Introduction

The world is entering the era of Agentic AI, where AI systems are capable of not only assisting users with information but also making decisions and executing tasks autonomously without requiring human instructions at every step. One emerging business application attracting significant attention is “Agentic Commerce,” where AI acts as an intelligent shopping assistant capable of searching for products, comparing prices, negotiating deals, and even completing payments on behalf of consumers in an end-to-end manner.

Beyond enhancing convenience and improving the shopping experience, Agentic Commerce is poised to become a major turning point in the future of online commerce. This shift could have far-reaching implications for commercial banks, influencing the design of financial products, payment infrastructures, customer engagement strategies, and regulatory frameworks. As AI increasingly participates in financial transactions, ensuring robust security, transparency, and consumer protection will become more critical than ever.

Understanding Agentic Commerce

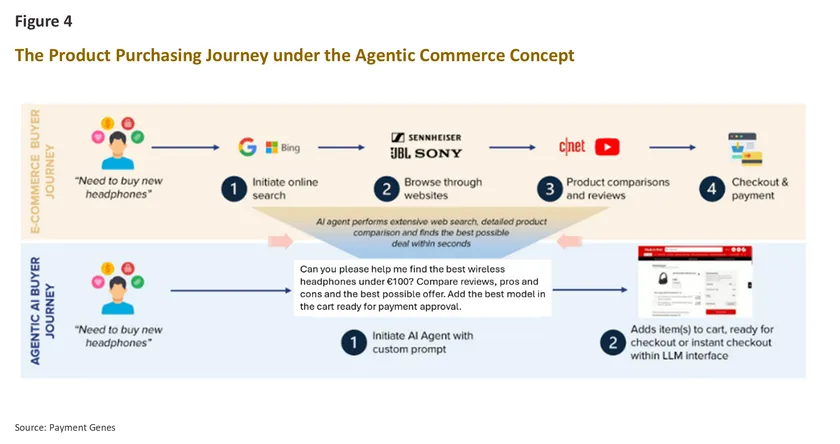

Consumers today are familiar with purchasing products through e-commerce platforms, typically by searching for products online, adding items to a shopping cart, and completing the payment process. However, the rise of AI Agents

1/ is beginning to transform this conventional online shopping journey. AI Agents are increasingly capable of making decisions and conducting transactions on behalf of consumers through simple text or voice interactions.

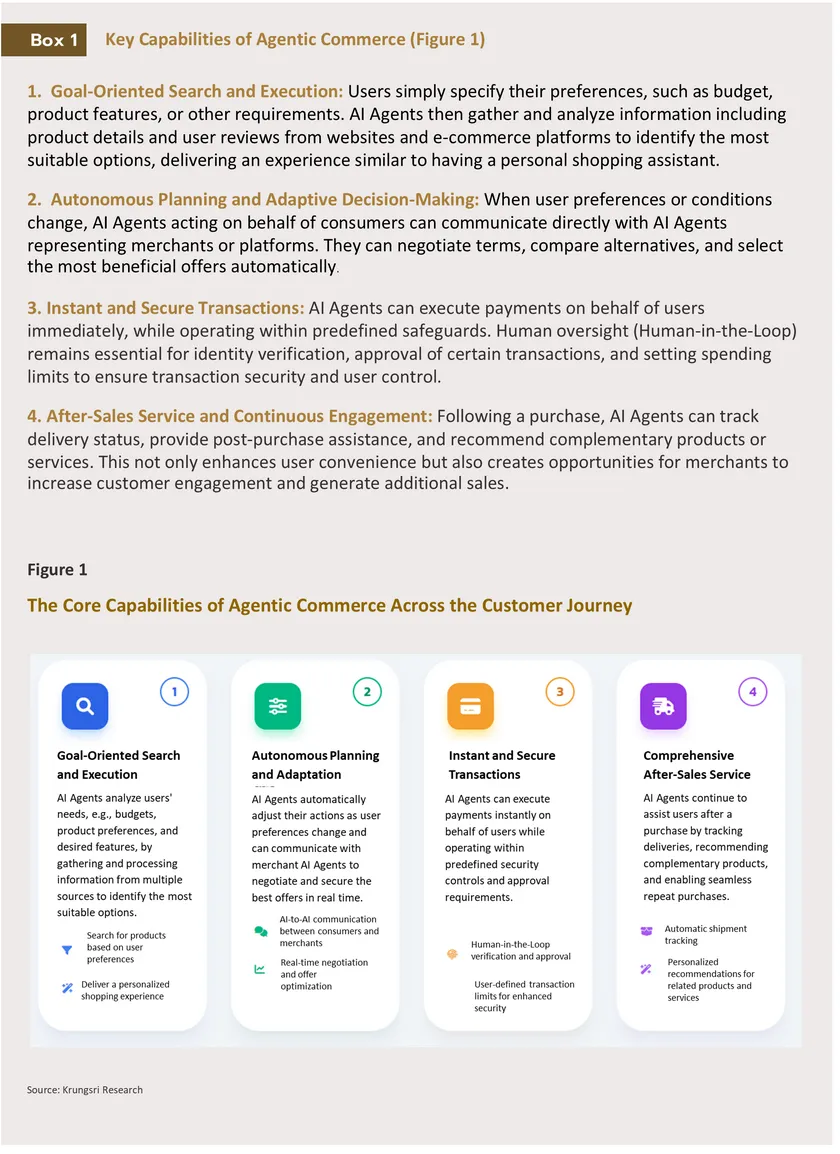

Consumers only need to specify their preferences, after which AI Agents can autonomously perform a wide range of tasks—from analyzing individual needs, searching for information, comparing and selecting products, placing orders, and making payments, to managing after-sales services and even automatically reordering products when supplies run low. Supporting this process is

Agentic Payments, an AI-driven payment system that enables AI Agents to make payment decisions and execute transactions on behalf of users based on predefined conditions. Together, these developments are giving rise to a new model of commerce known as

Agentic Commerce, or AI Shopping Agents.

