Overview

The real estate sector contributed 6% of Thailand’s GDP in 2019, which is significant to the national economy. A large amount of capital circulates within the economic system and supports rising employment and income. The sector is also has a large influence on the direction of related businesses such as construction, building materials, finance, consumer electronics, furnishings and decoration.

The property sector consists of three principal segments: residential, commercial, and industrial. In Thailand, two-thirds of the property market (by value) is derived from residential transactions (source: World Bank). Developers of residential properties normally focus on Thai customers because Thai law stipulates that non-Thais may legally own only condominiums and only up to 49% of total salable area in any project. For detached housing and townhouses (also called rowhouses or shophouses), the ownership regulations for non-Thais are more onerous.

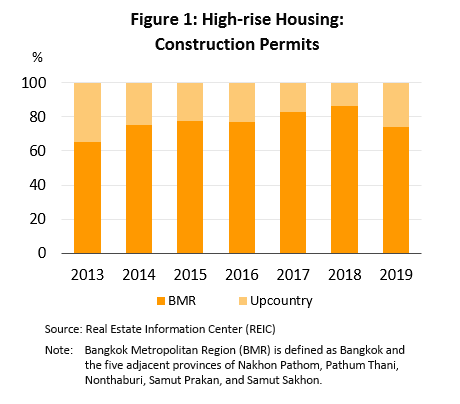

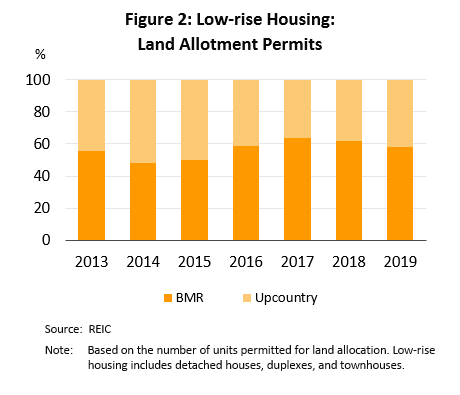

The housing market is split between self-built housing and housing projects. 70% of housing projects constructed during 2015-2019 are located in BMR (Fig. 1 and 2). This market had an annual value of around THB460bn but since 2012, developers have started to look beyond the Bangkok region. The shift in focus followed the major flooding in BMR and central region near the end of 2011 and the decision by the government in 2012 to increase spending on infrastructure in provinces. This prompted developers to place greater emphasis on investing in housing projects in provincial centers, the majority being low-rise housing due to the availability of land outside Bangkok. However, upcountry consumer purchasing power weakened in 2015 and 2016 after agricultural goods prices dropped, and this caused developers to switch their attention back to projects in the BMR.

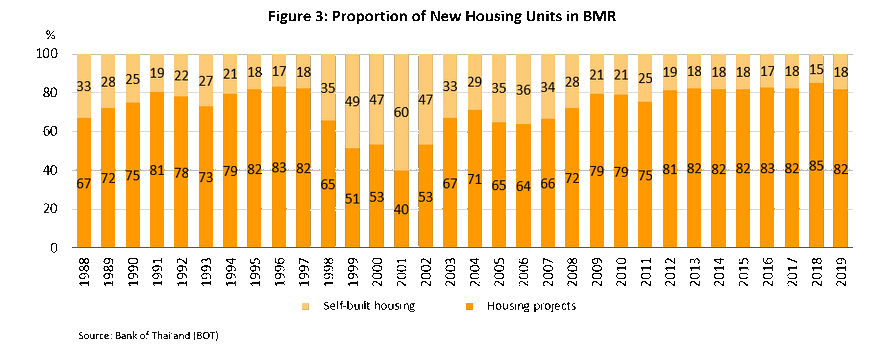

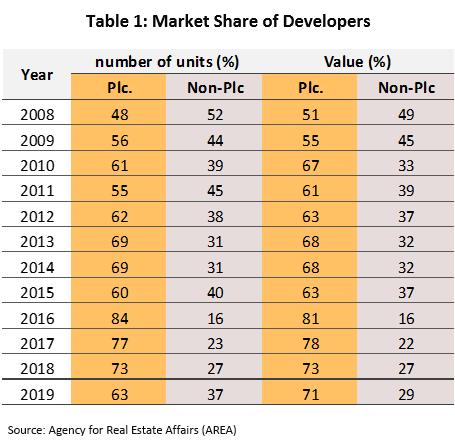

Currently, over 80% of new housing units in the BMR are in projects developed by commercial housing developers (Figure 3). Table 1 shows that large developers (those listed on the SET and their subsidiaries) control 60-70% of the market by volume and value. Because large companies are able to manage costs more effectively than their smaller peers, they are also in a position to buy larger land bank which would reduce project development cost. They can also undertake several projects simultaneously which improves economies of scale. And they benefit from stronger branding and marketing networks.

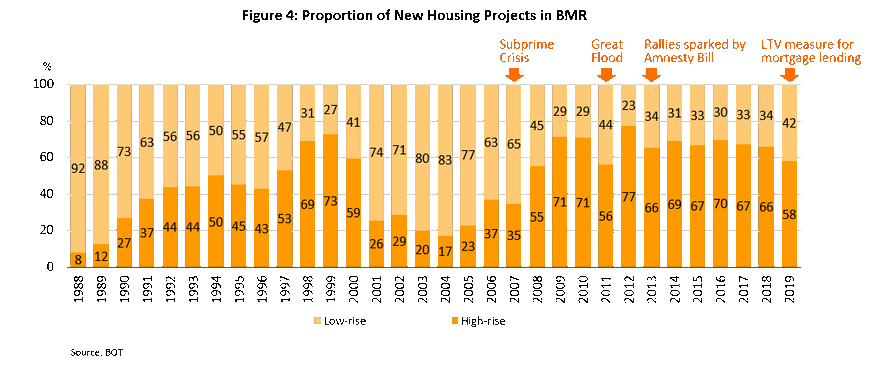

Since 2008, high-rise residential buildings have represented a larger share of new projects than low-rise segment. An average of 70% of new housing units in the market have been condominium units (Figure 4) due to the declining availability of land, and consequently, higher prices for development land. The extension of rapid mass transit lines (MRT and BTS) has also led to housing projects springing up along new routes and near stations. These led to the increasing popularity of high-rise residential developments.

