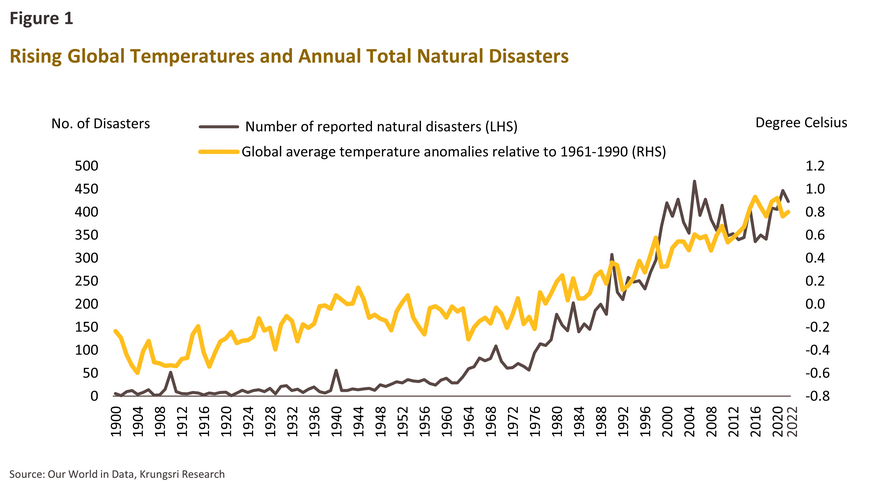

At the global level, the broadening and intensifying range of problems facing the environment is reaching a pitch that can no longer be ignored, while at the national level, Thailand was ranked the country 9th most seriously affected by long-term climate impacts over 2000 to 2019.1/ The severity of the current situation was only underscored by the UN Secretary General’s recent comments that “the era of global boiling has arrived”, and it is now clear that without rapid action, humanity faces the near-term threat of rapidly escalating environmental crises.

Against this background, businesses and other stakeholders across society are in the process of establishing and working towards global and national targets that are focused on adaptation and mitigation, including most obviously those that address net zero emissions and carbon neutrality. However, achieving the goals and tackling environmental problems requires a significant amount of funding. Given this and its role channeling investment flows towards environmentally responsible economic activities, the finance sector has a central role to play as a facilitator of the green transition, and in particular, green financing has the potential to make investing in projects or promoting economic activities that reduce environmental impacts or that remediate environmental damage both simpler and more attractive.

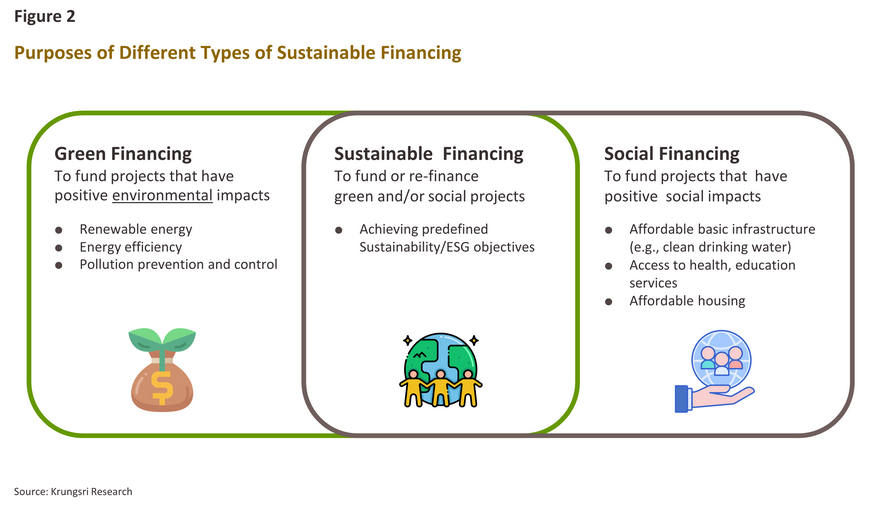

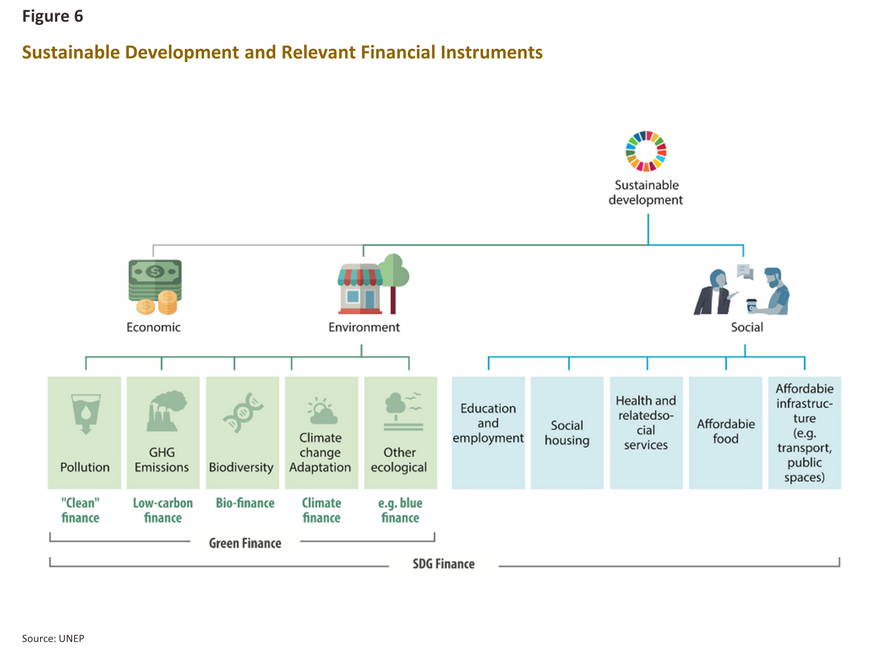

Following the move by the UN to define the 17 Sustainable Development Goals (SDGs) and then to use these to guide global development over 2015 to 2030, issues around sustainability have come to occupy a central place in framing organizational and national planning around the world. The SDGs cover a wide range of goals in the areas of the economy, society, and the environment, and so sustainable financing has become an important tool helping to direct investment funds to activities that yield positive benefits for society and the environment. In practice, many sectors often choose to start with the allocation of funds for environmental purposes (Green financing) as a first step.

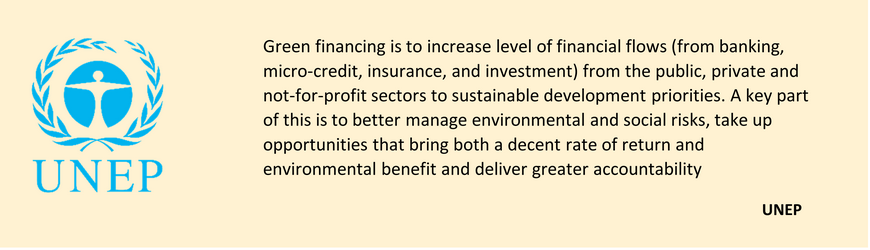

According to the United Nations Environment Programme (UNEP), green financing exists “to increase the level of financial flows (from banking, micro-credit, insurance and investment) from the public, private and not-for-profit sectors to sustainable development priorities. A key part of this is to better manage environmental and social risks, take up opportunities that bring both a decent rate of return and environmental benefit and deliver greater accountability.”

Green financing thus refers to the process of raising capital or sourcing funds through a variety of financial instruments for use in projects or activities that generate environmental benefits, and so green financing helps to bridge the gap between the sometimes contradictory imperatives of environmentalism and capitalism.

