Executive Summary

The EU's Packaging and Packaging Waste Regulation (PPWR) requires that any packaging placed on the EU market meet a series of conditions: it must be recyclable, contain a minimum share of recycled content, be free of hazardous substances, and carry standardized labeling. Some of these requirements take effect from August 12, 2026, and apply to all packaging sold in the EU market regardless of country of origin. As a result, the regulation will also affect Thai businesses exporting goods to the EU.

Thai products most likely to feel the impact fall into two groups: (i) packaging itself, particularly plastic packaging, and (ii) packaging-intensive products, particularly food and beverages, consumer goods, and electrical appliances and electronics. Businesses in these sectors are likely to face higher costs associated with redesigning packaging and preparing the technical documentation required to demonstrate compliance with the PPWR. At the same time, the regulation is expected to support long-term growth in circular economy sectors, particularly recycled plastics, bioplastics, businesses adopting sustainable packaging, and recycling-related businesses.

Understanding PPWR: A New Rule Pushing Businesses Toward Eco-Friendly Packaging

The Packaging and Packaging Waste Regulation (PPWR) forms part of the EU's Circular Economy Action Plan, which aims to shift production and consumption away from a “single-use” model toward a “circular economy.” As a dedicated packaging regulation, PPWR requires that packaging placed on the EU market be recyclable, contain a specified share of recycled plastic content, and be free of hazardous substances, among other conditions. It applies to all packaging sold in the EU regardless of where it is manufactured or exported from, which is why PPWR also affects Thai businesses exporting to the EU.

Key Requirements

PPWR's main substantive requirements include the following:

-

Recyclability: PPWR assesses "How well was this packaging designed to be recycled?" Packaging placed on the EU market must meet minimum recyclability requirements, with the standards becoming more stringent over time. During Phase 1 (2030–2037), packaging must achieve at least Grade C recyclability, meaning that at least 70% of the packaging by weight is recyclable. In Phase 2 (from 2038 onward), the minimum requirement rises to Grade B, or at least 80% recyclable. Recyclability also affects the fees charged under Extended Producer Responsibility (EPR)1/, which are paid by the entity that first places the packaging on the EU market. Packaging achieving Grade A recyclability, with at least 95% recyclability, will be subject to the lowest EPR fees (Table 1).

-

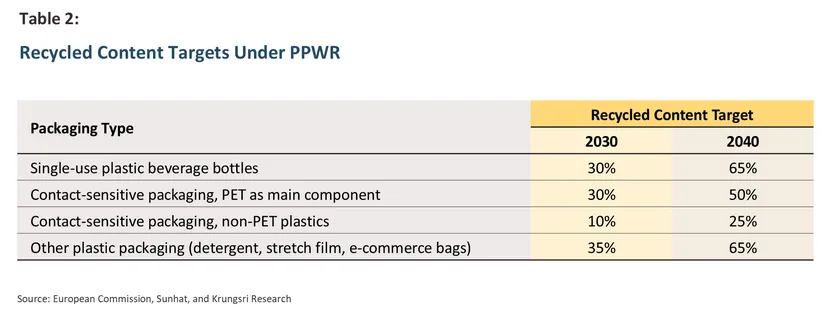

Recycled Content: PPWR asks “How much recycled material is used in this plastic packaging?” From 2030–2039, plastic packaging sold in the EU must contain 10–35% recycled content depending on packaging type. The requirement increases to 25–65% from 2040 onward. Contact-sensitive packaging made from plastics other than polyethylene terephthalate (PET) is subject to a lower requirement of 10–25% (Table 2). Certain packaging types are exempt from the recycled content requirement altogether, including food-contact packaging where health risks are a concern, packaging for medicines and medical devices, biodegradable plastic packaging, and packaging in which plastic accounts for less than 5% of total weight. Crucially, PPWR only recognizes recycled plastic sourced from post-consumer waste (Post-consumer Recycled: PCR) and does not allow manufacturing offcuts (Post-industrial Recycled: PIR) to count. This reflects the regulation's objective of reducing post-consumer waste, which currently has a much lower recycling rate than industrial scrap.

-

EU-wide harmonized labelling: PPWR sets out labelling requirements for packaging. By August 12, 2028, for example, all packaging must carry a label clearly identifying material composition to help consumers sort waste correctly. Alongside physical labels, packaging may also carry digital labels such as QR codes. In addition, by February 12, 2029, reusable packaging must be labelled to indicate its reusability along with return-point information accessible via QR code.

-

Restrictions on substances of concern (SoC): PPWR restricts substances of concern in packaging, particularly “forever chemicals,” or per- and polyfluoroalkyl substances (PFAS), which are heat-resistant, non-stick, and slow to degrade2/. These properties also make them an obstacle to recycling. From August 12, 2026, food-contact packaging must not exceed specified PFAS limits. Limits for other SoCs have not yet been finalized, but manufacturers must demonstrate that SoC levels have been reduced as far as reasonably possible.

Other obligations include minimizing packaging, reducing empty space within packaging, enabling packaging reuse, and banning certain packaging formats such as lightweight single-use plastic bags, except those used for loose fresh fruit and vegetables.

Enforcement

Implementation Timeline

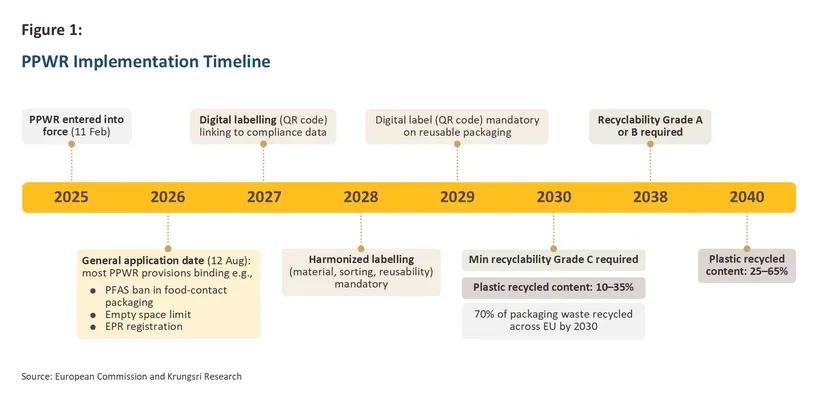

PPWR entered into force on February 11, 2025, and the EU will begin applying some of its provisions from August 12, 2026, including the restriction on forever chemicals (PFAS) in food-contact packaging and the minimum empty-space requirement. Labelling obligations follow in 2027–2029, while from 2030 onward the EU will begin enforcing the headline requirements like recyclability and recycled plastic content, which will tighten progressively over time (Figure 1).

