EXECUTIVE SUMMARY

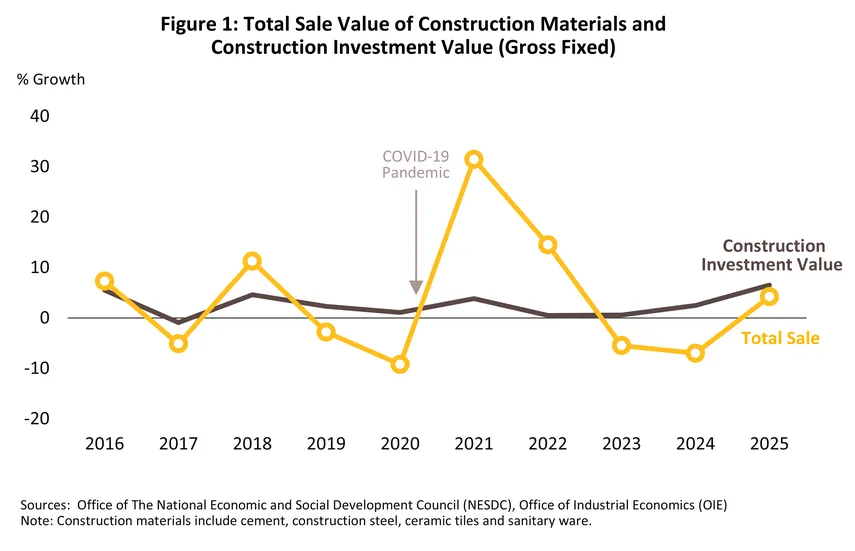

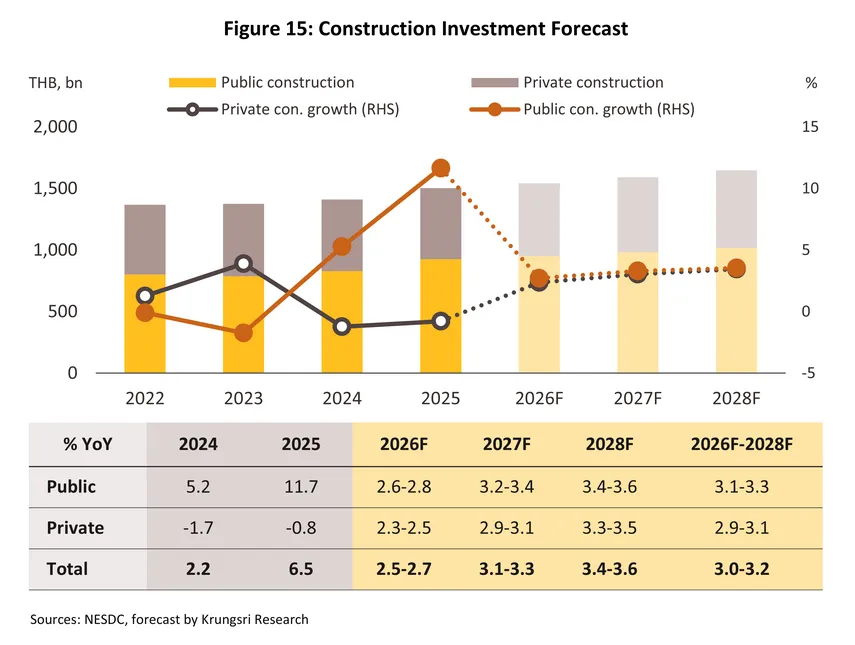

Overall demand for construction materials is expected to recover gradually over the 2026–2028 period. In particular, demand for structural materials will be supported by new investment projects and large-scale infrastructure developments. Meanwhile, although demand for finishing materials will continue to be driven by commercial and non-residential building construction, its growth will remain limited by the large inventory of unsold residential properties and purchasing power that has yet to recover. This is reflected in the construction market, which is projected to grow by 2.5–2.7% in 2026, before accelerating to 3.1–3.3% in 2027 and 3.4–3.6% in 2028.

In 2026, the business environment is expected to remain unfavorable for both construction material producers and traders due to energy and transportation pressures amid tensions in the Middle East. At the same time, the ability to pass on higher costs will remain limited amid subdued economic conditions and government price control measures. Nevertheless, the construction materials market is expected to improve in 2027–2028, supported by public investment projects and the gradual recovery of private investment, particularly in industrial estates and commercial buildings. However, the industry will continue to face pressure from low-priced imports from China, which continues to experience a property market downturn, as well as the transition of Thai producers toward environmentally friendly construction materials, which still involves higher unit production costs.

Krungsri Research view

Producers of construction materials:

-

Cement: Revenue is expected to remain stable or increase only slightly in 2026, before growing at a faster pace in 2027–2028, in line with the recovery in construction investment from both the public and private sectors. In addition, cement producers are expected to expand into new export markets, such as Australia and New Zealand, rather than relying primarily on CLM markets.

-

Construction steel (bar & section): Revenue of producers is expected to remain stable or contract slightly in 2026 due to competition from imports from China, where exporters have accelerated overseas shipments amid the domestic property crisis. Revenue is then expected to gradually recover in 2027–2028, although at a relatively modest pace, supported by the gradual increase in overall construction investment. However, competition from low-priced imports from China and Vietnam will remain a key pressure.

-

Ceramic tiles and sanitary ware: Revenue is expected to decline in 2026 due to the slowdown in the residential sector, despite support from commercial and other construction projects, which still account for a relatively small share of total revenue. Nevertheless, revenue is expected to improve during 2027–2028, in line with the recovery in the property sector and new investment. However, competition from low-priced imports will continue to limit growth to a relatively modest pace.

Traders of construction materials:

-

Modern traders: Revenue is expected to remain stable or grow only marginally in 2026 due to the economic slowdown, before gradually improving in 2027–2028. The improvement will be supported by: (i) resizing store formats to expand branches into residential communities; (ii) developing new retail formats in collaboration with major construction material manufacturers; (iii) strengthening distribution channels through partnerships with construction material traders; (iv) increasing the share of house-brand products; (v) expanding omni-channel distribution through online platforms and marketplaces; and (vi) placing greater emphasis on sustainability by allocating dedicated areas for environmentally friendly products (green materials) and adopting reduced-plastic packaging to better meet the needs of increasingly environmentally conscious consumers.

-

Traditional traders: Revenue is expected to decline or remain stable in 2026 due to weak purchasing power, particularly among middle- and lower-income consumers in regional markets, who continue to face high household debt. Revenue is then expected to gradually recover in 2027–2028 as economic conditions improve. For wholesalers, although revenue is expected to continue growing in line with the gradual recovery in the construction sector, they will continue to face intense competition from both modern trade construction material retailers and manufacturers that increasingly sell directly to end consumers. Meanwhile, revenue of retailers is expected to remain stable, with most revenue generated from repair and renovation materials, which are expected to continue recording modest growth. However, competitive pressure will remain intense, particularly from modern trade construction material retailers that continue to expand their presence in local markets.