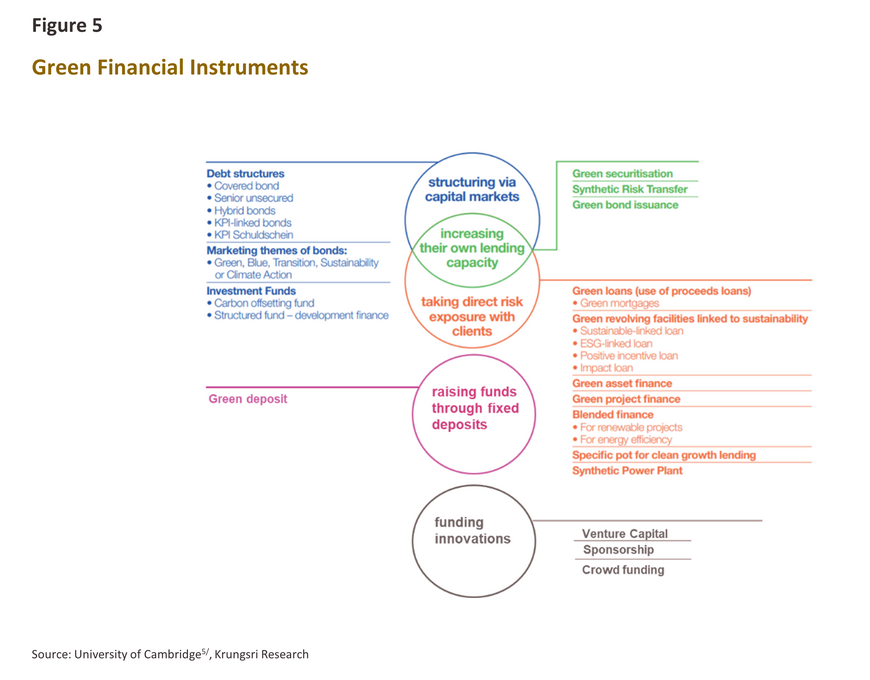

Pro-environment financial instruments

The most important forms taken by green financing are: (i) loan or debt instruments, of which the most significant are (i.a) loan provided by financial institutions, and (i.b) the issuing of green bonds or debentures, in either case with the capital raised from this used to fund economic activities with positive environmental impacts; (ii) equity through shares or green equity funds, with the resulting capital either invested in environmentally friendly activities or in venture capital funds used to support the development of environmental innovations; (iii) deposits, in particular time deposits that direct these savings to investments in businesses or projects with positive environmental impacts4/ ; and (iv) other activities, such as sponsoring startups or environmentally focused projects (Figure 5).

At present, the financial instruments playing a key role in the market for green finance are green bonds and green loans.

Green bonds are bonds issued by state bodies, private-sector organizations, or financial institutions that are used to fund investments in or the re-financing of activities that qualify as environmental projects. Banks may be involved in these processes as: (i) the bond issuer, with the funds raised then used either for direct investment in or to support the issuing of credit to projects or activities with positive environmental impacts; or (ii) the arranger or underwriter of the bond, which will be a client of the bank that needs to raise capital to fund an environmentally focused activity.

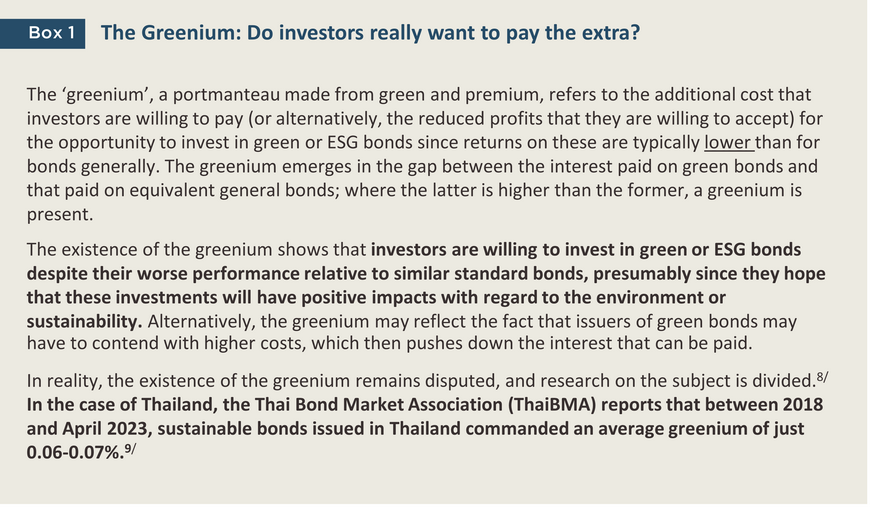

In broad terms, the process for issuing green bonds does not differ substantially from those governing the issuance of any other type of bond, though this will entail the additional step of having to pass set criteria with regard to the nature and goals of the activity being funded and its environmental impacts. Green bonds have proved to be a popular tool to use when raising funds for environmentally friendly activities, largely because of the low associated costs, the flexible qualifying criteria,6/ and the fact that issuers retain full control over the activities being funded. The City UK thus estimates that between 2012 and 2021, green bonds accounted for 93.1% of the value of all green finance raised globally.7/

Green loans channel funds from financial institutions or other types of lenders to borrowers who need financing for the development or overhaul of business processes such that this then yields positive environmental benefits. This typically takes one of two forms: (i) leasing, which is most suitable for spending related to buildings, vehicles, and plant and machinery that is used in business activities or to support other types of environmentally friendly activities; and (ii) project finance, which is preferred for investments in large environmental projects that operate over longer timeframes.

In addition to the financial instruments described above, other ways of raising the capital required to fund environmental projects include: (i) sustainability-linked bonds (SLBs), or bonds that have a variable interest rate that moves in line with the extent to which sustainability performance targets are met, the latter having been set in accordance with the issuer’s key performance indicators; and (ii) sustainability-linked loans (SLLs), or loans that link the interest rates payable on the loan to sustainability targets, thus encouraging borrowers to meet the latter.

Both of these are gaining wider acceptance since issuers of SLBs and SLL borrowers can invest in ESG-related projects while using monies raised from these as working capital.

Adoption of Green Financing

The global situation

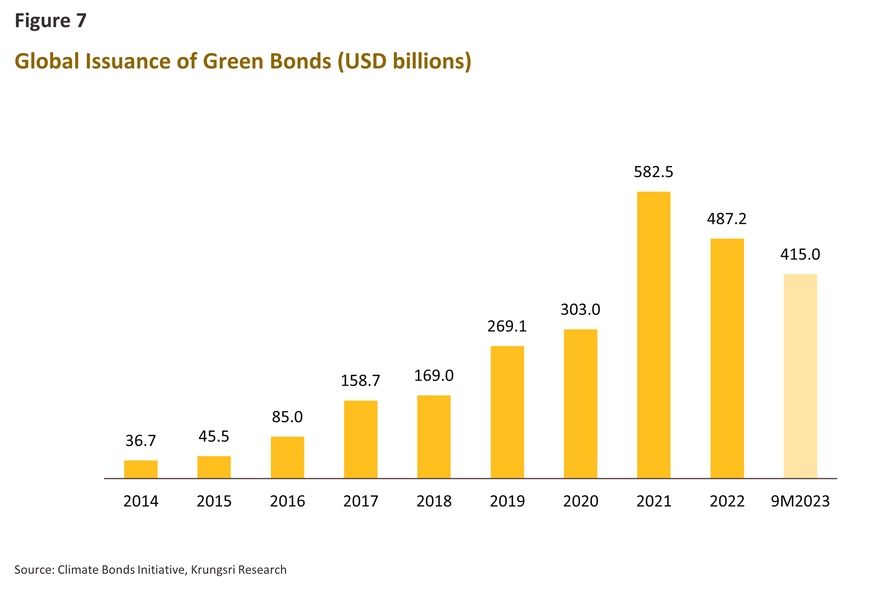

Global issuance of green bonds totaled USD 487.2 billion in 2022, a -16% fall from a year earlier. However, this was the first such decline in a decade12/ (Figure 7) and this disruption to long-term trends can be explained by the combination of uncertain economic conditions and tightening monetary policy in many countries.13/ The situation has now begun to reverse, and over the first 9 months of 2023, issuance of green bonds again increased, rising to USD 415 billion globally, or a 3% YoY rise.14/ Private-sector corporate financial institutions have been the main issuers of these,15/ and over 2014 to 2022, these were responsible for more than a quarter of the total worldwide market for green bonds.

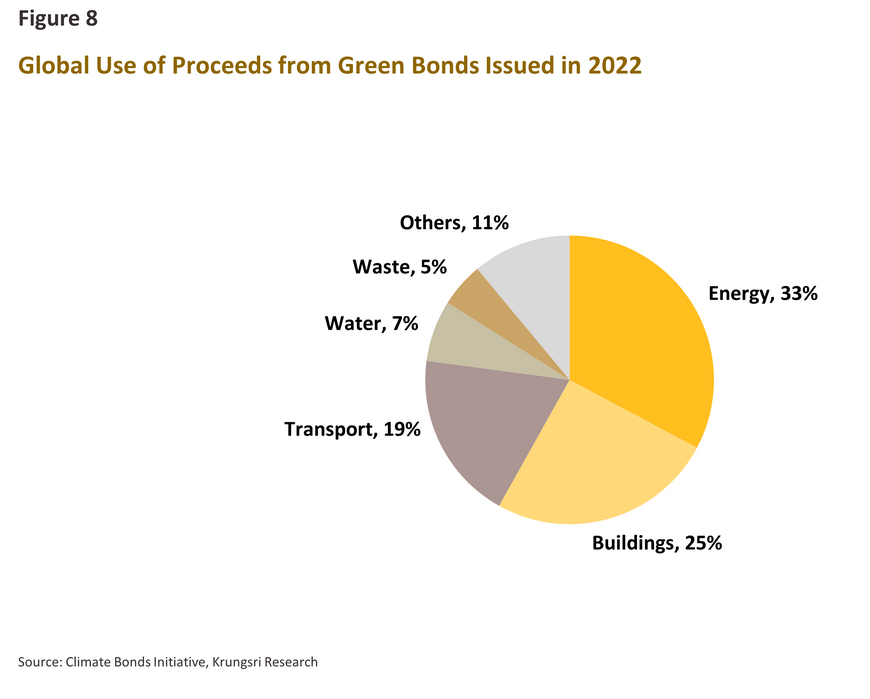

In 2022, capital raised from the issuance of green bonds was most often used in projects in the energy sector (33%) followed by green construction (25%) and transport (19%) (Figure 8).