Technologies Behind Agentic Commerce

The advancement of Agentic AI

2/—enabling AI systems to analyze, plan, and act autonomously—has laid the foundation for Agentic Commerce. Its operation relies on several key technological infrastructures, particularly Application Programming Interfaces (APIs),

3/ which allow AI systems and software applications to communicate seamlessly, as well as common standards and protocols that govern interactions and transactions between AI Agents and different systems.

Key examples include:

-

Agent-to-Agent Protocol (A2A)4/ – An open communication and coordination standard developed by Google together with more than 50 partners. It enables AI Agents to access product information, negotiate offers, place orders, and execute payments in a standardized manner.

-

Agent Payments Protocol (AP2)5/– A payment standard developed by payment companies such as Mastercard and PayPal, alongside technology firms including Google and Salesforce. It allows AI Agents to make payments securely on behalf of users through credit cards or bank transfers.

-

Agentic Commerce Protocol (ACP) – An open standard developed by OpenAI and Stripe6/ that defines how AI Agents interact and transact with merchants' systems. The protocol covers the entire transaction process—from accessing product and pricing information to secure payment execution—allowing users to complete purchases instantly without having to open a banking application or visit a payment provider's website.

In summary, two key technological foundations are enabling Agentic Commerce to become a reality. The first is technologies that allow AI Agents to access and interact seamlessly with product and service information across digital platforms. The second is secure and trusted payment technologies that enable AI Agents to execute transactions safely and efficiently on behalf of users.

Trend in the Development of Agentic Commerce Technology

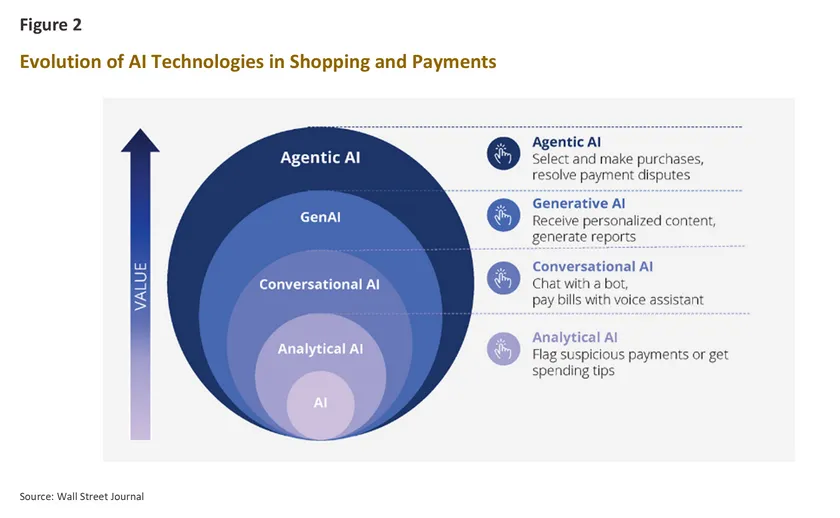

As consumers become increasingly familiar with AI in their daily lives, AI developers are accelerating the development of Agentic Commerce to meet rapidly evolving consumer demands (see Figure 2). This development is also expected to create new revenue streams, driven by the fast-growing base of AI users.7/

In September 2025, OpenAI introduced the “Instant Checkout” feature, enabling users to purchase products directly through ChatGPT. The system is powered by the Agentic Commerce Protocol (ACP), marking an evolution of ChatGPT from a conversational chatbot into an AI shopping assistant capable of acting on behalf of users.8/

Subsequently, in February 2026, Google launched a similar capability that allows AI-driven purchasing via Google Search and the Gemini chatbot, initially in a U.S. pilot phase. Users simply specify product requirements, after which the AI agent searches for the most relevant options and prompts users to confirm the order and complete payment.9/

