposals have put forward recommendations to address Thailand’s structural economic constraints. However, this article seeks to analyze and draw lessons from the Philippines experience during its economic crisis, and to compare those lessons with Thailand’s current economic context. While the two cases differ in terms of severity and the nature of their challenges, Thailand is facing structural pressures that are gradually eroding its growth potential.

The Philippines experience demonstrates that structural problems left unaddressed can eventually escalate into economic crisis, requiring a prolonged period of recovery before returning to previous levels.

Therefore, if Thailand seeks to avoid becoming a “Sick Man,” it must adopt comprehensive measures to strengthen its economic potential and prevent structural weakness from eroding long-term growth. Drawing on lessons from the Philippines experience, the following policy directions may be considered:

1. Addressing Structural Risks and Vulnerabilities

The Philippines experience highlights two key structural risks—some of which bear similarities to Thailand’s current situation—as follows:

-

First, the risk arising from regulatory and policy frameworks that are not conducive to competition: Although Thailand still maintains stronger governance standards and a more favorable investment climate than many countries in the region (Figure 4), there are signs that the quality of these factors may be beginning to deteriorate. For instance, Thailand’s 2026 Corruption Perceptions Index (CPI), which declined from the previous year4/ may reflect rising governance risks. The Philippines experience suggests that when rules and regulations lack transparency and fail to promote fair competition, resource allocation becomes distorted. As a result, investment tends to flow toward lower-productivity sectors, gradually accumulating structural fragilities that may ultimately lead to long-term economic risks.

-

Second, fiscal constraints: The Philippines experience illustrates how short-term, non-productive fiscal policies can become the starting point of long-term economic vulnerability. In Thailand’s case, the narrowing of fiscal space, partly due to rising future obligations, highlights the need for public spending to prioritize efficiency and long-term economic returns, rather than focusing solely on short-term stimulus measures.

2. Leveraging and Strengthening Thailand’s Existing Strengths

Although the Thai economy faces several structural constraints, it also retains notable structural strengths relative to other countries in the region. In particular, Thailand benefits from relatively well-developed infrastructure, including in energy, transportation, and digital connectivity.5/ Moreover, the country’s strategic geographic location positions it as a potential regional hub for economic connectivity and integration. Preserving and further enhancing these strengths can provide a solid foundation for upgrading Thailand’s future growth trajectory.

Moreover, Thailand’s difficulty in transitioning toward “new growth engines” characterized by higher value added and productivity represents a critical juncture commonly observed among countries caught in the middle-income trap. Since the 1990s, only 34 out of 108 middle-income economies have successfully advanced to high-income status (World Bank, 2024)6/ The common drivers of success among these countries include sustained investment in human capital and innovation, creating a competitive and enabling business environment, maintaining macroeconomic stability alongside fiscal discipline, and deepening integration into global value chains through trade and investment.

A key lesson is that these countries have maintained policy continuity and a long-term development vision that is not tied to the agenda or tenure of any single government.

However, Thailand faces its own unique challenge from rapidly entering an aging society, which further constrains the time and resources available for structural reform. At this critical juncture, when the country still retains economic potential and some remaining policy space, undertaking serious, systematic, and sustained structural reforms will be essential. Such efforts can help prevent Thailand from falling into an “aging and ailing” state and to enable it to overcome structural constraints in order to sustain its long-term growth potential.

Moreover, the earlier analysis indicates that Thailand’s key structural drags stem from weak productivity, institutional constraints, and the quality of economic policies. Strengthening these factors should therefore serve as a critical starting point for meaningful structural upgrading, because these are the fundamental conditions that enable a genuine.

Policy continuity, pro-competition regulatory frameworks, and stronger governance will together foster a more conducive investment climate in high-productivity and innovation-driven sectors. In turn, this will help boost investor confidence, unlock private sector potential, and reduce the risk that Thailand accumulates structural weakness that could eventually render it a “Sick Man,” as illustrated by the experience of the Philippines.

