EXECUTIVE SUMMARY

Thailand’s pharmaceutical industry is expected to expand during 2026–2028, driven by population aging, the rising prevalence of non-communicable diseases (NCDs), and broader access to healthcare. Growth will also be supported by government initiatives to strengthen domestic production of pharmaceuticals, active pharmaceutical ingredients (APIs), and biopharmaceuticals, thereby reducing import dependence and enhancing pharmaceutical security. Production volume is projected to grow by 1.5–2.5% in 2026 and accelerate to 2.7–3.7% annually during 2027–2028, while domestic pharmaceutical sales are forecast to increase by 3.0–4.0% and 4.0–5.0%, respectively. However, growth in 2026 may be constrained by geopolitical tensions in the Middle East, which could disrupt supply chains and increase production costs, as well as a fragile economic environment that may dampen healthcare spending. Pharmaceutical exports are expected to remain flat in 2026 amid global economic uncertainty before recovering to annual growth of 2.5–3.5% during 2027–2028, supported by stronger demand from key export markets, particularly ASEAN countries. Nevertheless, pricing pressure from low-cost producers in China and India is expected to persist.

Krungsri Research view

Growth prospects vary across industry segments:

-

Pharmaceutical Manufacturers: Revenue is expected to continue growing, supported by rising demand for treatments for non-communicable diseases (NCDs), which require long-term medication, and expanded public healthcare coverage that improves access to medicines and healthcare services. However, profitability may be constrained by intensifying competition from low-priced imported drugs, the entry of new competitors with strong technological and financial capabilities, and higher costs associated with environmentally sustainable production practices.

-

Pharmaceutical Distributors (Retailers and Wholesalers): Revenue is expected to continue growing, although competition is likely to intensify further from large operators and online platforms.

-

Stand-alone Pharmacies: Performance may come under pressure from the rapid expansion of large chain pharmacies, increased availability of medicines through modern trade and convenience stores, the growth of online pharmacies, and investment requirements to comply with pharmacy standards and digital pharmacy systems.

-

Pharmaceutical Wholesalers: Operators are increasingly expanding into retail through physical stores and online channels, while also offering pharmacy setup and advisory services. This diversification is expected to broaden their customer base and create additional revenue streams beyond traditional wholesale operations

Overview

The pharmaceutical industry comprises modern medicines and medical products used for the diagnosis and treatment of diseases. Modern medicines can be classified into two categories:

-

Original or Patented Drugs, which are developed through extensive research and development (R&D) and are protected by patent rights for up to 20 years1/

-

Generic drugs, which are produced after patent expiration and contain the same active ingredients and therapeutic properties as the original drugs but are typically offered at lower prices due to lower production costs and the absence of R&D expenses.

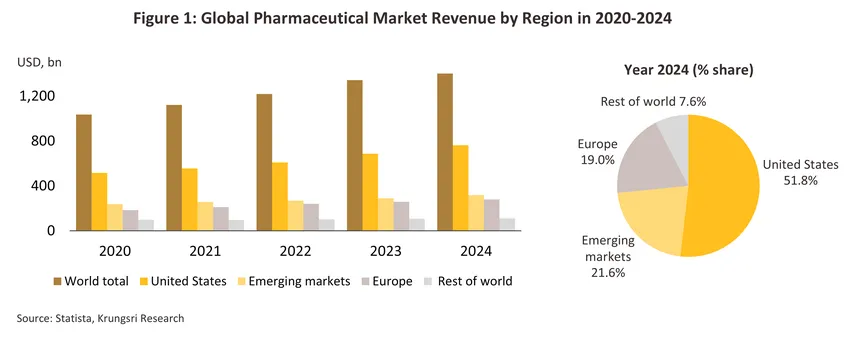

The pharmaceutical industry is highly research-intensive, requiring substantial and continuous investment in the development of new active pharmaceutical ingredients (APIs) and medicines. As a result, global production of innovative and patented drugs is concentrated in developed economies, particularly the United States and Europe, which possess strong capabilities in human capital, scientific research, and advanced manufacturing technologies. In contrast, most developing countries remain reliant on imports of higher-value patented medicines. In 2024, global pharmaceutical sales exceeded USD 1.5 trillion, representing annual growth of 9.5% (Figure 1). Leading global pharmaceutical companies include Pfizer, Merck & Co., and Johnson & Johnson (United States), as well as Novartis and Roche (Switzerland), and Sanofi (France).

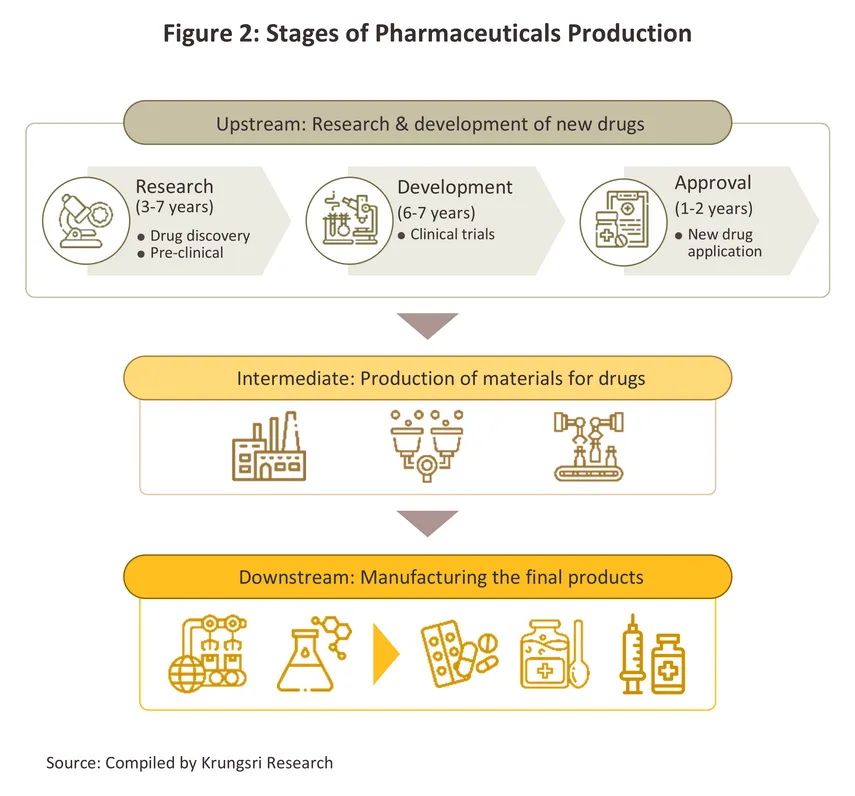

The pharmaceutical production value chain is divided into three stages (Figure 2):

-

Upstream: Research, discovery, and development of new drugs

-

Midstream: Production of pharmaceutical ingredients used in finished drug manufacturing, including active pharmaceutical ingredients (APIs) and excipients. This stage involves producing established drug compounds and developing manufacturing processes or molecular modifications, requiring advanced technology and substantial capital investment.

