EXECUTIVE SUMMARY

Overall, Thailand’s automotive parts production is projected to expand by 1.5–2.5% per year over 2026–2028. This growth is driven mainly by increased manufacturing capacity for electric vehicle (EV) components, supported by investment promotion policies to meet rising global and domestic demand, alongside measures encouraging the use of locally produced components within the EV supply chain. Domestic sales are expected to grow by 2.0–3.0% per year. Key drivers include OEM demand in line with higher EV production under policies promoting domestically manufactured parts, rising motorcycle production to support the expansion of ride-sharing and food delivery services, and stronger demand for replacement parts (REM) as vehicle lifespans are extended amid economic uncertainty. Meanwhile, export values are projected to rise by an average of 1.0–2.0% per year. However, the industry faces demand-side challenges from US tariff measures and geopolitical tensions in the Middle East, a key market for components such as wheels, gearboxes, body parts, and drive shafts. On the supply side, constraints persist from shortages of semiconductors and raw materials, compounded by geopolitical risks, US controls on advanced technology exports, and China’s restrictions on rare earth exports.

Krungsri Research view

Earnings of auto parts manufacturers across segments are expected to continue growing, albeit at a modest pace, supported by the following factors:

-

Auto parts and components manufacturers: OEM parts will benefit from rising vehicle production in Thailand and overseas, particularly EV output, supported by excise tax incentives for HEVs and MHEVs, compensation production for passenger BEVs under the EV 3.5 scheme, and continued growth in global EV demand. Meanwhile, REM parts will expand in line with the rising cumulative registered vehicle base, as consumers increasingly seek to extend used vehicle lifespans, supporting replacement market demand.

-

Tire manufacturers: Large producers benefit from strong production standards and technological readiness to support the transition to EV tire manufacturing. In addition, Thailand remains a key global source of natural rubber, enhancing cost competitiveness. However, the segment continues to face headwinds from U.S. tariff measures—its largest export market—including new tariffs effective in 2025 and anti-dumping measures in place since 2021.

-

Distributors of auto parts and accessories: Wholesalers and retailers of new auto parts and accessories, as well as distributors of used parts (salvage), will benefit from the trend of extending vehicle lifespans, particularly among middle- to lower-income drivers, as purchasing power remains fragile amid ongoing economic uncertainty.

Overview

Policies Promoting the Internal Combustion Engine (ICE) Automotive Industry and Parts

Thailand’s auto parts industry has been continuously promoted by the government since 19631/. In the early stage, policies focused on supporting domestic production and use of auto parts, particularly through higher import tariffs on completely built-up (CBU) vehicles and complete knock-down (CKD) kits. Subsequently, the Board of Investment (BOI) introduced incentives, including corporate income tax and machinery import duty exemptions, to attract foreign investment into Thailand’s manufacturing base. In addition, the government imposed local content requirements for vehicle manufacturing; however, these have since been abolished2/, particularly following the expansion of free trade agreements between Thailand and its trading partners, including the ASEAN Free Trade Area (AFTA), the Japan–Thailand Economic Partnership Agreement (JTEPA), and the Thailand–Australia Free Trade Agreement (TAFTA), which accelerated reductions in import tariffs on CBU and CKD. Nevertheless, passenger car production in Thailand still relies on locally manufactured parts for around 60–80% of total component value, while Eco-cars and pickup trucks have a local content ratio of about 90%, and motorcycles use almost entirely domestically produced parts.

Both Thai and foreign investors have continuously invested in Thailand’s auto parts industry. Key local and joint venture companies include Thai Summit Auto Parts Co., Ltd., Sammitr Autopart Co., Ltd., Somboon Advance Technology Public Company Limited, and Thai Auto Pressparts Co., Ltd. Major global players that have established production bases in Thailand include Robert Bosch, Denso, Magna, Continental, ZF, and Aisin Seiki. As a result of foreign investment supported by government incentives, Thailand has developed strong supply chain capabilities in several key auto parts segments, including:

-

Rubber-based components: Thailand benefits from abundant domestic natural rubber resources, supporting the production of rubber hoses, belts, window seals, and automotive tires, which require advanced manufacturing technology.

-

Powertrain and engine components: This segment involves complex supply chains3/ and accounts for more than one-third of total production costs for internal combustion engine (ICE) vehicles. It has also been consistently promoted across the entire supply chain by the government, covering components such as radiators, exhaust systems, fuel supply systems, fuel tanks, ignition systems, and transmissions.

Transition from ICE Vehicle Promotion Policies Toward Electric Vehicles (EVs) and Components

Policies Supporting Battery Electric Vehicles (BEVs)

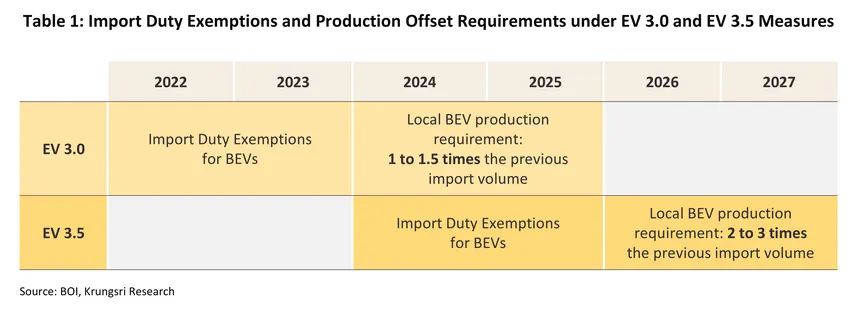

Policies to support the production and adoption of EVs in Thailand are regarded as a key pillar of the country’s energy strategy to achieve net-zero carbon dioxide emissions by 2050. In this regard, the National Electric Vehicle Policy Committee has set out a roadmap under the EV 30@30 policy4/. To stimulate domestic EV demand, incentives have been introduced under the EV 3.0 (2022–2023) and EV 3.5 (2024–2025) schemes5/, including direct subsidies, import duty reductions, and excise tax restructuring, together with production compensation requirements for EV manufacturing and conditions on the use of EV components, as outlined below:

-

EV 3.0 scheme: Supported manufacturers are required to undertake compensation production of electric vehicles during 2024–2025 at a ratio of 1–1.5 times their previously imported units for domestic sale (Table 1). They are also permitted to import nine categories of key EV components with import duty exemptions between May 16, 2022 and December 31, 2025, including (i) batteries, (ii) traction motors, (iii) electric vehicle compressors, (iv) battery management systems (BMS), (v) driving control systems, (vi) on-board chargers, (vii) DC/DC converters, (viii) inverters, including PCU inverters, and (ix) reduction gears6/.

