EXECUTIVE SUMMARY

In 2026, modern retail businesses are facing pressure from a slowing Thai economy, which is weighing on purchasing power amid ongoing global uncertainties. As a result, middle- to lower-income consumers are increasingly prioritizing essential goods. However, spending by middle- to upper-income consumers, together with the anticipated continuation of economic stimulus measures, is expected to help stabilize overall retail sales—particularly in the convenience store segment. In 2027–2028, sales are forecast to gradually recover alongside a slow economic rebound. Infrastructure investment will drive expansion into suburban and regional markets. Operators are expected to stimulate growth through new store formats, private label products, AI and Big Data-driven customer targeting, and continued online channel development to support long-term growth.

Key challenges stem from a slow recovery in consumer purchasing power amid Thai and global economic uncertainty, which is also weighing on tourism growth. Retail competition continues to intensify, while investment in technology and ESG standards has become a significant and unavoidable cost burden.

Krungsri Research view

The 2026-2028 outlook for individual segments is given below.

-

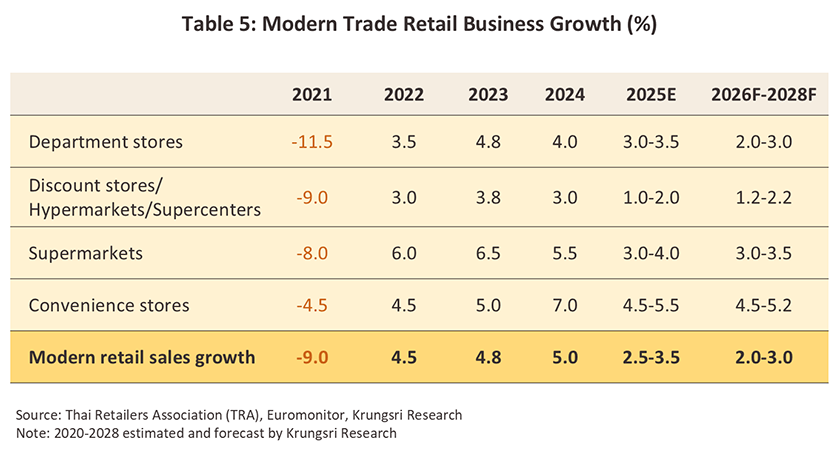

Department stores: Revenue is projected to grow at 2.0–3.0% annually, supported by a stable, higher-income customer base that is relatively resilient to economic cycles. Locations within CBDs and mass transit hubs provide a structural advantage from ongoing urbanization and transit expansion. Key risks include intensifying competition from newly opened luxury shopping centers, while a high fixed cost base, covering depreciation and utilities, may compress margins during periods of weaker footfall.

-

Discount stores/hypermarkets/supercenters: Revenue is projected to grow at 1.2–2.2% annually. The business benefits from economies of scale, enabling effective control of unit costs and efficient management of short shelf-life products. However, intense price and promotional competition may put pressure on margins, limiting their growth potential.

-

Supermarkets: Revenue is projected to grow at 3.0–4.0% annually, driven by product differentiation that reduces reliance on price competition. Agile, localized merchandising supports relatively healthy margins. Challenges include managing fresh food inventory, where short shelf life contributes to quality and price volatility. Imported goods are also pressured by currency fluctuation and freight costs, which may lead to earnings variability.

-

Convenience stores/minimarts: Revenue is projected to grow at 4.5–5.2% annually, supported by economies of scale that enable effective unit cost control and efficient management of short shelf-life products. However, intense price and promotional competition is likely to limit meaningful margin expansion

Overview

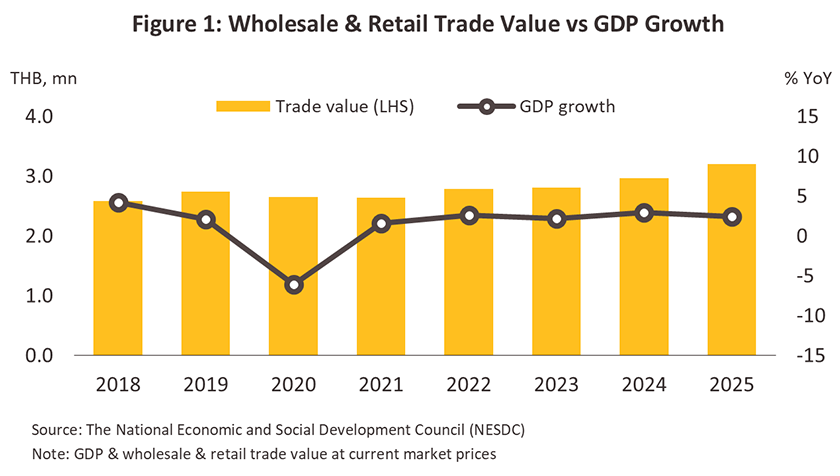

The modern trade industry falls within the broader wholesale and retail sector, which had a combined value of THB 3.2 trillion in 2025 (Figure 1), representing 16.4% of GDP. This made it the second-largest contributor to the Thai economy, behind only manufacturing, which had a 28.6% share of GDP. Modern trade players are generally major corporations that operate extended commercial networks, and because they buy in such large quantities, their market strength and negotiating position outweighs that of manufacturers and distributors1/. Stores are managed using modern logistics and distribution techniques, and players are in the process of leveraging a greater use of modern technology and an expanded online presence for the advantages that this provides to their marketing.

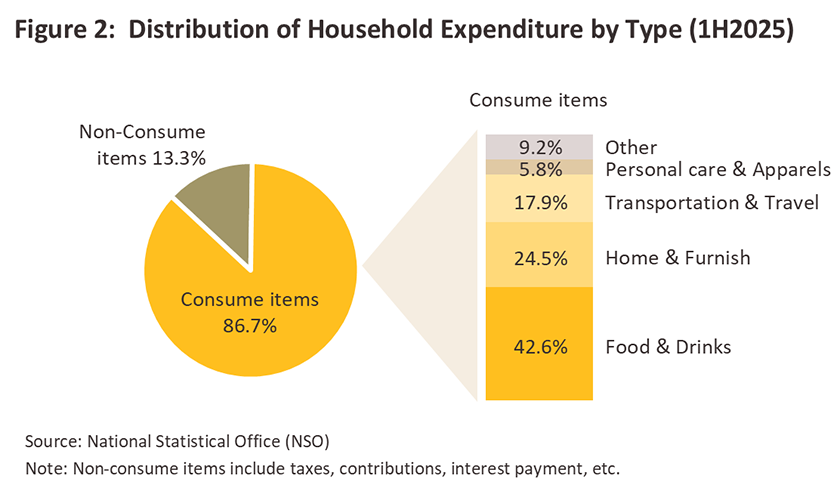

Modern trade outlets have enjoyed rapid growth in Thailand, especially in and around Bangkok, tourist areas, and other more urbanized parts of the country. Success has been built on: (i) government policy to allow foreign players that have access to modern management and operational technology to invest in the retail sector2/; (ii) catering to consumers who spend around 40% of their total expenditure on consumer goods on food and drink (Figure 2) and who favor retailers offering a unified shopping experience under a single roof that extends over food, personal care items, and household goods that are generally cheaper than equivalent goods sold in traditional outlets; and (iii) ongoing investment in expanding retailers’ customer base through the opening of new branches.

