Executive Summary

Thailand has pledged a new Net Zero target for 2050, bringing the deadline forward by 15 years from its previous commitment, and aims to reduce net greenhouse gas (GHG) emissions by -47% by 2035 compared to 2019 levels. This compels every sector of the economy to accelerate its transition toward a low-carbon economy. The energy and transport sectors, as the country's largest sources of GHG emissions, must urgently shift toward renewable energy and electric vehicles. Meanwhile, industrial sectors such as cement, steel, and chemicals will face regulatory pressures from both domestic and international measures, requiring them to restructure production processes toward low-carbon products to remain competitive. To achieve this target, the government should accelerate progress on key legislation and policies, including the Climate Change Act, carbon pricing mechanisms, and incentives for green industry investment, while strengthening international cooperation on technology and financing. At the same time, businesses must urgently measure and manage their carbon footprints, set corporate Net Zero targets, and seize opportunities in sustainable businesses that can deliver long-term growth.

Net Zero 2050: Thailand's Ambitious New Milestone

At the 30th Conference of the Parties to the United Nations Framework Convention on Climate Change (COP30) in November 2025,

Thailand announced a net-zero greenhouse gas emissions target for 2050 (Net Zero 2050), bringing the timeline forward by 15 years from its previous commitment of 2065 (Net Zero 2065). This pledge aligns with global efforts to limit the rise in average global temperatures to no more than 1.5°C above pre-industrial levels (the 1.5°C pathway), as set out in the Paris Agreement in 2015.

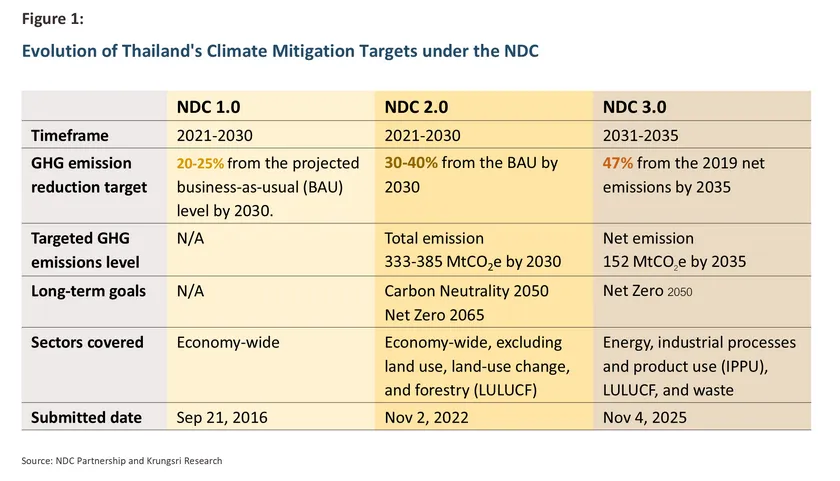

The Net Zero 2050 target forms part of Thailand's latest Nationally Determined Contribution (NDC), known as NDC 3.0, which provides the framework for reducing GHG emissions during the period 2031–2035, under the United Nations Framework Convention on Climate Change (UNFCCC) and the Paris Agreement mechanisms.

The targets set in NDC 3.0 are significantly more ambitious than in previous NDCs (Figure 1), with the following key elements:

-

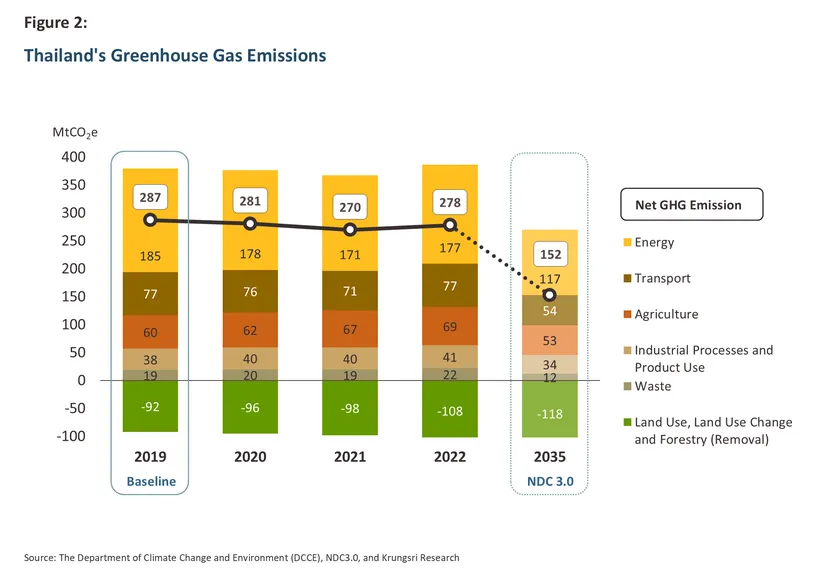

Reduce net GHG emissions by -47% by 2035 compared to 2019 levels—meaning Thailand aims to limit net GHG emissions to no more than 152 million tonnes of CO2 equivalent (MtCO2e) by 2035, nearly half the 287 MtCO2e recorded in 2019 (Figure 2). By 2050, Thailand must reach net-zero GHG emissions, with emissions from all sectors approximately equal to removals from land use, land-use change, and forestry (LULUCF).

-

Split the GHG reduction target into (1) domestic action (unconditional target), accounting for 70% of the target, and (2) international support (conditional target), for the remaining 30%.

-

Cover 5 sectors: energy (including transport), industrial processes and product use (IPPU), agriculture, waste, and land use, land-use change, and forestry (LULUCF).

This article analyzes the enabling factors and barriers to achieving Thailand's new Net Zero target, assesses which industries are likely to be most affected or to benefit from the transition to Net Zero, and ultimately offers a perspective on how Thailand can reach its Net Zero goal.

How Thailand’s Net Zero Target Compares Globally?