-

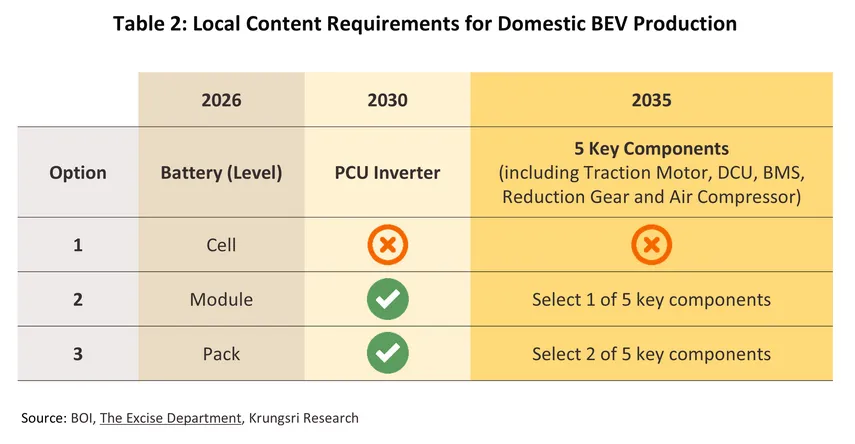

EV 3.5 scheme: Supported manufacturers are required to undertake compensation production of EVs during 2026–2027 at a ratio of 2–3 times previously imported units for domestic sale. Beneficiaries must also comply with new requirements on the use of domestically produced EV components, effective from January 1, 2026. Manufacturers must choose one of the following three options: (i) use domestically produced battery cells7/; (ii) produce battery modules with PCU inverters and one of five specified domestically manufactured key components; or (iii) conduct battery pack assembly with PCU inverters and two of five specified domestically manufactured key components (Table 2).

Policies Supporting Hybrid Electric Vehicles (HEVs)

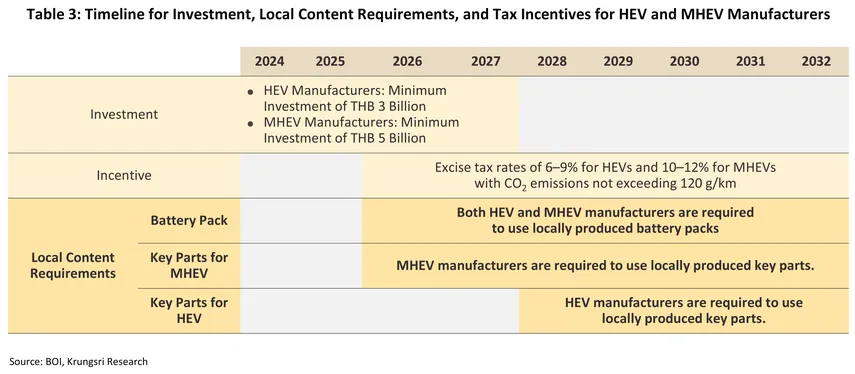

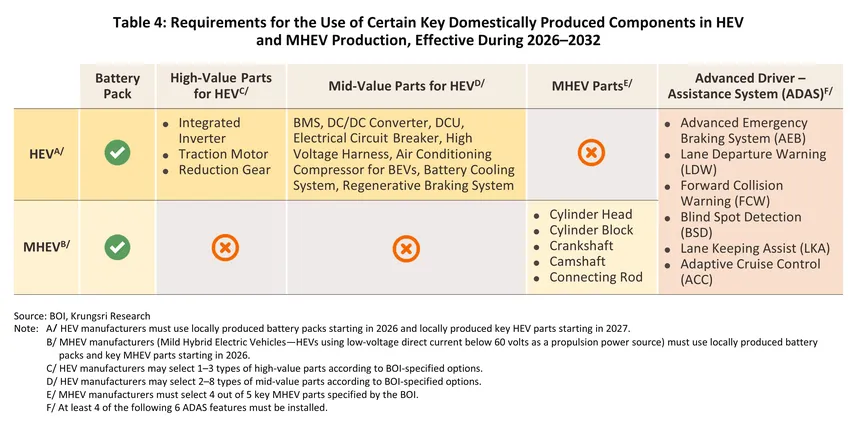

The Board of Investment (BOI) and the National Electric Vehicle Policy Committee (EV Board) have approved measures to support the transition to the electric vehicle industry, including reduced excise tax rates for HEV passenger cars and passenger vehicles with up to 10 seats for seven years (2026–2032) (Table 3), to stimulate domestic investment. The measures are subject to the following conditions and incentives:

-

Investment requirement: During 2024–2027, HEV manufacturers eligible for investment promotion are required to invest at least THB 3 billion.

-

Local content requirements: Manufacturers are required to use domestically produced key components in accordance with BOI criteria, as follows:

-

Battery Pack: Both HEV and MHEV manufacturers must begin using domestically produced battery packs from the start of excise tax incentives, effective 2026 onward.

-

Other key components for HEVs: HEV manufacturers are required to use BOI-specified domestically produced key components from 2028 onward (Table 4), comprising (i) high-value components—integrated inverters, traction motors, and reduction gears—and (ii) medium-value components—BMS, DC/DC converters, DCU, electrical circuit breakers, high-voltage harnesses, air-conditioning compressors for BEVs, battery cooling systems, and regenerative braking systems. Meanwhile, MHEV manufacturers must use at least four out of five BOI-specified key components from 2026 onward, namely cylinder heads, cylinder blocks, crankshafts, camshafts, and connecting rods.

-

Advanced Driver-Assistance Systems (ADAS): HEV and MHEV manufacturers must install at least four out of six BOI-specified ADAS features from 2026 onward, including Advanced Emergency Braking (AEB), Lane Departure Warning (LDW), Forward Collision Warning (FCW), Blind Spot Detection (BSD), Lane Keeping Assist (LKA), and Adaptive Cruise Control (ACC).

-

Excise tax incentives: Domestic manufacturers of HEVs and MHEVs will be entitled to excise tax incentives that maintain current rates based on CO2 emission criteria, provided they comply with the specified conditions for utilizing locally produced essential components. Specifically, HEV models with emissions not exceeding 100 and 120 g/km will be subject to tax rates of 6.0% and 9.0% respectively, whereas MHEV models will be taxed at 10.0% and 12.0% respectively.