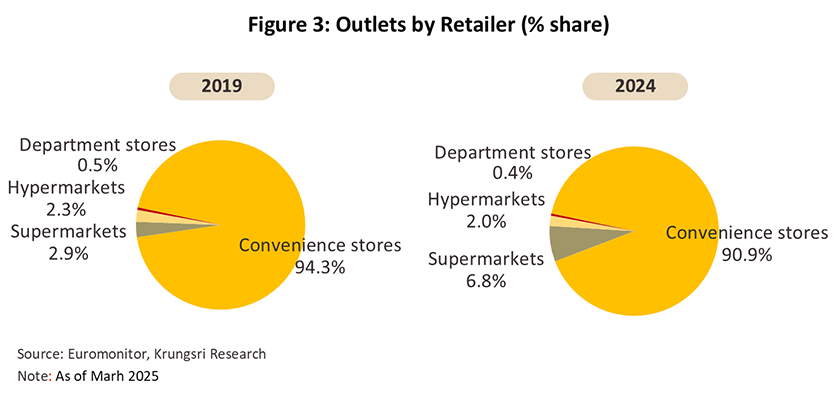

Operators have been steadily expanding their branch networks across different types of sites, including in community malls, service stations, and in areas that serve a large number of residential communities or that experience heavy traffic. Players have also been adjusting their branch sizes to make these more suitable for individual locations or particular consumer groups, and so as of 2025, there were 20,000 modern trade outlets open in Thailand, though more than 90% of these were convenience stores (Figure 3). Most operators continue to attract customers through price cuts, with many also pursuing O2O 6/ (online to offline) strategies that use branch outlets as distribution centers supporting deliveries to consumers in the immediate area, and because this gets goods rapidly into the hands of buyers, it can help to stimulate sales further.

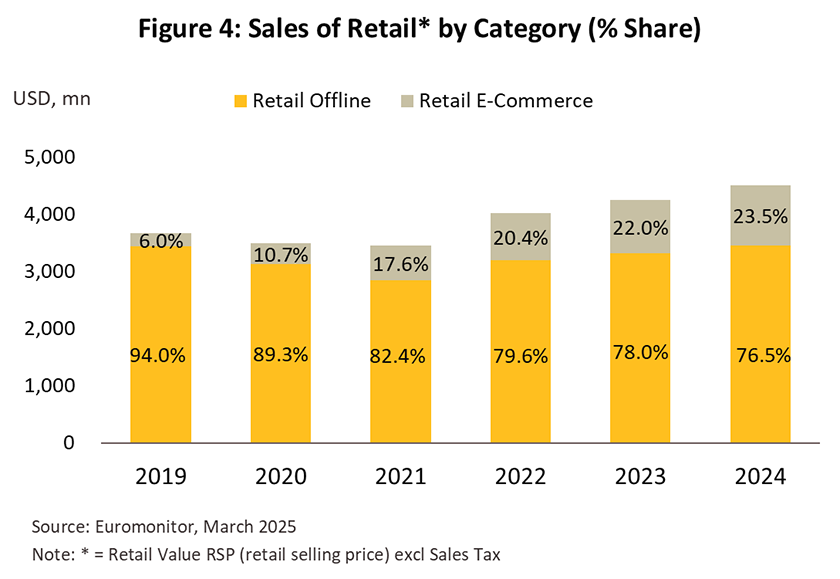

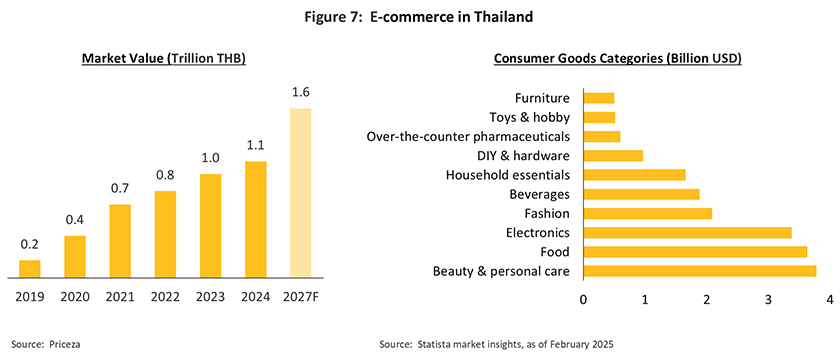

Competition within the modern trade retail business is quite intense. This results from high product similarity, a large number of branches, and the need to compete with the rapidly expanding retail e-commerce sector due to convenient access to smartphones and the internet. This is reflected in the 2024 data where the proportion of online sales accounted for 23.5% of total retail value compared to 6.0% in 2019, representing average annual growth of 36.8% (CAGR, 2019 - 2024). The online product categories with the highest growth rates are food with a 5.3% share of total online retail sales in 2024 growing at 38.0% per year , followed by health and beauty products with a 4.9% share at 35.5% per year, electrical appliances and electronics with a 13.1% share at 24.0% CAGR, and the fashion segment with a 7.6% share at 21.0% per year (Source: Euromonitor). Meanwhile, sales on marketplace e-commerce platforms, which represent 59.0% of all online sales, grew at 36.6% per year, making omnichannel commerce an essential strategy for operators seeking to increase sales

Situation

In 2024, the modern retail value reached THB 4.5 trillion, an increase of 6.0% from 2023 (Source: Euromonitor). Within this total, 76.5% originated from offline channels and 23.4% from online channels, with online retail sales growing rapidly by 379.0% compared to 2019, reflecting consumer behavior that prioritised digital channels for purchasing following the expansion of social media platforms.