BNP Paribas estimates that global issuance of green bonds reached around USD 600 billion in 2023, recovering from the 2022 contraction and beating the highs set in 2021. The market continues to be buoyed by the growing global recognition of the need to accelerate the green transition and to preserve what remains of the world’s biodiversity.16/ Likewise, the International Finance Corporation (IFC) forecasts that the total value of green bonds issued in emerging markets (excluding China) grew by 14% in 2023 relative to a year earlier.17/

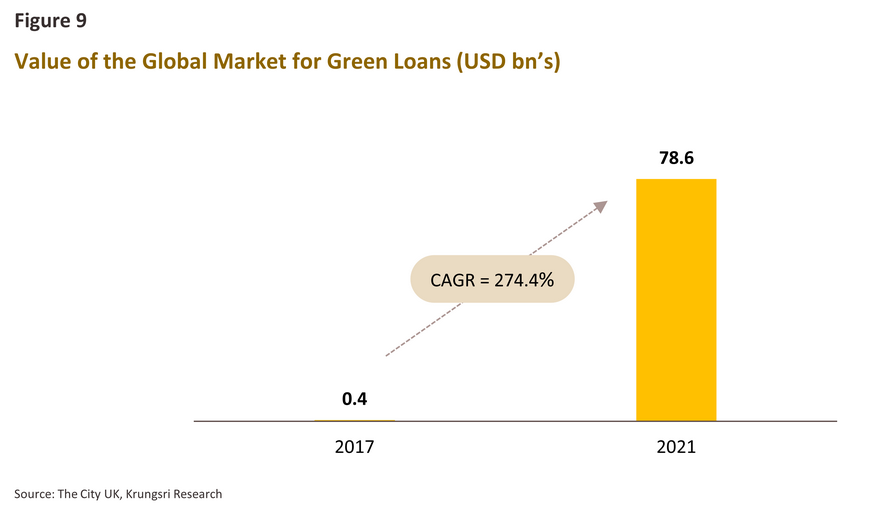

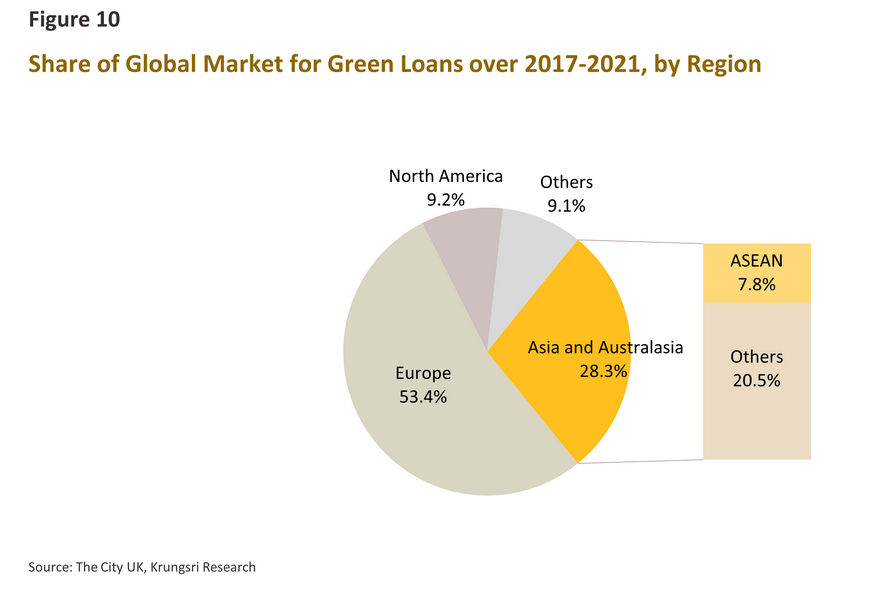

Growth in the other major type of green financing, green loans, has been even more dramatic, and information from The City UK shows that as of 2021, the value of global green lending18/ stood at USD 78.6 billion, up from just USD 432 million in 2017 (Figure 9). Over this period, the main drivers of the market were the European countries, with the ASEAN region accounting for just 7.8% of the global total. Although this percentage is not as high as in Europe, it is close to North America, which accounts for 9.2%, and within the ASEAN region, there is considerable room for future growth.

As environmental concerns deepen, growth in the value of the green finance market will accelerate

The environmental challenges faced by the world are closely entwined with the global economic and political system, and so dealing with these problems will require intense cooperation at the international level. We are therefore seeing governments, businesses and citizens themselves work together around the world to address these issues, and at the level of both nations and organizations, targets are now being set for net zero emissions and carbon neutrality. However, reaching these goals will depend on access to significant financial resources, and so the market for green financing has enormous potential.

In particular, growth will be accelerated by: (i) the global rollout of increasingly ambitious environmental policies; (ii) progress on technology that will make it easier to access relevant technology and more attractive to invest in environmental conservation; and (iii) the accelerating adoption of environmentally friendly policies in the private sector.

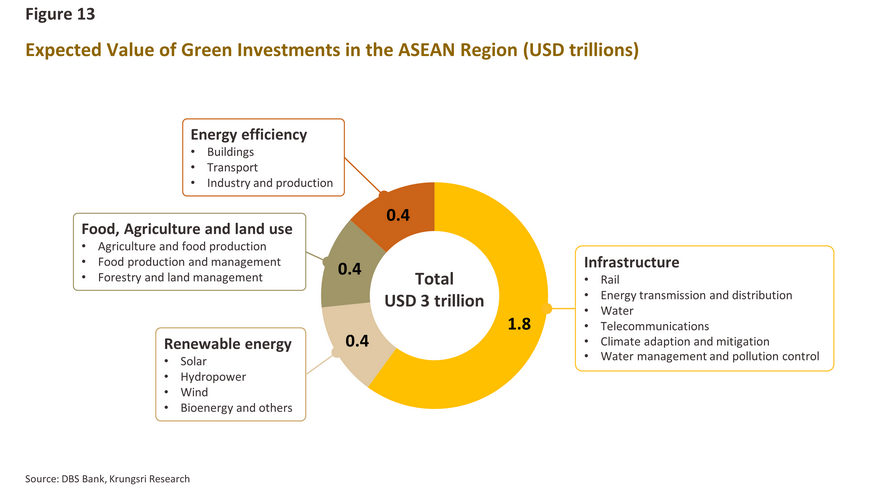

BloombergNEF estimates that by 2050, the cost of reaching net zero commitments will come to more than USD 200 trillion, or around USD 7 trillion annually over this period, but as of 2022, the value of green bond issuance, a key part of the green financing market, came to just 3% of total global bond issuance.20/ With demand for capital for use in environmental projects so high in many regions, there is clearly a major gap in the funding requirements. Bain & Co therefore see 2022 green capital inflows to the ASEAN region reaching USD 5.2 billion, with demand for green financing continuing to grow in the future. The bank DBS also estimates that demand for financing for use in environmental projects in the ASEAN countries will top USD 3 trillion over 2016-2030.21/ This will go mostly to infrastructure projects including the development of rail transport networks and energy transmission and distribution systems, though this will come at a cost of more than USD 1.8 trillion (Figure 13).