In addition, the BOI approved the “Local Content Promotion” measure on July 22, 2025, aimed at encouraging investors in the EV-related industries to increase the use of domestically sourced materials. The measure seeks to reduce reliance on imported inputs and strengthen the capabilities of domestic supply-chain players by granting a 50% reduction in corporate income tax for two years8/ to eligible businesses in the EV industry, EV components, and electrical appliances sectors. Supported projects must meet the following criteria:

-

Eligible projects must be new investment projects applying for BOI promotion or existing projects still within the promotion period, covering the following activities: manufacturing passenger BEVs and PHEVs, manufacturing electric buses and electric trucks (battery-powered), and manufacturing equipment for EVs9/.

-

Projects must obtain “Made in Thailand (MiT)” certification from the Federation of Thai Industries, with minimum domestic content ratios as specified: (i) passenger BEVs must use domestically produced components of no less than 40% of total raw material value; (ii) PHEVs, no less than 45%; (iii) electric buses and electric trucks, no less than 40%; and (iv) EV equipment, no less than 15%.

Market Structure of Thailand’s Auto Parts Industry

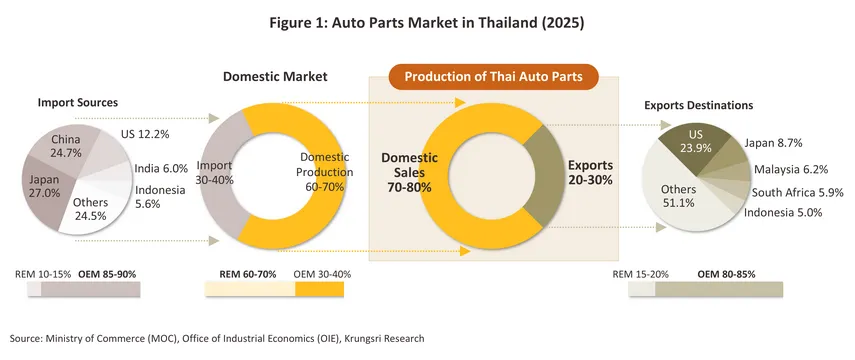

Thailand’s Auto Parts industry relies primarily on the domestic market, which accounts for around 60–70% of total industry revenue, comprising the Original Equipment Manufacturer (OEM) market for vehicle assembly and the Replacement Equipment Manufacturer (REM) market for replacement and aftermarket parts (Figure 1), as follows:

-

OEM parts: Account for 30–40% of the total domestic auto parts market value, expanding in line with vehicle production. More than 80% of parts used are domestically produced, while the remainder consists of imported high‑technology components sourced from parent companies or overseas suppliers, such as automotive electronics used in vehicle control systems (Microcontroller Chips: MCUs) from Japan. In addition, imports of ICE and EV components from China have increased to support Chinese automakers’ production bases in Thailand.

-

REM parts: Account for 60–70% of the total domestic auto parts market value, expanding in line with accumulated vehicle registrations in Thailand, driven by replacement demand over time and/or mileage. Distribution channels include authorized service centers and dealers, wholesale and retail auto parts stores, and independent repair shops. In terms of imports, REM parts account for around 10–20% of total auto parts imports, mainly from Japan (32.7%) and China (30.6%), followed by the United States (10.7%), which has been increasingly penetrating the Thai market.

Auto parts exports account for 20-30% of total industry revenue, comprising OEM parts (80–85% of total export value) and REM parts (15–20%). Thailand’s key export products include engines, wiring harnesses, body parts, glass, gear systems, tires, and rubber-based components. Thailand is considered highly competitive in the global market, supported by well-developed supply chain capabilities, accumulated technological expertise, and economies of scale, enabling the production of quality components at price levels acceptable to automakers. In addition, the country’s strategic location supports its role as a regional manufacturing hub for auto parts in ASEAN10/, making Thailand one of the world’s key global sourcing bases. This is reflected in 2025, when Thailand ranked first in ASEAN and 10th globally in auto parts exports across all categories. Key export items include automotive tires (3rd globally), other motorcycle parts11/ (5th), other auto parts11/ (8th), and engines (13th). Major export destinations are automotive production bases within ASEAN—namely Indonesia, Malaysia, Vietnam, and the Philippines—which together account for 25.5% of total export value, followed by the United States (23.9%) and Japan (8.7%).

Situation

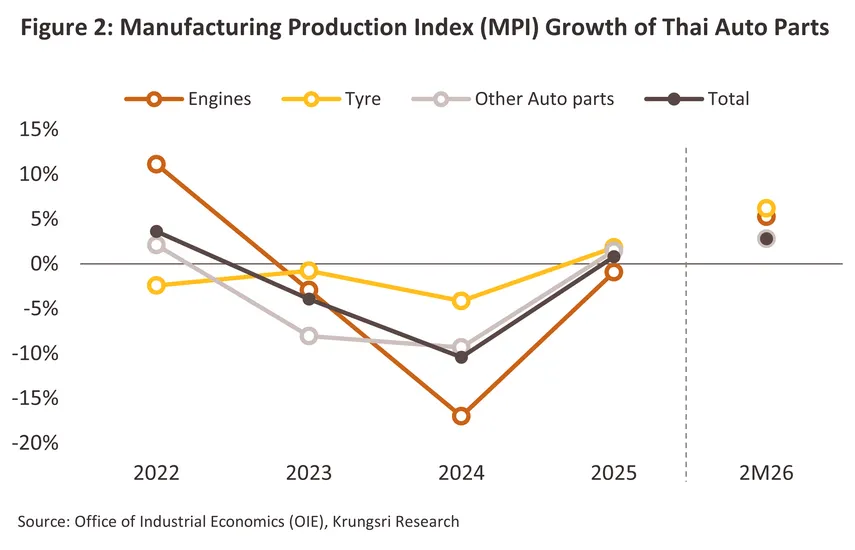

Overall auto parts production index in 2025 increased by 0.8% (Figure 2), driven mainly by growth in the vehicle tire production index and other auto parts (excluding vehicle tires and engines), which rose by 1.8% and 1.5%, respectively. Key growth drivers can be broadly categorized as follows:

-

Demand-side drivers: Demand-side drivers were supported by OEM demand, including (i) rising global EV production, which boosted Thailand’s export-oriented production of electronic control components and electric motors used in XEVs, as well as traditional ICE components for HEVs and PHEVs; (ii) continued domestic motorcycle production, which supported parts production for the local market, with nearly 99% of motorcycles produced in Thailand still being ICE-powered, relying largely on domestic supply chains; and (iii) the extension of vehicle lifespans in Thailand, which increased demand for replacement parts for vehicle maintenance.