Packaging in Scope

PPWR applies to all packaging placed on the EU market, regardless of whether it is produced inside or outside the EU. This includes packaging made of plastic, paper, metal, glass, wood, textiles, and ceramics, and covers both filled and empty packaging. Packaging within scope is divided into three levels (Figure 2):

-

Primary packaging / Sales packaging: Packaging that comes into direct contact with the product and is what consumers see on the shelf, also known as retail packaging, for example, bottles, boxes, and bags.

-

Secondary packaging / Grouped packaging: Packaging that groups multiple units together, such as shrink film around a pack of water bottles or a combined carton.

-

Tertiary packaging / Transport packaging: Packaging used for shipping goods, such as parcel boxes, pallets, and stretch film, including e-commerce packaging used to ship goods purchased online.

Who Must Comply with PPWR

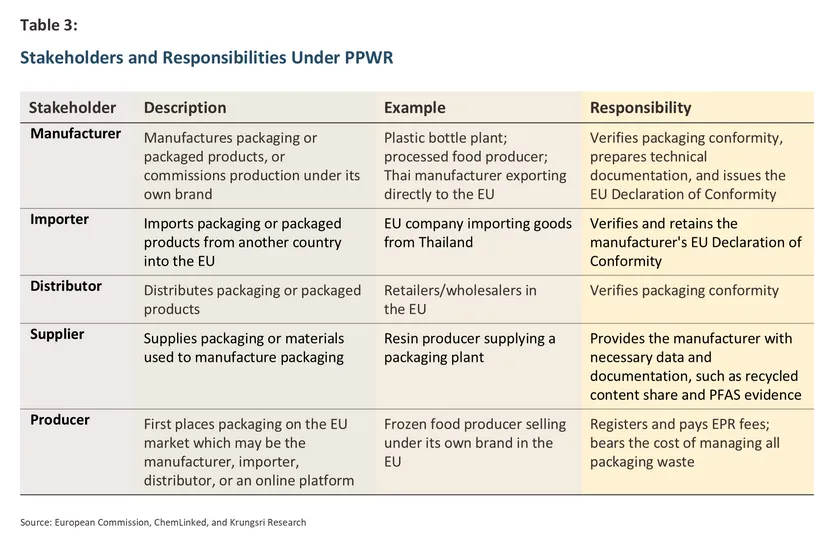

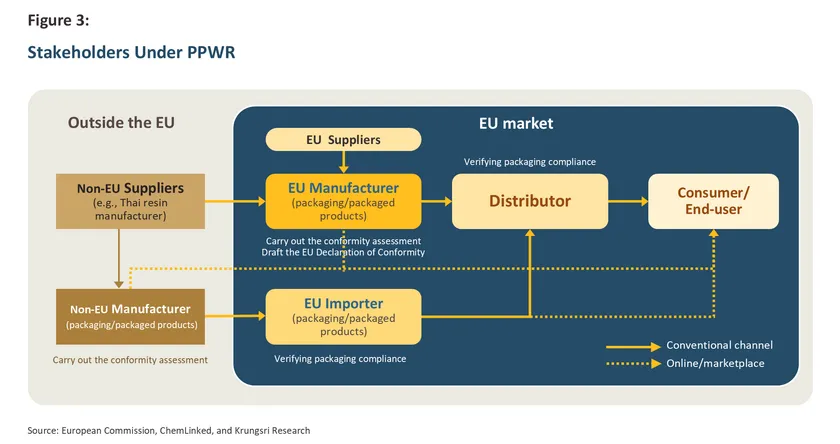

PPWR assigns obligations to stakeholders across the supply chain, including manufacturers, importers, distributors, and suppliers (Table 3). Notably, the regulation distinguishes the role of ‘the manufacturer’ from that of ‘the producer.’ The manufacturer of packaging or packaged products is responsible for ensuring the packaging's design complies with PPWR requirements, including preparing an EU Declaration of Conformity and other technical documentation. The producer, or the entity that first places packaging on the EU market, who may be the manufacturer, importer, or distributor, is instead responsible for fees associated with managing packaging waste under the principle of Extended Producer Responsibility (EPR).

The Impact of PPWR on Thai Businesses

Overall Impact

PPWR affects Thai businesses trading with the EU, whether as manufacturers, distributors, or exporters, across two main groups: (i) packaging itself, and (ii) packaged products, spanning virtually every industry. These businesses are likely to face the following effects:

-

Higher cost of doing business (compliance is achievable, but may come at a higher cost): PPWR creates two broad categories of costs for Thai businesses. The first is packaging transformation costs, including increasing the share of recycled plastic content, which generally costs more than virgin plastic; redesigning packaging to meet recyclability requirements; and producing new labels with the required information. The second is compliance costs, covering conformity assessments, preparation of technical documentation, establishment of traceability systems, third-party verification, and payment of EPR fees.

-

Possible erosion of trade competitiveness (failure to comply may mean losing market share): Some observers may view PPWR as a non-tariff measure (NTM), as businesses unable to meet its requirements may be unable to export goods to the EU—Thailand's fourth-largest export market after ASEAN, the U.S., and China. Over the longer term, businesses that fail to comply may also be excluded from supply chains in both the EU and other markets, as buyers switch to alternative suppliers whose packaging already meets the required standards. At the same time, similar packaging regulations are being adopted by other trading partners, including the UK, South Korea, and Japan. PPWR may also indirectly affect Thai packaging manufacturers that export to countries which subsequently export goods to the EU3/. As a result, Thai businesses could lose competitiveness not only in the EU market but also across multiple export markets simultaneously.