The Thai context

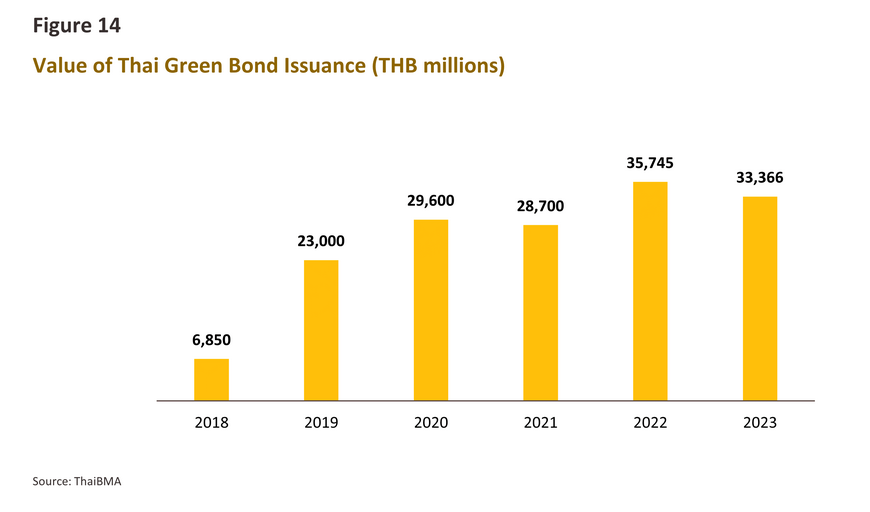

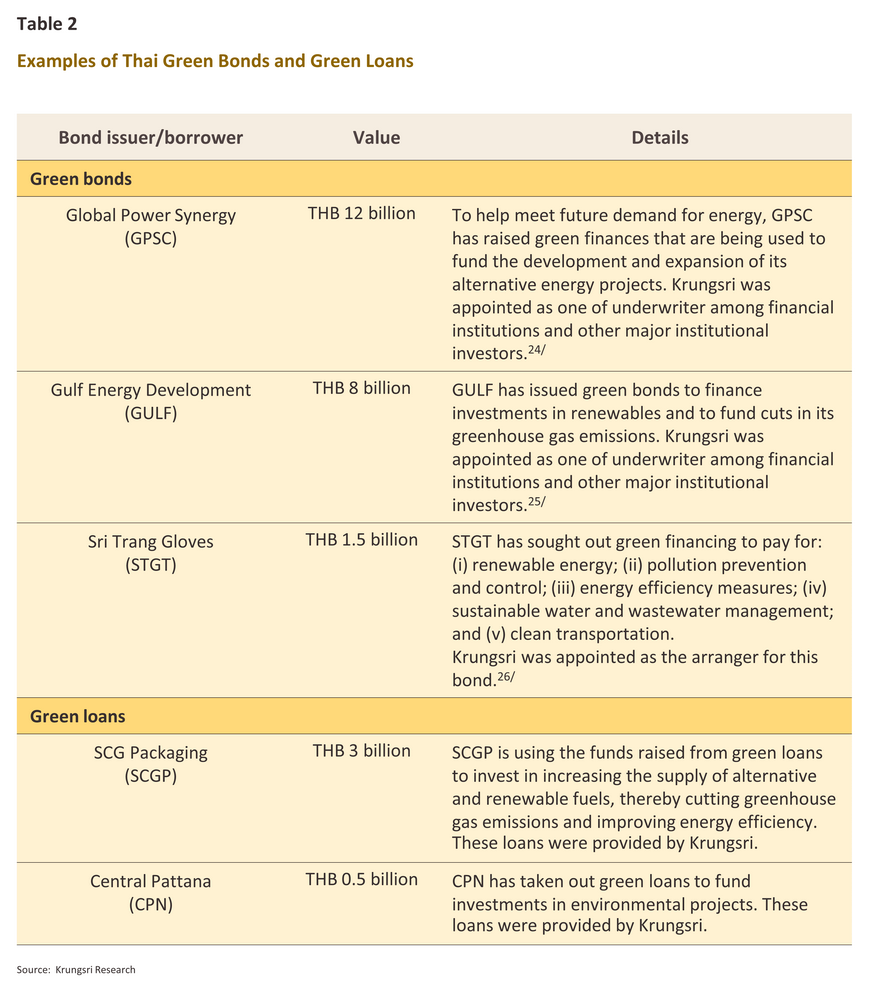

In 2023, the value of green bonds issued in Thailand came to THB 33 billion, or 4.3% of the value of all private-sector bonds issued in the year.22/ Over the period 2018 to 2023, green bond issuance totaled THB 157 billion, or 3.3% of the total market for bonds, thus placing Thailand close to the global average. However, over this period, issuance has been steadily increasing year on year, and in only one year did the value of new green bonds decline; this was in 2021, when the impacts of Covid-19 on the business environment caused widespread disruption.

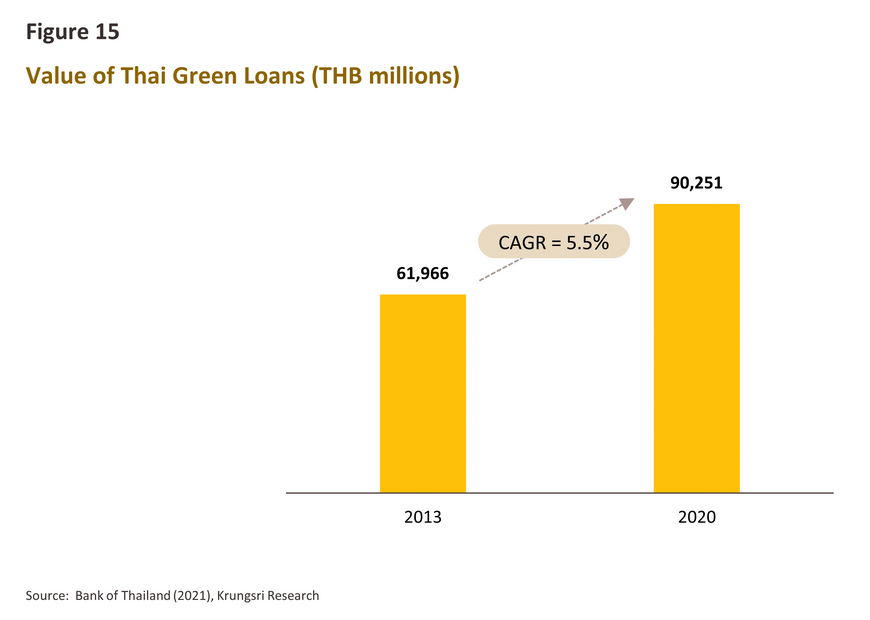

Research by the Bank of Thailand shows that the domestic market for green loans has also grown over the past few years, expanding from a value of around THB 62 billion in 2013 to THB 90 billion in 2020,23/ or compound annual growth of 5.5% (Figure 15). Thus, it can be said that investors, entrepreneurs, and financial institutions in Thailand are quite interested in allocating funds for environmental purposes.

Green financing in Thailand still has great potential for growth in the future, partly thanks to the government’s support for the development of the ‘bio-circular-green economy’. This provides a framework for future economic growth and will help to sharpen Thailand’s competitiveness across a range of industries, and it is expected that this will account for as much as 25% of Thai GDP by 2025. In addition, government policy is also attempting to hasten the transition to a low carbon society,27/ which will further add to demand for green financial instruments.

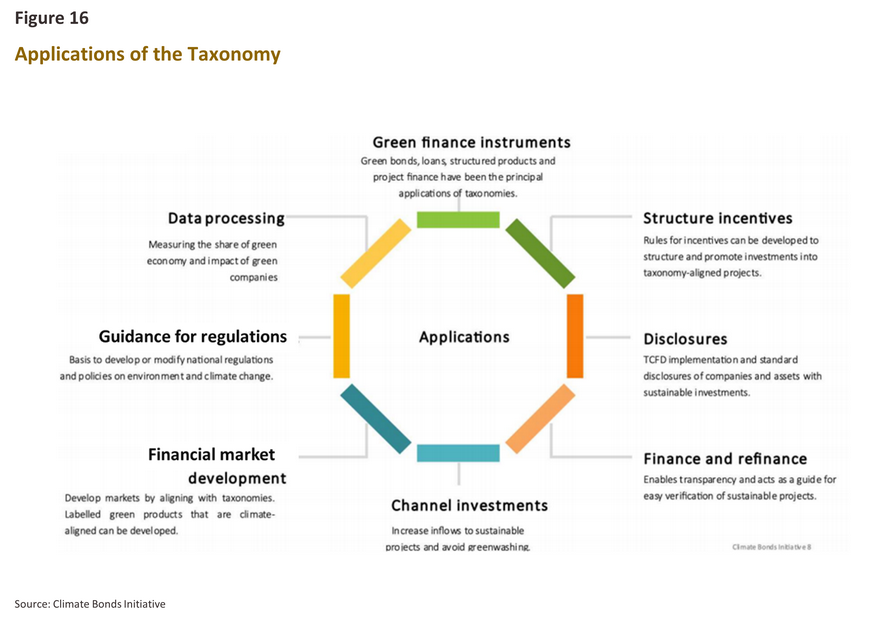

Thai regulatory bodies have also adopted measures that reflect their growing awareness of environmental issues and their eagerness to address these problems through green finance. To this end, the Bank of Thailand and the Securities and Exchange Commission (SEC) announced common reference standards for use in the classification of environmentally friendly business activities (i.e., phase 1 of the Thailand Taxonomy) in June 2023.28/ This will provide a core reference for use by government bodies, financial institutions and businesses when considering the environmental impacts of business operations or when designing new products or services. The SEC has also waived filing fees for applications and licenses for issuers of green bonds through to May 2025.29/

Challenges facing the development of the market for green financing

Due to the additional steps that are involved in this, raising finances through the use of green bonds or green loans is somewhat more complicated than raising capital through more traditional means. Projects or business activities being funded through green financial instruments need to meet eligibility requirements to ensure that these align with the Thailand Taxonomy and green bond standards, and so issuers of these are required to specify a ‘green bond framework’ that provides guidance on bond issuance to investors and other stakeholders.