Overview

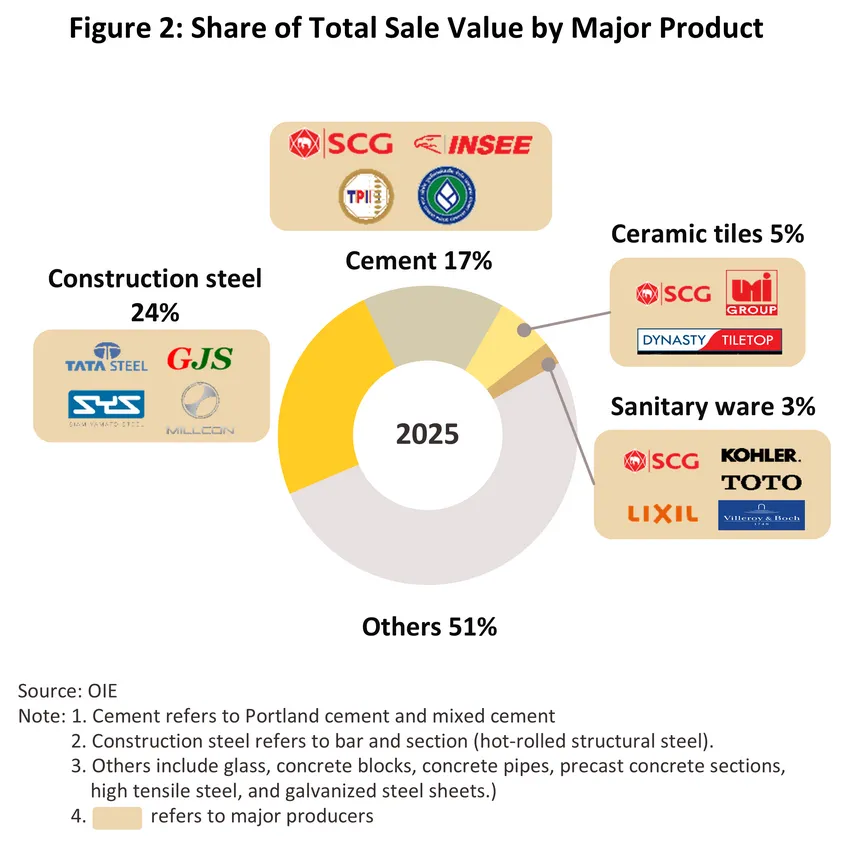

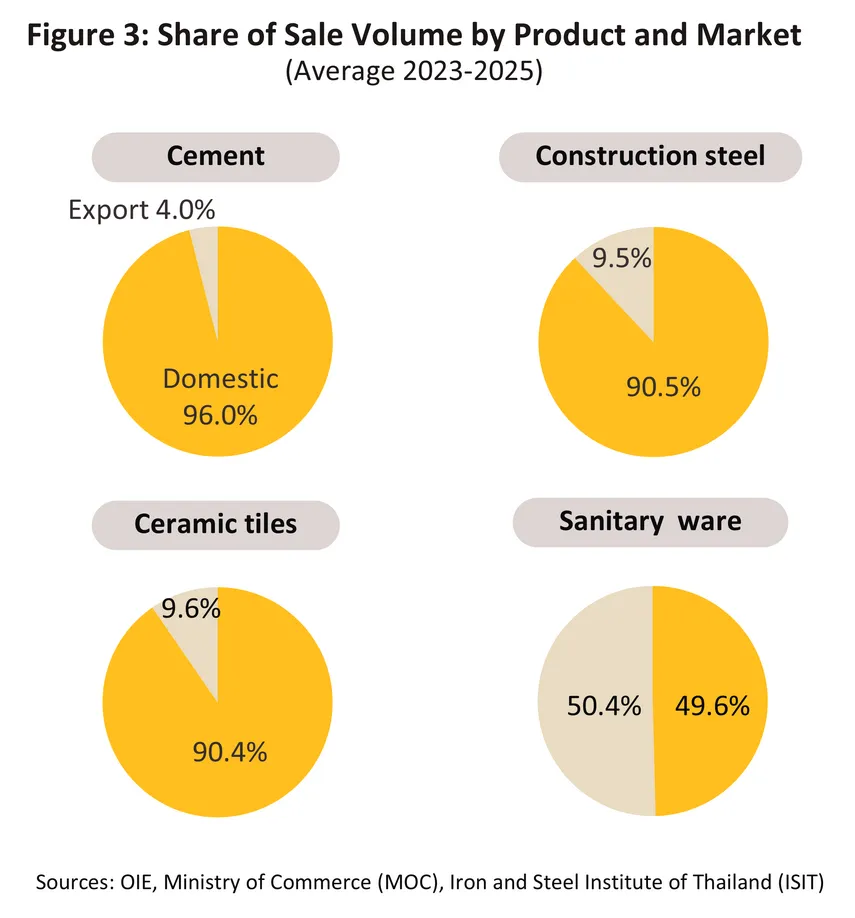

The construction materials industry is a key upstream sector supporting the construction and real estate industries, as construction materials account for as much as 50–60% of total construction costs. As a result, construction material sales generally move in line with trends in construction investment (Figure 1). Major construction materials can be broadly classified into two categories: structural materials (i.e., cement1/ and construction steel), which accounted for around 40% of total construction material sales by value, and construction finishing materials (i.e., ceramic tiles and ceramic sanitary ware), which accounted for nearly 10% in 2025 (Figure 2). Most major construction materials have a higher share of domestic sales than exports, with the exception of ceramic sanitary ware (Figure 3). Thailand serves as an export production base for several international sanitary ware brands that focus on high-quality products with distinctive designs. As a result, these products command high unit values, making exports to key markets such as the U.S. and Japan, where demand is concentrated in the premium segment, commercially viable. Meanwhile, although ceramic tiles are also exported, they face intense price competition, particularly from China and Vietnam, resulting in exports accounting for a significantly smaller share than domestic sales.

In addition, the transition toward environmentally friendly construction materials (Green Materials) is becoming an important trend in the construction industry, particularly for green cement and green steel. Although these products are more expensive than conventional construction materials, they are attracting increasing interest from manufacturers, consumers, and project developers seeking to align with the transition toward a greener economy and environmental sustainability, while supporting the long-term sustainability of construction projects.

Industry structure

-

Producers: There were 547 large and medium-sized manufacturers still in operation (latest data for 2024).2/ Most of these manufacturers benefit from advantages in terms of capital, production management, and bargaining power with suppliers (e.g., pricing and raw material delivery), enabling them to produce on a large scale and achieve lower unit production costs through economies of scale. In contrast, there were 2,033 small manufacturers, most of which have limited capital and therefore operate on a smaller production scale, resulting in higher unit production costs.

-

Traders: In 2024, there were 51,657 construction material traders,2/ comprising 1,738 large enterprises and 49,919 SMEs. These retailers can be classified according to their sales models and service formats as follows:

-

Modern Trader: Modern trade construction material retailers operate under systematic management, covering both front-end and back-end operations. They offer a wide range of products, including basic construction materials, repair and home improvement products, as well as furniture. Most are medium- to large-sized operators, benefiting from strong financial positions and efficient cost management. These retailers have continued expanding their branch networks into provincial areas to improve customer access, particularly to after-sales services, such as repair, and installation of materials and equipment for both interior and exterior applications. Major operators include HomePro (HomePro focuses on retail sales and home improvement products, while Mega Home focuses on wholesale customers and construction contractors), Thai Watsadu, Siam Global House, Dohome, and Boonthavorn (together accounting for approximately 30–40% of total revenue in Thailand's construction materials retail sector, Department of Business Development).

-

Traditional trader: Traditional construction material retailers are generally small operators with conventional management practices. They sell a range of products, from basic construction materials such as cement, sand, and hardware products (e.g., door latches and nails) to repair and home improvement materials, primarily serving customers within their local communities and nearby areas. Some retailers have adopted more integrated management practices to enhance their competitiveness against modern trade operators, including expanding product offerings (covering home improvement products), upgrading store layouts, improving distribution systems, particularly by adding online sales channels, implementing modern inventory management systems, and providing more efficient delivery services. Nevertheless, they continue to face disadvantages compared with modern trade retailers in terms of financial resources, marketing capabilities, and brand strength.

Situation

Construction material producers

In 2025, production and domestic sales of structural construction materials expanded strongly, supported by public infrastructure construction following the acceleration of budget disbursement after delays in the previous year. In contrast, construction finishing materials contracted in line with the slowdown in private residential construction (consistent with public construction investment, which increased by 11.7%, while private construction investment contracted by 0.8% in 2025). Meanwhile, export volumes declined3/ due to the continued slowdown in major trading partners' economies, resulting in high inventory levels for most manufacturers.

In 1Q26, production and domestic sales of most construction materials remained subdued. Although overall construction activity continued to expand (+6.1% YoY), many public construction projects had yet to enter the construction phase, while construction costs continued to rise. As a result, many contractors focused on reducing existing inventories rather than placing new orders. In addition, liquidity constraints faced by some businesses, together with the still-high level of housing oversupply, continued to weigh on demand for residential construction. On the external front, exports remained under pressure from weaker demand in key markets amid subdued business activity, as investment continued to be delayed due to the risks associated with the conflict in the Middle East. Exporters also faced intensifying competition, particularly from China, which continued to accelerate the export of excess supply. Meanwhile, imports continued to increase as low-priced products from China gained market share.

