EXECUTIVE SUMMARY

The new sales and leases of land in industrial estates during 2026-2028 are projected to grow at an average rate of 3.0-4.0% per year, equivalent to approximately 7,000-7,300 rai annually, supported by (i) the ongoing relocation of foreign investment, particularly from China and Japan, toward ASEAN, including Thailand, as firms seek to mitigate risks associated with trade barriers and supply chain disruptions, (ii) continued infrastructure investment, especially in the EEC, although new project rollouts may remain delayed in 2026 following the transition to a new government, with several projects approved in 2025 expected to gradually progress, and (iii) the anticipated rollout of investment incentives by the Board of Investment (BOI) on a continuous basis. However, businesses are expected to face several headwinds that may constrain growth. Prolonged conflict in the Middle East could delay investment decisions, while foreign investors are increasingly diversifying across multiple ASEAN countries. At the same time, Thailand is beginning to lose its competitive edge in attracting investment, particularly to Singapore and Malaysia, which offer more advanced technological infrastructure.

Krungsri Research view

-

Industrial estates in the eastern region: Revenue is expected to grow more prominently than in other regions, with strong demand for land sales and leases supported by infrastructure investment linked to the EEC across three key provinces—Chonburi, Rayong, and Chachoengsao. These developments are likely to attract both domestic and foreign investors, particularly in government-promoted target industries. However, new supply (including newly developed areas and expansions of existing estates) is expected to remain relatively limited, as land prices continue to rise and high-potential plots are becoming increasingly scarce.

-

Industrial estates in the central region: Revenue is projected to continue growing at a solid pace, particularly from utility service revenue and rental fees, given the region’s transportation and logistics advantages over other areas. Meanwhile, estate expansion remains somewhat constrained, as high-potential locations are largely concentrated in Bangkok, Samut Prakan, Ayutthaya, and Saraburi.

-

Industrial estates in other regions: Revenue is expected to remain relatively stable, in line with subdued demand for land sales and leases. Growth in these areas continues to depend on further government policy support, especially infrastructure development such as cross-border transportation links. As a result, industrial estates in these regions are likely to expand at a slower pace than those in the Eastern and Central regions, leading to more limited revenue growth.

Overview

The industrial estate business involves the development and allocation of land for sale or lease to support industrial and commercial operations, together with the provision of essential utilities and infrastructure services, such as electricity, water supply, flood prevention systems, and centralized wastewater treatment.

Industrial estates are regulated by the Industrial Estate Authority of Thailand (IEAT) and can be classified into i) estates owned and operated by the IEAT, and ii) estates jointly owned and managed by the IEAT and private operators. In addition, there are businesses with similar characteristics—namely industrial parks and industrial zones—which are privately owned and managed. These are supervised by the Board of Investment (BOI), with the Department of Industrial Works and the provincial industry offices designated as the responsible regulatory authorities.

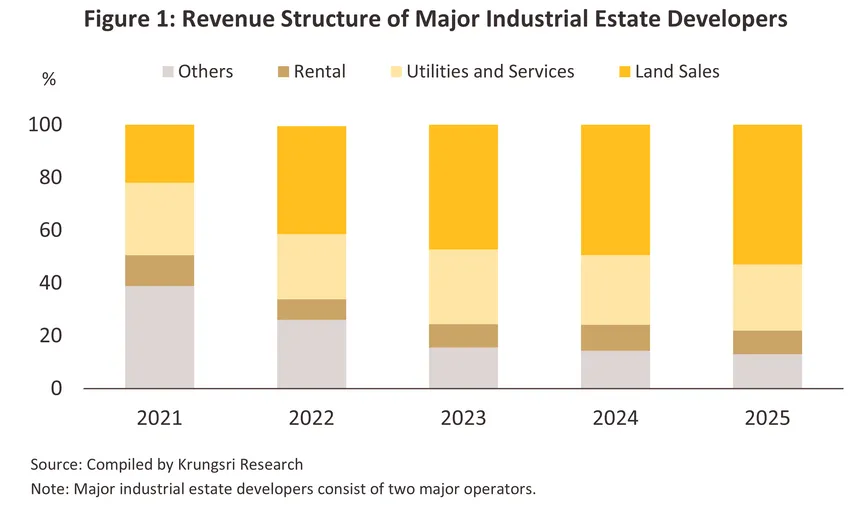

The main sources of revenue for operators of industrial estates and industrial parks/zones consist of two components: i) revenue from land sales and leases, and ii) revenue from related services, such as factory and warehouse rentals as well as utility services (e.g., electricity and water). The latter is classified as recurring income, which helps mitigate revenue volatility arising from fluctuations in land sales (the revenue structure of major industrial estate operators is illustrated in Figure 1).

Key factors why manufacturing operators tend to choose land within industrial estates or industrial parks/zones rather than investing in standalone plots outside designated zones are the availability of well-developed infrastructure, comprehensive utility services, and efficient logistics networks, as well as government incentives such as tax privileges and investment promotion measures. Major industrial estate operators include Amata Corporation Public Company Limited (AMATA) and WHA Corporation Public Company Limited (WHA Group), while leading industrial park/zone operators include Rojana Industrial Park Public Company Limited and Nava Nakorn Public Company Limited.