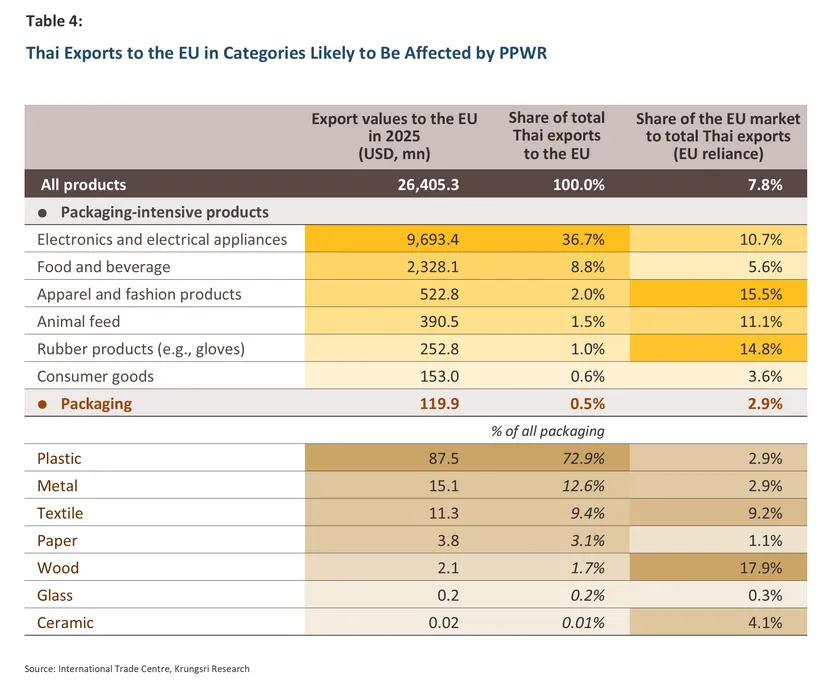

This raises the natural follow-up question: just how large is PPWR's impact on Thai industry likely to be? Krungsri Research has estimated the scale of impact based on the export value of two main product groups: packaging itself, and packaging-intensive goods (Table 4).

-

Packaging is the group most directly exposed. In 2025, Thailand exported USD 119.9 million worth of packaging to the EU, equivalent to 0.5% of total Thai exports to the EU, of which 72.9% was plastic packaging, followed by metal, textile, and paper. While packaging exporters as a whole have relatively low reliance on the EU market (2.9% of total exports), certain packaging categories are much more dependent on EU demand, particularly wood (17.9%) and textiles (9.2%). Beyond this, Thailand's USD 4.0 billion in packaging exports to markets outside the EU is also exposed to indirect effects, as manufacturers in those markets may opt for higher-standard packaging in order to trade with the EU.

-

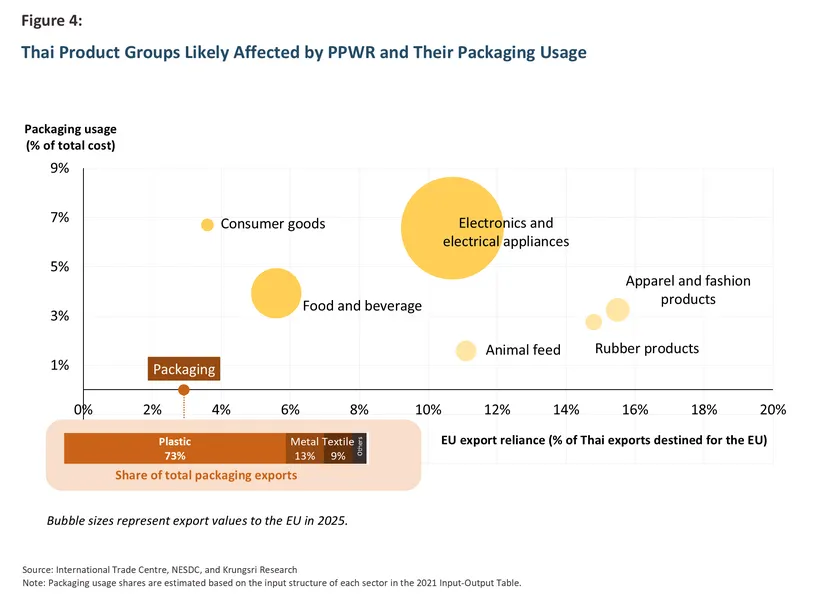

Packaging-intensive goods are products where export value and the share of packaging in total cost are both relatively high. These are mostly fast-moving consumer goods (FMCG) together with durable goods such as electrical appliances and electronics, as follows (Figure 4):

-

Food and beverages are generally packaging-intensive. Thailand exported a combined USD 2.3 billion of these products to the EU in 2025, or 8.8% of total exports to the EU, with top items including processed chicken, rice, processed fruit, sauces and seasonings, and instant noodles.

-

Other consumer goods, including pharmaceuticals, cleaning products, and cosmetics, account for just USD 153 million in exports, but carry the highest packaging cost share of any group, averaging around 7% of total production cost.

-

Electrical appliances and electronics such as computers, mobile phones, and air conditioners make up Thailand's largest export category to the EU by value, with the EU accounting for 10.7% of this group's total exports. These products have a longer service life than FMCG and so generate packaging waste less frequently per unit sold; however, most use multiple layers of packaging, including cardboard, plastic, and protective foam—which can generate a relatively large volume of packaging waste per purchase.

In summary, Thai exports with high direct exposure to PPWR total an estimated USD 13.5 billion (approximately THB 440 billion) per year, equivalent to around half (51%) of Thailand's total exports to the EU. In addition, Thailand's USD 4.0 billion (approximately THB 130 billion) in packaging exports to non-EU markets may also be indirectly affected.

Sector-by-Sector Impact

This section analyzes the sectors most likely to be significantly affected: packaging, particularly plastic packaging, and exporters of packaged products, particularly food and beverages, other consumer goods, and electrical appliances and electronics.

