Executive Summary

In 2025, Thailand’s warehouse rental sector benefited from a surge in international trade, driven by accelerated front-running import activity ahead of the US tariff hikes. However, weak domestic purchasing power and a slowdown in tourism dampened consumer goods demand, limiting growth in warehouse space usage. For 2026–2027, demand is expected to rise gradually in line with the slow recovery of both the Thai and global economies. Nonetheless, the continued expansion of e-commerce will provide some support to the market.

Looking ahead, warehouse operators will face intensifying competition from both expanding large-scale providers and new market entrants. At the same time, rising business costs, including land prices and labor costs, will add further pressure. To remain competitive, operators will need to enhance efficiency through technology adoption and the development of ESG-aligned warehousing solutions that support long-term sustainability.

Krungsri Research view

The outlook for individual segments over 2025-2027 is as follows:

-

General-purpose warehousing: Revenue in this segment is expected to outpace other segments, particularly for facilities in high-potential locations. However, rising investment from existing and new players will increase supply, intensifying pressure on traditional warehouses, which are already facing oversupply. In response, operators are likely to pursue strategic partnerships and invest in technology to modernize their facilities, helping to better meet customer needs and support long-term revenue growth.

-

Temperature-controlled units (cold storage facilities): Revenue is expected to remain flat or rise slightly, supported by growing demand for fresh, frozen, and ready-to-eat foods, as well as pharmaceuticals, amid rising health awareness. However, the market will face challenges from increasing supply due to new entrants, along with rising labor and electricity costs, which will constrain profit margins.

-

Storage space for grain crops/silos: Turnover in this segment tends to fluctuate with agricultural output, which is highly sensitive to changing weather conditions. The continued oversupply in the market is prompting operators to adopt more aggressive pricing strategies to retain customers, though this may put profitability at risk.

Overview

Warehouses are spaces used for the storage of goods, usually as part of the distribution process, and so these support the operation of supply chains connected to manufacturing (for the storage of raw materials, parts, and components) and distribution (for the storage of finished goods). Rented warehouse space therefore forms a part of the logistics sector, and the industry has an important role to play in facilitating business operations in a wide range of industries across the manufacturing, trade and transport sectors.

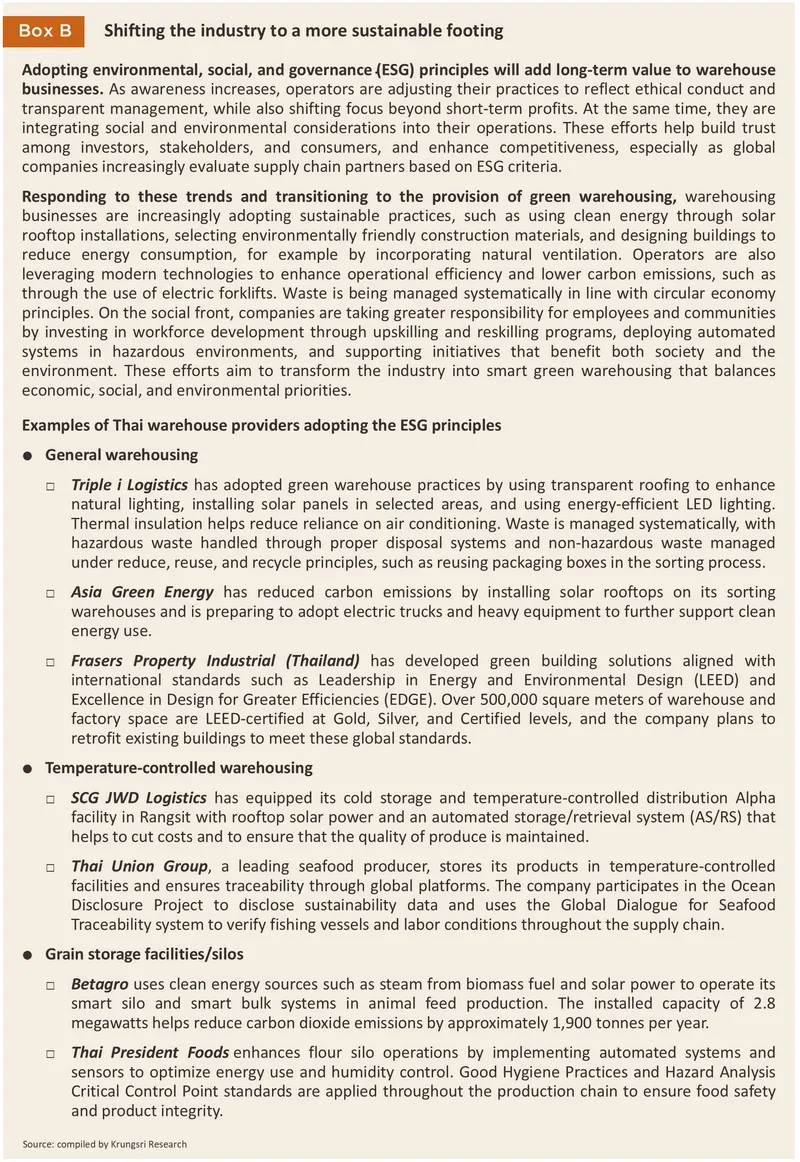

The Thai warehousing industry can be split into two main segments. (i) Traditional warehouses account for 95% of national supply and these typically emphasize the provision of a barebones service, with renters being provided with access to their warehouse space and basic utilities and amenities such as roads, electricity, water, telecommunications, and on-site security. (ii) Modern warehouses offer a much more comprehensive set of services, with operators providing tenants with access to appropriate digital technology and logistics systems that improve the efficiency of goods management (e.g., systems for storing and tracking inventory). These systems also make the procurement, management and distribution of inventory considerably easier, and this combines with the advantage of being less labor-intensive to make modern warehousing an attractive alternative that has the potential to meet market needs more precisely (Figure 1). At present, some providers of traditional warehousing are upgrading their facilities to offer modern warehousing services since this will then enable these companies to broaden their customer base and to generate receipts from additional services beyond core rent-based income streams. Players are also upgrading facilities in other ways, for example by investing in energy saving and environmental protection systems, which then helps to bring their facilities up to recognized industry standards (e.g., the Leadership in Energy and Environmental Design (LEED) scheme), and by installing facilities that increase protection against natural disasters, including floods and earthquakes. Warehouses have in addition been expanded by raising their floors and ceilings, which has the benefit of making the throughput of goods quicker and easier.

