Executive summary

The EV price war in Thailand began in 2022 due to intensifying market competition, forcing EV manufacturers to cut production costs to maintain profitability. Although price reductions aimed to boost EV sales, the Thai EV market in 2024 saw the opposite effect. Some consumers believed EVs were a “soon-to-be discounted” product and expressed concerns over potential future price reductions by automakers. However, signs of a slowdown in Thailand’s EV market competition emerged in early 2025, as EV prices began to stabilize during the Motor Show 2025 (March–April 2025). According to Krungsri Research, the EV price war in Thailand may persist through 2025, driven by moderate-to-high global market competition. In addition, some major EV brands are under pressure to clear inventory to resolve liquidity issues. However, the price war is expected to ease during 2026–2027, supported by two key factors: (i) rising production costs due to offsetting requirements under the EV 3.0 and EV 3.5 schemes, and (ii) with BEV passenger car prices now lower than those of ICE vehicles, EV automakers face less pressure to deploy intensive marketing strategies to maintain competitiveness.

Introduction

In recent years, global demand for electric vehicles (EVs) has surged, driven by government support policies, investments from major automakers, and declining battery costs. These factors have led to a continued drop in EV prices. In 2024, global EV sales rose by more than 25% to 17 million units, accounting for over 20% of total new car sales. Meanwhile, production volumes increased by more than 26%, with China remaining the main contributor to global EV manufacturing, accounting for over 72% of global output. By 2030, global EV sales are expected to continue rising, with their share projected to exceed 40% of total new car sales.

1/

The growing popularity of EVs has driven substantial investment in related industries. Since 2019, EV manufacturers and businesses involved in mining and processing minerals for battery production have begun to outperform traditional automakers and other clean energy technology companies in terms of financial performance and market valuation. Notably, in 2021, the aggregate market capitalization of EV manufacturers surged to a peak of USD 1.6 trillion, with investment returns continuing to rise through 2023. Meanwhile, between 2015 and 2022, investment in businesses related to battery minerals grew more than sixfold.

2/

Nevertheless, the rapid expansion of EV production capacity has led to an oversupply in certain markets, particularly China. This has triggered fierce price competition to capture market share, resulting in a “price war” among global automakers. While price cuts were intended to stimulate demand, they have had broader impacts, including reduced manufacturer profits and weakened consumer confidence, especially among early buyers. This report examines recent trends in EV market competition and price reductions, both globally and in Thailand, to address a key question:

When will the EV price war in Thailand come to end?

Global EV Market Competition

Structural Shifts in the Global EV Market

Global competition in the EV market has intensified, driven by the entry of new Chinese manufacturers. This trend has been largely driven by China’s sustained policy support for the EV industry since 2009, which has encouraged a wave of new market entrants. By 2014, the number of EV-related company registrations in China had exceeded 80,000. To this day, China continues to lead global EV production, with total output reaching approximately 12.4 million units in 2024, accounting for more than 70% of global EV production.

However, the Chinese government has begun to regulate its rapidly expanding domestic EV industry. After years of injecting substantial subsidies to stimulate market growth, the resulting surge in competition among Chinese EV manufacturers has intensified pressure to cut prices in order to remain competitive. In 2022, when the EV price war in China officially began, 95 models saw price reductions. The number of discounted models rose to 148 in 2023 (+55.8%) and further to 227 in 2024 (+53.4%).

2/ 3/ 4/

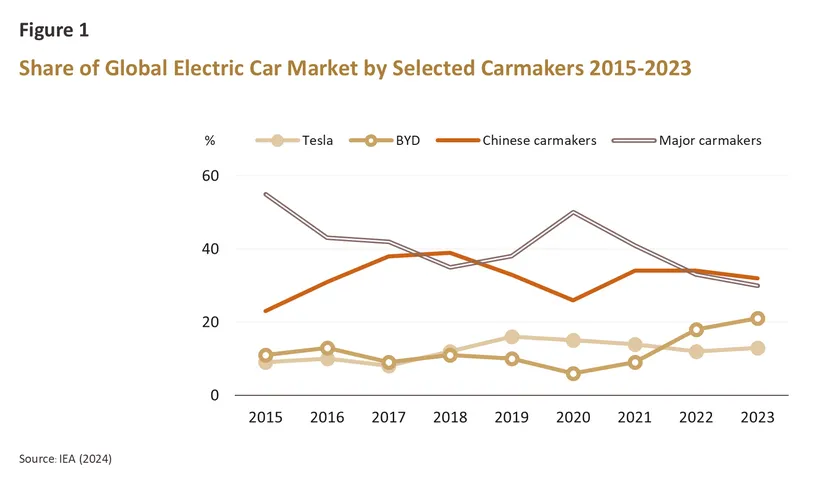

Moreover, intensifying competition in China’s EV market, combined with excess production capacity and signs of demand saturation, has prompted many Chinese automakers to accelerate EV exports to global markets. This shift has reshaped the global EV market structure (Figure 1). In 2015, early EV pioneers such as Nissan, Mitsubishi, and BMW held a combined market share of 55% of global EV sales. By 2023, their share had declined to just 35%, while new entrants captured more market share. For example, BYD’s market share rose to 21%, Tesla’s increased to 12%, and other Chinese manufacturers collectively accounted for 32%.

2/

The surge in EV exports from China has intensified the EV price war across more countries, particularly in developing markets where Chinese EVs hold a significant market share. This is largely due to their lower prices compared to EVs from other countries, especially in the small- and mid-sized BEV segments, where prices are now comparable to, or even lower than, ICE vehicles. This price advantage has enabled China to expand its EV exports to price-sensitive developing countries such as Indonesia, Thailand, and Mexico.

