Introduction

The data center industry serves as a critical digital infrastructure for the global economy, supporting a diverse range of activities such as e-commerce, digital finance, streaming, artificial intelligence, and government data management. As these activities rely on the processing of massive volumes of data, the capacity to efficiently store, process, and interconnect massive amount of information is a key indicator of a nation's long-term competitive potential.

The ASEAN region is currently attracting global investors, particularly in digital infrastructure, driven by a large potential user from population of over 695 million people and a rapidly growing digital economy. While Singapore previously served as the region's primary data center hub, it now faces increasing resource constraints and tighter regulations. Consequently, investors are shifting their focus toward other countries such as Malaysia, Indonesia, Vietnam, and Thailand, all of which possess the potential to host data center investments. ASEAN is thus undergoing a transformative leap from an emerging market to a strategic investment base for digital infrastructure.

This analysis aims to examine the competitiveness of the Thai data center industry within ASEAN by comparing the strengths, weaknesses, opportunities, and challenges of each country. The objective is to provide policy and strategic insights for stakeholders at both the regional and global levels.

Global data center industry overview and trends

Data centers are facilities or infrastructure used for the storage, processing, and transmission of digital data. Currently, there are more than 12,002 data centers globally, with nearly half of those number in the United States—the central hub for leading global cloud service providers—hosting 5,427 facilities. This is followed by European nations such as Germany (529 facilities) and the United Kingdom (523 facilities), while data centers in the Asia-Pacific region are concentrated in China (449 facilities), Australia (314 facilities), and Japan (222 facilities)

1/.

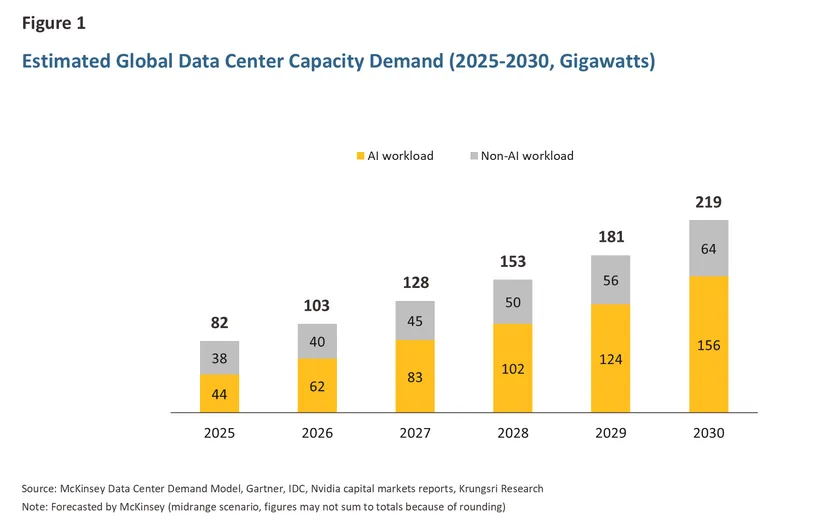

In 2025, the global data center industry is projected to be valued at USD 527.5bn and is expected to grow to USD 739.1bn by 2030, representing an annual growth rate of 7.0% (CAGR)2/. Furthermore, as the data center industry is highly energy-intensive, power demand is anticipated to experience exponential growth, rising from 82 gigawatts in 2025 to 219 gigawatts by 2030, or a significant growth of 21.7% CAGR. Specifically, energy demand driven by AI usage is projected to grow by as much as 28.8% CAGR

3/ (Figure 1).

The primary factors driving the significant expansion of the data center industry in recent periods, which are expected to provide continuous momentum, include:

-

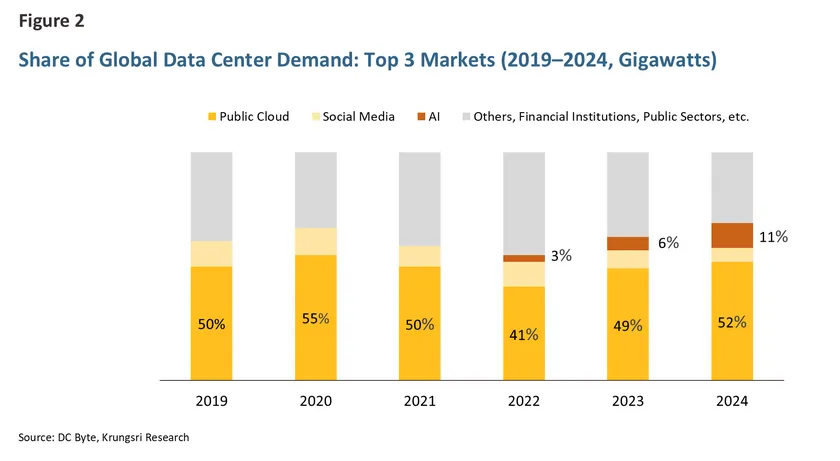

The public and private sectors are increasingly adopting cloud systems and migrating their operations to cloud platforms. This trend is evidenced by the fact that more than half of global data center energy consumption provides Public Cloud services4/ (Figure 2). Key advantages of using cloud services include reduced operating costs and enhanced data security, which are critical factors in an era where the concept of data sovereignty is gaining increased attention.

-

The development and application of Artificial Intelligence (AI) is considered one of the most significant drivers for the data center industry today. Because AI requires massive processing power, it necessitates modern infrastructure that differs from traditional data centers, particularly in term of high energy consumption and the need for large numbers of GPUs working in tandem. Data centers supporting AI processing show a significantly higher growth trend compared to general-purpose data centers (Figure 1), consistent with the steadily increasing proportion of data center energy consumption dedicated to AI processing (Figure 2).

-

The rising popularity of the Internet of Things (IoT), which serves as a source of massive amount of data, has increase the need of data centers to store and analyze this information. This stems from the rapid increase in connected devices, such as factory machinery, various home sensors, vehicles, and surveillance cameras. Much of this data requires processing near its source (edge computing) to reduce latency, resulting in a demand for distributed, smaller-scale data centers to support services closer to users.