-

Supply-side drivers: Supply-side drivers were supported by investment promotion measures for HEV and BEV components to accommodate rising EV production, including excise tax reductions for HEVs and MHEVs and the EV 3.0 and EV 3.5 schemes, which have encouraged auto parts manufacturers to invest in product development and production process improvements in recent years12/.

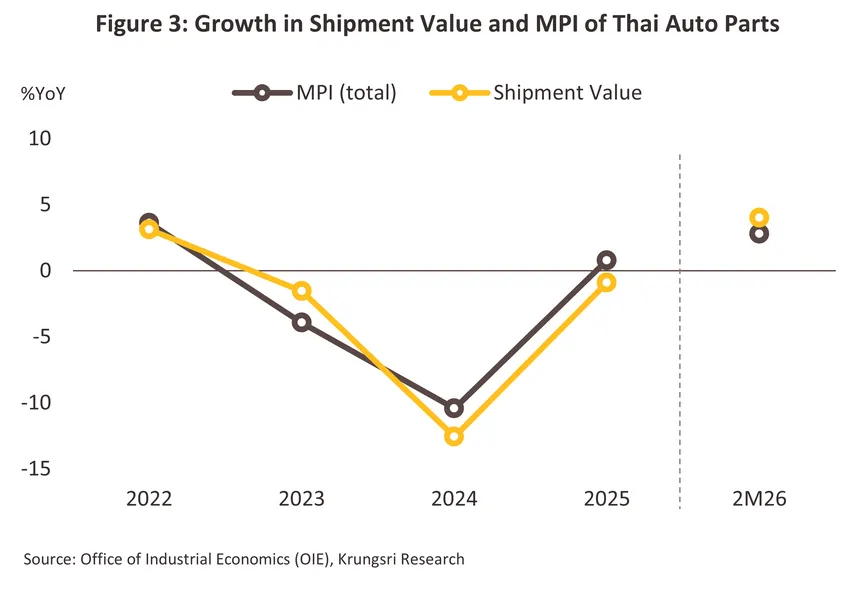

However, the overall auto parts production index grew at a slower pace than domestic auto parts sales and export value, which increased by 8.5% and 6.9%, respectively. This was constrained by (i) the decline in ICE vehicle production amid the accelerating global transition to electric vehicles, which require fewer parts—particularly engine and cooling components. The engine production index declined by -0.9%, in line with falling ICE output, as production of ICE passenger cars and pickup trucks dropped by -29.2% (to 247,929 units) and -3.0% (to 712,579 units), respectively, in 2025; (ii) stricter environmental standards in some trading partners, limiting Thailand’s production of components that do not yet meet required standards; and (iii) rising competition from imported parts, with total auto parts imports increasing by 7.7% in 2025, driven mainly by imports from China—the largest source, accounting for 30.9% of total import value—which surged by 34.2%. This trend may increase the risk of Thai exports being subject to rules-of-origin circumvention concerns.

In addition, although the auto parts production index began to show signs of recovery in 2025, the intense EV price war in recent years has pressured automakers—both ICE and EV manufacturers—as well as related auto parts producers to cut costs and reduce retail prices to maintain competitiveness. As a result, total revenue from domestic sales and exports declined by -0.9% (Figure 3), contrary to the upward trend in the overall auto parts production index.

During the first two months of 2026, the auto parts production index rose by 2.8% YoY, supported by the continued tailwinds seen in 2025. However, this growth remained below the expansion in revenue from domestic sales and exports, which increased by 4.0% YoY, reflecting a moderation in the EV price war in Thailand compared with the same period last year. This was partly due to automakers increasing the use of locally produced BEV components, which carry higher production costs than imported parts, in line with requirements under the EV 3.5 scheme. In addition, excise tax incentive measures also contributed to an expansion in MHEV production, which uses higher-value components than conventional ICE vehicles.