Cement

-

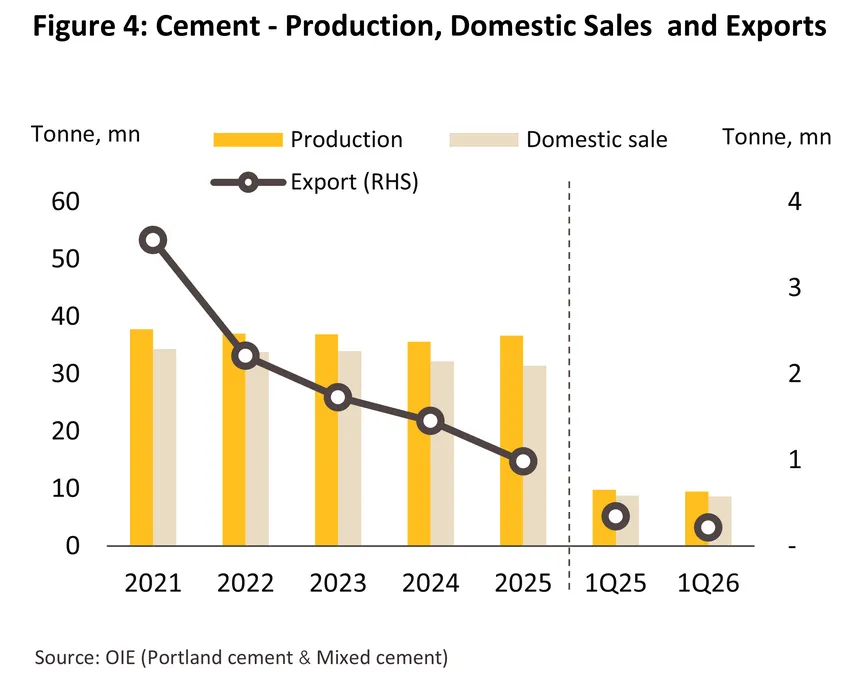

In 2025, cement production (Portland cement and blended cement) totaled 36.6 million tonnes, up 4.3%, while domestic sales reached 32.4 million tonnes, increasing by 0.6%. The main driver was stronger demand from public construction projects, compared with the low base in the same period of the previous year, which had been affected by delays in the enactment of the government budget. In particular, investment in transport infrastructure projects, such as highways, double-track railways, and mass transit systems, continued to move forward. These projects require large volumes of cement. In addition, private investment in factory expansion across several fast-growing target industries, including electric vehicles (EVs), electronics, and data centers, also supported cement demand, particularly in industrial estates.

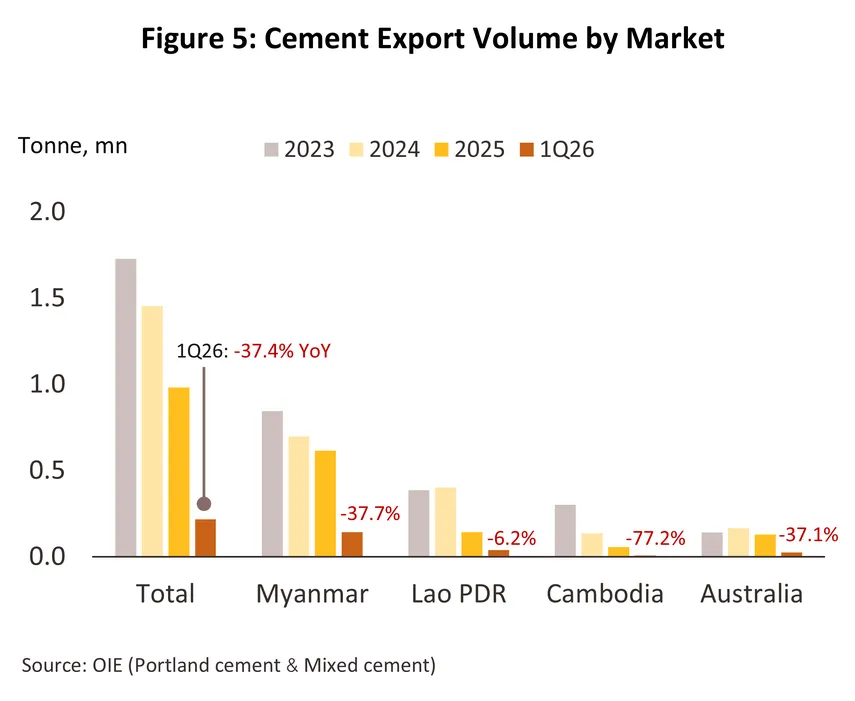

Meanwhile, cement exports (excluding clinker) declined by -32.5% to 0.98 million tonnes, with an export value of THB 2.5bn, down -30.1%, reflecting weaker demand in major export markets. Exports to Myanmar, which accounted for 63% of Thailand's total cement export volume, declined by -11.8%, partly due to increased cement imports from China. In 2025, China's cement exports (HS 2523) to Myanmar rose by 53.1%. Exports to Lao PDR, which accounted for 14% of total exports, fell by -64.8%, while exports to Cambodia (5% share) declined by -59.3%. The sharp contraction reflected subdued economic conditions as well as border closures following the escalation of the Thailand–Cambodia border dispute since mid-2025 (Figure 5).

-

In 1Q26, domestic cement sales declined by -1.6% YoY (Figure 4). Although public construction investment continued to expand, many projects remained in the budget disbursement phase rather than the actual construction stage, limiting the recovery in demand for key construction materials. At the same time, construction material and transportation costs increased in line with higher oil prices, which were affected by the conflict in the Middle East. As a result, the cement price index rose by 4.7% YoY, compared with a -0.6% YoY decline in the same period last year. Consequently, some contractors chose to use cement already available in their inventories instead of placing new orders, following stockpiling in the previous period. In addition, small contractors, many of whom had already been facing financial liquidity constraints, had limited capacity to absorb the higher construction costs. As a result, some construction projects were postponed.

Meanwhile, cement exports contracted sharply by -37.4% YoY to 0.22 million tonnes, with an export value of THB 598.3mn (Figure 5). The main drag came from Myanmar, which accounted for around 65% of Thailand's cement exports in the quarter, where export volume fell by -37.7% YoY amid ongoing unrest, intermittent closures of the Mae Sot–Myawaddy border crossing, and intensifying competition from low-priced Chinese cement. At the same time, exports to Cambodia, which represented around 3% of total cement exports, plunged by -77.2% YoY due to the prolonged closure of the Thailand–Cambodia border checkpoints. As a result, Thailand's overall cement exports remain under pressure in the near term.

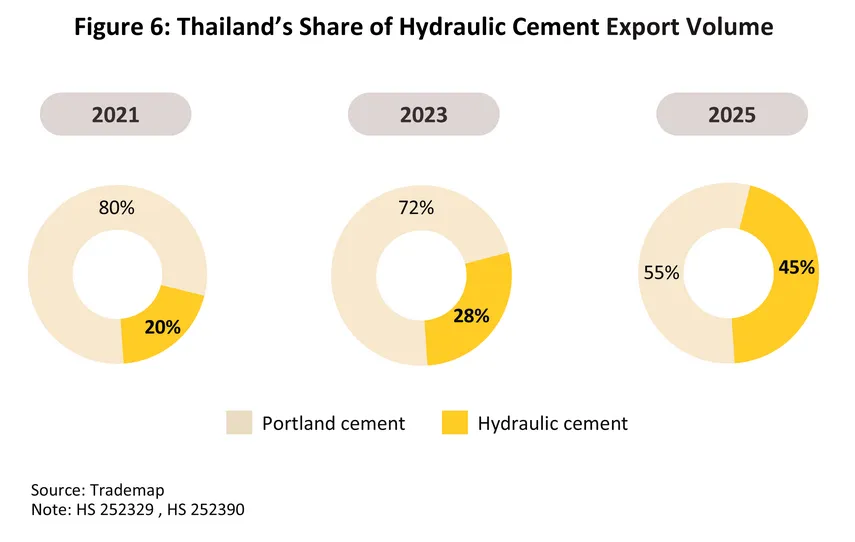

In recent years, large cement producers have increasingly adopted new technologies and innovations to improve their cement production processes in line with the principles of sustainable development. One notable example is the production of hydraulic cement, which uses environmentally friendly materials as substitutes for clinker4/ to reduce carbon dioxide (CO₂) emissions. In Thailand, the production of hydraulic cement has continued to increase to meet both domestic demand and export markets. In 2025, hydraulic cement accounted for 45% of Thailand's total cement exports (Figure 6). In addition, many producers have increasingly adopted renewable energy in their production processes, such as solar power and electricity generated from waste heat recovery systems (Waste Heat Power Generation: WHG).