1/

EV Market Situation in Thailand and the Price War

Competitive Landscape of Thailand’s EV Market

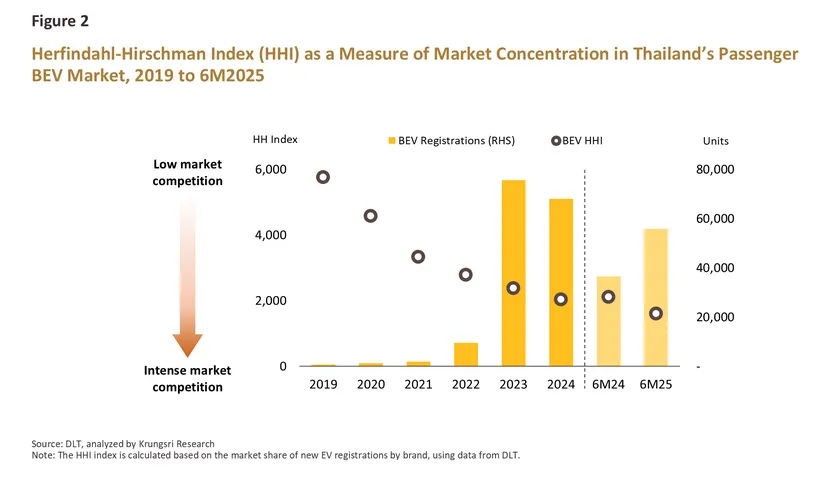

Government support through the EV 3.0 and EV 3.5 schemes has played a key role in boosting EV sales in Thailand and attracting new EV manufacturers to either establish local production bases5/ or introduce new models to the market. As a result, EV market share has become more distributed among new entrants. The Herfindahl-Hirschman Index (HHI)6/ can be used to measure the level of market concentration and competition in Thailand’s EV market, as follows:

-

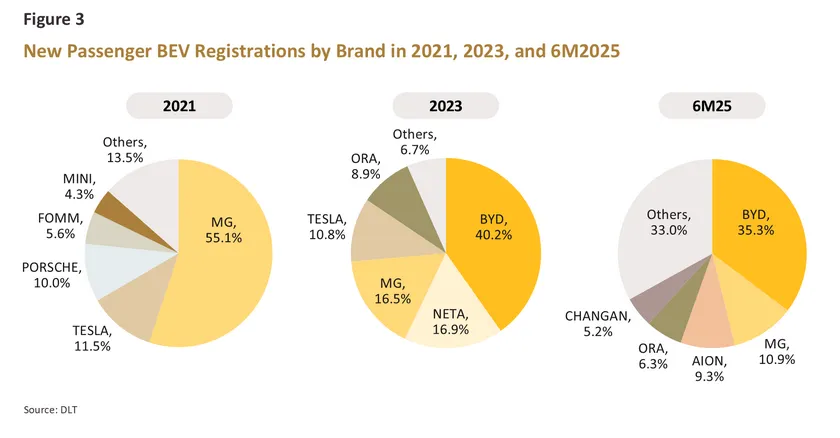

EV market competition during 2022–2023 under the EV 3.0 scheme: The scheme supported Thailand’s EV market through subsidies of up to 150,000 baht per BEV passenger car, along with other related tax measures.7/ These incentives drove BEV passenger car registrations to grow by an average of 524.2% per year, from 1,943 units in 2021 to 75,715 units in 2023,8/ and intensified market competition, as reflected by the entry of new automakers into the Thai EV market. In 2021, the EV market was highly concentrated, with MG holding a 55.1% share of total BEV passenger car registrations, consistent with a high HHI index of 3,339, indicating low market competition (Figure 2). By 2023, competition had increased, reflected by a decline in the HHI index to 2,382, suggesting moderate competition. New entrants began gaining market share, with BYD capturing 40.2%, NETA 16.9%, and ORA 8.9% of passenger BEV registrations in 2023 (Figure 3).

-

EV market competition during 2024–2025 under the EV 3.5 scheme: The scheme continued to support passenger BEV registrations, which rose 52.9%, compared to the same period last year, to 55,818 units in the first half of 2025. New EV brands entering the Thai market, along with existing players with previously limited market share, were able to expand their presence during this period. For example, AION and CHANGAN increased their market shares to 9.3% and 5.2%, respectively. In contrast, some earlier market leaders saw their shares decline, BYD dropped to 35.3%, MG to 10.9%, and ORA to 6.3%. These shifts contributed to intensified market competition, as reflected by a continued decline in the HHI index to 1,608, indicating a moderately high level of competition.