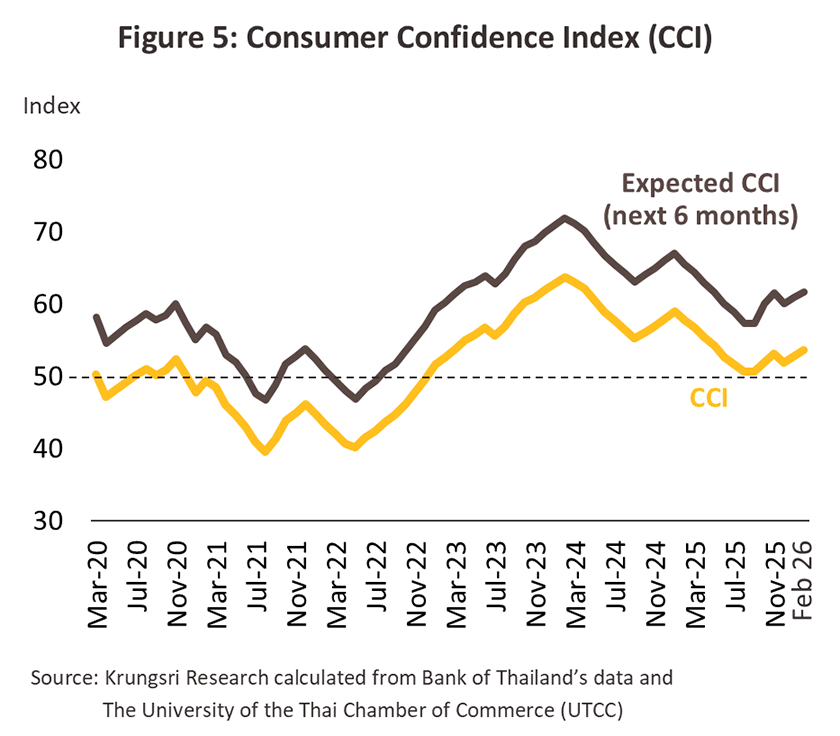

In 2025, the retail sector faced challenges from several factors. First, Thailand’s economic recovery remained fragile at 2.4%, slowing from 2.9% in 2024, while private consumption grew at 2.2% compared to 4.3% in 2024. This is due to purchasing power being undermined by household debt (86.8% of GDP as of 3Q2025) and a high cost of living, causing consumers to spend cautiously and become more price-sensitive. Particularly, the low-to-middle income groups chose to buy non-branded consumer goods which are cheaper than before and focused on basic necessities, consistent with the Consumer Confidence Index which continued to decline below 50.0 since June 2025 (Figure 5). Second, the tourism sector, a major driver of the Thai economy, grew more slowly. This is reflected by the number of foreign tourists to Thailand contracting -7.2% from 2024 to 33 million people, especially Chinese tourists (the highest shopping expenditure among all foreign tourists) which contracted -33.3% from 2024. Meanwhile, Malaysian tourists were affected by flooding in the southern region in late 2025. This weighed on retail sales for consumer goods retailers which rely on tourism, particularly convenience stores. Third, there was intensified competition from online retail businesses, including cross border e-commerce, which often stimulate sales through ease of search and promotional campaigns, giving consumers a wider range of product choices at various price levels. Fourth, there was an influx of cheap imported goods from China through small retailers including Chinese supermarkets, covering food and beverages, low-cost electronics and home appliances, mobile accessories, home decor, and fashion items, which captured market share from Thai modern trade businesses at a time when consumer purchasing power was limited. Fifth, the temporary closure of retail branches near the Thailand-Cambodia border (such as Surin, Buriram, and Sa Kaeo) affected sales in those areas.

However, the retail sector continued to benefit from several supporting factors. These included (1) government spending stimulus measures such as the Easy E-Receipt Project (January 16, 2025-February 28, 2025), the Digital Wallet Phase 2 (January 27, 2025-April 28, 2025), and the Khon La Khrueng Travel project (July 1, 2025-October 31, 2025). Specifically, the year-end consumption stimulus measures including the Khon La Khrueng Plus (October 29, 2025-December 31, 2025) and the Travel Well Get Refund measure (October 29, 2025 to December 15, 2025) helped stimulate sales and supported domestic spending, (2) the purchasing power of the middle-to-high income consumer group continued spending on consumer goods, though they slowed spending on beauty and luxury items or shifted toward value-for-money products. Furthermore, the 33 million foreign tourists in 2025 helped sustain retail sales in certain categories like food, beverages, and lifestyle products, especially in major tourist cities. (3) retail operators expanded their competitiveness by developing e-commerce, quick commerce5/, and local express delivery services alongside physical store sales, enabling them to maintain their customer base. This is consistent with the 11M2025 average Online Purchase Index, covering mail, television, telephone, and internet orders, which expanded 93.1% YoY. Priceza (operator of Priceza.com) estimated that Thailand's e-commerce market value grew 7.6% from 2024. Finally, (4) branch expansion continued in high-potential areas, particularly tourist destinations, suburban areas, and along mass transit routes following urban expansion (e.g. outer Bangkok, Bang Na-Srinakarin, Ram Inthra-Watcharaphon, Rangsit-Khlong Luang, and the Pink and Yellow Lines). Expansion also reached secondary cities (e.g. Khon Kaen, Udon Thani, Hua Hin, and Southern Chiang Mai – Hang Dong, San Kam Pang) where real estate projects were developed, leading modern trade operators to open branches to serve customers who prefer shopping near their residences. These factors contributed to total sales of modern trade retailers growing by around 2.5-3.5% from 2024, particularly for consumer goods in convenience stores and supermarkets.

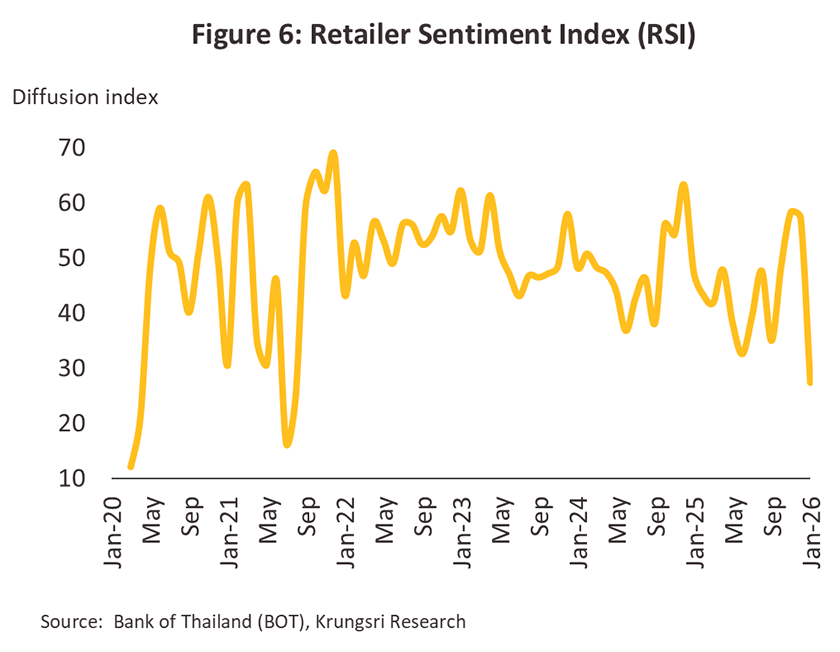

Retail operators are concerned about the fragility of purchasing power amid geopolitical tensions and trade wars which continue to weigh on the spending environment. The Retailer Sentiment Index (RSI) remained below 50.0 continuously since January 2025; however, government stimulus projects and year-end festival helped lift retail sales somewhat, causing the index in November to flip above 50.0 for the first time in 2025 (Figure 6). Due to intense competition and weakening purchasing power, operators moved quickly to adjust their marketing strategies to maintain revenue, such as more frequent promotional campaigns, price reductions, cost controls, and branch expansions. They also adapted business models to meet changing consumer behaviors, such as expanding rental spaces in hypermarkets to attract customers and increasing fresh food offerings and store sizes for convenience stores to resemble mini-supermarkets.

