U.S.–Iran Tensions and Risks to Global Oil Supply

Since late February 2026, geopolitical tensions in the Middle East have intensified significantly due to escalating conflict between the United States and Iran. Following strikes by the United States and Israel on Iran’s military infrastructure and key leadership figures, Iran retaliated by launching missiles and drones targeting multiple locations across the region. These developments have heightened the risk that the conflict could escalate further into a broader regional conflict.

One of the key concerns globally is the potential closure of the Strait of Hormuz, a critical route for global oil transportation. Approximately 34% of the world’s crude oil trade passes through this strait. Any attempt by Iran to block the shipping route or create insecurity in the surrounding waters could quickly tighten global oil supply and disrupt the transportation of goods across international markets, leading to significant supply disruptions.

The situation has led to a significant increase in global oil prices. Dubai crude oil prices have risen by approximately 61% from pre-conflict levels, reaching USD 115 per barrel (as of March 10, 2026). Many analysts estimate that if the escalation in the Middle East remains limited and supply disruptions are only temporary, oil prices could stabilize at around USD 80–100 per barrel. However, in a worst-case scenario, if the conflict expands into a broader regional war and causes prolonged disruptions to oil exports, prices could rise to USD 120–150 per barrel. Such a surge in oil prices would likely push global inflation higher and significantly slow global economic growth, particularly for energy-importing economies such as Thailand.

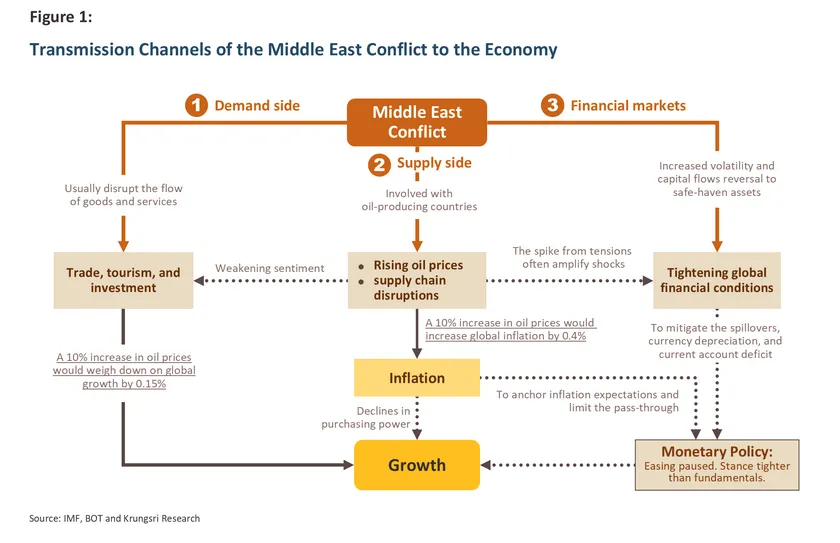

Transmission Channels to the Thai Economy

In terms of the transmission channels, the Middle East conflict could affect the economy through three main channels:

-

Supply-side channel, which is the most significant for the Thai economy. Higher global oil prices would push up inflation, as well as energy costs, production costs, and transportation expenses. This would put pressure on household purchasing power and private investment. In addition, freight rates and shipping insurance premiums could rise, while goods transportation may face delays. If the conflict becomes prolonged and more severe, it could also lead to supply chain disruptions.

-

Demand-side channel. Early signs of impact are already visible in Thailand’s tourism sector. Although tourists from the Middle East account for a relatively small share (around 2.3% of total tourist arrivals), safety concerns, along with airspace closures and the shutdown of several airports in the Middle East, which serve as major global transit hubs, have begun to reduce tourist arrivals from Western countries. According to data from Thailand’s Ministry of Tourism and Sports, between March 1-8, the number of tourists from Europe and the Middle East fell -18%1/ below normal travel trends. If the conflict persists, it could undermine investor confidence and significantly affect trade, investment, and tourism.

-

Financial markets channel. Heightened geopolitical tensions have led to increased volatility in global financial markets, with several countries experiencing capital outflows. However, the initial impact on Thailand may be limited due to the country’s relatively strong external stability, supported by a continued current account surplus and high international reserves. Nevertheless, in a worst-case scenario, global financial conditions could tighten amid elevated inflation, which would constrain monetary policy easing and negatively affect economic growth going forward.