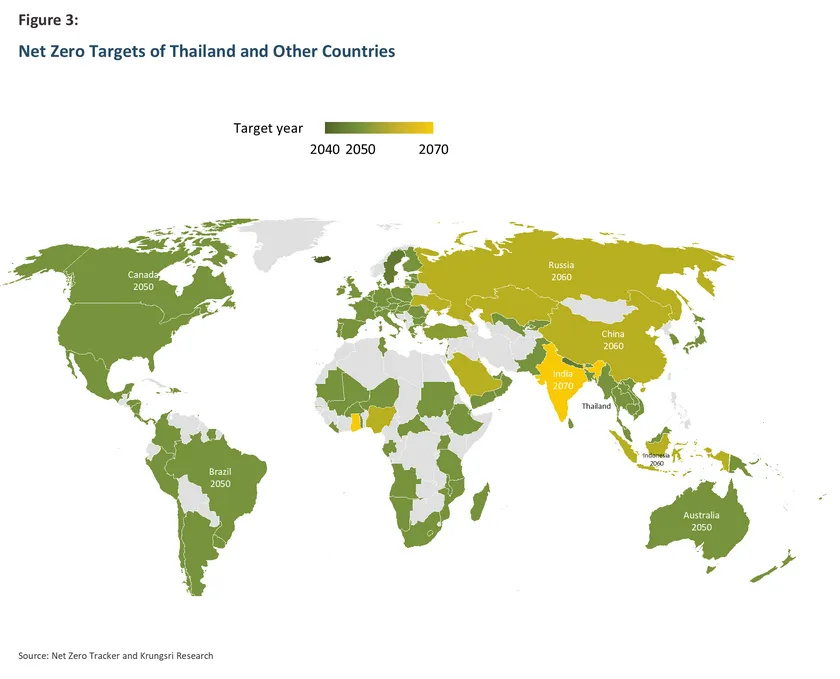

Currently, more than 150 countries have announced Net Zero targets or related environmental goals such as carbon neutrality, carbon negativity, and climate neutrality. Over 130 countries have set a 2050 target, including EU member states, Japan, Singapore, and Vietnam, while some have adopted more ambitious timelines, such as Antigua and Barbuda (2040) and Sweden and Nepal (2045). Others have set later deadlines, including Saudi Arabia, Nigeria, Indonesia, and China (2060), and India and Ghana (2070) (Figure 3).

Thailand’s revised 2050 target therefore reflects a concerted effort to strengthen its climate policy in line with global trends. By contrast, the previous Net Zero 2065 target placed Thailand among the least ambitious countries globally.

Key Factors Shaping Thailand’s Path to Net Zero

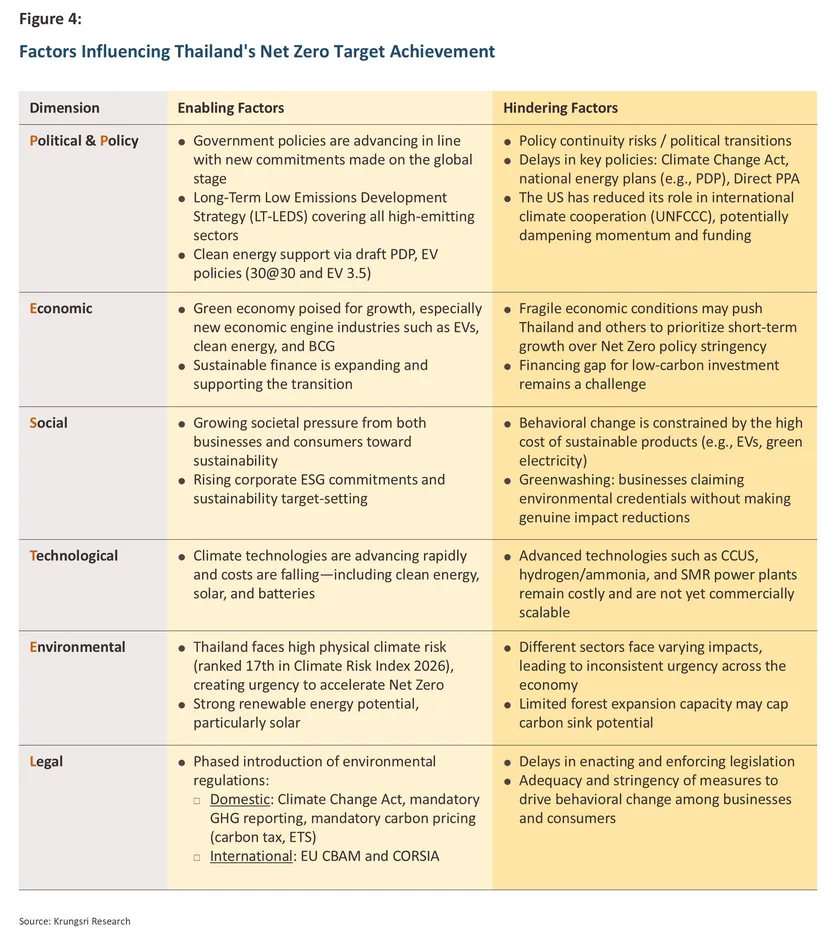

A critical question is whether Thailand can achieve its ambitious Net Zero target. To address this, Krungsri Research assesses the factors influencing the achievement of Net Zero using a PESTEL framework, examining six dimensions: political, economic, social, technological, environmental, and legal (summarized in Figure 4).

Politics and Policy (P)

Government has pursued Net Zero policy consistently, but progress depends on political dynamics.

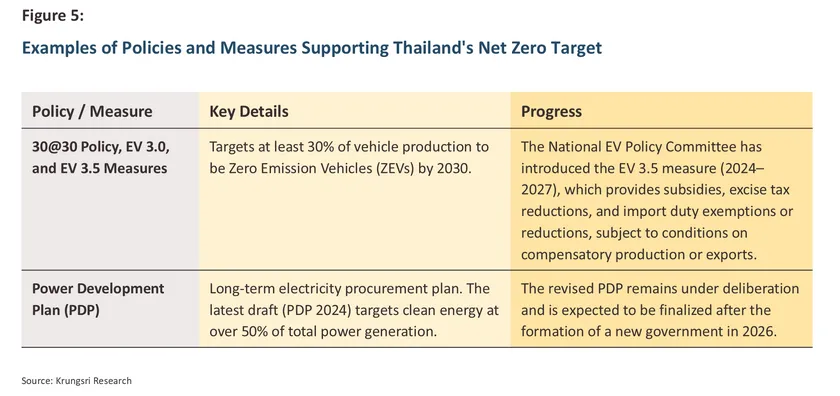

The Thai government has maintained a consistent commitment to Net Zero. In 2021, the government of Prime Minister Prayut Chan-o-cha announced the Net Zero 2065 target for the first time at COP26. Subsequently, in 2025, the government of Prime Minister Anutin Charnvirakul advanced the target to Net Zero 2050. Thailand has also developed a Long-Term Low Emissions Development Strategy (LT-LEDS) covering all sectors, energy, agriculture, industry, waste, and forestry, which is currently being revised for submission to the UNFCCC by the end of 2026. In parallel, relevant agencies are implementing sector-specific policies, such as expanding renewable energy use under the National Energy Plan1/, and promoting EV production and adoption through the 30@30 policy and EV 3.0 and EV 3.5 measures (Figure 5).

