Executive Summary

The 2026 Middle East conflict has disrupted global energy supply in ways that differ from past crises, particularly due to damage to multiple key energy infrastructure facilities. As a result, energy prices are likely to remain elevated for an extended period, even if the intensity of the conflict subsides.

ASEAN economies are directly exposed to these risks due to their reliance on imported energy and production inputs transported through the Strait of Hormuz. The impact therefore extends beyond oil prices to include liquefied natural gas (LNG), food costs, and other critical inputs. When considering vulnerabilities related to import dependence and external stability, the Philippines, Lao PDR, and Cambodia are among the most exposed economies, while Thailand, Indonesia, and Vietnam face relatively lower — but still notable — risks.

Many countries have adopted subsidy measures to limit the pass-through of higher energy prices to consumers, but these policies are increasingly weighing on fiscal stability. Diversifying import sources and implementing targeted support measures are therefore crucial to preserve fiscal space in a potentially more prolonged crisis environment.

Introduction

Since late February 2026, military conflict involving the United States, Israel, and Iran has caused a significant disruption to global energy supply, particularly affecting shipments through the Strait of Hormuz, where Iran has intermittently obstructed and closed shipping routes. The strait represents a critical strategic chokepoint for the transportation of crude oil, petroleum products, liquefied natural gas (LNG), and other key commodities to global markets.

While supply-driven energy price spikes are typically short-lived once geopolitical tensions subside, the current crisis may differ from past episodes. Military attacks by both sides have damaged key energy infrastructure across several key locations, potentially delaying supply recovery compared with previous conflicts1/. As a result, energy prices are likely to remain elevated for an extended period. According to the International Energy Agency (IEA)’s March 2026 Oil Market report, disruptions to the Strait of Hormuz have removed approximately 8% of total daily global oil supply from the market. Meanwhile, infrastructure damage could interrupt part of Qatar’s LNG production capacity for as long as 3–5 years, with limited scope for short-term replacement from alternative sources (QatarEnergy, cited in Reuters, 2026).

Given that most ASEAN economies rely heavily on imports of energy and other critical inputs from the Middle East, the region is particularly vulnerable to delays or disruptions in shipments passing through the Strait of Hormuz. The conflict has therefore raised concerns about the risk of stagflation in net energy-importing economies, characterized by slowing growth alongside persistently elevated inflation. Against this backdrop, this article focuses on three key areas of analysis: 1) transmission channels of the Middle East conflict affecting ASEAN economies; 2) the vulnerability of ASEAN countries to disruptions in energy and food imports, as well as external stability risks; and 3) policy responses related to energy price controls and the potential implications for fiscal stability.

Transmission Channels to ASEAN Economies

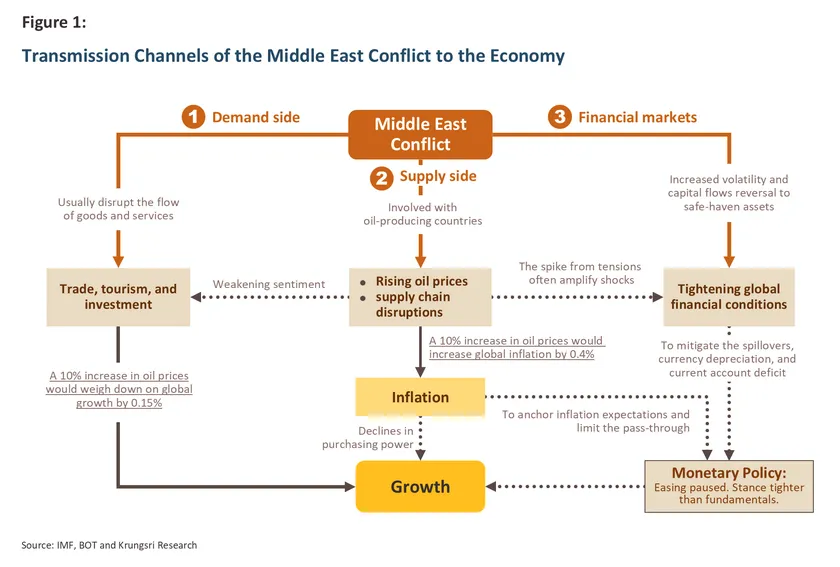

In general, conflicts in the Middle East tend to affect small open economies through three primary transmission channels:

1) supply-side pressures, particularly through higher costs of energy, food, and other key production inputs;

2) demand-side pressures, transmitted via trade, investment, and tourism; and

3) financial market pressures, reflected in tighter financial conditions and declining asset prices (Figure 1).