Within Thailand, the warehousing industry operates under the supervision of the Committee for the Management of Warehouses, Silos and Cold Storage Units, a part of the Ministry of Commerce. Organizations offering warehouses for rent in Thailand include state industries, such as the Public Warehouse Organization1/, private organizations operating under the management of and supported by the state (e.g., agricultural cooperatives), and fully independent commercial organizations.

The Department of Business Development (operating under the Ministry of Commerce) specifies three categories of rented warehouse operations. (i) General-purpose warehouses are buildings used for the storage of industrial and commercial goods (e.g., general consumer goods, raw materials, and parts and components). (ii) Cooled and frozen storage sites, or cold rooms, are temperature-controlled units that preserve (and so extend the shelf-life of) perishable food, such as seafood, dairy products, flowers, meat, fruit and vegetables, and medicines and vaccines. (iii) Silos are large temperature- and humidity-controlled cylindrical structures used for the bulk storage of cereals and similar crops, including rice, cassava, corn, flour, and rice bran. Selecting a warehouse that aligns with the nature of the business plays a crucial role, as it directly affects costs, transportation speed, and product quality.

The outlook for the warehouse industry is dependent on the general business conditions prevailing in manufacturing and commerce, together with overall levels of investment and household spending. The industry displays two important characteristics that help to determine its overall features: (i) Returns on investment typically occur over 8-13 years. On the one hand, upfront costs, especially those for land and construction tend to be high (on average, putting up new warehouses takes 6-18 months, though this depends on the footprint of the building), while on the other, income comes overwhelmingly from rent, which accumulates only gradually over the long term. Generally, rental rates will vary depending on the size of the space, the type of warehouse, its location, the provision of utilities, and the degree of competition in the area. (ii) The location of any particular warehouse plays a major role in determining its commercial success since this will strongly influence how well goods are stored and how easily they can be redistributed. Given this, evaluating the potential of different sites and the types of warehouses that ought to be constructed plays an important role in determining operators’ long-term growth in income.

Two types of rental agreement are used when renting or leasing warehouse space.

-

Short-term contracts (not exceeding three years) are generally agreed for those leasing traditional warehouse space. These are usually made with SMEs and/or businesses that experience uncertain or fluctuating business conditions, for example seasonal businesses such as traders in agricultural produce or players in the fashion trade. Operators working in this segment may thus experience higher levels of risk as a result of uncertainty over income.

-

Long-term contracts (longer than three years) are typically made with renters that are managing steadier and more predictable levels of stock, and these are generally for modern-style warehouse operations, though these may be either ready-built or built-to-suit spaces. The majority of players in this segment are larger operators that are active principally in the real estate and industrial estates industries, including WHA Corporation, SCG JWD Logistics, Wyncoast Industrial Park, and Frasers Property Thailand. Sites operated by these companies tend to be located close to industrial parks, distribution centers, and industrial and manufacturing zones. For landlords, agreeing long-term contracts offers the advantage of being able to manage sites more efficiently and of minimizing fluctuations in income.

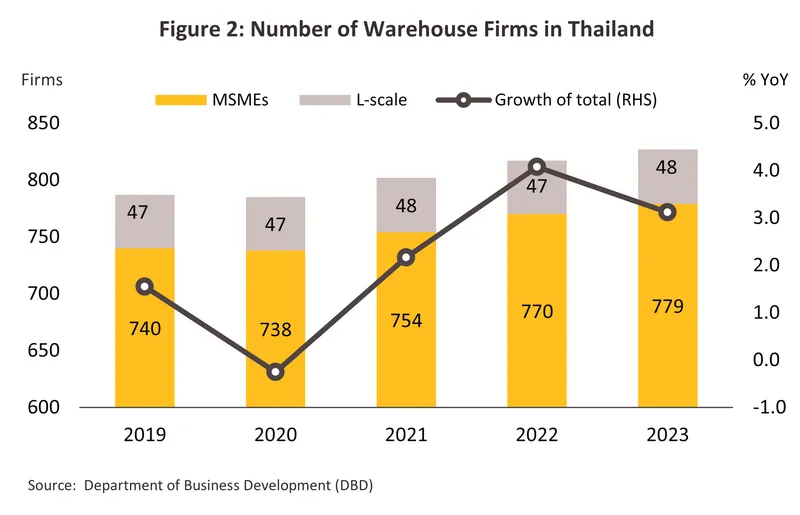

As of 2023, there were 827 companies offering warehouse space for rent in Thailand (Figure 2). These fall into the following two groups.

-

Large players: 48 companies (5.8% of the total number of operators) qualify as large operators. This group includes: providers of integrated logistics services and their affiliates, such as SCG JWD Logistics, Berli Jucker Logistics, and Mon Logistics Services; companies involved in food production and processing, such as Intersia, Mitr Phol Warehouse Company, and Pacific Cold Storage; distributors of household and office goods, such as Officemate Logistics and Tiger Distribution and Logistics; real estate developers, such as WHA Daiwa Logistics Property (a subsidiary of WHA Corporation) and Prospect Development; and joint ventures with overseas players, such as Suzuyo Distribution Center (Japan), WFS-PG Cargo (France), and Kerry Logistics (China/Singapore).

-

Medium, small, and micro enterprises (MSMEs): 779 companies (94.2% of all providers) fall into this category. Notable players include affiliates of SCG JWD Logistics, CRC Property and Development, MBK, K Line (Japan), Chia Tai, Lam Soon, MK Real Estate, and BFS Cargo DMK (a subsidiary of Bangkok Airways).