Plastics and Plastic Packaging

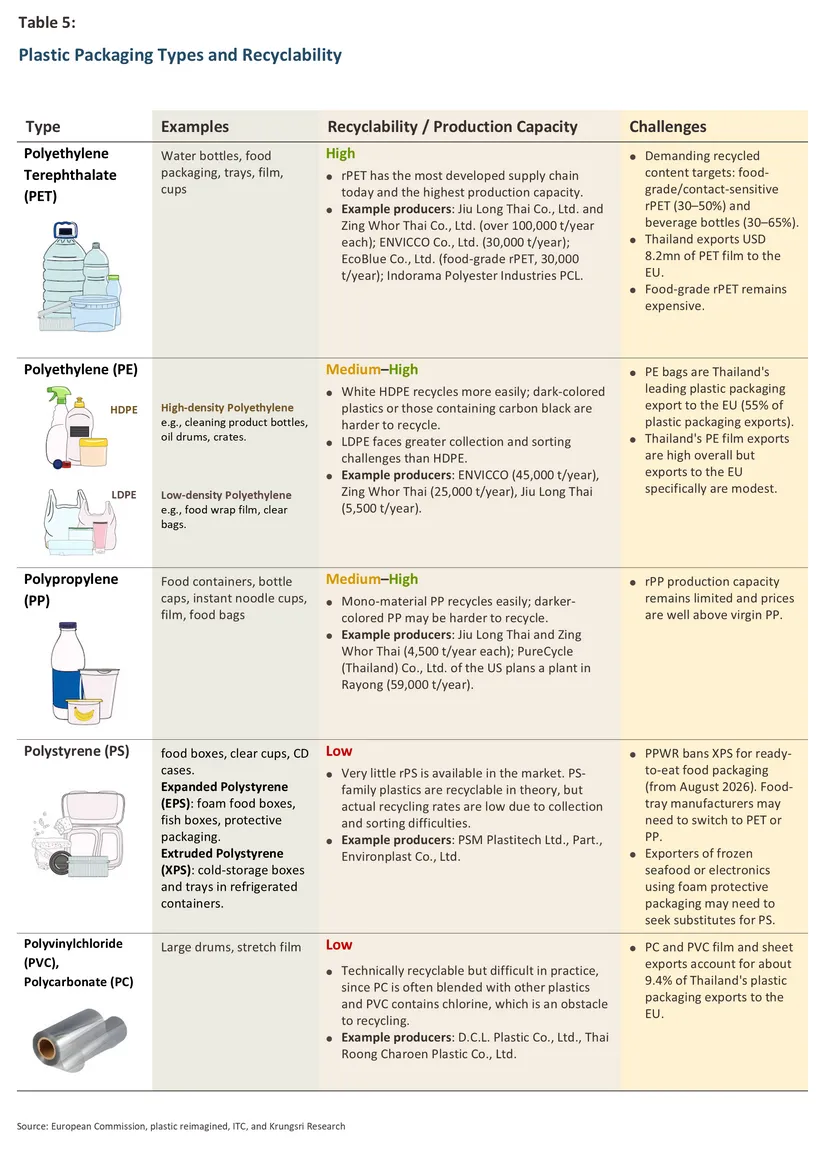

The plastics and plastic packaging industry is the segment most directly and most severely affected by PPWR, since plastic is both the most widely used packaging material and Thailand's largest packaging export. In 2025, Thailand exported USD 87.5 million worth of plastic packaging to the EU, of which more than two-thirds, or USD 57.2 million, was finished plastic packaging products (HS 3923), led by polyethylene (PE) bags such as carrier bags, which are also Thailand's largest plastic packaging export to the world. The next-largest category is plastic film and sheet (HS 3920), with USD 22.8 million in EU exports, particularly products made from polyethylene terephthalate (PET), polycarbonate (PC), and polyvinyl chloride (PVC) resins. In the near term, on top of feedstock shortages stemming from tensions in the Middle East, Thai plastic packaging manufacturers are likely to face rising costs from technical verification such as proving recyclability and recycled content share for customers in Thailand, the EU, and elsewhere. Failure to provide this data, or packaging that fails to meet PPWR criteria, could undermine these manufacturers' ability to compete.

Over the medium to long term, manufacturers of conventional fossil-fuel-based plastic (virgin plastic) may see some erosion in demand, while demand for recycled plastic is expected to rise. However, recycled plastic still faces significant challenges from limited supply and higher prices than virgin plastic. In 20254/, food-grade recycled PET (rPET) in Asian markets traded at a premium of roughly USD 300–500 per tonne over virgin PET5/. Other high-quality recycled plastics, including recycled high-density polyethylene (rHDPE), recycled low-density polyethylene (rLDPE), and recycled polypropylene (rPP), also generally command a premium over their virgin counterparts6/. Domestic supply of recycled plastic remains limited. Thailand produces approximately 9 million tonnes of plastic resin annually, about half of which is consumed domestically. This generates more than 2.7 million tonnes of plastic waste each year, of which only around 25% is recycled7/. As a result, Thailand's total domestic recycled-plastic production capacity is estimated at no more than 1 million tonnes per year, with rPET accounting for the largest share (Table 5).