In the short term, the most significant effects are likely to arise from supply-side pressures due to: 1) disruptions to the transportation of energy and production inputs, including crude oil, LNG, and other essential intermediate goods; and 2) delays in maritime shipping and logistics systems, which have led to a rapid increase in freight rates and marine insurance costs. These constraints are expected to translate into higher inflationary pressures in net energy-importing economies and could also disrupt supply chains more broadly in the event of feedstock shortages.

In addition, short-term spillovers may also materialize through tighter financial conditions, as heightened uncertainty tends to lead to declines in risk asset prices and capital outflows from certain economies. At the same time, rising inflation risks may compel central banks to maintain a tighter monetary policy stance than implied by underlying economic fundamentals. Such conditions could dampen private consumption through the wealth effect, as well as through higher financing costs.

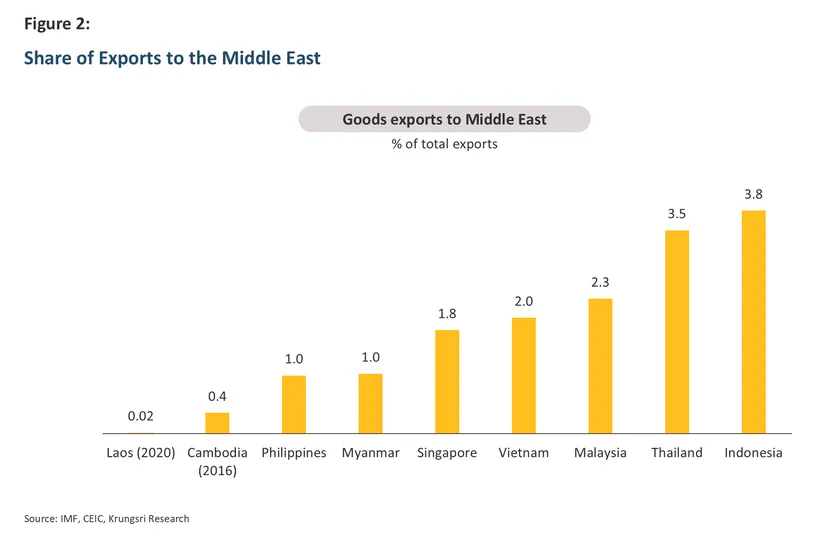

On the demand side, the short-term impact on trade and investment is expected to remain limited, as ASEAN exports to the Middle East account for less than 4% of total exports (Figure 2).

However, the tourism sector has already begun to show signs of impact. Heightened security concerns, together with airspace closures and the shutdown of several airports in the Middle East, are causing some travelers from Europe and the U.S. to postpone travel to Asia.

If the conflict becomes prolonged and extends to other strategic maritime chokepoints, such as the Bab el-Mandeb Strait, the risk of broader global supply chain disruptions would rise substantially, further weighing on investor confidence and intensifying demand-side pressures.