The 2025 modern retail situation can be summarized by segment.

Department stores: the slowdown in foreign tourists has affected premium product sales.

-

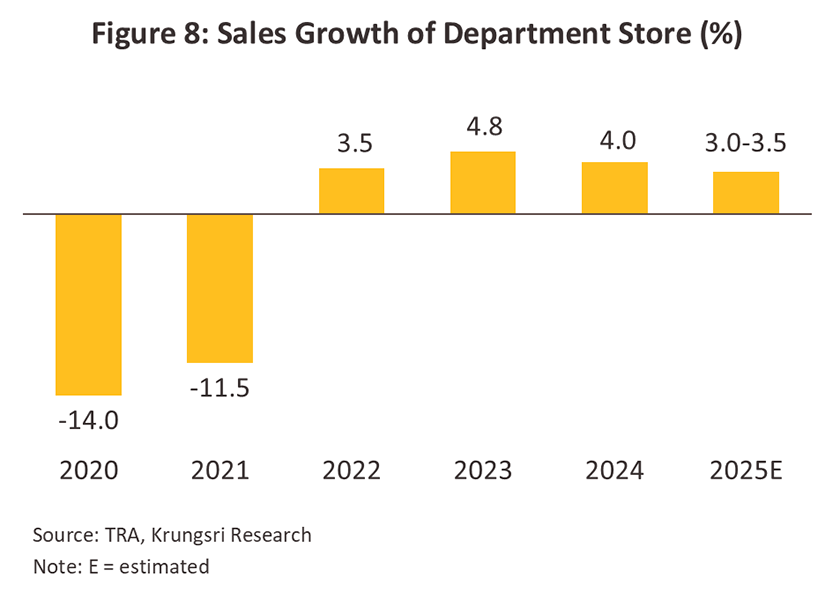

Sales growth slowed to 3.0-3.5% from 2024 (Figure 8). The business continued to support by high-purchasing middle-to-upper income customers and marketing strategies such as expanding luxury zones to attract target customers, sourcing unique authentic products, and adjusting rental spaces to align with new trends (e.g. luxury pop-ups and health and wellness zones). However, economic uncertainty caused more cautious spending, while purchasing power from foreign tourists, especially high-spending Chinese tourists, had not fully recovered, especially on core department store categories (brand-name goods, cosmetics, and health products). They also faced intense competition from online channels, global brand stores opening directly in Thailand, especially in Phuket to serve high-spending travelers from around the world, and international lifestyle stores (e.g. OH!SOME, a comprehensive retail brand popular in Singapore and Malaysia), all of which constrained sales growth.

-

Operators adjusted online strategies to attract customers through Super Apps, mobile platforms, and social media promotions to create targeted shopping experiences, developing virtual shopping (AR/VR-based immersive purchase experiences), and building personalized shopping journeys for premium customers.

-

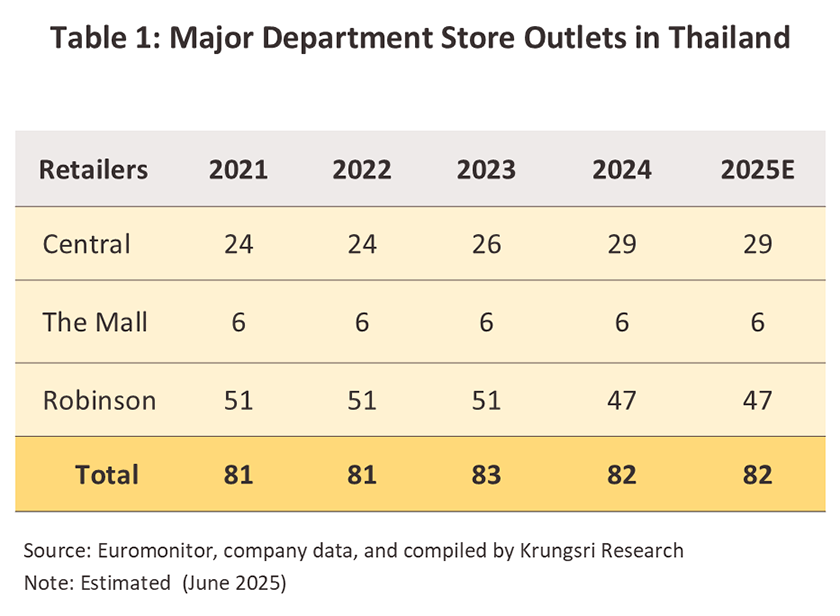

Large operators continued to expand branches, especially in tourist provinces (e.g., Central Krabi opening in October 2025), and adjusted formats toward shopping centers to increase rental income and partnering with other businesses such as tourism operators (Table 1).

Discount stores/hypermarkets: Sales are pressured by stagnant consumer purchasing power.

