Executive Summary

Thailand’s motorcycle industry is a key pillar of the global supply chain. However, the country is increasingly at risk of losing export market share to competitors, particularly within ASEAN, where electric motorcycle production for export has been expanding. Meanwhile, Thailand’s electric motorcycle production base and domestic market remain relatively small, constrained by reduced support measures, still‑unattractive pricing, concerns over hidden battery replacement costs, limited access to credit, unfamiliarity with new technologies, range limitations, and fragmented charging or battery‑swapping infrastructure across service providers.

Therefore, manufacturers, developers, and distributors of electric motorcycles should recalibrate their strategies by focusing on products tailored to diverse user segments, reducing battery costs, leveraging data and software, and accelerating ecosystem development. At the same time, the government should introduce continued support measures following the expiration of the EV 3.5 scheme, while also improving regulations that continue to constrain the domestic market, particularly the establishment of common standards for electric and battery infrastructure. Such coordinated efforts between the private and public sectors will help turn constraints into opportunities and enable Thailand’s electric motorcycle industry to sustain its key role in the global market.

Introduction

Thailand’s motorcycle industry plays an important role in the global supply chain, as evidenced by its large production volume, ranking among the world’s top five. Nevertheless, Thailand still faces several constraints in transitioning the industry toward electric motorcycles. Despite ongoing government support through the EV 3.0 and EV 3.5 schemes, sales and production of electric motorcycles in Thailand have remained limited in recent years. This has heightened the risk of losing export market share to competitors that have begun producing electric motorcycles for export, raising questions over how long Thailand can sustain its current standing in the global market.

This article reviews the recent landscape of Thailand’s electric motorcycle industry, including key constraints. These resemble a “chicken‑and‑egg” dilemma, where consumers await further technological advancements while manufacturers delay investment until the market matures. It also outlines strategic directions to drive the industry forward and sustain Thailand’s competitiveness as the global electric motorcycle market continues to expand.

The Transition toward the Electric Motorcycle Industry in Recent Years

Motorcycles have long been the primary mode of transportation for Thai consumers. Over the years, the government has continuously supported the motorcycle manufacturing industry, leading to sustained investment from new entrants, including manufacturers of small Internal Combustion Engine (ICE) motorcycles, big bikes, and electric motorcycles

1/.

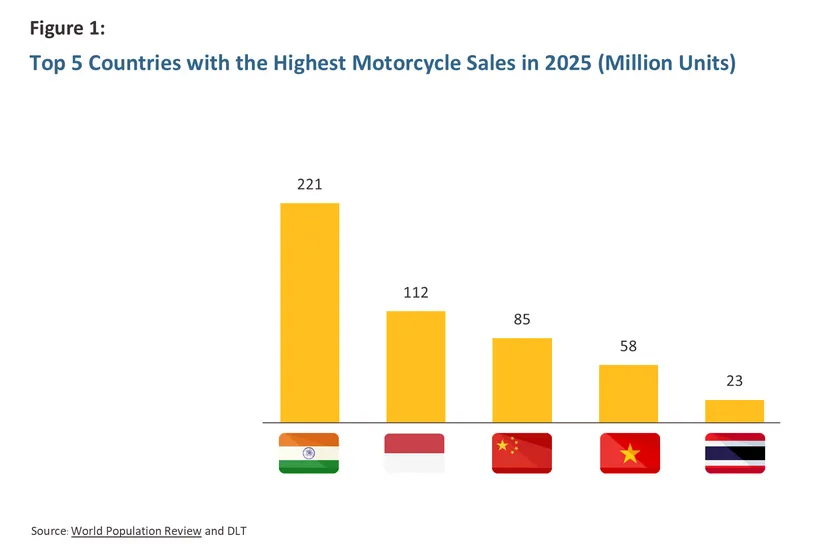

In 2025, Thailand ranked as the world’s fifth-largest motorcycle producer, with total output of 1.8 million units2/, of which more than 80% was produced for the domestic market. As a result, by the end of 2025, Thailand recorded the fifth-highest cumulative motorcycle registrations globally, totaling 23.3 million units3/ (Figure 1).

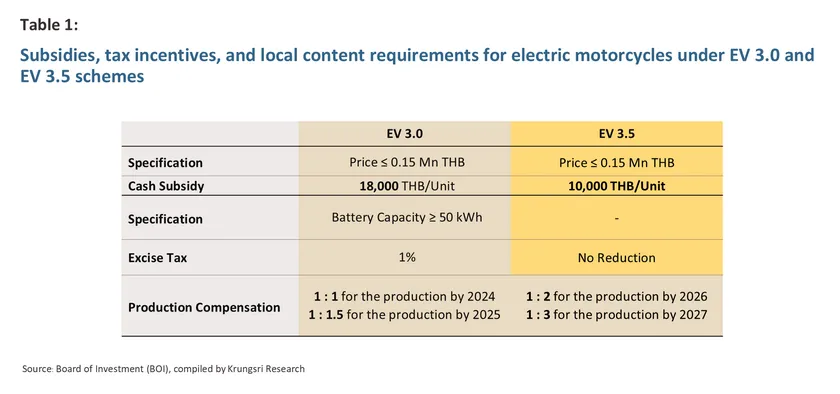

The production of electric motorcycles is one of the next-generation industries prioritized by the government to achieve carbon-emission reduction targets in the transport sector. In recent years, the government has promoted the industry through subsidies and related tax incentives under the EV 3.0 (2022–2025) and EV 3.5 (2024–2027)4/ schemes (Table 1), encouraging a number of new electric motorcycle manufacturers to invest in domestic production facilities. In particular, during 2022–2023, a total of 15 electric motorcycle manufacturers established production bases in Thailand, most of which were Thai-owned companies, such as ETRAN (THAILAND) CO., LTD., EDISON MOTOR CO., LTD., and H SEM MOTOR CO., LTD.