Boyce, J. K. (1993). The political economy of growth and impoverishment in the Marcos era. In The Philippines: The political economy of growth and impoverishment in the Marcos era. University of California Press. https://publishing.cdlib.org/ucpressebooks/view?docId=ft658007bk

Canlas, D. B. (2012). Monetary policy and economic growth in the Philippines [BSP-UP Professorial Chair Lecture Series]. Bangko Sentral ng Ng Pilipinas. https://www.bsp.gov.ph/Pages/ABOUT%20THE%20BANK/Events/By%20Year/2012/BSP-UP%20Professorial%20Chair%20Lecture%20Series/BSP_3a_canlas_paper.pdf

Committee for the Abolition of Illegitimate Debt (CADTM). (2019). The Philippine debt: A never-ending story. https://www.cadtm.org/The-Philippine-debt-a-never-ending-story

Dohner, R. S., & Intal, P., Jr. (1989). Debt crisis and adjustment. In J. D. Sachs & S. M. Collins (Eds.), Developing country debt and economic performance, volume 3: Country studies - Indonesia, Korea, Philippines, Turkey (pp. 524–558). National Bureau of Economic Research; University of Chicago Press. https://www.nber.org/system/files/chapters/c9053/c9053.pdf

Haggard, S. (1989). The political economy of the Philippine debt crisis. In J. D. Sachs (Ed.), Developing country debt and economic performance, volume 3: Country studies - Indonesia, Korea, Philippines, Turkey (pp. 415–460). National Bureau of Economic Research; University of Chicago Press. https://www.nber.org/system/files/chapters/c9047/c9047.pdf

Noland, M. (2000). How the sick man avoided pneumonia: The Philippines in the Asian financial crisis (Working Paper No. 00-5). Peterson Institute for International Economics. https://www.piie.com/publications/working-papers/how-sick-man-avoided-pneumonia-philippines-asian-financial-crisis

Poapongsakorn, N., Siamwalla, A., & Tangkitvanich, S. (2014). Chapter 1: Economic reform for reducing political conflict: Introduction and summary of findings. In Economic reform for social justice. Thailand Development Research Institute (TDRI).

Sicat, G. P. (n.d.). Philippine public finance in recent history. Philippine Social Science Council. https://pssc.org.ph/wp-content/pssc-archives/Works/Gerardo%20Sicat/Philippine%20public%20finance%20in%20recent%20history.pdf

Tadem, E. C. (2022). The Marcoses and the plunder of the Philippine economy. Europe Solidaire Sans Frontières. https://www.europe-solidaire.org/spip.php?article64009

Thailand Development Research Institute (TDRI). (2017). Synthesis report year 1: Growth and institution. https://tdri.or.th/wp-content/uploads/2017/06/Synthesis-Report-Year-1-Growth-and-Institution.pdf

The World Bank. (2024). World development report 2024: The middle-income trap. https://www.worldbank.org/en/publication/wdr2024

Warr, P. (2019). Long-term growth and poverty reduction in Thailand [Conference paper]. Puey Ungphakorn Institute for Economic Research. https://www.pier.or.th/files/conferences/2019/pier_symposium_2019_1_1_paper.pdf

1/ A total of 81 financial institutions collapsed between 1984 and 1985 (23 in 1984 and 58 in 1985), including Banco Filipino, the nation's largest savings bank, which ceased operations in July 1984. This crisis caused private sector credit to contract by 50% in real terms, as commercial banks shifted their portfolios toward government bonds rather than lending. This resulted in a severe liquidity crunch for the corporate sector, triggering widespread bankruptcies, particularly among industries within the import substitution sectors.

2/ Economic rent, or surplus returns, refers to returns accruing to owners of limited factors of production, or benefits derived from government policies that are granted only to

specific groups. Examples include gains from receiving exclusive concessions or export quotas, as such concessions and quotas are fixed in number (Poapongsakorn et al., 2014).

3/ The analysis is conducted within the framework of the Cobb–Douglas production function, which explains the relationship between economic growth and

the primary factors of production—capital (K) and labor (L)—under the assumption that growth depends on the level of technology or total factor productivity (A).

The model is typically expressed as Y=AKαLβ , where the coefficients represent the output elasticities of each respective input factor.

4/ In the 2026 Corruption Perceptions Index (CPI), Thailand’s score declined to 33 out of a possible 100, placing the country at 116th out of 182 economies worldwide. This represents Thailand’s lowest CPI score in 19 years, reflecting that governance remains a significant challenge to the country’s development.

5/ Read more: ASEAN’s Investment Appeals under Trump 2.0: Resilient or Vulnerable?

6/ Most of these countries are in Eastern Europe and East Asia, including South Korea, Taiwan, and Singapore.