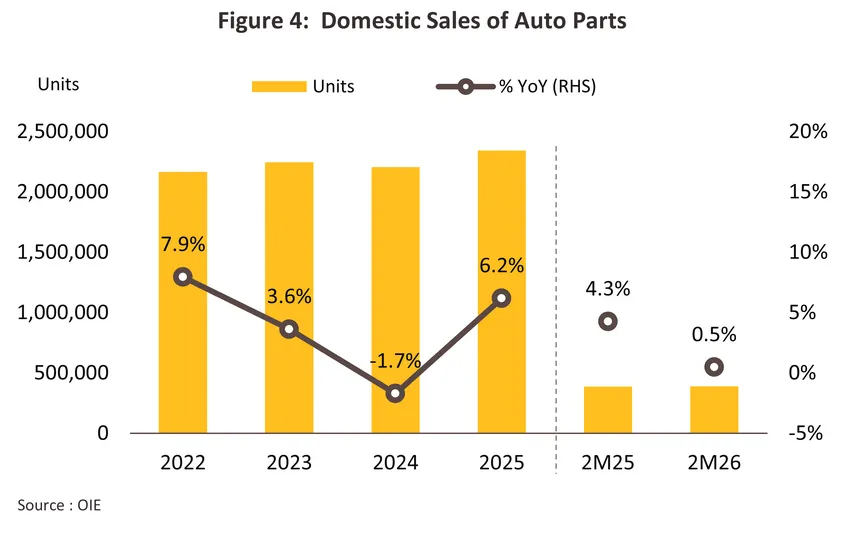

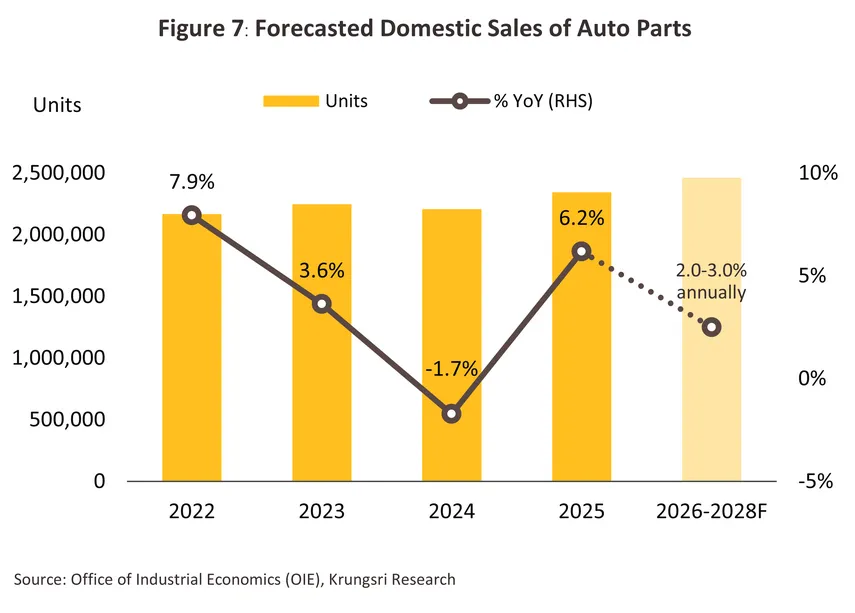

Domestic auto parts sales in 2025 increased by 6.2% to 2.3 billion units (Figure 4), supported by the following factors:

-

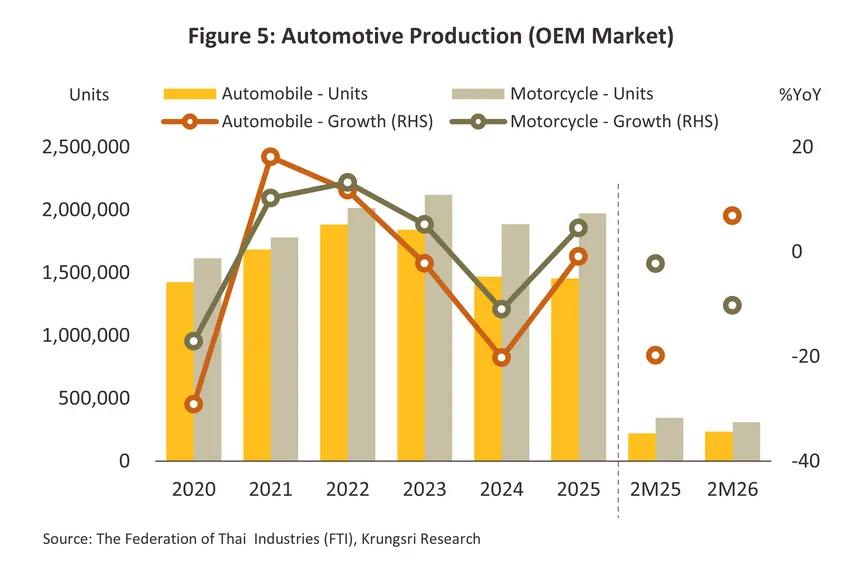

Motorcycle production rose 4.5% to 1,972,902 units (Figure 5), driven by stronger domestic sales, particularly (i) 125 cc motorcycles, which increased 15.6%, reflecting rising demand for motorcycles used for income-generating activities among rider groups, as well as some lower- to middle-income consumers opting for smaller motorcycles instead of cars amid a still-fragile economic recovery; and (ii) 250–399 cc motorcycles, which grew 3.3%, in line with higher hire-purchase loan approvals for mid- to large-sized motorcycles and sustained purchasing power among upper-middle-income consumers.

-

Passenger XEV production surged 45.1% to 302,527 units, led by HEVs, which accounted for 70.8% of total passenger XEV output. This supported demand for auto parts used in ICE powertrains and in‑vehicle electrical systems, as most HEV manufacturers in Thailand are established Japanese brands sourcing a large share of components from domestic supply chains. Meanwhile, passenger BEV production jumped 632.0%, driven by accelerated compensation production to meet EV 3.0 requirements by 2025, alongside policies promoting greater use of locally produced auto parts, such as interior fittings, leather seats, and body parts13/.

-

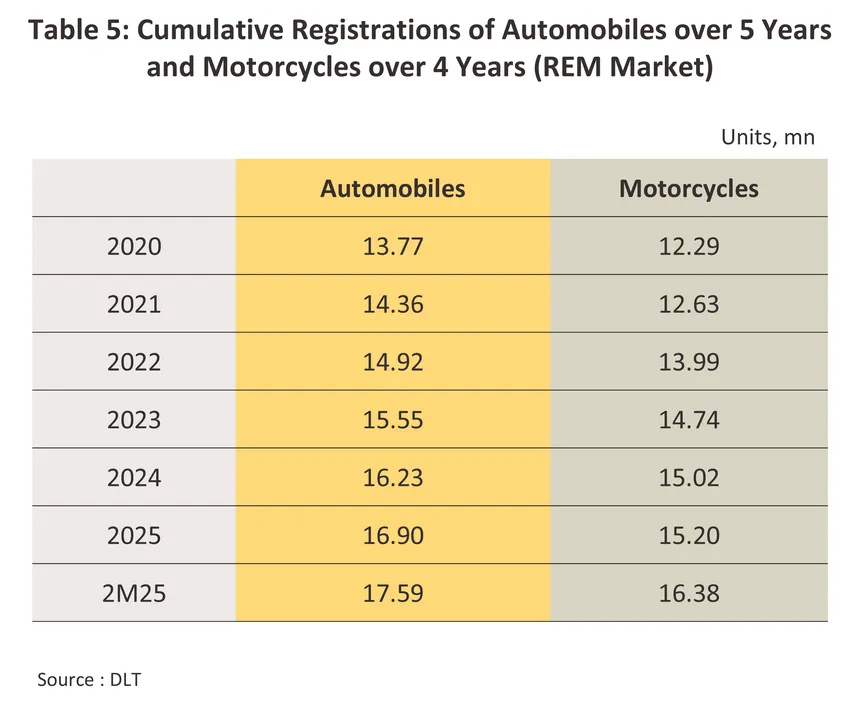

REM demand expanded in line with growth in the accumulated number of vehicles aged five years and older and motorcycles aged four years and older, which increased at average CAGR of 4.2% and 4.3%, respectively, during 2020–2025 (Table 5). In addition, many vehicle owners postponed new vehicle purchases and extended the lifespan of existing vehicles due to weaker purchasing power and persistently high household debt since the COVID-19 pandemic. Some consumers also shifted toward used vehicles, further boosting demand for replacement parts for maintenance and repair.