However, political transitions and policy discontinuity may impede Net Zero momentum, as reflected in delays to key laws, plans, and policy measures that have been deferred pending clarity on the formation of a new government. These include the landmark Climate Change Act, the National Energy Plan, particularly the new Power Development Plan (PDP), which will set the direction for the energy transition in the power sector (responsible for roughly one-fifth of national GHG emissions), as well as green electricity access mechanisms such as the Utility Green Tariff (UGT) and Direct Power Purchase Agreements (Direct PPA).

Beyond domestic factors, global geopolitics may also affect Thailand’s Net Zero trajectory, particularly the role of the US. The US did not participate in COP30, and on January 7, 2026, President Donald Trump announced the country’s withdrawal from the UNFCCC, having already withdrawn from the Paris Agreement on his first day in office. The US is the world’s largest cumulative GHG emitter and had pledged over USD 3 billion to the Green Climate Fund2/. As the US reduces its Net Zero ambitions, this could create a ripple effect, prompting other countries to scale back their commitments and leaving developing countries, including Thailand, with fewer opportunities to access international climate finance.

Economy and Finance (E)

Net Zero and economic growth can go hand in hand, with finance playing a key supporting role.

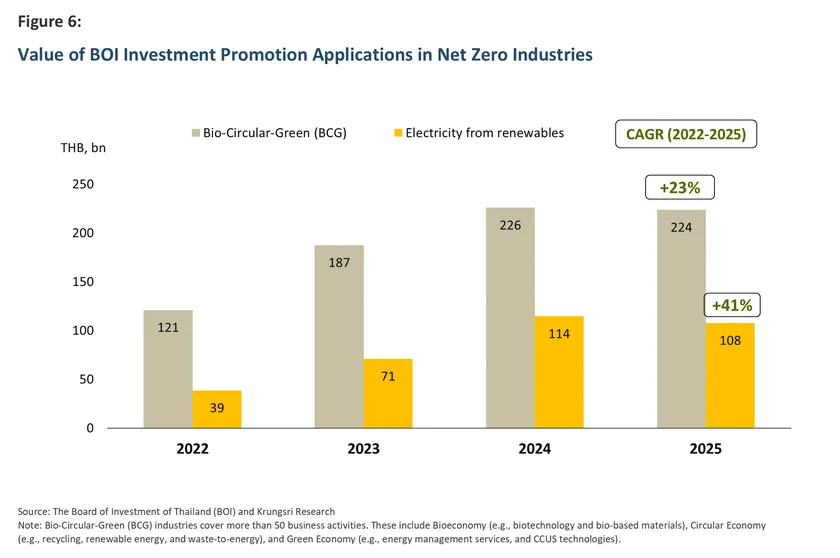

Fragile economic conditions may lead many countries, including Thailand, to place greater emphasis on short-term economic stabilization, potentially easing the stringency of Net Zero policies to support businesses. In the long run, however, Thailand can pursue economic growth and Net Zero simultaneously, as environmentally friendly industries, including electric vehicles, clean energy, and other GHG-reducing technologies, play a vital role in driving the economy and are designated as strategic industries with government backing. These sectors have expanded steadily in line with the global green economy trend. During 2022–2025, the value of investment promotion applications submitted to the Board of Investment (BOI)3/ under the Bio-Circular-Green (BCG) umbrella grew at an average rate of 22.7% per year. Renewable energy businesses, in particular, submitted over THB 330 billion in BOI applications during the same period, representing an average annual growth of 40.9% (Figure 6). The BOI has set a target for BCG industries to account for 24% of Thailand’s GDP by 2027. Meanwhile, the World Bank estimates that advanced green manufacturing, including EVs, solar panel components, and high-efficiency cooling systems, could add 2.9% to Thailand’s GDP by 2035.4/ This demonstrates that environmentally friendly industries not only help reduce GHG emissions but also create economic value and strengthen the country’s competitiveness.

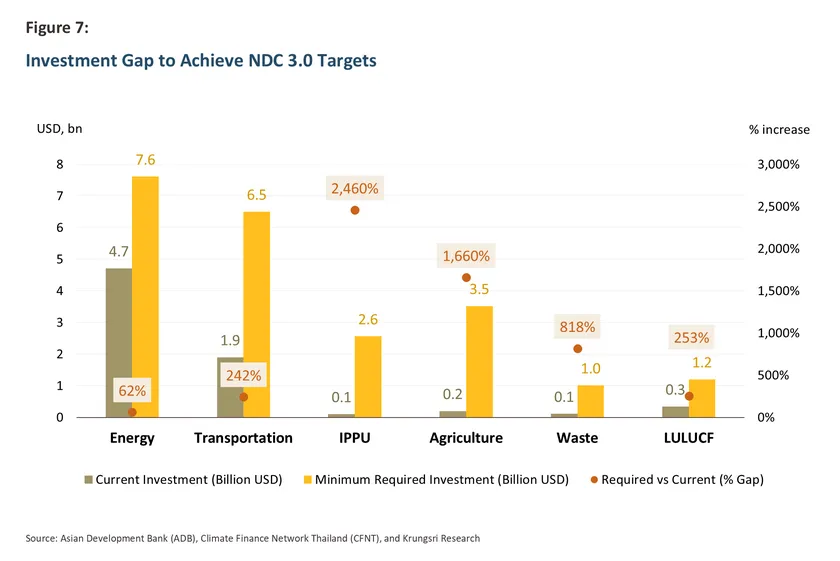

On the financing side, capital is indispensable for achieving Net Zero, and the sustainable finance market has been growing steadily. The outstanding value of ESG bonds5/ increased at an average annual rate of 86.8% during 2019–2025. Thailand's various sectors have collectively invested THB 1.7 trillion in GHG mitigation activities from 2018 through May 2025,6/ with the energy sector accounting for the largest share at approximately 45.8%, followed by transport at 18.5%. Nevertheless, the Asian Development Bank (ADB) estimates that Thailand still requires an additional investment (investment gap) of THB 500–700 billion per year on average to meet its NDC 3.0 targets through 2035, particularly in industry and agriculture, which require the largest proportional increases relative to their current investment levels (Figure 7).