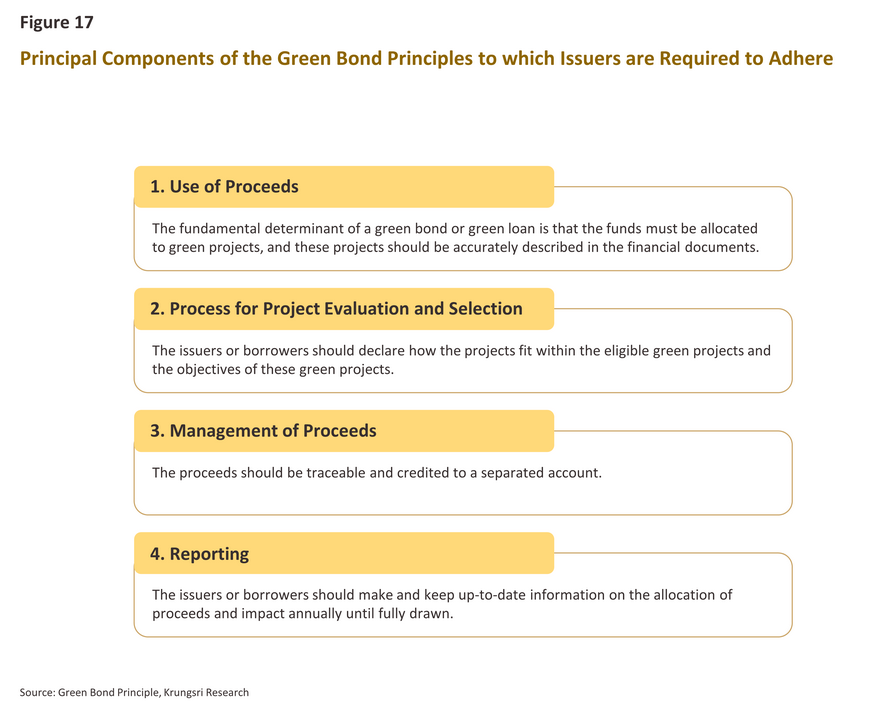

However, the SEC does not specifically require issuers of green bond to follow any particular standard but instead requires them to adhere to internationally recognized standards.30/ In this area, the most commonly applied rules and regulations are the International Capital Market Association (ICMA)’s Green Bond Principles (GBPs).31/ These lay out a system for categorizing environmental activities together with guidelines that green bond issuers and green loan debtors are required to adhere to. The 4 principal components of these are as follows.32/

1) Use of proceeds: Issuers of green bonds are required to use the capital raised from these to fund green projects, as defined in the Green Bond Principles. Details of these should be specified in the bond prospectus.

2) Processes for project evaluation and selection: Green bond issuers must inform potential investors of the processes in place for the evaluation and selection of projects receiving funding via green bonds, their environmental objectives, and the procedures for identifying and managing environmental risks.

3) Management of proceeds: Monies raised through the issuance of green bonds should be managed through separate sub-accounts to facilitate the tracking of spending on environmental projects

4) Reporting: Companies raising funds through green bonds should regularly report on how these have been used and what progress has been made on the projects for which the funds were raised. This should include details of what stage of implementation has been reached, how much of the funds have been spent and how much remains, and the establishment of channels for the disclosure of facts relating to the environmental impacts associated with these projects. Reports should be made annually until all funds have been exhausted.

In addition to the GBP, other internationally recognized standards applicable to the issuance of green bonds include the Climate Bond Initiative’s (CBI) Climate Bond Standard,33/ the ASEAN Green Bond Standards,34/ and the EU’s Green Bond Standard.35/

Although the additional requirements to adhere to standards such as those described above, including the use of procedures such as external reviews,36/ adds to costs and makes the process of issuing green bonds more burdensome, this helps to ensure that issuers are acting appropriately. The importance of this is underscored by research by the ADB, which shows that almost all Thai institutional investors agree that due to the greater transparency and disclosure that they promote, external reviews have an important role to play in building confidence among investors that environmental projects will achieve their stated goals and because of this, they exert a strong positive influence on decisions to buy green bonds.37/

Greenwashing refers to the process by which organizations create a public image and/or release information that misrepresents their activities. This has the goal of convincing the public that the organization is more committed to responsible environmental stewardship than is actually the case. Important facilitators of greenwashing include a lack of knowledge or understanding among stakeholders and a lack of disclosure of or clarity around relevant environmental information. Greenwashing can therefore be thought of as a kind of camouflage of misinformation that allows businesses to capture finances targeting environmental projects but then to direct this to other ends. To counter this, better information is needed, and this can be sought in the Thailand Taxonomy since this classifies business activities exactly according to their environmental impacts. Using this information will then help stakeholders to better understand the real impacts of an organization’s activities and to assess the scope of particular projects. The outcome of this will then be to allow investors and the financial sector generally to better allocate capital to environmental projects and to set appropriate interest rates for this.

At present, environmentally friendly investing is an alternative to mainstream investment vehicles, but if investors wishing to protect the environment lack sufficient information to make a well-informed choice, this may raise the risk that they will direct their investments into projects that do not generate environmental benefits or the yields that they hope for. Investors may also face liquidity risks if they need to sell their bonds but there is a shortage of buyers in the market. In addition, some projects may depend on advanced technology or new innovations, as well as on specialist knowledge, or there may be significant delays until the promised environmental benefits are realized. Investors will therefore need to carefully consider the value proposition represented by individual projects.

For banks, their role as financial intermediaries exposes them to risk as a result of their allocating capital or releasing credit to projects that typically have high capital requirements and long repayment horizons. This may then generate a maturity mismatch, with the bank taking on short-term obligations in the form of deposits or borrows, and then allocates or lends long-term funds.

Benefits accruing to the banking sector from green financing

Issuing green finance provides banks with the opportunity to develop new and sustainable income streams. At the same time, banks will be able to drive economic growth and to help protect the environment, while drawing the following additional benefits.

1) Contributing to the development of society and the economy

Green financing will help to power the ‘great green multiplier effect’,40/ thereby providing a range of benefits for society and the economy. This will include injecting funds into environmental projects and activities, which will then aid the transition to the green economy and help both the nation and individual organizations reach their environmental targets in a timely manner. Moreover, companies that receive green funding should also be able to cut their energy consumption and improve their operating efficiencies.

2) Opening new income streams

With competition in the financial services sector stiff, green financing represents another important means by which banks are able to generate additional income, particularly against the backdrop of growing interest in environmental conservation and sustainability. Beyond this, green financing also provides a vehicle that banks can use to penetrate new markets. This could include releasing credit to companies looking to invest in new innovations or to expand into new industries that are linked to environmental protection but where companies have difficulty raising funds. This could also include helping the bank’s customers issue their own green bonds.

Beyond this, banks could offer consultancy services relating to green financing, while partnering with other companies to promote the green transition will be another viable avenue for business development since this will be an unknown area for many bank customers. For example, a survey by McKinsey demonstrates that in the US, 64% of bank customers wanted advice from their bank on the wisdom of investing in rooftop solar power.41/

3) Improving customer and staff engagement

Consumers are increasingly concerned about the environment, and this is now affecting decisions over which goods and services to buy and how and where to invest, and so within this evolving consumer environment, if banks make their environmental concerns evident through their involvement in green financing schemes, this will undoubtedly help to improve their public image. In addition, this will make it easier for banks to expand market share in segments where interest in the environment is strongest, such as among baby boomers, a target group that from the bank’s point of view has the advantage of strong financial security relative to other age cohorts and a desire to reduce its environmental footprint. These individuals are thus generally willing to pay higher prices for goods and services, if these have positive environmental impacts.42/ Moreover, a survey carried out by JobsDB in mid-2023 showed that 48% of 18-23-year-old Thais would choose to work for a company that was concerned about the environment and so making a clear public commitment to this will also help to improve staff recruitment and retention.43/

4) Reducing environmental risk

Environmental problems are giving rise to 2 distinct classes of risk: (i) physical risk, or the risk of losses to property or disruption to operations resulting from natural disasters or climate change; and (ii) transition risk, or the risk arising from the need to address environmental problems by transitioning to a low-carbon economy. Problems relating to this may manifest in changes to consumer or investor preferences, or revisions to laws, government policies, or the rules of international trade, which would then impact business operations. Indeed, the significance of these factors is steadily rising, and environmental risk is increasingly impacting operations within the financial sector, and one means of countering this is greater involvement in green financing. In addition, supporting green financing initiatives will also help to reduce exposure to risk resulting from changes to environmental policy and legislation for bank customers and banks themselves.