Situation

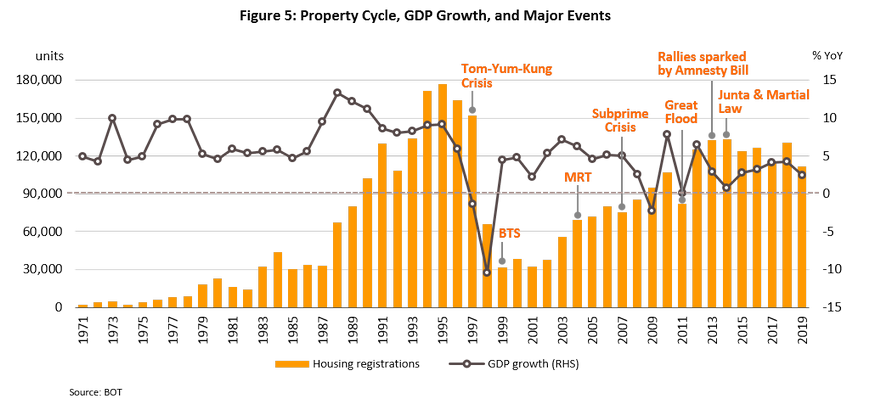

Following the 1997 Asian Financial Crisis, the housing market flipped from a “bubble” to “oversupply” as new supply had outpaced sales over several years.

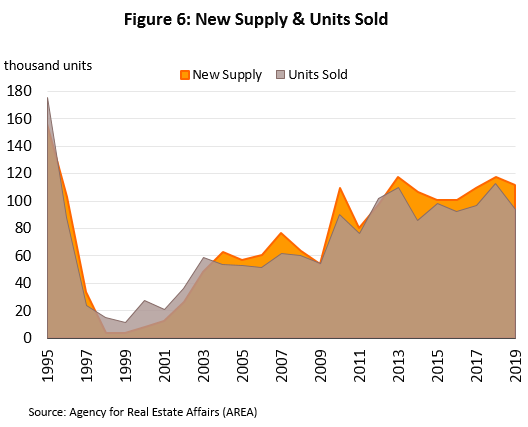

- 1997-2006: The 1997 Asian Financial Crisis led to a 5-year depression in the BMR property market (1997-2001). The collapse in consumer purchasing power triggered a dramatic slide in the sale of new units to an average of only 20,000 per year. This was sharply lower than the pre-crisis average of 148,000 units per year in 1994-1996. In 2003, after the economy recovered, new investment started to pick up again (Figure 6). During 2003-2004, there was significant investment in low-rise housing projects for the high-end market on the western side of the Bangkok Outer Ring Road; there is still excess supply of detached housing to this day. In 2006, the decision to extend the BMR rapid mass transit networks prompted a corresponding increase in investment in high-rise buildings, with condominiums selling well and seeing a shorter absorption period than low-rise housing.

- 2007-2009: The effects of the US subprime crisis was felt across the world, and Thailand was no exception. The crisis slowed the domestic property market, both in terms of supply and demand. In 2009, 59,000 units were sold while 54,000 units were launched, down 10.4% and 14.3% from 2008. But they picked up in 2010 along with an improving economy.

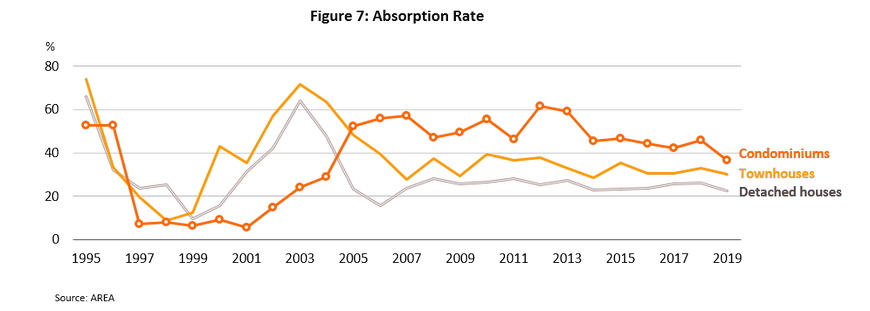

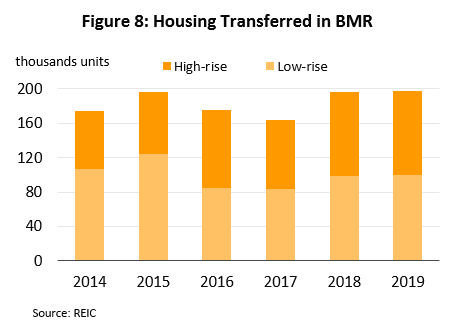

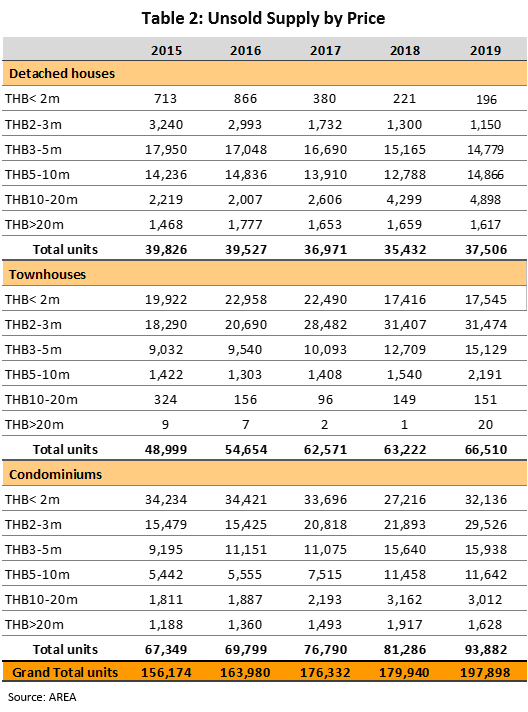

- 2010-2018: The BMR saw an average of 105,000 new units each year but only about 96,000 were sold annually (Figure 6), which pushed up housing inventory. This supply-demand imbalance was partly caused by the private sector’s response to the government’s incentive for first-time house buyers in 2011 and 2012. It led to record-breaking investments in condominium projects in 2012-2013, but problems started to arise because the incentive had encouraged buyers to bring forward property purchases to 2011-12, especially condominium units. In addition, domestic political conflicts and a weak Thai economy in 2013-2017 also suppressed demand for housing. This is reflected in the lower absorption rate (Figure 7) and number of property transfers (Figure 8). Consequently, there was 176,000 unsold housing units (+7.5% YoY) in the BMR. Of these, more than 60% were units priced below THB3m (Table 2).