Construction steel (bar and section)

-

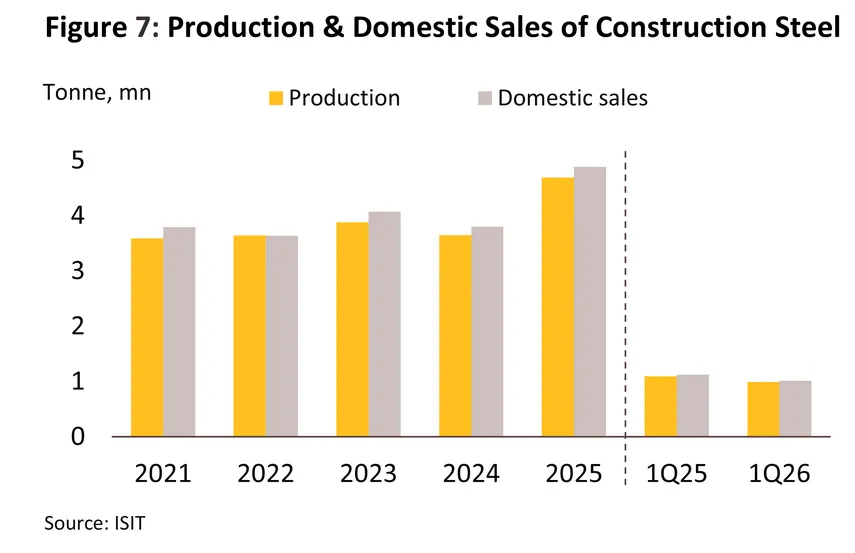

In 2025, Thailand's steel industry showed a relatively strong recovery. Overall production of bar and section steel reached approximately 4.69 million tonnes, an increase of 28.9%, while domestic sales rose by 28.5% to 4.88 million tonnes, following contractions in both production and sales in the previous year (Figure 7). The main driver was the acceleration of public infrastructure investment from a low base in 2024, particularly the resumption of major transportation and public utility projects. In addition, demand from private investment projects in the industrial and commercial sectors also increased, especially for the construction of factories, warehouses, and logistics facilities in industrial estates, most of which were projects in targeted industries, such as data centers and electric vehicles (EVs). Meanwhile, demand for construction steel from the residential sector had yet to fully recover.

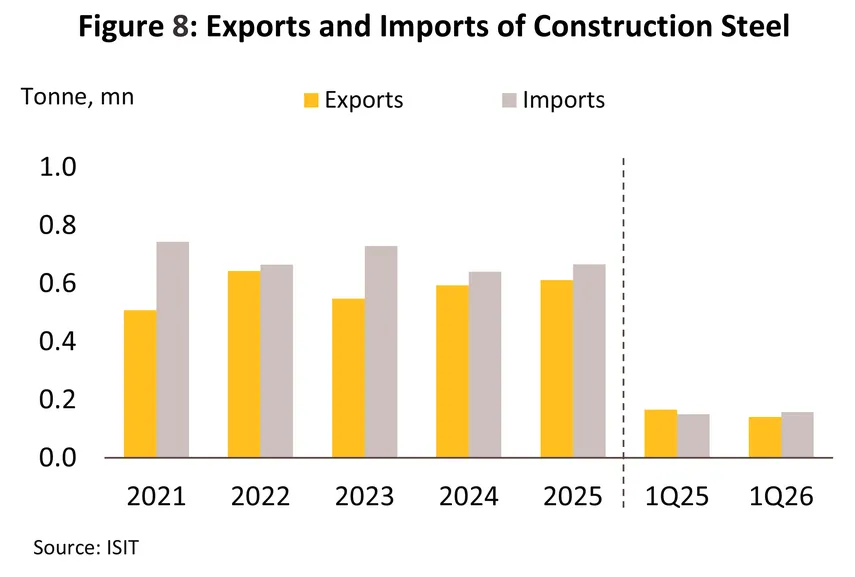

On the export side, bar exports remained broadly stable at around 0.3 million tonnes, increasing by only 0.1% (Figure 8). Export growth was mainly supported by the Lao PDR and Indonesia, where exports increased by 58.1% and 59.2%, respectively, driven by continued investment in urban development and infrastructure projects. This contrasted with declines in some major export markets, including Canada, Myanmar, and India, where exports fell by -6.6%, -2.6%, and more than -100%, respectively, as these countries increasingly relied on domestically produced steel and faced stronger competition from Chinese steel. Meanwhile, exports of section increased by 9.3% to approximately 0.33 million tonnes, with Singapore remaining the key export market. On the import side, imports continued to increase for both bar and section steel, rising by 3.3% and 14.8%, respectively. Most imports came from China, Japan, and South Korea, with China continuing to account for the largest share, representing approximately 51% of total steel imports.

-

In 1Q26, domestic production and sales of bar and section steel declined by -9.6% YoY and -9.8% YoY, respectively (Figure 7), reflecting weaker demand. Many contractors postponed new steel purchases in line with the slowdown in economic activity and investment following the Middle East crisis. In addition, contractors continued to draw down steel inventories that had been accumulated when steel prices fell significantly in 2025, before prices gradually increased from March 2026 onward. As a result, steel demand declined markedly, particularly in construction activities with relatively low steel intensity, such as building renovation and utility infrastructure works.

Meanwhile, steel exports totaled 0.14 million tonnes, down -15.5% YoY (Figure 8), with declines recorded in both bar steel (-27.6% YoY) and section steel (-2.2% YoY). In contrast, steel imports continued to increase by 4.6% YoY, driven by inflows of low-priced steel from China. As contractors sought to control costs amid rising construction material prices, higher energy costs, and increasing transportation costs, domestic steel producers continued to face intense price competition, putting further pressure on capacity utilization in the domestic steel industry.