In summary, the growth of green finance and the broader green economy will accelerate GHG reductions across all sectors. However, economic fragility and financing gaps may hinder Thailand's transition toward its Net Zero goal.

Social, Consumer, and Business (S)

Businesses and consumers are increasingly aware of environmental issues, but behavioral change remains constrained by purchasing power.

Businesses and consumers are placing greater importance on environmental sustainability. Notably, many large Thai companies set corporate Net Zero 2050 targets even before Thailand announced its new national goal. These companies span diverse industries: agri-food, including Charoen Pokphand Foods PCL, Thai Union Group PCL, and Thai Beverage PCL; energy, including PTT Exploration and Production PCL; industry, including Siam Cement Group PCL and PTT Global Chemical PCL; services, including Bangkok Dusit Medical Services PCL, Minor International PCL, and True Corporation PCL; and the financial sector, including Bank of Ayudhya PCL (Krungsri),7/Kasikornbank PCL, and Siam Commercial Bank PCL8/. Businesses are also increasingly committing to 100% renewable energy (RE100), both among multinationals and Thai companies. As of March 9, 2026, 443 leading global companies had adopted RE100 targets9/, including Delta Electronics, Microsoft, and Unilever. The growing presence of data centers is also adding pressure on Thailand to scale up its share of renewable power generation.

Thai consumers are also displaying heightened environmental awareness. According to the Thailand Consumer Trends Outlook 2025 by Intellify, 91% of Thai consumers say they care about sustainability and environmental issues, while 65% consider climate change an urgent concern. Furthermore, 58% are willing to pay approximately 11.7% more for environmentally friendly products10/, signaling demand for businesses to develop sustainability-aligned products and services.

However, some businesses may engage in greenwashing or creating an image of sustainability without genuinely reducing environmental impact. At the same time, financial constraints may limit the extent to which businesses and consumers can change their behavior, as environmentally friendly goods such as electric vehicles and green electricity remain expensive, particularly for small businesses and consumers with limited purchasing power.

Technology (T)

Technological advances are driving Net Zero, but cost and commercial readiness remain significant barriers.

Advances in climate technology are a critical enabler of Net Zero achievement. Renewable energy technologies in particular are becoming increasingly capable and progressively more cost-competitive, including solar panels and battery energy storage systems (BESS)11/, driving widespread adoption. Meanwhile, Sustainable Aviation Fuel (SAF) produced via the Hydroprocessed Esters and Fatty Acids (HEFA) process from used cooking oil is already commercially viable12/, with Bangchak Group and PTT Group as Thailand's key producers.

In addition, both the public and private sectors in Thailand have begun investing in and developing Carbon Capture and Storage (CCS), which can reduce carbon emissions from the energy sector and hard-to-abate industries. PTTEP has launched a pilot CCS project at the Arthit gas field, expected to be operational in 2028 with a storage capacity of 1 million tonnes of CO2 per year. The government is also advancing the Eastern Thailand CCS Hub project, targeting carbon capture from industrial facilities in the Eastern Economic Corridor (EEC) for offshore storage in the Gulf of Thailand, with an anticipated completion in 2034 and capacity of up to 10 million tonnes of CO2 per year.13/

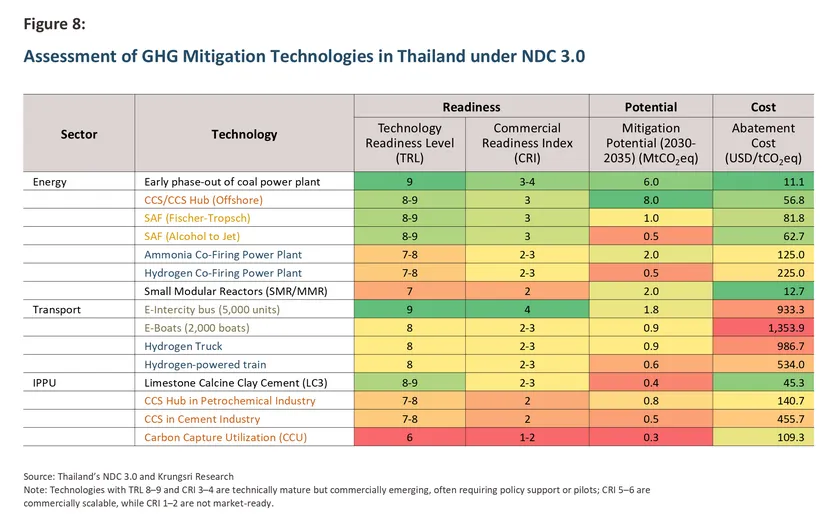

Nevertheless, many low-carbon technologies remain costly and are not yet commercially scalable, particularly the use of CCS in cement and petrochemical industries, hydrogen and ammonia co-firing in natural gas power plants, and hydrogen-powered transport, all of which carry high abatement costs per unit (Figure 8). Small Modular Reactors (SMRs), while offering low per-unit abatement costs and the potential to meet growing clean energy demand, remain at a low level of commercial readiness.14/

Environment (E)

Escalating physical risks from climate change will drive Thailand to take its Net Zero target more seriously.

Thailand’s exposure to climate change risks is intensifying. In 2026, Thailand ranked 17th globally in the Climate Risk Index (CRI 2026), rising sharply from 72nd in 2022 (CRI 2022), reflecting increasing vulnerability to extreme weather events, including heat waves, heavy rainfall, and flooding, as demonstrated by the major floods in Southern Thailand in 2025.15/

Furthermore, the World Economic Forum’s Global Risks Report 2026 identifies extreme weather events as the world’s top risk over the next decade (2026–2035). The escalating physical risks from climate change therefore represent a key imperative for both the world and Thailand to implement emission reduction policies in earnest.

However, different sectors face different climate change risks and impacts, resulting in varying levels of motivation and urgency to act on Net Zero. For instance, while the energy and industrial sectors are larger GHG emitters than agriculture, they face lower physical risk than the agricultural sector, which is exposed to both flooding and drought, meaning agriculture may have stronger direct incentives to act, despite emitting less.

Furthermore, NDC 3.0 places equal emphasis on nature-based sequestration and direct emission reduction or avoidance, as reflected in a 28% increase in the LULUCF sequestration target while the overall emission reduction across sectors is set at -29%. However, Thailand's potential to expand forest cover as a carbon sink may be limited by land availability, competing agricultural use, urbanization, and forest degradation, all of which could affect the country's ability to meet its Net Zero target as set.