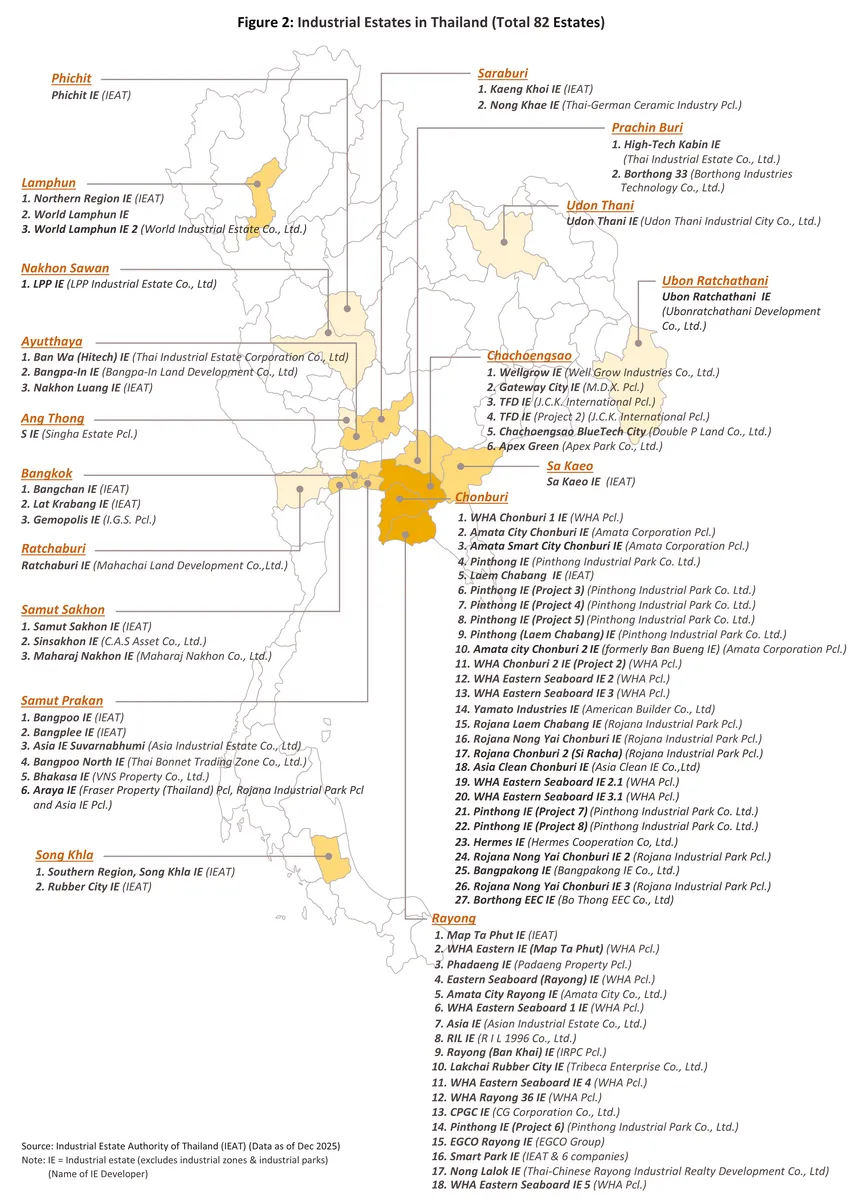

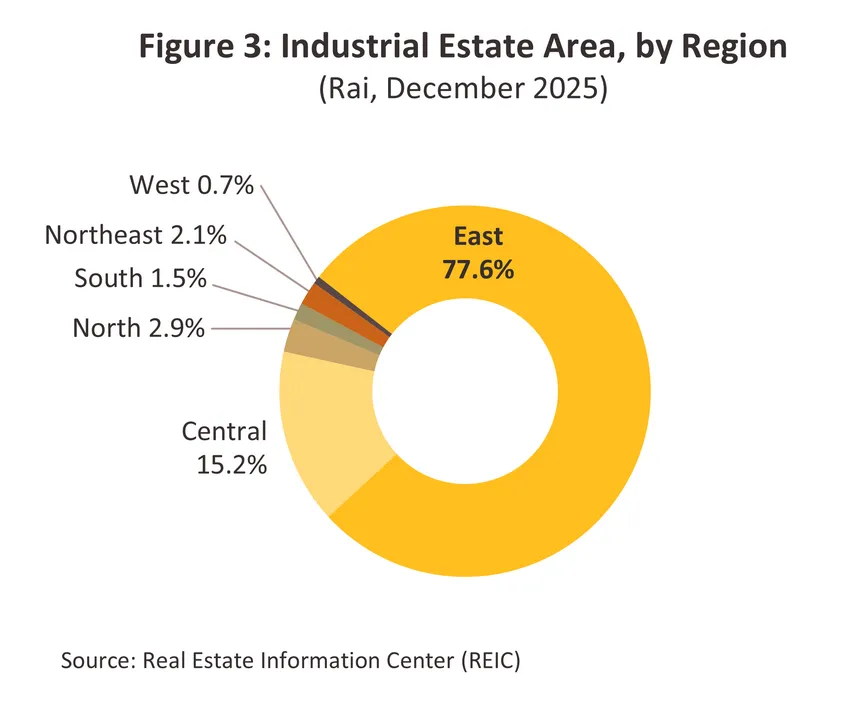

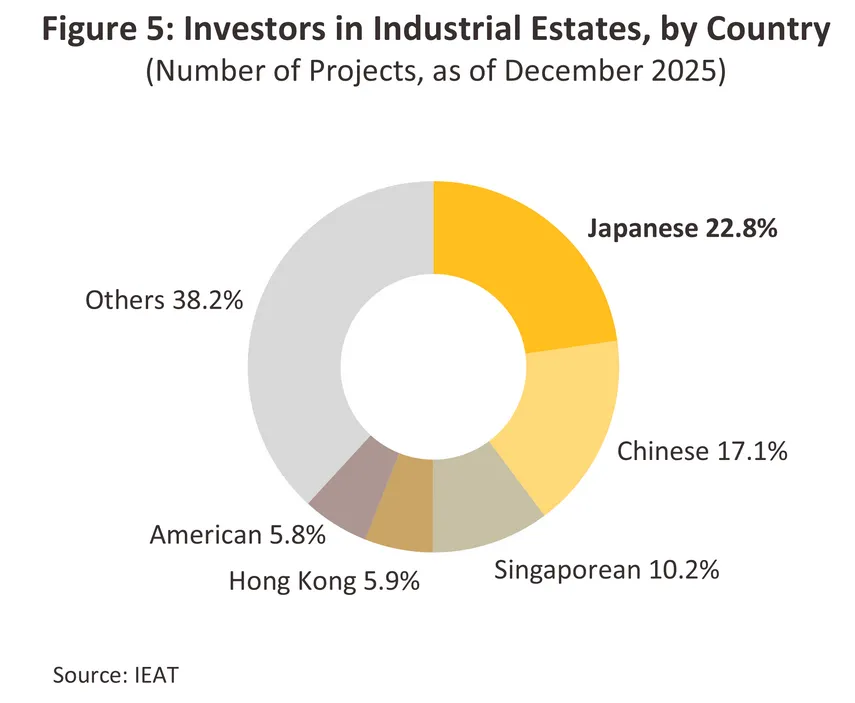

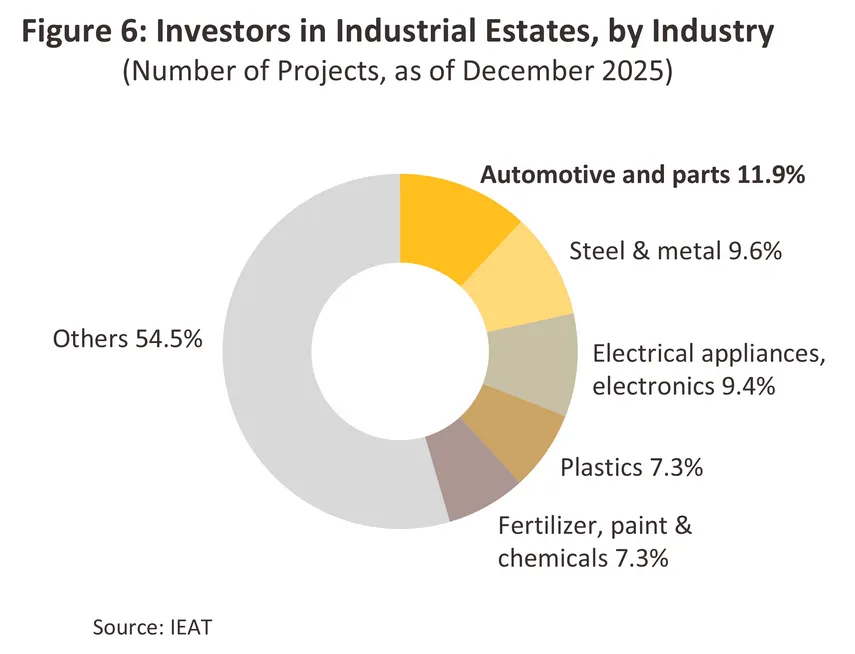

The main factors driving growth in the industrial estate business include i) global economic trends and domestic economic and political conditions; ii) multinational corporations’ policies to diversify their production bases and investment into Thailand; iii) the country’s physical and geographical advantages; and iv) government regulations and policies that support industrial investment, including additional privileges granted to investors within industrial estates. As of December 2025, Thailand had a total of 82 industrial estates located across 18 provinces (Figure 2), comprising 14 estates operated solely by the IEAT and 68 jointly operated with private partners. The majority of industrial estate areas are concentrated in the Eastern region, accounting for 77.6% of the total (Figure 3). In 2025, the cumulative number of investment projects in industrial estates was led by Japanese investors (Figure 5), followed by those from China and Singapore, respectively, while the automotive and auto parts manufacturing sector recorded the highest volume of investment nationwide (Figure 6).