Krungsri Research view: An opportunity for the financial sector to drive the development of the green economy

It is increasingly clear that adaptation and mitigation measures that address our environmental problems are becoming a necessity rather than a choice, and with this shift, green financial instruments will likely also move into the core of mainstream investing. These changes are then opening up new markets for players in the financial sector, and banks should seize these opportunities by responding to the varied needs of investors looking for green financing instruments. This will entail developing a range of environmentally focused financial services and products, and should extend to include the release of sustainability-linked bonds and loans, another financial product that is gaining in popularity and for which the market will expand in the future. As part of their response to changes in the market, banks will need to prepare their staff, in particular by educating them about green financing and the opportunities and risks that these products entail, as well as ensuring that their operations in these areas align with the relevant regulations. This will then help to support the development of green and sustainable financial instruments that respond to the needs of both customers that are ready to adapt rapidly to these changes and those that will make the move somewhat slower.

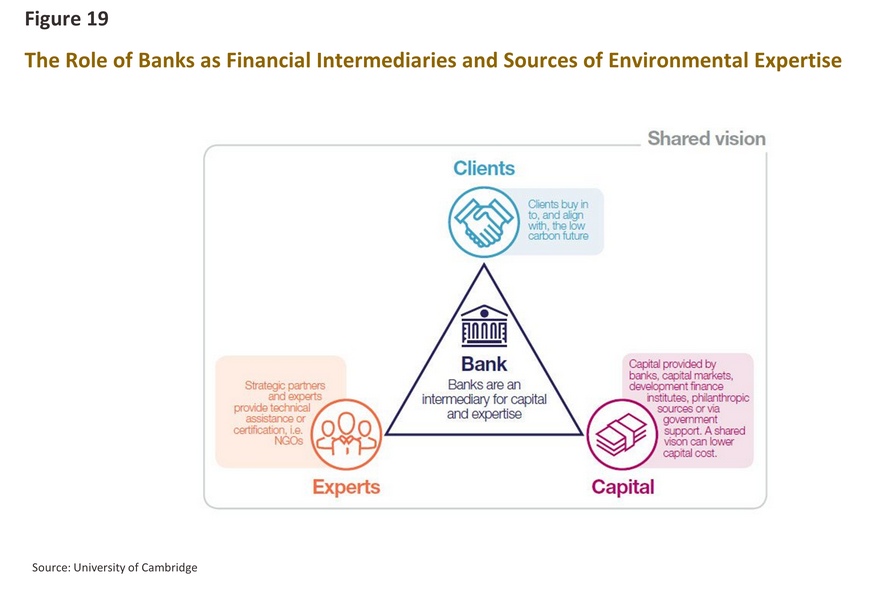

More broadly, banks will be able to establish themselves as knowledge hubs providing advice on green financial products and services that address the particular circumstances of individual business customers and partners. Banks will therefore be able to raise awareness of environmental issues and motivate their customers to make their operations more environmentally friendly. Banks will also be able to develop partnerships and knowledge-exchanges with organizations with expertise in environmental issues.

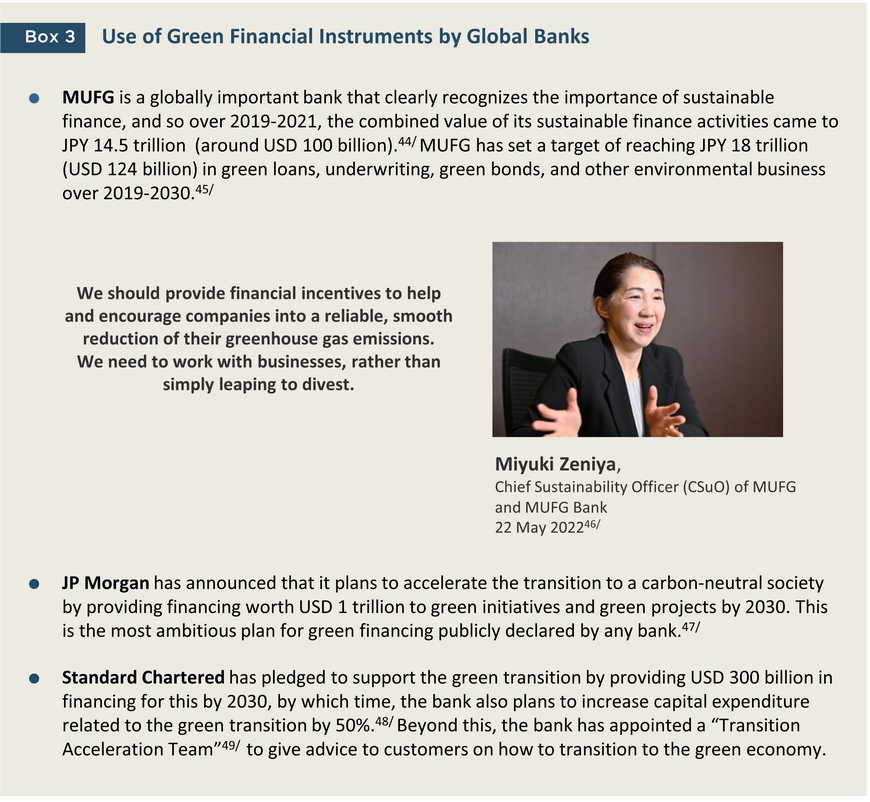

However, the banking sector’s engagement with these issues cannot be limited to simply designing and releasing green financial instruments. Rather, financial institutions will need to demonstrate a concrete commitment to the environment that takes practical forms, such as by integrating environmental issues into core business strategies, announcing clear goals for the level of green financing that will be made available, raising awareness of the importance of environmental issues among bank staff, and joining relevant international organizations that are committed to environmental protection, such as the Net Zero Banking Alliance (NZBA).50/

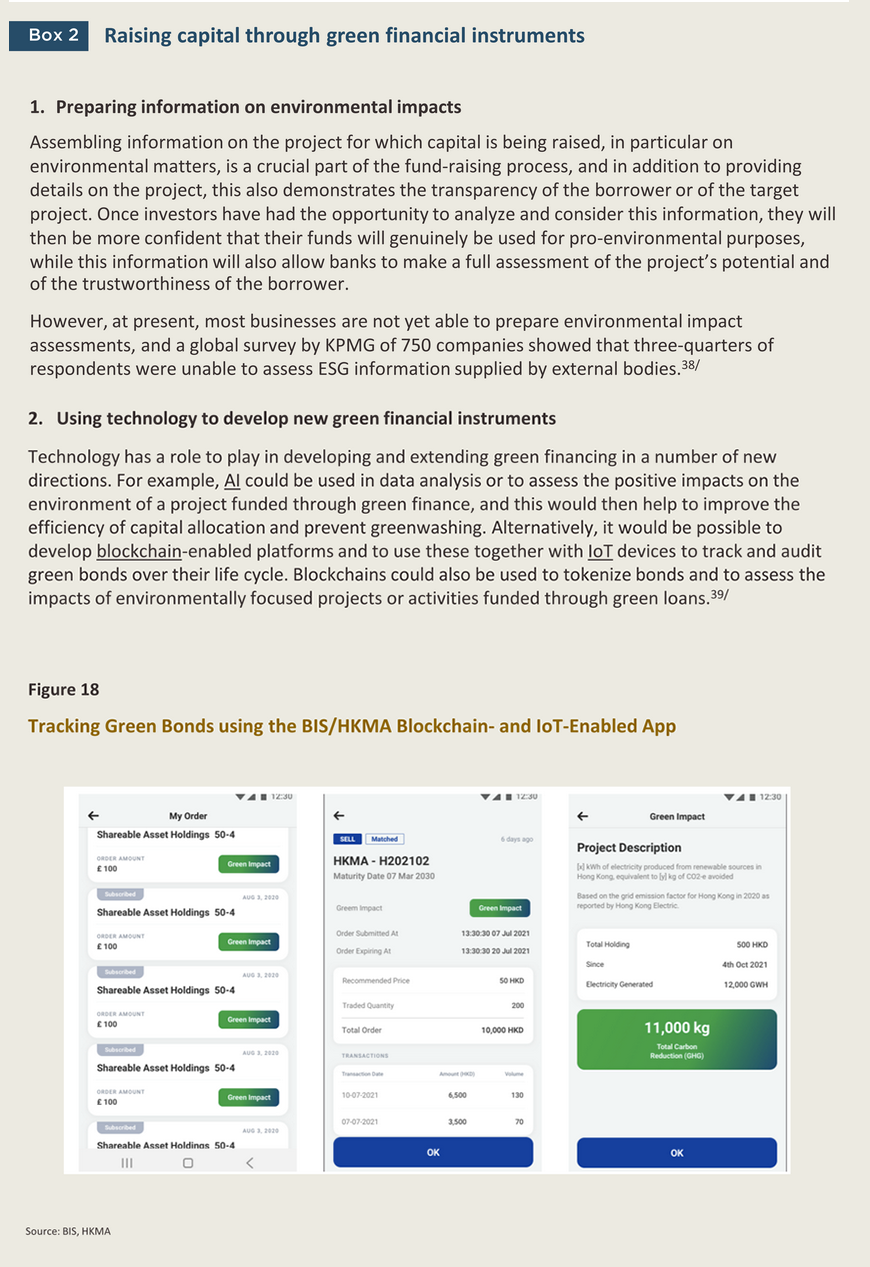

Banks also need to build awareness among customers and industry stakeholders about the importance of gathering and disclosing information on the environmental impacts of their operations, while banks could also assist in the development of technology to foster innovation and reduce risk arising from the use of green financial instruments. An example of the potential of this area can be seen in the “NovA!” platform developed jointly by the Monetary Authority of Singapore (the Singaporean central bank), financial institutions, and other private-sector players. This uses AI to analyze data and to assess the risks and environmental impacts associated with the issuing of green finance, which has then helped to reduce greenwashing and increase the efficiency of capital allocation in the green finance space.51/