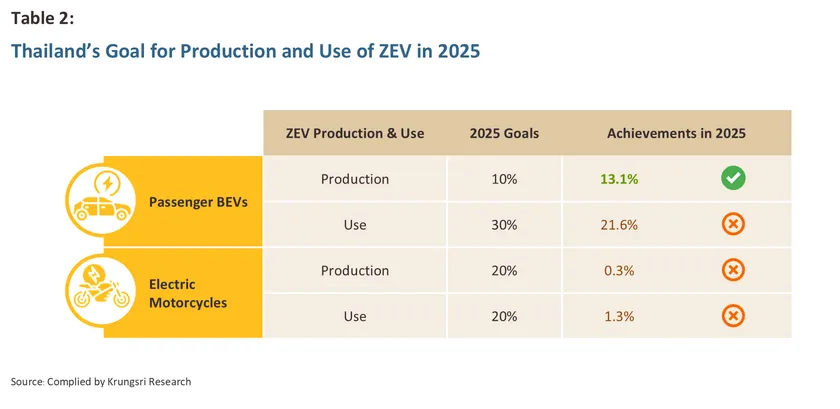

However, Thailand’s electric motorcycle market has remained relatively limited in recent years. In 2025, electric motorcycles accounted for only 1.3% of total new motorcycle registrations

5/ and just 0.3% of total motorcycle production across all segments6/. These figures remain well below the EV Board’s target of a 20% share in both sales and production by 2025. In contrast, the passenger BEV market has continued to gain traction and was the only electric vehicle segment to achieve its production target in 2025, with production and sales shares reaching 13.1% and 21.6%, respectively (Table 2).

Electric Motorcycle Production in Recent Years

The promotion of electric motorcycle production under the EV 3.0 and EV 3.5 schemes, introduced since 2022, has yet to meet production targets but has nevertheless contributed to a shift in the industry structure.

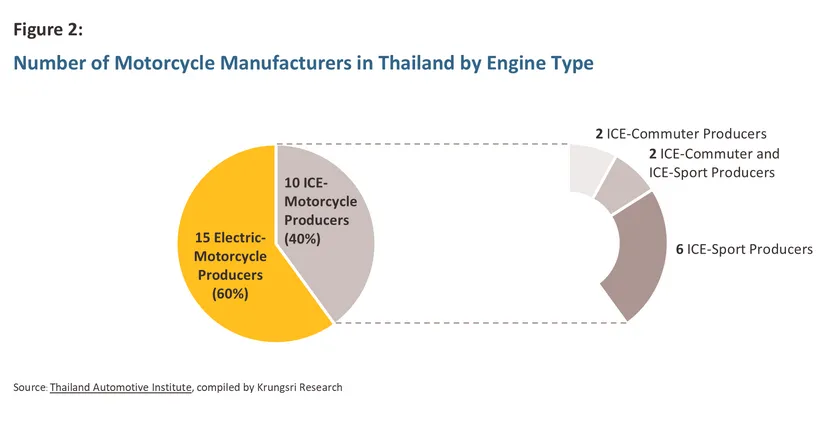

This is evident from the current number of electric motorcycle manufacturers, which now account for more than half of all motorcycle manufacturers in Thailand. As of end-2025, Thailand had a total of 25 motorcycle manufacturers with production facilities either in operation or under construction in the country, comprising 15 electric motorcycle manufacturers (60.0%) and 10 ICE motorcycle manufacturers

7/ (40.0%) (Figure 2).

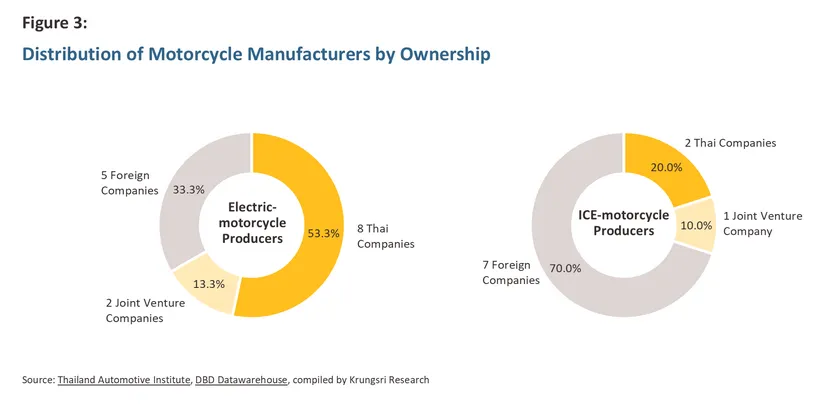

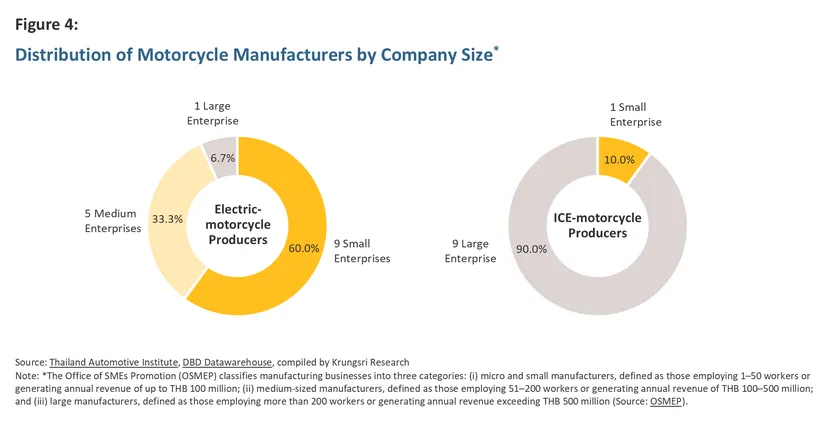

However, most new electric motorcycle manufacturers remain Thai‑owned and are predominantly small and medium‑sized enterprises. This is evident from (i) company nationality: electric motorcycle manufacturers in Thailand comprise 66.6% Thai‑owned firms and Thai–foreign joint ventures (with the remainder being foreign firms), in contrast to ICE motorcycle manufacturers, where Thai firms account for only 30.0% (Figure 3); and (ii) company size: SMEs represent 93.3% of electric motorcycle manufacturers, compared with just 10.0% among ICE motorcycle manufacturers (Figure 4).