Legislation (L)

Regulations will accelerate business transition, but this depends on the timeliness and stringency of enforcement.

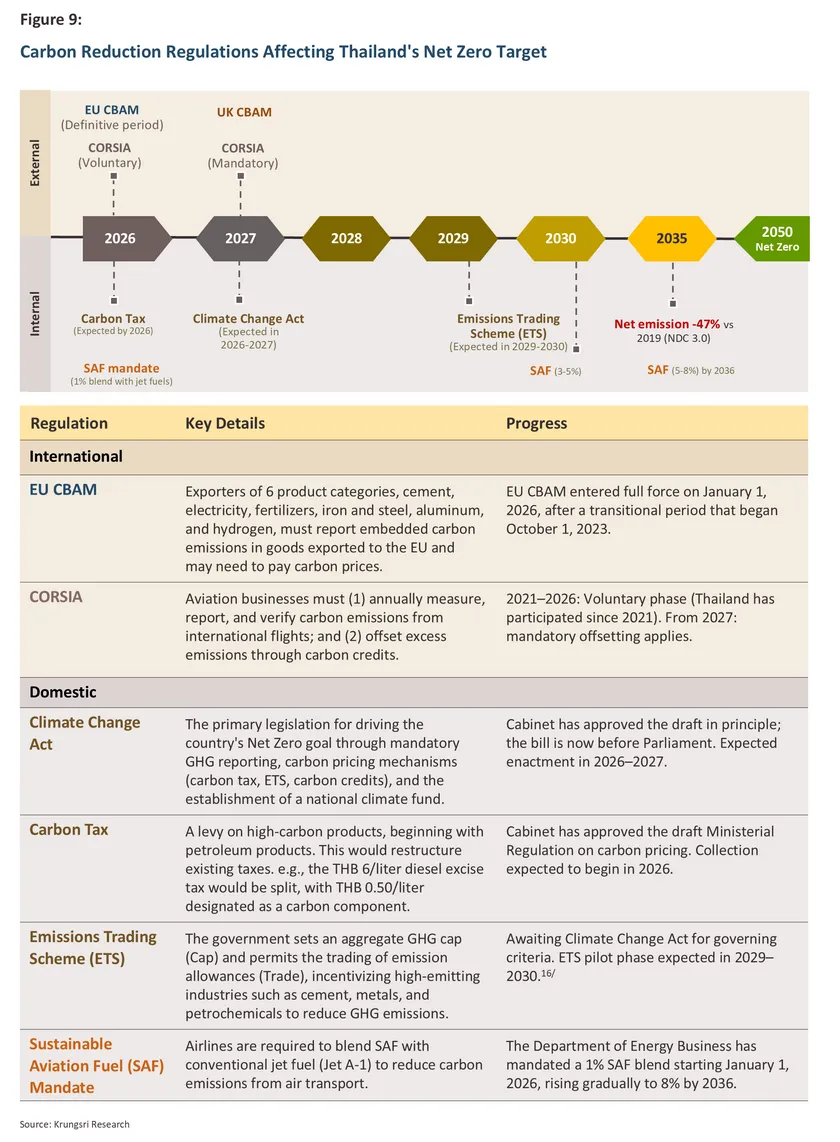

Carbon management laws and regulations are tightening on both domestic and international fronts. International trade rules are already creating significant pressure on Thai businesses, particularly the EU’s Carbon Border Adjustment Mechanism (CBAM), which entered the full implantation phase on January 1, 2026. Exporters of covered goods, especially steel, aluminum, and cement, must now report the embedded carbon content of their exports to the EU and may face carbon pricing. The UK CBAM is expected to follow in 2027. The International Civil Aviation Organization (ICAO) has also introduced the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), requiring Thai airlines to report and offset carbon emissions from international flights, thereby driving the adoption of Sustainable Aviation Fuel (SAF).

At the domestic level, Thailand is developing a legal framework to support its Net Zero target. The Department of Climate Change and Environment is drafting the Climate Change Act, which will require businesses to report GHG emissions. The government is also advancing mandatory carbon pricing mechanisms, including a carbon tax on petroleum products and the establishment of an Emissions Trading Scheme (ETS), targeting high emitting industries such as cement, metals, and petrochemicals to incentivize carbon reduction across the economy (Figure 9).

However, progress on Thailand’s Net Zero legislation remains delayed. As of March 9, 2026, the Climate Change Act has not been enacted and mandatory carbon pricing has not been implemented. This may lead businesses to defer investment in low-carbon technologies. It will also be important to monitor whether the measures, once enacted, are sufficiently stringent to drive meaningful behavioral change. For instance, if carbon prices or penalties are set too low, they may fail to provide adequate incentives for emissions reduction.

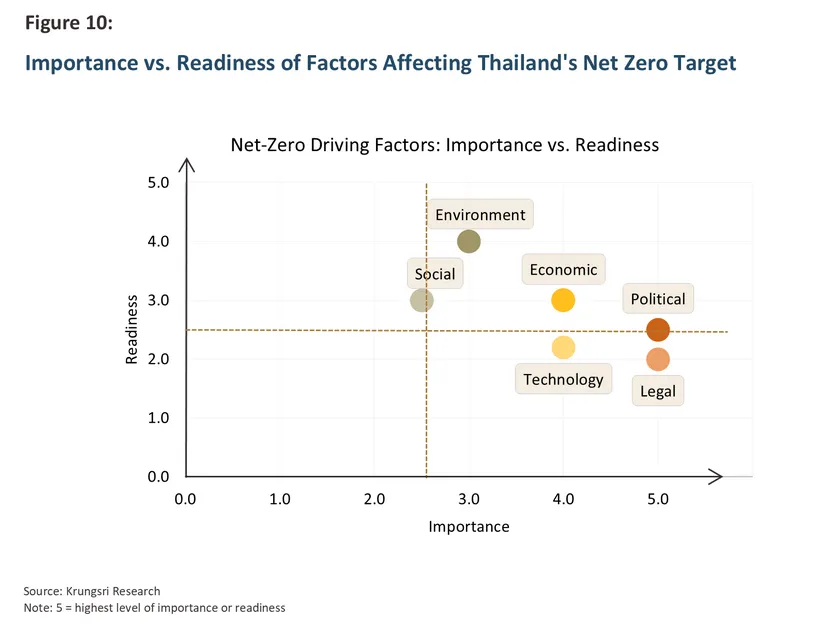

From the PESTEL analysis above, each dimension presents both enabling factors and barriers. For Thailand to move closer to its Net Zero finish line, it must accelerate progress and reduce friction across all fronts. Which dimensions should be prioritized? To identify the most urgent areas for action, Krungsri Research assesses the relative importance and readiness of all six PESTEL factors (Figure 10). The results suggest that Thailand should prioritize the political and legal dimensions, which carry the greatest weight in driving Net Zero but remain at low to medium readiness. This reflects a policy direction that is broadly advancing, including the revised Net Zero target, but constrained by delays in key legislation and policies such as the Climate Change Act, carbon pricing mechanisms, and clean energy plans.