-

Downstream: Manufacturing of finished pharmaceutical products, often using imported raw materials (Thailand imports approximately 90% of the pharmaceutical ingredients used in domestic drug production). Products are primarily generic drugs in various dosage forms, including tablets, liquids, capsules, creams, powders, and injectables. Analgesics and antipyretics account for the largest share of production value. Most Thai pharmaceutical manufacturers operate in this segment.

Thailand has approximately 1442/ GMP-certified pharmaceutical manufacturing facilities, of which only nine3/ are capable of producing active pharmaceutical ingredients (APIs), primarily for use in their own finished drug production. New drug research and development remains limited, with vaccine development being the main area of activity across both upstream and downstream segments.4/ Thailand has implemented the National Vaccine Policy and Strategy since 2005 and is currently operating under the Second National Vaccine Strategy (2023–2027), which aims to ensure adequate vaccine coverage5/ for all citizens in both normal and emergency situations. The strategy also promotes domestic production of essential vaccines to reduce import dependence.

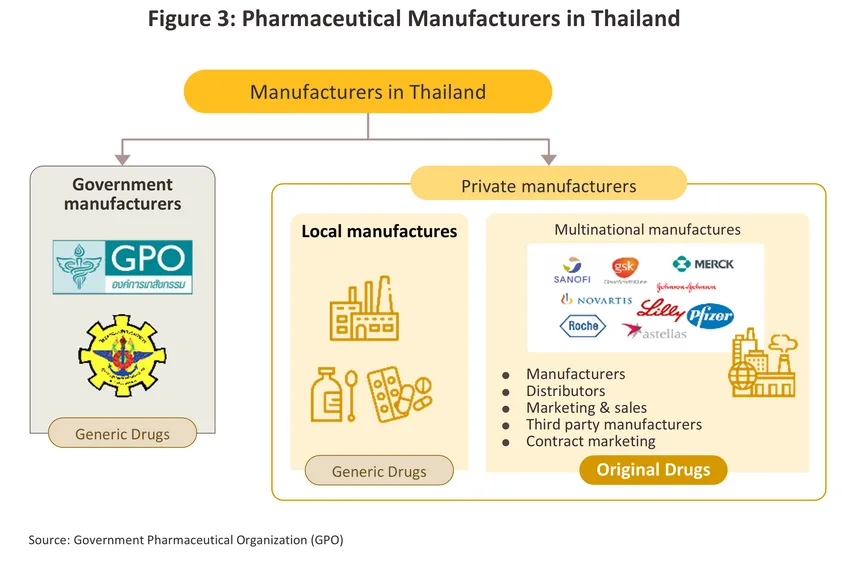

Pharmaceutical industry participants can be classified into two groups (Figure 3):

1. Public Sector Organizations: These include (1) the Government Pharmaceutical Organization (GPO), which manufactures essential medicines under the national health system and selected import-substitution products, particularly for non-communicable diseases (NCDs), to improve affordability and access; and (2) the Military Pharmaceutical Factory, which primarily produces generic drugs for the domestic market as substitutes for imported medicines. Under Thailand’s Public Procurement and Supplies Administration Act B.E. 2560 (2017), the GPO operates on the same competitive basis as private-sector firms, resulting in greater market competition from both domestic and foreign pharmaceutical manufacturers, particularly low-cost producers from India and China.

2. Private Pharmaceutical Companies: These comprise (1) Thai-owned pharmaceutical companies, which mainly produce generic drugs and, in some cases, provide contract manufacturing services. Representative Thai pharmaceutical companies include Berlin Pharmaceutical Industry, Thai Nakorn Patana, Siam Pharmaceutical, and Biopharm Chemicals. Some companies, such as Biolab and MEGA Lifesciences, also provide contract manufacturing services. (2) Multinational companies (MNCs), which either import and distribute patented medicines or operate finished-drug manufacturing facilities in Thailand. Key market participants include Zuellig Pharma and Abbott Laboratories, among others.

Pharmaceutical manufacturing in Thailand is governed by two key laws: the Patent Act B.E. 2522 (1979), which protects patent rights for pharmaceutical inventions and is administered by the Department of Intellectual Property, and the Drug Act B.E. 2510 (1967), including subsequent amendments,6/ which regulates the manufacture, importation, and sale of pharmaceuticals. The Food and Drug Administration (FDA) is responsible for licensing and product registration for medicines marketed in Thailand.

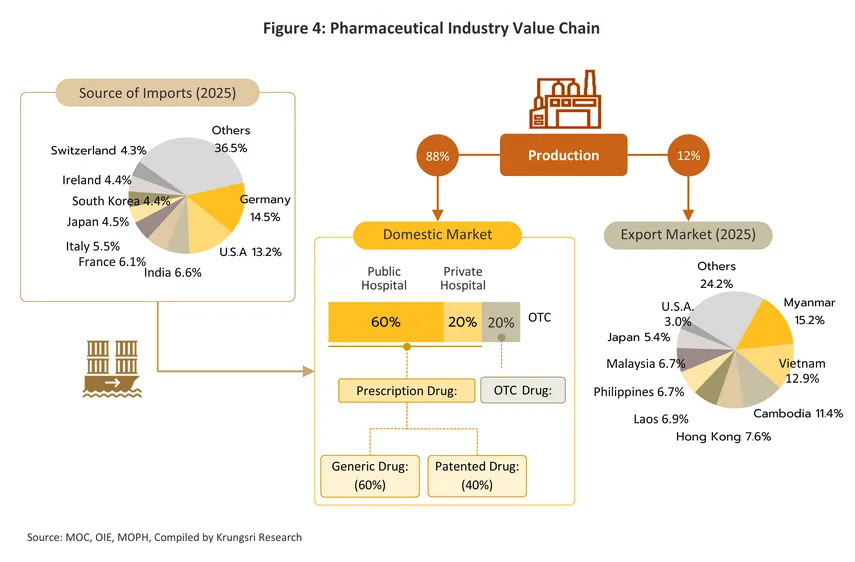

In 2024, approximately 88.4% of domestically produced pharmaceuticals were consumed in the local market, while 11.6% were exported.7/ Pharmaceutical expenditure accounted for 21.7%8/ of total healthcare spending, supported in part by Thailand’s Universal Health Coverage (UHC) scheme, which covered 99.7%9/ of eligible beneficiaries. This reflects broad access to healthcare services and supports continued growth in pharmaceutical consumption. In addition, the government has set the FY2026 budget for the National Health Security Fund at THB 270 billion, up 15.3% from the previous year, while expanding access to healthcare through digital services such as telehealth and telemedicine.

Thailand’s domestic pharmaceutical market is distributed through two main channels (Figure 4):

-

Hospital Channel: Accounting for approximately 80%10/ of total pharmaceutical sales, this channel comprises public hospitals (60%) and private hospitals (20%). The hospital channel mainly distributes prescription medicines that require physician authorization, including generic drugs (60% of sales value) and patented drugs (40%). Although patented drugs account for a smaller share, they are growing faster due to rising demand for treatments of non-communicable diseases (NCDs), such as hypertension, diabetes, and cardiovascular diseases.