EV Price War in Thailand

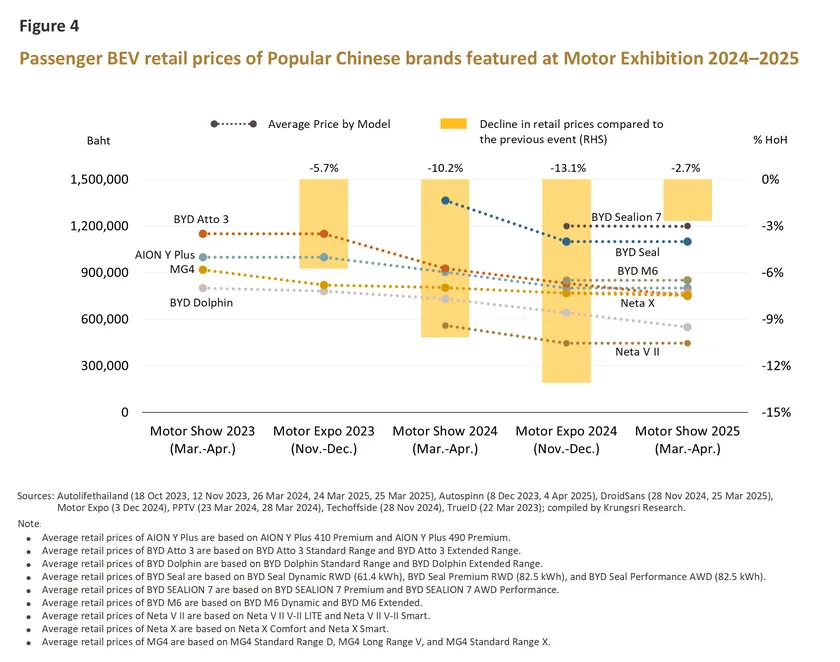

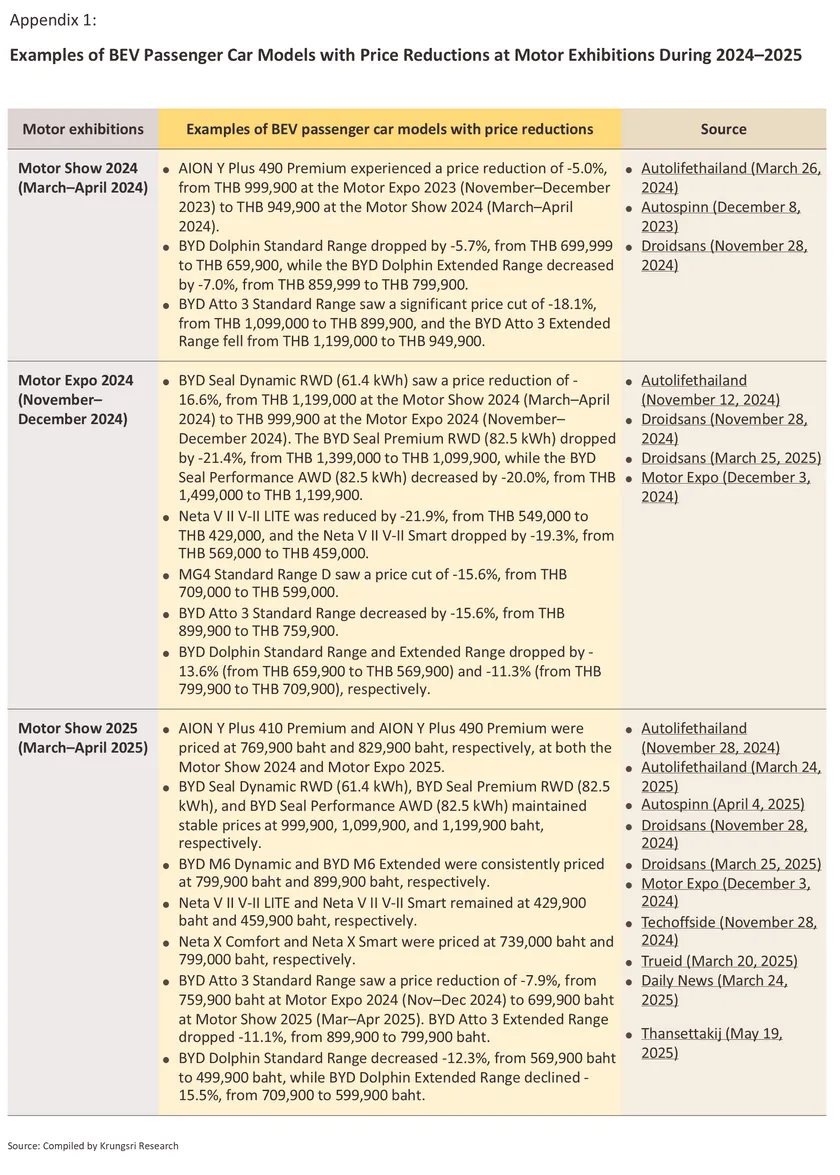

The global EV price war, which intensified since late 2022, along with aggressive export efforts by Chinese automakers and government support measures, has made Thailand one of the key markets for affordable Chinese EVs. Based on passenger BEV prices observed at Thailand’s motor exhibitions since 2024, prices have declined at varying rates across different periods. (Details of BEV passenger car price reductions are provided in Appendix 1.)

- Motor Show 2024 (March–April 2024): Chinese EV brands reduced passenger BEV prices by an average of -10.2% compared to prices at the Motor Expo 2023 (November–December 2023). Newly launched models (less than one year old) saw price cuts of around -5% to -8% (Figure 4). Meanwhile, BYD reduced prices of existing models at a rate higher than the average to clear stock; for example, the BYD Atto 3 dropped by -18% to -21% compared to its price during the Motor Expo 2023.

- Motor Expo 2024 (November–December 2024): The EV price war intensified, with most Chinese brands cutting passenger BEV prices by an average of -13.1% compared to the Motor Show 2024, aiming to boost demand amid a sluggish market and fierce competition. The steepest discounts were seen in newly launched models from early 2024, marking their first price cuts in Thailand, with reductions averaging -16.0% to -21.0% — e.g., BYD Seal dropped -19.3% and NETA VII -20.6%. Older models that had already been discounted saw further price cuts of around -11.0% to -16.0%; for example, MG4 Standard Range D (-15.6%), BYD Atto 3 Standard Range (-15.6%), and BYD Dolphin (-11.3% to -13.6%).