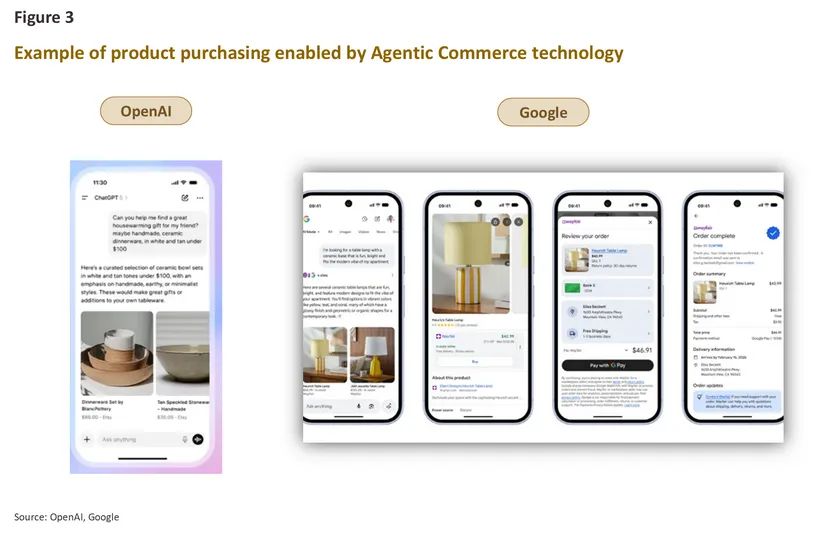

In addition, Google has partnered with global apparel retailer GAP to test Gemini as a new sales channel. Consumers can inquire about product details such as style, color, and size through Gemini. The AI then identifies matching items, facilitates ordering, and enables instant payment completion (see Figure 3).10/

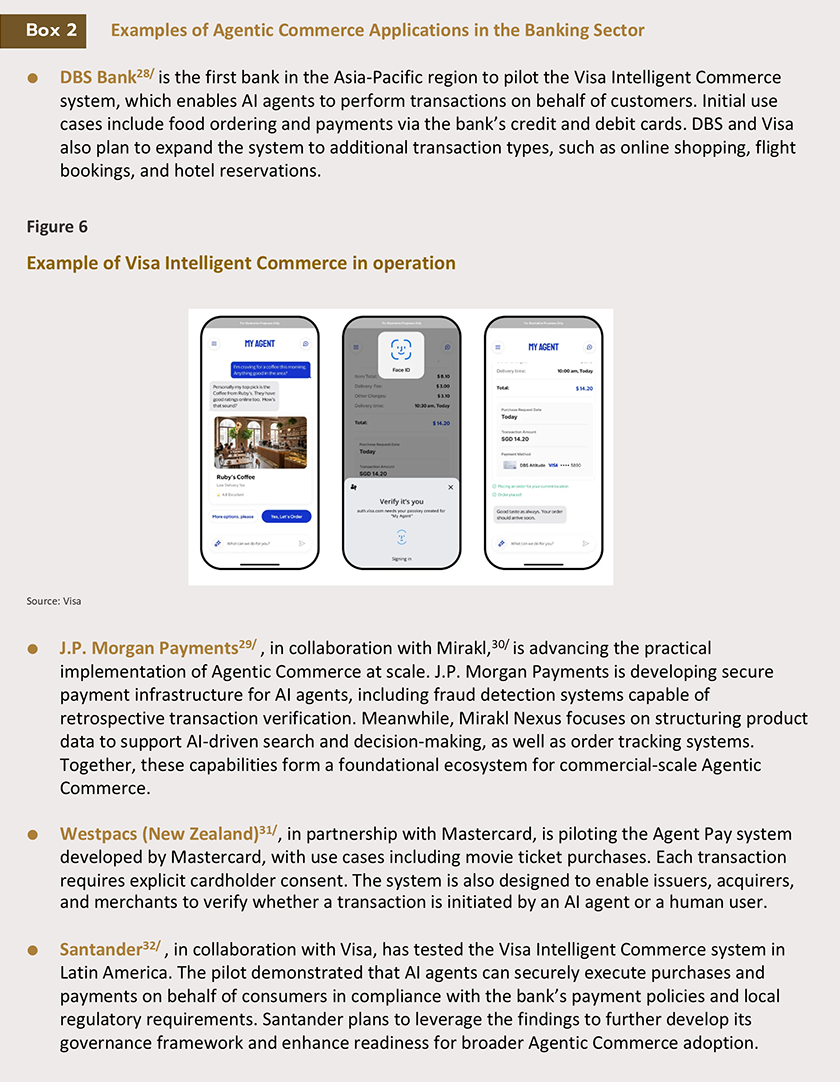

On the other side of the ecosystem, payment service providers are also accelerating the development of technologies to support Agentic Commerce. Visa11/ has launched “Intelligent Commerce,” a platform designed to enable AI agents to purchase goods and make payments on behalf of consumers. The system emphasizes stringent transaction security through authentication mechanisms and access controls, allowing only authorized AI agents to execute transactions. It also incorporates tokenized payment technology, which replaces sensitive credit card information with randomized tokens to reduce the risk of data breaches.

Similarly, Mastercard has introduced “Agent Pay,” a payment infrastructure built to enable AI agents to conduct transactions on behalf of users in a secure manner. Key safeguards include AI agent authentication, permission-based access controls, and transaction validation processes to ensure accuracy and security.12/

Thai businesses are also beginning to adopt Agentic Commerce in real-world transactions. In May 2026, Big C Supercenter Public Company Limited, in collaboration with Amazon Web Services (AWS), a global provider of cloud and AI technologies, launched the “Shopping Assistant AI Chat” feature within the Big C mobile application. The feature allows customers to interact with an AI assistant and specify desired products. The AI then analyses the request, compiles relevant items into a shopping cart, and prepares the order for payment, which completes the process within seconds.13/

Meanwhile, in April 2026, Mastercard partnered with KTC, a credit card issuer, to pilot the use of AI agents for booking and paying for ride-hailing services via the global transport platform Elife. The initiative aims to enhance travel experiences in Thailand by making transactions more seamless and frictionless.