Situation

The warehouse industry saw improving conditions through 2024 thanks to a variety of factors. (i) The Thai economy continued to expand, helped first and foremost by growth in tourist arrivals, which jumped 20.1% to 35.5 million. This then added to demand for food, beverages, and consumer goods, while imports and exports also rose by respectively 6.3% and 5.8%, and since warehousing provides the keystone bridging and connecting the manufacturing, trade, and logistics industries, uptake of this was lifted further. (ii) Government spending rose 4.8%. (iii) Intensifying geopolitical and trade tensions are encouraging manufacturers to shift production facilities to Thailand and as such, FDI inflows surged 51% by volume and 255% with regard to the number of individual investment targets. (iv) E-commerce expanded by another 9.5% from its level a year earlier (source: Department of Business Development). Online retail performed especially well2/, and at THB 4.5 trillion, online purchases now account for 23.5% of all retail sales, up from 20.5% in 2022, thereby driving greater demand for warehouse space to store and distribute these goods. In response to evolving market conditions, players have expanded their customer base by developing new warehousing units, especially around the Rangsit-Pathum Thani area, which provides an important link connecting the Bangkok Metropolitan Region and nearby industrial zones. The situation for individual segments is described below.

-

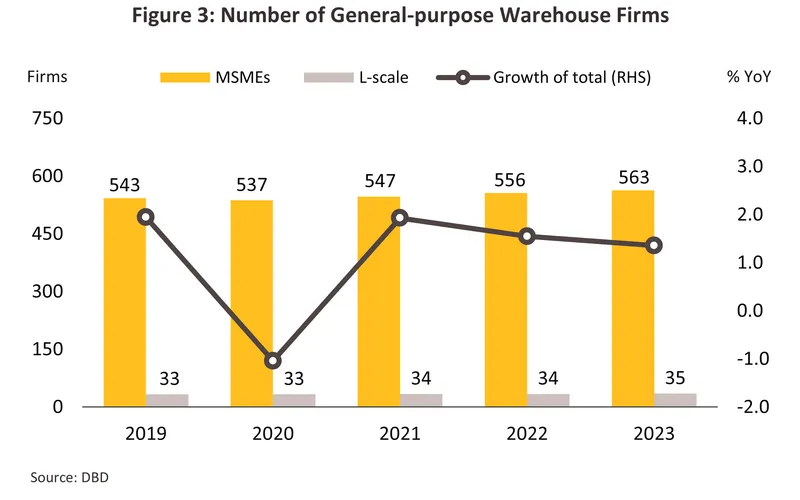

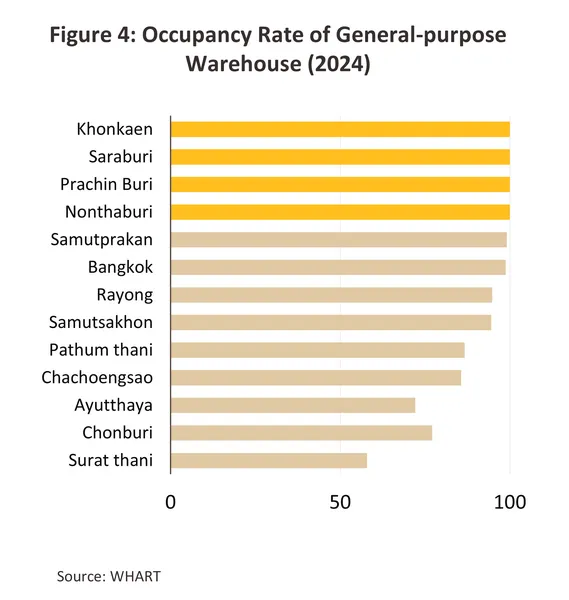

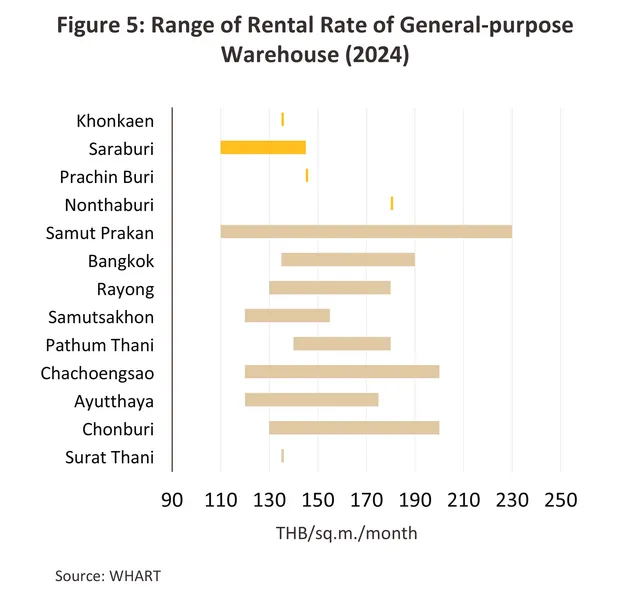

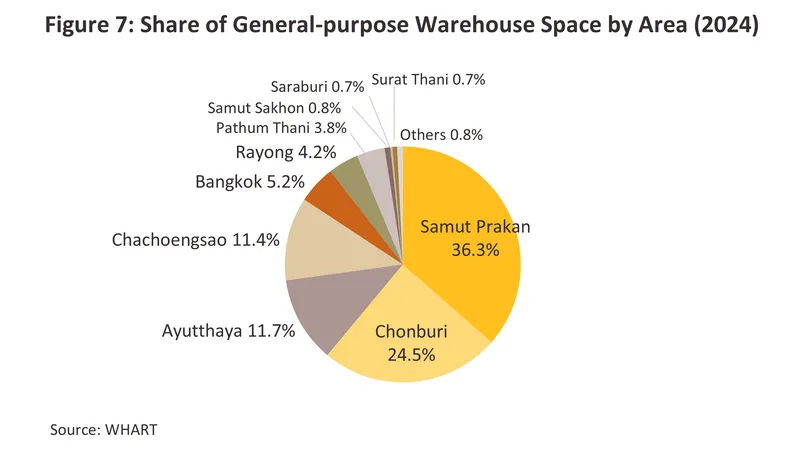

General-purpose warehousing: This segment accounts for over 70% of total supply and, as of 2023, 65% of the industry’s revenue. Supply is overwhelmingly concentrated in the central and eastern parts of the country, with 36% of rented warehousing space in Samut Prakan, 24% in Chonburi and 12% in Ayutthaya. There are 35 major players active in the segment (5.9% of all providers of general-purpose warehousing), though these operate primarily in a number of different industries, including logistics, the manufacturing and distribution of consumer goods, and the development and operation of industrial estates. The remaining 94.1% of players (or 563 companies) are thus micro, small or medium-sized enterprises (MSMEs) (Figure 3). Rental and occupancy rates can vary strongly by location and the level of competition in particular areas (Figure 4 and 5) but overall, 2024 rental rates rose 5.2-5.5% from a year earlier to reach averages of THB 110-230 per square meter per month (source: WHART). In the Bangkok Metropolitan Region (BMR) and the Eastern Economic Corridor, rates averaged THB 165/sq.m. (up 2.3%), slightly ahead of the central region’s average of THB 143/sq.m. (up 4.4%, though this excludes the BMR). Areas with the highest rates included Samut Prakan (THB 230/sq.m.), the industrial provinces of Chonburi and Chachoengsao (THB 200/sq.m.), the BMR, Pathum Thani, Nonthaburi and Rayong (THB 180-190/sq.m.), and Ayutthaya and Samut Sakhon (areas noted for their manufacturing and distribution centers), where rental rates averaged THB 175/sq.m. and THB 155/sq.m., respectively.

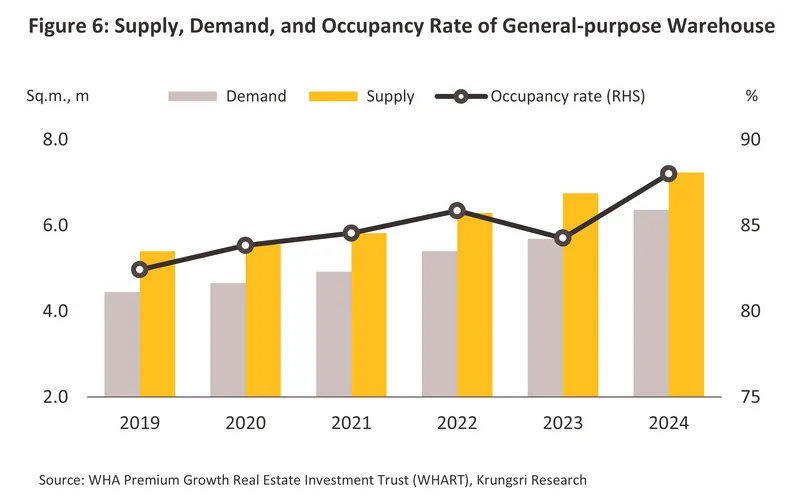