The growth potential of the industry varies from area to area across the country. Details for individual regions are given below.

-

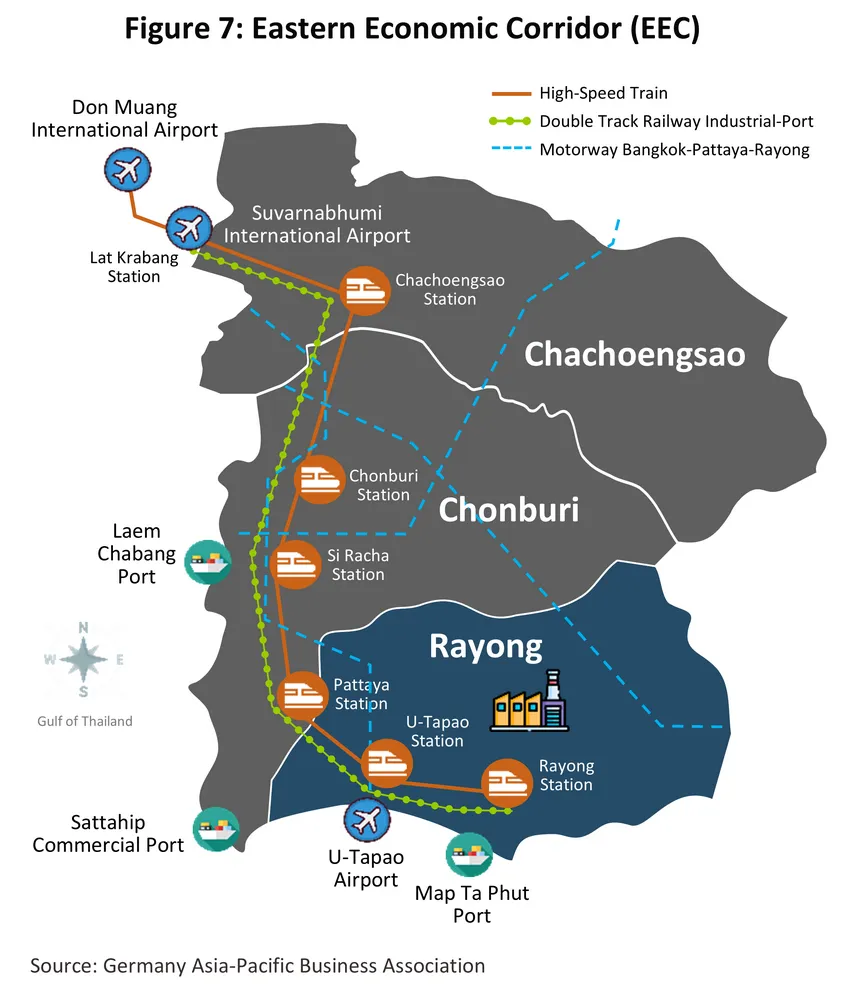

The eastern region: The Eastern region has the highest growth potential for industrial estates in Thailand, reflecting its role as the country’s primary manufacturing base under the Eastern Seaboard development framework. The region benefits from strategic location advantages and strong multimodal transport connectivity—by road, air, and sea—situated near Suvarnabhumi and U-Tapao international airports, as well as Laem Chabang Port and Map Ta Phut Industrial Port, while remaining within convenient distance from Bangkok. It serves as a hub for key industries such as petrochemicals, automotive and auto parts, electronics, and processed food, and has consistently received strong government support. Consequently, investment has been concentrated in the Eastern region more than in other parts of the country, particularly in Chonburi, Rayong, and Chachoengsao, which have been designated as the EEC area. These provinces are well equipped with infrastructure and positioned to attract investment in 12 targeted industries2/ that require high levels of capital and advanced technology, alongside the development of five special industry clusters3/ to align with Thailand’s evolving investment structure in the years ahead.

The EEC initiative continues to enhance the region’s attractiveness to investors, supported by large-scale public infrastructure projects aimed at strengthening connectivity and logistics efficiency. Key projects include i) the high-speed rail linking three airports, ii) the expansion of U-Tapao International Airport, iii) intercity motorways, iv) double-track railway development, v) Laem Chabang Port Phase 3, and vi) Map Ta Phut Industrial Port Phase 3.

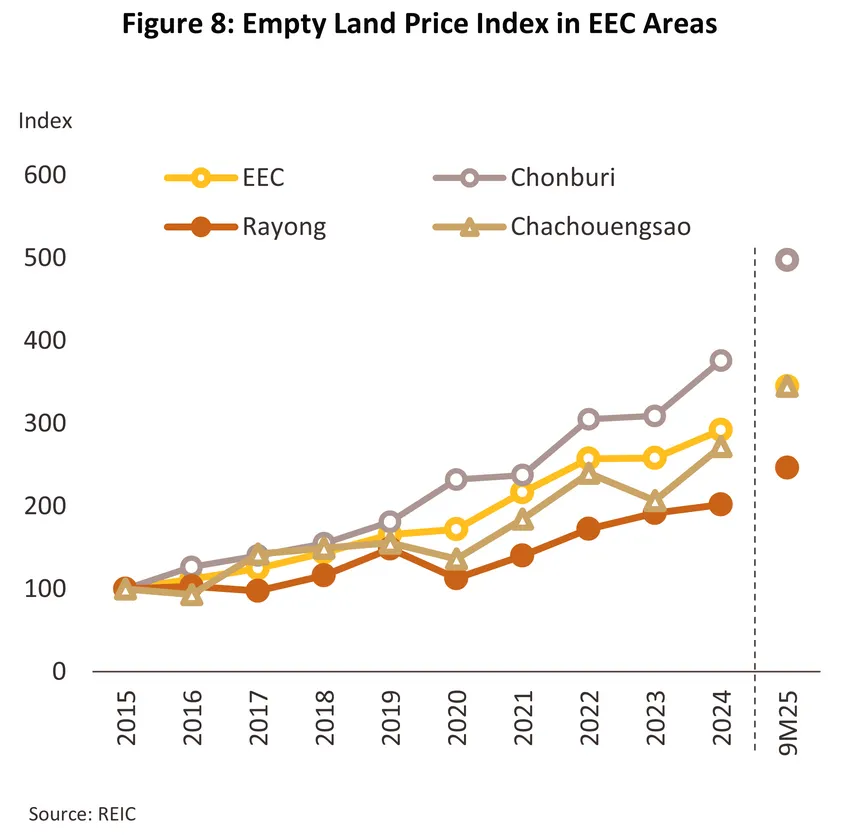

Strong policy support for large-scale public infrastructure investment has significantly driven up land prices in the EEC area (including land prices within industrial estates) compared with levels prior to the EEC’s development. According to data from the Real Estate Information Center (REIC), the empty land price index in the EEC area rose at an average rate of 14.1% per year (CAGR) during 2020–2024. Chonburi and Rayong recorded average annual growth rates of 12.8% and 15.7%, respectively. Meanwhile, in the first nine months of 2025, empty land prices in Chonburi surged by 41.3% YoY—well above the overall EEC average increase of 22.6% YoY (Figure 8).