-

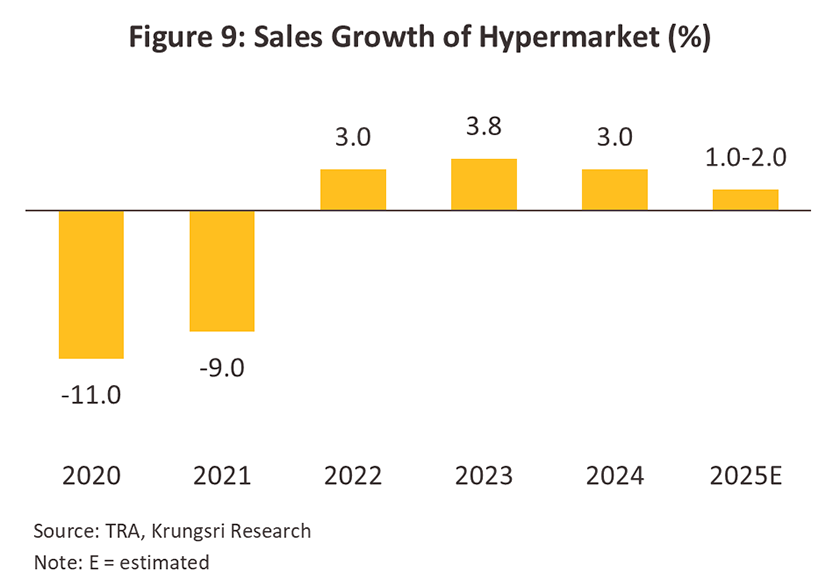

In 2025, sales are projected to grow modestly by 1.0-2.0% from 2024 (Figure 9) due to continued demand for fast moving consumer goods (FMCG) and indirect benefits from government stimulus. However, the core mid-to-lower income base had limited purchasing power and spent more cautiously, buying smaller quantities from nearby convenience stores instead of bulk buying, and using online channels, which offers easy access, fast delivery (e.g., within 1 hour or same-day) and easy price comparison. As a result, operators rapidly adjusted models to attract customers: Big C shifted to "Mini Hypermarkets" with smaller sales areas for better accessibility, compared to traditional branches, while Lotus’s developed models similar to supermarkets (Lotus’s Go Fresh Supermarket) by adding quality products and imported fresh food to serve high-purchasing power groups. Additionally, the merger between Makro and Lotus’s helped improve cost management efficiency.

-

Operators have driven growth by developing robust omnichannel strategies to connect directly to consumers who increasingly prefer online shopping. Furthermore, they have collaborated with partners (such as GrabMart, and LINE MAN) to develop end-to-end Quick Commerce services, while some operators have partnered with platforms (such as Lazada, Shopee, and Facebook Live Commerce) to boost sales. In addition, there is a strong focus on using Data Analytics for deep consumer insights and implementing loyalty programs/ membership systems to drive repeat purchases.

-

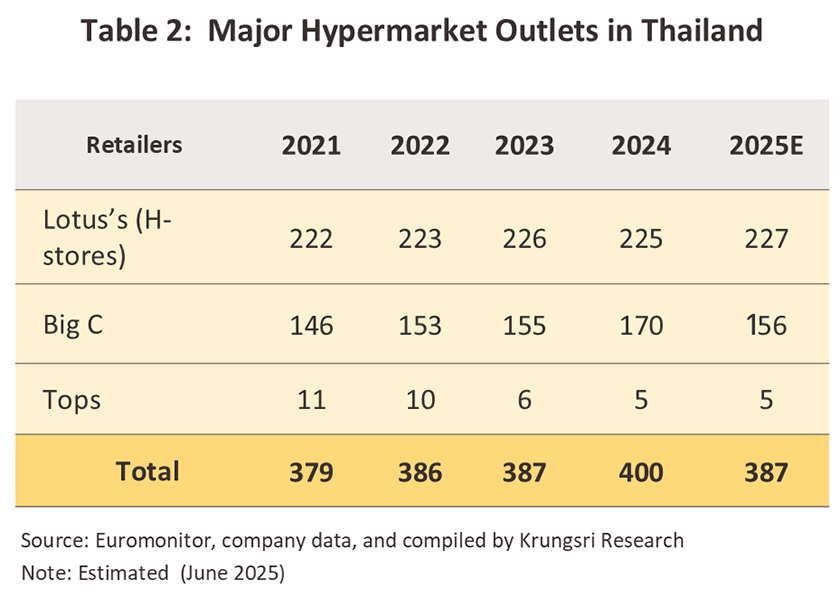

Operators continued to expand branches domestically and abroad (Cambodia, Laos, and Vietnam) to maintain revenue. In Thailand, they planned smaller store models (4,000 square meters) for urban locations and shopping center formats (40,000-50,000 square meters compared to 25,000-30,000 square meters for hypermarkets) in certain areas (e.g., CBD and city centers) to attract high-spending consumers and increase rental, encouraging customers to spend more time in-store (Table 2).

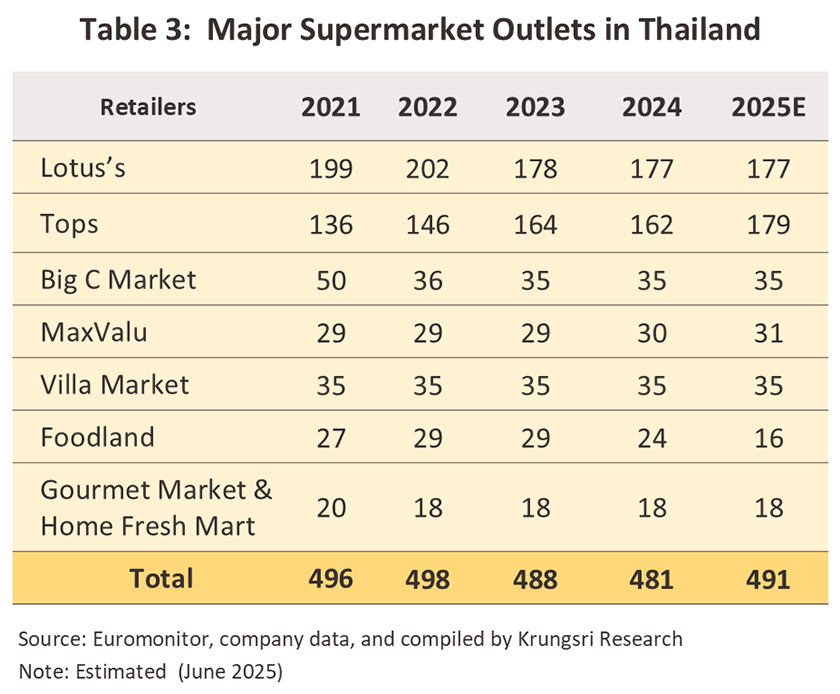

Supermarkets: Continued growth from high-purchasing power customers.