Demand for general-purpose warehousing has continued to rise steadily as the economy has grown and demand for consumer goods has expanded. In addition, demand has been boosted by companies including EV manufacturers and suppliers of related goods (e.g., auto and electrical parts and components) relocating production facilities to Thailand, worsening global geopolitical tensions that have encouraged an uptick in imports and exports as players look to hedge against potential shortages, and an increasing tilt among consumers towards online shopping that dates back to the pandemic. As such, demand for warehousing space rose 11.9% in 2024 to a total of 6.4 million sq.m. Providers3/ responded to stronger current and future demand by releasing an increasing amount of both ready-built and built-to-suit units, and thus supply expanded 7.2% to 7.2 million sq.m. Partly thanks to the gap between growth in supply and demand, the overall occupancy rate rose to 88.0%, up from the pre-pandemic level of 82.4% (Figure 6).

New supply that came to market in 2024 was largely located in areas that offered logistical advantages in the BMR, including around Suvarnabhumi Airport, the Bang Na-Trat highway in Samut Prakan, in Bang Pakong District in Chachoengsao Province, as well as in Pathum Thani, Ayutthaya, and the EEC. These areas are attractive to players since they provide easy access to distribution and travel networks, and are near to ports, Lat Krabang Inland Container Depot (ICD) and Suvarnabhumi Airport. Alternatively, new sites may be found in or near industrial estates that serve as distribution hubs for central warehouses.

-

Temperature-controlled units (cold storage facilities): Demand for cold storage units is benefiting from rising consumer interest in processed, chilled and frozen foods, and ready-to-eat meals (access to which is improving as more lines are stocked by offline and online retailers), an increase in tourist arrivals that is then supporting growth in the restaurant and hotel industries, stronger demand for imported foods, and the need to use temperature-controlled units to store exports of these (e.g., to ripen Cavendish bananas and to store durians, longans, Gros Michel bananas, etc.). With demand rising, investment funds have flowed into the segment, partly from players in other industries (e.g., the food processing, seafood, fruit and vegetable, bakery and dairy goods, and livestock industries) but the result of this has then been to erode existing suppliers’ customer bases.

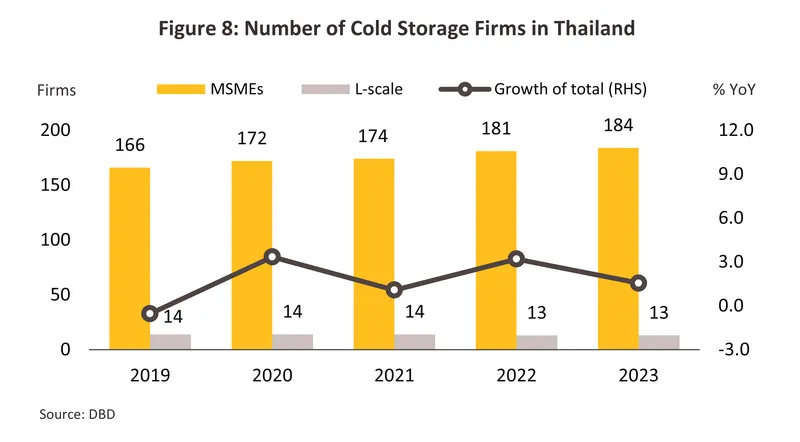

The latest data, which is correct as of 2023, show that there are 197 providers of cold-storage facilities active in the country (Figure 8), of which 13, or 6.6%, are classified as large enterprises. These are mostly subsidiaries of food manufacturers or food processors, and some of these now plan to expand overseas into the ASEAN region (e.g., into Malaysia, the Philippines, Indonesia and Vietnam), where they hope to meet demand from companies operating in the food and healthcare industries (source: SCG JWD Logistics). The remaining 184 companies (93.4% of the total) are thus micro, small and medium-sized enterprises. Players in this segment are currently adopting new technologies including robotics, automated storage and retrieval systems (ASRS), which facilitate faster sorting, storage and selecting of goods, and cold chain management systems (CCMS), which provide realtime tracking of goods in storage.