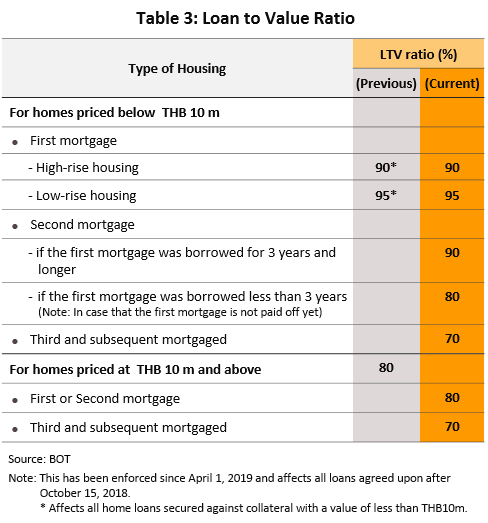

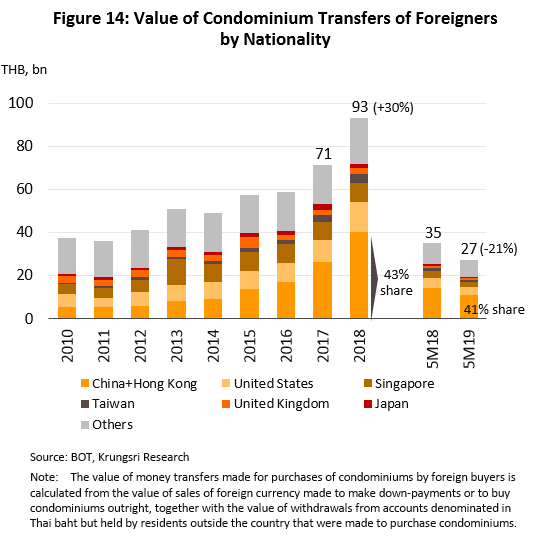

In 2018, Thailand economy grew by 4.1%. This boosted spending power and consumer confidence, and subsequently, residential property transactions (units) by 16.4%. This was the largest increase in 5 years, led by the sale of mid- to high-priced properties; most of these buyers were looking to buy a second home (generally condominiums priced at more than THB3m) in locations that allowed for easy travel to the city center. Demand from the expat market was also strong, especially from the Chinese, for condominiums. Buyers from China and Hong Kong accounted for 43% of all transfers of title deeds among non-Thai nationals. On the supply side, developers had increased investments in condominium projects near new or extended metro lines and increased the share of high-end projects in their portfolios; the latter pushed up average house price to THB4.5m per unit in 2018 (+17.2% from 2017 average). This prompted the Bank of Thailand to tighten rules governing housing loans[1] at the end of 2018, when officials moved to reduce speculative pressure in the housing market. However, buyers had rushed to complete purchases before the new rules came into effect on April 1, 2019. Therefore, in the last quarter of 2018, housing transfers jumped 17% YoY.

In 2019, the housing market slowed again due to: (i) weaker domestic spending power as GDP growth dropped to +2.4%; (ii) tighter rules on LTV ratios (Table 3), which specified revised debt to collateral rates and delayed purchasing decisions given higher down payment; and (iii) the slowing global economy, coupled with an appreciating baht which cut foreign spending on Thai real estate. These discouraged new property purchases and reduced investor confidence. However, the government responded by stimulating purchases by genuine owner-occupiers, which pared down the excess housing stock in the BMR. They did this by cutting tax for first-time buyers of properties priced at less than THB5m[2], reducing fees for transferring title deeds and registering mortgages to 0.01% of property value[3], and introducing the baan dee me down program[4]. But unfortunately, these measures were less effective than hoped and the residential market remained weak throughout 2019, as described below.

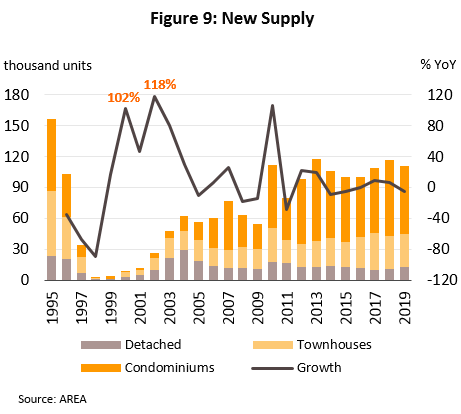

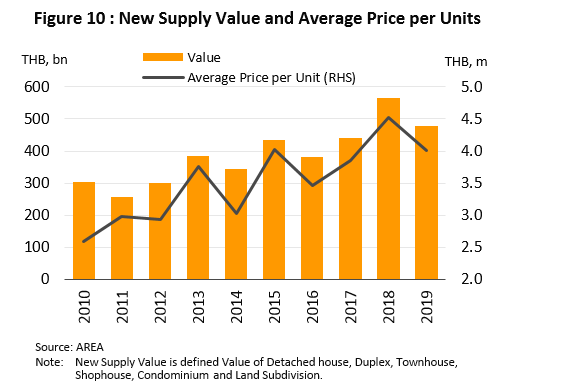

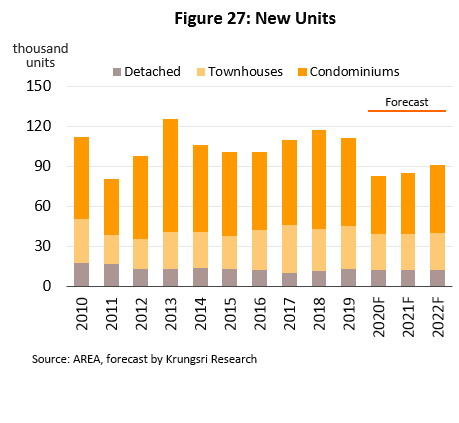

- In 2019, the volume of new housing units in the market dropped by 4.9% to 118,975 units (Figure 9). By value, the drop was larger at -15.7% to THB477bn, the lowest in 14 years (Figure 10). AREA also reported that in 2019, over 200 new projects had been abandoned, either due to failure to secure approval for environmental impact assessment or financing, or the projects were simply not attractive to buyers. In response, developers tried to adjust operations and reduce exposure to risks when undertaking new projects by focusing on smaller projects and cutting back on product features, make the projects more appealing to other market segments, and offering incentives such as free goods and price discounts. These helped to attract owner-occupiers. But the outcome was that average property price fell by 11.4% to THB4.0m per unit.