-

The central region: The Central region benefits from strong locational advantages, serving as the country’s core hub for production, logistics, and transportation. It encompasses Bangkok, where industrial estates command the highest unit land prices nationwide, as well as key industrial provinces such as Samut Prakan, Ayutthaya, Saraburi, Samut Sakhon, and Ang Thong. Industrial estates in this region are characterized by a concentration of manufacturing industries with well-established supply chains and strong export linkages, including automotive parts, electrical appliances, and electronics. In addition, industries that rely on locally available resources—such as food and beverages, downstream petrochemicals, and construction materials—also maintain a significant presence.

-

The northern and northeastern regions: These regions have attracted comparatively limited investor interest, largely due to delays in major transportation infrastructure projects. Ongoing road development projects include Motorway No. 6 (Bang Pa-in–Nakhon Ratchasima), where civil works have been completed in 38 out of 40 sections (Source: Thailand Update, Feb 24, 2026). Rail connectivity projects linking Thailand with neighboring countries, including Vietnam and China, are also under development. In the North, the Den Chai–Chiang Rai–Chiang Khong double-track railway spans 323 kilometers, while in the Northeast, the Ban Phai–Nakhon Phanom double-track railway covers 355 kilometers. Provinces hosting industrial estates in the Northern region include Lamphun, Phichit, and Nakhon Sawan, while in the Northeastern region, they are located in Udon Thani and Ubon Ratchathani.

-

The western region: The Western region remains in a waiting phase for further development opportunities. The Industrial Estate Authority of Thailand (IEAT) had previously planned to develop industrial estates in this area to align with and support the Dawei Deep-Sea Port and industrial estate project in Myanmar. However, the Dawei project was subsequently deprioritized as Myanmar shifted its focus toward the development of the Thilawa Special Economic Zone (Thilawa SEZ). In 2025, the first zone of Thilawa SEZ commenced operations and expansion into subsequent phases is underway (Source: Thilawa SEZ Management Committee). As a result, industrial estates in the Western region—currently located in Ratchaburi province—continue to await stronger growth momentum.

-

The southern region: The Southern region is undergoing gradual development with the aim of strengthening economic linkages with Malaysia. There are two industrial estates located in Songkhla province, with rubber-related industries forming the core activity base. However, recurring security concerns in parts of the South, persistent electricity supply constraints, and infrastructure that is not yet fully developed have limited the success and expansion of industrial estates in this region.

Situation

In 2025, new land sales and leases in industrial estates declined. This was partly due to heightened global economic uncertainty and the United States’ import tariff increase policy, which weighed on investment sentiment. The slowdown also reflected a high base effect from the strong performance recorded in 2024.

-

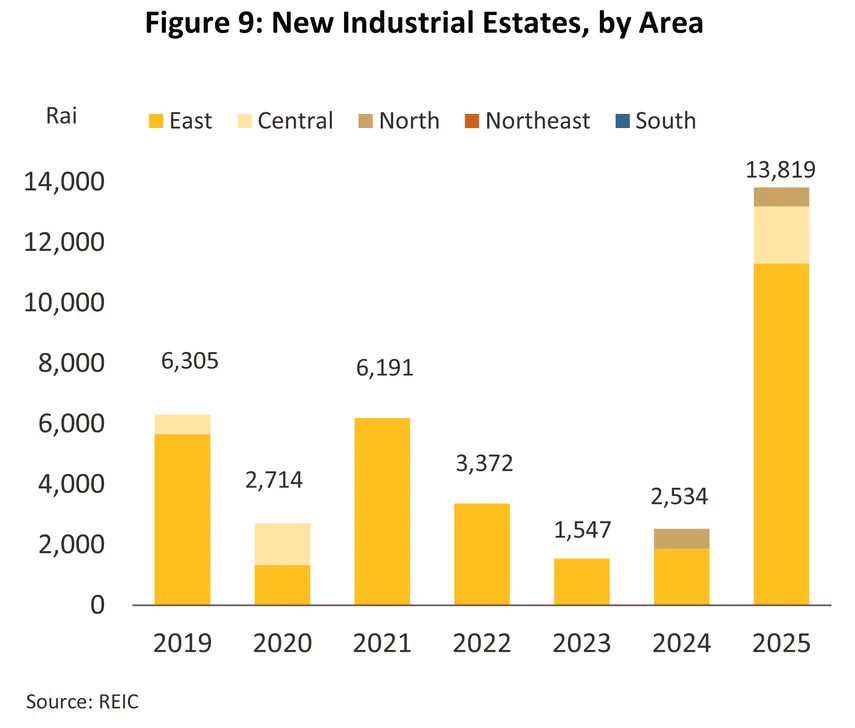

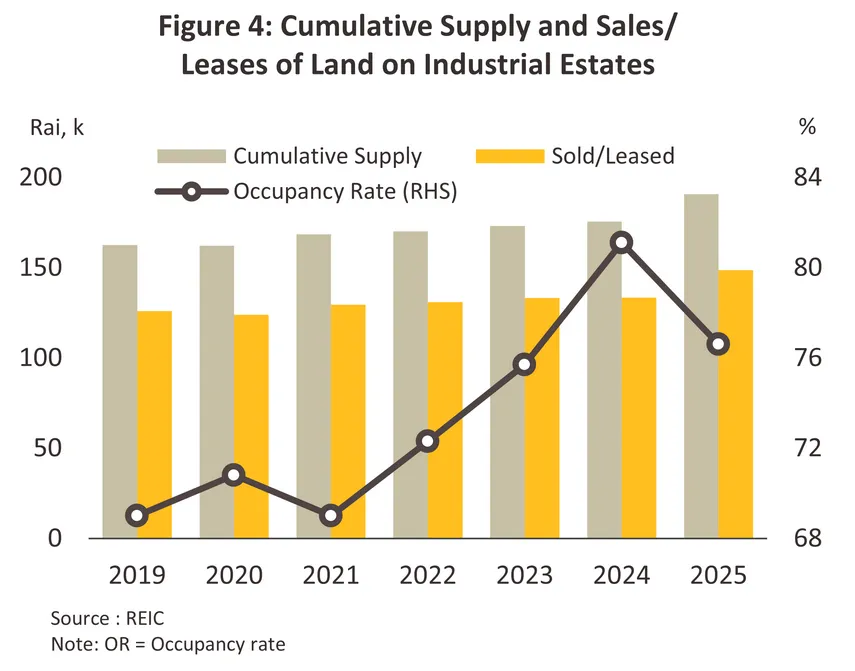

In 2025, a total of ten new industrial estates were established, comprising eight in the Eastern region, one in the Central region, and one in the Northern region, adding 13,819 rai of new land (Figure 9). As a result, the total number of industrial estates nationwide increased to 82, with a combined area of 190,618 rai (+8.7%). The Eastern region continued to host the largest concentration, with 54 estates covering 147,961 rai, accounting for 77.6% of the country’s total industrial estate area. This was followed by the Central region (including Bangkok), with 18 estates spanning 29,060 rai, representing a 15.2% share.