-

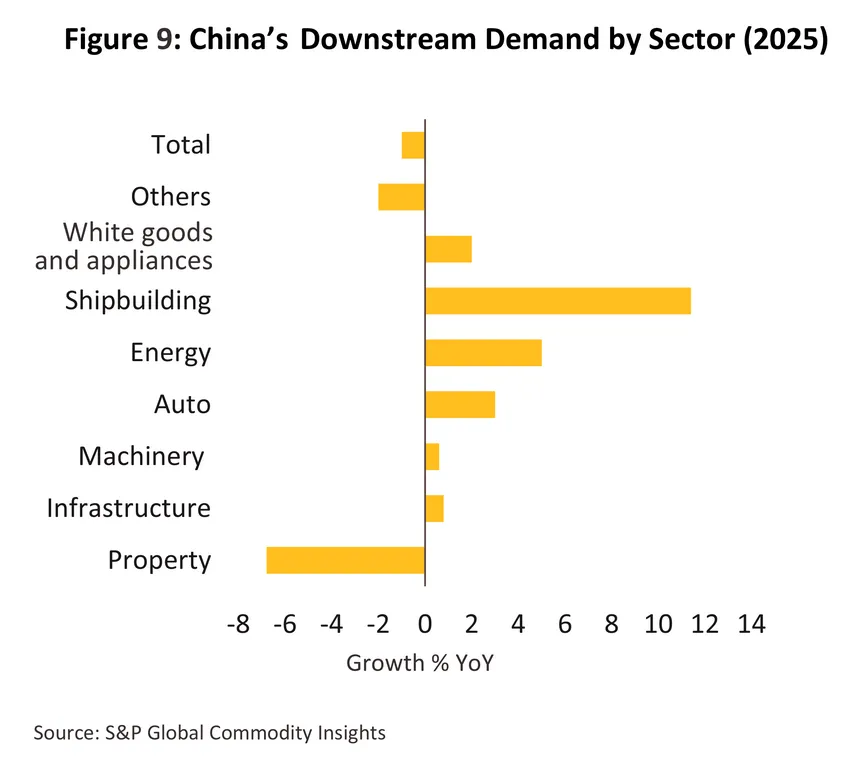

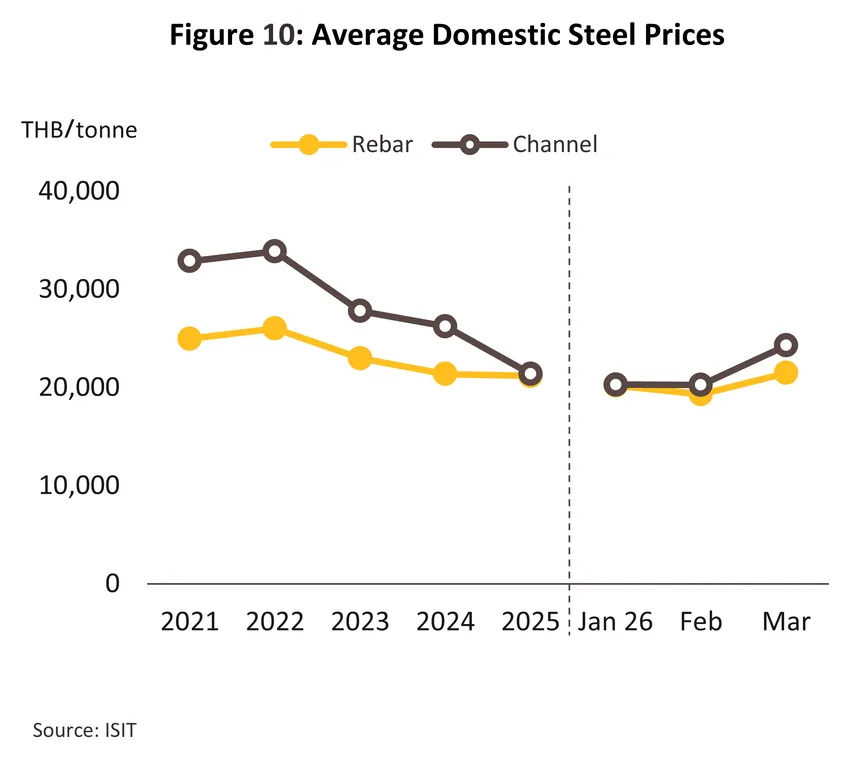

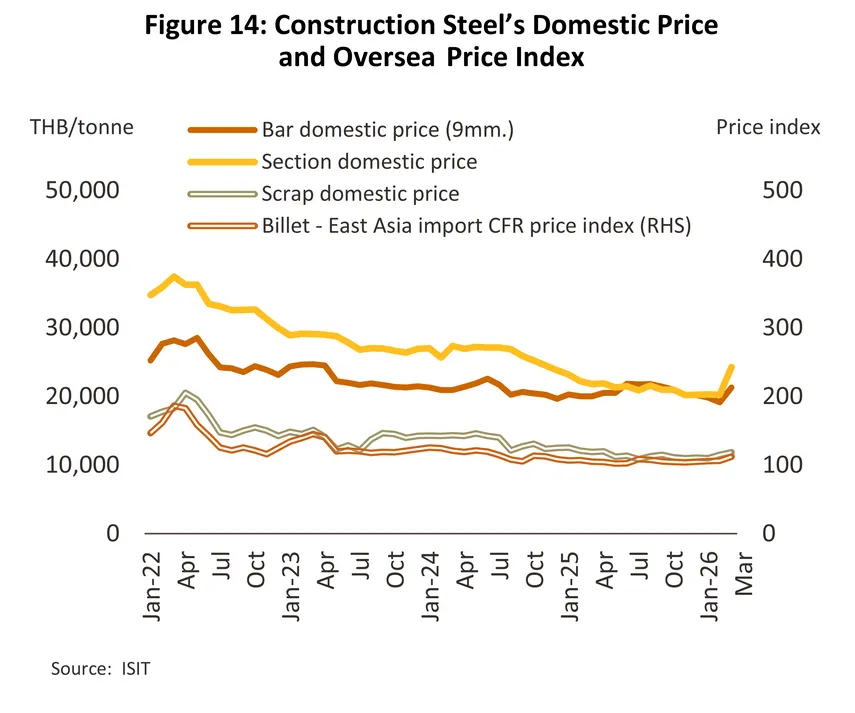

In 2025, global steel prices continued to decline amid the persistent increase in global oversupply, driven by China's accelerated exports of steel products to the global market. This was mainly due to the prolonged property crisis, which caused steel demand from China's property sector to decline by -6.8% (Figure 9). As a result, steel prices in Thailand also came under downward pressure. For example, the average price of channel steel declined to THB 21,391 per tonne (-18.4%), while the average price of rebar steel fell to THB 21,165 per tonne (-0.9%). In the first quarter of 2026, the prices of rebar and channel steel continued to decline by -6.0% YoY and -3.5% YoY, respectively (Figure 10). However, considering March 2026 alone, the prolonged conflict in the Middle East pushed up costs across the steel supply chain, including energy prices, freight rates, and transportation costs, resulting in higher steel import costs. Consequently, some producers gradually raised selling prices to reflect the higher costs, leading to increases in the prices of rebar and channel steel in March 2026 by 5.0% YoY and 11.5% YoY, respectively.

Ceramic tiles and sanitary ware

-

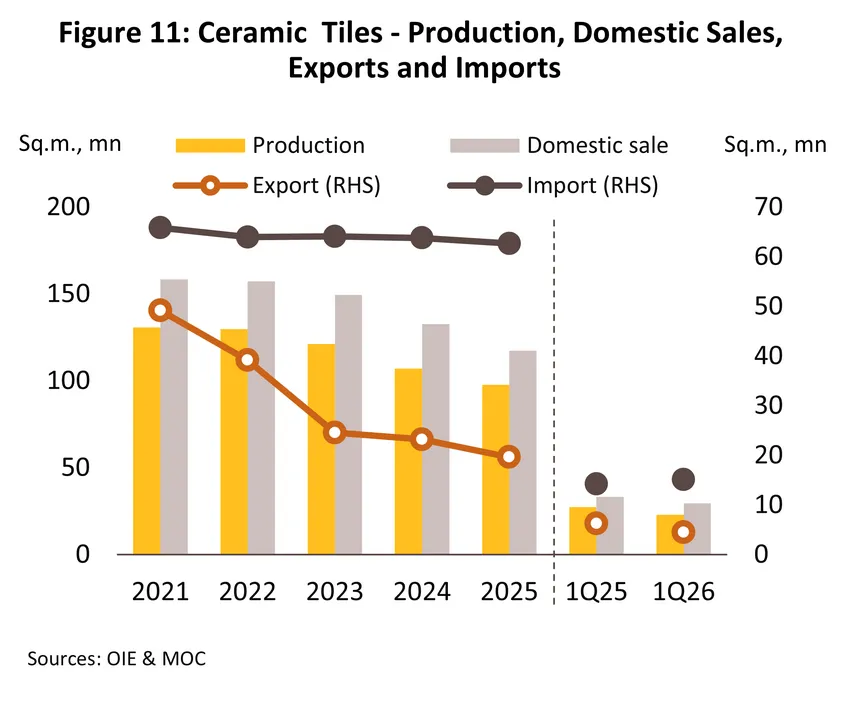

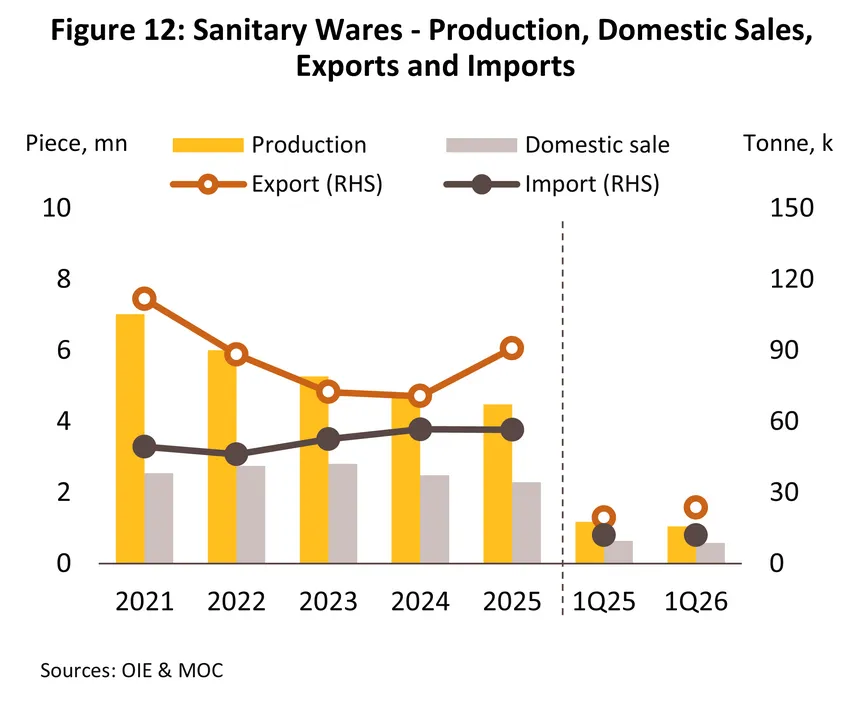

In 2025, the ceramic tile and sanitary ware industry continued to face pressure from the limited recovery in purchasing power, persistently high household debt, and tighter lending conditions by financial institutions. As a result, the residential property market continued to slow, leading to declines in both production and domestic sales of these products. Ceramic tile production decreased by -8.7% to -97.7 million sq.m., while sanitary ware production declined by -7.6% to 4.7 million pieces. Meanwhile, domestic sales of ceramic tiles fell by -11.6%, marking the sixth consecutive year of decline, while domestic sales of sanitary ware decreased by -9.3%, amid continued competition from low-priced imports from China, which remained a major source of pressure on domestic manufacturers (Figures 11 and 12).

Regarding exports and imports, ceramic tile exports declined by -15.0%, mainly due to contractions in key markets such as Cambodia and Japan. In contrast, sanitary ware exports increased by 28.6%, supported by stronger demand from the U.S. market, where importers accelerated purchases ahead of higher import tariffs. Meanwhile, imports of ceramic tiles and sanitary ware declined by -17.1% and -10.2%, respectively, reflecting the continued slowdown in Thailand's residential construction sector. As a result, contractors and construction material distributors continued to hold high inventory levels.