-

Retail Pharmacy Channel (Over-the-Counter: OTC): Representing around 20%10/ of total pharmaceutical sales, pharmacies serve consumers with minor illnesses and conditions that do not require physician consultation. The market consists of stand-alone pharmacies, which account for approximately 75% of modern pharmacies and are largely operated by SMEs, and chain pharmacies, which are typically operated by large companies through branch networks or franchise models. As of March 2026, Thailand had 20,733 pharmacies nationwide11/, including 18,178 modern pharmacies (87.7% of the total). Of these, 17.8% were located in Bangkok and 82.2% in other provinces. The number of modern pharmacies declined to 18,178 in March 2026 from 19,206 in 2025.

Competition in Thailand’s pharmacy retail market remains intense, driven by strict regulatory requirements and the continued expansion of chain pharmacies. Large domestic operators, including Health Up, eXta Plus, Save Drug, Fascino, and Pure, as well as international operators such as Watsons, Boots, Matsumoto Kiyoshi, and Tsuruha, have strengthened their market presence through extensive branch networks, placing independent pharmacies at a competitive disadvantage, particularly in terms of cost efficiency, and leading stand-alone operators to gradually cease operations.

In international markets, Thailand’s pharmaceutical exports grew at an average annual rate of 3.8%12/ during 2020–2025, accounting for only 0.2% of the country’s total export value, as exports are largely concentrated in lower-value generic drugs. The CLMV countries remain the primary export destinations, collectively accounting for around 50% of total pharmaceutical exports. Meanwhile, pharmaceutical imports consist of APIs, finished drugs, and high-value originator drugs, such as hematopoietic agents, antibiotics, and lipid-lowering drugs, sourced mainly from Germany, the United States, France, and India. The COVID-19 pandemic led to a sharp increase in vaccine imports from China, Belgium, Germany, the United States, and France. During 2021–2022, vaccines accounted for more than 46.4% of Thailand’s total pharmaceutical import value before declining to 25.8% in 2025.

Private pharmaceutical manufacturers face several challenges: (i) competition from low-cost imports, particularly from India and China; (ii) difficulty competing with public-sector manufacturers, which benefit from lower production costs and better access to distribution channels; (iii) government-set reference prices that limit price increases for certain products; (iv) compliance with PIC/S GMP14/ standards following Thailand’s membership in the Pharmaceutical Inspection Co-operation Scheme (PIC/S), resulting in higher operating costs; and (v) requirements to maintain adequate pharmaceutical storage and distribution facilities in accordance with regulatory standards. These pressures are driving manufacturers to enhance efficiency and strengthen competitiveness in an increasingly challenging market environment.

Situation

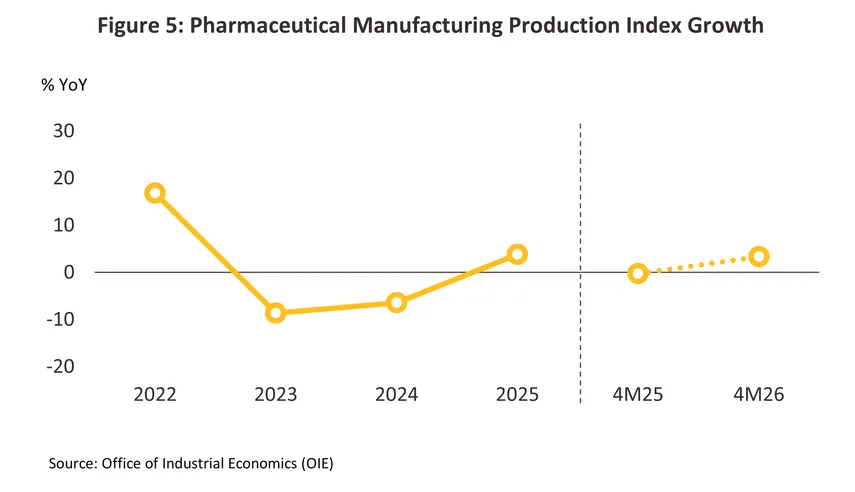

Domestic pharmaceutical production rebounded in 2025 after declining over the previous two years, as reflected by a 3.8%15/ increase in the Pharmaceutical Manufacturing Production Index (Figure 5). Growth was driven by (i) higher production to meet rising demand for medicines, particularly those used to treat seasonal infectious diseases, (ii) increased export-oriented production, especially generic drugs, and (iii) government measures supporting domestic pharmaceutical production and consumption. Injectable drugs recorded the strongest growth (+15.0%), followed by tablets (+9.4%) and powders (+4.0%). Despite the recovery, manufacturers continued to face challenges from price competition with lower-cost imported medicines, particularly from China and India, as well as growing imports of innovative drugs and biopharmaceuticals, where domestic production capabilities remain limited. Rising imports of pharmaceutical ingredients also put pressure on the industry, resulting in lower production of liquid medicines (-6.5%), creams (-9.5%), and capsules (-0.1%). During the first four months of 2026, pharmaceutical production continued to expand, supported by increased healthcare demand, including a rise in influenza cases driven by volatile weather conditions and reduced preventive health behaviors. Overall pharmaceutical production increased by 3.4% YoY, led by tablets (+15.0% YoY) and liquid medicines (+5.6% YoY). In contrast, production of injectables (-38.9% YoY), creams (-22.4% YoY), capsules (-8.2% YoY), and powders (-1.3% YoY) declined.