However, Thailand’s auto parts industry continues to face several headwinds weighing on domestic sales, including (i) a decline in overall vehicle production, particularly 1‑ton pickup trucks, which has continued since 2022 amid still‑weak purchasing power among lower‑ to middle‑income consumers14/. As a result, financial institutions remain cautious in approving loans for pickup trucks, which use more parts per vehicle than passenger cars and motorcycles; and (ii) import privileges for BEV components under the EV 3.0 scheme, whereby BEV manufacturers are still allowed to import high‑value BEV components15/ for assembly in Thailand during 2024–2025, such as batteries, traction motors, and battery management systems (BMS). This has limited the ability of most Thai auto parts manufacturers to integrate into the production supply chains of Chinese automakers in recent years.

During the first two months of 2026, domestic auto parts sales increased by 0.5% YoY, driven mainly by higher sales of auto parts in line with the 6.9% YoY growth in Thailand’s overall vehicle production. In contrast, motorcycle parts sales declined, tracking a -10.3% YoY contraction in motorcycle production. Overall, auto parts sales continued to be dominated by established Japanese automakers and motorcycle manufacturers, which predominantly source components from domestic supply chains.

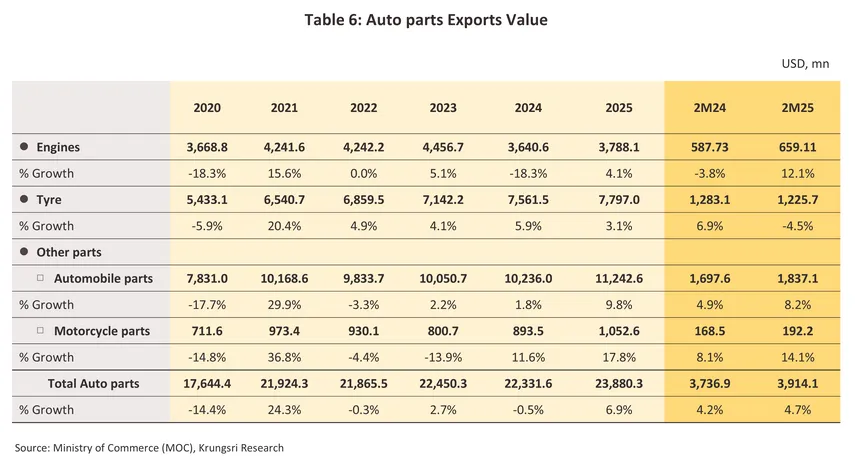

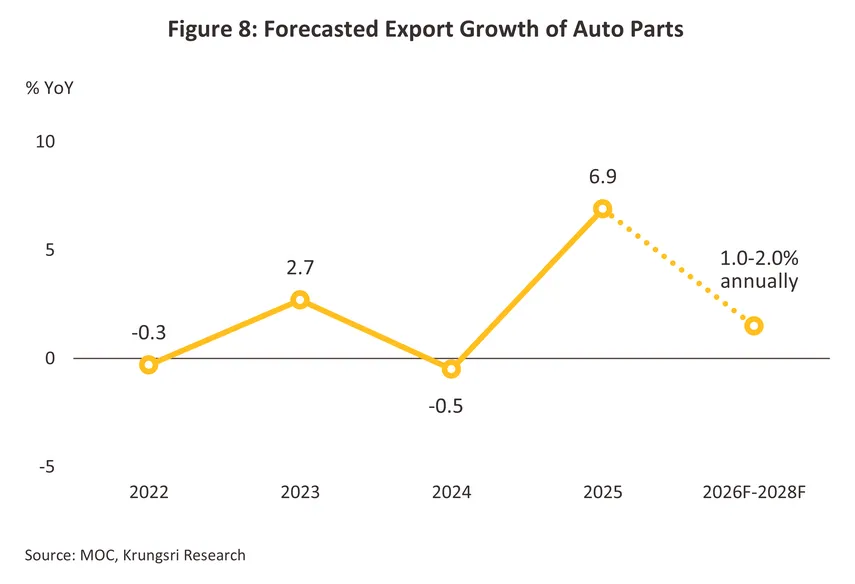

Auto parts export value increased by 6.9% to USD 24.0 billion (Table 6), broken down as follows:

-

Engines: Export value rose 4.1% to USD 3.8 billion, supported by stronger exports of ICE vehicles to trading partners that continue to rely on ICE vehicles, such as South Africa, Thailand’s largest export destination for piston ICE engines and related components, accounting for 10.6% of total exports in this category. Exports also benefited from countries with rising HEV and PHEV production, largely led by Japanese automakers that favor Thai-made components, notably Indonesia, Thailand’s second-largest market with a 10.1% share. Nevertheless, the increase in ICE engine-related exports in 2025 mainly reflected cyclical restocking demand from a low base in 2024, when exports in this segment contracted sharply by -18.3%, partly to support growing HEV production in several markets. Overall growth in this category remained below the 6.9% increase in Thailand’s total auto parts exports, consistent with the accelerating global transition toward EVs.

-

Tires: Export value increased 3.1% to USD 7.8 billion, supported by Thai manufacturers’ competitive advantages in durability, quality standards, and readiness to supply EV tires, which have gained popularity in recent years. Thailand continued to expand tire exports to countries with the top 10 highest vehicle production volumes globally, including Japan (+16.9%), China (+16.0%), South Korea (+9.9%), and the United States (+0.3%). However, growth moderated, partly due to the impact of U.S. trade measures, as the U.S. remains Thailand’s largest export market for vehicle tires (accounting for 45.4% of total tire export value), encompassing both new tariffs implemented in 2025 and anti-dumping measures in place since 2021.

-

Other auto parts: Export value rose 9.8% to USD 11.0 billion, despite headwinds from higher U.S. import tariffs on vehicles and auto parts—with the U.S. being Thailand’s largest export destination (a 16.3% share of total auto parts exports in 2025). While total U.S. auto parts imports from global suppliers declined -6.2% due to higher overall import costs, U.S. imports from Thailand increased 16.9%, particularly for components where Thailand has strong competitive advantages, such as suspension systems and parts including shock absorbers and drive axles with differential, which surged 132.9% and 33.4%, respectively. These components are largely supplied to support HEV and PHEV production lines that are gaining popularity in the U.S. Moreover, Thailand’s continued investment promotion measures for auto parts manufacturing across ICE and XEV segments since 2023 have helped strengthen domestic production capacity.