Macroeconomic Impacts on the Thai Economy

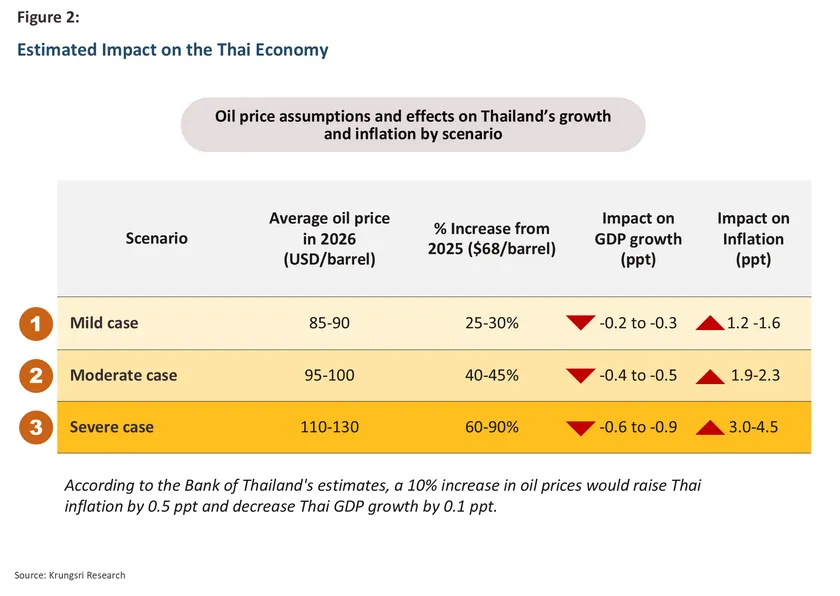

Thailand is a net oil importer and relies heavily on crude oil imports from the Middle East, which account for around 58% of its total crude oil imports. Therefore, an increase in global oil prices could affect the Thai economy through multiple macroeconomic channels. Depending on different scenarios, the potential impacts on the Thai economy can be summarized as follows (Figure 2).

-

Limited escalation scenario: If tensions remain contained and the average oil price for the year is around USD 85–90 per barrel, inflation in Thailand could increase by around 1.2–1.6 percentage points above the baseline, while GDP growth may decline by about -0.2 to -0.3 percentage points from the baseline.

-

Worst-case scenario: If the average oil price rises to USD 110–130 per barrel and the government is unable to subsidize domestic energy prices and the cost of living, domestic inflation could accelerate significantly to around 3.0–4.5 percentage points above the baseline, potentially causing Thailand’s GDP to fall by about -0.6 to -0.9 percentage points from the baseline.

Impacts on Thai Industries

The Middle East conflict may affect Thailand's industrial sectors in multiple dimensions. Impacts can be categorized into direct and indirect effects as follows:

Direct impacts occur within industries in the supply chain in two ways:

(1) feedstock supply shortages, primarily affecting oil refineries and the petrochemical industry; and

(2) disruptions to imported production inputs, affecting industries reliant on imports from the Middle East, such as chemicals, fertilizers, and metals.

Additionally, industries may face indirect impacts through three main channels: (1) production cost pressures from rising energy prices, which increase the burden on energy-intensive industries;

(2) export demand, as demand for Thai goods in the Middle East may slow; and

(3) logistics disruptions, including delays and rising transportation costs resulting from disruptions to regional shipping routes.

Direct Impacts on Industries

1) Feedstock Supply Shortages

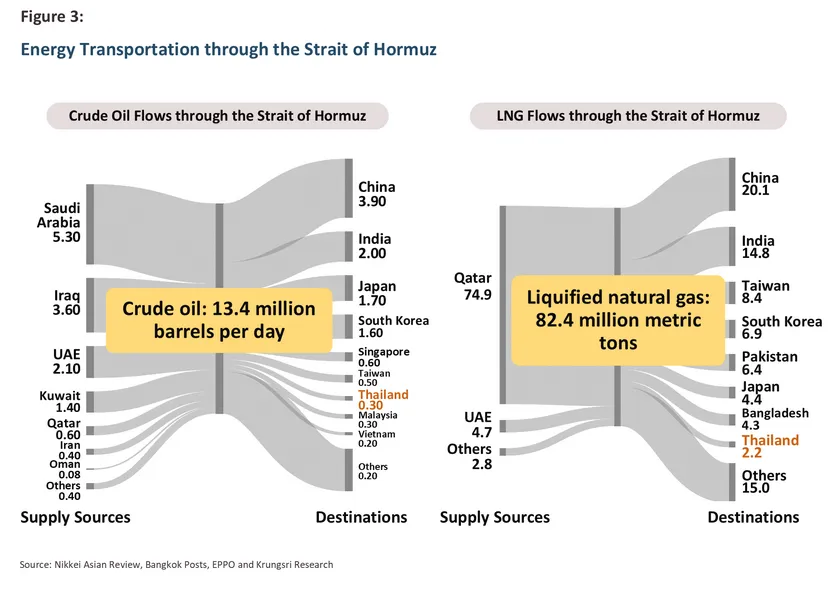

The Strait of Hormuz is a critical global energy artery. In 2025, approximately 13.4 million barrels of crude oil per day were transported through this route, accounting for roughly one-third of global seaborne oil trade, with over 80% of that volume destined for the Asian region.