- Motor Show 2025 (March–April 2025): The EV price war began to stabilize, with most Chinese brands reducing BEV passenger car prices by only -2.7% compared to the Motor Expo 2024. This was due to shrinking profit margins resulting from continued price cuts in the EV market, along with requirements under the EV 3.0 scheme for incentivized automakers to begin local production. However, with limited production volumes, most manufacturers have yet to benefit from economies of scale. As a result, most brands maintained passenger BEV prices at the same level as the Motor Expo 2024. Some, however, continued to cut prices for models launched over two years ago to clear stock; for example, BYD Atto 3 dropped -7.9% to -11.1%, and BYD Dolphin dropped -12.3% to -15.5%.

Following continuous price reductions by automakers in Thailand, the average price of BEV passenger cars in 2024 has declined to match that of ICE cars. According to IEA (2025), the average retail price of BEV passenger cars in Thailand stands at USD 35,000 (THB 1.19 million), comparable to ICE vehicles priced at USD 34,000 (THB 1.16 million). Notably, Chinese-branded BEVs are priced even lower, with an average retail price of USD 30,000 (THB 1.02 million), approximately -11.8% below the average price of ICE vehicles.

Impact on EV Manufacturers in Thailand

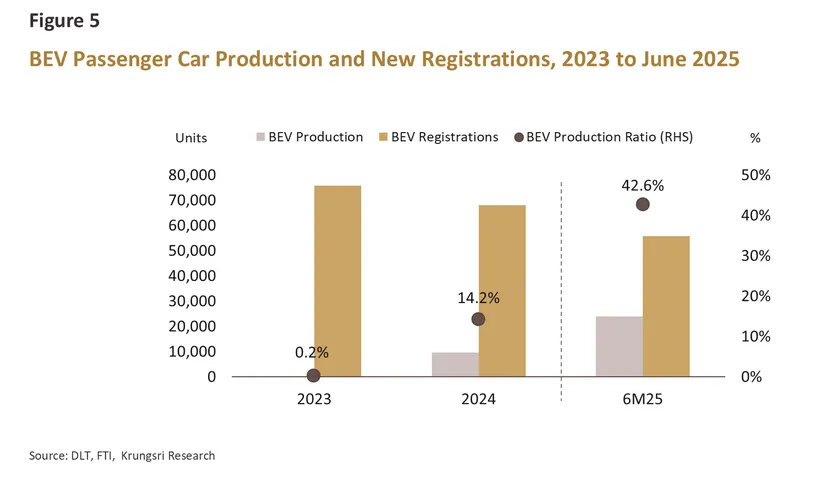

During 2024–2025, the share of locally produced BEV passenger cars for domestic sales in Thailand increased, mainly due to production requirements under the EV 3.0 scheme. In 2023, local production accounted for just 0.2% of total BEV passenger car registrations (164 units; local production) (Figure 5). The local production rose to 14.2% (9,688 units) in 2024 and 42.6% (23,798 units) in the first half of 2025, as investment-promoted manufacturers were required to produce BEVs at 1 to 1.5 times the volume of previously imported units, respectively.

However, on 4 December 2024, the National EV Board approved a resolution allowing BEV automakers to postpone compensatory production under the EV 3.0 scheme, as 2024 BEV sales did not meet expectations. Manufacturers were permitted to extend the timeline under EV 3.5 conditions instead, requiring production at 2–3 times the volume of prior imports by 2026–2027. This change is expected to delay some BEV production in Thailand during 2025, with automakers shifting to importing lower-cost BEVs from China to stay competitive amid the ongoing EV price war.

Impact on EV Dealerships

The growing popularity of passenger BEVs, in contrast to ICE vehicles, along with the ongoing price war, has forced ICE dealerships to adapt. Some have exited the market,9/ while others have transitioned to selling EVs.10/ This shift is reflected in the rising number of EV dealership branches. For example, as of June

2025, BYD showrooms increased by approximately 47.6% compared to the same period last year,

11/ in line with the company’s average annual sales growth of 67.2%

12/ during 2023–2025.

However, the ongoing price war in global markets has begun to affect some EV dealerships. For instance, NETA’s parent company in China has faced continued losses, while sales in Thailand have slowed. This has led to declining dealer confidence, prompting some to offer price promotions on selected EV models to clear inventory and maintain liquidity,

13/ and remove long-term warranties.

14/ In addition, some dealers exited the market, bringing NETA’s total dealerships down to 53

15/ as of May 2025, from 66 in March 2024.

Impact on Consumers

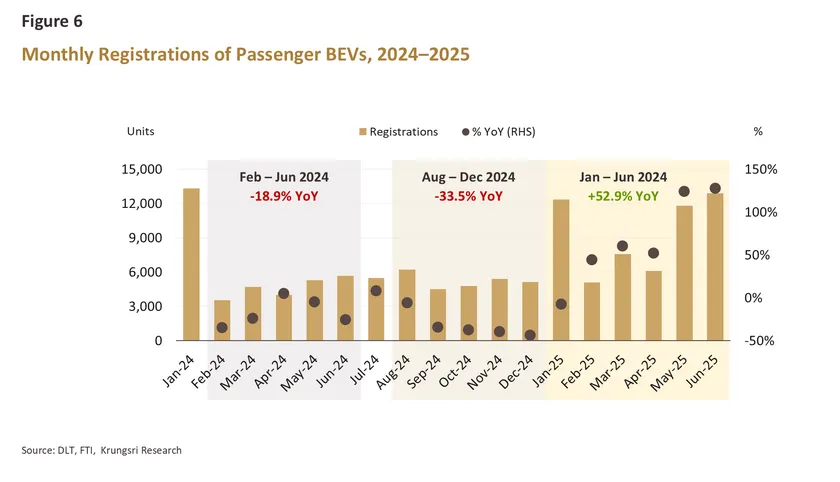

Although price reductions typically stimulate demand, the opposite effect was observed in Thailand’s passenger BEV market. For example, in June 2024, Chinese EV brands