ASEAN Vulnerabilities to Commodity Imports and External Stability References

Vulnerability to Commodity Imports

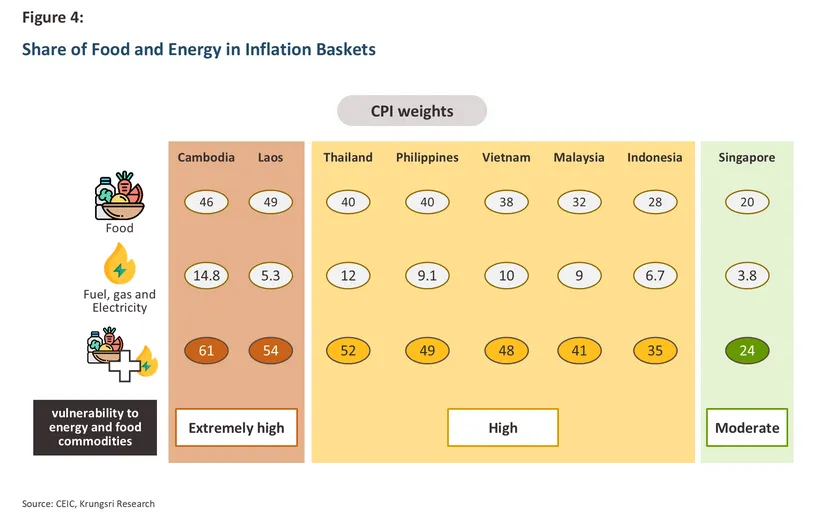

Although this article primarily focuses on energy, other key commodities, particularly food, must also be considered in the ASEAN context, as several economies in the region are net food importers and rely heavily on energy as a critical production input. Even food-producing economies depend on imported intermediate inputs, such as fertilizers sourced largely from the Middle East. Moreover, the share of food in inflation baskets across ASEAN economies is significantly higher than in advanced economies

2/.

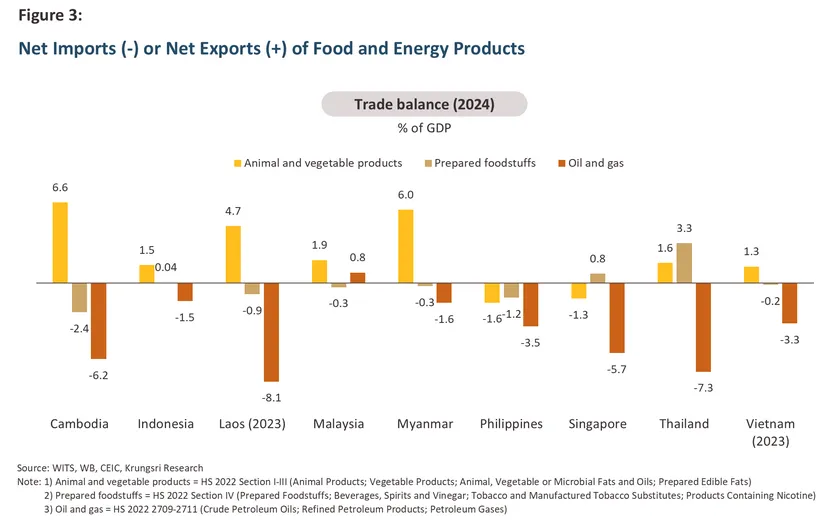

As a result, the region is particularly vulnerable to disruptions in both energy and food imports amid tightening supply conditions. Vulnerabilities can be classified based on each country’s net import or

net export position in key commodities, reflecting the degree of import dependence of each country (Figure 3).

- Highly vulnerable economies are those that are net importers of both energy and food (energy and food deficit), including the Philippines, Lao PDR, and Cambodia. The Philippines relies heavily on oil imports from the Middle East, alongside relatively high dependence on food imports. In addition, the share of food and energy in its inflation basket is the highest among regional peers (49% in Figure 4). Meanwhile, Lao PDR is particularly vulnerable given its landlocked geography, which necessitates full reliance on imported oil, as well as its status as a net importer of processed food products3/.

-

Moderately vulnerable economies are those that are net importers of either energy or food (energy or food deficit), including Thailand, Indonesia, and Vietnam. Within this group, Thailand exhibits the highest vulnerability due to its heavy reliance on imported oil and natural gas, combined with a relatively large weight of energy and food in its inflation basket. Although Thailand is a net food exporter, it remains dependent on imported key inputs such as fertilizers from the Middle East4/. Indonesia faces somewhat lower vulnerability despite being a major exporter of several commodities, as it remains a net oil importer and exhibits sensitivity to fluctuations in energy and food prices, as reflected in the relatively high share of food and energy in its inflation basket. Vietnam’s primary vulnerability lies in energy dependence, particularly its heavy reliance on crude oil imports from Kuwait (more than 80% of total imports). Rapid industrial expansion has also driven strong growth in energy demand, while strategic petroleum reserves remain limited, covering less than one month of consumption5/.

Vulnerability to External Stability

Beyond vulnerabilities arising from commodity imports, global financial market conditions may also affect ASEAN economies through external stability risks, particularly via exchange rate volatility that could increase the burden of foreign-currency-denominated debt. Countries with higher vulnerability are typically those that rely heavily on external financing and maintain relatively high levels of external debt.