-

In 1Q26, although private construction investment returned to growth, the expansion was driven mainly by non-dwelling projects, such as office buildings, factories, and commercial developments. Meanwhile, the residential sector continued to face pressure from the large inventory of unsold housing amid still-weak purchasing power, particularly following the impact of the conflict in the Middle East. As a result, demand for home decoration materials remained subdued, with domestic sales of ceramic tiles and sanitary ware declining by -11.4% YoY and -8.2% YoY, respectively (Figures 11 and 12).

Regarding exports and imports, ceramic tile exports declined by -27.8% YoY, mainly due to contractions in key markets such as Myanmar and the United States, which contracted by -38.7% YoY and -9.0% YoY, respectively. This reflected weaker economic conditions amid higher living costs, which slowed construction activity and building renovation projects requiring ceramic tiles in many key markets. However, sanitary ware exports increased by 22.4% YoY, mainly supported by the U.S. market, which accounted for 62% of Thailand's total sanitary ware exports and recorded strong growth of 69.6% YoY. This was partly attributable to trade diversion, as the United States continued to reduce imports from China following higher import tariffs. Meanwhile, imports of ceramic tiles and sanitary ware increased by 5.8% YoY and 39.7% YoY, respectively (Figures 11 and 12), to meet demand in the premium and niche market segments, where domestic producers remain less competitive in terms of product design and production technology. These include large-format tiles, customized tile designs, smart sanitary ware, and products related to the hotel and tourism industries, where demand is expected to remain steady in line with the gradual recovery of the service sector.

Construction Materials Price Index

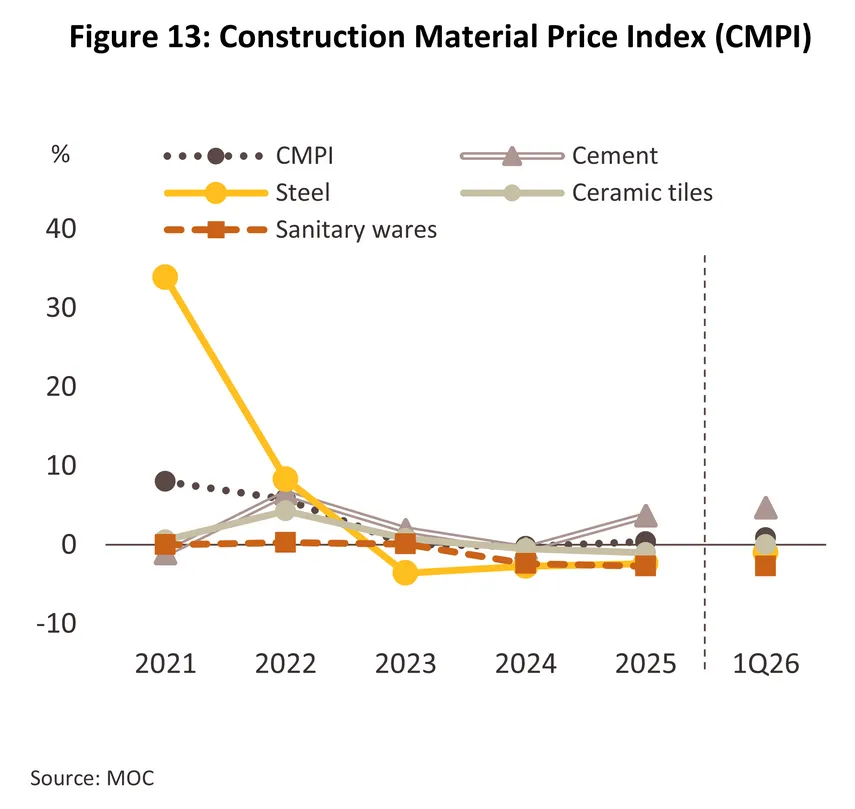

The Construction Materials Price Index (CMPI) increased by only 0.4% in 2025, compared with a -0.2% decline in 2024 (Figure 13). The steel and steel products price index, which accounts for approximately 28% of the construction materials cost basket used in the index calculation, declined by -2.4%, mainly due to continued oversupply following China's continued dumping of excess steel into the global market amid the slowdown in the property sector, particularly for bar and section steel. Meanwhile, the sanitary ware and ceramic tile price indices continued to decline by -2.7% and -1.0%, respectively, reflecting the still-high inventory of residential properties and the slowdown in new investment in the property sector. In contrast, the cement price index, which accounts for 12% of the index basket, increased by 3.7%. This was partly driven by the cement industry's transition toward the use of clean energy and low-carbon cement production processes in response to trade regulations, particularly those introduced by the European Union, as well as Thailand's Net Zero target by 2050. The transition has resulted in higher production costs, with producers gradually passing part of these costs on to consumers through higher selling prices. Meanwhile, the concrete products price index increased slightly by 0.9%, reflecting adjustments in production processes to reduce carbon emissions, together with higher costs of key raw materials such as cement, stone, and sand.

In the first quarter of 2026, the Construction Materials Price Index (CMPI) continued to increase slightly by 0.9% YoY (Figure 13). Prices of most major construction material categories remained on an upward trend, particularly the cement category, which increased by 4.7%, reflecting higher selling prices in line with rising energy costs, as well as stronger demand from the public sector. Meanwhile, the concrete products category increased by 1.4%, driven by higher raw material prices and transportation costs. In contrast, the sanitary ware price index remained weak, declining by -2.7%, while the ceramic tile price index remained broadly unchanged, in line with the property sector, which has yet to fully recover. At the same time, the steel and steel products price index continued to decline slightly by around -1.0%, reflecting the persistent global oversupply, particularly from China, which continued to put downward pressure on prices.

However, on a monthly basis, signs of a turnaround have begun to emerge. In March 2026, one month after the outbreak of the conflict in the Middle East, steel prices increased by approximately 11.2% MoM and 5.0% YoY, respectively, driven by higher prices of key raw materials, including billet and steel scrap, as well as rising freight rates and transportation costs resulting from the conflict. Overall, construction material prices have continued to increase gradually, mainly supported by the cement and concrete products categories, which have been affected by cost pressures, while the steel and steel products and finishing materials categories continue to face pressure from global oversupply and the slow recovery in demand (Figure 14).

Outlook

Overall demand for construction materials is expected to increase, particularly for structural materials, supported by new investment projects and large-scale infrastructure development. Meanwhile, demand for finishing materials is also expected to benefit from investment in commercial and non-residential buildings. However, sales growth is likely to remain constrained by the residential construction sector, where a large inventory of unsold housing remains amid still-weak purchasing power. This outlook is reflected in the expected recovery of the construction market, which is projected to expand by 2.5–2.7% in 2026, before accelerating to 3.1–3.3% in 2027 and 3.4–3.6% in 2028 (Figure 15). Nevertheless, the outlook for 2026 may remain challenging for the construction materials industry as a whole, as producers and traders are expected to continue facing pressure from both supply- and demand-side factors. The prolonged conflict in the Middle East has pushed up oil prices, leading to higher production costs for construction materials, particularly for energy-intensive industries. In addition, construction materials are bulky and heavy products, resulting in higher transportation costs for both raw materials and finished products. At the same time, manufacturers may have limited ability to pass these higher costs on to consumers and contractors amid the still-sluggish economic environment. Furthermore, many construction materials remain subject to government price controls.

In addition, competition from imported products from China is expected to remain intense, as China continues to offload surplus products resulting from its domestic property crisis. This will require Thai producers to further strengthen their competitiveness by improving product quality and standards to better meet market demand, particularly through the development of environmentally friendly materials, such as energy-saving and low-carbon materials. Looking ahead, the revenue outlook for construction material manufacturers and distributors is expected to improve in 2027–2028, supported by public investment projects and the gradual recovery of private investment, particularly in industrial estates and commercial building developments.

Producers of construction materials: Overall revenue is expected to continue increasing in line with the gradual recovery of the construction sector. Demand for cement and construction steel is expected to recover faster than that for ceramic tiles and sanitary ware, supported by large-scale public construction projects, particularly those linked to the EEC and provinces serving as regional investment hubs. These projects are expected to induce further growth in private construction investment, especially in the construction of factories and industrial estates in related areas. Nevertheless, manufacturers are expected to continue facing pressure from higher costs and intense competition from Chinese imports, particularly in the construction steel and ceramic tile segments.