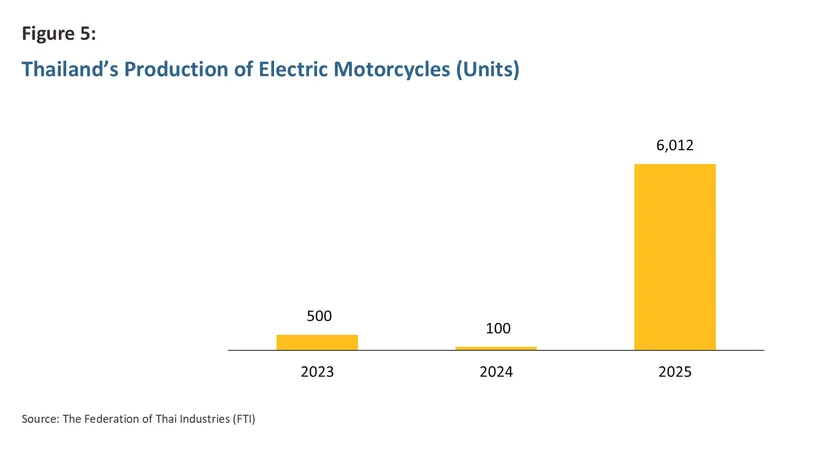

Thailand officially began producing electric motorcycles in 2023, with an initial output of 500 units (Figure 5). Production rose to 6,012 units in 2025, representing a CAGR of 246.8% during 2023–2025, driven by some manufacturers accelerating production to compensate for previously imported units to meet EV 3.0 requirements, which expire in 2025.However, electric motorcycle production accounted for only 0.3% of total motorcycle output, as some manufacturers postponed compensation production to 2026–20278/ (under the EV 3.5 scheme), reflecting the relatively low adoption of electric motorcycles in Thailand.

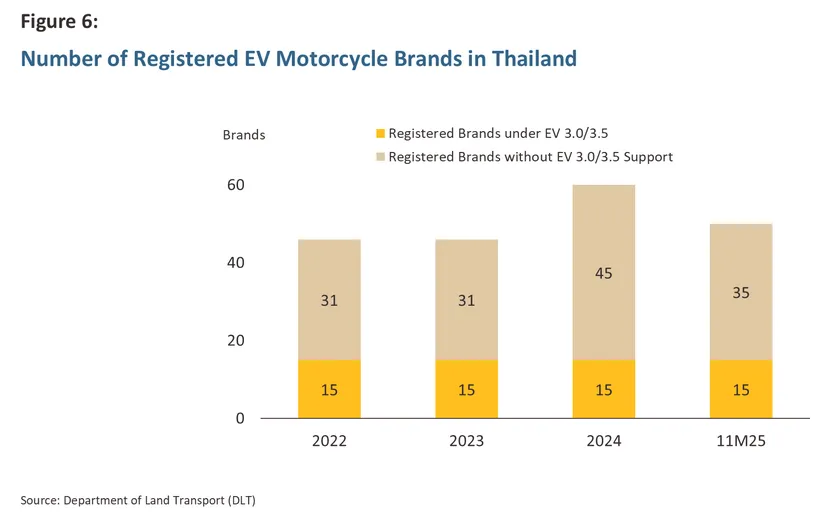

However, despite the currently limited popularity of electric motorcycles in Thailand, the market still has long-term growth potential, supported by two key factors: (i) Thailand is the world’s fifth-largest motorcycle market, prompting some manufacturers to import electric motorcycles to test the Thai market independently of the EV 3.5 scheme, which mandates post-subsidy production compensation. As a result, during 2024–2025, the number of brands selling and registering electric motorcycles without government subsidies increased to 35–45, up from 31 brands in 2022–2023 (Figure 6); and (ii) government investment in EV infrastructure—totaling over THB 6.9 billion during 2022–2025—has supported the development of 555 battery swapping stations for electric motorcycles and 20,080 EV charging stations9/.