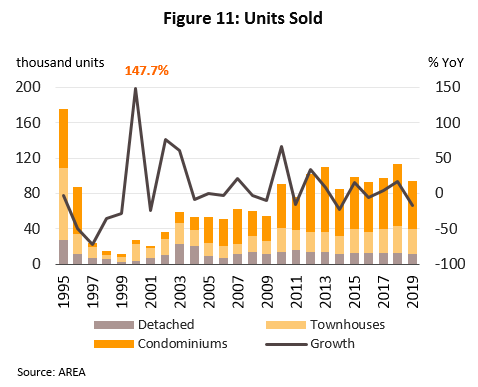

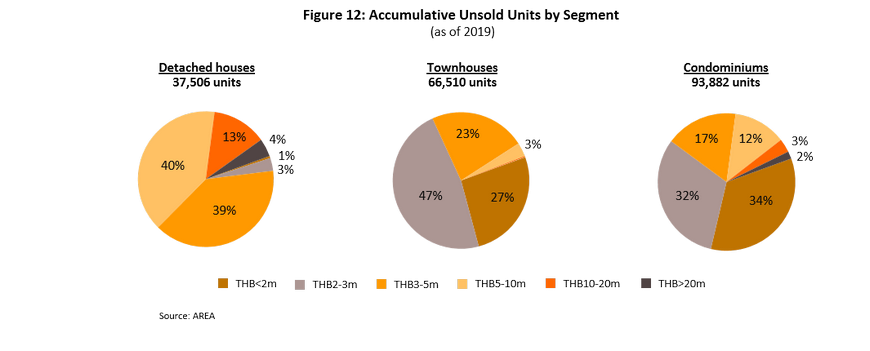

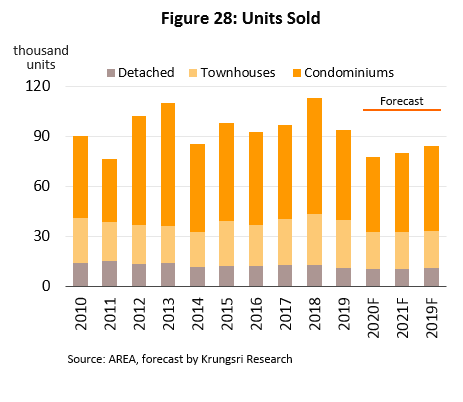

- 2019 sales slipped 16.8% to 94,012 units, the lowest in 4 years (Figure 11). But, because sales were lower than the number of new properties coming into the market, the cumulative volume of unsold units rose by 9.7% from end-2018 level to 197,898 units, the highest in 4 years. Of this, over 50% were properties priced at less than THB3m each (Figure 12).

- In 2019, 198,033 housing units were transferred, an increase of 0.7% (Figure 13). These comprised (1) condominiums (50% of total, or 98,809 units), (2) townhouses (29%, or 56,937 units), (3) detached houses (14%, or 26,916 units) and (4) ‘other’ types of housing, such as semi-detached houses and shophouses (7%, or 15,371 units). For each of these four categories, annual registrations had changed by +1.5%, +2.0%, -0.9% and -6.0%, respectively. The numbers had been affected by the rush to complete transfers in the first quarter of the year, prior to the April enforcement of the new LTV rules, as well compliance with industry regulation for developers to transfer condominium units sold in the last 1-2 years. However, purchasing power of foreign investors was weak and in the first 5 months of 2019, transfers to foreign buyers slipped 21% YoY (Figure 14).

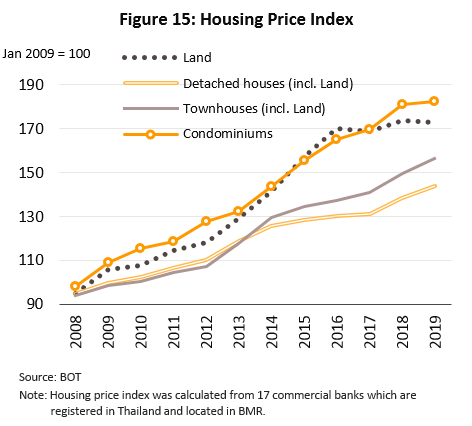

- Prices rose for all segment of residential housing in 2019. Price indices for townhouses and detached houses rose by 4.7% and 4.0%, respectively, reflecting developers’ decisions to focus on the middle and upper segments of the market. However, the price of condominium units rose by only 0.8%, partially due to stricter LTV rules removing much of the earlier demand for investment or speculation

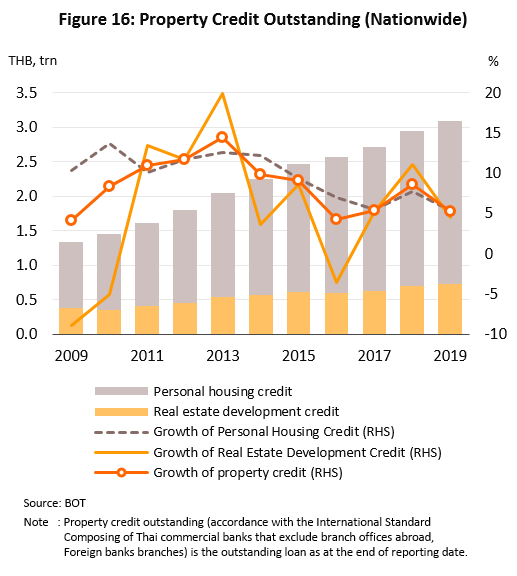

- According to data from the Bank of Thailand, growth in housing loans slowed sharply to +5.2% in 2019 from +8.7% average between 2009 and 2018.

- The value of approved pre-finance loans for property developers rose by only 4.5% in 2019 from +11% in 2018, as developers held back new projects to see how the market would evolve. At the same time, banks had tightened the release of new credit, but despite this, pre-finance loans were still required for new developments to meet anticipated demand near new metro lines in the BMR.

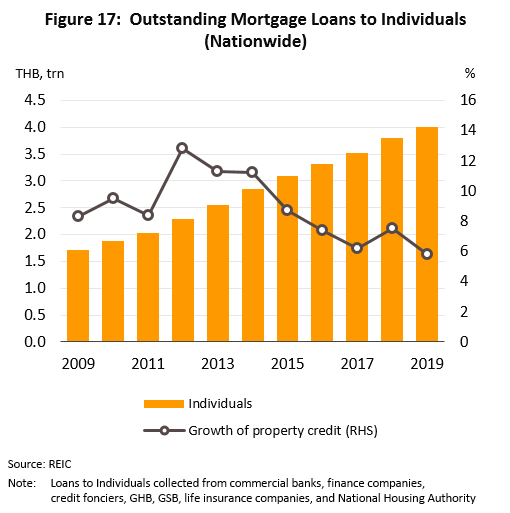

- Growth of personal post-finance loans dropped to 5.4%, the lowest rate in 17 years, following the weaker domestic economy and introduction of new LTV rules. This increase the share of rejected loan applications to 30-40% from 20-30% the year before. Total personal housing loans grew by 5.8% in 2019, the lowest in 13 years (source: REIC) (Figure 17).