-

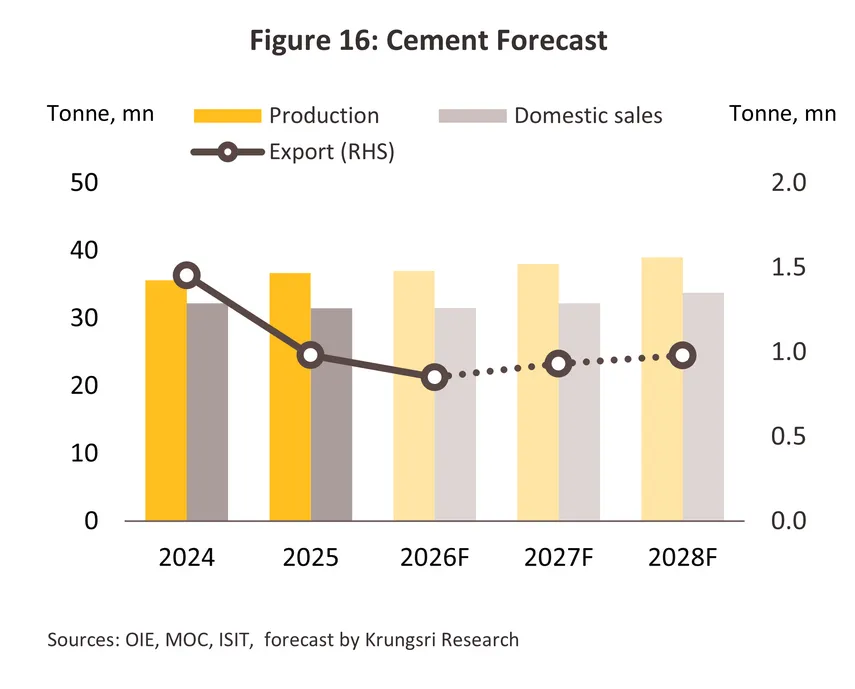

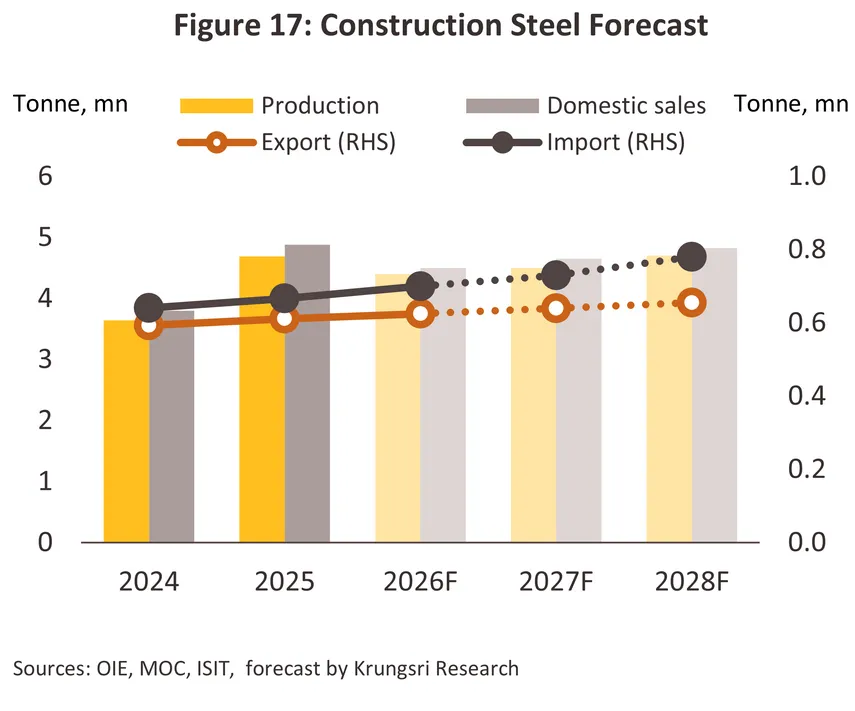

Cement and construction steel: During 2026–2028, domestic sales of cement and construction steel are expected to grow by an average of 2.5–3.5% per year (Figures 16 and 17). However, in 2026, the market is expected to remain broadly stable or record only limited growth, as investment in several construction projects may continue to face delays.5/ These include public infrastructure projects, many of which still face implementation challenges, as well as private residential construction projects, which continue to be affected by weak purchasing power, a large inventory of unsold housing, and financial liquidity constraints faced by some contractors. At the same time, construction material, energy, and transportation costs are expected to remain elevated due to the impact of the conflict in the Middle East, placing additional pressure on the operations of both construction contractors and construction material producers.

-

The market is expected to expand at a faster pace during 2027–2028, supported by the gradual increase in public infrastructure investment, including transportation projects, public utility infrastructure works, and large-scale construction projects that are expected to increasingly enter the construction phase. In particular, double-track railway, mass transit, high-speed rail, and development projects in the EEC are expected to support a gradual recovery in demand for key construction materials. In addition, rising industrial investment and factory construction projects by foreign investors are expected to provide further support for demand for cement and construction steel in the coming years. Nevertheless, Thai steel producers are expected to continue facing intense price competition, particularly from low-priced steel imports from China, which are likely to continue flowing into the ASEAN market due to China's persistent excess production capacity, coupled with a slower-than-expected recovery in domestic demand. As a result, Chinese producers are expected to accelerate the offloading of surplus steel products to overseas markets, which will continue to affect Thailand's steel exports to key markets, particularly ASEAN, despite the expected increase in steel demand.6/ Consequently, these conditions may continue to limit the ability of Thai producers to raise prices and put pressure on their profitability in the period ahead.