Electric Motorcycle Sales in Recent Years

Electric Motorcycle Market in Thailand

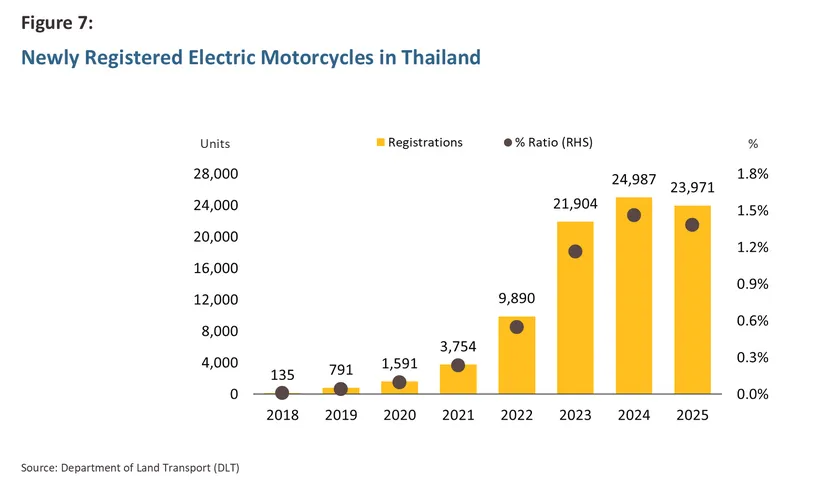

Electric motorcycles have yet to gain strong traction in Thailand in recent years, as reflected by cumulative registrations of 80,752 units over 2022–2025, accounting for only 1.0% of total cumulative registrations of all motorcycle types (Figure 7), despite support from government incentive schemes. During 2022–2023, under the EV 3.0 scheme, new registrations of electric motorcycles expanded at an average rate of 141.6% per year, reaching 21,904 units in 2023, yet still accounting for only 1.1% of total new motorcycle registrations. Meanwhile, during 2024–2025 under the EV 3.5 scheme, new registrations rose only marginally at an average of 4.6% per year to 23,971 units in 2025, or 1.3% of total new registrations. This was partly due to a reduction in subsidy amounts from THB 18,000 per unit under EV 3.0 to THB 5,000–10,000 per unit under EV 3.5, together with stricter production compensation requirements, which were raised from 1:1–1.5 units under EV 3.0 to 1:2–3 units under EV 3.5. As a result, the rollout of new electric motorcycle models at affordable price points to stimulate market demand has remained limited.

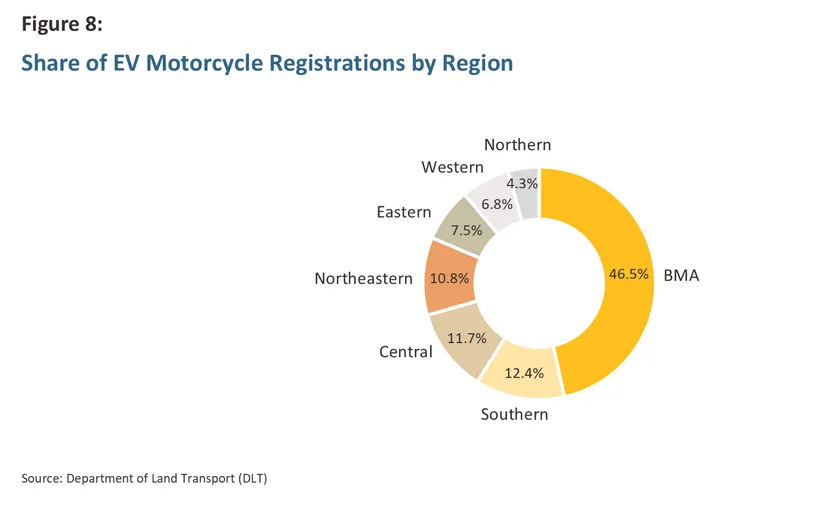

In addition, a regional breakdown (Figure 8) shows that electric motorcycles remain highly concentrated in the Bangkok Metropolitan Region. In 2025, the area accounted for 46.5% of total new electric motorcycle registrations nationwide, in line with the greater availability of EV infrastructure—both charging stations and battery swapping stations—as well as the continued concentration of food delivery and ride-hailing services in Bangkok and its surrounding areas in recent years.

Thailand’s Position in the Global Electric Motorcycle Market

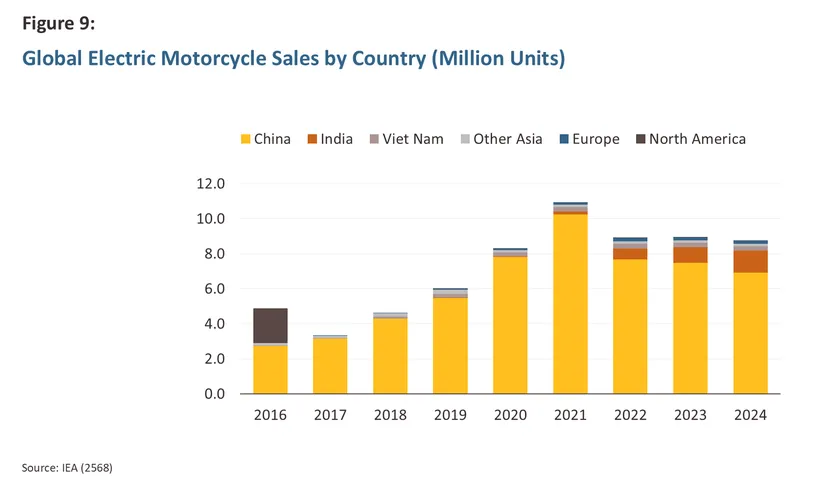

Global sales of electric motorcycles have remained at a high level in recent years10/. In 2024, worldwide sales reached 10 million units, accounting for 15% of total motorcycle sales (Figure 9). Motorcycles are also the fastest segment to electrify among all vehicle types, as reflected by cumulative electric motorcycle sales accounting for around 7% of total cumulative motorcycle sales, higher than passenger BEVs and electric pickup trucks at 4% of total cumulative passenger vehicle and pickup truck sales. China, India, and ASEAN remain the largest markets for electric two- and three-wheelers, collectively accounting for around 80% of global electric motorcycle sales in 2024.

Key factors supporting the global adoption of electric motorcycles in recent years10/ include more affordable pricing compared with other types of electric vehicles, the launch of new models with longer driving ranges, supportive government policies11/, and more convenient charging. Electric motorcycles can be charged using household electricity without additional equipment, while some models offer battery swapping, reducing charging time compared with passenger BEVs.

However, new registrations and production of electric motorcycles in Thailand have remained relatively low in recent years, in contrast to strong and steadily growing global sales and production. In addition, the expansion of production bases by Chinese manufacturers into other countries12/ may pose a risk for Thailand to fall behind in the global electric motorcycle market, as it could lose export market share to competitors in China, India, and ASEAN, and potentially its position as the world’s fifth-largest motorcycle producer in the future.