-

The digital economy is growing rapidly, reflected through online transactions, digital payments, and the continuous increase in social media usage. This results in a vast amount of digital data being created and transmitted daily, causing data traffic to increase exponentially. In recent years, volume has increased immensely; in 2020, approximately 129 zettabytes5/ of data were created globally. This represents a leap compared to 2010, when global data totaled only 2 zettabytes, reflecting growth of over 64 times in just 13 years. In the future, it is expected that the total volume of data created, stored, and consumed worldwide will continue to grow and exceed 290 zettabytes by 2027 (IDC 2023). This exponential growth of digital data is directly driving the rapidly increasing demand for data center construction and investment to accommodate the continuous expansion of storage and processing needs.

The ASEAN data center industry

The data center industry in ASEAN is significantly attracting attention from global investors and leading companies, as it is a region with high growth potential. Its economic size was approximately USD 4.0tn in 2024, ranking 5th in the world, with a combined population of over 695 million, reflecting a large consumer market with a strong future growth trend. Furthermore, the ASEAN digital economy in 2025 has a gross merchandise value of USD 185bn and is expected to grow at a compound annual rate of 14.2% until reaching USD 359bn in 2030. These increasing digital transactions, whether through e-commerce platforms, cloud services, or various online applications, all require large-scale data storage and processing, driving up the demand for data center infrastructure in this region.

The ASEAN data center industry has a total value of approximately USD 14.07bn in 2025 and is projected to grow to USD 19.46bn in 2030, representing a compound annual growth rate (CAGR) of 6.7%6/. Meanwhile, the region's artificial intelligence market is expected to be valued at USD 65bn by 2035, and AI adoption is anticipated to boost ASEAN GDP by as much as USD 1.0tn by 2030

7/.

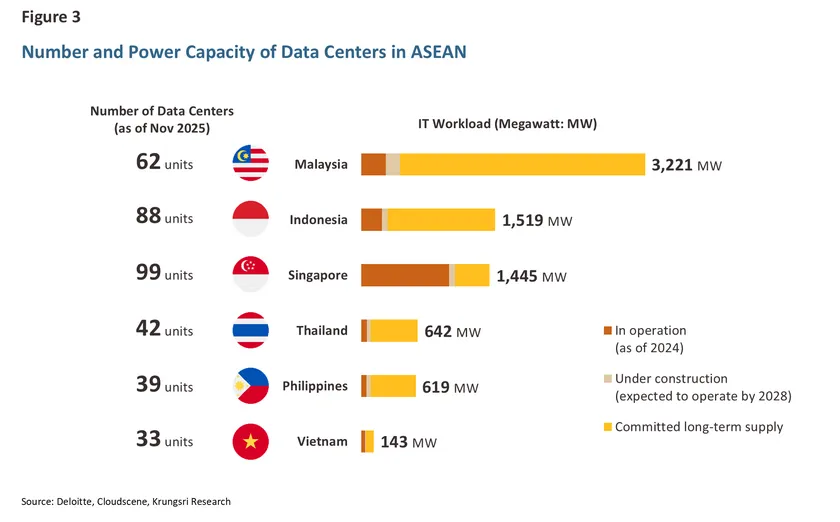

Currently, there are 377 data centers8/ in the ASEAN region, distributed across several countries, particularly Singapore (99 facilities), Indonesia (88 facilities), and Malaysia (62 facilities), while Thailand, the Philippines, and Vietnam are accelerating their development in this industry.

Regarding power capacity, operational data centers in ASEAN in 2024 consume 1.68 gigawatts, while those under construction and scheduled for completion by 2028 are projected to require an additional 0.4 gigawatts. Meanwhile, planned data center projects could bring power consumption as high as 5.51 gigawatts (Figure 3).

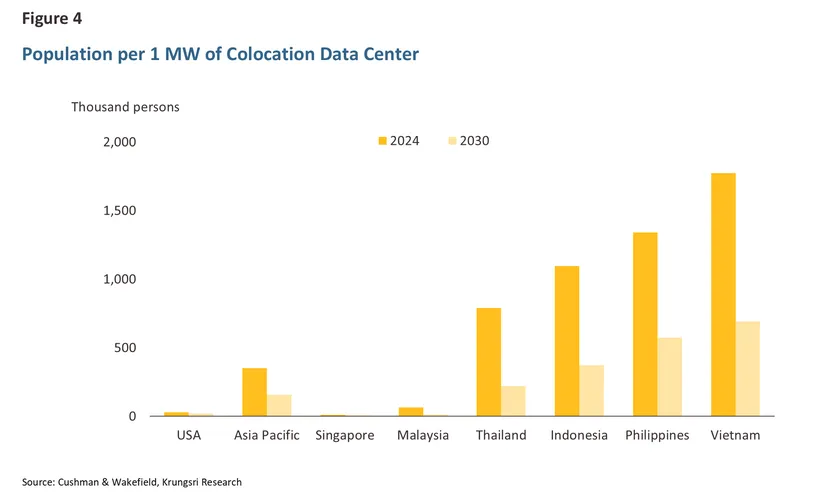

When considering the population per colocation megawatt (Population per Colo Megawatt), which serves as an indicator reflecting the adequacy of data center infrastructure relative to population size (Figure 4), it is found that ASEAN countries, including Indonesia, Thailand, Vietnam, and the Philippines, remain significantly below the Asia-Pacific average and well below developed nations like the United States. This reflects that the data center infrastructure in these countries has not yet reached saturation and has not entered a state of oversupply. Even by 2030, despite the expectation of continuous increases in data center investment, these population per colocation megawatt numbers are projected to remain at high levels. This indicates that the growth of the digital economy in ASEAN is expanding faster than the data center infrastructure, leaving room for additional investment in the medium to long term.

Historically, Singapore served as the primary data center hub of the region due to its robust infrastructure, particularly its highly stable power supply and strong telecommunications systems, as well as its strength in international internet connectivity. However, Singapore faces resource constraints, as data centers require immense amounts of electricity and water to cool servers. Consequently, the Singaporean government implemented measures to manage these resources, including a moratorium on new data center approvals between 2019 and 2022, and requirements for new projects to meet high energy efficiency standards while increasing the proportion of renewable energy use. Although these measures promote sustainability, they have led some investors to increasingly consider alternatives in neighboring countries9/. This has resulted in the regional dispersion of the data center industry into Malaysia, Indonesia, Vietnam, and Thailand. These countries offer several advantages, including lower land and energy costs, supportive government policies, and rapidly growing domestic digital markets. In particular, Johor in Malaysia and Batam in Indonesia have attracted significant interest due to their proximity to Singapore, enabling efficient connectivity to existing infrastructure via direct subsea cables. Furthermore, both cities have developed Special Economic Zones to support direct investment, making them the region's new data center investment hotspots. This is reflected in the power capacity of data centers in Johor, which increased by over 260.0% CAGR during 2019-2024, while Batam saw an increase of over 145.0% CAGR during the same period.