For Thailand, any delays or disruptions along this route pose a direct risk, as Thailand imports 0.3 million barrels per day through the strait, accounting for 58% of its total crude oil imports. Liquefied natural gas (LNG) is another key commodity from the Middle East transported through this route. Nearly 80% of LNG passing through the strait is destined for Asian markets, particularly LNG shipments from Qatar, which rely exclusively on this route.

Thailand currently imports approximately 2.22/ million metric tons of LNG annually via the Strait of Hormuz, representing 24% of its total LNG imports3/. A closure of the strait would therefore directly impact Thailand's primary fuel for electricity generation.

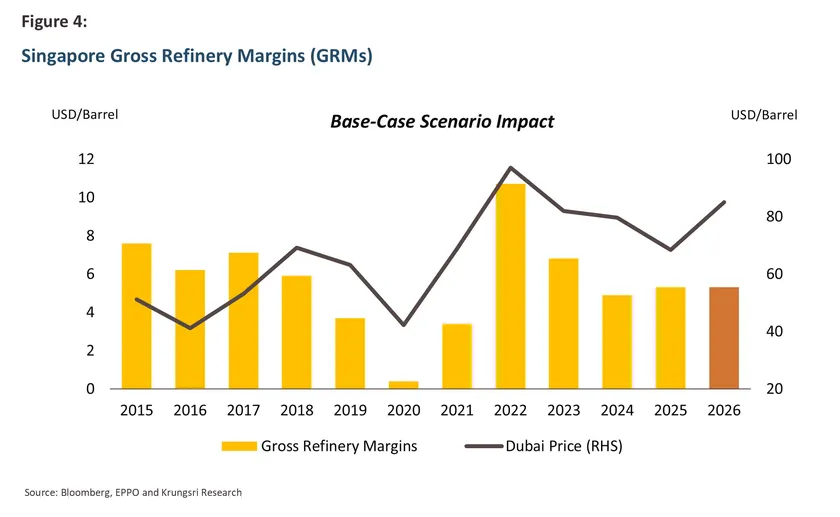

A closure of the Strait of Hormuz would impact oil refineries and the petrochemical industry, which rely heavily on Middle Eastern feedstocks. Under the base-case scenario (limited conflict), Thai oil refineries are likely to benefit in the short term from rising global crude prices, as the value of existing crude inventories would increase immediately. However, downstream industries, particularly petrochemicals, are likely to face margin compression as feedstock prices (e.g., naphtha and natural gas) rise in line with energy costs, while producers are unable to pass on higher prices due to government price controls aimed at managing the cost of living. In addition, supply shortages for petrochemical plants that rely heavily on Middle Eastern feedstocks may force production cuts or temporary shutdowns (force majeure), similar to what occurred at the olefins plant operated by Siam Cement Group.

Should the situation escalate into a full-scale regional conflict (worst-case scenario), Gross Refinery Margins (GRMs) would face significant downward pressure due to: (1) rising production costs as refineries must purchase new crude at elevated prices once existing low-cost inventory is depleted; and (2) limited ability to raise refined product prices, as global energy demand weakens amid stagflation and government retail price controls restrict cost pass-through. This contrasts with the 2022 Russia–Ukraine crisis, when strong global growth and a critical diesel shortage supported refinery margins. The 2026 crisis unfolds against a backdrop of already weak global demand, significantly reducing net profit margins. Furthermore, the power generation sector, which relies heavily on natural gas, would also face direct impacts from potential feedstock supply disruptions. More than 60% of Thailand’s electricity generation uses natural gas as fuel.

For downstream sectors such as petrochemicals, plastics, and packaging, the impact will be far more severe than in the base case. Feedstock costs will spike amid a weakened economic environment, meaning consumers may lack sufficient purchasing power to absorb cost pass-throughs. At the same time, petrochemical plant shutdowns may become more widespread and prolonged, threatening the profitability and stability of related industries over the longer term.