-

Motorcycle parts: Export value increased by 9.8% to USD 11.0 billion, supported by growth potential in Southeast Asian markets, where motorcycles remain the primary mode of transportation. Demand has been driven mainly by the replacement market, as consumers seek to repair and extend the lifespan of older motorcycles amid a slow economic recovery and still‑weak purchasing power across the region. At the same time, demand for new motorcycle assembly continued to expand in key markets, including Myanmar (+36.8%), the Philippines (+27.8%), and Cambodia (+17.1%). Nevertheless, Cambodia—Thailand’s largest export destination for motorcycle parts, accounting for 16.4% of total motorcycle parts export value in 2025—has faced growth headwinds due to escalating Thailand–Cambodia tensions since May 2025.

During the first two months of 2026, Thailand’s overall auto parts export value increased by 4.7% YoY to USD 3.9 billion, supported by continued demand from key trading partners with large production and sales volumes of HEVs, PHEVs, and ICE vehicles, including the United States, Japan, South Africa, Argentina, and Indonesia. This drove higher export values in engine-related parts (+12.1% YoY) and other auto parts (+8.2% YoY). Meanwhile, exports of motorcycle parts rose 14.1% YoY, led by markets with strong growth potential, particularly Southeast Asia (+5.0% YoY) and Brazil (+121.7% YoY), an emerging market benefiting from the rapid expansion of the delivery business. By contrast, escalating Thailand–Cambodia tensions resulted in a -16.3% YoY decline in Thailand’s motorcycle exports to Cambodia.

Outlook

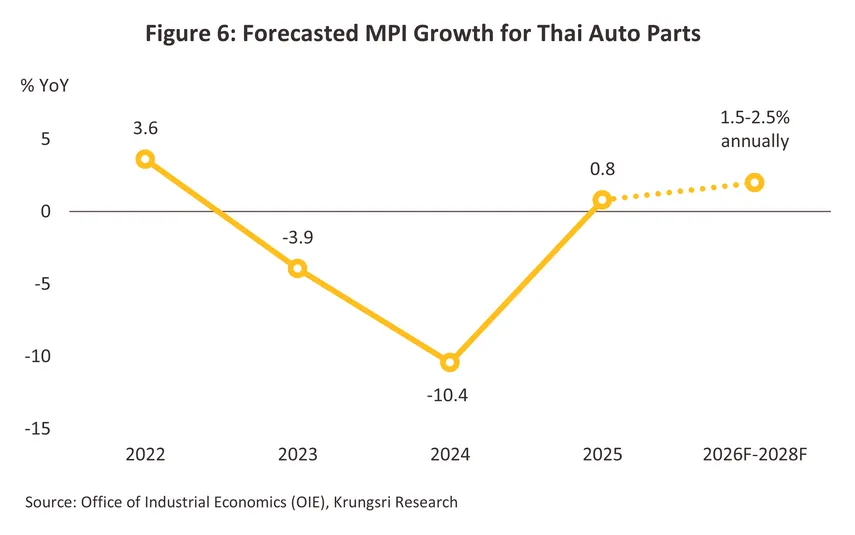

Thailand’s overall auto parts production is expected to expand at a moderate pace. The auto parts production index, a key supply-side indicator reflecting production trends, is projected to increase by 1.5–2.5% per year during 2026–2028 (Figure 6), supported by the following factors:

-

Expansion of EV component production capacity: This has been driven by a rise in BOI‑approved investment promotion projects16/ across the EV value chain to accommodate growing demand for EV components in both global and domestic markets, supported by recent policy measures. These include BEV compensation production under the EV 3.5 scheme and continued support for HEV production through excise tax restructuring, resulting in an average 5.6% per year increase in production capacity among Thailand’s overall auto parts manufacturers during 2022–202517/.

-

Local content promotion measures: This scheme offers a 50% corporate income tax reduction for two years to automakers and parts manufacturers within the EV supply chain certified as “Made in Thailand (MiT)” by the Federation of Thai Industries, thereby reducing reliance on imported components and stimulating domestic demand for locally produced EV parts.

However, Thailand’s auto parts production continues to face risks of supply chain disruptions and rising input costs, largely stemming from geopolitical tensions that exert pressure through multiple channels. These include (i) ongoing conflicts in the Middle East, which may lead to delays in raw material deliveries and higher prices for key inputs used in auto parts production, such as plastics and naphtha, raising the risk of production disruptions in automotive plastic parts and polymer systems over the period ahead18/; (ii) China’s export controls on rare earths and critical minerals, which could disrupt the production of related auto parts, including automatic transmission systems, throttle bodies, alternators, motors, sensors, seatbelts, speakers, lighting systems, electric power steering, and surround‑view cameras19/; and (iii) the ongoing tech war between the United States (and its allies) and China, arising from U.S.-led restrictions on exports of advanced technologies and potential retaliatory measures that could disrupt the production and export of chips and semiconductor equipment used in vehicle manufacturing20/.

Domestic auto parts sales are projected to grow by 2.0–3.0% per year (Figure 7), supported by the following factors:

-

Rising use of domestically produced HEV and MHEV components: Under policies encouraging HEV and MHEV manufacturers to use locally produced components from 2026 onward, through excise tax reductions, demand is expected to increase for key components, including (i) HEV components such as integrated inverters, traction motors, reduction gears, BMS, DC/DC converters, DCU, electrical circuit breakers, high‑voltage harnesses, and regenerative braking systems; (ii) MHEV components such as cylinder heads, cylinder blocks, crankshafts, camshafts, and connecting rods; and (iii) ADAS components, including Advanced Emergency Braking (AEB), Lane Departure Warning (LDW), Forward Collision Warning (FCW), Blind Spot Detection (BSD), Lane Keeping Assist (LKA), and Adaptive Cruise Control (ACC).

-

Increasing use of domestically produced BEV components: Under the EV 3.5 scheme, BEV manufacturers are required to undertake compensation production at a higher ratio of 2–3 times previously imported units, supporting stronger demand for BEV components. From 2026 onward, BEV manufacturers must also comply with local content requirements under EV 3.5, boosting demand for key components such as battery packs, PCU inverters, traction motors, drive control units (DCU), battery management systems (BMS), reduction gears, and air compressors.