Agentic Commerce reshapes consumer behavior and expands business opportunities

Agentic Commerce is expected to enhance consumer experience while creating new revenue expansion opportunities for businesses. According to Grand View Research, the global market size of Agentic Commerce is projected to reach USD 65.5 billion in 2033, rising from USD 7.7 billion in 2026, representing a compound annual growth rate (CAGR) of 35.7%.

14/ Overall, Agentic Commerce is likely to reshape both consumer behavior and business dynamics (see Figure 5) in several ways.

-

First, shopping behavior is expected to become increasingly AI-dependent. Consumers worldwide are showing greater openness to using AI for purchasing goods and services through online platforms. A 2025 Deloitte survey found that 46.0% of U.S. consumers already use AI to search for better prices and deals.15/ Similarly, Thai consumers are increasingly receptive to AI as a shopping assistant. A Google and Bain & Company survey (2025) reported that 92.0% of Thai respondents are willing to allow AI access to their shopping history.16/ This trend is a key driver of Agentic Commerce growth. AI agents are expected to play an increasingly important role in purchase decision-making by analyzing user behavior and preferences. This helps reduce search and comparison time while improving the likelihood of finding more cost-efficient products that better match individual needs through hyper-personalization.17/

-

Second, businesses have opportunities to create new revenue channels. Agentic Commerce enables a deeper understanding of customer needs, as consumers interact with AI agents to specify detailed purchasing conditions, including budget constraints and individual preferences. This allows businesses to deliver more precise product offerings, promotions, and experiences that better match consumer demand. In addition, consumers purchasing through AI-driven recommendations tend to exhibit higher purchase intent compared with other channels. According to Adobe (July 2025), users arriving at websites via AI recommendations show higher engagement than general visitors, spending around 10.0% more time on sites and often visiting at a later, more purchase-ready stage of the decision journey.18/ Similarly, data from Shopify19/ indicates that customers who receive product recommendations through AI generate higher business value than those acquired via traditional search engines. These users are approximately 50.0% more likely to complete a purchase, while their average order value is about 14.0% higher, reflecting more qualified and pre-filtered purchasing decisions driven by AI recommendations.20/

The above evidence indicates that Agentic Commerce is not merely a new sales channel, but is increasingly playing a significant role in shaping consumer purchasing decisions. It also expands opportunities for businesses to reach a broader customer base. As such, it represents a new and emerging revenue stream that businesses should not overlook.

Challenges of adopting Agentic Commerce for businesses

- Customer access through AI:

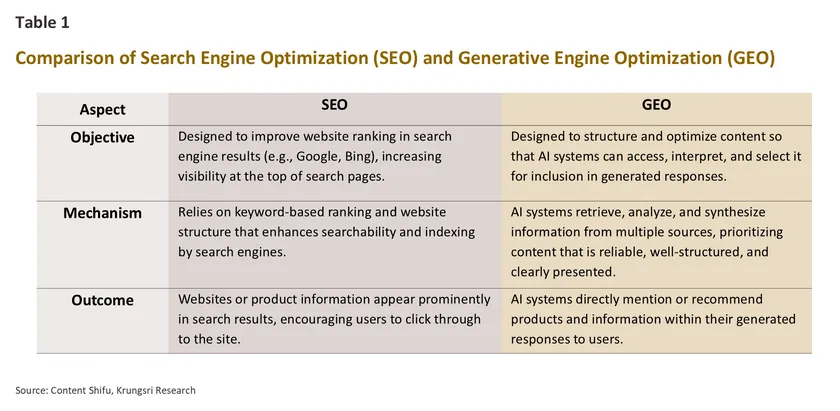

In the past, consumers typically began their product search using search engines such as Google or Bing, which have served as the primary gateway between buyers and sellers. As a result, businesses have placed strong emphasis on

Search Engine Optimization (SEO), adjusting website structure and content to align with search engine algorithms in order to improve visibility in search rankings. However, in the next phase, as AI becomes capable of analyzing and making purchase decisions on behalf of consumers,

businesses will need to shift their strategies toward Generative Engine Optimization (GEO). This involves designing and tailoring content to align with how AI systems process and interpret information, so that AI agents are more likely to select and recommend their products to users.

According to IDC, businesses that adopt GEO strategies can increase the likelihood of being mentioned in AI-generated responses by up to 40.0%.

21/ This highlights the growing role of AI as an intermediary between consumers and businesses.

- User trust and accountability:

While Agentic AI enhances convenience for consumers, it may also undermine user trust in certain scenarios. For instance, an AI agent may purchase goods without explicit authorization or execute transactions incorrectly, leading to potential financial losses. This raises important questions regarding liability—who should be held responsible when an AI agent makes a purchasing error that results in disputes between buyers and sellers.

To address these concerns,

Agentic Commerce systems must be designed with a “human-in-the-loop” approach, ensuring that humans retain final control over critical decisions before transactions are executed. Safeguards may include biometric authentication (e.g., facial recognition or fingerprint scanning) and predefined spending limits or transaction caps that restrict the value of autonomous AI-driven purchases. These mechanisms help maintain consumer confidence by ensuring users retain oversight over important financial decisions, even when delegating tasks to AI agents.