In addition to its direct impacts on the environment, green financing will clearly play an important role within the banking sector and its increasing shift to sustainable growth, but creating a more livable world will depend on the cooperation and joint efforts of all sections of society and all parts of the economy. Nevertheless, although banks are just one cog in a hugely complex machine, by leveraging their position as one of the sources of green finance, banks will be able to raise awareness of environmental issues across a broad front and to push forward with the green transition.

References

ACMF (2019): “ASEAN Green Bond Standards”. Retrieved Aug 23 2023

Asian Development Bank (2022): “Green Bond Market Survey for Thailand Insights on the Perspectives of Institutional Investors and Underwriters”. Retrieved Aug 23 2023 from https://www.adb.org/sites/default/files/publication/801601/green-bond-market-survey-thailand.pdf

Asian Development Bank (2023): “Three-quarters of firms globally are not ready for new ESG rules, KPMG finds”. Retrieved Oct 23 2023 from https://www.reuters.com/sustainability/three-quarters-firms-globally-are-not-ready-new-esg-rules-kpmg-finds-2023-09-26/

BloombergNEF (2022): “The $7 Trillion a Year Needed to Hit Net-Zero Goal”. Retrieved Nov 19 2024 from https://about.bnef.com/blog/the-7-trillion-a-year-needed-to-hit-net-zero-goal/

BNP Paribas (2023): “Green bond growth to return in 2023”. Retrieved Nov 24 2023 from https://globalmarkets.cib.bnpparibas/green-bond-growth-to-return-in-2023/

CDP (2020): “CDP Financial Services Disclosure Report 2020”. Retrieved Sep 17 2023 from https://www.cdp.net/en/research/global-reports/financial-services-disclosure-report-2020

Climate Bonds Initiative (2023): “Climate Bonds Standard V4.0”. Retrieved Aug 23 2023 from https://www.climatebonds.net/files/files/CBI_Standard_V4.pdf

Climate Bonds Initiative (2023): “SUSTAINABLE DEBT GLOBAL STATE OF THE MARKET 2022”. Retrieved Aug 9 2023 from https://www.climatebonds.net/files/reports/cbi_sotm_2022_03e.pdf

Climate Bonds Initiative (2023): “Sustainable Debt Market Summary Q3 2023”. Retrieved Jan 19 2024 from https://www.climatebonds.net/files/reports/cbi_susdebtsum_q32023_01e.pdf

CNBC (2021): “JPMorgan pledges $2.5 trillion over the next decade toward climate change”. Retrieved Dec 19 2024 from https://www.cnbc.com/2021/04/15/jpmorgan-pledges-2point5-trillion-over-10-years-toward-climate-change.html

DBS (2017): “Green Finance Opportunities in ASEAN”. Retrieved Oct 14 2023 from

Eckstein (2021): “Global Climate Risk Index 2021”. Retrieved Aug 25 2023 from

Financial Times (2023): “New standards keep the greenwash off green bonds”. Retrieved Aug 5 2023 from https://www.ft.com/content/e8d0976e-e67e-46bb-89d3-9ae7efe99ec8

Infoquest (2022): “GPSC ออกกรีนบอนด์ 1.2 หมื่นลบ.ดอกเบี้ย 2.55-4.40% ขายสถาบัน-รายใหญ่ 7-9 มิ.ย.”. Retrieved Nov 5 2023 from https://www.infoquest.co.th/2022/206028

International Capital Market Association (2021): “หลักการของตราสารหนี้เพื่ออนุรักษ์สิ่งแวดล้อมแนวปฏิบัติภาคสมัครใจในการออกตราสารหนี้เพื่ออนุรักษ์สิ่งแวดล้อม มิถุนายน 2564 (2021)”. Retrieved Aug 23 2023 from https://www.icmagroup.org/assets/documents/Sustainable-finance/Translations/Thai-GBP-2021-06.pdf

International Finance Corporation (2023): “Emerging Market Green Bonds”. Retrieved Nov 12 2023 from https://www.ifc.org/content/dam/ifc/doc/2023/ifc-amundi-emerging-market-green-bonds-july2023.pdf

Jodsdb (2023): “คนทำงานรุ่นใหม่ใส่ใจสิ่งแวดล้อม นำองค์กรก้าวหน้า”. Retrieved Oct 6 2024 from

Kelkar (2023): “How Does Green Finance Benefit Organizations and the World”. Retrieved Aug 23 2023 from https://emeritus.org/blog/finance-what-is-green-finance/

McKinsey Sustainability (2023): “Green growth: Unlocking sustainability opportunities for retail banks” .Retrieved Aug 23 2023 from https://www.mckinsey.com/capabilities/sustainability/our-insights/green-growth-unlocking-sustainability-opportunities-for-retail-banks

MUFG (2022): “MUFG Sustainability Report 2022”. Retrieved Dec 16 2024 from https://www.mufg.jp/dam/csr/report/2022/sr2022_en.pdf

Reuters (2022): “Nissan gets $1.44 bln green loan for zero-emission mobility investments”. Retrieved Dec 18 2023 from https://www.reuters.com/business/autos-transportation/nissan-gets-144-bln-green-loan-zero-emission-mobility-investments-2022-11-30/

Sato Y. (2023): “MUFG: Leading Finance's Net-Zero Transition”. Retrieved Dec 16 2024 from https://project.nikkeibp.co.jp/ESG/atcl/eng/sdgf/56/

SEB (2023): “Green Bond Investor Report”. Retrieved Oct 8 2023 from

ThaiBMA (2023): “การศึกษา Green Premium ในตลาดตราสารหนี้ไทย”. Retrieved Sep 25 2023 from https://www.thaibma.or.th/EN/Investors/Individual/Blog/2023/170823.aspx

ThaiBMA (2023): “สรุปภาวะตลาดตราสารหนี้ไทย 2023”. Retrieved Jan 25 2024 from https://www.thaibma.or.th/doc/press/y2024/Doc012024.pdf

TheCityUK (2022): “Green finance: a quantitative assessment of market trends”. Retrieved Aug 15 2023 from https://www.thecityuk.com/our-work/green-finance-a-quantitative-assessment-of-market-trends/

University of Cambridge (2023): “Bank 2030: Accelerating the transition to a low carbon economy”. Retrieved Oct 18 2023 from https://www.cisl.cam.ac.uk/system/files/documents/bank-2030.pdf

กรุงเทพธุรกิจ (2023): “ปี 2566 Green Bond กลับมาเติบโตอีกครั้ง”. Retrieved Sep 16 2023 from https://www.bangkokbiznews.com/environment/1052242

การเงินธนาคาร (2023): “รัฐบาลหนุน ESG เตรียมมาตรการการเงิน 4.5 แสนลบ. ลงทุนเศรษฐกิจสีเขียว ส่งเสริมสู่ความยั่งยืน”. Retrieved Dec 15 2023 from https://moneyandbanking.co.th/2023/65696/

ธนาคารแห่งประเทศไทย (2021): “SMEs ไทยจะพลิกฟื้นโตยั่งยืนอย่างไรภายใต้ภูมิทัศน์โลกใหม่การเงินสีเขียว (ตอนที่2)”. Retrieved Sep 23 2023 from https://www.bot.or.th/th/research-and-publications/articles-and-publications/articles/Article_21Jul2021.html

ธนาคารแห่งประเทศไทย (2023): “Thailand Taxonomy กติกาใหม่เพื่อโลกที่ยั่งยืน”. Retrieved Nov 27 2023 from https://www.bot.or.th/th/financial-innovation/sustainable-finance/green/Thailand-Taxonomy.html

1/ https://www.germanwatch.org/sites/default/files/Global%20Climate%20Risk%20Index%202021_2.pdf

2/ ‘Scope 3: Indirect Emissions’, which are defined as emissions resulting from the use of resources or assets that are not owned by or under the direct control of a particular organization, or that result from the activities of a stakeholder external to the organization but within its supply chain. Examples of indirect emissions that can be attributable to banks include those that result from activities funded by a bank via credit or other types of investment.