2) Disruptions to Imported Production Inputs

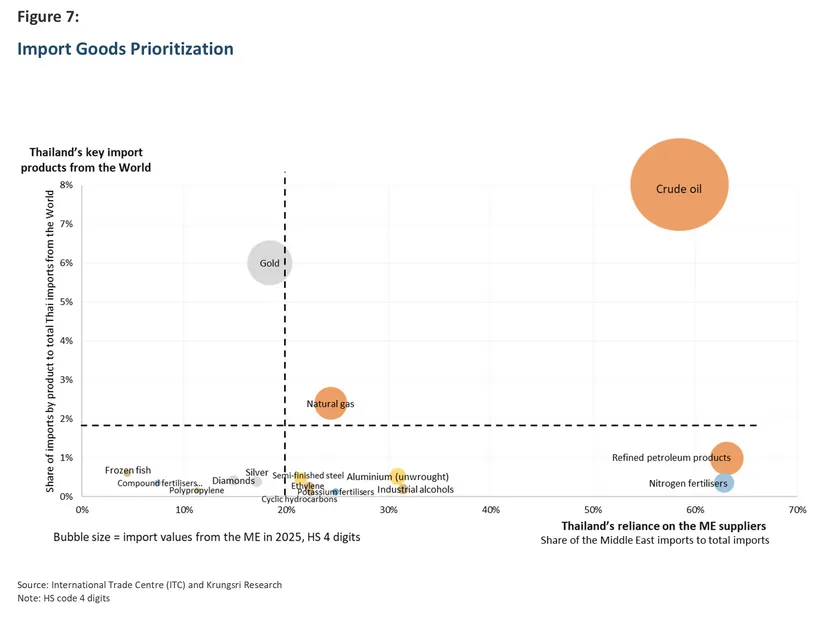

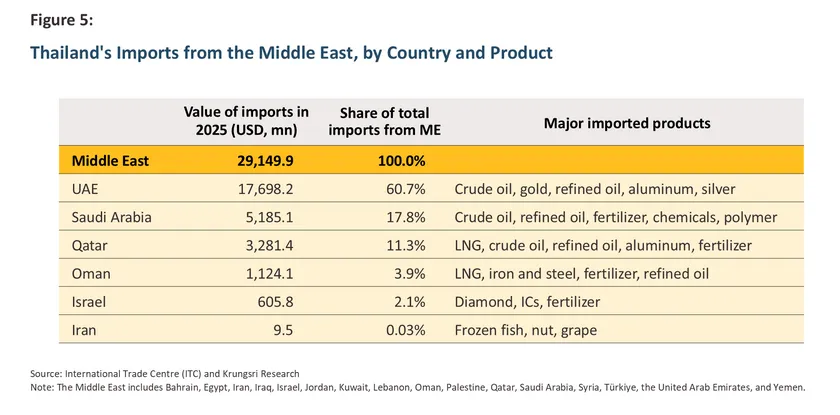

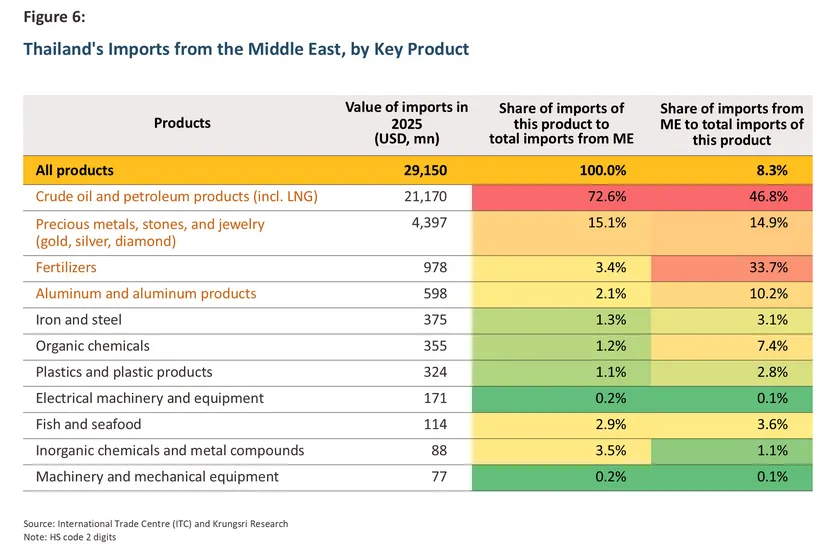

In 2025, Thailand's total imports from the Middle East amounted to USD 29,150 million, representing 8.3% of total imports. Beyond energy, Thailand also imports other critical production inputs from the region in significant volumes, including petroleum products, fertilizers, aluminum, iron and steel, chemicals, and plastic resins and products, which could affect downstream industries. Key source countries include the UAE, Saudi Arabia, and Qatar, while imports from Israel and Iran account for only a small share.

A key input to monitor is fertilizers, for which Thailand relies on imports from the Middle East for roughly one-third of its total imports. Should fertilizer supplies fall short, agricultural production costs could rise, posing risks to food security. However, the Ministry of Commerce expects Thailand's current fertilizer stockpile to last through August 20264/.

In addition, Thailand sources around 10% of its aluminum imports from the Middle East, suggesting that downstream industries in manufacturing and construction may also face potential supply risks.

When examining imports at the product level, affected goods can be grouped into three categories based on import value and the degree of reliance on Middle Eastern suppliers:

-

High reliance, high import value: Crude oil, refined petroleum, LNG, and fertilizers. This group relies heavily on imports from the Middle East and requires close monitoring, as supply disruptions could directly affect the costs and continuity of domestic industrial and agricultural production.