Challenges to the Growth of Thailand’s Electric Motorcycle Market

The persistently low sales of electric motorcycles in recent years have been driven by multiple constraining factors that extend beyond pricing and technological readiness, reflecting broader structural limitations in the external environment that influence both consumer decisions and overall business investment. To systematically assess these factors in a comprehensive manner,

the PESTEL framework can be applied, which evaluates macro-environmental conditions across Political (P), Economic (E), Social (S), Technological (T), Environmental (E), and Legal (L) dimensions, as outlined below.

Political Factor (P)

- Diminishing incentives from support measures: Although the government has actively promoted the electric motorcycle industry through the EV 3.0 and EV 3.5 schemes since 2022, subsidies under EV 3.5 during 2024–2025 were reduced to a maximum of THB 10,000 per unit, compared with up to THB 18,000 per unit under EV 3.0 in 2022–2023. This comes despite relatively low registration levels, accounting for only 1.1% of total motorcycle registrations, resulting in insufficient market stimulus and keeping electric motorcycle registrations at a low level thereafter.

Economic Factors (E)

-

Unattractive pricing: Electric motorcycles sold in Thailand generally remain less price-competitive compared with ICE motorcycles, partly due to imports without government subsidies. Models that meet functional performance requirements and offer a driving range of 101–150 kilometers per charge are priced at around THB 60,000–80,000, while popular ICE motorcycles in the 110 cc and 125 cc segments are priced lower, typically in the range of THB 40,000–70,000.

-

Hidden costs from battery replacement: Consumers remain concerned about the cost of battery replacement after the warranty period, as the battery is the most expensive component, accounting for around 30–50% of the total price of an electric motorcycle. In addition, the average battery warranty period in Thailand ranges from 2–10 years, which is shorter than the actual usage period for many motorcycle owners, as reflected by motorcycles aged over 10 years still accounting for as much as 39.6% of total cumulative registrations in the country13/.

-

Rapid depreciation in resale value: The resale value of electric vehicles generally declines faster than that of ICE vehicles14/, driven by several factors15/. These include consumer concerns over potential battery degradation in used electric vehicles, as well as the introduction of newer models offering longer driving ranges at lower prices amid intensifying price competition, which has reduced demand for used electric vehicles. During 2021–2025, cumulative registrations of used electric motorcycles accounted for only 0.1% of total cumulative registrations of all used motorcycles16/.

-

Limited access to financing: Financial institutions remain more cautious in extending loans for electric motorcycles compared with ICE motorcycles17/, partly due to several risk factors. These include (i) the risk of business closures among new electric motorcycle brands in Thailand, many of which are still in the market-testing phase through imports without participating in government support schemes; (ii) weak purchasing power among middle- to lower-income consumers amid an incomplete economic recovery, persistently high household debt, and elevated levels of non-performing and special mention loans (NPLs and SMLs) in the auto loan segment; and (iii) the risk of faster depreciation in the resale value of electric motorcycles compared with ICE motorcycles.

Social Factors (S)

-

Unfamiliarity with new technology: Electric motorcycles offer a riding experience that differs from conventional ICE motorcycles, which have long been widely adopted, leading to a lack of familiarity among some consumers. Key aspects include (i) differences in riding dynamics, with quicker acceleration and braking compared with ICE motorcycles, where speed changes are more gradual; (ii) greater planning requirements, as users need to manage charging more carefully given the still-limited availability of charging and battery swapping stations, as well as longer charging times compared with refueling; and (iii) unfamiliarity with battery swapping models, as some Thai consumers are not yet accustomed to owning an electric vehicle without full ownership of the battery, limiting broader adoption18/.

-

Concerns over after-sales service: Thai consumers remain concerned about after-sales support, as most electric motorcycle brands in the market still have limited service networks and face the risk of discontinuing after-sales services. More than half of the brands are imported without support under the EV 3.0 and EV 3.5 schemes, resulting in a lack of clear plans to invest in local production bases. In addition, a shortage of skilled technicians for electric motorcycle maintenance has constrained the availability of general repair shops capable of providing such services.

Technological Factors (T)

-

Range limitations: Current battery technology still offers relatively limited energy density, resulting in constrained driving range per charge for electric motorcycles. The top three best-selling electric motorcycle models in Thailand in 2025 provide a range of only 60–80 kilometers per charge19/, which remains insufficient to meet the needs of most consumers and is not well suited for long-distance travel.

-

Charging time constraints: Although electric motorcycles can be charged at home using a standard 220-volt power supply, charging typically takes around 2–7 hours17/. In addition, charging infrastructure remains limited in upcountry areas, which may not yet support commercial use cases effectively—particularly in time-sensitive delivery services such as parcel and food delivery.

-

Battery weight limitations: Despite recent investments in battery swapping infrastructure for electric motorcycles in Thailand, this model has yet to gain traction. This is partly due to relatively heavy battery packs, which weigh around 10–12 kilograms20/, making them less convenient and not well aligned with most consumers.

Environmental Factors (E)

-

Consumer concerns over lifecycle emissions reduction: Although electric motorcycles help reduce emissions during operation, some environmentally conscious consumers remain hesitant to purchase due to doubts over whether they meaningfully reduce carbon emissions across the entire value chain. In addition, Thailand still lacks clear regulations and dedicated facilities for lithium-ion battery recycling, which may pose environmental risks21/.

-

Flood-related damage risks: Although electric motorcycles are designed to be water‑resistant and comply with IP (Ingress Protection) standards, some consumers—particularly in Bangkok and the surrounding metropolitan areas, where flood‑prone locations are common—remain concerned about riding through flooded roads when water levels exceed wheel‑hub height22/. Such conditions may increase the risk of short circuits and potential damage to the battery, which is the most costly component in terms of repair and replacement.