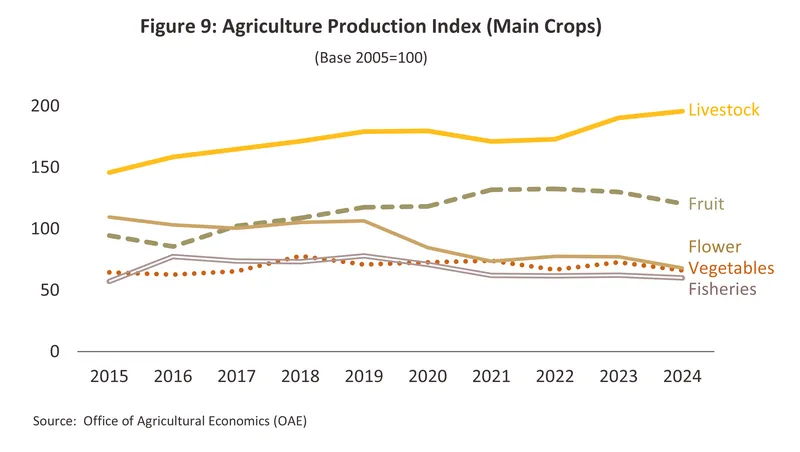

Overall demand was lifted through 2024 by an improving outlook for the economy and the ongoing rebound in the tourism sector, which together acted as tailwinds lifting sales of food and beverages. As such, demand for warehouse space to use in the transport and storage of frozen food and ready-to-eat meals likewise strengthened. In addition, Thailand’s position as a major supplier of food to world markets also meant that demand benefited from stronger sales of goods including milk and dairy products (+21.3%), tinned and processed fruits (+18.3%), tinned and processed seafood (+10.6%), fresh, chilled and frozen seafood (+5.7%) and processed, chilled and frozen shrimp (+29.6%). Nevertheless, unfavorable weather that included droughts in the first half of the year and then floods in the second impacted yields of some crops. Thus, the production index of vegetables slipped -8.9% relative to 2023, with the most notable declines seen in outputs of lychees (-65.8%), longkong (-25.7%), durian (-13.1%), orchids and cut flowers (-11.9%) and vannamei shrimp (-3.3%), and this then dragged on growth in demand for cold-storage facilities (Figure 9).

-

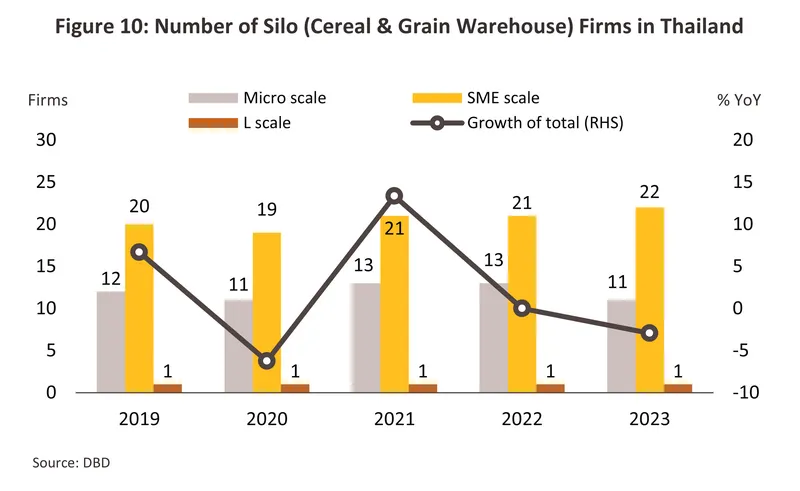

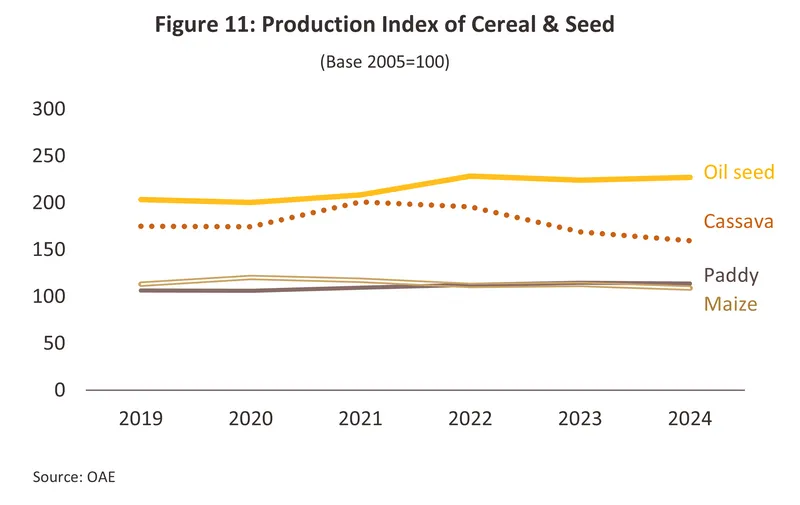

Grain storage units/silos: 97.0% of players in this segment are MSMEs (Figure 10), and 82.8% are located in the north, northeast or east of the country since these are the main areas for growing rice, cassava and maize. These areas also serve as collection points for agricultural products bound for export markets or for use in downstream industries in special economic zones or nearby areas. The remaining 17.2% of supply is found in the west and center of the country (including the BMR), areas where crops (e.g., rice, cassava, maize and coconuts) are grown and collected, and from which these are then distributed across the region to downstream food processors that are generally located in industrial areas.

Demand for silo storage space remained flat through 2024. Cereal crops suffered under the impacts of the drought that had begun in 2023, and so outputs of grains and other food crops declined by -2.4%. However, prices for some goods moved in the opposite direction, and so these rose 54.0% for rubber, 24.4% for sugarcane, and 13.7% for oil seed. Moreover, intensifying geopolitical stresses have lifted purchases of Thai food and agricultural products, and these factors then boosted demand for storage space.