16/ announced further price cuts, up to hundreds of thousands of baht, just three months after similar discounts during the Motor Show 2024. This led to dissatisfaction among earlier buyers, who felt pressured by dealerships to purchase before the new round of discounts. The move also triggered competitive pricing responses from other EV brands.

17/ As a result, many potential buyers began to delay their purchases, fearing that the models they intended to buy might be discounted further.

Rising consumer concerns during this period led to a sharper decline in passenger BEV registrations in the second half of 2024, contrary to automakers’ expectations that price cuts would help stimulate demand. Between February and June 2024,

18/ BEV registrations fell by -18.9%

19/ compared to the same period last year (Figure 6), and the decline accelerated to -33.5% YoY between August and December 2024. The price war also prompted some buyers to postpone delivery of vehicles booked during the Motor Expo 2024 by 3–4 months, as they waited to see whether Q1 2025 campaigns would offer deeper discounts or additional benefits.

20/

However, BEV passenger car registrations picked up again in early 2025 as the price war began to stabilize. The sharp drop in profit margins earlier limited manufacturers’ ability to cut prices further. This was reflected in the prices of Chinese passenger BEVs at the Motor Show 2025, which fell only -2.7% from late 2024. This rate was significantly lower than the -10.2% drop at the Motor Show 2024 (March–April 2024) and the -13.1% drop at the Motor Expo 2024 (November–December 2024).

The stabilizing prices, along with pent-up demand from consumers who had planned to purchase BEV passenger cars since 2024, helped boost registrations in the first half of 2025 by 52.9% compared to the same period last year, to 55,818 units.

Krungsri Research’s View: Will Thailand’s EV price war continue from 2025 to 2027, or come to end?

Intense competition in China’s EV market has affected the global auto industry, as Chinese manufacturers offload excess supply, triggering a global EV price war. In Thailand, BEV passenger car sales declined in the second half of 2024, and manufacturers delayed production. To answer the question, “When will Thailand’s EV price war come to end?”, we can analyze both external and internal factors influencing EV prices, as follows.

An analysis of external factors through Porter’s Five Forces framework shows that global EV market competition remains moderately high, with the following details:

-

Industry rivalry remains high, as the global EV market still has a large number of active manufacturers. However, competition among producers is expected to ease in the future, supported by several factors: (i) global investment in EV production and related supply chains has started to decline during 2024–2025, (ii) many small-scale manufacturers have exited the market in recent periods, and (iii) some EV brands are facing financial difficulties, leading to business closures. This aligns with the view of the Chairman of Chongqing Changan Automobile, who expects that between 2026–2028, around 60–70% of Chinese EV manufacturers may not survive in the market.21/ Additionally, He Xiaopeng, CEO of XPeng Motors, anticipates that 2025–2027 will be the “Elimination Round” 22/ of the EV industry.

-

Bargaining power of buyers is moderate. Although the EV market offers a wide range of models from various brands, giving consumers more options, bargaining power of buyers remains constrained by several limiting factors: (i) the declining share of new ICE vehicle models,23/ (ii) the growing trend of consumer acceptance toward EV technology, and (iii) stricter environmental regulations in certain countries, which are driving consumers toward increased EV usage.

-

Bargaining power of suppliers is moderate. Although batteries, the highest-cost component in EVs, remain a specialized technology produced by only a few suppliers, EV manufacturers have increasingly invested in upstream supply chains. This has led to an oversupply of batteries and related minerals,24/ reducing the bargaining power of existing suppliers. Moreover, when considering other types of components, especially those with multiple suppliers (e.g., body parts, chassis, motors), the overall bargaining power of suppliers remains at a moderate level.

-

Threat of new entrants is moderate. Although the market previously saw a surge of new EV manufacturers, the number of new entrants is expected to decline, as profit margins have been continuously squeezed by the price war that began in 2022, raising the risk of losses. Moreover, global EV sales growth has started to slow down, while some countries are beginning to phase out their EV support policies due to the large number of EV manufacturers and the weakening momentum in the EV market.

-

Threat of substitutes is moderate. Although the transition toward clean energy vehicles is expected to accelerate in the future, leading more consumers to shift from ICE vehicles to BEVs, HEVs and PHEVs remain highly popular during this transitional phase of the EV industry, which continues to limit the growth of BEV sales.

However, an analysis of domestic factors reveals that production costs and pricing will likely encourage automakers to slow down future EV price reductions, as follows:

-

Production costs are expected to rise in line with rising local compensatory EV production under the EV 3.0 and EV 3.525/ schemes. This will support a greater share of locally produced EV sales. However, EVs produced in Thailand are expected to have higher costs than Chinese imports during 2022–2025, due to the smaller domestic market and limited export demand.26/ As a result, Thai EVs have yet to achieve economies of scale comparable to Chinese EVs, which are produced in much larger volumes. Moreover, under the EV 3.0 and EV 3.5 schemes, Thai EVs must use locally sourced components, which currently cost about 10–15%27/ more than those in China. This poses a key constraint for automakers aiming to cut EV prices over the next 2–3 years. Meanwhile, the revised rules under the EV 3.0 and EV 3.5 schemes allow each passenger BEVs produced for export to be counted as 1.5 units28/ of compensatory production, rather than the standard rate of 1 unit, encouraging automakers to prioritize exports and helping reduce the risk of oversupply in the domestic EV market, which could otherwise trigger another round of price wars.