-

High reliance, lower import value: Aluminum, iron and steel, petrochemicals, and chemicals. This group also warrants monitoring, as these are key raw materials used in a wide range of downstream industries.

-

Moderate imports and reliance: Gems and precious metals. This group poses relatively lower risk, as firms are generally better able to adjust supply chains and secure alternative sources.

Indirect Impacts on Industries

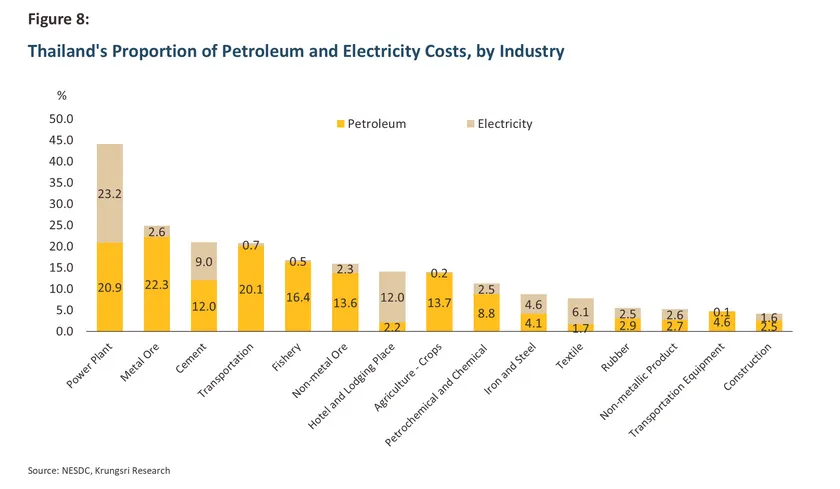

1) Rising Energy Costs

The Middle East conflict, by driving up energy costs, will affect energy-intensive industries. Analysis of energy cost structures shows that the power generation sector is the most vulnerable intermediate industry, with petroleum (primarily natural gas) and electricity costs accounting for 44.1% of total operating expenditures. Volatility in energy prices in this sector becomes a fundamental cost that is transmitted across the broader economy, as electricity is a key input for most industries. As such, the power sector faces both direct risks from potential feedstock supply shortages and indirect pressures from rising energy costs.

Downstream industries facing the highest energy cost pressures include metal ore (combined petroleum and electricity costs accounting for 24.9% of total operating expenditures), cement (21.0%), and transportation (20.8%). In particular, tin ore production, which is highly energy-intensive, could create ripple effects across downstream sectors such as automotive manufacturing, electronics, and food packaging (canning). The transportation sector faces risks across water, road, and air transport due to its heavy reliance on fuel.

The impact may extend further to agriculture and fisheries, where energy costs account for 16.9% for fisheries and 13.9% for agricultural services, potentially increasing production costs across the food supply chain. The petrochemical and chemical industry faces not only the risk of feedstock shortages for plastic resins production (32% of total costs), but also 11.3% energy costs for plant operations.

In the services and infrastructure sectors, the tourism industry, particularly hotels, is sensitive to rising electricity costs, which account for 12% of the total cost structure. For the construction sector, while energy proportions are not exceptionally high, rising energy costs in cement, iron, and steel production (key construction inputs) may be passed through significantly to construction and infrastructure project budgets nationwide.