-

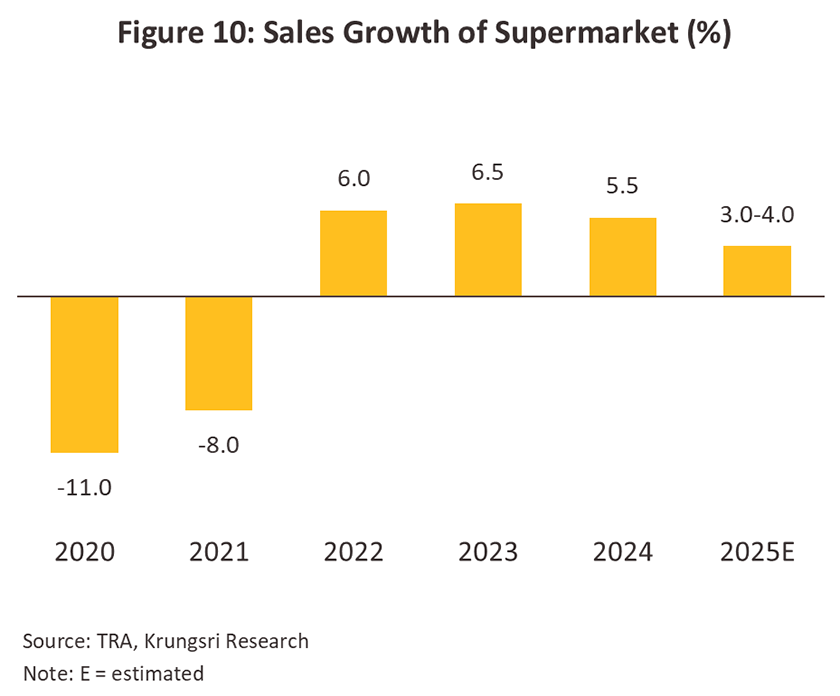

In 2025, sales are estimated to grow 3.0-4.0% from 2024, the highest among all segments (Figure 10), Growth is driven by purchasing power from mid-to-high income and foreign customers, who represent a stable customer base and are less affected by the economic slowdown. In addition, the segment’s strengths include trust in product quality, especially fresh food, premium imported products, organic products, and health food. Operators have different focuses: Tops Market (Central Retail Group) increased share of organic and high-quality local products for urban health trends; Gourmet Market (The Mall Group) opened "Eat Well – Live Well" zones emphasizing for plant-based and premium imports; Foodland modified some branches to "Foodland Grocerant" to generate additional revenue from freshly cooked food services.

However, the segment faces intensifying competition from other retail segments that are developing models similar to supermarkets (such as Lotus’s Go Fresh, which focuses on high-quality products and premium fresh food). Competition also comes from players within the same segment, both domestic and international (such as Dear Tummy, a Thai supermarket in ICONSIAM, and LOPIA Japan, a Japanese supermarket with plans to open four branches in 2026)—as well as online supermarkets (such as LazMart, which consolidates a wide range of consumer goods on a single platform and offer rapid delivery services).

-

Operators enhanced services through technology to improve consumer convenience such as smart shopping carts with touchscreens for promotions and price calculation, and self-checkout machines to speed up payment processing. They also partnered with suppliers across the supply chain in various countries to expand the share and variety of imported goods, particularly health and functional foods, to differentiate themselves from other retail formats.

-

Operators expanded branches into new residential areas and high-purchasing-power tourist provinces, including locations along suburban mass transit routes (such as Ramintra, Min Buri, and Ratchaphruek) and sites near residential communities, as well as key tourist provinces such as Phuket — driven by luxury real estate development — and Surat Thani (Koh Samui). This supported continued sales growth underpinned by a diversified customer base comprising both Thai and foreign consumers. Among large operators, Gourmet Market planned to open one to two new branches in 2026 with a greater emphasis on stand-alone store models (Table 3).

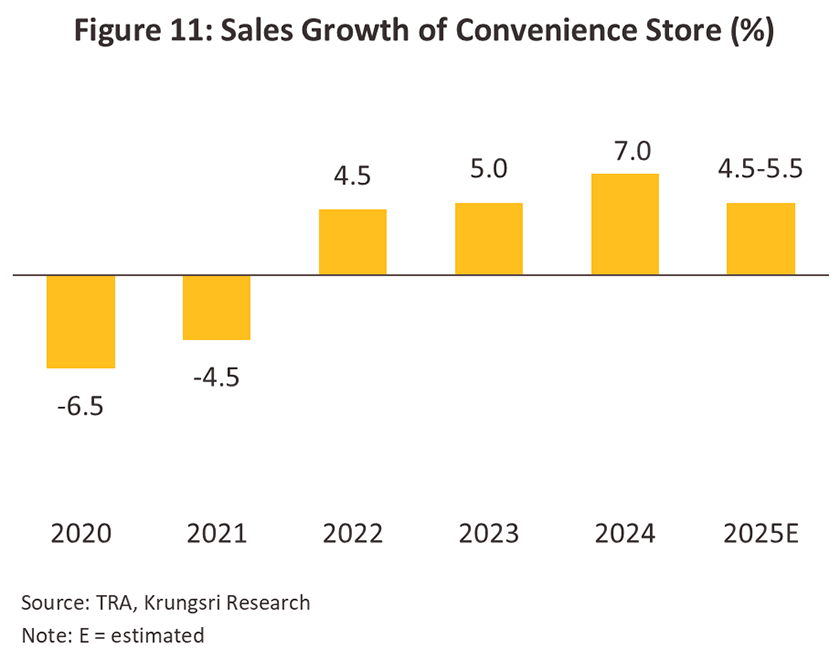

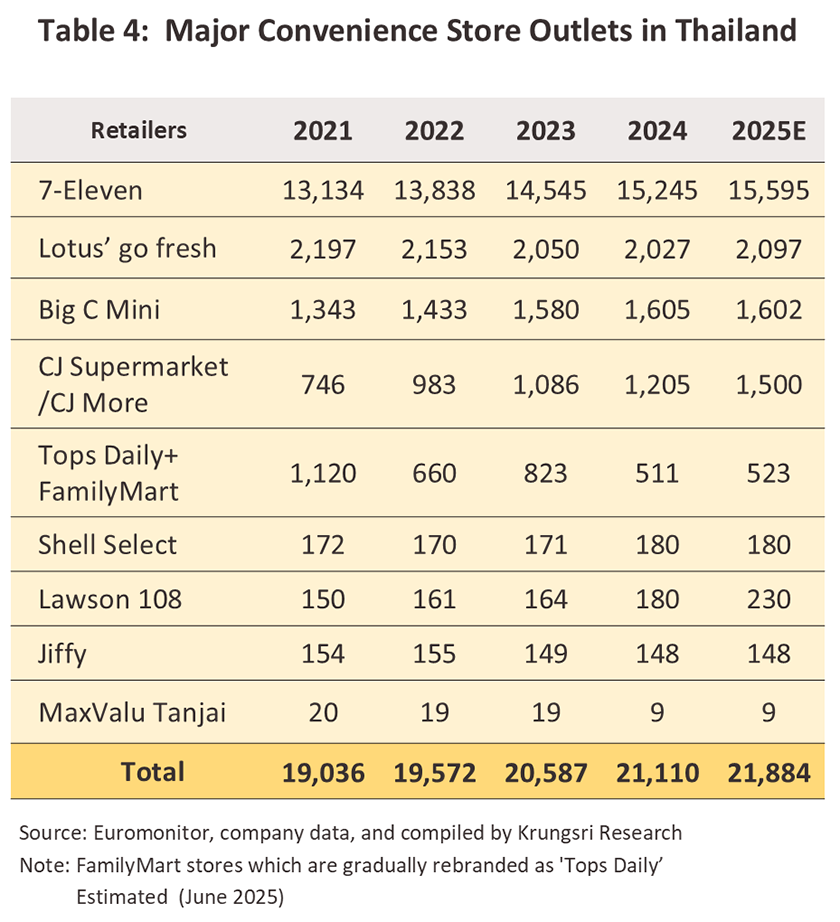

Convenience stores: Growth continued from branch expansion covering customer groups.