Economic and technological factors rank second in importance. Economic readiness is relatively high, driven by the sustained growth of the green economy, EVs, clean energy, and green finance. Low-carbon technologies are advancing rapidly, but most remain constrained by high costs and limited commercial scalability, particularly advanced technologies such as CCS and hydrogen.

Finally, environmental and social factors carry comparatively lower weight, but exhibit medium to high readiness. Physical climate risk awareness represents the highest readiness across all six dimensions, given the increasingly tangible impacts of climate change. Social readiness is moderate as Thai consumers and businesses are more sustainability-minded, but concrete transitions remain limited by the high cost of green goods, services, and technologies. That said, while many stakeholders may have previously acted on sustainability on a voluntary basis, as Net Zero targets become more demanding, businesses may find themselves compelled to act, whether in response to rising risks or emerging economic opportunities.

Who Faces Disruption or Gains from Net Zero?

Sectors Affected by Net Zero

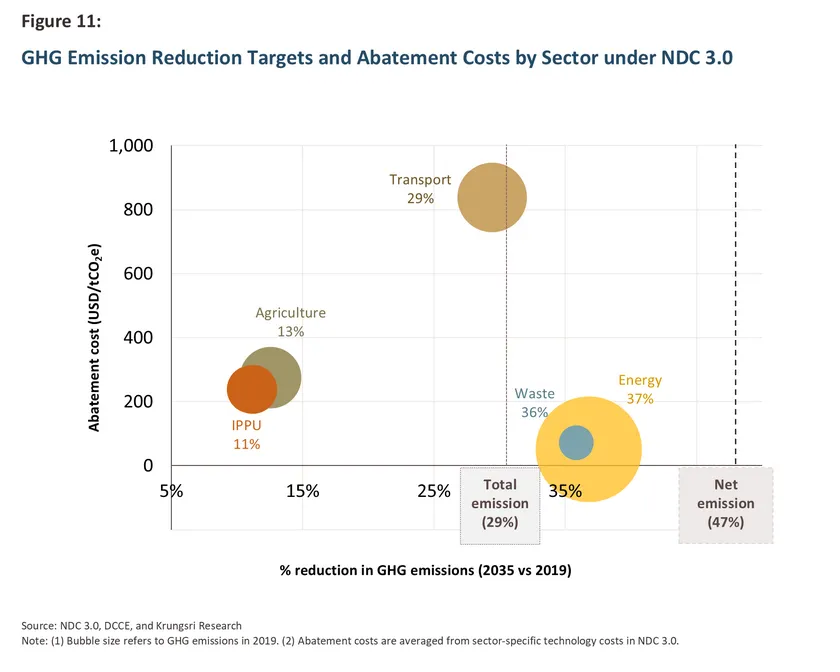

With NDC 3.0 requiring Thailand to reduce net GHG emissions by -47% by 2035 compared to 2019 levels, all sectors face intensifying pressure to transition. This section assesses the sectors most exposed to Net Zero disruption based on four factors: (1) 2019 GHG baseline; (2) 2035 GHG reduction targets relative to 2019; (3) average abatement costs of key technologies; and (4) additional pressures such as regulatory and trade requirements. The sectors most affected can be ranked as follows:

-

Energy sector: The energy sector is Thailand's largest GHG emitter at 185.2 MtCO2e in 2019 and must reduce emissions by -37% by 2035 (Figure 11), making it the most pressured sector, given that energy use represents an indirect carbon cost for all other businesses. NDC 3.0 estimates the sector's average abatement cost at USD 51.1 per tCO2e, lower than that of other sectors. However, significant challenges remain due to Thailand’s heavy reliance on fossil fuels, which account for around 70% of total electricity generation. The absence of a coal phase-down policy, combined with the high cost of upgrading natural gas power plants with cleaner fuels such as hydrogen or ammonia, continues to constrain the energy transition.

-

Transport sector: Transport emits 76.8 MtCO2e, second only to the energy sector, and must reduce GHG emissions by -29% by 2035. While passenger EVs and electric buses (E-buses) are expanding, other transport modes face very high transition costs, as highlighted in NDC 3.0, including marine vessels, trucks, intercity electric buses, and hydrogen-powered trucks and trains. The sector is also likely to face pressure from a carbon tax on petroleum products, which may not immediately affect retail fuel prices but could raise transport costs if tax rates are increased over time

-

Industrial sector (IPPU): The industrial sector faces the smallest required reduction at only 11%, reflecting the high cost of available decarbonization technologies. Hard-to-abate sub-sectors, such as cement, chemicals, steel, and aluminum, require CCS technology and hydrogen-based production processes. Heavy industry also faces intense pressure from trade regulations, particularly the EU CBAM. Research by the Puey Ungphakorn Institute for Economic Research (PIER) found that after CBAM entered its transition phase in 2023, Thai exporters of CBAM-covered goods to the EU decreased by -24% compared to other Thai exporters to the EU.17/

-

Agriculture sector: Agriculture accounts for 18% of Thailand's total GHG emissions, with rice cultivation and livestock farming as the primary sources, releasing methane, which has a global warming potential approximately 28 times that of carbon dioxide. GHG reduction technologies in agriculture remain costly, including modified livestock feed formulations to reduce enteric fermentation and precision fertilizer application (precision farming). The sector is also highly vulnerable to physical climate risks and is dominated by smallholder farmers.