3/ https://www.cdp.net/en/research/global-reports/financial-services-disclosure-report-2020

4/ For further details, please see: Green Deposits for Greater Sustainability

5/ https://www.cisl.cam.ac.uk/system/files/documents/bank-2030.pd

6/ For example, by adjusting the term and amount of the bond in line with future cash earnings.

7/ https://www.thecityuk.com/our-work/green-finance-a-quantitative-assessment-of-market-trends/

8/ Variations in the outcomes of the research may be explained by the use of different methodologies or the different conditions that exist in different countries.

9/ https://www.thaibma.or.th/EN/Investors/Individual/Blog/2023/170823.aspx

10/ SEB Green Bond Report FY2022

11/ https://www.reuters.com/business/autos-transportation/nissan-gets-144-bln-green-loan-zero-emission-mobility-investments-2022-11-30/

12/ https://www.climatebonds.net/files/reports/cbi_sotm_2022_03e.pdf

13/ https://www.bangkokbiznews.com/environment/1052242

14/ https://www.climatebonds.net/files/reports/cbi_susdebtsum_q32023_01e.pdf

15/ In 2022, these accounted for 28.7% of the total.

16/ https://globalmarkets.cib.bnpparibas/green-bond-growth-to-return-in-2023/

17/ https://www.ifc.org/content/dam/ifc/doc/2023/ifc-amundi-emerging-market-green-bonds-july2023.pdf

18/ The accuracy of data on the value of green loans may be limited by problems with disclosure since much of this will be restricted to agreements between banks and borrowers.

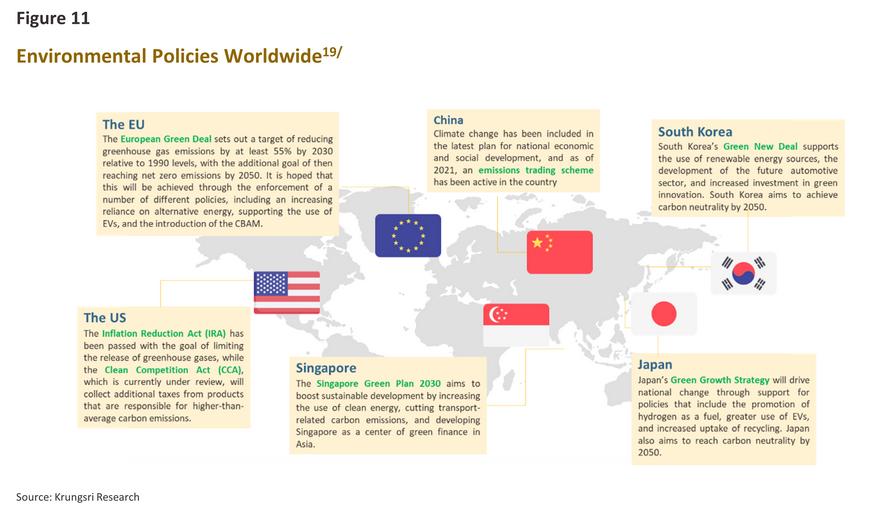

19/ For further details, please see: Countdown to the CBAM: How prepared is Thailand for the introduction of the EU carbon tax?

20/ https://www.climatebonds.net/files/reports/cbi_sotm_2022_03e.pdf

21/ https://www.dbs.com/iwov-resources/images/sustainability/insights/Green_Finance_Opportunities_in_ASEAN.pdf?pid=sg-group-pweb-sustainability-pdf-Green_Finance_Opportunities_in_ASEAN

22/ In 2023, domestic issuance of long-dated bonds by the private sector came to THB 1.02 trillion. For more details, please see: https://www.thaibma.or.th/doc/press/y2024/Doc012024.pdf

23/ https://www.bot.or.th/th/research-and-publications/articles-and-publications/articles/Article_21Jul2021.html

24* https://www.infoquest.co.th/2022/206028 และ https://market.sec.or.th/public/ipos/IPOSDE01.aspx?TransID=428076&SD=0706256509062565

25/ https://www.thansettakij.com/sustainable/zero-carbon/560455 และ https://market.sec.or.th/public/ipos/IPOSDE01.aspx?TransID=509005&SD=2703256629032566

26/ https://www.krungsri.com/th/newsandactivities/krungsri-banking-news/sri-trang-gloves-green-bond และ https://market.sec.or.th/public/ipos/IPOSDE01.aspx?TransID=448393&SD=2309256527092565

27/ https://moneyandbanking.co.th/2023/65696/

28/ Phase 1 of the Thailand Taxonomy covers the energy and transport sectors. Further details are available at: https://www.bot.or.th/th/financial-innovation/sustainable-finance/green/Thailand-Taxonomy.html Phase 2 will extend to cover activities related to manufacturing, construction, real estate waste management, and agriculture. Feedback on this will be solicited in Q4 of 2024.

29/ https://shorturl.at/gjAQ5

30/ https://publish.sec.or.th/nrs/9584a14.pdf

31/ https://www.ft.com/content/e8d0976e-e67e-46bb-89d3-9ae7efe99ec8

32/ For further details please see: https://www.icmagroup.org/assets/documents/Sustainable-finance/Translations/Thai-GBP-2021-06.pdf

33/ The Climate Bond Initiative is an international non-profit organization that promotes investment in the low-carbon economy as well as in climate change adaption and mitigation. For more details, see https://www.climatebonds.net/climate-bonds-standard-v4 In 2020, a quarter of green bonds issued globally adhered to the CBI standards https://www.ft.com/content/e8d0976e-e67e-46bb-89d3-9ae7efe99ec8

34/ https://www.theacmf.org/initiatives/sustainable-finance/asean-green-bond-standards

35/ https://www.consilium.europa.eu/en/press/press-releases/2023/10/24/european-green-bonds-council-adopts-new-regulation-to-promote-sustainable-finance/

36/ External reviews take 4 different forms: (i) second-party opinions (SPOs) on the green bond framework; (ii) verification and assurance of the green bond’s compliance with its stated framework; (iii) certification that the bond qualifies as a green bond; and (iv) scoring and rating of the green bond.

37/ https://www.adb.org/sites/default/files/publication/801601/green-bond-market-survey-thailand.pdf

38/ https://www.reuters.com/sustainability/three-quarters-firms-globally-are-not-ready-new-esg-rules-kpmg-finds-2023-09-26/

39/ Platforms such as this have been developed under the Genesis project, a joint venture between the Hong Kong Monetary Authority (the Hong Kong central bank) and the Bank for International Settlements https://www.bis.org/about/bisih/topics/green_finance/green_bonds.htm

40/ https://emeritus.org/blog/finance-what-is-green-finance/

41/ https://www.mckinsey.com/capabilities/sustainability/our-insights/green-growth-unlocking-sustainability-opportunities-for-retail-banks

42/ https://www.everydaymarketing.co/trend-insight/voice-of-green-marketing-cmmu-eco-trend-2020/

43/ https://th.jobsdb.com/th/career-advice/article/คนทำงานรุ่นใหม่ใส่ใจสิ่งแวดล้อม นำองค์กรก้าวหน้า

44/ https://www.mufg.jp/dam/csr/report/2022/sr2022_en.pdf

45/ This forms one part of the bank’s sustainable finance targets, for which the total 2019-2030 target is JPY 35 trillion (around USD 240 billion). For further details, please see: https://www.mufg.jp/dam/csr/report/progress/202304_en.pdf

46/ https://project.nikkeibp.co.jp/ESG/atcl/eng/sdgf/56/

47/ https://www.jpmorganchase.com/news-stories/financing-the-green-transition and https://www.cnbc.com/2021/04/15/jpmorgan-pledges-2point5-trillion-over-10-years-toward-climate-change.html

48/ https://av.sc.com/corp-en/content/docs/Standard-Chartered-Bank-Transition-Finance-Framework.pdf

49/ https://www.sc.com/en/feature/transition-finance-imperative-conversation-simon-cooper/

50/ As of September 2023, 133 banks from 43 countries had joined the Net-Zero Banking Alliance, and these controlled 41% of all assets in the global banking system. However, as yet, no Thai banks are members. Members of the Net-Zero Alliance are committed to reaching net zero emissions by 2050. This includes emissions resulting from: (i) the banks own operations, and (ii) the activities of other companies within the same commercial group and those of customers being funded by the bank https://www.unepfi.org/net-zero-banking/members/

51/ https://www.mas.gov.sg/news/media-releases/2022/ai-utility-nova-to-unlock-opportunities-for-green-financing-and-combat-greenwashing