-

The price of BEV passenger cars in Thailand is on a downward trend and is expected to fall below that of ICE cars, especially Chinese BEVs, which have already been priced lower than ICEs29/ since 2024. This gives consumers more choices and increases the likelihood of switching from ICE to BEV. As a result, EV manufacturers no longer need to rely on aggressive promotional campaigns to boost sales and compete for market share as they did in the past.

Based on the aforementioned factors, Krungsri Research expects that

global competition in the EV market, which remains moderate to high, continues to drive Thailand’s EV price war. In 2025, pressure intensified as major EV makers facing liquidity issues accelerated stock clearance.

However, domestic factors, particularly local production under the EV 3.0 and EV 3.5 schemes, which involve higher costs than imported Chinese EVs, are expected to slow the price war. This effect will be more pronounced during 2026–2027, when the volume of locally produced EVs is projected to increase. The easing price war is likely to restore confidence among consumers who had previously postponed purchases, thereby supporting growth in BEV passenger car registrations. Automakers that withstand intense competition are likely to become more profitable as the price war begins to ease.

References

Autolifethailand. (2023, November 12). "ส่วนลด 110,900 ! ราคาพิเศษ MG4 Electric รถไฟฟ้า100% : 599,000 บาท (ประกอบไทย) | เฉพาะรุ่น D สีส้ม เท่านั้น". Retrieved from https://autolifethailand.tv/official-discount-price-mg4-d-standard-range-nov-2024/

Autolifethailand. (2023, October 18). "ส่วนลด 50,000 บาท ! ลดราคา NETA V รถไฟฟ้า100% : 499,000 บาท | แบต LFP 40.7 kWh วิ่งไกล 384 km." Retrieved from https://autolifethailand.tv/discount-price-neta-v-ev-bev-2023-thailand/

Autolifethailand. (2024, March 26). "ส่วนลด 250,000 ! ราคาพิเศษ BYD Atto 3 (MY2023) รถไฟฟ้า100% : 899,900 – 949,900 บาท | Motor Show 2024". Retrieved from https://autolifethailand.tv/special-price-byd-atto3-my2023-motor-show-2024/?utm

Autospinn. (2023, December 8). "รวมโปรสุดคุ้ม รถอีวีค่ายดัง Motor Expo 2023". Retrieved from https://www.autospinn.com/2023/12/promotion-motor-expo-2023-134228

Autospinn. (2024, July 4). "สงครามราคา EV มีอะไรดี?". Retrieved from https://www.autospinn.com/2024/07/car-ev-price-war-in-thailand-137614?utm

Autospinn. (2025, April 4). "โปรเดือด!! รถยนต์ไฟฟ้าขนาดเล็ก โค้งสุดท้าย Motor Show 2025". Retrieved from https://www.autospinn.com/2025/04/promotion-ev-car-motor-show-2025-142406

Bangkok Business. (2025, May 28). "วิกฤติ EV ‘สต๊อกล้น’ ทั่วโลก จุดพลุสงครามราคารอบใหม่". Retrieved from https://www.bangkokbiznews.com/business/economic/1182188

Bangkok Post. (2024, November 18). Raft of issues hindering EV industry". Retrieved from https://www.bangkokpost.com/business/motoring/2904017/raft-of-issues-hindering-ev-industry#:~:text=EV%20manufacturers%2C%20particularly%20Chinese%20companies%2C%20are%20monitoring%20EV,high%20household%20debt%20to%20the%20EV%20price%20war

Bloomberg. (2024, July 9). "China’s Batteries Are Now Cheap Enough to Power Huge Shifts". Retrieved from https://www.bloomberg.com/news/newsletters/2024-07-09/china-s-batteries-are-now-cheap-enough-to-power-huge-shifts

Business Insider. (2025, January 10). "Xpeng's CEO says the auto industry will enter an 'elimination round' from 2025 to 2027". Retrieved from https://www.businessinsider.com/xpeng-ceo-2025-2027-kick-off-ev-industry-elimination-round-2025-1?utm

CarNewsChina. (2024, February 27). "New Zeekr 001 launched in China with 580 kW for 37,500 USD". Retrieved from https://carnewschina.com/2024/02/27/new-zeekr-001-launched-in-china-with-580-kw-for-37500-usd/

CarNewsChina. (2025, April 15). "Zeekr 007 GT station wagon launched in China for 27,200 USD". Retrieved from https://carnewschina.com/2025/04/15/zeekr-007-gt-station-wagon-launched-in-china-for-27200-usd/

CNN Business. (2024, April 24)."A brutal elimination round is reshaping the world’s biggest market for electric cars". Retrieved from https://edition.cnn.com/2024/04/24/business/china-ev-industry-competition-analysis-intl-hnk

Droidsans. (2024, November 28). "BYD ประกาศลดราคารถยนต์ไฟฟ้าทุกรุ่น ในงาน Motor Expo 2024 ทั้ง SEALION 7, ATTO 3, Dolphin, Seal, SEALION 6". Retrieved from https://droidsans.com/byd-motor-expo-2024/