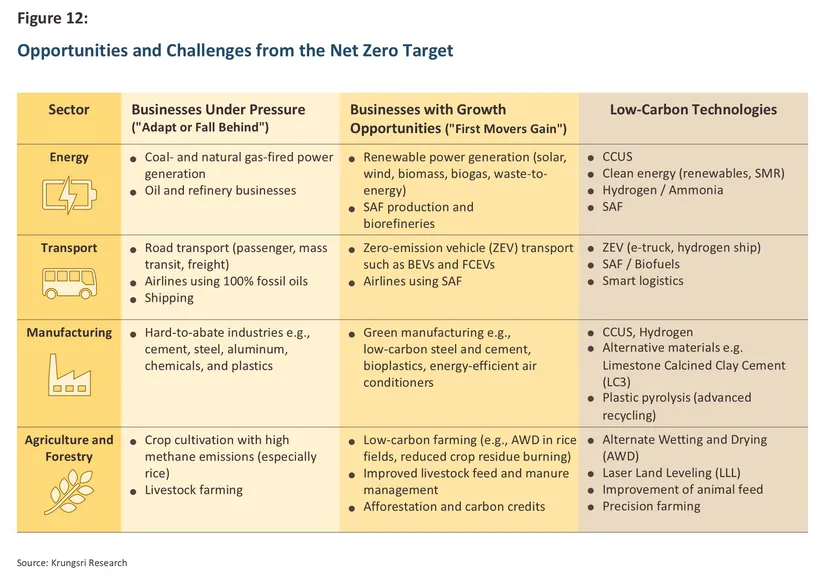

Businesses Positioned to Benefit from Net Zero

The Net Zero transition creates opportunities for environmentally friendly industries and businesses across all sectors. The standout beneficiaries, those both driving and benefiting from Net Zero, are as follows:

-

Renewable Energy: Electricity generation from renewable sources, particularly solar and wind, is set for sustained growth, driven by declining equipment and technology costs, including solar panels and batteries, making it increasingly cost competitive with fossil fuel power. Green electricity demand is also rising as businesses pursue sustainability targets in response to tightening environmental standards, reflected in the growing number of companies committing to 100% renewable energy (RE100), including data centers and cloud service providers investing in Thailand that require substantial clean power. The government is accelerating renewable power expansion, with the new PDP expected to raise the renewable energy share to 50-60% in line with the new Net Zero target, while improving private sector access through Direct PPA and UGT mechanisms18/. Thailand’s large agricultural and food processing base also provides a strong feedstock advantage for bioenergy development, including Sustainable Aviation Fuel (SAF) from used cooking oil and agricultural residues. Demand for SAF is expected to grow in line with Thailand’s blending mandate and the aviation sector’s Fly Net Zero 2050 goal.

-

Electric Vehicles (EVs): EV adoption in Thailand is on a strong upward trajectory. As of January 31, 2026, cumulative battery electric vehicle (BEV) registrations reached 418,091 units, up from 11,382 in 2021, representing a compound annual growth rate of 139.2% during 2021–2025. Passenger cars account for 77.6% of total BEVs, followed by motorcycles at 21.2% and electric buses at 0.7%.19/ Krungsri Research expects EV sales to continue growing during 2026–2028, with new BEV passenger car registrations averaging around 125,000 units per year, supported by government subsidies under EV 3.5, new model launches with extended range, and the enforcement of Euro 6 emissions standards, which will increase the cost of internal combustion engine vehicles.20/

-

Green Manufacturing: Environmentally friendly products are gaining traction, including low-carbon steel and cement, bioplastics, and energy efficient equipment. The World Bank highlights Thailand’s potential to build on its existing industrial base to develop green manufacturing capabilities, such as transitioning the automotive sector toward EV production and components, and producing energy efficient air conditioners, building on Thailand’s position as a major air conditioner producer, accounting for approximately one third of global production.

-

Net Zero Enablers: Low-carbon technologies such as Carbon Capture, Utilization and Storage (CCUS) play an important role in reducing emissions from fossil fuel intensive industries. Hydrogen may emerge as an alternative fuel for power generation, freight transport, and heavy industry. Carbon management services will also benefit, including measurement, reporting, and verification (MRV) consulting, digital platforms for carbon footprint tracking, and carbon credit producers. The Ministry of Finance is also working to designate carbon credits as a deliverable commodity on the Thailand Futures Exchange (TFEX)21/, which would further support market growth.

Krungsri Research View: How Can Thailand Achieve Net Zero?

What Should Thailand Prioritize?

Net Zero 2050 is a long term and highly ambitious goal for Thailand, one that is not easy but achievable, contingent on timely action by all stakeholders. Krungsri Research identifies three priority areas: (1) enacting mandatory regulations; (2) strengthening investment incentives for the low-carbon economy; and (3) advancing international cooperation on technology and finance.

-

Accelerate legislation and policy. Thailand should expedite the Climate Change Act to establish mandatory carbon reporting and carbon pricing mechanisms, which will drive behavioral change across businesses, industries, and consumers. In parallel, the National Energy Plan, particularly the PDP, should be finalized to set a clear pathway for expanding renewable energy and reducing reliance on fossil fuels. Beyond mitigation, Thailand should also prioritize adaptation measures to manage climate risks, alongside a just transition approach that minimizes adverse impacts on high-carbon legacy industries.

-

Strengthen investment incentives. The government should promote investment in high value, low-carbon industries such as clean energy, EVs, and green manufacturing through targeted incentives and infrastructure development, particularly in green electricity, which is a key attractor for investors committed to net-zero value chains. Authorities should also promote businesses' use of the Thailand Taxonomy as a transition framework,22/ enabling firms aligned with its criteria to access greater financing opportunities. In addition, businesses should be supported in developing carbon footprint measurement systems to enable effective carbon management, especially among small and medium-sized enterprises.

-

Advance international cooperation. Thailand should deepen partnerships to support the development of advanced technologies and mobilize financing. Existing examples include the Thai Smile Bus electric bus project supported by Switzerland, and two solar farm projects by Minebea Super Solar Power Co., Ltd. and Impact Electrons Siam Co., Ltd.23/, supported by Japan under the Joint Crediting Mechanism (JCM). Going forward, Thailand should expand collaboration in capital-intensive technologies such as CCUS and hydrogen24/, while leveraging international platforms such as COP to access climate finance, including the Green Climate Fund and the Loss and Damage Fund.

How Should Businesses Prepare?

With the world and Thailand committed to Net Zero, businesses must align their strategies to reduce exposure and capture opportunities along the Net Zero pathway.

Krungsri Research recommends that businesses prepare through three key steps: "Ready, Set, and Go Sustainable!"