Legal Factors (L)

-

Lack of battery standardization enabling cross‑brand interoperability: Thailand has more than 91 registered electric motorcycle brands, each adopting different electrical standards for chargers and batteries. These differences include battery safety standards, electrical connectors, and communication protocols between the battery, the vehicle, and battery swapping stations. As a result, many electric motorcycles are not compatible with cross‑brand battery swapping cabinets that operate under different electrical standards, limiting interoperability across brands17/.

-

Lack of regulations restricting ICE motorcycle use in key areas: Thailand currently lacks regulations limiting ICE vehicle use to reduce carbon emissions in major urban areas or key tourist destinations—measures that could otherwise support electric motorcycle adoption. This contrasts with countries where electric motorcycles are widely adopted, such as China, India, and Vietnam, which have implemented bans or restrictions on ICE motorcycles in key urban zones. Such policies have played a significant role in encouraging consumers to shift toward electric motorcycles23/.

-

Restrictions on registering electric motorcycles for public motorcycle taxi services: At present, riders—who are increasingly adopting electric motorcycles for work—continue to face difficulties in registering their vehicles under the public motorcycle taxi category (Category 17 under the Thai vehicle registration system), as most motorcycles are acquired through hire‑purchase arrangements, leaving riders without formal proof of ownership required for registration24/.

Krungsri Research View: From Constraints to Opportunities in Thailand’s Electric Motorcycle Industry

To elevate Thailand’s electric motorcycle industry into a new growth engine and enhance its global competitiveness, existing “constraints” must be transformed into “opportunities.”

This requires the adoption of strategic business approaches25/ to strengthen the capabilities of EV motorcycle manufacturers and distributors in Thailand, enabling them to access both domestic and export markets in a sustainable manner, as outlined below.

1. Product development aligned with customer needs: To address social (S) constraints, particularly consumers’ limited familiarity with new technologies, EV motorcycle manufacturers and designers should develop products tailored to clearly defined target segments, considering usage purposes, vehicle design, and accessibility to supporting infrastructure. Customers can be broadly categorized into two groups, as follows:

-

Personal mobility users: This group typically uses motorcycles for short-distance travel and prefers plug-in charging models. Manufacturers should therefore focus on developing small-sized, affordable EV motorcycles with durable batteries, while forming business partnerships with charging station operators to expand nationwide charging network coverage.

-

Commercial and occupational users: This group generally travels longer distances and requires fast energy replenishment through battery swapping. Manufacturers should prioritize the development of battery-swapping EV motorcycles with lightweight batteries that are easy to handle, while establishing strategic collaborations with battery-swapping service providers to ensure product compatibility with providers’ electrical standards and to support the expansion of battery-swapping stations nationwide.

2. Cost reduction: To enhance economic viability (E), EV motorcycle manufacturers should invest in technologies to lower production costs—particularly battery costs, which account for approximately 30–50% of total EV motorcycle production costs—through a design‑to‑value approach, as outlined below:

- Large manufacturers: Beyond in‑house battery development, which entails high R&D costs, manufacturers can reduce costs through battery pack assembly, an increasingly adopted approach that offers flexibility to optimize vehicle performance and safety. In addition, forming strategic partnerships or vertical integration with battery manufacturers—a critical supply‑chain component—can facilitate the co‑development of high‑quality batteries26/ and help lower production costs over the long term27/.

- SME manufacturers: With limited capital for R&D of new battery models, SMEs can adopt a platform standard battery strategy by establishing business collaborations between battery‑swapping service providers and swappable battery manufacturers, rather than developing batteries in‑house, which requires substantial investment.

3. Leading business transformation through data and software: To address social (S) constraints related to consumers’ limited familiarity with new technologies and after‑sales service concerns, and to offset technological (T) constraints stemming from limited range, manufacturers and distributors can develop software solutions and data analytics systems to enhance business performance across several dimensions, including:

-

Product development: EV motorcycle manufacturers and designers can build driving‑behavior data platforms to analyze usage patterns and develop new models better suited to Thai riders. For example, data from battery and motor temperature sensors can be used to design cooling systems appropriate for Thailand’s climate, reducing the risk of premature battery degradation. In addition, manufacturers can develop and regularly update user‑friendly software, such as region‑ and behavior‑specific vehicle control systems and peer‑to‑peer motorcycle‑sharing features.

-

Marketing: EV motorcycle distributors can strengthen brand awareness and consumer acceptance by adopting hybrid sales channels that combine the convenience of online product selection and information access with offline customization options and test‑ride opportunities, helping to build consumer confidence in EV motorcycle technology.

-

After‑sales services: Distributors and service centers can deploy software‑enabled after‑sales systems, such as over‑the‑air diagnostics, to support preventive maintenance. These systems can improve planning for spare‑parts inventory, service personnel allocation, and service appointment scheduling, enhancing overall service efficiency and customer satisfaction.

4. Business ecosystem development: To address economic (E) constraints from limited credit availability, social (S) constraints related to concerns over insufficient charging infrastructure, and technological (T) constraints stemming from limited driving range per charge, EV motorcycle manufacturers and distributors need to build partnerships and invest in a broader business ecosystem, as follows:

-

Electrical infrastructure: EV motorcycle manufacturers and distributors can form direct partnerships with battery‑swapping and charging station operators to develop electrical systems aligned with providers’ technical standards. In addition, partnerships with site‑based businesses, such as convenience stores and fuel stations, can support expanded nationwide infrastructure investment.

-

Finance and insurance: EV motorcycle manufacturers and distributors should collaborate with financial institutions to improve access to credit for EV motorcycle purchases, while working with insurance providers to design fair usage‑based premiums differentiated by driving behavior. Such premiums can be determined using data on riding behavior, location, and vehicle condition from onboard sensors.

5. Scaling sustainably: To mitigate environmental (E) constraints, manufacturers should adopt an upstream production planning approach, including sourcing recyclable and reuse‑friendly battery cells. They should also prioritize renewable‑energy‑based materials, particularly steel and aluminum, which account for around 10% of global greenhouse gas emissions. In addition, manufacturers should advance green manufacturing by expanding the use of clean energy—such as solar power systems—and improving machinery efficiency to reduce energy consumption, lower product carbon footprints, and strengthen consumer confidence amid rising environmental awareness.