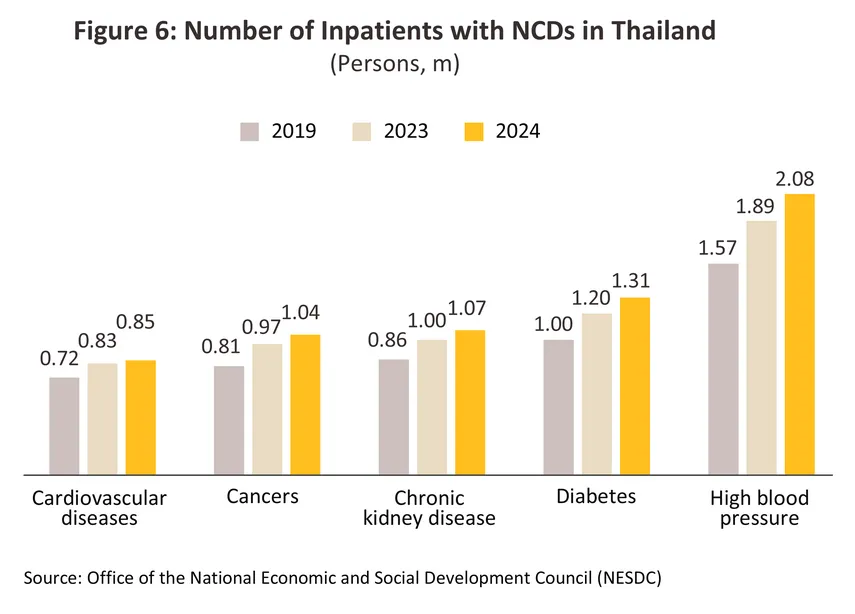

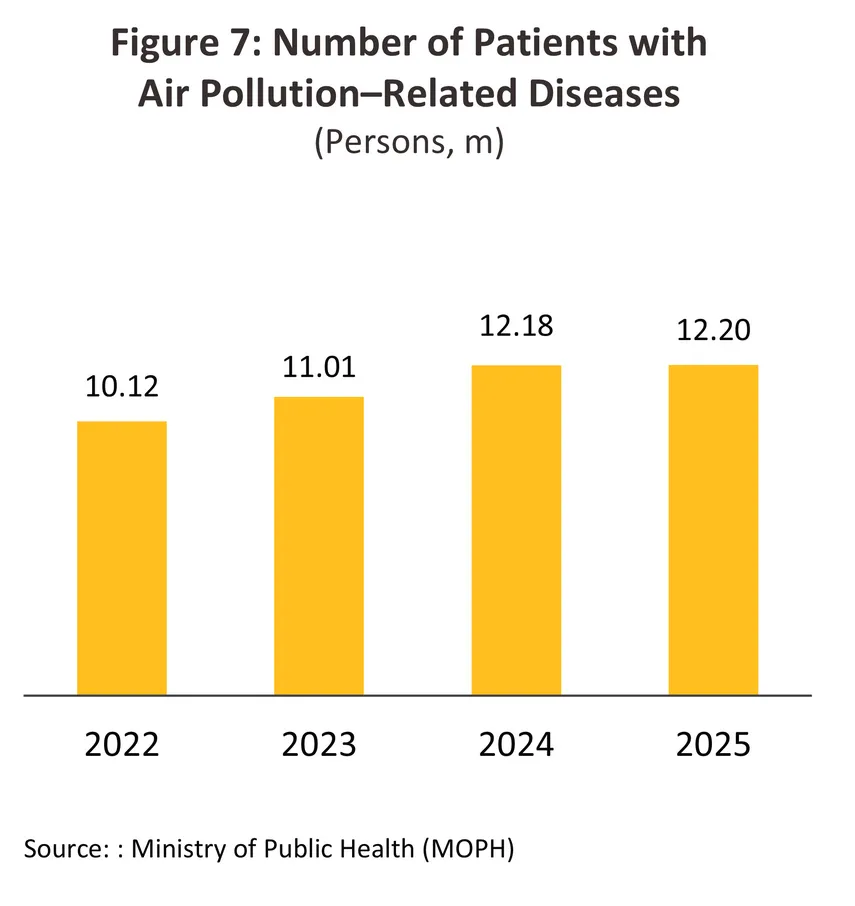

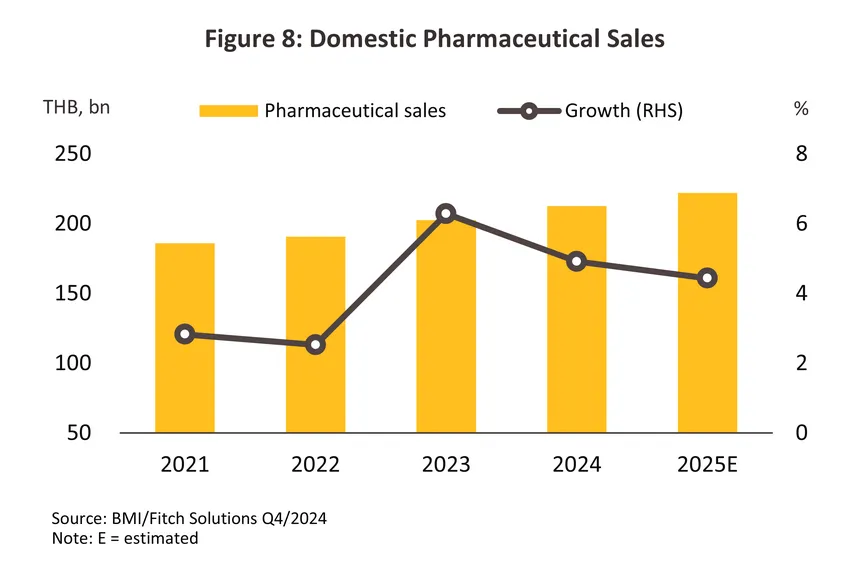

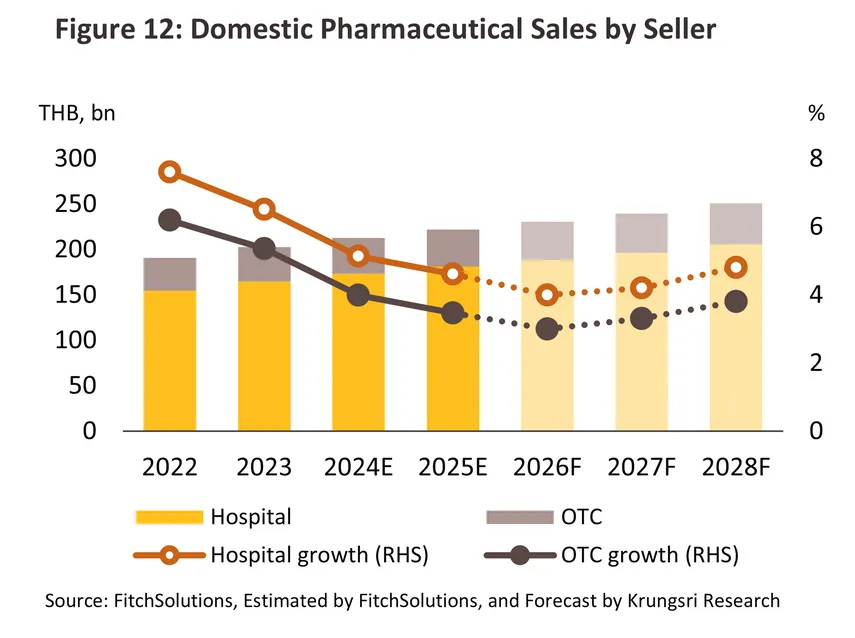

Domestic pharmaceutical consumption continued to expand in 2025, with pharmaceutical sales increasing by 4.4% (Figure 8). Growth was driven by seasonal disease outbreaks and the rising prevalence of non-communicable diseases (NCDs), particularly hypertension, diabetes, and respiratory illnesses, which continued to increase amid severe air pollution, especially PM2.5 levels16/ (Figures 6 and 7). This was reflected in a higher number of patients receiving treatment at hospitals.17/ However, growth in pharmaceutical consumption was partly constrained by weak domestic purchasing power, a slower-than-expected recovery in tourism due to a decline in foreign tourist arrivals, and the introduction of a co-payment scheme under which patients are required to bear part of their healthcare expenses under the health insurance system in March 2025, which reduced unnecessary healthcare utilization.