2) Export Market Demand Slowdown

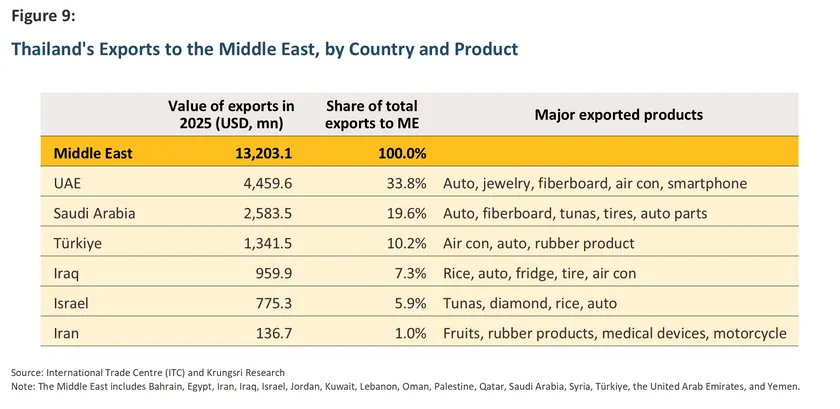

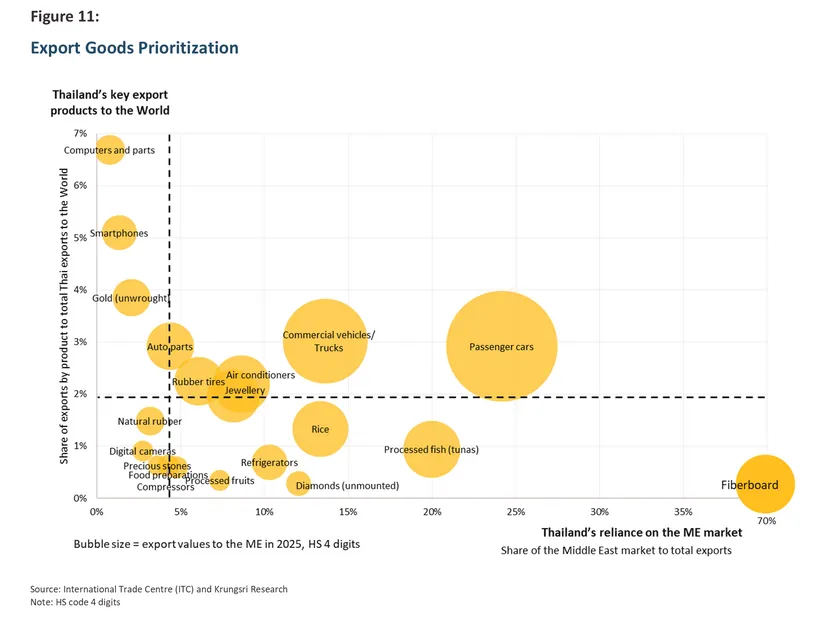

While Thailand is a net importer from the Middle East, the region also serves as an important export market. In 2025, Thailand's exports to the Middle East totaled USD 13,203 million, accounting for 3.9% of total exports, with more than half destined for the UAE and Saudi Arabia.

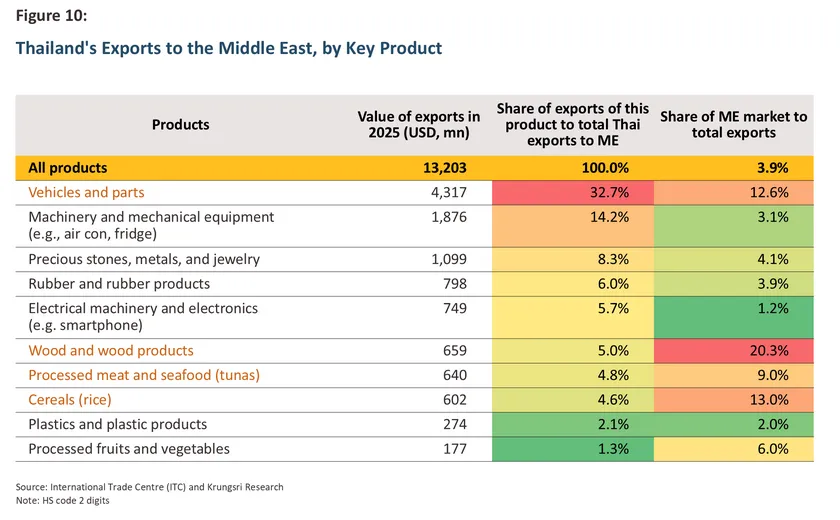

Key export products include vehicles and parts, food products (particularly tuna and rice), air conditioners, jewelry, electronics, rubber, and wood products, many of which are among Thailand's major export categories. This suggests that if regional tensions persist and economic conditions weaken, slowing purchasing power in these markets could negatively affect Thai exporters in these sectors.

Examining export impacts at the product level, affected goods can be grouped into three categories based on overall export value, export value to the Middle East, and the degree of reliance on the Middle Eastern market:

-

High reliance, high export value: Passenger cars (24.2% Middle East reliance), commercial vehicles, air conditioners, rubber tires, and jewelry. This group requires high-priority monitoring, as prolonged regional tensions causing demand slowdown for these goods could broadly impact Thai export performance.

-

High reliance, lower export value: Tuna (20% Middle East reliance), rice, processed fruits, fiberboard (72.8% reliance), and refrigerators. This group also warrants monitoring, though some agricultural and food products may be less affected as the Middle East is expected to continue sourcing these goods to support food security.

-

High export value, low reliance: Hard disk drives (HDDs) and smartphones. This group poses relatively lower risk, as Thailand primarily exports these products to other markets, limiting exposure to potential demand shocks from the Middle East.

3) Logistics Disruptions

The closure of strategic routes in the Middle East not only affects energy supply but also creates significant barriers to global trade, particularly container shipping. This segment accounts for about 11% of global seaborne trade, with approximately 26 million containers passing through the region annually. Recent disruptions have left more than 150 vessels carrying around 450,000 containers stranded at sea, effectively severing the Asia–Europe trade corridor. As a result, delivery delays are emerging for goods that depend heavily on this route, particularly electronics, automotive parts, and retail goods, which could eventually lead to inventory shortages in global markets. Perishable agricultural products transported in refrigerated containers also face the risk of significant spoilage if transit delays persist.