Housing market in 2018

- Detached housing

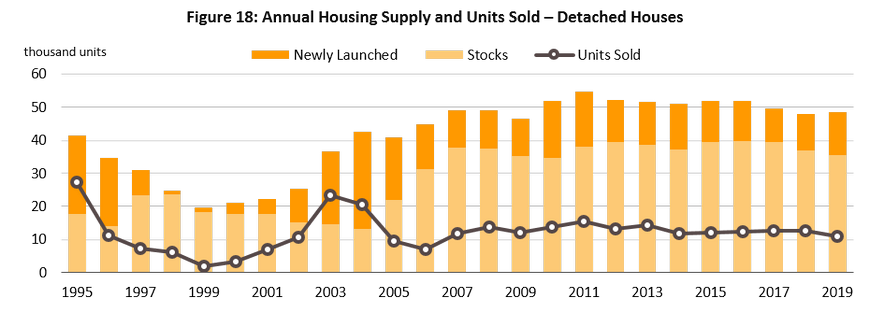

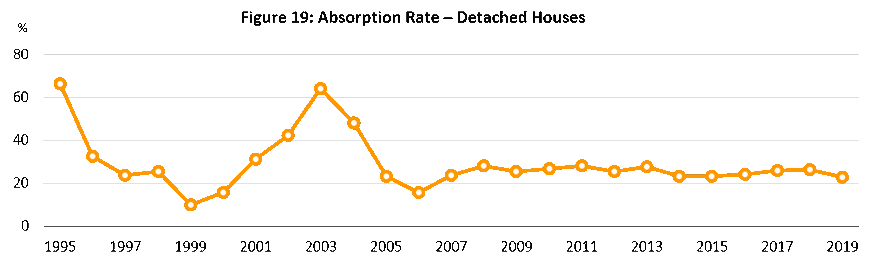

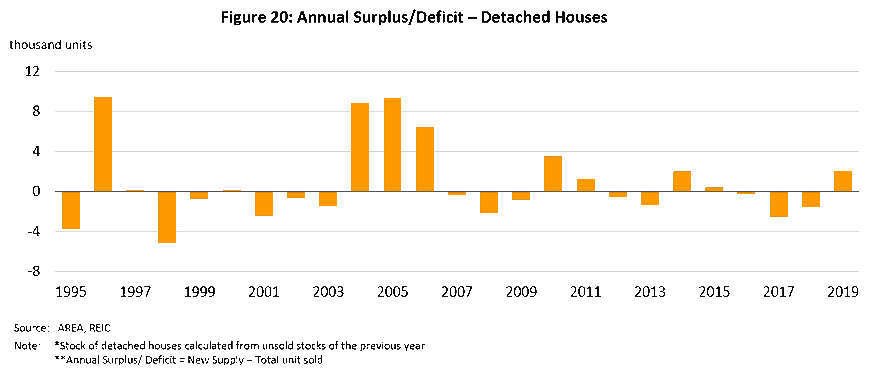

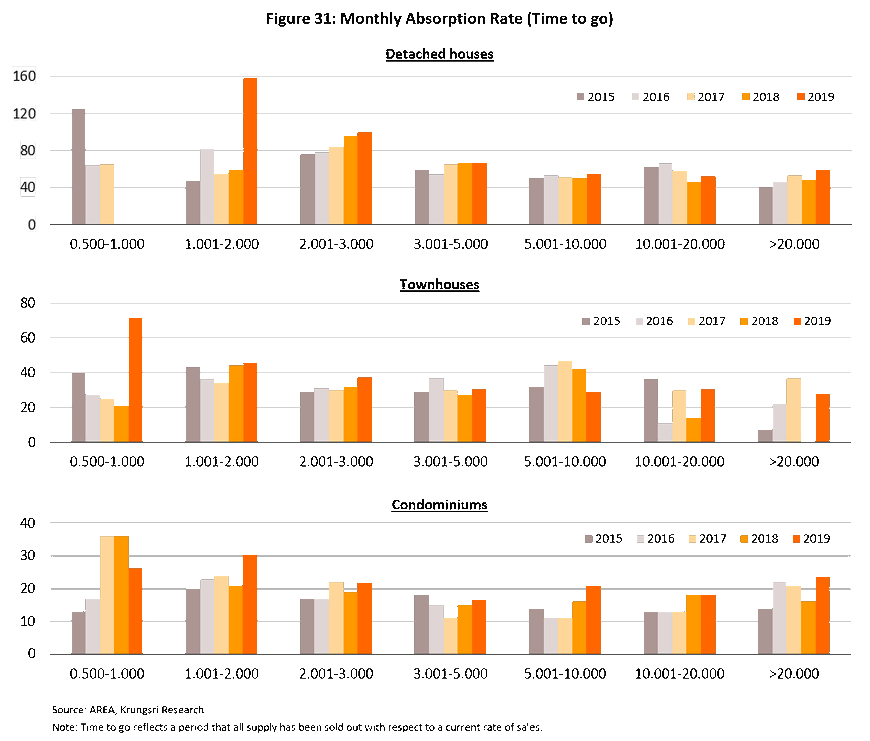

- The market for detached housing saw a steady increase in demand as major transport routes were extended into the suburbs and new roads were constructed. But new supply outpaced demand throughout 2019, and unsold detached housing accounted for 19% of total unsold housing stock in the BMR. Meanwhile, the absorption rate has remained at 25% since 2005, compared to a high of 64% during the property boom in 2003.

- In 2019, 13,084 new detached houses came onto the market, representing an 18.2% increase over 2018 and 11.7% of all new residential housing units. The average price of a new detached house dropped to THB8.0m from THB9.2m the year earlier, but despite this, the share of new houses priced at THB10m and over had increased from 17% of new housing supply to 20% as developers increasingly turned their attention to high-income earners. At the same time, the tighter LTV rules and a weaker economy reduced the volume of new houses sold by 12.7% to 11,010 units, most in the THB5-10m price band. Because of this, the number of unsold detached houses rose by 5.7% to 37,506 units.