-

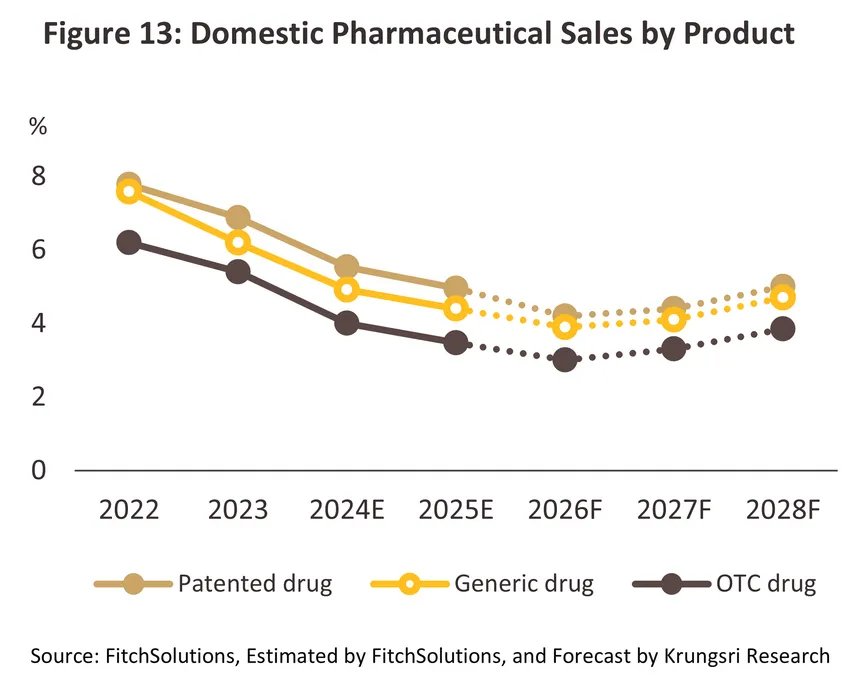

Prescription Drugs: Prescription medicines remained the largest market segment. According to Fitch Solutions (Q4/2024), sales of generic drugs were projected to reach THB 108 billion in 2025, up 4.4%, while patented drug sales were expected to reach THB 73 billion, growing by 5.0%, supported by continued demand for NCD treatments in hospitals.

-

Over-the-Counter (OTC) Drugs: OTC drug sales reached THB 41 billion in 2025, increasing by 3.5%. Pharmacies have assumed a growing role in Thailand’s healthcare system as community-based healthcare providers and dispensing points under the Universal Health Coverage scheme through the “30-Baht Treatment Anywhere” program. Under the program, eligible UHC beneficiaries can consult pharmacists and receive medicines for 32 minor ailments18/ at participating pharmacies. In addition, the “Suk Kai Sabai Krapao” initiative, launched in November 2025, allows patients to fill hospital prescriptions at retail pharmacies, improving convenience and reducing healthcare costs. Combined with the expansion of tele-pharmacy and e-commerce channels, these developments are expected to support continued growth in the OTC market.