Non-Plastic Packaging

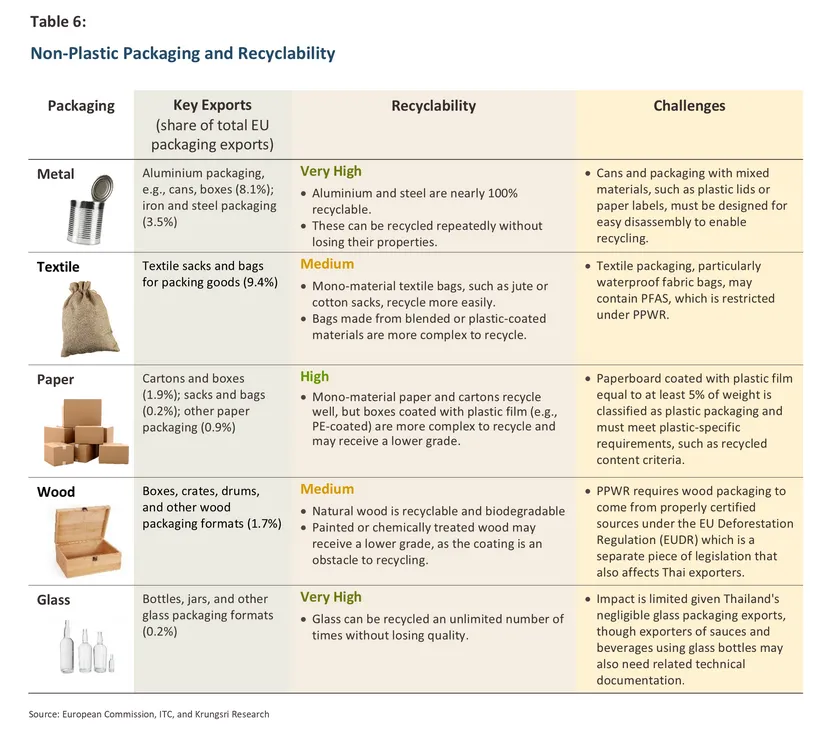

Beyond plastic, Thailand's largest non-plastic packaging export to the EU is metal packaging, particularly aluminium, followed by textile, paper, and wood packaging, while glass packaging exports to the EU are negligible (Table 6). Combined, non-plastic packaging exports to the EU total just USD 32.4 million, accounting for 27.1% of total Thai packaging exports to the EU, far smaller than plastic packaging. Overall, non-plastic packaging has high recyclability, particularly metal and glass, which can be recycled repeatedly without significant loss of material properties. This group of packaging materials is therefore likely to feel less impact from PPWR than plastic and may even benefit from businesses seeking to reduce plastic use. For example, food manufacturers may increasingly switch to metal, glass, or paper packaging to avoid plastic-specific requirements or the high cost of food-grade recycled PET (rPET).

That said, manufacturers of non-plastic packaging may face their own challenges, particularly in designing multi-material packaging to meet PPWR recyclability criteria. Examples include metal cans with plastic lids, paper packaging coated with plastic film, and fabric bags made from blended fibers or coated with plastic. In addition, paper and wood packaging may face further traceability requirements under the EU Deforestation Regulation (EUDR)8/.

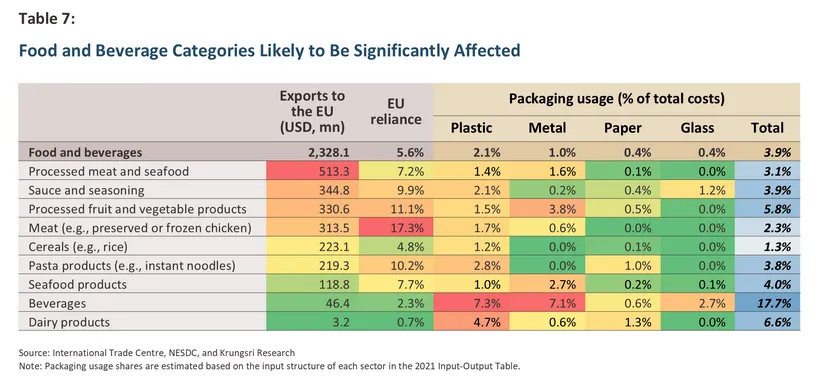

Food and Beverages

The food and beverage industry is likely to face significant impact given how packaging-intensive it is. In 2025, Thailand exported a combined USD 2.3 billion of these products to the EU, or 8.8% of total Thai exports to the EU. Products warranting particular attention are processed meat and seafood, sauces and seasonings, processed fruit and vegetables, and meat, which together account for roughly two-thirds of total Thai food and beverage exports to the EU (Table 7). These categories also rely heavily on the EU market, notably meat (such as chilled or frozen chicken), where EU reliance reaches 17.3%, and processed fruit and vegetables, at 11.1%. They are also packaging-intensive, particularly processed fruit and vegetables (such as canned fruit in metal tins) and sauces and seasonings (plastic or glass bottles).

Pasta products (such as instant noodles) rank next by export value, with EU reliance of 10.2% and plastic accounting for 2.8% of total cost (such as sachets or instant-noodle cups). The beverage industry, meanwhile, is also likely to face significant pressure. Although EU exports total only USD 46 million, beverages carry the highest total packaging cost share of any food and beverage category at over 17.7% of total cost, comprising plastic (7.3%), metal (7.1%), and glass (2.7%). Plastic beverage bottles also face one of the most demanding recycled content targets under PPWR, rising to 65% by 2040.

In addition, food and beverage packaging may be subject to further requirements, such as the PFAS restriction and the ban on XPS foam for ready-to-eat food. That said, food-contact plastic packaging may be exempt from the recycled content requirement if using recycled material would pose a health risk, or in the case of packaging for medical-purpose foods and infant formula.

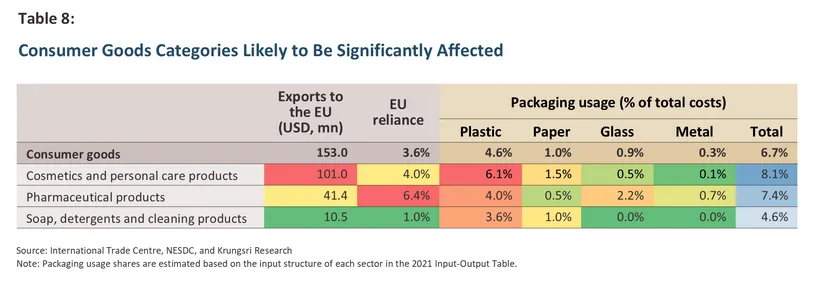

Other Consumer Goods

Although Thai exports of cosmetics, pharmaceuticals, and cleaning products to the EU together account for just 0.6% of total Thai exports to the EU, this group carries the highest average packaging cost share of any category at 6.7% of total cost, most of it from plastic (4.6%). The product warranting closest attention is cosmetics and personal care, with USD 101 million in exports and a packaging cost share of 8.1% (Table 8), of which 6.1 percentage points is plastic, mainly bottles and tubes. Cosmetics packaging also commonly combines multiple materials (multi-layer/composite packaging), such as squeeze tubes with both plastic and aluminium layers, or cartons coated with plastic film, adding to recycling complexity. That said, contact-sensitive packaging benefits from a lower recycled content requirement. If made from non-PET plastics, it is required to contain only 10% recycled content by 2030, well below the threshold for most other plastic packaging.