-

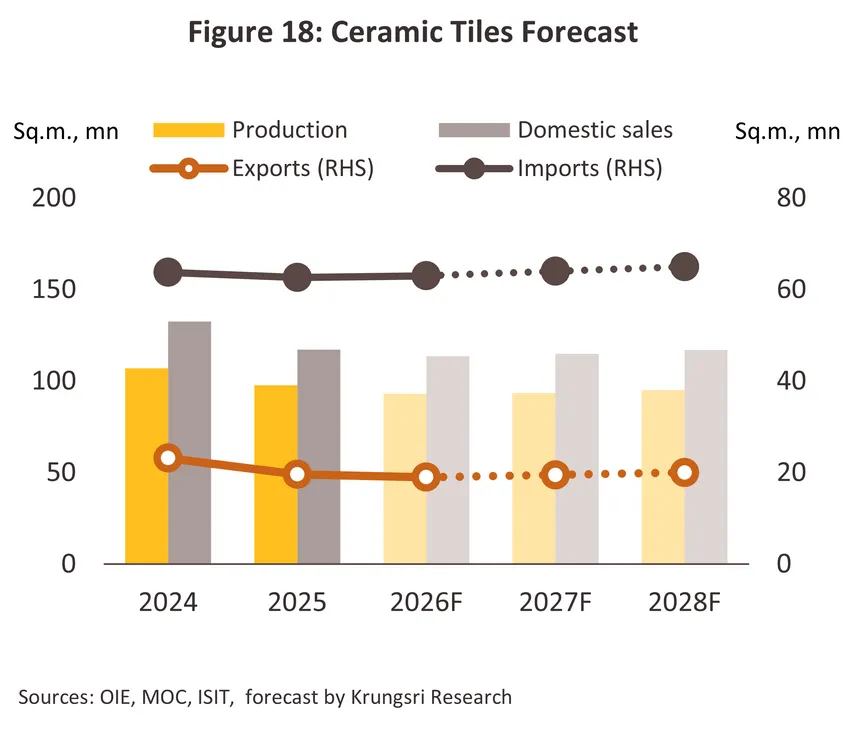

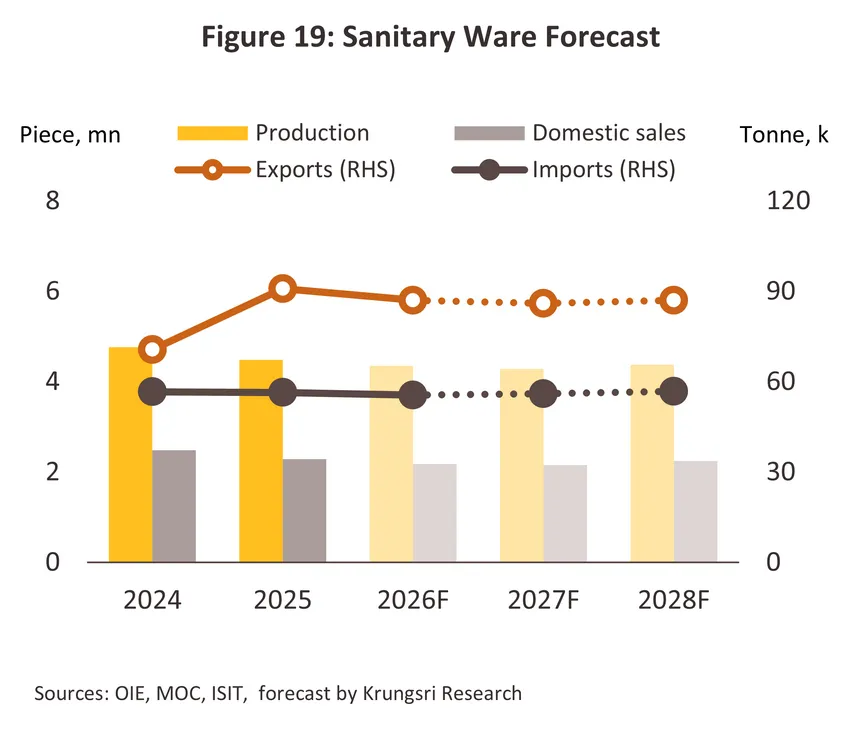

Ceramic tiles and sanitary ware: During 2026–2028, domestic sales of ceramic tiles and sanitary ware are expected to grow by only 1.0–1.5% (Figures 18 and 19). Sales are expected to remain broadly stable or decline slightly in 2026, reflecting the slowdown in the property sector amid economic uncertainty, with continued pressure from high energy costs and weak purchasing power. They are then expected to gradually recover at a modest pace during 2027–2028, in line with the recovery of the property sector and private investment. Meanwhile, exports of ceramic tiles and sanitary ware are expected to continue declining before returning to growth in 2028, amid continued intense competition from Chinese products in the global market.

Traders: During 2026–2028, modern trade is expected to continue outperforming traditional trade in terms of growth potential. Nevertheless, operators are expected to continue facing intense competition, particularly in 2026, when consumer purchasing power is likely to remain under pressure from the economic slowdown amid the high cost of living driven by elevated energy prices.

-

Modern traders: Revenue is expected to remain broadly stable or grow only modestly in 2026, in line with the economic slowdown, before gradually increasing during 2027–2028, supported by the recovery of activity in the property market and the home repair and renovation market. Operators have accelerated strategic adjustments by expanding their distribution channels and diversifying their business models, including (i) adjusting store formats and sizes to expand branches into community areas; (ii) developing new store formats in collaboration with major construction material manufacturers, such as SCG Home Boonthavorn; (iii) cooperating with construction material traders on distribution channels and product zones, such as CPAC–Global House; (iv) increasing the share of private-label products; (v) developing omni-channel distribution through online platforms and marketplaces, such as Lazada and Shopee; and (vi) placing greater emphasis on sustainability by allocating display areas for environmentally friendly products, or green materials, and using packaging that reduces plastic consumption to meet the needs of environmentally conscious consumers. These initiatives help strengthen retailers' positive brand image in line with the global sustainability trend.

-

Traditional traders: Revenue is expected to decline or remain broadly stable in 2026, reflecting still-weak purchasing power, particularly among lower- and middle-income consumers in regional markets, who continue to face high household debt. Revenue is then expected to gradually recover during 2027–2028 as the economy improves, supported by infrastructure investment, which is expected to stimulate private sector investment. Nevertheless, traditional retailers are expected to continue facing intense competition from modern construction material retailers, which are expanding their branch networks into more secondary cities, as well as from manufacturers that have increasingly shifted toward selling directly to small construction contractors.

Challenges facing the industry: Construction material producers are expected to accelerate the transition of their production lines toward environmentally friendly construction materials, resulting in a higher cost burden due to greater investment in advanced production technologies and more sophisticated manufacturing processes. At the same time, producers continue to face pressure from persistently high energy prices, resulting in higher production costs and, consequently, higher product prices. For example, green steel is estimated to be approximately 15–40% more expensive than conventional steel, depending on the steel grade, the intensity of hydrogen used in the production process, and the level of low-carbon certification (Source: blog-tatanexarc.com, Nov 25). Meanwhile, construction material traders continue to face intense competition in operations, marketing, and customer services, while also investing in online platforms and integrated service offerings. These factors are expected to place additional pressure on maintaining market share and profitability, particularly for SMEs.

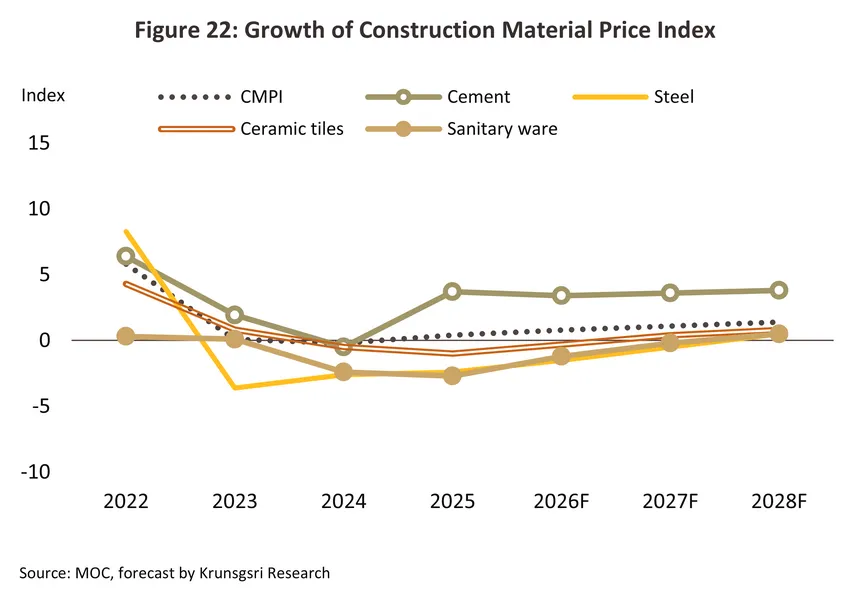

Construction material prices are expected to gradually increase during 2026–2028 (Figure 22), driven mainly by (i) the recovery in construction demand, particularly during 2027–2028, when construction investment, especially in the residential sector, is expected to gradually recover. Meanwhile, public construction activity is expected to increase after public construction activity is expected to record relatively weak growth in 2026, partly due to delays associated with the formation of the new government, together with expanded investment in large-scale infrastructure projects. These developments are expected to support demand for construction steel in Thailand. Although production cuts in China may help support global steel prices, exports of low-priced steel from China are expected to continue weighing on the market. Nevertheless, public infrastructure investment is expected to strengthen domestic demand, leading to a gradual increase in construction material prices; (ii) higher costs associated with technologies and innovations used in the production of environmentally friendly construction materials. For example, the production cost of low-carbon cement may be up to 45% higher than that of conventional cement due to the adoption of technologies such as carbon capture and clean energy (Source: McKinsey & Company, Cementing Your Lead: The Cement Industry in the Net-Zero Transition, Oct 23); and (iii) persistently high energy costs, as geopolitical tensions are expected to remain prolonged, particularly the conflict in the Middle East, which is expected to continue putting upward pressure on global energy prices, resulting in higher production and transportation costs.

1/ Including Portland cement and mixed cement

2/ Ministry of Commerce, based on businesses that remained in operation in 2024.

3/ Exports are largely of cement, construction steel, ceramic tiles, and sanitary ware.

4/ Examples of clinker substitutes include limestone (commonly used in Thailand due to its abundant supply and high quality),

lime, fly ash, pozzolanic materials (e.g., silica fume, rice husk ash, and kaolin clay), and blast furnace slag, among others.

5/ Progress on all four key projects remains behind schedule to varying degrees. In particular, the High-Speed Rail Linking Three Airports project is still under negotiation on the terms and conditions of the public-private partnership. Meanwhile, the U-Tapao Airport Development Project continues to face delays due to contractual and financial issues. The Laem Chabang Port Phase 3 project has also been delayed as the government and the private sector have yet to reach agreement on the interpretation of the technical requirements for the land reclamation works. Although the Map Ta Phut Port Phase 3 project has made more progress than the other projects, it also remains delayed, as the government has yet to decide whether Phase 2 of the port and commercial area development (Plots A and C) will be implemented under a public-private partnership (PPP) or a government-to-government (G2G) arrangement.

6/ The World Steel Short Range Outlook (April 2026) projects that steel demand in the ASEAN-5 (Indonesia, Malaysia, the Philippines, Thailand, and Vietnam) will continue to grow by 1.3% and 2.4% in 2026 and 2027, respectively, increasing total steel consumption to nearly 90 million tonnes.

7/ The major greenhouse gases are: carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), and fluorinated gases, including the hydrofluorocarbons (HFCs), sulfur hexafluoride (SF6), perfluorochemicals (PFCs), nitrogen trifluoride (NF3), and the chlorofluorocarbons (CFCs).

.webp.aspx)