-

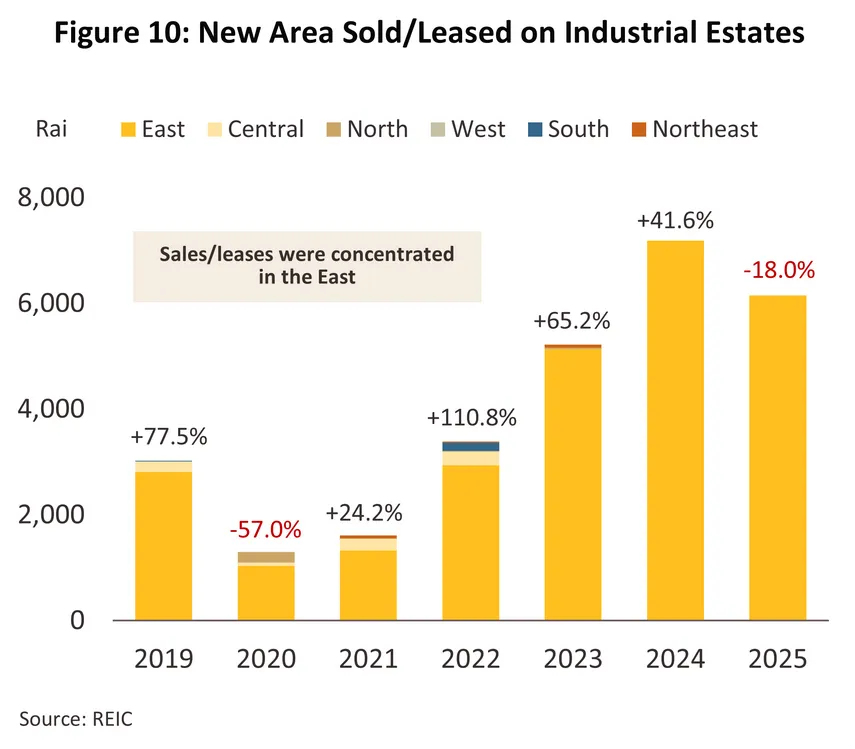

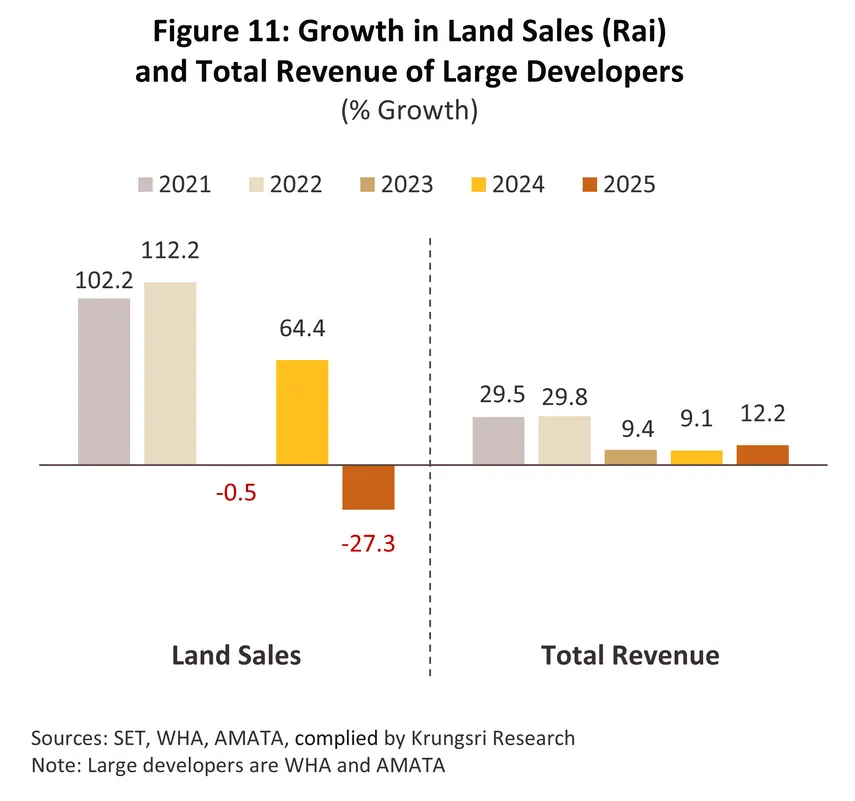

New land sales and leases in industrial estates totaled 6,531 rai (Figure 10), representing a contraction of -18.0%, with declines recorded across all regions. Nevertheless, the Eastern region continued to attract the greatest investor interest, accounting for 6,152 rai, or approximately 94% of total newly sold and leased land nationwide, despite a -14.4% decline. This was followed by the Central region (including Bangkok and its vicinity), which recorded 379 rai, down -47.7%. As a result, cumulative sold and leased land reached 148,574 rai in 2025, translating into an overall occupancy rate of 76.6% (Figure 4), declining from 81.1% at the end of 2024. Considering the two major industrial estate developers—AMATA and WHA Group—combined land sales (in rai) declined by -27.3%. In contrast, their total revenue increased by 12.2% (Figure 11), supported by recurring income streams from other business segments, such as rental services and utility services, which helped offset the decline in land sales.

-

Investment momentum in 2025 remained strong. The total value of investment promotion applications nationwide reached THB 1.9tn, up 67.2%. Of this, applications in the Eastern Economic Corridor (EEC) rose by 105.9% to THB 1.0 tn, accounting for 54% of total approved investment promotion applications. Meanwhile, the value of approved investment projects increased by 66.0% to THB 1.6tn, with THB 1.1tn (70% of total approved value) concentrated in target industries. In addition, the value of investment promotion certificates issued—an indicator closely aligned with actual investment—expanded by 36.0% to THB 1.2tn.