Outlook

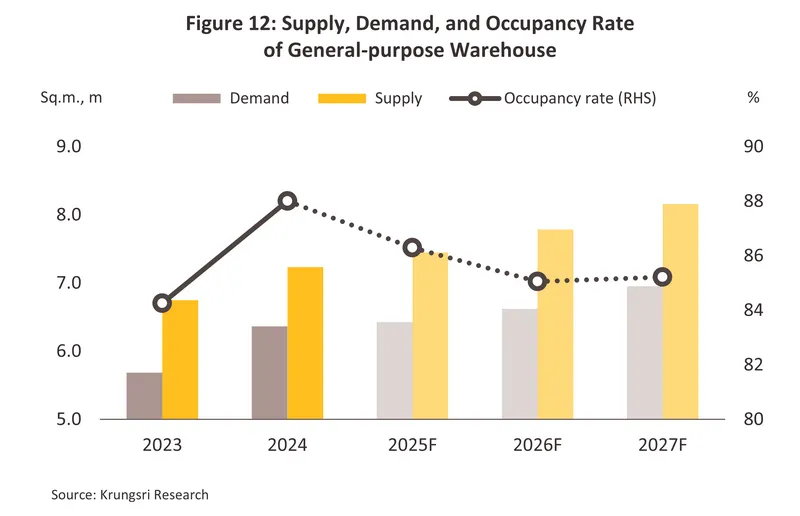

An uptick in international trade boosted demand for warehousing space through the first half of 2025. The announcement of sharp hikes in US tariffs earlier this year frontloaded demand, as companies rushed through orders before these new rates came into effect. Therefore, by value, imports to and exports from Thailand jumped by respectively 11.6% and 15.0% YoY in the period. At the same time, the agricultural production index rose by an average of 5.7% YoY, further contributing to demand for warehousing. However, the tariff hikes are coming into effect in the latter half of the year, and Thailand will feel the effects of the resulting softening of international trade. At the same time, weak purchasing power is undercutting domestic demand, further darkening the outlook for the industry. Nevertheless, imports from both the US and China may rise, in the former case because of recent negotiations that resulted in the 0% of duties on imports of over 10,000 products, while in the latter, faced with difficulties accessing the US market, Chinese exporters will likely step up efforts to sell cheap goods into the Thai market. As a result of these trends, declines in demand will be restrained and for 2025 overall, this is expected to rise 1.0% from a year earlier. This will, though, contrast with a forecast 3.0% increase in supply as earlier developments now come to market. These include over 200,000 sq.m. of new space from Origin Property that is due to become available over 2025 and 2026, plans by SC Asset to bring over 110,000 sq.m. of warehousing to market in the first half of 2025, with this rising to 150,000 sq.m. by the end of the year, and Sena Metrobox’s intentions to make available 25,000 sq.m. of new space in 2026. This new supply will be concentrated in the EEC, where it will serve demand from the auto, electronics, and fast-moving consumer goods industries.

Projected slow growth in the Thai economy will support only a weak expansion in demand for warehouse space over 2026-2027 (Figure 12), though operators will continue to add to the supply of both ready-built and built-to-suit units, the former targeting new and the latter existing clients. However, ‘green warehousing’ will become more common as players adapt to growing demand for goods and services that align with the theory of the circular economy and with ESG principles. The outlook for individual segments is described below.

1) The global and Thai economies are expected to experience only weak growth over the next two years, and so the IMF sees the world economy growing by 3.1% and 3.2% in 2026 and 2027. This sluggish outlook reflects the impact of higher US tariffs, which are expected to affect Thailand’s manufacturing sector across multiple industries, leading to weak domestic purchasing power and subdued consumer demand, including for warehousing services. However, the mild recovery in tourism, with international arrivals projected to reach 38 million tourists by 2027, will help support a modest improvement in demand for consumer goods.

2) More progress will be made on major government infrastructure projects, the buildout of industrial estates, and the development of special economic zones. Work will be concentrated in the Eastern Economic Corridor, where the implementation of phase 2 of the EEC development plan (2023-2027) will increase investment in infrastructure and transportation networks that connect to the wider region. These will include the Motorway Route 7 extension to U-Tapao Airport (construction is expected to start in September 2025 and the project should then be completed in 2028), and stage 1 of phase 3 of the Map Ta Phut Port development (due to be completed in 2027). Distribution centers will also be opened, including in the Nong Khai SEZ, the Chiang Khong multimodal transport and logistics center, and the logistics park in the Udon Thani industrial estate.

3) Thailand is welcoming international companies looking to relocate or expand their manufacturing and operating facilities. These operate in areas including electric vehicles, electrical appliances, electronics, datacenters, pharmaceuticals, and food processing. Some of the most high-profile examples of these include Tyson Foods, which wishes to set up a facility for producing meat- and plant-based proteins for distribution to the Thai and broader Asia-Pacific markets, Pfizer, which wants to export pharmaceuticals from Thailand, and SK Bioscience, which plans to manufacture vaccines in Thailand and then export these to the ASEAN region. Naturally, this will boost demand for warehouse space, though this will particularly affect units in duty-free zones, which will be sought after by companies connected to auto supply chains and import-export businesses looking to benefit from government tax incentives.

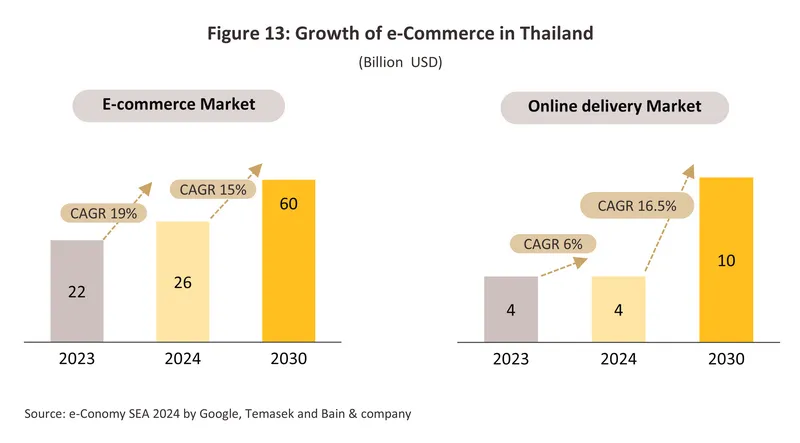

4) Continuing growth in e-commerce and logistics will benefit the industry. The e-Conomy SEA 2024 report indicates that over 2025-2027, the Thai e-commerce market will grow by 15.0% annually, with demand for express delivery services rising at the even faster rate of 16.5% per year (Figure 13). This will then lift demand for space to store goods in transit, though e-commerce fulfilment centers will enjoy especially strong levels of growth.