Analyzing the competitiveness of the data center industry in each country

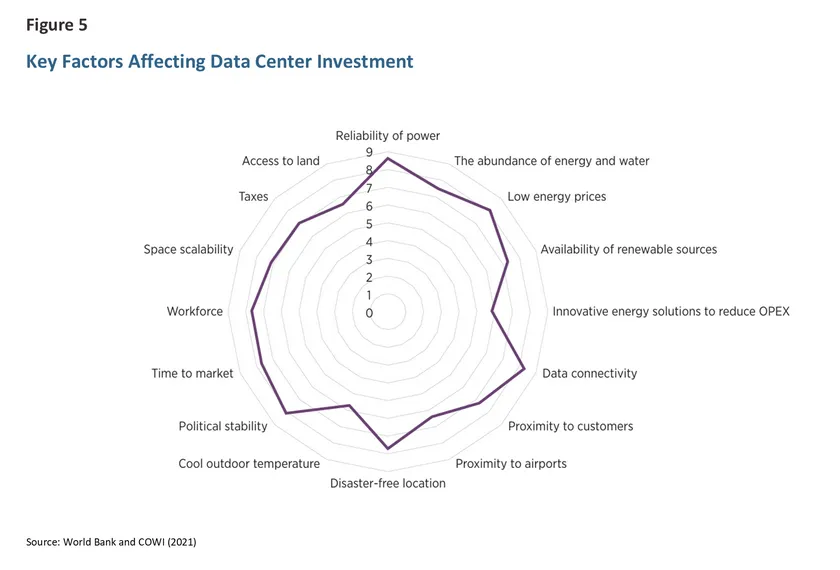

We can analyze the competitiveness of ASEAN member states in the data center industry by considering key factors influencing investment decisions. This analysis is based on the World Bank’s report

10/, "Advancing Cloud and Data Infrastructure Markets: Strategic Directions for Low- and Middle-Income Countries" (Figure 5), in conjunction with Krungsri Research's analysis. The key factors can be categorized into five pillars: (1) power system stability, (2) data connectivity, (3) natural disaster risk, (4) labor market, and (5) political stability. This study covers the ASEAN-5 countries—Indonesia, Malaysia, Thailand, the Philippines, and Vietnam—excluding Singapore, as it is already the region's established data center hub but faces land and power constraints. Therefore, the analysis focuses on identifying which country among the ASEAN-5 holds the highest potential to attract investment, while highlighting Thailand's strengths and weaknesses across various dimensions.

1. Power Infrastructure

The stability of the electrical system is the most critical factor, as data centers rely on a continuous power supply. Any power system failure could result in significant economic costs and long-term erosion of user confidence.

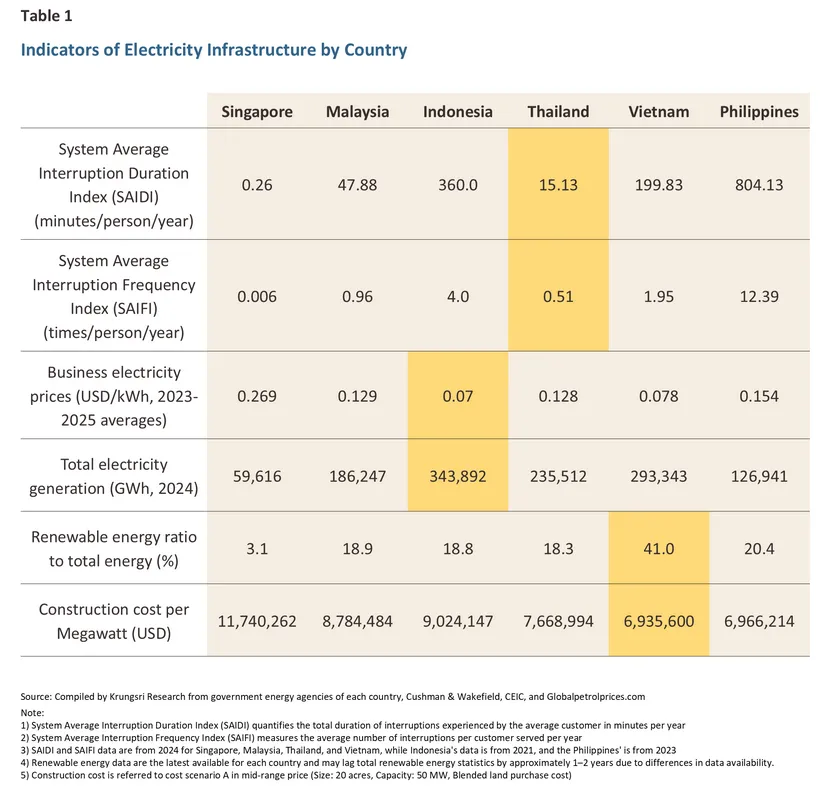

Thailand is considered to have the most stable electrical system, reflected by its SAIDI (System Average Interruption Duration Index), which measures the average duration of power interruptions per person per year, and SAIFI (System Average Interruption Frequency Index), which measures the average frequency of power interruptions per person per year. These indicators are at the lowest levels compared to other 4 countries. Meanwhile, electricity prices and construction costs remain competitive, with construction costs being lower than those in Malaysia. However, the proportion of electricity generation from renewable energy relative to total capacity remains low compared to some other nations.

Malaysia possesses a power system with stability levels close to Thailand’s, though slightly trailing. It maintains competitive electricity prices and construction costs, with these costs being lower than those in Indonesia, and features a better renewable energy generation proportion than Thailand. Nevertheless, when compared to other countries in the region, this proportion remains at a moderate level.

Indonesia offers low electricity prices and has the highest total power generation capacity. However, construction costs are high, and the stability of the power system remains low, which may serve as a constraint for data center investments that primarily prioritize energy security.

Vietnam is notable for its high proportion of renewable energy generation, coupled with low electricity prices and construction costs. Although its power system stability is not yet high, it outperforms Indonesia and the Philippines. The strength in renewable energy enhances its potential to attract investment from data center operators who prioritize sustainability issues.