Droidsans. (2025, March 25). "รวมโปร เปิดตัวราคารถยนต์ไฟฟ้าใหม่ รวมถึงรถไฟฟ้าเก่าลดราคา ในงาน Motor Show 2025 ที่อิมแพ็ค เมืองทองธานี" Retrieved from https://droidsans.com/motor-show-2025-ev-car-promotion/

IEA. (2024). "Global EV Outlook 2024". Retrieved from https://www.iea.org/reports/global-ev-outlook-2024

IEA. (2025). "Global EV Outlook 2025". Retrieved from https://www.iea.org/reports/global-ev-outlook-2025

InsideEVs. (2025, January 2). "Prepare For An Electric Car Price War In 2025". Retrieved from https://insideevs.com/news/746040/ev-price-war-2025-xpeng/

Investopedia. (2025, June 10). "Herfindahl-Hirschman Index (HHI): Definition, Formula, and Example". Retrieved from https://www.investopedia.com/terms/h/hhi.asp?utm

Motor Expo. (2024, December 3). "Neta จัดขบวนรถไฟฟ้าหลากสไตล์ พร้อมสัมผัส Neta S Shooting Brake ครั้งแรกในงาน Motor Expo 2024 !". Retrieved from https://www.motorexpo.co.th/news/4937

PPTV. (2024, March 23). "Motor Show 2024 ยลโฉม NETA V-II รถไฟฟ้า 100% เริ่มต้น 5.49 - 5.69 แสน". Retrieved from https://www.pptvhd36.com/automotive/news/220559

PPTV. (2024, March 28). "MG จัดหนัก MOTOR SHOW 2024 เปิดตัวรถใหม่ 4 รุ่น". Retrieved from https://www.pptvhd36.com/automotive/news/220429

Prachachart Business. (2025, January 16). "ดีลเลอร์รถ EV อ่วมเกมหั่นราคา ยอดขายอืด-ขาดสภาพคล่อง". Retrieved from https://www.prachachat.net/prachachat-top-story/news-1734331

Prachachart Business. (2025, July 30). "บอร์ดอีวี ปรับเกณฑ์ EV3-EV3.5 จูงใจผลิตส่งออกขยายเวลาจดทะเบียนอีก 1 เดือน". Retrieved from https://www.prachachat.net/finance/news-1855474

Prachachart Business. (2025, June 4), "‘เนต้า’ EV จีนระส่ำแห่ปิดโชว์รูม โละสต๊อกเหลือคันละ 2.99 แสน". Retrieved from https://www.prachachat.net/motoring/news-1822232

Prachachat Business. (2024, December 1). "ดีลเลอร์รถรายใหญ่ ย่านรังสิต ถอดใจยุติธุรกิจ หันปล่อยเช่าโชว์รูมแทน". Retrieved from https://www.prachachat.net/motoring/news-1706488

Prachachat Business. (2024, October 9). "ตลาดรถทรุดเหลือแค่ 6 แสนคัน ดีลเลอร์แห่ปิดตัว-ย้ายขาย EV". Retrieved from https://www.prachachat.net/motoring/news-1670221

Prachachat Business. (2025, June 30). "เบนซ์ สตาร์แฟลก ยุติบทบาทดีลเลอร์ เบนซ์ มีผล 1 กรกฎาคม 2568". Retrieved from https://www.prachachat.net/motoring/news-1837438

Reuters. (2025, May 27). "China auto market price war stokes fears of industry shake- out". Retrieved from https://www.reuters.com/business/autos-transportation/china-auto-market-price-war-stokes-fears-industry-shake-out-2025-05-27

Reutes. (2024, September 4). "Volvo Cars abandons 2030 EV-only target". Retrieved from https://www.reuters.com/business/autos-transportation/volvo-cars-scales-back-electric-vehicle-ambition-2024-09-04/

South China Morning Post. (2025, January 7). "Chinese EV makers cannot stop ‘aggressive’ price-cutting – even as it imperils them". Retrieved from https://www.scmp.com/business/china-business/article/3293635/chinese-ev-makers-cannot-stop-aggressive-price-cutting-even-it-imperils-them

South China Morning Post. (2025, July 4). "Only 1 in 10 EV makers may hit 2030 profit goal in China’s discount war, AlixPartners says". Retrieved from https://www.scmp.com/business/china-business/article/3316864/chinas-ev-price-war-dashes-profit-hopes-90-brands-alixpartners-says

Techoffside. (2024, November 28). "เปิด ราคา BYD SEALION 7 พร้อมเผยโฉม BYD SHARK 6 ครั้งแรกในไทย ที่งาน Motor Expo 2024". Retrieved from https://www.techoffside.com/2024/11/reve-motor-expo-2024-byd-sealion7-shark6-launch/

Thai Rath. (2024, July 2). "“จิราพร” สั่ง สคบ. ตรวจสอบแคมเปญรถยนต์ไฟฟ้าเจ้าดัง หลังกระหน่ำลดราคา". Retrieved from https://www.thairath.co.th/news/politic/2797683

Thansettakij. (2024, July 3). "งานเข้า BYD สคบ. เรียกชี้แจง ปมจัดโปรฯลดราคาสูงสุด 3.4 แสนบาท". Retrieved from https://www.thansettakij.com/business/economy/600785

Thansettakij. (2025, May 19). "ดีลเลอร์เนต้า Cut Loss ล็อตใหญ่ ลดราคา NETA V-II ต่ำกว่า 4 แสนบาท". Retrieved from https://www.thansettakij.com/motor/ev/627880