-

Economies reliant on external financing, such as Indonesia and the Philippines, face structural vulnerabilities associated with twin deficits — current account deficits alongside fiscal deficits — and therefore require sustained capital inflows. Heightened geopolitical risks tend to trigger capital outflows from higher-risk emerging markets, exerting depreciation pressure and greater exchange rate volatility relative to regional peers.

-

Economies with elevated external debt burdens, such as Lao PDR, are particularly exposed to exchange rate fluctuations, as currency depreciation increases the local-currency value of foreign debt obligations.

-

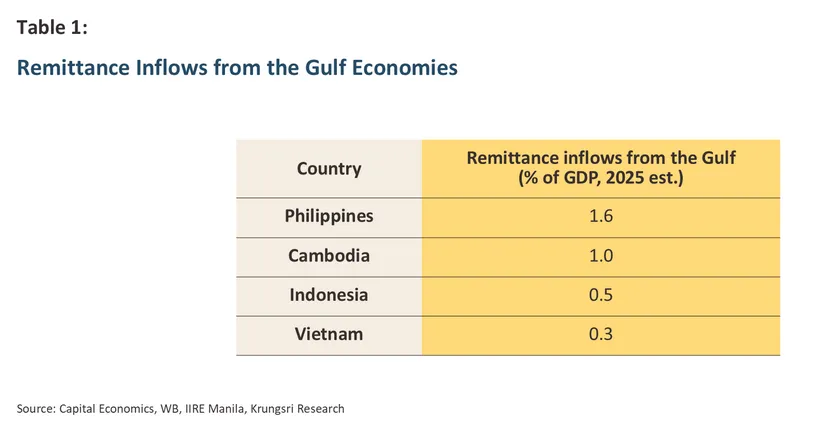

In addition, the Philippines faces further exposure through reliance on remittance inflows, particularly from the Gulf Cooperation Council (GCC) economies6/. While remittances from GCC countries account for approximately 1.6% of the Philippines’ GDP, they represent a meaningful share of total remittance inflows, which amount to around 8% of GDP. Remittances from the GCC account for roughly 18% of total remittance receipts, making them an important source of external income that could be adversely affected should economic conditions in Gulf economies weaken significantly (Table 1).

Ranking ASEAN Economies by Vulnerability

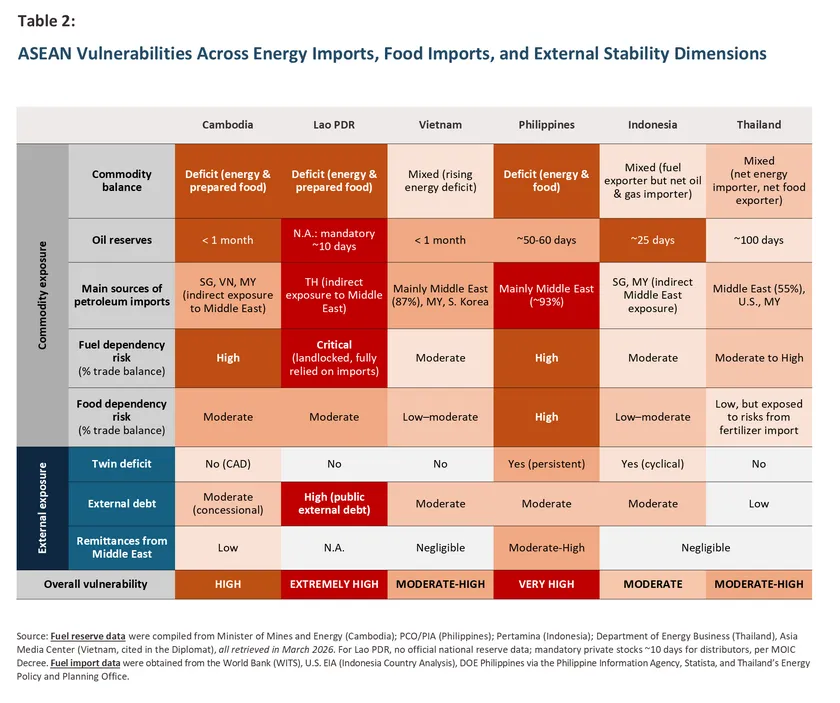

Considering vulnerabilities related to commodity imports (energy and food) alongside external stability risks (Table 2), the economies facing the highest overall exposure are Lao PDR and the Philippines. The Philippines exhibits elevated vulnerability due to its strong reliance on both energy and food imports, combined with dependence on external financing. Meanwhile, Lao PDR faces similar constraints but with more severe structural vulnerabilities, including heavy dependence on imported energy and a high external debt burden.