-

Ready: Prepare by measuring carbon. Businesses should begin by measuring and recording GHG emissions. While the upfront cost of investing in measurement, reporting, and verification (MRV) systems may be significant, early movers can gain a long-term competitive advantage as pressure intensifies from regulations, trade rules, and sustainability focused customers and partners.

-

Set: Define a Net Zero target. With carbon data in place, businesses should establish emission reduction targets, and a corporate Net Zero goal aligned with national direction, supported by a clear transition plan toward low-carbon operations. Clear targets and roadmaps enhance credibility with investors, customers, and regulators, while enabling effective carbon management.

-

Go: Act and capture opportunities. Businesses should accelerate emissions reduction across operations and supply chains, while using carbon credits to offset residual emissions where appropriate. At the same time, firms should actively identify opportunities in the green economy, whether by entering new markets or repositioning existing businesses to meet sustainability- driven demand, as well as opportunities in carbon markets. Achieving Net Zero will require financing, and many commercial banks, including Krungsri, are increasingly ready to support businesses in transitioning to sustainability. Krungsri provides support through a range of products including sustainability-linked loans, green deposits, and sustainability knowledge services under the Go Sustainable with krungsri campaign.25/

Ultimately, Thailand’s success in achieving Net Zero will depend not only on government policy, but also on decisive private sector action. Businesses that move early will be better positioned to manage regulatory and environmental risks, unlock new growth opportunities, and remain competitive over the long term.

References

Climate Finance Network Thailand (CFNT). (2026). Financing NDC 3.0: Challenges and opportunities toward Net Zero 2050 (Thailand). Retrieved from https://climatefinancethai.com/th/financing-ndc-3-0-challenges-and-opportunities-toward-net-zero-2050-th/

Puey Ungphakorn Institute for Economic Research (PIER). (2025). The Impact of the EU CBAM on Thai Exporting Firms: Analysis of Firm-level Data. Retrieved from https://www.pier.or.th/dp/243/

United Nations Framework Convention on Climate Change (UNFCCC). (2025). Thailand’s NDC 3.0. Retrieved from https://unfccc.int/sites/default/files/2025-11/TH%20NDC%203.0.pdf

United Nations Framework Convention on Climate Change (UNFCCC). (2022). Thailand Long-Term Low Emissions Development Strategy (LT-LEDS), Revised Version. Retrieved from https://unfccc.int/sites/default/files/resource/Thailand%20LT-LEDS%20%28Revised%20Version%29_08Nov2022.pdf

World Economic Forum (WEF). (2026). Global Risks Report 2026. Retrieved from https://www.weforum.org/publications/global-risks-report-2026/

1/ The National Energy Plan (NEP) is Thailand's overarching energy framework, comprising five sub-plans: the Power Development Plan (PDP), Alternative Energy Development Plan (AEDP), Energy Efficiency Plan (EEP), Gas Plan, and Oil Plan.

2/ US Withdrawal from Paris Agreement May Restrict Thailand’s Access to Climate Finance as Global Warming Intensifies | iGreen

3/ BOI-promoted BCG businesses receive incentives such as up to 8 years of corporate income tax exemption.

4/ Thailand Can Capture Major Growth Gains by Scaling Up Green Manufacturing, World Bank Says | The Nation

5/ Data from the Thai Bond Market Association.

6/ Data from the Climate Finance Tracker by the Climate Finance Network Thailand (CFNT), aggregating GHG-reduction investments from the private sector, public sector, and financial institutions. Energy 7/accounts for approximately 45.8%, transport 18.5%, while IPPU, agriculture, waste, and LULUCF together account for approximately 7.2%

In 2023, Krungsri launched the Krungsri Race to Net Zero initiative. In 2024, Krungsri set a target to achieve Net Zero from its own operations by 2030 and Net Zero from all financial services by 2050.

8/ Some SMEs have also begun setting Net Zero targets under the Science Based Targets initiative (SBTi), including RISE Accel (consulting) and Starboard, Airush, and SOMWR (retail).

9/ RE100 Members | RE100

10/ Thailand Consumer Trends Outlook 2025 | Intellify Market Research

11/ Solar panel prices have declined at an average of -10.4% per year (2019–2024); BESS costs have fallen -7.1% per year (2019–2025).

12/ Other SAF production pathways, such as Alcohol-to-Jet and Fischer-Tropsch, remain under development.

13/ On January 6, 2026, the Cabinet approved in principle the deployment of CCS technology for GHG mitigation, selecting the Upper Gulf of Thailand as a pilot area to assess offshore carbon storage potential. The Eastern Thailand CCS Hub is expected to be operational around 2034, with the Department of Mineral Fuels as the project owner. High-Stakes CCS Hub in the Gulf of Thailand: Caretaker Government Bets the Country’s Future on a Costly Solution | BangkokBizNews

14/ Countries such as Russia, China, and Canada have already deployed SMRs, but these are still at early stages and at high cost. Thailand is studying feasibility and considering SMR as a long-term option, subject to legal, social acceptance, and infrastructure constraints.

15/ Thailand ranks Top 17 globally, facing extreme weather risks | BangkokBizNews

16/ DCCE, SEC, and SET discussed the framework for trading GHG emission allowances under the draft Climate Change Act | The Department of Climate Change and Environment (DCCE)

17/ "How Concerning is CBAM for Thailand's Exports, and How Should We Respond?" | PIER

18/ Further reading: Industry Outlook: Renewable Energy | Krungsri Research

19/ Statistical data | Electric Vehicle Association of Thailand (EVAT)

20/ Further reading: Industry Outlook: Electric Vehicle Industry | Krungsri Research

21/ "Ekniti" greenlights green capital market, approves carbon credits as referenced commodity on Thailand Futures Exchange | Thai Government

22/ The Thailand Taxonomy currently covers 6 sectors: energy, transport, manufacturing, agriculture, construction/real estate, and waste. See also: Decoding the Thailand Taxonomy | Krungsri Research.

23/ Projects of joint ventures between Minebea Mitsumi Inc. and Super Energy Corporation PCL—generating electricity for electronics and machinery factories; and Impact Electrons Siam (IES)—partnering to supply clean energy to data centers.

24/ Thailand is in negotiations with Singapore to co-invest in the Thailand CCS Hub project. PTTEP is advancing CCS and urging the government to issue tax measures, targeting expansion to 60 million tonnes in the Upper Gulf of Thailand. | Thansettakij

25/ GO Sustainable with krungsri | Krungsri