The Wall Street Journal. (2023, August 17). "Tesla Cuts Prices in China as Price-War Truce Fails". Retrieved from https://www.wsj.com/business/autos/tesla-cuts-prices-in-china-as-price-war-truce-fails-60af6d4d?msockid=23f6b874aa9a60fa0af4ab4bab3161f7

The Wall Street Journal. (2025, March 25). "Tesla’s EU Sales Plunged Again in February". Retrieved from https://www.wsj.com/business/autos/teslas-eu-sales-plunged-again-in-february-d14937c0

Trueid. (2023, March 22). "อัปเดตราคารถใหม่ เอ็มจี (MG) งานมอเตอร์โชว์ 2023". Retrieved from https://news.trueid.net/detail/ZnEaVgpDVzmn

1/ Source: IEA (2025)

2/ Source: IEA (2024)

3/ Source: South China Morning Post (January 7, 2025)

4/ Source: Wall Street Journal (August 17, 2023)

5/ Details of EV manufacturers establishing production bases in Thailand can be found in Thailand Industry Outlook 2024–2026: Electric Vehicle Industry, page 16.

6/ The HHI index is calculated based on the market share of new EV registrations by brand, using data from the Department of Land Transport (DLT). In general, the HHI ranges from 0 to 10,000. An HHI below 1,500 indicates a highly competitive market; an HHI between 1,500 and 2,500 suggests moderate competition; and an HHI above 2,500 reflects low competition, with market share concentrated among a few players. (Source: Investopedia; June 10, 2025)

7/ Further details can be found in Thailand Industry Outlook 2024–2026: Electric Vehicle Industry.

8/ EV registration data used in this analysis is sourced from the Department of Land Transport (DLT).

9/ For example, Mitsu Republic Co., Ltd. announced the termination of its dealership for Mitsubishi vehicles effective December 1, 2024, while Benz Star Flag Co., Ltd. ended its dealership for Mercedes-Benz on July 1, 2025. (Source: Prachachat Business (December 1, 2024) and Prachachat Business (June 30, 2025))

10/ For example, Synergetic Auto Performance PCL reduced some branches of its Japanese brands and shifted to become a dealer for Deepal. Similarly, the Honda Rama 3 Group transitioned to represent both GWM and Deepal. (Source: Prachachat Business (October 9, 2024))

11/ There were 155 showrooms as of July 2025. (Source: compiled from Rever Automotive’s website as of June 30, 2025)

12/ Source: DLT

13/ For example, the NETA V-II model announced a price cut in June 2025 to 299,000–339,000 baht per unit, along with various promotional offers such as “Buy 4, Get 1 Free” or a 20% discount. (Source: Prachachat Business (June 4, 2025))

14/ Examples include first-class insurance coverage under the compulsory motor insurance scheme for one year, an 8-year or 180,000 km battery warranty, a 5-year or 150,000 km vehicle warranty, free labor and parts for the first maintenance check, and a Wall Box. (Source: Prachachat Business (June 4, 2025))

15/ Meanwhile, Neta’s total workforce in Thailand—covering both its headquarters and factory, declined from 50 to 40 employees. (Source: Prachachat Business (June 4, 2025))

16/ In June 2025, BYD launched a promotion for its BYD DOLPHIN EV model, offering a discount of 140,000–160,000 baht, significantly higher than the previous 40,090 baht discount, which had urged consumers to purchase by April 30, 2024. (Source: Thairath (July 2, 2024))

17/ Examples of EV models with price reductions during this period include the BYD Dolphin Standard Range (cut from 699,999 baht to 559,900 baht), BYD Atto 3 Dynamic (MY2023) (cut from 899,000 baht to 799,000 baht), and Neta V-II (Lite) (cut from 549,000 baht to 499,000 baht). (Source: Thairath (July 2, 2024))

18/ Support under the EV 3.0 scheme ended in January 2024, while support under the EV 3.5 scheme began in February 2024.

19/ Source: DLT

20/ Source: Prachachat Business (January 16, 2025)

21/ Source: Wall Street Journal (August 17, 2023)

22/ Source: Business Insider (January 10, 2025)

23/ The share of new ICE and HEV models declined to 65.9% of all car models in 2024 and is projected to fall further to 58.3% by 2027 (IEA, 2025).

24/ In 2023, there was a global oversupply of minerals used in battery production. For example, lithium, primarily used in Chinese EV batteries, had an excess supply of 10%, while cobalt and nickel, mainly used in EU and U.S. EVs, had surplus levels of 6.5% and 8%, respectively. In 2024, global battery cell production capacity expanded to a level three times higher than the market demand for electric vehicles and energy storage systems (IEA, 2024 and IEA, 2025).

25/ EV manufacturers supported under the EV 3.0 scheme are allowed to fulfill their local production requirement in 2025 at a ratio of 1.5 times the number of imported units sold during 2022–2023. Alternatively, they may defer production and fulfill the requirement under the EV 3.5 scheme at a ratio of 2 to 3 times during 2026–2027, in accordance with the resolution of the National EV Policy Board on December 4, 2024.

26/ Thailand officially exported its first batch of BEV passenger cars in April 2025, totaling 660 units, accounting for only 1.0% of total vehicle exports in the same month (Source: FTI).

27/ Source: Bangkok Post (November 18, 2024)

28/ According to the resolution of the National EV Policy Board meeting on July 30, 2025 (Source: Prachachat Business; July 30, 2025).

29/ Chinese BEVs had an average retail price of USD 30,000 in Thailand, approximately 11.8% lower than the average price of ICE vehicles at USD 34,000 (Source: IEA, 2025).