In addition, relevant government authorities should play a more active role in easing domestic market constraints and supporting manufacturers’ export expansion through the following policy mechanisms:

-

Production support: To offset policy (P) constraints, the government should continue promoting the EV motorcycle manufacturing industry and stimulating domestic demand after the expiration of the EV 3.5 scheme through measures such as subsidies and tax incentives. Support should also extend to large‑sized EV motorcycles, which offer export growth potential given the limited global development of new models28/, covering both new EV manufacturers and established ICE big‑bike producers with the capability to transition into large‑sized EV motorcycle production for recreational riding markets.

-

Regulatory framework: To reduce legal (L) constraints, the government should revise regulations that hinder domestic market development, particularly by establishing common standards for electrical infrastructure providers and battery manufacturers29/. This would enhance interoperability among charging connectors, battery‑swapping systems, and batteries across brands, while reducing duplicative infrastructure investment costs. In addition, barriers to yellow‑plate registration for rider groups should be eased by allowing vehicle registration copies to be used for registering EV motorcycles under Category 17 under the Thai vehicle registration system.

-

Technology development: To address economic (E), social (S), technological (T), and legal (L) constraints, the government should promote research and development, particularly in battery technology and electrical infrastructure for EV motorcycles. Priority should be given to technologies that enable longer driving range, faster charging, lighter batteries that are easier to swap, and lower production costs. In parallel, the government should also support the development of software solutions that enhance riding performance.

Although Thailand’s electric motorcycle industry continues to face challenges, the country retains key structural strengths, notably a strong domestic manufacturing supply chain and a large domestic market. Accordingly, the private sector should focus on developing technologies tailored to specific consumer segments, while building trust through high‑quality after‑sales services. At the same time, the public sector should support relevant infrastructure development. Such public–private coordination will help transform constraints into opportunities and enable Thailand’s electric motorcycle industry to maintain its role in the global market over the long term.

References

Digital Trends. (June 26, 2024). "Used EV prices are falling quicker than those of gas cars, and that’s good". Retrieved from https://www.digitaltrends.com/cars/used-ev-prices-are-falling-quicker-than-those-of-gas-cars-and-thats-good/

ENTEC. (2023). "Battery Swapping Regulations and Standards in ASEAN". Retrieved from https://sustmob.org/EMOB/pdf/2_3WheelerConf/e2wBattSwapASEAN_Nuwong_30sep23.pdf

IEA. (2025). "Global EV Outlook 2025". Retrieved from https://iea.blob.core.windows.net/assets/7ea38b60-3033-42a6-9589-71134f4229f4/GlobalEVOutlook2025.pdf

Krungsri Research. (2025). "Industry Outlook 2025-2027: Motorcycle Industry". Retrieved from https://www.krungsri.com/getmedia/c88a0548-9308-4828-9c5a-0b8ea3a29e3f/IO_Motorcycle_250428_EN_EX.pdf.aspx

krungsri Research. (2025). "Industry Outlook 2026-2028: Electric Vehicle Industry". Retrieved from https://www.krungsri.com/getmedia/a116caed-ff69-4ad1-9937-c1bcfab15442/IO_BEV_251202_EN_EX.pdf?ext=.pdf

Krungsri Research. (2025). "Used Electric Vehicles: Supply and Resale Value". Retrieved from https://www.krungsri.com/getmedia/d02d56be-4e48-4ee6-943e-14c613c87360/RI_Used_BEVs_250127_EN_EX.pdf.aspx

McKinsey. (August 17, 2023). "The real global EV buzz comes on two wheels". Retrieved from https://www.mckinsey.com/industries/automotive-and-assembly/our-insights/the-real-global-ev-buzz-comes-on-two-wheels

Nikkei Asia. (January 10, 2026). "Honda to debut electric two-wheeler in Vietnam and Thailand". Retrieved from https://asia.nikkei.com/business/transportation/honda-to-debut-electric-two-wheeler-in-vietnam-and-thailand

UNDP. (2025). "Analysis of EV Battery End-of-Life". Retrieved from https://www.undp.org/sites/g/files/zskgke326/files/2025-01/analysis-of-ev-battery-end-of-life.pdf

ทีดีอาร์ไอ. (13 พฤศจิกายน 2568), "มอเตอร์ไซค์ไฟฟ้าไทย…ทำไมยังไม่เกิด?: ส่องช่องว่างตลาด โอกาสของผู้ประกอบการไทย". Retrieved from https://tdri.or.th/2025/11/thai-ev-motorcycles-market-gap-article/?

fbclid=IwY2xjawOHXY5leHRuA2FlbQIxMABicmlkETFpOFFkaVJVVlJ3eWFXZEpVc3J0YwZhcHBfaWQQMjIyMDM5MTc4ODIwMDg5MghjYWxsc2l0ZQEyAAEeOZ0U7Efk67HQuO66vryOW05AitUux15l7A9eNGMLDTWGPw1yXAILvjYxGZU_aem_yXadNVn1IXdGC6YYPHjIBA

ประชาชาติธุรกิจ. (17 พฤศจิกายน 2568). "ไรเดอร์เฮ ดีอี-ขนส่ง ปลดล็อกใช้สำเนาเล่มรถ จดทะเบียน รย.17-18". Retrieved from https://www.prachachat.net/ict/news-1921560

สมาคมยานยนต์ไฟฟ้าไทย (EVAT). (30 มิถุนายน 2568). "การเตรียมตัว เมื่อเกิดเหตุการณ์น้ำท่วมกับยานยนต์ไฟฟ้า". Retrieved from https://evat.or.th/ev-new/ev-technology/%E0%B8%81%E0%B8%B2%E0%B8%A3%E0%B9%80%E0%B8%95%E0%B8%A3%E0%B8%B5%E0%B8%A2%E0%B8%A1%E0%B8%95%E0%B8%B1%E0%B8%A7-%E0%B9%80%E0%B8%A1%E0%B8%B7%E0%B9%88%E0%B8%AD%E0%B9%80%E0%B8%81%E0%B8%B4%E0%B8%94%E0%B9%80/

Marketeer. (23 พฤษภาคม 2567). "วินฟาสต์ พับแผน ‘ขายรถ เช่าแบตฯ’ หันส่งอีโคคาร์ อีวี ประเดิมตลาดไทย". Retrieved from https://marketeeronline.co/archives/354479

1/ Additional details are available in Industry Outlook 2025-2027: Motorcycle Industry, page 4.