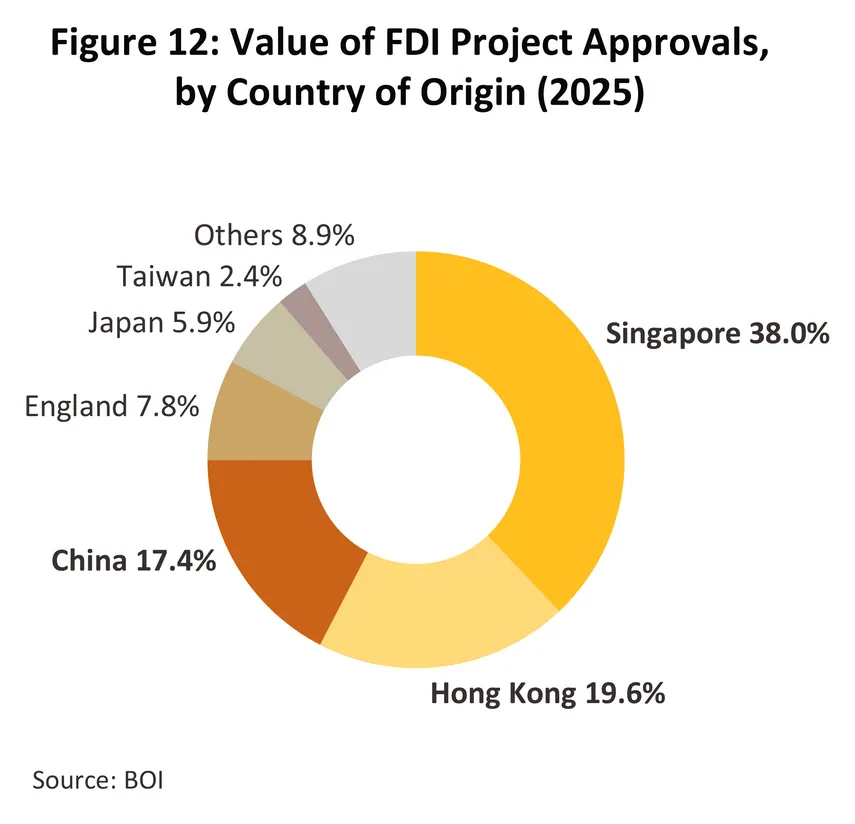

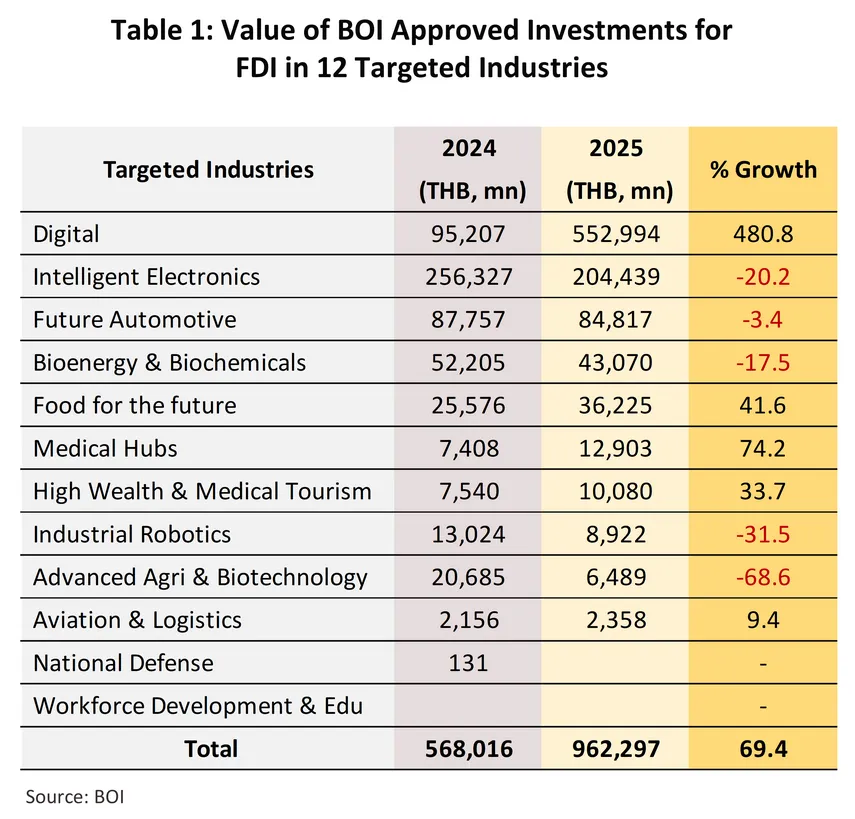

In terms of foreign direct investment (FDI), the value of applications and approved investment promotion projects in 2025 amounted to THB 1.4tn (+66.1%) and THB 1.1tn (+56.9%), respectively. The largest source of approved foreign investment was Singapore, totaling THB 430bn, representing 38% of total approved FDI value, followed by Hong Kong and China (Figure 12). Approved projects in the 12 S-curve industries were valued at THB 960bn (+69.4%), with Digital Industries accounting for the largest share at THB 550bn, followed by Intelligent Electronics at THB 200bn (Table 1). During the period from 2018—when the Eastern Economic Corridor Act B.E. 2561 (2018) came into effect—through 2025, the cumulative value of FDI investment promotion certificates issued in the EEC totaled THB 3.3tn, expanding at an average annual rate of 12.1%. The top five sources of FDI during this period were Singapore, China, Japan, Hong Kong, and the United States, respectively.

Outlook

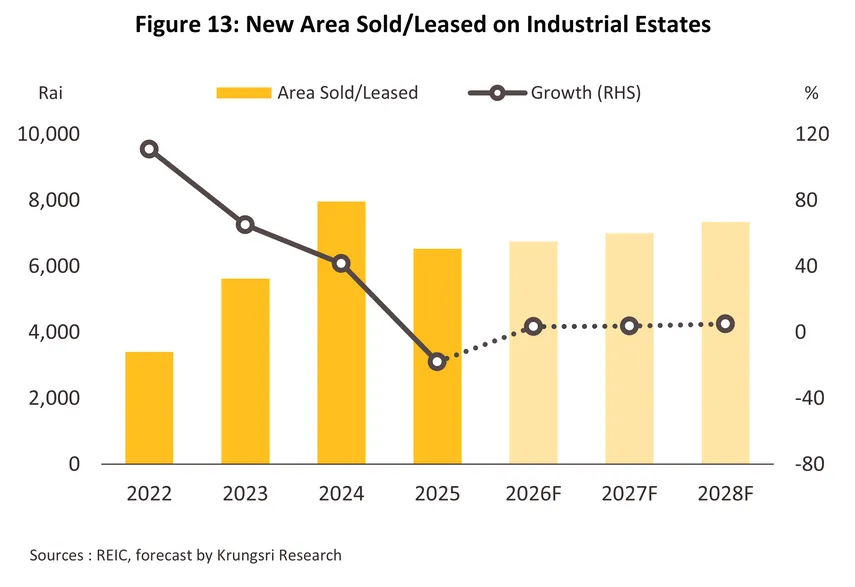

New land sales and leases in industrial estates are projected to grow at an average rate of 3.0–4.0% per year, or approximately 7,000–7,300 rai annually, during 2026–2028 (Figure 13). Key supporting factors include:

-

A growing wave of investment relocation from overseas—particularly from China and Japan—into ASEAN, including Thailand, reflects efforts to mitigate risks from trade protection measures and ongoing supply chain disruptions. Thailand stands to benefit from this shift, supported by its strategic positioning as a regional manufacturing base and trade hub, alongside well-developed logistics connectivity across road and rail networks. New greenfield investment in industrial estates has been largely concentrated in modern, technology-driven and sustainability-oriented sectors, including electronics, digital services, clean energy, and advanced materials supporting smart devices and next-generation vehicles. These industries form part of the upstream segment of modern value chains, which is expected to strengthen self-reliance among developing economies in Asia, reducing their reliance on imported upstream inputs.

-

Infrastructure investment is expected to increasingly support more comprehensive connectivity, particularly in the EEC under Phase 2 of the development plan (2023–2027). While new projects may continue to face delays in 2026 due to budgetary constraints and procurement approval processes following the transition to a new government, projects that have already secured budget approval since 2025 are expected to make more progress including: (i) the High-Speed Rail Linking Three Airports (Don Mueang–Suvarnabhumi–U-Tapao), which is expected to begin construction in 2027-2028 following contract amendments anticipated to be completed in 2026; (ii) the Map Ta Phut Port Phase 3 project, currently under Phase 2 construction (MTP 3.2), focusing on gas, liquid cargo, and service terminals, with construction commencing on October 15, 2025 and gas and liquid terminals are targeted to open in 2026 (Source: Bangkokbiznews, Dec 30, 2025); (iii) Laem Chabang Port Phase 3 has reached approximately 90% completion in marine works (dredging and reclamation); however, progress is currently delayed due to delays in site handover among the relevant agencies (Source: Krungthep Turakij, Apr 24, 2026); and (iv) the U-Tapao Airport and Eastern Aviation City project, with the first phase targeted to commence operations in 2028, despite ongoing delays in the high-speed rail project.