Pharmaceuticals rank second by export value but show the highest EU reliance in the group at 6.4%, and rely more heavily on glass packaging than other categories. While packaging for medicines and medical devices is exempt from the recycled content requirement on safety grounds, it must still fully comply with PPWR's other requirements. Cleaning products such as soap and detergent have the lowest export value and EU reliance in the group, but still rely on plastic for 3.6% of cost (such as HDPE cleaning-product bottles) and will need to adapt packaging to PPWR standards in order to retain the EU market over the long run.

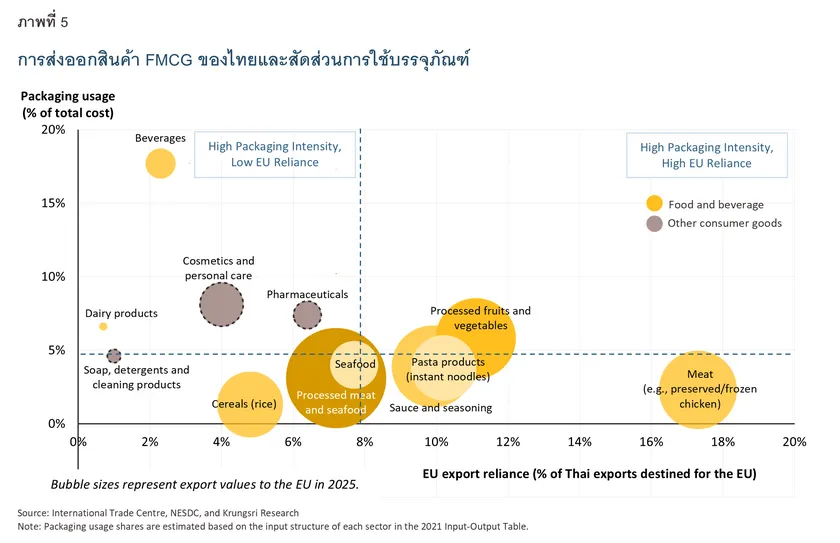

Taken together, FMCG products, including food, beverages, pharmaceuticals, and other consumer goods, are likely to face significant challenges from PPWR because they rely heavily on packaging and will therefore need to ensure it complies with EU standards. Weighing export value, EU reliance, and packaging intensity together, the FMCG categories Thailand should prioritize are: (i) processed fruit and vegetables, instant noodles, and seasonings, which score relatively high across export value, EU reliance, and packaging use; (ii) meat and processed meat, which have either very high export value or very high EU reliance; and (iii) beverages, cosmetics/personal care, and pharmaceuticals, which, while lower in export value, are the most packaging-intensive of all (Figure 5).

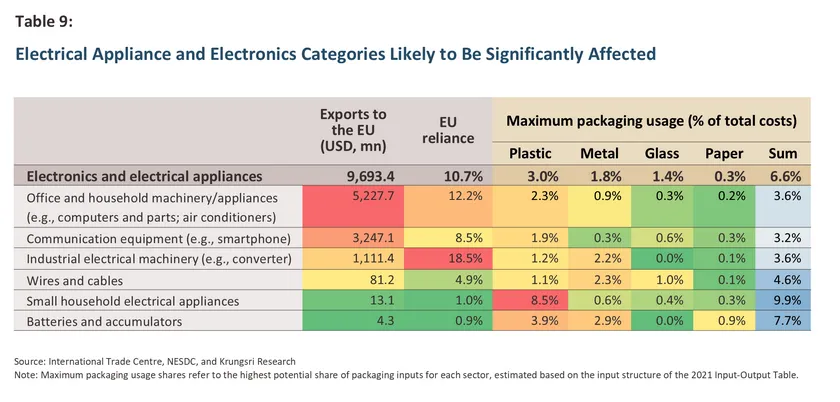

Electrical Appliances and Electronics

Electrical appliances and electronics make up Thailand's single largest export category to the EU by value, at USD 9.7 billion9/, or 36.7% of total Thai exports to that market. These are durable goods with a longer service life than FMCG, and so generate packaging waste less frequently per unit; however, packaging in this category typically combines cardboard, plastic, and protective foam, which can generate a relatively large volume of packaging waste per purchase. In addition, all electrical and electronic products that run on electricity or batteries also fall under the Waste Electrical and Electronic Equipment Directive (WEEE Directive)10/, meaning exporters in this category must comply with two circular-economy regulations simultaneously. PPWR covers the packaging, while WEEE covers the product itself and its end-of-life management.

Two groups warrant particular attention: (i) office/household electrical equipment and communication equipment, which together account for the largest EU export value in this category, at almost USD 8.5 billion or roughly 87.5% of the group, led by computers and parts, mobile phones, and air conditioners; and (ii) power converters, where Thailand's EU reliance reaches as high as 18.5% of total exports. These categories therefore carry significant risk of losing high-value export markets if their packaging fails to meet PPWR standards.

Beyond packaging manufacturers and producers of packaged goods discussed above, wholesale and retail businesses that aggregate goods or act as sourcing agents for EU importers are also likely to feel PPWR's effects. While these businesses are not directly responsible for packaging design since they do not manufacture the goods themselves, they will need to verify that the packaging of products they distribute carries complete PPWR conformity documentation before it enters the EU market. Such technical documentation is set to become an increasingly important requirement for doing business with the EU.