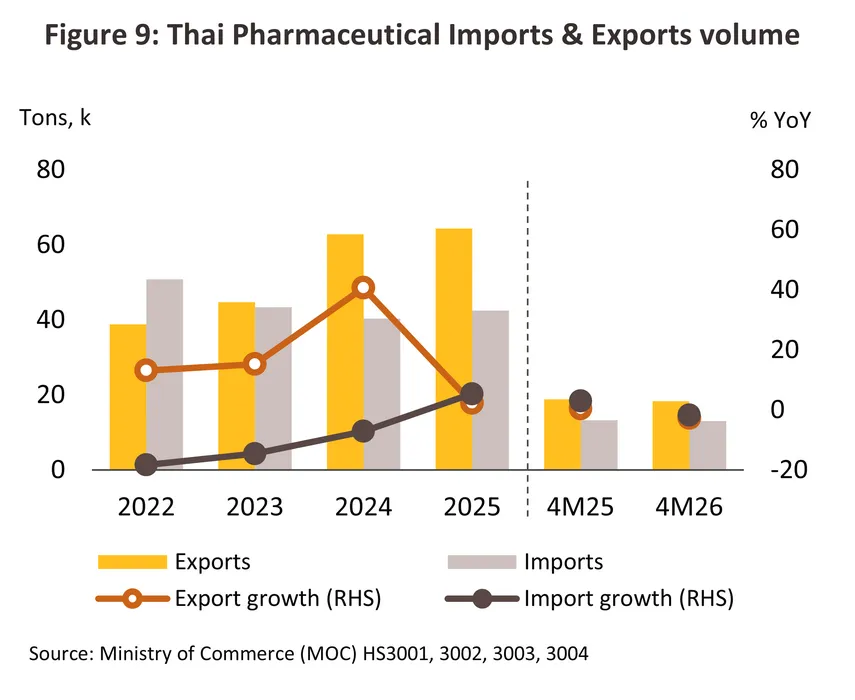

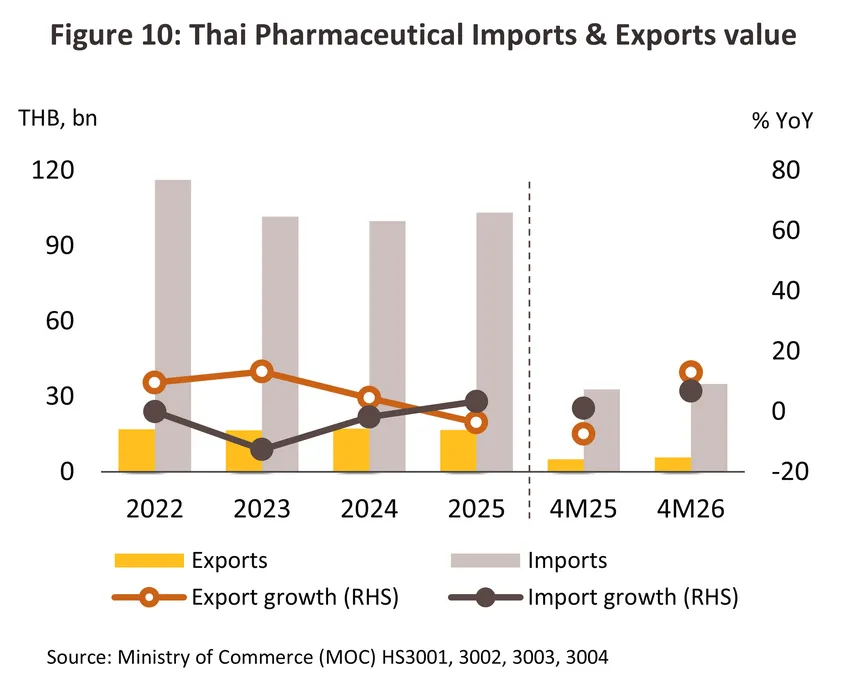

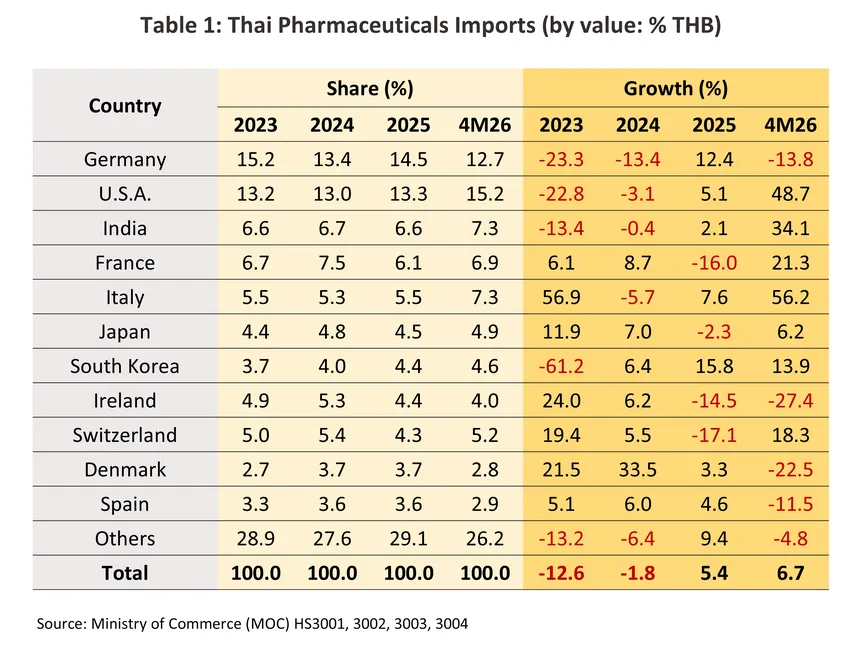

Pharmaceutical exports expanded in volume but declined in value in 2025. Export volume increased by 2.3% to 64,000 tonnes (Figure 9), driven primarily by stronger demand from India (+65.4%), Hong Kong (+9.8%), and Laos (+5.8%). In particular, vaccine exports rose by 19.7%, reflecting Thailand’s growing role as a vaccine manufacturer and exporter to neighboring countries. However, intense price competition, especially in the generic drug segment, caused the value of pharmaceutical exports to decline by 3.7% to THB 16.6 billion (Figure 10). Export value to Vietnam, Thailand’s largest export market, fell sharply by 33.8%, while Vietnam’s pharmaceutical imports from China increased by 4.3% in 2025. Pharmaceutical imports increased in both volume and value, reaching 42,000 tonnes (+5.4%) and THB 103.2 billion (+3.4%), respectively, driven by rising domestic demand for medicines, particularly specialty drugs and vaccines imported from Europe and Asia, including Germany, the United States, India, and Italy (Table 1). Imports from India, South Korea, Spain, and Belgium increased in both volume and value, accounting for a combined 18.2% of Thailand’s total pharmaceutical import value. During the first four months of 2026, Thailand’s pharmaceutical exports and imports recorded lower volumes but higher values. Export volume declined by 2.6% YoY, while export value increased by 13.0% YoY. Similarly, import volume fell by 1.7% YoY, whereas import value rose by 6.7% YoY. This reflected rising pharmaceutical prices amid higher production costs, while demand in both domestic and export markets weakened due to economic uncertainty associated with the Middle East conflict.