Townhouses

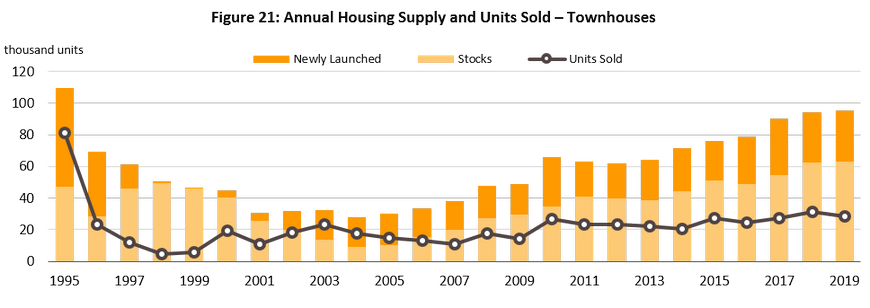

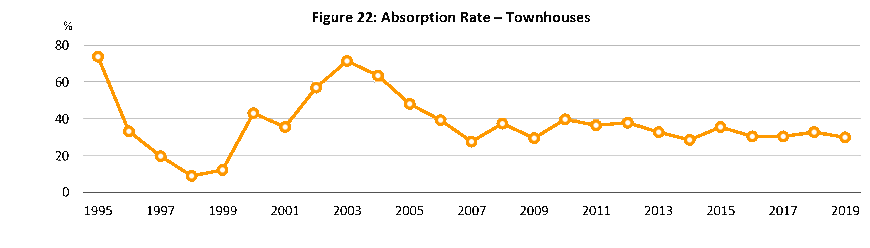

- Rising land prices spurred demand for townhouses as alternatives to more expensive detached housing. However, like other market segments, supply had risen at a faster pace than demand and since 2007, the number of unsold townhouse units had been rising steadily. In addition, between 2009 and 2018, there was falling interest in townhouses in favor of condominiums located near BTS lines (referred to as ‘city condos’), with the latter having advantages in terms of pricing and easy access (via mass rapid transportation) to the city center. These shifts in the market reduced absorption rate for townhouses to an average of 34% from 56% during the townhouse boom period of 2002-2006. Despite this, since 2014, developers had been developing expensive townhouses priced over THB10m per unit. These townhouses typically have three or more floors, are located on the fringe of Bangkok city center, and are relatively close to BTS stations, such as Rama 3, Sathu Pradit, Yannawa, and Lat Phrao. In addition, developers also invested in townhouses located in smaller alleyways that connect to mass transit systems, priced at THB2-3m each to target mid-to-low income earners.

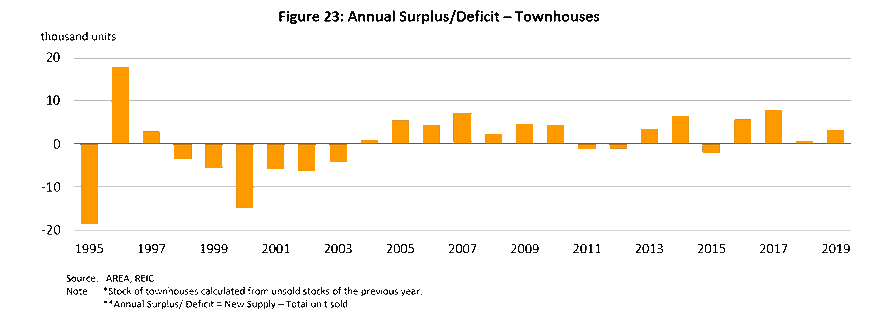

- The number of new townhouses available for sale in 2019 only inched up 0.9% to 31,987 units (29% of all new housing), but average price increased by 1.8% to THB2.9m per unit. Like detached housing, the volume of new townhouse units sold fell by 7.6% to 28,699 units in 2019 as the slowing economy weakened demand and high household debt prompted lenders to consider loan applications more carefully. This was especially the case for middle and low income earners which normally go for properties priced under THB3m each. This property segment comprised the largest group of unsold townhouses. At the end of 2019, 66,510 townhouses were unsold in the BMR, up 5.2% from the year before.

Condominiums

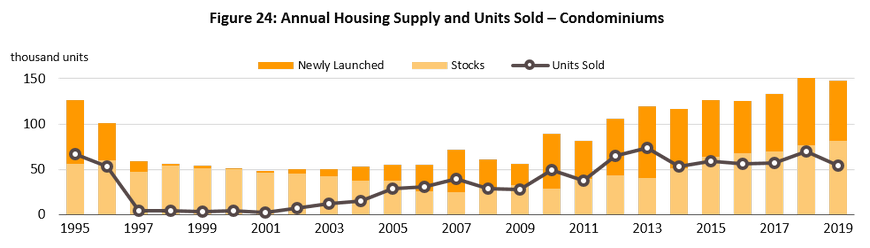

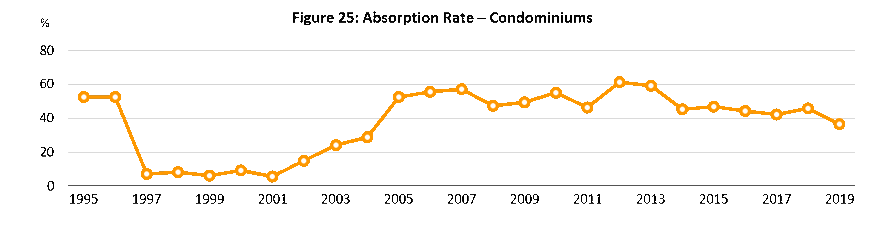

- Condominiums have been popular with a rising number of new projects since 2007 due to: (i) the extension of mass rapid transit lines and better connection within the communications network, which makes public transportation more convenient; (ii) changing consumer behavior driven by a desire to save money and to reduce commuting time, leading to a switch in preferences from low-rise housing in suburbs to high-rise accommodation in the city center; (iii) changing social structures in Thailand, with more people living in smaller units and nuclear families; and (iv) the declining availability of development land and rising land prices. The combination of these factors prompted developers to build condominiums to meet demand for housing with over 50,000 new units available annually. Buyers of these condominium units can be split into two distinct groups. (1) Real demand accounts for around 60% of the market; and (2) those who buy for investment, which can itself be split into those who buy to rent out (25-30% of the market) and those who buy for speculation (the remaining 10-15%). Thai law specifies that non-Thais may own condominium units subject to a maximum of 49% of the total floor-space in the project; this also led to condominium projects registering higher absorption rates than low-rise buildings. Between 2009 and 2018, the absorption rate for condominiums averaged 50% compared to only 25% for detached houses 34% for townhouses.

- Despite this, the condominium market slowed down from 2014 to 2018, especially demand for mid- to low-end units (i.e. priced below THB3m each), due to high debt levels and a sluggish economy. As a result, buyers in this property segment were forced to be careful about spending and had delayed property purchases. But in the top end of the market, units continued to sell and remained popular among high-income earners and foreigners.

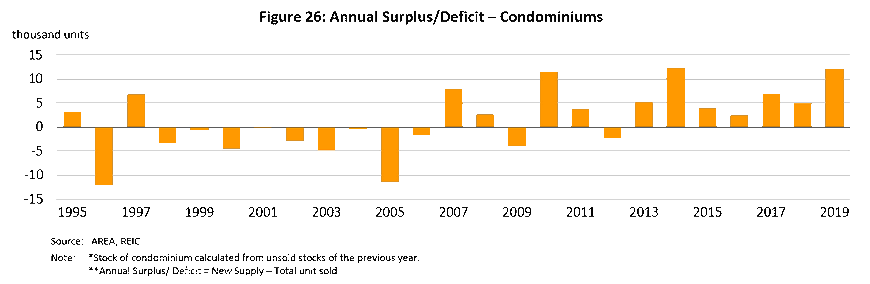

- Last year, 66,376 newly completed condominiums came into the market (60% of all new housing stock) but this represented a drop of 10.8% YoY, the first drop in 3 years. Average price also fell sharply by 17.8% to THB3.7m (lowest in 2 years) as developers tried to counter the effects of a weakening economy by reducing exposure to risk through running down inventory rather than launch new projects, the effects of the BOT’s stricter LTV regulations, and a 7.6% appreciation of the THB. Like in other property segments, the combination of these factors reduced speculation and investment demand. Consequently, in 2019, the number of condominiums sold in the BMR fell by 21.7% to a 4-year low of 54,303 units. The number of unsold condominium units also hit an historic high of 93,882 units (up 14.7%) as absorption rate slowed to a 14-year low of 37%, implying it would now take 2 years for developers to clear inventories. Nevertheless, the absorption rate for condominiums is still higher than for low-rise units and as such, which means developers would be able to clear condominium inventory faster than other types of housing.