The Philippines is at a disadvantage across almost every dimension compared to other countries, particularly regarding power system stability, which is at the lowest level compared to other 4 countries. Although it offers low construction costs and has a higher proportion of renewable energy than Malaysia, Indonesia, and Thailand, its actual power generation volume is considered the lowest among all studied countries.

2. Data Connectivity

Data connectivity acts as the backbone of digital infrastructure, enabling the transmission of vast amounts of data and ensuring rapid, seamless access to cloud systems. For this pillar, we consider infrastructure readiness, ranging from subsea cables for international connectivity to domestic broadband systems.

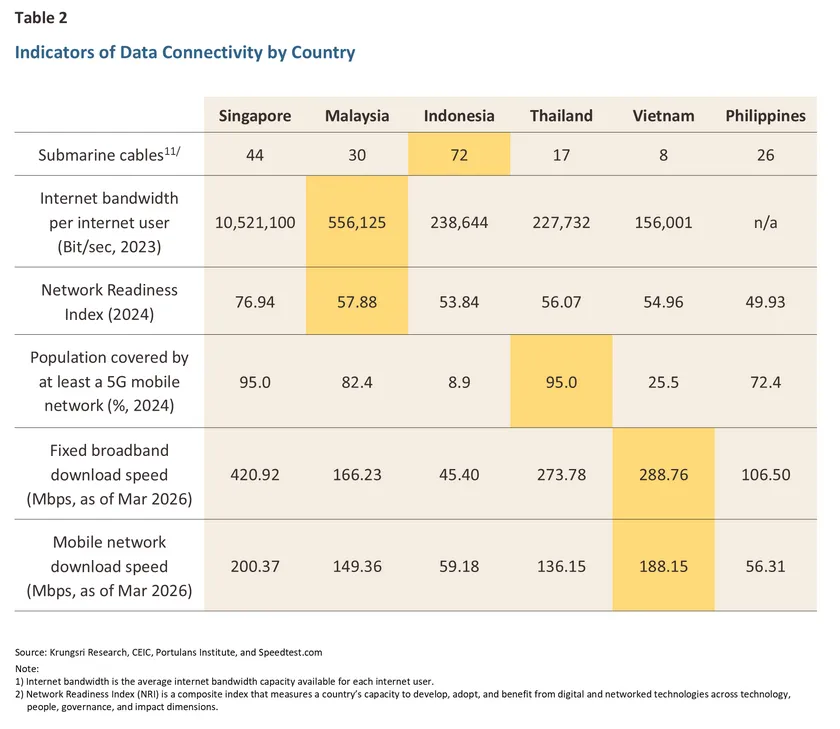

Thailand excels in domestic networking, with a proportion of the population accessing 5G networks at the highest level alongside Singapore, reflecting readiness for advanced digital services. Furthermore, broadband and mobile internet speeds are high and competitive. However, the number of international subsea cable connections remains limited compared to Indonesia and Malaysia, which may pose constraints regarding the diversity of international connection routes.

Malaysia possesses strengths in overall network quality, as reflected by its relatively high Network Readiness Index, compared to regional peers, and this is coupled with a high volume of internet usage per user. Although its 5G network coverage trails behind Thailand and its number of subsea cables is lower than Indonesia's, Malaysia maintains an advantage in terms of the convenience and low cost of connecting to Singapore.

Indonesia holds an advantage in international connectivity, possessing the highest number of subsea cables. This is partly due to its archipelagic geography, which necessitates inter-island connections. However, its domestic infrastructure remains limited in terms of internet speed and 5G network coverage, which is still at a very low level. Additionally, a low Network Readiness Index poses challenges for supporting data centers that require high-quality connectivity.

Vietnam is notable for its domestic internet speeds, both in broadband and mobile networks. However, the number of subsea cables remains low, and 5G network coverage is limited, which may serve as an obstacle to developing into a data center hub that relies heavily on high-level international connectivity.

The Philippines has limited competitiveness despite having a moderate number of subsea cables, consistent with its archipelagic geography that facilitates international connections. Nevertheless, both broadband and mobile internet speeds remain low. Combined with the lowest Network Readiness Index among the group, its potential to support large-scale data centers remains relatively restricted.

3. Geographic Conditions

Geographic location is a fundamental factor that directly impacts the physical risks of data centers, including natural disasters, the frequency of extreme events, and the ability to diversify spatial risks. Selecting a low-risk location helps reduce operational costs and the risk of service interruptions.

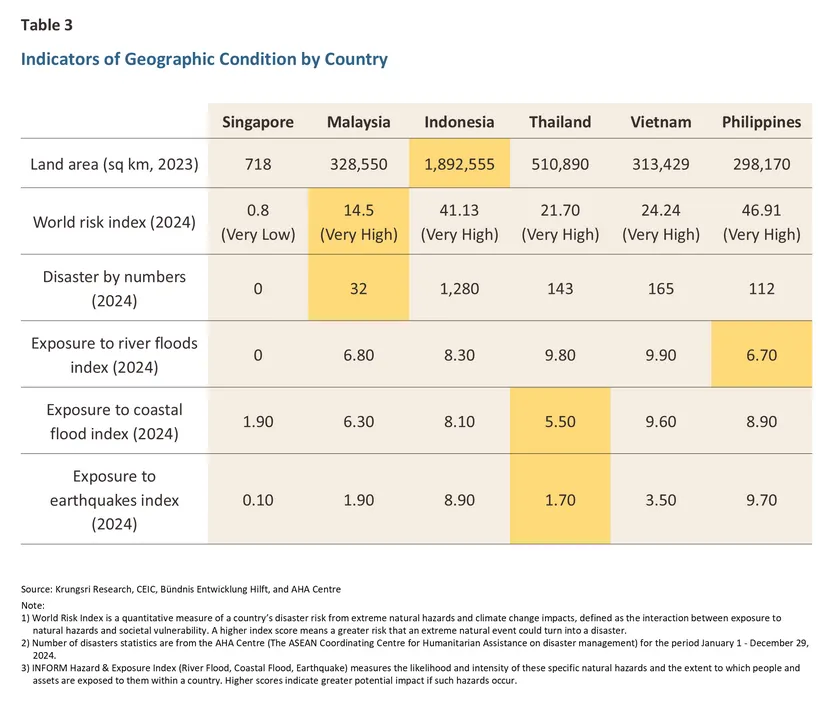

Thailand possesses a geographic advantage due to its central location within ASEAN and its low level of seismic risk. Although it faces high risks of riverine flooding and has a relatively high World Risk Index score, this score remains lower than that of many other ASEAN countries. Additionally, the overall number of disasters remains limited compared to regional peers, giving Thailand the potential to serve as a site for data centers requiring long-term physical stability.