Businesses Likely to Benefit from PPWR

While PPWR will impose cost burdens on businesses and industry, it also opens opportunities for businesses aligned with the circular economy trend to grow over the long term. Key business groups likely to benefit include the following:

-

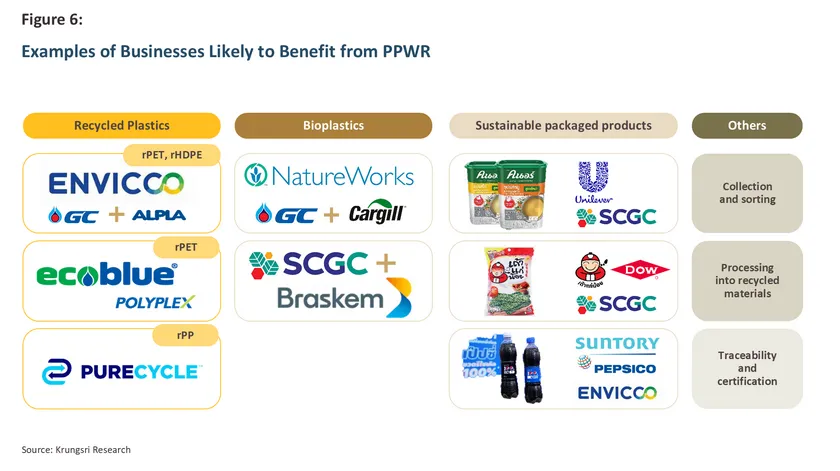

Recycled plastics industry: PPWR will help drive up demand for recycled plastic used in packaging production. Grand View Research expects the global recycled plastics market to be worth USD 60.8 billion in 2025, rising to USD 132.3 billion by 2033, an average annual growth rate of 10.4%. Large producers, both Thai and foreign, have steadily invested in recycled-plastic plants in Thailand, particularly for rPET, rHDPE, and rPP (Figure 6). Examples include ENVICCO Co., Ltd., a joint venture between PTT Global Chemical PCL (GC) and Austria's Alpla; EcoBlue Co., Ltd., part of the Polyplex (Thailand) PCL group (parent company based in India); and PureCycle (Thailand) Co., Ltd., a U.S. firm that has also received investment promotion support from Thailand's Board of Investment (BOI).

-

Bioplastics industry: The EU may also allow packaging made from bioplastics that are produced from natural feedstocks such as starch, sugar, straw, and sugarcane bagasse, as an alternative pathway to compliance alongside recycled plastic, with plans to set targets for bio-based feedstock use in plastic production by 2028. This is expected to lift demand for bioplastics further. Grand View Research projects the global bioplastics market will reach USD 67.4 billion by 2033, roughly half the size of the recycled plastics market, but growing faster, at an average of 17.6% per year between 2026 and 2033. Thailand has the potential to become a significant global production base for bioplastics, reflected in joint ventures between major Thai conglomerates and leading international partners building bioplastic plants in the country, including NatureWorks Asia Pacific Co., Ltd., a joint venture between GC and Cargill of the U.S. with 75,000 tonnes/year of capacity, and Braskem Siam Co., Ltd., a joint venture between SCG Chemicals (SCGC) and Brazil's Braskem, building a 200,000-tonne/year bio-ethylene plant11/ (a feedstock for bioplastic resin). That said, bioplastics still face a key challenge regarding production costs that can run roughly 1.5–4 times higher than fossil-fuel-based plastics12/.

-

Businesses adopting sustainable packaging: Businesses that upgrade their packaging to PPWR standards stand to gain an edge in the EU market. Thai businesses have grown increasingly active on the circular economy front, particularly food and beverage companies partnering with packaging manufacturers to develop recycled packaging. Examples include Unilever Thailand partnering with SCGC to develop recycled packaging for the Knorr brand13/; Taokaenoi Food & Marketing PCL partnering with SCGC and Dow Thailand to design seaweed snack packaging from recycled plastic14/; and Suntory PepsiCo Beverage (Thailand) Co., Ltd., which uses 100% rPET bottles produced by ENVICCO for its 550ml Pepsi beverage15/. These examples all reflect early preparation for PPWR-equivalent standards.

-

Recycling and support businesses: Businesses across the recycling supply chain, from collection and sorting, to scrap purchasing and wholesale, through to processing materials into feedstock for plastic, metal, glass, and paper packaging, stand to benefit from rising demand for recycled material. Opportunities also extend to small businesses, particularly in collection and sorting, which require less technology and capital investment, while processing into recycled feedstock requires more advanced technology and larger capital outlays, which has so far drawn investment mainly from large players. In addition, PPWR also opens opportunities for businesses providing traceability and certification services, since exporters of packaging and packaged products need technical documentation to demonstrate regulatory compliance. This includes verifying that recycled materials qualify as post-consumer recycled (PCR) and documenting their traceability throughout the supply chain. Providers in this space are becoming indispensable players in this new era of trade.

Krungsri Research View: How Should Businesses Respond to Seize the Circular Economy Opportunity?

Turning Challenge into Opportunity

PPWR is a sustainability regulation with sweeping reach, since virtually every product on the market involves packaging in some form. It is therefore a challenge that businesses producing or selling goods in any industry cannot avoid

. However, Krungsri Research believes that, over the long run, adapting to the EU's PPWR will benefit Thai businesses and the broader economy in several ways:

-

Businesses become better prepared for an expanding wave of circular economy regulation. Beyond the EU's PPWR, other countries are introducing their own sustainable packaging requirements. The UK has legislated to make businesses responsible for packaging waste management costs (Extended Producer Responsibility: EPR)16/, while South Korea and Japan have set minimum recycled content requirements for PET packaging, and China has issued national standards covering design for recycling. Thailand's own regulations are also trending stricter. The Pollution Control Department has drafted a Sustainable Packaging Management Act based on EPR principles, requiring producers to take responsibility for returning their packaging into the recycling system17/. This means businesses that adapt to PPWR's packaging requirements first will gain an advantage and face lower compliance costs when other regulations follow.

-

Businesses can capture the growth opportunity in the circular economy. Investment in Thailand's circular economy is trending upward. Applications for investment promotion in the Bio-Circular-Green (BCG) industry submitted to the BOI grew by an average of 21.7% per year between 2021 and 2025. Circular economy projects (Category C) alone accounted for over THB 400 billion in cumulative applications over that period, growing at an average of 47.2% per year, driven in part by recycled-resin manufacturers, recycled-pulp producers, and waste-processing plants. The government continues to support the BCG industry, while the current administration is advancing its ‘Green Economy Plus’ policy to promote environmentally friendly economic activity alongside sustainable growth. This suggests government policy and the pressure created by PPWR are moving in the same direction, opening opportunities for businesses ready to invest in the recycling supply chain and sustainable packaging.