- Data readiness and system integration:

As AI requires real-time data to make purchasing decisions on behalf of consumers, access to high-quality product and service data becomes essential. Businesses must therefore maintain structured and up-to-date product information, including specifications, pricing, inventory levels, and delivery conditions. In addition, system integration across customer relationship management (CRM) platforms and real-time payment systems is necessary to enable seamless AI access to enterprise data.

However, poorly structured or disconnected data systems may prevent AI agents from accurately retrieving or purchasing products, resulting in lost commercial opportunities. At the same time, access to data must be governed by strict security and privacy controls to ensure consumer data protection remains a top priority.

- Dependence on AI platforms for sales generation:

As Agentic Commerce expands, AI platforms are expected to become key customer access channels, creating unavoidable platform dependency for businesses seeking to reach consumers. For example, OpenAI has reportedly tested transaction fees of approximately 4.0% on merchant sales conducted through ChatGPT’s Instant Checkout feature.22/

Beyond adapting marketing models, businesses must therefore consider rising transaction costs and intensifying competition. Moreover, heavy reliance on AI platforms may limit direct access to customer data, including valuable behavioral insights and preferences, while also reducing opportunities to build proprietary shopping experiences through owned channels such as websites, applications, or online storefronts.

- Cybersecurity risks and emerging fraud mechanisms:

Cybercriminals are increasingly leveraging AI agents to conduct fraudulent activities. The World Economic Forum23/ projects that by 2028, more than one-quarter of organizations could experience cyberattacks involving AI agents. As Agentic Commerce requires AI access to sensitive consumer data, including bank accounts and credit card information, the risk of data breaches and financial loss increases significantly.

Fraudsters may manipulate product information to appear more credible, undercut prices, or generate large volumes of fake positive reviews to influence AI agents’ purchasing decisions. These malicious agents can automate the entire fraud cycle, increasing the risk that financial and personal data may be compromised immediately after a transaction is completed.

How financial institutions should adapt in the era of Agentic Commerce

As AI increasingly acts as an intermediary in consumer purchasing decisions, financial institutions must expand their role to enable a secure and seamless Agentic Commerce ecosystem. Development strategies should therefore cover technology infrastructure, security, and customer experience in an integrated manner.

-

Develop payment infrastructure to support AI-driven transactions: Payment systems are a critical enabler of Agentic Commerce. While today’s payment processes are designed for human authorization at nearly every step, the next phase requires systems that allow consumers to delegate transaction authority to AI agents while still ensuring security and control. Financial institutions must therefore develop payment infrastructures that are compatible with emerging standards and protocols from payment companies and technology providers, enabling seamless interoperability. Early movers in building such infrastructure are likely to become key financial service providers in the Agentic Commerce ecosystem.

-

Strengthen fraud and cybersecurity measures: Agentic Commerce may significantly increase the complexity and severity of fraud risks. However, many financial institutions are not yet fully prepared for these emerging threats. According to an Accenture survey (2025), 78.0% of financial executives believe that Agentic Payments will increase fraud, while more than 60.0% of institutions are not yet equipped to handle fraud involving AI agents.24/ Key mitigation measures include: (1) using AI to detect anomalous transactions based on customer and AI agent behavior, (2) implementing strict governance frameworks to define clear operational boundaries for AI agents, and (3) enhancing cybersecurity controls to address emerging AI-driven threats. Institutions that adopt these measures early will be better positioned to maintain customer trust and minimize potential losses.

-

Develop AI agent identity verification (Know Your Agent: KYA): Financial institutions should establish dedicated mechanisms to verify and govern AI agents in a systematic manner, ensuring trust in AI-mediated financial transactions. The KYA framework should be designed around four key principles: (1) verifying the identity and authorization source of AI agents, including the individual or organization that deploys them, (2) defining transaction scope, including spending limits, permissible transaction types, and time boundaries, (3) monitoring and auditing AI agent behavior to ensure compliance with financial regulations and institutional policies, and (4) implementing real-time safeguards such as transaction suspension, customer alerts, or confirmation requests when abnormal activity is detected.25/

-

Develop AI-discoverable financial products: Financial institutions must adapt to the growing use of AI as a primary channel for information search and product comparison. According to Adobe, AI-driven referrals to financial websites increased by 2.7 times between November and December 2025 compared with the same period a year earlier. Users referred by AI also spent 21.0% 26/ more time on websites than average visitors, indicating higher engagement and stronger purchase intent. This reflects AI’s growing role in financial services, particularly in delivering personalized product recommendations. Institutions that are surfaced by AI will have a significant competitive advantage in customer acquisition. Therefore, financial providers should accelerate digital marketing transformation, e.g., improving product data structuring and adopting Generative Engine Optimization (GEO) strategies, to enhance discoverability and ensure their products are effectively recommended by AI systems.

However, Agentic Commerce may also erode customer loyalty for financial institutions in the future. A McKinsey survey conducted in August 2025 found that 41.0% of respondents in the United States use AI to support their decision-making when selecting financial products.