Malaysia is notable for its relatively low overall risk level, as reflected by a relatively low World Risk Index score compared to other ASEAN countries and a very low frequency of actual disasters. Furthermore, risks from earthquakes and coastal flooding are also comparatively low, making its locations high-potential sites for long-term data center investment.

Indonesia faces significant geographic constraints. Although its large landmass facilitates the distribution of data center locations, its position along the Ring of Fire results in high levels of seismic and other disaster risks. This is reflected in a very high World Risk Index score and a high number of disaster events compared to other countries in the group. Such risks may increase infrastructure costs and investment risk management for data centers.

Vietnam faces high risks of both riverine and coastal flooding, consistent with its long coastline and extensive low-lying areas. While its seismic risk is at a moderate level, the overall number of disasters remains relatively high. Consequently, data center site selection must be conducted meticulously, which may increase risk-mitigation costs.

The Philippines faces the greatest geographic challenges in the group, having the highest World Risk Index score and high risks of both earthquakes and coastal flooding. Combined with a high annual frequency of disaster events and an archipelagic geography that adds complexity to risk diversification and infrastructure connectivity, its attractiveness for data center investment from a geographic perspective is relatively limited.

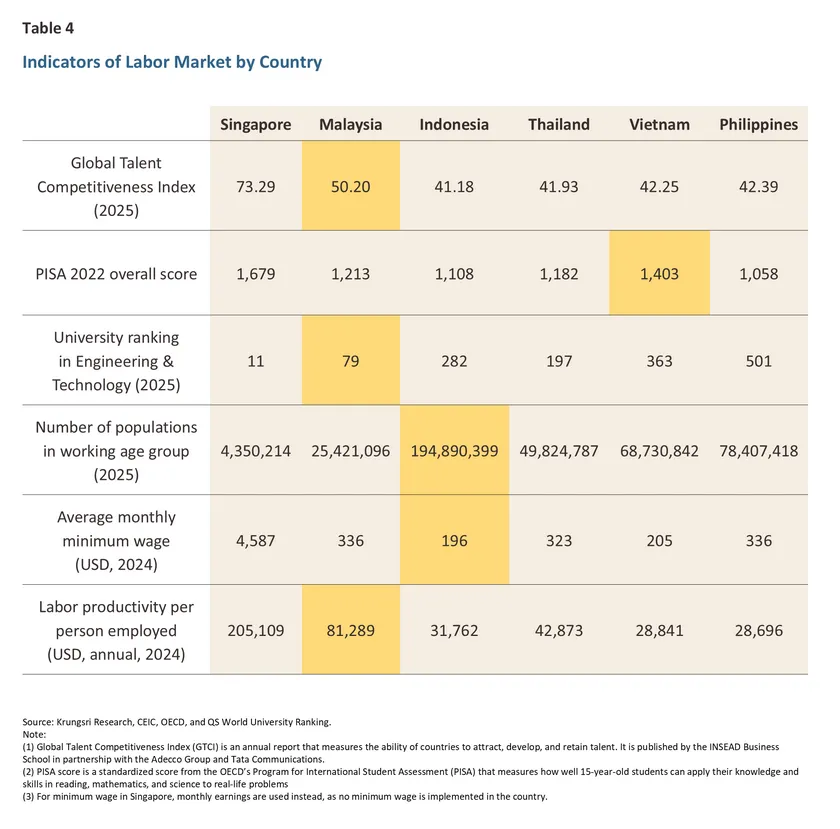

4. Labor Market

The labor market is one of the strategic factors determining a country's competitiveness in attracting data center investment. As this industry relies heavily on high-skilled labor, workforce quality, labor costs, and the size of the talent labor pool are essential components of the investment decision-making process.

Thailand maintains a moderate level of competitiveness, with its Global Talent Competitiveness Index (GTCI) and labor productivity ranking among the top in the group. However, there are constraints regarding the foundational skills of the future workforce, as reflected in PISA (Program for International Student Assessment) scores—which measure international learning quality and analytical potential—trailing behind Vietnam and Malaysia. Nevertheless, its engineering and technology university ranking of 197 out of 551 institutions in the world remains a strong foundation for producing supporting personnel, outperforming Indonesia, Vietnam, and the Philippines.

Malaysia possesses a structural advantage in labor quality compared to its peers, as reflected by a high GTCI score coupled with favorable university rankings in engineering and technology. While its labor productivity per person is the highest in the group, labor costs remain at a competitive level. This provides Malaysia with a balance between labor quality and cost, facilitating data center investments that require high-skilled personnel.

Indonesia holds an advantage in having the largest labor pool in the region, which facilitates large-scale recruitment, combined with the lowest labor costs in the group. However, labor quality remains a significant constraint, as evidenced by low GTCI and PISA scores, as well as lower labor productivity per person compared to other nations in the group. Consequently, data center investments requiring high-skilled labor may necessitate additional human resource development.

Vietnam is notable for its labor skills, achieving the highest PISA scores in the group and a GTCI higher than those of Thailand and Indonesia, reflecting improving population quality. Combined with advantageous minimum wage levels that help reduce operating costs, it still faces constraints such as low labor productivity and technology university rankings that remain lower than those of Thailand and Indonesia.

The Philippines has a relatively large labor market and low labor costs. However, overall labor quality indicators remain low across PISA scores, university rankings, and labor productivity per person. As a result, its potential to support data centers requiring advanced engineering and technological personnel remains relatively limited.