-

In 2025, sales grew 4.5-5.5% from 2024 (Figure 11), driven by operators’ ability to meet the needs of time-pressed consumers who preferred buying daily necessities, especially food and beverages, at nearby stores, with a "small basket, quick trip" spending behavior. Some operators expanded household product sections (e.g., cooking ingredients and snacks, mops, plates, bowls, and towels) and enlarged select branches into a "Compact Supermarkets" format with parking and a wider product range, which indirectly encouraged consumers to shop closer to home and reduce travel. In addition, the segment also benefitted from the tourism sector which boosted traffic at branches in tourist destinations and major cities. However, sales per branch showed a downward trend due to weakened purchasing power.

-

Large operators developed comprehensive omnichannel ecosystems by adding in-store services to drive traffic and frequency, such as real-time delivery and pre-order/pick-up services, using data analytics to design personalized promotions and connecting quick commerce services to external delivery platforms. Consequently, online sales proportions rose; 7-Eleven’s online sales accounted for an average of 11.0% of total sales, up from 3.0% and 8.0% in 2020 and 2021, respectively. Lotus’s Go Fresh developed the Lotus’s Smart App and partnered with Grab and LINE MAN (1H2025 online sales increased 33.5% YoY, Source: CPAXTRA Report 2025), and Tops Daily recorded average online sales growth of 25.0-28.0% per year through Tops Online (Source: Central Retail 2025 Strategy Update).

-

Operators increased branch density to reach customers by expanding branches into high-potential locations such as airports, mass transit systems (BTS/MRT), hospitals, and office buildings. 7-Eleven has maintained a target of 700 new branches per year, while Big C Mini planned to open branches of 300-square-meter (sq.m.) up from 200 sq.m. for the first time in April 1, 2026, with a total of 200 stores in 2026 and 300 in 2027. Lotus’s planned to expand its Go Fresh concept as a mini-supermarkets format to reach more communities, Tops Daily targeted 8-10 new branches per year, and CJ Express planed 600 branches in 2026 from 1,900 in 2025. Mini Big C gradually closed underperforming branches (approximately 170 closures in 2025) (Table 4).

-

Competition intensified as retailers from other segments developed smaller models to more effectively target customers, such as Lotus’s SAVE+ (opened in 2025), a small-format store model focusing on low-priced daily necessities (excluding fresh food) with fast inventory turnover and house brand products. Some operators built modern mom-and pop networks (low-cost convenience stores) reaching consumers at the sub-districts and villages, such as Thuk Dee Mee Mattrathan stores (TD Tawan Daeng Group) with approximately 8,000 branches, Don Jai (Big C) with 19,844 branches, Buddy Mart (Makro) with 2,000 branches, and Ran Nee Khai Dee (Lotus’s) targeting 30,000 branches by 2027. Consequently, convenience store operators pursued partnerships with businesses in other sectors to differentiate their offerings, such as CP Group-IKEA-Decathlon collaboration, which launched the "Future Convenience Store" (the first branch in Chiang Mai) and plans to expand the format to other locations nationwide, tailoring brand offerings and services at each branch to align with the needs of local customers.

Outlook

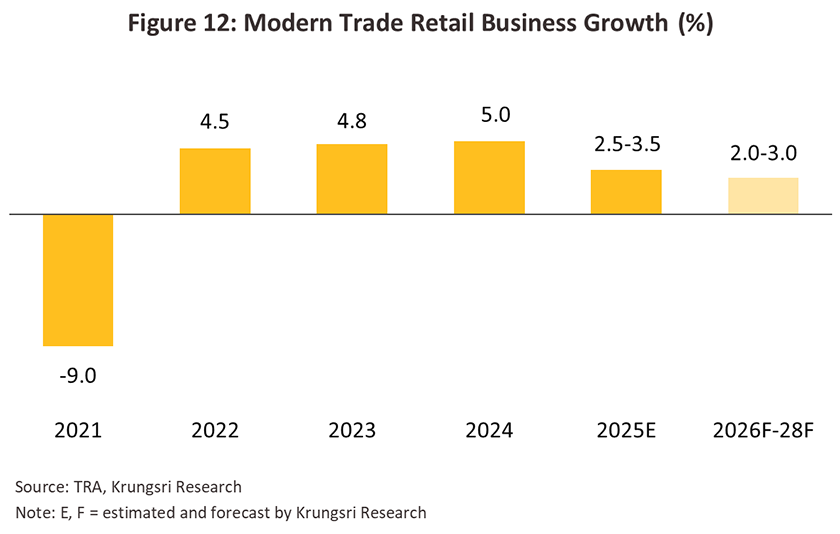

In 2026, modern retail businesses face challenges from global economic volatility and a more fragile Thai economy, which is projected to grow below 2.0%, down from 2.4% in 2025. Amid rising energy prices resulting from tensions in the Middle East, the cost of living is trending higher accordingly, leading consumers to become more cautious with spending. This is particularly true for middle-to-lower income groups pressured by household debt issues who will focus primarily on essential goods and value for money, driving the Retailer Sentiment Index (RSI) in January to its lowest level in 4 years and reflecting intensified concerns regarding sales. However, it is expected that middle-to-upper income consumers will be the group helping to sustain sales from a severe decline, while the government is likely to continuously issue economic stimulus policies following the government formation, including accelerating budget disbursements to oversee the economy. These aforementioned factors will help support sales of goods, especially in the food and beverage category, while products with good growth trends include ready-to-eat meals, daily necessity groups, and health and beauty products. Krungsri Research forecasts overall sales of modern trade retailers to grow 1.5-2.5%, slowing down slightly from 2025, while in 2027-2028, sales are expected to improve at an average level of 3.0-3.5% per year (Figure 12) due to several supporting factors.

1) Domestic purchasing power is likely to recover gradually in line with the Thai economy, which is expected to grow at an average of 2.0-2.5% per year, while the tourism sector will benefit from foreign tourist arrivals increasing to 35.5 million people by 2028. Continuous large-scale infrastructure development according to government plans will stimulate regional economic circulation, increasing income and purchasing power to support the continuous growth of modern trade sales.