The supply of warehouse space is expected to expand by 3.0-4.0% per year. This will partly be driven by large players expanding into the industry from other parts of the economy (e.g., Origin Property, from the real estate sector, and Mister D.I.Y. Holdings, which has a background in retail). The overall rise in supply will outstrip growth in demand and so the occupancy rate is forecast to fall from 88.0% in 2024 to 85-86% over 2025-2027. New supply will largely be a mix of built-to-suit units rented out through long-term leases and ready-built warehouses that will meet short-term demand and will be available for rapid occupation. To help expand the domestic and regional B2B2C customer base, fulfillment centers will also be included in the mix, while players will increasingly develop smaller urban units that will meet demand from clients looking for ways to speed up deliveries. Alongside this, stock management systems will become more reliant on technology and companies will invest more heavily in energy- and labor-saving systems, which could include making use of robots to pick stock, sensors to track items, and energy storage devices to cut energy costs. This will then make it easier for landlords to raise rents and to agree leases that are longer than those typically agreed for traditional ready-built units.

-

Temperature-controlled units (cold storage facilities): The segment will benefit from: (i) expansion in consumption of seafood, chilled and frozen food, fresh fruit and vegetables, and ready-to-eat meals (Krungsri Research sees consumption of the latter rising by 5.0-6.0% annually); (ii) growth in non-food industries that need to use temperature-controlled storage facilities, including manufacturers of pharmaceuticals, vaccines, medical supplies, cosmetics, and animal feed; and (iii) an expected rise in food export as a consequence of: (a) growing concerns about health and wellness, which are driving stronger demand for health-conscious diets and functional food products; and (b) geopolitical tensions and climate volatility, which are disrupting yields of certain crops and prompting countries to increase food imports to build buffer stocks and strengthen food security. For 2024-2029, SCG JWD Logistics thus forecasts annual growth of 8.0% for the cold chain logistics industry.

Large players in this space will continue to add to the supply of cold-storage units. To speed up transportation and distribution times, these will typically be located in major provincial centers (e.g., Pathum Thani, Chiang Mai, Khon Kaen and Phuket) or in areas that are well integrated into transportation networks (e.g., Samut Sakhon and Samut Prakan). Beyond this, companies that are primarily focused on other parts of the economy will also invest in purpose-built temperature-controlled warehousing. This will include: (i) units in local areas that will be used to chill/freeze fruits or processed products on behalf of agricultural cooperatives and community enterprises prior to their distribution or export; (ii) cold-storage facilities operated by major seafood processors and producers of confectionary/bakery goods that will allow provenance and supply-chain checking to be carried out, as required by importing nations; and (iii) warehousing and agricultural distribution centers in airport free zones at Suvarnabhumi Airport. Incumbents currently planning to expand their supply of cold-storage space include Alpha Industrial Solutions, which is opening a 14,000 sq.m. cold-storage distribution center at its Alpha Rangsit site later in 2025, and SCG JWD Logistics, which intends to expand its provision of temperature-controlled space by 24% over 2024-2029, concentrating in particular on units in Pathum Thani, Saraburi, Chiang Mai, Khon Kaen, and Phuket.

-

Storage space for cereal crops/silos: Demand will tend to fluctuate with agricultural outputs of the major crops, which will in turn be determined by the climate. Overall, operators will tend to cut back on investments in additional supply as a result of: (i) the considerable pre-existing oversupply of storage space; and (ii) the anticipated onset of El Niño conditions in 2027 which is expected to reduce crop outputs. Nevertheless, periodic improvements in demand may be seen as a result of: (i) competition among silo operators, traders and middlemen, manufacturers of animal feed (interested primarily in maize) and power generators (interested primarily in wood chips) to build stocks for export or to sell back to the market during periods of high prices; and (ii) rising demand from downstream industries overseas (e.g., in 2025, China and Saudi Arabia plan to purchase respectively 440,000 tonnes and 20,000 tonnes of cassava from Thailand).

Areas that have the greatest potential to attract new investment inflows will most obviously include those that are in line for improvements to their logistics and transportation systems, which will in turn be dictated by the 2023-2027 National Logistics Development Action Plan. This will include: (i) Phases 1 and 2 of the construction of the twin-track railway4/, especially the Khon Kaen-Nong Khai section since this will connect to the Lao-China (Kunming-Vientiane) and Bangkok-Nong Khai high-speed rail lines; and (ii) the three-airport high-speed rail link, phase 3 of the development of Laem Chabang and Map Ta Phut ports, and the construction of the second (Nong Khai-Vientiane) and fifth (Bueng Kan-Bolikhamsai) Thai-Lao Friendship Bridges5/. When these projects are completed, multimodal transportation options within the region will be transformed and new opportunities to invest in areas that serve as transportation nodes will appear. Some of these are described below (Figure 14).

-

Warehouse space located close to centers of production: This includes the Bangkok Metropolitan Region, industrial estates, regional centers in the provinces, and areas that are recipients of government support for targeted industries. This includes Ayutthaya province (a hub for the production of electronics and electrical appliances that also connects to transportation routes to the North and Northeast) and the EEC (a center for manufacturing and international trade connected to the new S-curve industries, including EVs and electronics).

-

Warehouse space located close to consumer markets: In response to growth in e-commerce in the Bangkok Metropolitan Region (especially in Samut Prakan, which has become a center for e-commerce and logistics) and important regional centers (e.g., Chonburi, Phitsanulok, Nakhon Ratchasima, Khon Kaen, Ubon Ratchathani, and Surat Thani), micro-fulfilment centers may be set up in easy-to-access urban areas.