-

BOI and EEC incentive measures, both tax and non-tax, which are expected to continue being rolled out. These include enhanced tax privileges to attract investors, regulatory relaxations to facilitate business operations, and extensions or refinements of existing investment promotion measures, all of which are likely to further support foreign investment inflows.

However, industrial estate operators are expected to face a range of risks and challenges that could weigh on growth over 2026–2028, including:

-

Prolonged conflict in the Middle East may lead to a broader delay in investment decisions by foreign investors, reflecting rising uncertainty over the global economic outlook and the likelihood of higher oil prices, which could lead to higher transportation costs. In addition, disruptions to logistics systems along related transport routes may further affect international trade and investment flows. However, the direct impact from Middle Eastern investors on this business is expected to remain limited, considering that investors from the Middle East accounted for only 12 applications for investment promotion in 2025 with a combined investment value of THB 1.8bn, compared with a total of 2,421 applications worth THB 1.36tn overall.

-

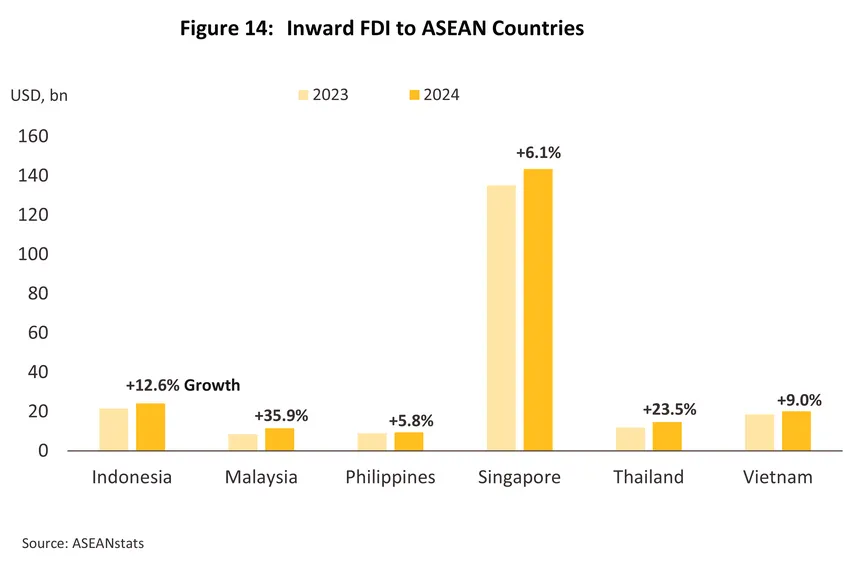

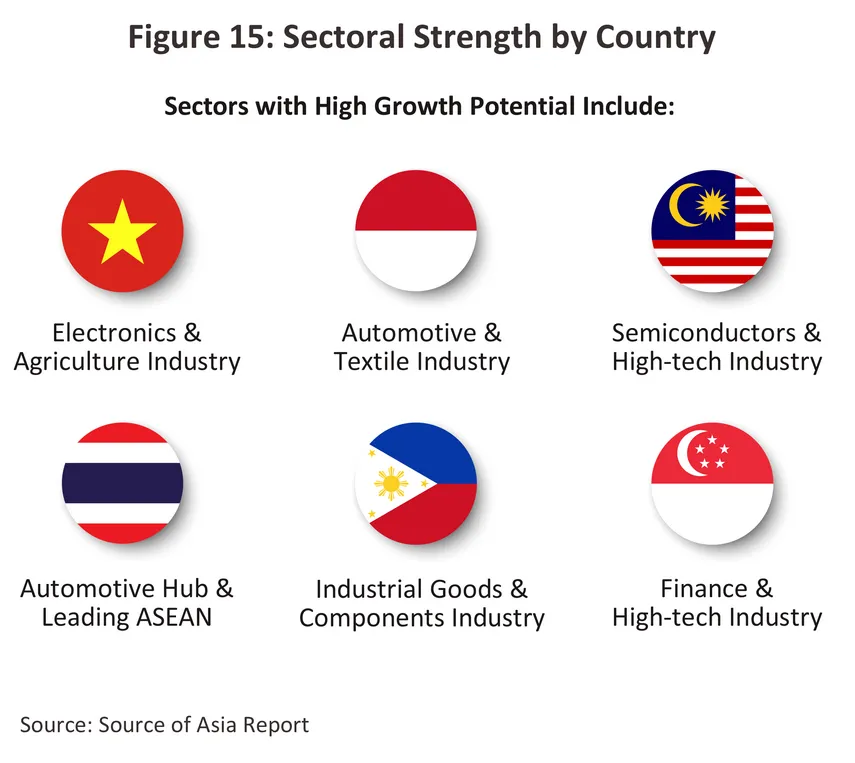

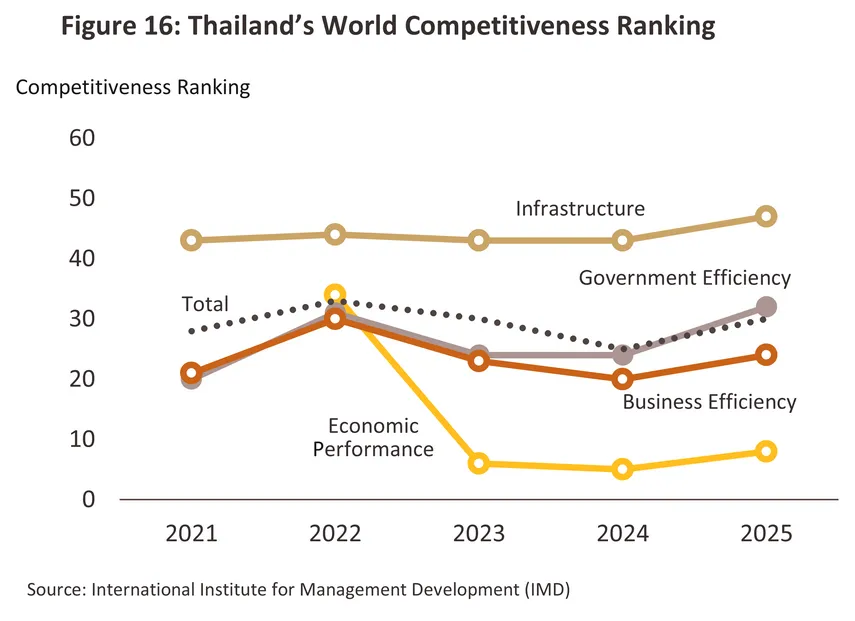

Foreign direct investment (FDI) is increasingly being distributed across multiple ASEAN countries to reduce supply chain risks (Figure 14), resulting in a partial shift of investment toward economies with stronger structural advantages. In recent years, Thailand has faced intensifying competitive pressure from Vietnam in terms of cost and labor, particularly in electronics, from Malaysia in semiconductors, and from Singapore in advanced technology industries and as a regional financial hub (Source: Source of Asia Report, Figure 15). As a result, Thailand’s competitiveness has come under pressure in both cost and technological dimensions, which may limit the growth of investment in industrial estates going forward, particularly when compared with Singapore and Malaysia, which may have stronger advantages in attracting new foreign investment in technology-intensive projects that rely on well-developed industrial ecosystems. According to the International Institute for Management Development (IMD), Thailand ranked 30th out of 69 economies in 2025, declining from 25th in 2024, while Singapore ranked 2nd (down from 1st) and Malaysia ranked 23rd (improving from 34th). In terms of technological infrastructure4/, Thailand’s competitiveness remains below both Singapore—ranked 1st in 2024 and 2025—and Malaysia, which improved from 27th to 25th, while Thailand declined from 25th to 32nd over the same period. This is consistent with the Milken Institute’s Global Opportunity Index 2026, which ranks Malaysia as the most attractive investment destination in Southeast Asia among emerging markets.