Industry Outlook

Krungsri Research forecasts a difficult year for the BMR housing market in 2020. Developers will see a sharp contraction in demand as purchasing decisions and investor confidence would be severely hurt by: (i) the Covid-19 impact, slowing spending on infrastructure projects, and drought in Thailand, would hurt domestic and international spending power severely in the first half of the year. In 2020, the domestic economy is forecast to shrink by 5.0%, the worst performance in 22 years; (ii) tighter lending criteria and the enforcement of new LTV rules for buyers of second and subsequent homes; and (iii) significant supply glut in some areas, which would drag ‘time to go’.

- In the first quarter of 2020, the number of new residential property units coming into the market collapsed 43.9% YoY. In detail, new condominium units fell by 67.5% YoY and detached houses by 36.1% YoY. Overall, developers had cut back on new projects and in response to declining interest from buyers since 2019, they had switched to selling inventory units by offering attractive deals such as larger-than-usual price discounts, leasing deals, and up to 2 years of payment-free accommodation. The worsening business conditions were reflected in the drop in first-month take-up rates for all market segments; it was especially bad for condominiums which fell to a 13-year low of 18.5% (compared to 61.5% average in the first quarter of each of the past 5 years). For townhouses, take-up rate fell to a 20-quarter low of 14.2%, while for detached houses it hit a 52-quarter low of 3.9%.

- For all of 2020, the number of newly launched units is expected to shrink by 26% to an 9-year low (Figure 27). And because most developers will postpone new projects until at least the second half of the year, when the economic outlook would be better, presales are forecast to fall by 17%, following a 16.8% decline the year earlier (Figure 28). Likewise, housing transfers is projected to drop by 24.3%, with the sharpest drop in the first 6 months of the year, when Thai and overseas buyers are likely to postpone transfers, and possibly cancelling if they have lost their jobs or their loan applications are rejected .

In 2021 and 2022, the housing market should gradually recover along with the economy, accelerating works on mega-projects, greater investment in the Eastern Economic Corridor (EEC), and stronger demand from expatriates investing or working in Thailand. This would stimulate work on new projects, and the number of new properties coming into the market is forecast to rise by 5.0% (Figure 27), most from large developers with a secure financial footing. Condominiums will remain the mainstay of the market but to help maintain profitability, developers will likely increase the share of low-rise properties because these usually generate returns more rapidly (around 3-6 months on average) and most are bought by owner-occupiers rather than speculators and investors. Developers will also continue to sell inventory units especially in the sub-THB3m segment which accounts for over 50% of all unsold stock.

Competition will stiffen in the BMR, especially from domestic property developers that are usually active in other parts of the economy (for example, Singha Estates and BTS Group Holdings), and overseas developers (especially from Japan, Singapore, Hong Kong and China). Given this, in order to increase competitiveness, some developers may form joint-ventures with foreign investors for high-value projects. This would also expand their customer base overseas; an example is the partnership between Origin Property and the South Korea’s GS Engineering & Construction to develop a THB4bn residential project. Overall, in the coming period, property developers will try to expand their offerings to target several customer segments, for example by offering long-term leasehold properties in prime areas for 30-40% cheaper than freehold properties in the same area, mixed-use developments[5] which combine hotels, retail space and residential units all within the same project, or high-tech projects to meet demand from the health-conscious. The buyer profiles for these properties will also change; they will increasingly come from China, Hong Kong, Singapore, Britain and Japan, and will be looking for permanent homes, second-homes and investment properties for rental.

However, the factors that could have the greatest influence on the direction of Thailand’s property market include: (i) slower-than-expected economic recovery; (ii) rising household debt; (iii) changing consumer behavior (especially with regard to housing) following the Covid-19 pandemic; for example, the work-from-home trend might increase demand for larger, low-rise housing units in the suburbs in favor of smaller condominium units near the city center; and (iv) the enforcement of the Land and Building Tax Act in 2020[6] may lead to more land transactions or it increase the tax burden on developers that hold properties for more than 3 years from the date of the implementation of the Act.

The outlook for potential areas in BMR in 2020-2022

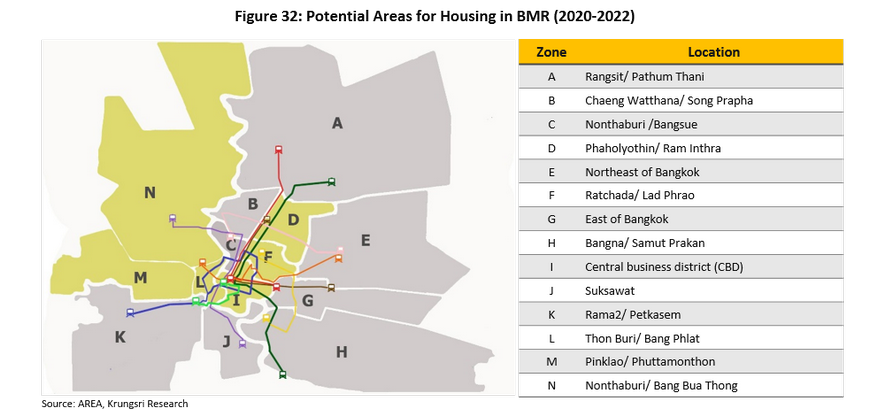

Krungsri Research believes that within the BMR, there are three zones near rapid mass transit extensions and two zones in the center of Bangkok that will have significant commercial potential between 2020 and 2022.

- Green Line Extension (North) (Mo Chit – Saphanmai – Khu Khot, zone D) is an older residential area, especially the housing and apartment projects. However, condominium projects have been springing up to meet rising demand, and that is anticipated to increase following the scheduled completion of the BTS extension line in 2020. The area is also home to several government offices, hospitals, universities, and is near Don Muang Airport. Currently, the average absorption rate for townhouses in the area is 33.9% and 21.1% for detached housing. Condominium projects are the most common in the area now and the absorption rate is 33.6%.