For Cambodia, although import-related vulnerabilities are broadly comparable to the above group, external stability risks are more moderate. Despite persistent current account deficits, external financing is largely supported by concessional loans. In addition, exchange rate volatility remains relatively low due to a crawl-like exchange rate management framework.

The next tier of vulnerability includes Thailand, Indonesia, and Vietnam. Thailand’s exposure primarily stems from its reliance on energy imports, but this risk is partly mitigated by relatively strong external stability. Indonesia, despite being a major exporter of several commodities, remains a net oil importer and continues to rely on foreign capital inflows. For Vietnam, the key vulnerability lies in its heavy reliance on crude oil imports from the Middle East, combined with strong expansion in urbanization and industrial activity.

Energy Price Policy Responses in ASEAN

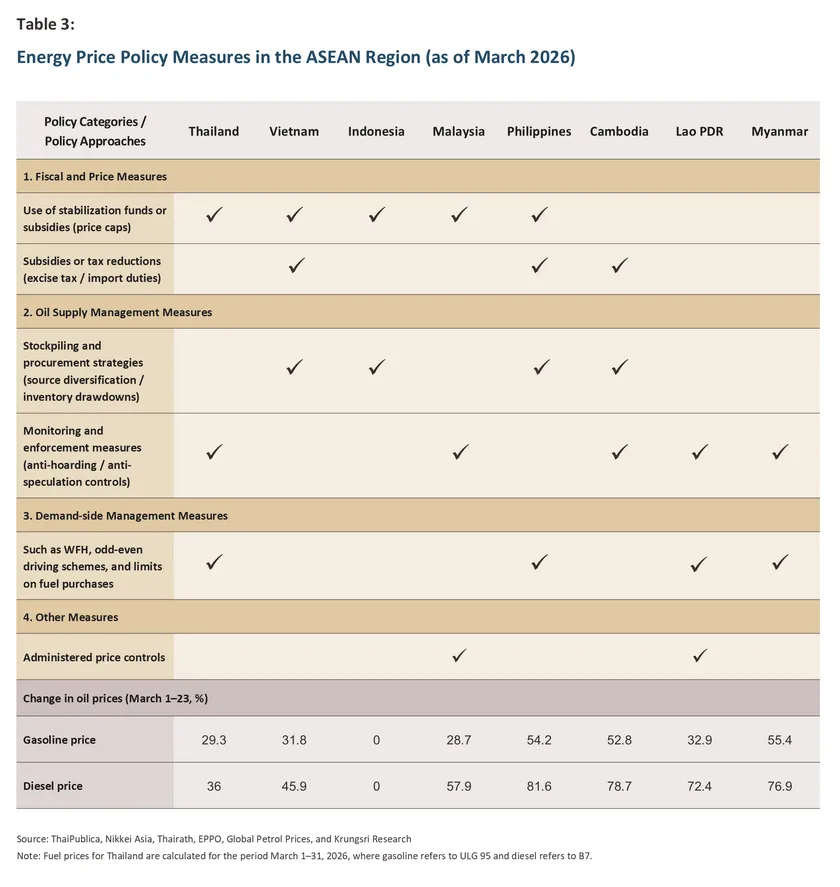

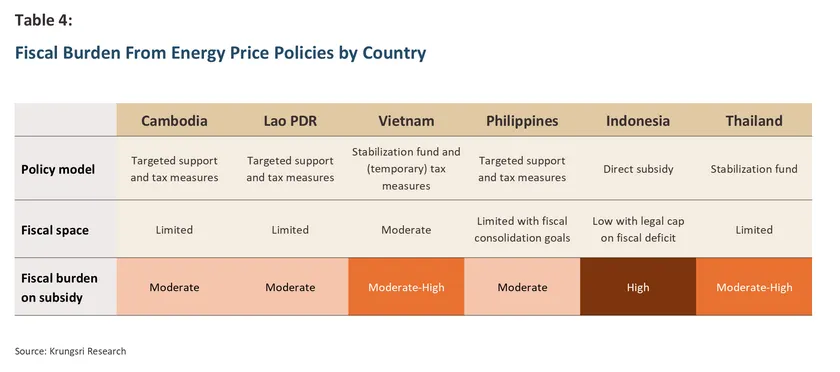

Amid the rapid increase in global oil prices, ASEAN economies have adopted a range of policy measures to mitigate the impact, including reductions in excise taxes, price subsidies, anti-hoarding measures, and adjustments to public sector working days (Table 3).