2/ Source: Federation of Thai Industries (FTI)

3/ Source: Department of Land Transport (DLT)

4/ Additional details are available in Industry Outlook 2025-2027: Motorcycle Industry, page 5.

5/ New electric motorcycle registrations totaled 23,971 units in 2025 (Source: Department of Land Transport: DLT).

6/ Electric motorcycle production totaled 6,012 units in 2025 (Source: Federation of Thai Industries: FTI).

7/ ICE motorcycle manufacturers can be categorized as follows: (i) 2 manufacturers focusing on small (commuter) motorcycles; (ii) 2 manufacturers producing both small (commuter) and large (sport) motorcycles; and (iii) 6 manufacturers focusing on large (sport) motorcycles.

8/ Additional details are available in Industry Outlook 2026-2028: Electric Vehicle Industry, page 5.

9/ Additional details are available in Industry Outlook 2026-2028: Electric Vehicle Industry, page 7 and 8.

10/ Source: IEA (2568)

11/ For example, (i) China’s electric motorcycle scrappage and replacement program, which has helped stimulate sales—particularly among urban users who may switch to electric motorcycles due to their lower cost and ability to access bicycle lanes or restricted areas where conventional motorcycles are not permitted; and (ii) India’s PM Electric Drive Revolution in Innovative Vehicle Enhancement (PM E-DRIVE) scheme, which provides subsidies of up to INR 5,000 per kWh for lithium-ion batteries, with a target to support sales of 2.5 million electric two-wheelers (Source: IEA (2025))

12/ Chinese manufacturers have increasingly sought growth opportunities overseas in recent years, driven by a maturing domestic market. For example, Yadea, China’s largest electric motorcycle producer, began construction of a new assembly plant in Indonesia valued at USD 150 million in 2024, with a planned production capacity of 3 million units by 2028.Meanwhile, other Chinese manufacturers have stepped up investments across Southeast Asia (including Vietnam, the Philippines, and Thailand), enabling them to emerge as some of the top five electric motorcycle brands in the region. (Source: IEA (2025))

13/ Source: DLT

14/ For example, used passenger BEVs sold in Thailand experience an initial depreciation of around -22.9% after first sale. Thereafter, prices decline further by approximately -5.6% to -9.4% per kilometer driven, a steeper rate than the global average for used vehicles, which falls by around -5.2% over the same distance (see Used Electric Vehicles: Supply and Resale Value for more details).

15/ Further details can be found in Digital Trends (June 24, 2024) and Used Electric Vehicles: Supply and Resale Value.

16/ During 2021–2025, cumulative registrations of used electric motorcycles totaled 289 units, compared with 845,628 units for all used motorcycles (Source: DLT).

17/ Source: TDRI (November 18, 2025)

18/ For example, VinFast previously introduced its 100% electric vehicle model, the VinFast VF e34, at the 2024 Motor Show, adopting a business model that separated the battery from the vehicle and required customers to lease the battery on a monthly basis. However, Thai consumers remained unfamiliar with this model, prompting VinFast to subsequently revise its strategy by shifting to a bundled sales approach that includes the battery with the vehicle (Source: Marketeer (May 23, 2024)).

19/ The top 3 electric motorcycle models by new registrations in 2025 were (i) Deco Hannah (2,747 units), offering a range of 60 kilometers per charge; (ii) EM Legend (2,455 units), with a range of 80 kilometers per charge; and (iii) Lion SKS Z2 (1,837 units), with a range of 70 kilometers per charge (Source: DLT; compiled by Krungsri Research).

20/ Average Weight of 150–170 kWh Batteries (Source: ENTEC (2023))

21/ Source: UNDP (2025)

22/ Source: EVAT (June 30, 2025)

23/ Vietnam plans to restrict the use of ICE motorcycles in certain areas of Hanoi starting in July 2026 to improve air quality. The report notes that following the announcement of this plan, some consumers began postponing purchases of ICE motorcycles, while others started shifting toward electric motorcycles instead (Source: Nikkei Asia (January 10, 2026))

24/ Source: Prachachat Business (November 17, 2025)

25/ Business strategies for the Thai context, drawing on McKinsey’s (2023) study “The 7 Key Factors for Winning in the 2‑Wheeler Electric‑Vehicle Market,” categorize strategies into core business drivers—namely Know the Market, Control Costs, Be Present, Make EV Ownership Easy, and Lead the Charge (data‑ and software‑driven leadership)—and enabling strategies, comprising Scale Sustainably and Create Supportive Policies.

26/ For example, ensuring clean manufacturing processes and reducing the risk of electrical short circuits.

27/ Vertical integration can reduce battery assembly costs by approximately 12–17% (Source: McKinsey (2023)).

28/ This is because Chinese manufacturers, which account for the largest share of global electric motorcycle production, continue to focus primarily on producing small-sized, low-speed models for their domestic market (Source: TDRI (November 18, 2025)).

29/ For example, standards for battery safety, electrical interfaces, and communication protocols between batteries, vehicles, and swapping stations.