Furthermore, the shipping disruption has caused freight rates to rise rapidly due to: (1) significantly longer transit distances. According to the Thailand National Shippers' Council (TNSC)5/, ships must reroute around the Cape of Good Hope, adding 7,500 km and a total transit time of 35–40 days. This diversion occurs because the Bab-el-Mandeb Strait, a key Asia-Europe connector through the Red Sea and Suez Canal, is under the influence of Houthi and Hezbollah forces acting as Iranian proxies; (2) higher energy prices directly increasing transport costs; and (3) elevated risk-related surcharges, such as war risk premium, congestion surcharge, emergency surcharge, and Transit Disruption Surcharge of up to USD 1,500 per TEU or USD 3,500 per refrigerated container (reefer). Together, these factors lead to longer lead times for goods and raw materials, as well as significantly higher transportation costs for industries. If the conflict persists, the risk of shortages of goods and critical raw materials transported along this route will increase, including agricultural inputs such as urea fertilizer.

Escalating conflict has also severely disrupted the global aviation industry. Airspace closures across multiple countries, including Iran, Iraq, Israel, Bahrain, Kuwait, Qatar, and Syria, have forced the cancellation or rerouting of more than 20,000 flights, stranding over 1 million passengers worldwide6/. Major hub airports in Dubai, Abu Dhabi, and Doha were either temporarily closed or operating at limited capacity following attacks, disrupting the key Europe–Asia aviation corridor via the Persian Gulf. Jet fuel prices surged by 56% following the initial strikes, rising from USD 2.5 per gallon in late February to USD 3.95 on March 6, pushing airfares sharply higher. At the same time, flight suspensions and restrictions have reduced belly cargo capacity on passenger aircraft, disrupting global air freight networks. As a result, spot freight rates on the Asia–Europe route have risen significantly due to rerouting, as well as capacity, crew, and airport slot constraints.

This situation presents both opportunities and risks for Thailand. Some Thai carriers have rerouted direct flights to Europe, benefiting from higher load factors as passengers increasingly prefer direct routes. However, cargo operations may face higher freight rates, reduced capacity, and longer transit times due to rerouting. These disruptions could particularly affect exporters of time-sensitive or high-value goods, such as electronics, fresh produce, pharmaceuticals, and aircraft parts, which may require longer advance booking periods. If the conflict persists, supply shock risks for Thailand’s industrial sector are likely to increase. Prolonged disruptions to aviation networks could last for several weeks and ultimately affect logistics systems, tourism flows, and the broader global economy.

Thailand's Response Measures and Impact Mitigation

The government has introduced measures to address risks arising from the conflict, particularly in the energy sector, with a focus on maintaining energy supply stability and mitigating impacts on the cost of living. Key measures include:

Oil Security

-

Oil Reserves: On March 6, 2026, the Ministry of Energy confirmed that Thailand currently holds a total petroleum reserve (including both domestic stockpiles and in-transit stocks) sufficient for approximately 65 days of domestic consumption without additional imports. Confirmed purchase orders for an additional 30 days of supply bring Thailand’s total effective reserves to around 90–95 days7/.

-

Diversification of crude oil import sources: While the majority of Thailand's crude oil imports come from the Middle East, Thailand has been diversifying its energy imports from other regions, including the U.S., West Africa, and Malaysia. Currently, approximately 42% of crude oil imports come from non-Middle Eastern sources, helping reduce supply risks associated with disruptions in any single region.

-

Price stabilization measures: The government is using the Oil Fund to help maintain domestic energy price stability, particularly temporarily capping diesel prices, to limit the impact on transportation costs and household living expenses.

Electricity Security

-

LNG procurement: Thailand sources roughly one-quarter of its LNG imports from the Middle East, particularly Qatar, making supply disruptions a potential concern. In response, the government is seeking alternative LNG sources such as the U.S. and Myanmar to diversify supply risks. The Energy Regulatory Commission (ERC) has approved the procurement of three additional LNG cargoes for delivery during March–April 2026 to support fuel supply for electricity generation.

-

Potential policy adjustments for fuel and electricity cost management: If the conflict persists, the government may adopt power generation management measures similar to those implemented during the Russia–Ukraine crisis. These could include prioritizing lower-cost domestic gas (e.g., from the Gulf of Thailand), maximizing the use of coal-fired and hydropower plants to reduce reliance on LNG, purchasing surplus electricity from small power producers, and implementing a two-tier electricity pricing structure with lower rates for households than for industrial users to help ease the public’s financial burden.

However, these measures can only provide short-term relief and may not fully offset the impact if the Middle East conflict persists and keeps global energy prices elevated over an extended period.