Policy approaches to energy price management can be classified into three main categories:

-

Group 1: Economies implementing direct price subsidies such as Indonesia and Malaysia. Indonesia maintains fixed retail fuel prices, with the government compensating for the price differential, resulting in elevated fiscal risks. Malaysia, meanwhile, adopts a targeted subsidy approach, which helps partially contain fiscal costs but still entails some budgetary burden.

-

Group 2: Economies utilizing stabilization funds to mitigate price volatility such as Thailand and Vietnam. These countries utilize oil stabilization funds to smooth price volatility and partially limit the pass-through of global energy prices. While this approach provides greater flexibility, it may still pose fiscal risks if global oil prices remain elevated for a prolonged period.

-

Group 3: Economies adopting targeted support alongside tax measures, such as the Philippines, Cambodia, and Lao PDR. These policies emphasize tax reductions or targeted assistance for affected groups. Most recently, Vietnam (March 2026) has introduced temporary reductions and exemptions on certain energy-related taxes and fees, including parts of excise taxes, with measures in effect until April 15, 2026.

Overall, most ASEAN economies have attempted to slow the pass-through of rising global energy prices to domestic consumers, reflecting a trade-off between protecting household purchasing power and maintaining fiscal sustainability.

As shown in Table 4, Indonesia faces the highest fiscal risk due to extensive energy price subsidies alongside relatively limited fiscal space. Thailand and Vietnam rely on stabilization funds, resulting in moderate fiscal exposure but with increasing risks if high energy prices persist. The Philippines, Cambodia, and Lao PDR rely more heavily on market-based pricing mechanisms and tax measures, leading to lower fiscal subsidy burdens but greater pass-through of energy prices to consumers.

Krungsri Research View

The current Middle East conflict has disrupted global energy supply through intermittent closures of the Strait of Hormuz, attacks on key energy infrastructure across the region, and most recently, the March 19, 2026 attack on LNG infrastructure in Qatar — the world’s second-largest LNG exporter.

These developments suggest that the current supply shock is more complex than previous episodes, characterized by simultaneous disruptions across multiple segments of the energy supply chain. For ASEAN, the impact of this crisis extends beyond oil and gas prices to other production inputs that rely on imports from the Middle East, thereby affecting the cost of living, production costs, and broader economic activity.

Comparisons with the 1990–1991 Gulf War (Iraq–Kuwait), which represents one of the closest historical parallels, reveal both similarities and important differences. In terms of similarities, oil prices in 1990 surged from around USD 15 to USD 40 per barrel within a few months, a pattern comparable to recent price dynamics. However, the current Middle East conflict differs from the Gulf War in at least three key dimensions, as follows:

-

First, energy risks are no longer limited to crude oil. In 1990, LNG had not yet emerged as a major global commodity, particularly in Asia (IEA, 2019; Enerdata, 2020). At present, however, risks extend to both oil and LNG, which are closely linked to fertilizer and food supply chains (Quitzow et al., 2025; FAO, 2025), causing broader spillovers to ASEAN economies beyond oil prices alone.

-

Second, widespread damage to energy infrastructure across multiple strategic locations may prolong supply recovery relative to past crises. Persistently tight supply conditions could therefore keep energy prices elevated for an extended period, even if geopolitical tensions begin to ease.

-

Third, many economies face constraints in deploying fiscal policy, as elevated public debt accumulated during the COVID-19 crisis has reduced fiscal buffers compared with the past, limiting the scope to maintain energy subsidy measures over the longer term.

Lessons from past crises highlight three key insights: 1) heavy reliance on concentrated energy supply sources increases vulnerability to external shocks; 2) prolonged energy price controls create fiscal burdens and distort market mechanisms; and 3) economies with stronger external stability, as well as greater energy and food security, are better positioned to withstand volatility.

In the current context, ASEAN economies should accelerate the diversification of energy import sources and design targeted, time-bound support measures to contain long-term fiscal burdens while preserving fiscal space. Priority should be given to initiatives that enhance economic efficiency amid an increasingly complex global environment, where crises may become more prolonged than in the past.