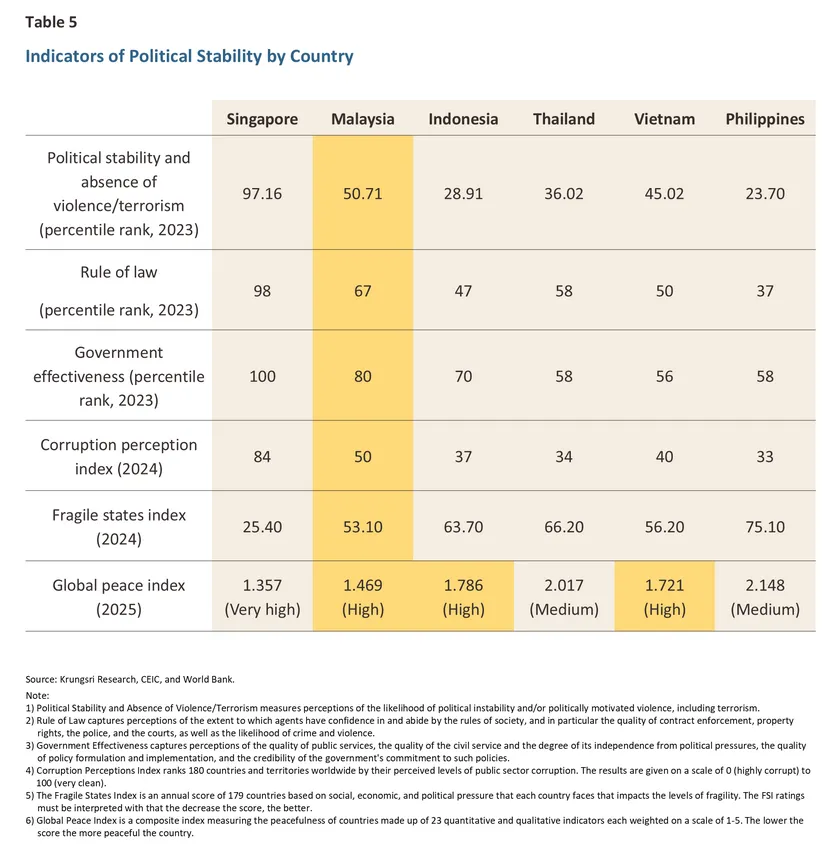

5. Political Stability

Political stability and government administrative efficiency are crucial factors for investment decisions in the data center industry, which involves large-scale, capital-intensive projects with long payback periods. Consequently, an efficient government, policy continuity, and clear legal enforcement are essential for reducing uncertainty and long-term investment risk costs.

Thailand possesses a moderate level of competitiveness, with strengths in legal enforcement and government efficiency that outperform Indonesia and Vietnam. However, significant weaknesses are reflected in its political stability and corruption indices, as well as a State Fragility Index that is higher than those of Malaysia and Vietnam. These factors may impact the continuity of government policies aimed at supporting the industry across various sectors.

Malaysia exhibits the highest competitiveness in the group, with outstanding scores across all governance dimensions. Its legal enforcement and government efficiency indices are conducive to long-term investment. Furthermore, it possesses the best corruption and state fragility indices in the group, helping to reduce structural risks and build greater confidence for long-term business operations compared to its peers.

Indonesia faces challenges stemming from relatively low political stability and legal enforcement. While its government efficiency index is at a relatively high level—indicating efforts to drive economic policies—the high level of corruption and a State Fragility Index that trails behind Malaysia and Vietnam present overall challenges to the investment climate.

Vietnam is notable for its domestic stability and order, consistent with a State Fragility Index that is the second lowest after Malaysia. This helps reduce structural risks and creates an environment conducive to investment. However, constraints remain regarding transparency due to corruption and the effectiveness of legal enforcement.

The Philippines is the least attractive in the group according to most indicators regarding governance dimensions. It faces the greatest challenges in the State Fragility Index and has the highest risk of violence and terrorism. Additionally, it records the lowest scores for corruption and legal enforcement in the group, which may serve as significant challenging factors for data center industry investment.

Investment promotion and sustainability policies of each country

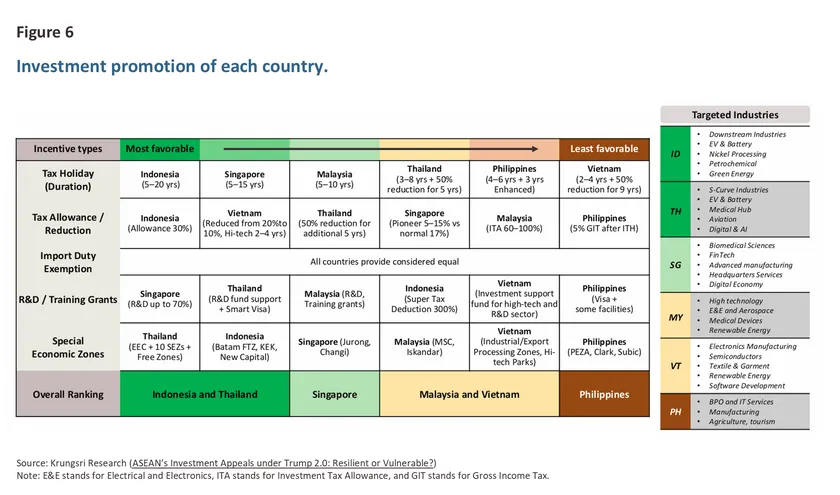

Government policies for investment promotion are another critical factor. However, if a country relies solely on attractive investment incentives while lacking infrastructure readiness, it may fail to attract investment in the data center industry—an industry characterized by high capital expenditure that requires comprehensive consideration. The summary and analysis of investment promotion policies are as follows

12/:

1) Investment Promotion Policies

When considering the factors attracting data center investment, Indonesia, Thailand, and Singapore are classified as the group with the highest investment incentive measures in ASEAN, as follows:

Indonesia offers competitive tax benefits, featuring corporate income tax exemption periods and deduction rates that surpass those of regional peers. A notable Special Economic Zone that successfully attracts data center investment is Nongsa Digital Park (NDP) on Batam Island, located near Singapore. The development of high-performance networks and subsea cable systems—both operational and under development—enables it to effectively accommodate demand spillover from Singapore.

Thailand, while not as prominent in tax incentives as Indonesia, offers greater diversity and comprehensiveness. Specifically, it defines incentive measures linked to strategic areas and various Special Economic Zones, which align with the needs of target industries. These include support for R&D and digital labor development, along with the role of numerous Special Economic Zones that help reduce costs and increase flexibility in site selection. The government is also driving the digital industry under the Thailand 4.0 policy and the Cloud First policy, which promotes the migration of government systems to the cloud to generate domestic demand.

Singapore, despite not having the highest level of tax benefits, remains attractive for data center investments focused on high value-added services and regional operations. It emphasizes strong support for R&D and a robust digital ecosystem. However, policy requirements, sustainability conditions, and power constraints are becoming factors hindering large-scale expansion, making tax advantages secondary compared to other nations. Nevertheless, a market like Singapore remains vital for regional connectivity, shifting its role toward becoming 'Control Towers'—serving as an anchor for the regional ecosystem while pushing for quantity-based expansion into neighboring markets instead.