-

Thailand may reduce reliance on imported feedstock and strengthen plastics supply chain resilience. Lessons from the recent resin shortage caused by conflict in the Middle East underscore the growing strategic role of recycled plastic. In the first half of 2026, the closure of the Strait of Hormuz left the petrochemical industry facing a shortage of crude oil and naphtha, the feedstock used to produce resin, driving resin prices up 40–75% in April compared with February, before the crisis began18/, which in turn pushed up domestic plastic packaging prices. Therefore, over the long run, relying on domestic feedstock and using recycled material in packaging production under PPWR not only meets trade requirements, but also helps mitigate the risks of feedstock insecurity and price volatility stemming from geopolitical uncertainty.

How Should Businesses Prepare?

Thai manufacturers and exporters selling into the EU market should prepare along three main fronts

(Redesign–Recheck–Review):

-

Redesign packaging to meet the standard: Businesses should assess their current packaging and adapt it to meet PPWR's recyclability and recycled content criteria, securing reliable sources of recycled material (PCR), updating labelling to the required standard, and screening for hazardous substances, among other steps. Packaging manufacturers and brand owners may also collaborate to develop sustainable packaging together, which would support the design of packaging that works in practice with real products and is accepted by consumers.

-

Recheck conformity and complete the documentation: Since PPWR requires technical evidence for every piece of packaging, businesses must prepare or verify conformity documentation, covering material composition and recycled content share, and may also need to register under the EU's EPR system or appoint an authorised representative, particularly for businesses selling directly to EU consumers online without an importer as intermediary.

-

Review and track regulatory developments on an ongoing basis: Businesses should monitor PPWR's technical details, which will be issued progressively through 2026–2028, particularly criteria for Design for Recyclability (DfR) and rules relating to bioplastics. Businesses must also track similar legislation in other export markets, such as the UK, South Korea, Japan, and China, as well as Thailand's own recycling-related laws.

Ultimately, PPWR is not the only piece of legislation Thai businesses must contend with, but one part of a broader, increasingly far-reaching wave of sustainability regulation sweeping the world. A single business may face requirements from multiple regulations at once, which tend to share a common thread: a focus on sustainability across every component and stage of business operations. Businesses should therefore move quickly to gather data and assess sustainability across their entire supply chain, building the readiness needed to turn these challenges into long-term opportunity.

References

European Commission. (2025). Waste from Electrical and Electronic Equipment (WEEE). Retrieved from https://environment.ec.europa.eu/topics/waste-and-recycling/waste-electrical-and-electronic-equipment-weee_en

European Commission. (2026). Annex to the Communication to the Commission. Retrieved from https://environment.ec.europa.eu/document/download/3d59ca88-539c-4b6b-a623-0f61068e853e_en?filename=Annex%20to%20the%20Communication%20to%20the%20Commission.pdf

European Union. (2025). Regulation (EU) 2025/40 of the European Parliament and of the Council on packaging and packaging waste (PPWR). Retrieved from https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=OJ:L_202500040

Grand View Research. (2024). Bioplastics market size and share | Industry report, 2025-2033. Retrieved from https://www.grandviewresearch.com/industry-analysis/bioplastics-industry

Grand View Research. (2024). Recycled plastics market size & share | Industry report, 2025-2033. Retrieved from https://www.grandviewresearch.com/industry-analysis/recycled-plastics-market

1/ Extended Producer Responsibility (EPR) is a system requiring whoever first places packaging on the EU market to bear the cost of managing that packaging's waste once consumers have used it. EPR fees are calculated as packaging weight multiplied by a fee rate that varies by material; PPWR further requires that EPR fee rates differ according to recyclability.

2/ PFAS are used across a range of industries, including food packaging, cosmetics, apparel, and cleaning products.

3/ Thailand exports most of its plastic packaging to the U.S., Japan, and ASEAN; businesses may face indirect effects since these countries will need PPWR-compliant packaging in order to trade with Europe.

4/ From 2025 into early 2026, resin feedstock remained in oversupply, keeping prices low, before tensions in the Middle East disrupted feedstock supply and pushed resin prices higher.

5/ Recycled Polymers | S&P Global | S&P Global

6/ Virgin vs. Recycled Plastics: Price Gaps in 2026 - Advanced Plastic Washing and Recycling Machinery | Ableplas

7/ Plastic Waste | Office of Natural Resources and Environmental Policy and Planning (ONEP)

8/ The EU Deforestation Regulation (EUDR) requires seven categories of traded goods—rubber, palm oil, cattle, wood, coffee, cocoa, and soy—to be verified and reported as deforestation-free. See further: EUDR: Ensuring exports to the EU are deforestation-free | Krungsri Research

9/ Focused on the consumer electronics and electrical appliances category.

10/ The WEEE Directive requires manufacturers and distributors of electrical and electronic equipment to bear the full cost of managing end-of-life products throughout their lifecycle, including collection, treatment, and recycling. The directive has been in force since 2012.

11/ BOI grants FastPass to Braskem Siam to accelerate investment in Asia's first bio-ethylene plant, due for completion in 2028 | PostToday

12/ PHA/PLA resin prices versus PP/PE in 2026 | THAIDA GLOBAL TRADE

13/ Unilever partners with SCGC to unlock recycled packaging innovation in the food industry, launching food-grade eco-friendly packaging for the ‘Knorr for Professionals’ brand under ISCC PLUS certification — a first in ASEAN | SCGC

14/ Taokaenoi, SCGC, and Dow showcase seaweed-pouch innovation using advanced recycling technology to give plastic waste new life | SCGC

15/ ENVICCO and Pepsi launch Thailand's first use of InnoEco PCR PET resin | GC

16/ From 2025, the UK requires producers, importers, and retailers to bear the cost of collecting, sorting, recycling, and disposing of all packaging, with fees adjusted according to recyclability (eco-modulation). Packaging that is harder to recycle attracts higher fees.

17/ Pollution Control Department unveils plan to push the packaging law, proposing a 1-baht-per-bottle scheme expected to cut waste by 20% | Bangkok Biz News

18/ PP, PE, and PS resin prices surge 40–75% amid the Hormuz crisis | PSM Plasitech