27/ This suggests that, in the future, customers may no longer choose financial products based on familiarity or long-standing relationships with financial institutions, as in the past, but increasingly based on AI-generated recommendations. As a result, financial institutions may need to accelerate the development of more competitive financial products that are closely aligned with specific customer needs and objectives. Moreover, in the era of Agentic AI, direct interactions between financial institutions and customers may decline. Customers may visit banks’ applications or websites less frequently, or delegate the entire decision-making and transaction process to AI agents. This could reduce opportunities for financial institutions to build customer engagement, deliver positive experiences, and strengthen long-term relationships, ultimately increasing the risk of losing customer loyalty—similar to what may be observed in other industries.

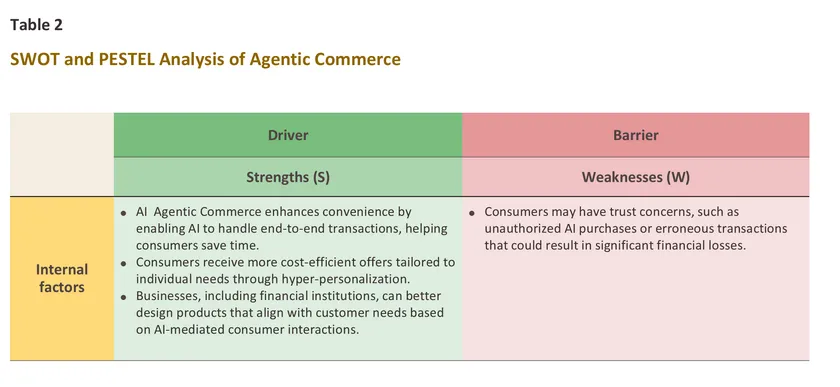

An analysis of the future of Agentic Commerce through SWOT and PESTEL frameworks suggests that, although this technology can significantly enhance convenience and improve consumer experience, several limitations must still be considered. These include consumer trust, regulatory readiness, and cybersecurity risks. Key details are summarized in Table 2.

Krungsri Research View

In the future, Agentic Commerce is expected to play an increasingly important role in consumers’ daily lives, beginning with basic transactions such as bill payments and the purchase of low-value consumer goods. The development of Agentic Commerce therefore requires a careful balance between transactional convenience and user security and trust.

Looking back, the financial sector has historically played a key role in enabling the transition to the digital commerce era by developing financial infrastructure that made online transactions secure and reliable. Similarly, in the near future, financial institutions are expected to accelerate the development of payment systems that support AI-agent-driven transactions, while simultaneously addressing emerging cybersecurity risks in various forms. Financial institutions should therefore continue to strengthen their core advantage in trustworthiness and adhere strictly to regulatory requirements, while also designing payment systems that are compatible with the evolving Agentic Commerce ecosystem in several key dimensions:

-

Building partnerships with technology ecosystem players to develop secure payment systems. To enable Agentic Commerce to scale as a viable transaction channel, financial institutions may need to collaborate closely with ecosystem participants such as AI developers, payment service providers, and e-commerce platforms. Such collaboration will help ensure that AI agents can access and execute financial transactions seamlessly, securely, transparently, and reliably—thereby strengthening overall confidence in digital financial transactions.

-

Collaborating with regulators to align regulatory frameworks with international security standards. As financial institutions are responsible for safeguarding transaction data conducted by AI agents on behalf of consumers, regulatory adaptation will be essential. While specific regulations governing Agentic Commerce are still limited, some jurisdictions have already begun addressing the issue. For example, in January 2026, the Consumer Bankers Association in the United States issued a report recommending that industry stakeholders and regulators jointly review consumer protection frameworks to accommodate Agentic Commerce. This includes dispute resolution mechanisms and liability frameworks in cases where AI-driven transactions result in financial harm. Thai financial institutions and regulators should closely monitor these developments and adapt appropriate frameworks to the local context.

-

Leveraging the trust advantage of financial institutions to support Agentic Commerce growth. Financial institutions possess a unique competitive advantage that is difficult for other industry players to replicate, which is “trust.” This trust is built on strict regulatory oversight, proven and secure payment systems, and long-standing customer relationships. These strengths form a critical foundation for expanding into Agentic Commerce, as users will only delegate decision-making authority to AI agents when they have full confidence in the underlying service provider.

In an era where AI plays an increasingly central role in consumer decision-making, Agentic Commerce will significantly reshape purchasing behavior and the overall commerce landscape. Businesses and financial institutions that are able to adapt quickly will gain a stronger competitive advantage, while those that fail to adjust may ultimately lose customers and business opportunities.

References

English

Adobe. (2025). “Adobe AI Traffic Trends Report: Industry insights” Retrieved April 9, 2026, from https://business.adobe.com/resources/sdk/adobe-ai-traffic-report.html

Agarwal, S. (2025). “Agentic payments in commerce—the future is here” Retrieved March 7, 2026, from https://bankingblog.accenture.com/agentic-payments-commerce

Arroyo, C. (2026). “Google pushes AI shopping features in search and Gemini chatbot” Retrieved 3 May, 2026, from https://www.bloomberg.com/news/articles/2026-02-11/google-pushes-ai-shopping-features-in-search-and-gemini-chatbot

AstraSync AI. (2025). “Know Your Agent (KYA): Establishing the standard for AI agent identity and trust” Retrieved May 9, 2026, from https://medium.com/@astrasyncai/know-your-agent-kya-establishing-the-standard-for-ai-agent-identity-and-trust-d0fb779fc657