-

Location-related risks of industrial estates may intermittently affect trade, transportation, and cross-border procedures, particularly in border areas. In the case of ongoing tensions between Thailand and Cambodia, periodic disruptions have led to delays in logistics processes and increased operating costs for businesses. At the same time, border areas face infrastructure limitations compared with core industrial zones, resulting in more fragile investment confidence. This is reflected in the industrial estate in Sa Kaeo province, which has been affected by the Thailand–Cambodia border situation, with its occupancy rate remaining low at only 7.7% in 2025 (Source: REIC, Mar 2026).

-

Land-related regulations may remain misaligned with current investment areas, particularly certain zoning laws, thereby constraining the development of industrial estate land and limiting the addition of new supply to the market going forward. This constraint is especially evident in strategic areas undergoing rapid industrial expansion, where available land may be insufficient to meet investor demand—particularly among large foreign investors requiring sizeable plots. In key areas such as the EEC, large industrial land plots and designated industrial (purple zone)5/ areas have continued to decline, with plots exceeding 50 rai within industrial estates becoming increasingly scarce and more costly. As a result, industrial estate operators may need to accelerate the release of new land supply to the market. In early January 2026, the BOI established a special subcommittee to review zoning regulations and address constraints related to public land and irrigation channels, which have historically been key bottlenecks and required lengthy approval processes (Source: Thansettakij, Jan 5, 2025). Nonetheless, government policies on zoning reform and industrial estate development are expected to remain focused primarily on designated target areas, leaving other areas to require further development over time.

Industrial estate developers are expected to continue investing in business transformation through various approaches.

-

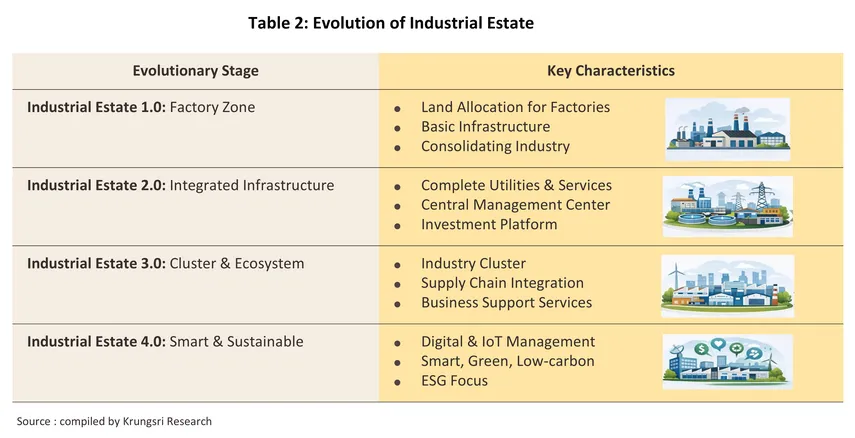

The development toward smart parks and smart eco-industrial estates, enhancing modernization across production technologies, transportation systems, communication networks, and energy management. The objective is to improve operational efficiency and strengthen business competitiveness. Estate developers are therefore likely to step up investment in advanced technologies, including robotics, automation systems, and digital platforms—particularly the integration of AI and IoT to enhance production efficiency for operators within the estates. This will be accompanied by stronger environmental management (Table 2), with a clear transition toward clean energy sources such as solar and biomass, replacing fossil fuels to achieve long-term sustainability goals.

-

The transformation of industrial estates toward a more integrated “industrial ecosystem” model reflects a shift in focus among operators, who are no longer relying solely on competitive strategies based on marketing or site selection but are increasingly emphasizing service-oriented strategies and the development of comprehensive and sustainable infrastructure over the long term. This includes enhancing core infrastructure such as logistics systems and automation, promoting industry clustering within designated zones (e.g., EV, battery, and advanced petrochemical clusters), and strengthening linkages with research centers, academic institutions, and Science & Technology Parks to enhance the competitiveness of businesses across the estate supply chain, enabling them to better compete with regional peers in the global market.

Industrial estates in the Eastern region are expected to continue recording outstanding growth, particularly in Chonburi and Rayong (Table 3). Key supporting factors include both strategic location advantages and continued government support under the EEC development plan, which emphasizes comprehensive large-scale infrastructure investment to accommodate target industries. Most recently, the Eastern Economic Corridor (EEC) Policy Committee has proposed the inclusion of Prachinburi as the fourth EEC province to support the anticipated influx of investment, which is currently under a feasibility and suitability study during July–September 2025 (Source: Banmuang, Sep 8, 2025). In contrast, industrial estates in other regions have attracted relatively limited investor interest, mainly due to location disadvantages and the need for further area-based development—particularly in terms of infrastructure enhancement—to strengthen their attractiveness to investors.

1/ The key differences between industrial estates and industrial parks/zones are as follows. First, foreign companies that have not received BOI approval are permitted to purchase land within industrial estates, whereas they are not allowed to purchase land in industrial parks or zones. Second, in industrial estates, the Industrial Estate Authority of Thailand (IEAT) serves as the certifying authority and provides related services, including the issuance of construction permits and factory operation licenses. As a government agency, the IEAT is able to coordinate and submit applications to the Department of Industrial Works more efficiently and promptly. By comparison, industrial parks/zones are privately owned and managed, requiring operators to handle such procedures independently through the relevant authorities.

2/ The 12 targeted industries comprise: 1) Future Automotive; 2) Intelligent Electronics; 3) High Wealth and Medical Tourism; 4) Advanced Agriculture and Biotechnology; 5) Food for the Future; 6) Industrial Robotics; 7) Avia on and Logistics; 8) Bioenergy and Biochemicals; 9) Digital; 10) Medical Hubs; 11) National Defense; and 12) Workforce Development and Education.

3/ The five special targeted industry clusters consist of: 1) Next-Generation Automotive Cluster; 2) Digital Cluster; 3) Medical and Comprehensive Healthcare Cluster; 4) Bio-Circular-Green Economy Cluster; and 5) Services Cluster.

4/ Technological Infrastructure refers to a country’s readiness in technological systems and supporting infrastructure that enhance the competitiveness of businesses and industries. It encompasses multiple dimensions, including digital infrastructure, investment in technology

and innovation, national IT and digital capabilities, and the regulatory and institutional environment that supports technological development.

5/ Purple-zone land under urban planning regulations refers to areas primarily designated for industrial and warehouse activities. These zones are suitable for factories, logistics centers, and industrial estates. A limited portion of the area may be developed for residential or commercial use under specific conditions, but high-rise buildings are generally not permitted unless they are part of an industrial facility.

.webp.aspx)