- Ratchada and Lat Phrao (Zone F) are centers for housing, business activities and entertainment. They can be considered a new extension of the central business district (CBD). Within the area, work is ongoing for the Yellow Line (Lat Phrao-Samrong) and should be completed by end-2020. This would improve travel connections to the rest of Bangkok and beyond. Currently, the majority of property developments in Zone F are condominiums and the area is popular with both Thai and foreign residents, especially the Chinese. The absorption rate for condominiums is 42.9%. For low-rise developments, although there is demand, the supply of suitable land is limited. The average absorption rate for detached housing and townhouses is 38.4% and 54.2%, respectively.

- The center of Bangkok (Zone I) consists of Silom, Sathorn, Rama IV Road, Ploenchit, Wireless Road, Asoke and Sukhumvit. They enjoy good travel connections, being served by two rapid mass transit networks - BTS and MRT - and the elevated expressway. The area is popular with foreigners, a large number of whom live in Zone I. For these reasons, residential properties here are more expensive than in other zones. The majority of new developments will be high-end condominium projects which typically attract foreign investors. Average take-up rate is 41.2%. Low-rise housing projects in this area would be dominated by premium projects with an average price tag of over THB20m. Each project would also offer a limited number of individual units. As such, absorption rates would also be high, averaging 43.2% for detached housing and 42.1% for townhouses.

- The area served by MRT Blue Line Extension (Zone L) and the area on the west side of Bangkok (Zone M) both offer convenient metro links to the heart of Bangkok and the central business district (around Silom and Sathorn roads). The Blue Line is fully operational along the entire stretch of Hua Lampang-Bang Khae and Bang Sue-Tha Phra, with an interchange to the Green Line at Bang Wa. There is also easy access by road (i.e. Petchkasem, Kanlapaphruek, Ratchaphruek and Phran Nok-Phutthamonthon Sai 4 roads). Accommodation in Zone L is mostly condominiums with an average sales rate of 39.5%. In Zone M, accommodation is mostly detached housing and townhouses with average sales rates of 29.4% and 30.7%, respectively.

- The western bank of the Chaophraya River (Zone N) is on the outskirts of the BMR but has potential given the area’s transport connections, including an expressway which takes commuters to central Bangkok. The zone is also served by two major retail malls (Central Westgate and Mega Bangyai), and in the future, the Bangyai-Kanchanaburi motorway will provide an additional transport link. These make the area attractive to property developers; low-rise project have been well received with 24.0% average absorption rate. The best seller is townhouses, followed by detached houses, with 25.8% average absorption rate.

Typically, new housing projects near rapid mass transit lines register higher absorption rates. But over the past two years, the rush to develop projects near mass transit lines has pushed up unsold inventory in some districts. This is especially the case near the Purple Line in zones N, M, C and D, where it will take some time for the market to absorb the surplus. Hence, new developments in these areas would normally see lower absorption rates. Nevertheless, given rising potential for property demand in these areas in the future and developers possibly reducing new launches, the oversupply problem should abate with time.

Krungsri Research’s view

Looking at 2022, major developers of residential projects in the BMR will see their business expand, while SMEs operating in this sector will experience stiffer competition which would reduce their earning. The business environment will be marked by weaker consumer spending power and rising development costs, especially land prices in areas with high potential. This would encourage developers to seek joint-ventures or mergers with other Thai real estate developers or foreign investors. By going down this path, incumbent developers will be able to build a more secure financial foundation and improve their competitiveness. But this will also alter the market structure by increasing the number of active large players. This means small operations with limited access to financing may have difficulty managing sufficient liquidity and may be forced out of the market.

- Large developers will register rising revenues, driven by their ability to adapt to the new industry structure and the advantages they enjoy over SMEs, especially in seeking cheaper funding through the stock and bond markets. On the other hand, SMEs will see their market share in an increasingly challenging business environment, and operations that are not part of an extended commercial network would find it hard to compete. Some SMEs will also find it more difficult to secure financing and loans from banks than large players. Hence, they may experience acute cash flow problems.

- Developers of condominium projects in central BMR and along metro lines are mostly large corporations that are skilled in project management, marketing and controlling working capital. But competition will worsen and restrict the developers’ ability to generate profits, and earning growth will remain close to 2019 levels.

- SME developers of condominium projects will likely focus on new projects up to eight stories high in more suburban areas, which are more remote and less popular than sites for high-rise and low-rise (townhouses and detached houses). Because of this, profitability may be lower than for low-rise projects. Some projects may even be loss-making.

[1] The new rules came into force in April 2019 and cover property loans, specifically loan to value ratios (LTVs) for new loans.

For purchasers of first properties with a value of less than THB10m, there is no change to the regulations.

For purchasers of second homes, if repayments on the first home are made on a schedule of 3 years or over, the deposit must be at least 10% of the loan value. If repayments on the first home are made on a schedule of less than 3 years, or if the value of the property against which the loan is made is over THB10m, the deposit must be at least 20% of the loan value.

For purchasers of a third (or subsequent) house, if the buyer has outstanding mortgages, whatever the value of the loan, the deposit must be at least 30% of the loan value.

Top-up loans are loans that are made against the same collateral as a housing loan or another loan (such as a ‘home for cash’ remortgaging-type arrangement) but which provide additional funds to the borrower. This excludes (i) loans made against accident and life insurance and (ii) loans made to SMEs.

[2] The cuts in tax for first-time home buyers provided for reductions in personal income tax (calculated according to the cost of purchases) up to a value of THB 200,000 for those buying houses and land together or apartments with a value of not more than THB 5m. These measures ran from April 30 to December 31, 2019.

[3] Charges for the transfer of title deeds and for registering mortgages have been cut from respectively 2% and 1% of the estimated value of the property to only 0.01% of its value. This reduction applies to (i) purchases of property with a value of not more than THB 1m made between June 24, 2019 and May 31, 2020 and (ii) those with a value of not more than THB3m made between November 1, 2019 and December 24, 2020.

[4] The ‘baan dee mee down’ program was run by the Ministry of Finance, and under this, a contribution of THB 50,000 was made by the government to the down-payments of those purchasing new properties. The program was limited to 100,000 applicants, who had to have an annual income of not more than THB 1.2m. The scheme ran from December 11, 2019 to March 31, 2020.

[5] Mixed-use real estate developments include both commercial and residential uses. Mixed-use developments may thus contain retail units, office space and residential accommodation within the same project.

[6] The Land and Building Tax Act B.E. 2562 was announced in the Royal Gazette on March 13, 2018. Payment of land and building tax under the new Act will be required from January 1, 2020, onwards. Fixed Maximum tax rates for Land and Buildings are classified by category as follows: 1) agricultural - 0.15%; 2) residential - 0.30%; 3) others - 1.20%; and 4) vacant]unused - 1.20% (if the land or building is unused for more than three years, the rate will be increased by 0.30% every three years, until the rate reached 3.0%)

.webp.aspx)