Ayers, J. (2026). “AI agents could be worth $236 billion by 2034 – if we ensure they are the good kind” Retrieved May 19, 2026, from https://www.weforum.org/stories/2026/01/ai-agents-trust/

Brohan, M. (2026). “OpenAI expands agentic commerce push” Retrieved June 19, 2026, from https://www.digitalcommerce360.com/2026/02/16/openai-expands-agentic-commerce-push/

Deloitte. (2025). “Agentic AI: Point of view for banking and capital markets” Retrieved February 19, 2026, from https://www.deloitte.com/content/dam/assets-zone3/us/en/docs/industries/financial-services/2025/bcm-agentic-ai-pov.pdf

Evans, M., Derow, R., Krogman, M., & Gregor, L. (2025). “Agentic commerce is redefining retail—here’s how to respond” Retrieved January 30, 2026, from https://www.bcg.com/publications/2025/agentic-commerce-redefining-retail-how-to-respond

Fattahi, A. (2026). “Global fragmentation of AI governance and regulation” Retrieved May 29, 2026, from https://bisi.org.uk/reports/global-fragmentation-of-ai-governance

Finextra. (2026). “Mastercard and Visa enlist banks for agentic payment pilots” Retrieved March 18, 2026, from https://www.finextra.com/newsarticle/47316/mastercard-and-visa-enlist-banks-for-agentic-payment-pilots

FinTech Magazine. (2026). “Mastercard launches Agent Pay for AI payment transactions” Retrieved May 21, 2026, from https://fintechmagazine.com/articles/mastercard-launches-agent-pay-for-ai-payment-transactions

Google, Temasek, & Bain & Company. (2025). “e-Conomy SEA 2025: From digital decade to AI reality – Accelerating the future in ASEAN” Retrieved May 29, 2026, from https://services.google.com/fh/files/misc/thailand_e_conomy_sea_2025_report.pdf

Grand View Research. (2026). “Agentic commerce market size & share report, 2026–2033” Retrieved June 9, 2026, from https://www.grandviewresearch.com/industry-analysis/agentic-commerce-market-report

IDC. (2025). “Marketing’s new imperative: The shift from SEO to LLM optimization” Retrieved June 4, 2026, from https://www.idc.com/resource-center/blog/marketings-new-imperative-the-shift-from-seo-to-llm-optimization/

Loyd, W. (2026). “CBA releases white paper examining agentic AI, consumer payments, and the future of regulation” Retrieved May 21, 2026, from https://consumerbankers.com/press-release/cba-releases-white-paper-examining-agentic-ai-consumer-payments-and-the-future-of-regulation/

Parikh, S., & Surapaneni, R. (2025). “Powering AI commerce with the new Agent Payments Protocol (AP2)” Retrieved June 1, 2026, from https://cloud.google.com/blog/products/ai-machine-learning/announcing-agents-to-payments-ap2-protocol

PYMNTS. (2026). “Shopify merchants to pay 4% fee on ChatGPT checkout sales” Retrieved June 6, 2026, from https://www.pymnts.com/news/ecommerce/2026/shopify-merchants-to-pay-4percent-fee-on-sales-made-through-chatgpt-checkout/

Risley, K. (2026). “AI-referred shoppers convert better and spend more: What Shopify's early data shows” Retrieved June 2, 2026, from https://www.shopify.com/enterprise/blog/ai-search-insights

RTTNews. (2026). “Google expands AI shopping features, integrating ads and direct purchases into search and chatbots” Retrieved May 5, 2026, from https://www.nasdaq.com/articles/google-expands-ai-shopping-features-integrating-ads-and-direct-purchases-search-and

Silliman, E., Boudet, J., Robinson, K., Oppong, D., & Shah, N. (2025). “New front door to the internet: Winning in the age of AI search” Retrieved May 4, 2026, from https://www.mckinsey.com/capabilities/growth-marketing-and-sales/our-insights/new-front-door-to-the-internet-winning-in-the-age-of-ai-search

Visa. (2026). “DBS is first bank in Asia Pacific to pilot Visa Intelligent Commerce for everyday payments” Retrieved April16, 2026, from https://www.visa.com.sg/about-visa/newsroom/press-releases/dbs-is-first-bank-in-asia-pacific-to-pilot-visa-intelligent-commerce-for-everyday-payments.html

Visa. (2026). “Enabling AI agents to buy securely and seamlessly” Retrieved April 20, 2026, from https://www.visa.com/en-us/solutions/intelligent-commerce

Thai

Ditto. (2025). “API คืออะไร? ช่วยในการเชื่อมต่อระบบในองค์กรยุคดิจิทัลอย่างไร” Retrieved Apr 29, 2026, from https://www.dittothailand.com/th/dittonews/what-is-api/

Money & Banking Magazine. (2026). “ไม่ต้องพิมพ์ค้นหา บิ๊กซี จับมือ AWS ใช้ AI สั่งของจบในแชต รับศึกอีคอมเมิร์ซแสนล้าน” Retrieved May 29, 2026, from https://moneyandbanking.co.th/2026/247286/

Thairath Money. (2026). “รู้จัก Know Your Agent - KYA เข้าสู่ยุค AI ต้องยืนยันตัวตน เพราะมนุษย์เปิดทางให้ AI เข้าถึงเงิน” Retrieved June 11, 2026, from https://www.thairath.co.th/money/tech_innovation/digital_transformation/2929954

1/ AI Agents refer to AI-driven entities specialized in specific tasks, such as information retrieval agents, payment agents, and supervisory agents that coordinate or instruct other AI systems.