2) The expansion of communities following government infrastructure development increases market opportunities for retailers to expand branches to outskirts of Bangkok and provinces, such as the Orange Line (Thailand Cultural Centre–Min Buri) supporting the opening of shops in the eastern zone around Ramkhamhaeng–Rom Klao, and the South Purple Line (Tao Poon–Rat Burana) stimulating branch expansion in the Thonburi side. For the double-track railway phase 2 (Lop Buri–Pak Nam Pho, Nakhon Pathom–Chumphon, Thanon Chira Junction–Ubon Ratchathani), as well as Special Economic Zone projects in border provinces such as Tak, Nong Khai, and Sadao, will support the opening of retail stores in regional provinces.

3) The (draft) new Bangkok Comprehensive Land Use Plan (4th revision), which is under preparation and expected to be announced in 2027, will expand residential and commercial land use in certain areas such as Ratchayothin and Lat Phrao-Ram Intra, which will be adjusted from medium-density to high-density residential use, while the Wongwian Yai-Suksawat area will be adjusted from low-density to medium and high-density, increasing opportunities for branch expansion and sales for retail stores in suburban communities.

4) The economic growth of neighboring countries, with the IMF forecasting CLMV economies to grow between 2.0-4.8% per year, will support retail sales growth in regional border provinces and regional hubs from the purchasing power of local consumers, nearby provinces, and neighboring countries, as well as increase opportunities for operators to expand branches in neighboring countries.

Modern retail operators are expected to continue expanding branch networks, renovating existing outlets, and developing new business models to enhance revenue per square meter. Key strategic adaptations include:

1) The development of integrated online and offline channels (Omnichannel) has become a core infrastructure for sustaining sales growth. Leveraging advanced technologies—such as AI, machine learning, and big data—enables deeper analysis of consumer behavior and demand, allowing more precise customer targeting and personalized marketing to strengthen engagement. Retailers are also increasingly collaborating with partners (e.g., offering parcel drop-off and pick-up points). A survey by KEX Express indicates that younger consumers prefer sending parcels while visiting convenience stores or shopping for household goods. E-commerce in Thailand is projected to grow at an average of 7–9% annually. For instance, Priceza estimates the market will reach THB 1.2 trillion in 2026, expanding by 7% year-on-year, while Euromonitor forecasts retail e-commerce to grow by 9% annually during 2024–2029, with its share rising from 27% in 2025 to 32% by 2029. This growth is driven by consumer preferences for convenience, speed, and seamless omnichannel experiences. A 2025 survey by DoubleVerify found that 38% of Thai consumers use social media platforms to research products before purchase, 50% complete purchases directly on these platforms, and 40% expect to spend more time on social media over the next 12 months. This underscores the importance for retailers to strengthen online channels alongside offline operations. Looking ahead, “instant commerce”—ultra-fast delivery within short timeframes (e.g., 30 minutes)—is emerging as a key trend and may become a new standard, potentially increasing the share of online retail sales relative to total sales.

2) A stronger focus on developing new products and service formats is expected to better align with the growth of local communities and the transition toward an aging society, where consumption patterns and needs differ. This includes “senior-friendly” products (e.g., easy-to-open packaging, larger fonts, easy-to-digest food, and ergonomic items), “age-friendly” store designs (e.g., flat flooring and seating areas), and targeted services such as senior care commerce.At the same time, retailers are adapting to increasingly value-conscious consumers by offering quality products at more accessible prices and expanding the share of private label products.

3) Expanding investment into overseas markets is a key strategy to diversify revenue streams, particularly in Vietnam which offers strong growth potential, is a key strategy. For example, TCC Group aims to increase its international sales contribution to 20–40% by 2027, while Big C and Lotus’s Go Fresh plan to expand in Laos and Cambodia, and 7-Eleven continues to grow its presence across CLMV markets.

Business challenges in the next period include: (1) slow economic growth in Thailand amid high household debt curbing consumer purchasing power, combined with global economic uncertainty and conflict in many areas affecting the spending of Thai and foreign consumers, while the tourism sector may recover more slowly. (2) intensified business competition from existing and new operators gradually entering the market, such as LOPIA JAPAN which plans to open 20 branches in Thailand by 2028, and online operators, especially Chinese platforms like Temu, Shein, and AliExpress expanding warehouses in the EEC, as well as an increasing number of C2C Market operators causing modern trade market share to likely decrease to some extent; (3) cheap products from China flowing in to compete in the Thai retail market both directly and indirectly; and (4) the burden of technology investment and the transition to ESR (Economic-Social Responsibility Retail). Examples include CPALL (7-Eleven) with the “7 Go Green” project installing solar roofs in over 3,000 branches and reducing single-use plastic; Lotus’s installing Solar Rooftops and energy-saving cooling systems in over 400 branches while changing packaging to biodegradable materials; and Central Retail developing “Green & Circular Malls” with waste and wastewater management systems according to international standards and preparing to use Extended Producer Responsibility (EPR) measures in 2027.

Krungsri Research assesses investment opportunities for modern trade businesses classified by

1/ One reason why large modern trade operations are able to offer goods at price points below those of traditional retailers is that they are in a position to collect fees from manufacturers and distributors wishing to sell through their shops. Sources of income include: (i) initial fees for stocking new lines; (ii) charges for marketing and other services, e.g., for hosting display stands, access to shelf space, signage, bonuses in the case that sales exceed monthly targets, and the transport and logistics fees incurred in shipping goods from distribution centers to stores; (iii) the fees for producing leaflets and flyers, as well as the provision of free or additionally discounted goods on special occasions (e.g., New Year, the opening of new branches, store renovations and re-openings, and during festivals); (iv) credit terms that extend to 90-120 days; and (v) contracts that allow players to terminate business relations unilaterally.

2/ The 1999 Foreign Business Act allows non-Thais to operate in the retail and wholesale industries (reserved occupations as per Appendix 3 of the Act) if they invest at least THB 100 million in Thailand. Potential investors must also apply for a license from the Foreign Business Committee.

3/O2O Marketing is a business model that blends the strengths of online and offline sales channels to elevate service quality, boost revenue and expand the customer base.

4/ A Marketplace is an online platform that brings multiple sellers together in one place, allowing buyers to browse and purchase a wide variety of products from different sellers. Popular examples include Shopee, Lazada, Kaidee, and LINE Shopping.

5/ Quick Commerce (Q-Commerce) focuses on delivering products to customers in the shortest time possible — typically between 10 minutes and 1 hour — meeting the demands of consumers who want goods and services instantly.

6/ Source: PwC’s Voice of the Consumer Survey 2024

.webp.aspx)