-

Rising motorcycle production volumes: Growth is expected to be driven mainly by ICE motorcycles, particularly the 125 cc segment, which benefits from the continued expansion of ride‑sharing and food delivery services, as well as demand from lower‑ to middle‑income consumers and some provincial users who opt for motorcycles over passenger cars amid a slow economic recovery and tightened auto loan approval standards.

-

Growing demand for replacement parts (REM): Demand is expected to rise, particularly among lower‑ to middle‑income vehicle owners, who are likely to extend vehicle usage periods amid ongoing economic uncertainty driven by risks from U.S. trade measures, Middle East tensions, a still‑incomplete tourism recovery, elevated household debt, and rising living costs.

However, domestic auto parts sales may face constraints, resulting in slower growth than in previous periods, due to (i) a continued decline in ICE vehicle production amid the global transition toward EVs, together with concerns over higher fuel costs stemming from Middle East tensions, which continue to weigh on demand for ICE engine components; and (ii) limited access to Chinese BEV supply chains, as Thai auto parts producers generally face higher production costs than Chinese competitors. As a result, many Chinese BEV manufacturers operating in Thailand continue to import key components from China or bring in their own supplier networks21/. In addition, Thai manufacturers’ technological capabilities remain relatively limited compared with Chinese peers22/, constraining their ability to produce certain high‑value components in line with automakers’ required standards.

Thailand’s overall auto parts export value is projected to grow by an average of 1.0–2.0% per year (Figure 8), supported by several factors: (i) demand-side support from the continued expansion of global XEV production, which is expected to boost Thailand’s auto parts output, covering both BEV-related components and ICE components still used in HEV production during the transition period; (ii) supply-side support from ongoing investment promotion in components linked to the EV value chain and ADAS (Advanced Driver Assistance Systems), which enhance advanced driver-assistance capabilities. These investments enable components manufactured in Thailand to better comply with stricter environmental standards and safety requirements in key export markets; and (iii) import rule easing in certain major trading partners, notably Argentina (accounting for 6.1% of Thailand’s total export value in 2025), following the removal of the requirement for CHAS certification (Certificado de Homologación de Autopartes de Seguridad)23/, creating opportunities for Thailand to expand exports of safety-related auto parts such as brake linings, braking systems, tires, suspension components, and safety glass.

However, Thailand’s auto parts exports continue to face headwinds, including (i) the impact of U.S. trade measures, with the U.S. accounting for 16.3% of Thailand’s total export value in 2025, and the risk that Thai auto parts—particularly those linked to China—could be classified as transshipment products; (ii) disruptions stemming from Middle East conflicts (Thailand’s export share: 3.7%), which may affect key products that Thailand has exported in large volumes in recent years, such as wheels, gearboxes, body parts, and drive axles24/; and (iii) risks from Thailand–Cambodia tensions, as Cambodia is Thailand’s largest export market for motorcycle parts, potentially prompting Cambodia to shift sourcing to alternative suppliers in the future.

1/ In the early stage of Thailand’s automotive manufacturing development, production relied heavily on imports of complete knock-down (CKD) kits from parent companies or affiliated suppliers of multinational automakers, which were then assembled domestically into complete built-up (CBU) vehicles.

2/ The World Trade Organization (WTO) prohibits member countries, including Thailand, from imposing country-specific local content requirements, prompting

the Thai government to abolish such requirements effective January 1, 2000.

3/ Engine production requires more than 2,000 components and parts.

4/ Further details are available in Industry Outlook 2026-2028: Electric Vehicle Industry, page 4.

5/ Further details are available in Industry Outlook 2026-2028: Electric Vehicle Industry, page 5-7.

6/ Source: Ministry of Finance announcement dated May 25, 2023.

7/ The EV Board approved revisions to the EV 3.0 and EV 3.5 measures for EV batteries by extending the grace period for counting the value of Thailand-origin materials for imported battery cells by six months, from the original end-2025 deadline to June 30, 2026. During the extended period, the share of imported battery cell value eligible to be counted as domestically produced input will be capped at 10%, reduced from the previous 15% of the ex-factory EV price, to ensure compliance with Free Zone or Export Processing Zone criteria (Source: BOI (November 25, 2025))

8/ From the end of the corporate income tax exemption period

9/ This also covers the manufacturing of electrical appliances and smart electronics.

10/ Due to Thailand’s strategic location connecting East Asia and South Asia, supported by well-developed transportation infrastructure such as deep-sea ports and airports, as well as the Eastern Economic Corridor (EEC) covering Chonburi, Rayong, and Chachoengsao, which is well positioned to accommodate industrial growth.

11/ Excluding engines and vehicle tires.

12/ Further details are available in Industry Outlook 2025–2027: Automobile Industry, page 8–9.

13/ Source: PPTV (October 20, 2025)

14/ Further details are available in Industry Outlook 2025–2027: Automobile Industry, page 12.

15/ Namely 1) Batteries, 2) Traction Motors, 3) EV Compressors, 4) Battery Management Systems (BMS), 5) Driving Control Systems, 6) On‑board Chargers, 7) DC/DC Converters, 8) Inverters, including PCU Inverters, and 9) Reduction Gears (Source: Ministry of Finance announcement dated May 25, 2023)

16/ The value of BOI-approved investment projects in the auto parts sector increased by an average of 73.1% per year during 2022–2025 (Source: BOI)

17/ Production capacity increased from 2.3 billion units in 2022 to 2.7 billion units in 2025 (Source: OIE).

18/ Source: Nikkei Asia (March 18, 2026)

19/ Source: Autoblog (June 2, 2025)

20/ For example, a dispute between Nexperia, a Chinese chip manufacturer, and the Dutch government, where the company is headquartered, led Nexperia to temporarily cut chip deliveries to certain automakers. Honda was among those affected and was forced to reduce production in the United States during November–December 2025, as well as halt production lines in China during December 2025–January 2026. As a result, the company’s profits declined by more than USD 950 million, and it temporarily switched to using general‑purpose chips (Source: Nikkei Asia (January 11, 2026)).

21/ Source: Krungthep Turakij (August 31, 2025) and Krungthep Turakij (February 8, 2026).

22/ Source: Amarin TV (December 23, 2025).

23/ Source: Prachachat Business (September 16, 2025).

24/ Thailand’s auto parts exports to the United States in 2025 were concentrated mainly in wheels (30.6% of total auto parts

export value to the U.S.), followed by gearboxes (12.2%), body parts (10.6%), and drive axles (9.5%) (Source: Trademap).

.webp.aspx)