-

Warehouse space in border regions: Demand will tend to grow in these areas with progress on road, rail, air and sea transportation infrastructures that will then tighten connections between Thailand and neighboring countries, especially in areas where there are SEZs, including Tak, Mukdahan, Sa Kaew, Trat, Songkhla, Chiang Rai, and Nong Khai. The North will also develop as a gateway to further international trade thanks to the development of the Chiang Saen and Chiang Khong ports, which will connect Thailand, China and the Mekong River Sub-region. In support of this, the Chinese authorities have approved the designation of Guanlei Port in Yunnan Province as an official fruit import checkpoint (effective as of July 29, 2024), allowing Thai fruits to be shipped from Chiang Saen to China with fewer customs checks. Chiang Khong will also evolve into a logistics center linking road, water and rail transport modalities once the Den Chai-Chiang Rai-Chiang Khong line is complete. The development of cross-docking facilities will further boost cross-border trade, with the Natha and Nong Khai facilities helping to support Thai-Lao commercial exchanges; over the first 5 months of 2025, this came to a total value of THB 380 billion, higher than all other cross-border trade between Thailand and its neighbors. The Ministry of Commerce hopes to develop cross-border trade further, with the aim of pushing this to a total annual value of THB 2 trillion by 2027.

Players will continue to invest in new supply. This will involve partnering with other businesses to design logistics solutions that better respond to the needs of their customers and may include expanding operations into neighboring countries that are enjoying solid economic growth (e.g., Vietnam and Indonesia). This could take a form of joint ventures or 100% investments in countries including Vietnam, Indonesia, Singapore, Malaysia (in SEZs or free industrial zones), and the UAE (in duty-free zones). Thai companies that currently plan to invest overseas include WHA, which is partnering with the Japanese Daiwa House Industry to build a logistics center in the DPL Vietnam Minh Quang industrial estate, and SCG JWD Logistics, which plans to invest in temperature-controlled warehousing in Malaysia, the Philippines, Indonesia, and Vietnam.

Overall, competition is likely to strengthen in the coming period. (i) Large corporations, including WHA, Kerry Logistics, SCG JWD Logistics, and Prospect Developments, will continue to invest in the build out of new supply. This will include both ready-built and built-to-order units, and with an oversupply likely to develop in some areas, there will be only limited scope for increases to rents. (ii) New entrants are increasing their investments in warehousing space. These come especially from the real estate and construction industries6/, and these players may use more aggressive pricing strategies as they look to break into the market. (iii) Restrictions placed on the siting of warehouses by planning regulations will also affect the industry, for example by specifying that construction should be in ‘purple zones’ and that in ‘green zones’ (farming and agricultural areas), sites for the collection and cold-storage of goods cannot have a footprint in excess of 2,000 sq.m. In other zones, operators may face higher costs when trying to obtain construction permits. (iv) Costs are rising for land, construction, finance, utilities, technology and labor (the latter as a result of long-running shortages). In response to these challenges, providers of warehousing space will need to adjust their offerings, revise their operating procedures, and improve their productivity, for example by making greater use of technology, automation and AI, cutting costs, and switching to eco-friendly warehouse design. This will then help companies adapt to the needs of the market, in particular to increasing demand for speed, efficiency and supply-chain traceability, and over a more extended timeframe, this will then help to build long-term sustainability and competitiveness.

1/ The Public Warehouse Organization (PWO) is a state enterprise tasked with maintaining stable prices for agricultural products. To fulfil this remit, the PWO offers services for the storage and gradual distribution of agricultural produce to domestic and international markets, as determined by government policy. The PWO also offers services to state and private organizations for the depositing of agricultural goods and their use in ‘pledging schemes’, as well as operating a wharf for the loading and unloading of goods in transit in and out of the country.

2/ Trade Policy and Strategy Office, Ministry of Commerce.

3/ These included the following. (i) ESR Group is a major industrial real estate developer operating across the Asia-Pacific region. The company plans to open a 200,000 sq.m. warehouse and distribution site in Ayutthaya that will target players operating in the fast-moving consumer goods and e-commerce spaces. Work on this began in 2025. (ii) Prospect Development, a subsidiary of MK Real Estate, is investing in a 200,000 sq.m. project in Bang Pakong in Chachoengsao. The site will be located in Bangkok Free Trade Zone 4 (BFTZ4) and so this will be within the duty-free area close to Laem Chabang Port and Suvarnabhumi Airport. As of 2024, 100,000 sq.m. of the site was in operation, with the remainder due to open in 2025. (iii) Frasers Property Industrial (Thailand) is close to opening up the first phase of its 100 rai (16 hectare) development in the area of the Bang Na-Trat highway. The project should be completed in 2025 and will provide services to data centers and European semiconductor manufacturers. (iv) To meet growing demand from small businesses and e-commerce companies, the Thai Post Office is expanding its fulfillment centers in 8 provinces. These house storage, packing, distribution and payment processing facilities and together have a combined footprint of 3,235 sq.m.

4/ The twin-track railway from Kanchanaburi to Baan Phu Nam Ron will connect Thailand to Myanmar, the Den Chai-Chiang Rai-Chiang Khong and Baan Phai-Mukdahan-Nakhon Phanom sections will link the country to Lao PDR, the Map Ta Phut-Rayong-Chanthaburi-Trat line will connect Thailand and Cambodia, and the Hat Yai Junction-Padang Besar section will join Thailand and Malaysia.

5/ The rail bridge connection to the Second Friendship Bridge (Nong Khai–Vientiane) is still under construction, while the Fifth Friendship Bridge (Bueng Kan–Bolikhamsai) has been completed and is expected to open in December 2025.

6/ Over 2025-2029, SCX Corporation, a subsidiary of SC Asset, plans to open up 700,000 sq.m. of new warehousing space located in Bang Na, the EEC and Ayutthaya. ESR, a real estate investment management firm, is developing new warehouse facilities under its ESR Asia Laem Chabang and ESR Asia Wang Noi projects, with work on this expected to begin in 2025. Meanwhile, Pruksa Holdings is working with the Singaporean CapitaLand Investment Group, the Taiwanese Allies Logistics Property, and the Japanese Mitsui O.S.K. Lines to construct a fully integrated automated warehouse covering more than 200,000 square meters in the Omega Bangna Logistics Campus. The facility will operate as a distribution hub serving the ASEAN region, and the first phase of work is expected to be completed in early 2026.

.webp.aspx)