Krungsri Research View

From a macroeconomic standpoint, tensions between the U.S. and Iran represent a significant risk to both the global economy and the Thai economy. The primary impacts are likely to be transmitted through the supply channel, particularly via higher global energy prices. However, if tensions intensify and persist, additional effects could emerge through the demand channel and financial markets.

For Thailand, the overall impact will depend on the severity and duration of the conflict in the Middle East. The main transmission mechanism would be through higher energy costs, rising goods prices, and increased transportation costs, which would put upward pressure on inflation and could reduce Thailand’s economic growth by around -0.2 to -0.9 percentage points from the baseline.

The ongoing conflict is likely to increase downside risks to Thailand’s economic growth forecast for 2026, which Krungsri Research projected at 2.0% (as of February 26, 2026). However, measures such as energy stockpiling, diversification of oil import sources, efforts to strengthen energy security, and policies aimed at stabilizing domestic prices should help Thailand maintain a certain degree of resilience to short-term shocks. At the same time, it will be important to closely monitor the government’s policy direction and potential economic stimulus measures going forward.

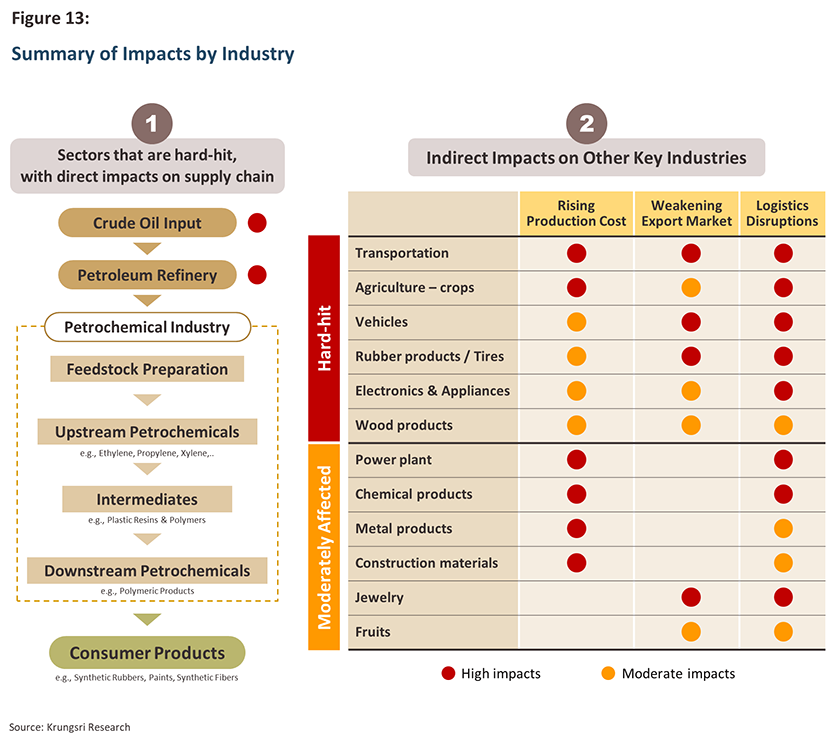

Thailand must also remain vigilant about potential impacts on the industrial sector, which are expected to vary in severity depending on industry structure, as follows:

-

Hard-hit industries: (1) Directly affected industries, including oil refineries, petrochemicals, and power generation, that may face feedstock supply shortages. This category also includes industries highly reliant on inputs from the Middle East, particularly energy-intensive sectors, agriculture, construction materials, and petrochemical-dependent industries such as plastics, where supply chain disruptions could significantly raise production costs. (2) Indirectly affected industries exposed to all three impact channels, including rising energy costs, weakening export demand from the Middle East, and logistics disruptions affecting the delivery of goods and raw materials. These include transportation, agriculture, automotive, electronics, rubber products, and wood products.

-

Moderately impacted industries: Primarily heavy industries that are mainly affected by rising production and operating costs, such as metals, chemicals, and gems and jewelry.

The overall magnitude of the impact will depend primarily on the duration of the conflict. This situation also underscores the importance of diversifying energy and raw material supply sources for countries, including Thailand, in order to strengthen long-term economic resilience.

1/ War Crisis Hits Tourism: Europe–Middle East Visitor Markets Contract by 18% | Thai Post

2/ Almost all LNG imports through the Strait of Hormuz originate from Qatar.

3/ The remaining LNG imports are mostly from the U.S., Australia, and Malaysia, collectively accounting for over 50% of total imports.

4/ 'Urea fertilizer not scarce, supply lasts through August 2026' | BangkokBizNews

5/ 'War disrupts sea freight; Thai exporters fear shipping lines halting bookings, freight rates surge' | BangkokBizNews

6/ ‘Iran strikes disrupt flights: Why travel insurance may fall short | CNBC

7/ 'Atthapol confirms Thailand not facing oil shortage; energy sector ready to handle Middle East crisis'| Post Today