Malaysia and Vietnam are in the group with moderate competitiveness. Although their tax durations and conditions are less favorable to those of the first group, they offer additional benefits for target industries. Malaysia offers the Digital Ecosystem Acceleration Scheme (DESAC), granting tax incentives to digital infrastructure providers, as well as the Johor-Singapore Special Economic Zone (JS-SEZ), which is well-equipped to absorb spillover from Singapore due to its proximity, similar to Indonesia's Nongsa Digital Park. It also grants special tax rates for industries related to the AI supply chain and quantum computing.

The Philippines has relatively limited competitiveness regarding data center related incentives. Its tax measures remain narrow in scope and are primarily focused on attracting investment in the service sector. Despite having Special Economic Zones and regulatory facilitation, these measures have yet to sufficiently compensate for the limited tax benefits for projects requiring high capital investment and long payback periods.

2) Sustainability policies related to data centers

When considering the sustainability policies and renewable energy access of various ASEAN countries, the findings are as follows:

Thailand has implemented industry-upgrade measures (Smart and Sustainable Industry), offering additional corporate income tax exemptions of up to 100% of the investment value for 3 years to facilitate machinery upgrades that improves energy efficiency, promote renewable energy usage, or incorporate energy storage systems. Furthermore, the country is currently developing and piloting the Direct Power Purchase Agreement (DPPA) scheme. Currently, a pilot phase has commenced for the Utility Green Tariff (UGT) covering 2,000 megawatts, while the Third Party Access (TPA) framework is in the legislative drafting stage. Although there is a push for Green Data Center policies, specific promotional policies or measures have not yet been formally established.

Singapore has implemented the Green Data Centre Standard through the SS 564 and BCA-IMDA Green Mark standards, which focus on measuring Power Usage Effectiveness (PUE) and Water Usage Effectiveness (WUE). It is also upgrading to the Tropical Data Centre standard (SS 697) to enhance cooling efficiency in hot and humid climates in alignment with global standards. Additionally, the DC-CFA (Data Centre - Call for Application) process serves to select new data center providers that prioritize clean energy innovation and grid flexibility. This is complemented by financial support measures for projects aimed at carbon reduction and improving energy efficiency. While Singapore does not have a DPPA system, it utilizes a Virtual PPA system that allows for corporate PPAs in the form of commercial or financial contracts through Renewable Energy Certificates (RECs).

Malaysia offers GITA (Green Investment Tax Allowance) and GITE (Green Investment Tax Exemption) for activities related to green technology and renewable energy usage. Furthermore, it has implemented the Corporate Renewable Energy Supply Scheme (CRESS), a mechanism designed to support DPPA by allowing clean energy buyers and sellers to negotiate prices directly and transmit electricity through the national grid. Malaysia also addresses the green data center sector through its Guideline for Sustainable Development of Data Centers (2024).

Vietnam has implemented government policy Decree 58/2025/ND-CP, which enhances confidence in credit access via power purchase guarantees. Under this decree, the state guarantees the purchase of at least 80% of clean electricity, facilitating easier bank loan approvals for renewable energy projects supplying data centers. Additionally, it supports green data centers through the Master Plan for Digital Infrastructure 2021-2030 and has officially approved and enforced a DPPA mechanism. The government has issued regulations allowing large-scale electricity consumers to purchase renewable energy directly from producers via the state grid or private networks, including Virtual PPA options.

Indonesia currently lacks a DPPA system. Despite having national policy goals, it continues to face challenges regarding a closed electricity market, which prevents systematic direct access to renewable energy. There is also a lack of regulatory incentives to attract private sector clean energy investment. While there is a push for green data center policies, specific promotional measures have not yet been established. However, Indonesia does provide investment incentives for projects related to clean energy.

The Philippines utilizes the Green Energy Auction Program (GEAP), through which the government auctions clean energy to drive down prices. It has also introduced regulatory change allowing 100% foreign ownership in renewable energy projects. Although there is no specific green data center policy, the Green Lane measure has been implemented to expedite licensing for data center projects utilizing clean energy. While a formal DPPA policy is absent, the Green Energy Option Program (GEOP) functions similarly by allowing consumers with a demand of at least 100 kW to choose and purchase electricity directly from renewable energy producers.

Where does Thailand stand? Summarizing Thailand's competitiveness through SWOT Analysis

Based on the aforementioned factors, we can summarize Thailand's competitiveness through an analysis of Strengths, Weaknesses, Opportunities, and Threats (SWOT Analysis) as follows:

Strength

-

Power system stability: Thailand possesses a stable electrical energy infrastructure, which is the primary priority in data center investment decisions.

-

Competitive total costs: Whether regarding electricity costs, construction costs, or labor costs, Thailand remains competitive. Although costs may be higher than those in the Philippines, Indonesia, or Vietnam, the overall quality makes investing in Thailand a high-value proposition.

-

Strong domestic digital network: Thailand has the highest 5G access rate in ASEAN, a favorable Network Readiness Index, and top-tier internet speeds. This efficiently facilitates the future expansion of services such as AI, IoT, and Cloud.

-

Manageable geographic risk: Overall geographic risks are at a manageable level, with low seismic risk. While riverine flooding risk is high, it remains within a manageable range.

Weakness

-

Low proportion of renewable energy: Compared to competitors like Vietnam, Thailand may be at a disadvantage if investors prioritize strict renewable energy conditions.

-

Limited subsea cable connections: This may reflect restricted international connectivity, potentially resulting in higher latency for data transmission.

-

Labor quality challenges: Competitiveness scores regarding various labor dimensions remain lower than several competitors. Furthermore, relative labor costs are considered high, and the labor pool is smaller.

-

Inconsistent political stability: Specifically, its scores for political stability and corruption trail behind Malaysia and Vietnam, reflecting a need for improvement in government policy continuity.

Opportunity

-

Positioning as ASEAN’s Secondary Hub: Thailand can position itself as a supplementary hub to Singapore, offering lower costs while providing similar infrastructure quality.

-

Accelerating renewable energy and Green Data Center policies: If the government can concretely drive these ESG related policies, it will help Thailand address ESG weaknesses rapidly and gain prominence.