References

Alcorta, A., Mithal, A., Molloy, P., & Weiss, T. (2026, January 28). Cultivating a lower-carbon food supply chain: Unlocking Scope 3 progress through fertilizer emissions reduction. Retrieved from Center for Green Market Activation: https://gmacenter.org/news/article-cultivating-a-lower-carbon-food-supply-chain-unlocking-scope-3-progress-through-fertilizer-emissions-reduction/

Enerdata. (2020, September). The new LNG markets and their geopolitical implications. Retrieved from https://www.enerdata.net/publications/executive-briefing/lng-markets-and-geopolitical-implications-enerdata-brief.pdf

FAO. (2025, June). Fertilizer market update. Retrieved from Food Outlook: https://openknowledge.fao.org/server/api/core/bitstreams/0c79f9df-b2eb-43cb-9b84-977efea5b197/content

IEA. (2019, June 19). LNG Market Trends and Their Implications. Retrieved from https://www.iea.org/reports/lng-market-trends-and-their-implications

IEA. (2026, March 12). Oil Market Report - March 2026. Retrieved from https://www.iea.org/reports/oil-market-report-march-2026

IIRE Manila. (2026, March 19). On the Middle East crisis and the Philippines. Retrieved from International Viewpoint: https://internationalviewpoint.org/On-the-Middle-East-crisis-and-the-Philippines

Kpler. (2026, March 5). Middle East conflict - oil market implications: a continuing assessment. Retrieved from https://www.kpler.com/blog/middle-east-conflict---oil-market-implications-a-continuing-assessment?utm_source__c=chatgpt.com

Nikkei Asia. (2026, March 5). Fuel anxiety spreads in Asia as Hormuz closure throttles supplies. Retrieved from https://asia.nikkei.com/business/energy/fuel-anxiety-spreads-in-asia-as-hormuz-closure-throttles-supplies

Quitzow, R., Balmaceda, M., & Goldthau, A. (2025, January 17). The nexus of geopolitics, decarbonization, and food security gives rise to distinct challenges across fertilizer supply chains. One Earth, 8(1). Retrieved from https://www.sciencedirect.com/science/article/pii/S2590332224006031

Reuters. (2026, March 20). Exclusive: Iran attacks wipe out 17% of Qatar’s LNG capacity for up to five years, QatarEnergy CEO says. Retrieved from https://www.reuters.com/business/energy/iran-attack-damage-wipes-out-17-qatars-lng-capacity-three-five-years-qatarenergy-2026-03-19/

ThaiPublica. (2026, March 8). ASEAN Roundup อาเซียนออกมาตรการดูแลความมั่นคงพลังงาน หลังราคาน้ำมันพุ่งจากสงครามตะวันออกกลาง. Retrieved from https://thaipublica.org/2026/03/asean-weekly-roundup-344/

Thairath. (2026, March 17). Measures Taken by 10 Asian Countries to Tackle the Oil Crisis Triggered by the Iran War. Retrieved from https://en.thairath.co.th/scoop/world/2920719

1/ Tightness in energy supply reflects 1) concentrated spare production capacity in the Persian Gulf that cannot be exported if the Strait of Hormuz is closed; 2) refining disruptions due to infrastructure damage; and 3) limited substitutability of alternative shipping routes (Kpler, 2026).

2/ The share of food in inflation baskets in the U.S. and the European Union is approximately 13–14%, whereas in ASEAN economies the share is significantly higher, at around 30–40%.

3/ Although Lao PDR and Cambodia are net exporters of primary food products (mainly agricultural raw materials), their domestic capacity for food processing and production of processed food remains limited. As a result, both economies continue to rely on imports of processed food products, leaving them exposed to food security risks, particularly under conditions of tight global supply. In the case of Lao PDR, currency depreciation would further increase import costs.

4/ See also Middle East Tensions: Implications for Thailand’s Economy and Industries

5/ Vietnam Asks Japan, South Korea For Help Accessing Crude Oil Supplies, The Diplomat (March 17, 2026)

6/ The Gulf States, or the Gulf Cooperation Council (GCC), refer to the six member countries: Saudi Arabia, the United Arab Emirates, Kuwait, Qatar, Bahrain, and Oman,

which are part of the broader Middle East region. Remittance inflows received by Filipino workers are sourced primarily from GCC economies.