2/ For more details on Agentic AI technology, please refer to: Banks in the Age of Agentic AI

3/ Application Programming Interface (API) refers to a set of instructions that enables different software systems to communicate and work together. For example, a food delivery application may use the Google Maps API to display restaurant locations and map data within the app. Similarly, in-app payment systems may use APIs provided by commercial banks to facilitate payment transactions (Source: API คืออะไร? ช่วยในการเชื่อมต่อระบบในองค์กรยุคดิจิทัลอย่างไร | Ditto)

4/ Source: What Is Agent2Agent (A2A) Protocol? | IBM

5/ Source: Announcing Agent Payments Protocol (AP2) | Google Cloud Blog

6/ Stripe is a global payment technology company that develops infrastructure to support online transactions for businesses and digital platforms.

7/ AI developers are increasingly seeking new revenue streams to support continued investment in AI infrastructure. In 2026, capital expenditures on AI-related infrastructure by Google, Amazon, Meta, and Microsoft are estimated to reach USD 650 billion. (Source: Google Pushes AI Shopping Features in Search and Gemini Chatbot - Bloomberg)

8/ OpenAI has partnered with Stripe and PayPal to develop payment systems. (Source: OpenAI expands agentic commerce push)

9/ Source: Google Expands AI Shopping Features, Integrating Ads And Direct Purchases Into Search And Chatbots | Nasdaq

10/ Source: Gap partners with Google Gemini to offer AI platform checkout

11/ Visa collaborates with several companies, including Anthropic, IBM, Microsoft, Mistral AI, OpenAI, Perplexity, Samsung, and Stripe, to develop solutions that enable AI agents to conduct secure and seamless purchases Source: (Enabling AI agents to buy securely and seamlessly | Visa)

12/ Source: Mastercard Launches Agent Pay for AI Payment Transactions | FinTech Magazine

13/ Source: ไม่ต้องพิมพ์ค้นหา บิ๊กซี จับมือ AWS ใช้ AI สั่งของจบในแชต รับศึกอีคอมเมิร์ซแสนล้าน |Money & Banking Magazine

14/ Source: Agentic Commerce Market Size, Share | Industry Report 2033

15/ Source: The future of commerce in an agentic world: How agentic AI will reshape commerce and what payment networks must do next | Deloitte

16/ Source: e-conomy_sea_2025 report – Thailand | Google

17/ Hyper-personalization refers to the use of in-depth customer data (e.g. behavior and preferences), combined with AI technology, to analyse and tailor products, services, or experiences to meet individual customer needs. For more details, please refer to: Hyper-personalization: Giving banks AI-powered insight into their customers

18/ Source: Agentic Commerce is Redefining Retail - How to Respond | BCG

19/ Shopify is an e-commerce platform that enables businesses to create online stores, manage products, accept payments, and handle sales operations all in one place.

20/ Source: AI-referred shoppers convert better and spend more (2026) | Shopify

21/ Source: Marketing’s new imperative: The shift from SEO to LLM optimization | IDC

22/ Source: Shopify Merchants to Pay 4% Fee on ChatGPT Checkout Sales | PYMNTS

23/ Source: AI agents could be worth $236 billion by 2034 – if we ensure they are the good kind | World Economic Forum

24/ Survey of Chief Technology Officers (CTOs) and payment executives at financial institutions. (Source: Agentic payments in commerce—the future is here | Accenture Banking Blog)

25/ Source: Know Your Agent (KYA): Establishing the Standard for AI Agent Identity and Trust by AstraSync AI | Medium & รู้จัก Know Your Agent - KYA เข้าสู่ยุค AI ต้องยืนยันตัวตน เพราะมนุษย์เปิดทางให้ AI เข้าถึงเงิน | Thairath Online

26/ Source: Quarterly AI Traffic Report | Adobe for Business

27/ Survey of 1,927 consumers (Source: Winning in the age of AI search | McKinsey)

28/ Source: DBS is First Bank in Asia Pacific to Pilot Visa Intelligent Commerce for Everyday Payments | Visa

29/ J.P. Morgan Payments is the payments business unit of J.P. Morgan, providing payment infrastructure, processing services, and fraud detection capabilities within payment systems.

30/ Mirakl is a French technology company that develops platforms for building and managing online shopping marketplaces.

31/ Source: Mastercard and Visa enlist banks for agentic payment pilots | Finextra

32/ Santander is a Spanish banking institution operating in more than 10 countries across Europe and the Americas, with a customer base of over 180 million. For more details, please refer to: How we help people and businesses prosper | Santander

33/ Source: Global Fragmentation of AI Governance and Regulation | Bloomsbury Intelligence and Security Institute (BISI)

34/ Source : 25680178.pdf | BOT

36/ Source: CBA Releases White Paper Examining Agentic AI, Consumer Payments, and the Future of Regulation | The Consumer Bankers Association (CBA)