-

Geopolitical risk diversification: Amidst the "China+1" trend and global supply chain realignments, global technology companies and investors view neutral countries like Thailand as high-potential destinations for increased investment.

-

Specialized labor skill upgrades: Opportunities to reskill or upskill specifically for the data center and AI industries can rapidly enhance capabilities, allowing Thailand to compete effectively with Vietnam and Indonesia.

Threat

-

Competition from Malaysia: Malaysia holds advantages over Thailand in terms of renewable energy proportions, political stability, and connectivity with Singapore. Additionally, it serves as a production base for upstream products like semiconductors.

-

Long-term structural advantages of competitors: Countries like Indonesia possess large markets and a massive workforce. If Indonesia successfully develops its infrastructure, labor skills, sustainability policies, subsea cable count, and Singapore connectivity, it will become a formidable competitor.

-

Net zero Vietnam’s ESG prominence: Due to its high proportion of renewable energy, Vietnam may become the primary choice for data center investments that must comply with Net Zero goals.

-

Escalating climate risks: Particularly the risks of flooding and extreme climate change, which may increase costs and challenges for long-term infrastructure design.

Krungsri Research View

The data center industry in Thailand possesses significant strengths derived from power system stability and a robust domestic digital network. Meanwhile, total costs—including electricity, construction, and labor wages—remain at a competitive level. However, Thailand still faces a critical constraint regarding the low proportion of renewable energy usage, which may pose as an obstacle to attracting investors with Net Zero targets. Furthermore, the limited number of subsea cables and challenges concerning high-skilled labor quality are factors that may undermine long-term competitiveness.

To enhance its attractiveness, Thailand must urgently take action in three primary areas:

-

Clean Energy: Expedite the implementation of Direct Power Purchase Agreement (DPPA) policies and the Utility Green Tariff (UGT) structure to become fully operational in practice, meeting the demand for Green Data Centers.

-

Connectivity Infrastructure: Promote additional investment in international subsea cables to reduce latency and increase the diversity of data connection routes.

-

Human Resources: Accelerate reskilling and upskilling policies for the workforce, particularly in specialized skills related to AI and technological engineering, to accommodate the demands of advanced digital industries.

However, many parties remain concerned that data center investment may generate limited economic value added. In the initial phase, the primary benefits often concentrate in the construction sector for a short duration. In the long term, direct employment tends to be low, as this industry focuses on a small number of high-skilled personnel. Additionally, most equipment is imported, resulting in relatively limited benefits for the domestic upstream and downstream value chains. These issues require clear answer if the government intends to position Thailand as ASEAN’s Secondary Hub to accommodate demand spillover from Singapore.

If Thailand can find these answers and overcome the aforementioned obstacles, this industry will not only help attract Foreign Direct Investment (FDI) but will also serve as a vital foundation for driving the domestic digital economy, including AI services and the Internet of Things (IoT). These elements will enhance business sector efficiency and create a structural competitive advantage for Thailand in the sustainable digital economy era.

References

World Bank. (2024). Advancing Cloud and Data Infrastructure Markets: Strategic Directions for Low- and Middle- Income Countries. World Bank. https://www.worldbank.org/en/publication/advancing-cloud-and-data-infrastructure-markets

Cushman & Wakefield. (2025). Asia Pacific Data Centre Investment Landscape. Cushman & Wakefield. https://cushwake.cld.bz/investmentlandscape-06-2025-apac-regional-en-content-datacentres

DC Byte. (2025). Global Data Centre Index 2025. DC Byte. https://www.dcbyte.com/global-data-centre-index/2025-global-data-centre-index/

DC Byte. (2025). Data Centres in Johor and Batam. DC Byte. https://www.dcbyte.com/market-infographics/data-centres-in-johorbatam/

DC Byte. (2025). Thailand’s Data Centre Surge. DC Byte. https://www.dcbyte.com/market-spotlights/thailand-data-centre-surge/

Deloitte. (2025). Southeast Asia’s data centres and AI infrastructure imperative. Deloitte. https://www.deloitte.com/content/dam/assets-zone1/southeast-asia/en/docs/industries/technology-media-telecommunications/2025/sea-tmt-ai-data-centres-and-ai-infrastructure-imperative-sep2025.pdf

Knight Frank. (2025). Data Centres Global Report – 2025. Knight Frank. https://content.knightfrank.com/research/2982/documents/en/data-centres-global-report-2025-12054.pdf

McKinsey & Company. (2025). What is a data center?. McKinsey & Company. https://www.mckinsey.com/featured-insights/mckinsey-explainers/what-is-a-data-center

Cushman & Wakefield. (2025). Asia Pacific Data Centre Construction Cost Guide 2025. Cushman & Wakefield. https://cushwake.cld.bz/asiapacificdatacentreconstructioncostguide-01-2025-apac-regional-en-content-datacentres

AHA Centre. (2024). From response to resilience AHA annual report 2024. AHA Centre. https://ahacentre.org/publication/annual-report-2024/

Pornchanok Tapkham. (2025). Data Centers Ecosystem. Bank of Thailand. https://www.bot.or.th/content/dam/bot/documents/th/research-and-publications-pdf/articles-and-publications/articles/download/2026/article-20260101.pdf

ASEAN. (2024). ASEAN Key Figures – 2024. ASEAN. https://asean.org/wp-content/uploads/2025/02/ASEAN-Key-Figures-2024.pdf

1/ Number of Data Centers by Country (November 2025) | Cargoson

2/ Data Center - Worldwide | Statista Market Forecast

3/ What is a data center? | McKinsey

4/ Private Cloud refers to a cloud system where resources and infrastructure are allocated for the exclusive use of a specific organization and are not shared with others. In contrast, Public Cloud is a cloud system that provides services to multiple users sharing the same infrastructure via the internet, managed by a cloud service provider.

5/ A unit of digital data measurement, where 1 zettabyte is equivalent to 1 trillion gigabytes.

6/ Data Center - ASEAN | Statista Market Forecast

7/ Southeast Asia’s data centres and AI infrastructure imperative | Deloitte Southeast Asia

8/ Number of Data Centers by Country (November 2025) | Cargoson

9/ Data Centres in Johor and Batam | DC Byte

10/ Advancing Cloud and Data Infrastructure Markets | World Bank

11/ Subsea cables include those expected to be operational within the next 5 years, based on data from the Submarine Cable Map by TeleGeography.

12/ Advancing Cloud and Data Infrastructure Markets | World Bank