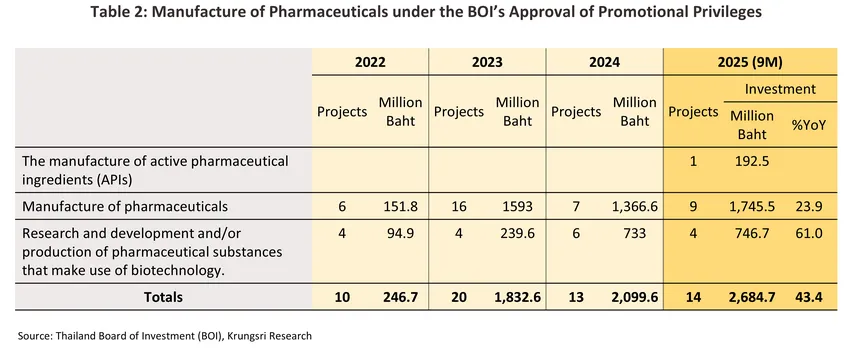

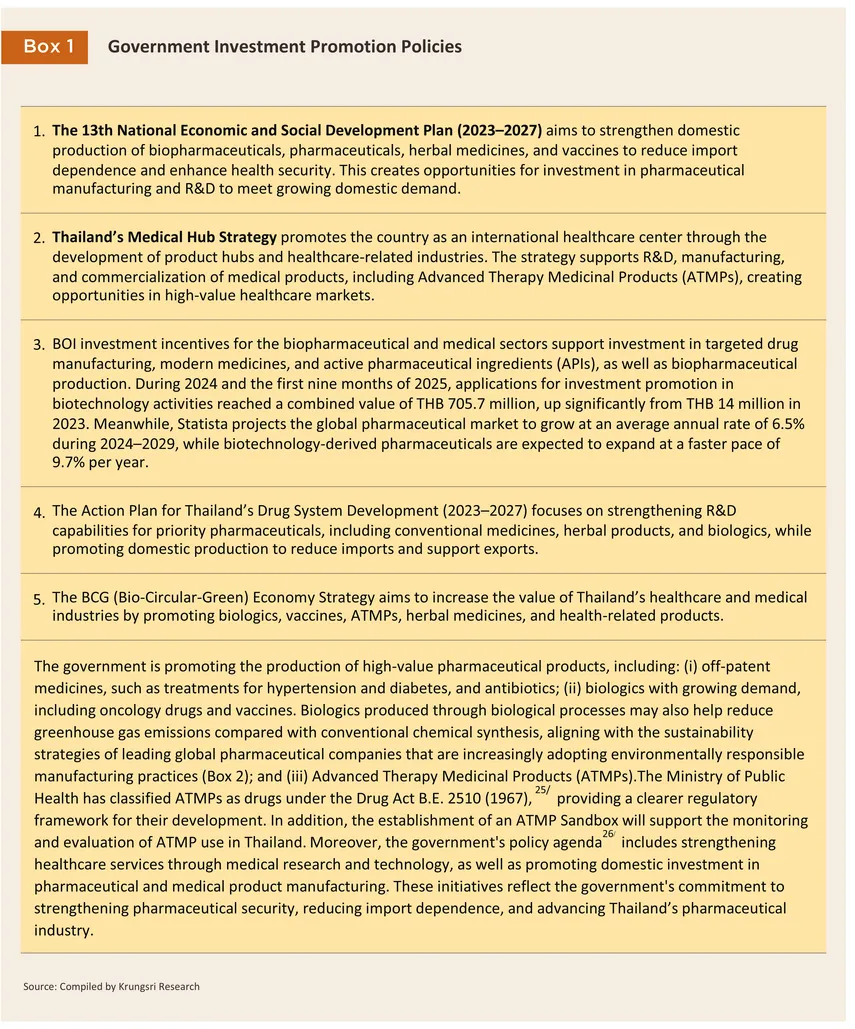

Investment in Thailand’s pharmaceutical industry continued to gain momentum during the first 9 months of 2025, with 14 approved projects across the pharmaceutical value chain worth a combined THB 2.68 billion (Table 2), up 43.4% YoY from THB 1.87 billion in the same period of 2024.The approved projects can be grouped into three segments. First, finished pharmaceutical manufacturing accounted for 65.0% of total approved investment value and increased by 23.9% YoY. Most of these investments were directed toward Targeted medicines19/ including treatments for cancer and immunodeficiency disorders, which represented 74.3% of total investment in finished drug production. Second, biotechnology R&D and biopharmaceutical production accounted for 27.8% of total investment value and surged by 61.0% YoY, reflecting strong growth prospects for biologics and alignment with the government’s strategic priority industries. Third, API manufacturing accounted for 7.2% of total approved investment value, representing the first investment in API manufacturing in six years, with an investment value of THB 192.5 million. This development signals growing efforts to reduce dependence on imported pharmaceutical ingredients and strengthen the long-term resilience of Thailand’s pharmaceutical supply chain.

Outlook

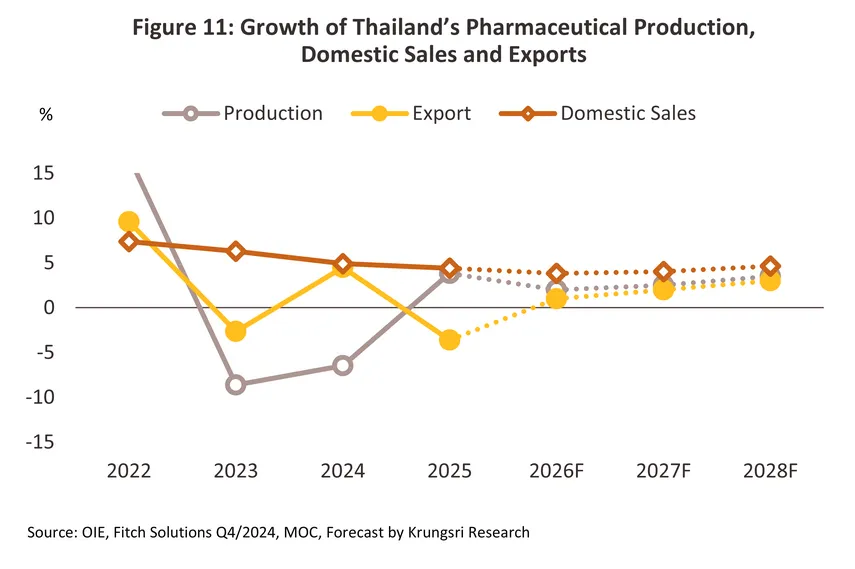

Pharmaceutical production is projected to grow by 1.5–2.5% in 2026 (Figure 11), supported by demand-side factors, including rising domestic demand for medicines, particularly generic drugs, and supply-side factors, including increased investment in pharmaceutical R&D and domestic production aimed at reducing import dependence. This is in line with government policies aimed at reducing import dependence, strengthening pharmaceutical security, and promoting the development of high-value medicines. However, production growth may be constrained by the prolonged Middle East conflict, which could disrupt pharmaceutical supply chains through periodic raw material shortages, leading to production delays and higher manufacturing costs. During 2027–2028, pharmaceutical production growth is expected to accelerate to 2.7–3.7% per year (Figure 11). This will be supported by (i) a gradual economic recovery, which is expected to strengthen patient purchasing power and increase demand for healthcare services through hospitals and pharmacies, thereby boosting pharmaceutical demand in both domestic and export markets; and (ii) government investment promotion measures (Box 1), which are expected to attract further investment in domestic pharmaceutical manufacturing, particularly in API production to reduce import dependence and biopharmaceuticals to meet growing demand.

Domestic pharmaceutical consumption is expected to continue growing in 2026, with pharmaceutical sales projected to increase by 3.0–4.0%, moderating slightly from 4.4% growth in 2025. Hospital-channel sales are forecast to grow by 3.5–4.5%, while over-the-counter (OTC) sales through pharmacies are expected to expand by 2.5–3.5%. Growth will be supported by the rising prevalence of non-communicable diseases (NCDs), population aging, and expanded healthcare coverage and benefit schemes that improve access to medical services. However, growth is expected to moderate due to several challenges. First, the ongoing Middle East conflict could cause periodic disruptions to pharmaceutical supply chains, creating risks of shortages of certain imported raw materials and constraints in plastic packaging supply, requiring manufacturers to seek alternative packaging materials. As a result, manufacturers may face higher production costs, while hospitals may rely more on existing inventories before replenishing drug stocks. Second, slower economic growth and weaker purchasing power may encourage consumers to reduce discretionary healthcare spending by limiting non-essential medicine purchases, reducing the frequency of hospital visits, or substituting herbal medicines for conventional medicines used to treat minor ailments. Third, medical tourism may soften, particularly among patients from the Middle East, a key market for Thailand’s hospital sector, due to travel safety concerns and higher travel costs. During 2027–2028, domestic pharmaceutical sales are expected to accelerate to 4.0–5.0% annual growth. Sales through hospitals are projected to expand by 4.0–5.0% per year, while OTC sales are expected to grow by 3.0–4.0% annually (Figures 12–13). In addition to the gradual recovery in economic activity and consumer purchasing power, further growth will be supported by:

-

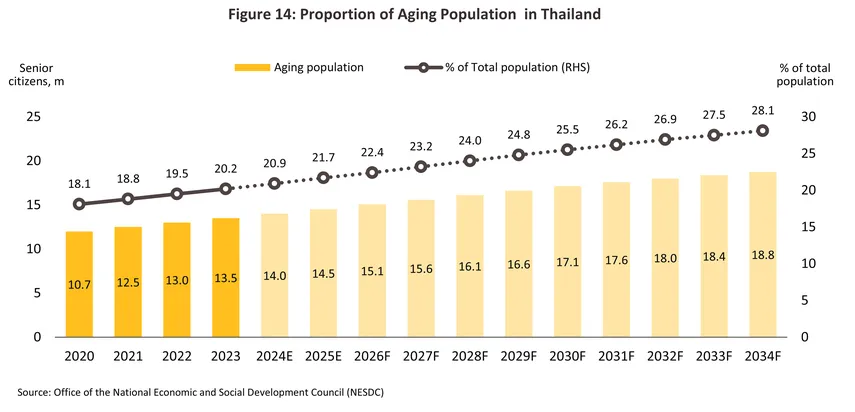

Rising prevalence of non-communicable diseases (NCDs) and air pollution-related illnesses. Key NCDs, including hypertension (+200k patients p.a.), diabetes (+100-200k patients p.a.), chronic kidney disease, cancer, and cardiovascular diseases, have continued to increase (Source: NESDC; Figure 6) and are expected to rise further in the coming years. This trend is being reinforced by Thailand’s rapidly aging population, with the country projected to become a super-aged society by 2034, when more than 28% of the population will be aged 60 and above (Figure 14). As older adults are more likely to suffer from chronic illnesses requiring long-term treatment, demand for medicines is expected to increase accordingly. Urbanization and changing lifestyles, including lower levels of physical activity and unhealthy dietary habits, are also contributing to the growing burden of chronic diseases. These trends are expected to support demand for chronic disease treatments and specialty medicines, particularly high-value innovative therapies such as targeted drugs, GLP-120/ therapies immunotherapies, and advanced cancer treatments. At the same time, the number of patients affected by air pollution-related illnesses is expected to continue rising, particularly in urban areas. Demand for pharmaceuticals, vaccines, and medical products will also be supported by the increasing incidence of infectious diseases requiring close monitoring, including influenza cases increased by 54.4% in 2025, as well as the risk of emerging, re-emerging, and zoonotic diseases. In addition, climate change is likely to increase the prevalence of vector-borne diseases, respiratory illnesses, and heat-related conditions, further supporting long-term growth in pharmaceutical demand.

-

Expanded healthcare coverage and improved access to medicines. Growth will be supported by (i) broader healthcare benefits under Thailand’s Universal Health Coverage (UHC) scheme, reflected in the National Health Security Fund budget of THB 270 billion for fiscal year 2026, up 15.3% from the previous year. Key initiatives include the “30-Baht Treatment Anywhere” program, the “Cancer Anywhere” program, expanded preventive care and disease screening services, and new healthcare delivery models such as telemedicine, all of which improve access to medical treatment and vaccines. In addition, the Social Security Office has expanded healthcare benefits through initiatives such as the SSO Cancer program, which improves access to treatment options and selected high-cost medicines, as well as enhanced dental care benefits. (ii) Rising participation in private health insurance schemes is also expected to support pharmaceutical demand. In the first half of 2025, health insurance premium income increased by 18.9% YoY21/ reflecting greater health awareness and efforts to mitigate rising healthcare costs. Together, these developments are expected to drive continued growth in domestic pharmaceutical demand.

-

Growth in medical and wellness tourism. According to the Global Wellness Institute, the global wellness tourism market is projected to reach USD 1.3 trillion by 2028, growing at an average annual rate of 9.0% during 2026–2028 (Figure 15). This presents an opportunity for Thailand as a leading global destination for medical tourism, supported by its high healthcare standards and competitive treatment costs. According to ABeam Consulting, the number of international patients in Thailand is expected to grow by an average of 5.3% per year22/ during 2026–2028. Additional support comes from initiatives such as the Andaman Wellness Corridor (AWC), investments in integrated wellness centers, and the development of healthcare facilities within leading resorts. International wellness tourism is also expected to recover further in 2027–2028 after a temporary slowdown in 2026 due to the Middle East conflict. These trends are expected to increase demand for pharmaceuticals, particularly anti-aging drugs, weight management drugs, and preventive healthcare medicines, especially among middle- and high-income consumers.

-

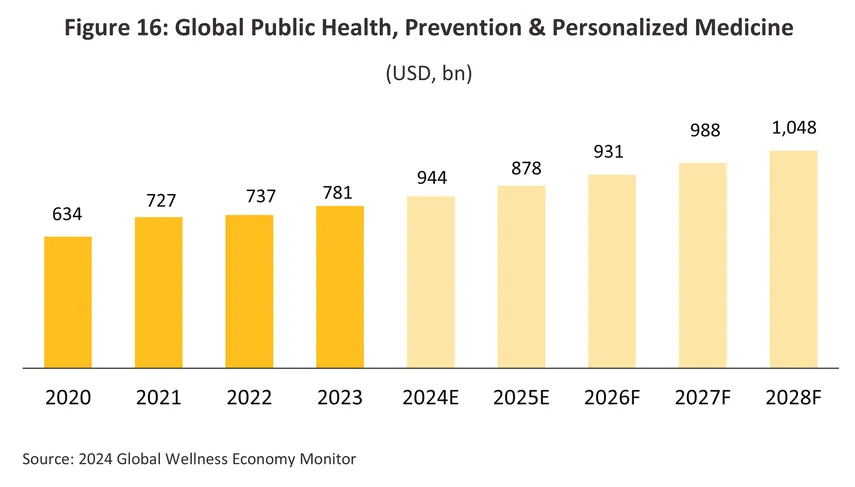

Growing emphasis on preventive healthcare and personalized medicine. Consumers are placing greater importance on long-term health management, particularly older adults and working-age populations who increasingly focus on disease prevention and healthy aging. This trend is expected to support demand for preventive healthcare products, including weight management drugs (particularly GLP-1 therapies), herbal medicines, vitamins, and dietary supplements. At the same time, advances in medical science and data analytics are accelerating the adoption of personalized medicine, enabling more accurate diagnosis and treatment selection tailored to individual patients. This improves treatment outcomes and supports demand for specialty drugs, particularly targeted therapies, biologics, and immunotherapies. Consistent with this trend, the Global Wellness Institute projects the global Public Health, Prevention & Personalized Medicine market to grow at an average annual rate of 6.1% during 2026–2028 (Figure 16).

-

Adoption of advanced technologies and digital platforms to enhance pharmaceutical manufacturing efficiency. Increasing investment in modern technologies across the pharmaceutical value chain, from drug discovery and development to manufacturing and distribution, is expected to improve productivity and competitiveness. Key developments include (i) the use of artificial intelligence (AI) and machine learning to accelerate drug discovery;23/ (ii) the application of big data analytics to patient and drug utilization data to improve the efficiency of pharmaceutical research and production; and (iii) the adoption of digital manufacturing and supply chain systems, such as Manufacturing Execution Systems (MES), e-Batch Records, and drug traceability solutions, to enhance product safety and supply chain transparency. Beyond improving operational efficiency, these technologies can also help reduce environmental impacts and support the long-term sustainability of Thailand’s pharmaceutical industry. (For further details, see Box 1 in the Pharmaceutical Industry Outlook 2025–2027)

Pharmaceutical export value is expected to remain broadly flat in 2026, against a low base in the previous year, amid economic uncertainty across key export markets. This may weigh on purchasing power and healthcare spending among consumer groups particularly sensitive to rising living costs. During 2027–2028, export value is projected to return to growth of 2.5–3.5% per year (Figure 11), supported by rising pharmaceutical demand in ASEAN, Thailand’s primary export market. Growth will be driven by the gradual economic recovery, population aging, and improved access to medicines through the continued development of healthcare systems across the region. According to Statista, the ASEAN pharmaceutical market is expected to grow at an average annual rate of 4.9% during 2025–2028. On the supply side, expanding investment in pharmaceutical and vaccine manufacturing, together with efforts to upgrade production standards in line with international requirements, will enhance Thailand’s export potential. Nevertheless, manufacturers are expected to continue facing pricing pressure from lower-cost producers in China and India.

Key challenges for Thailand’s pharmaceutical industry:

-

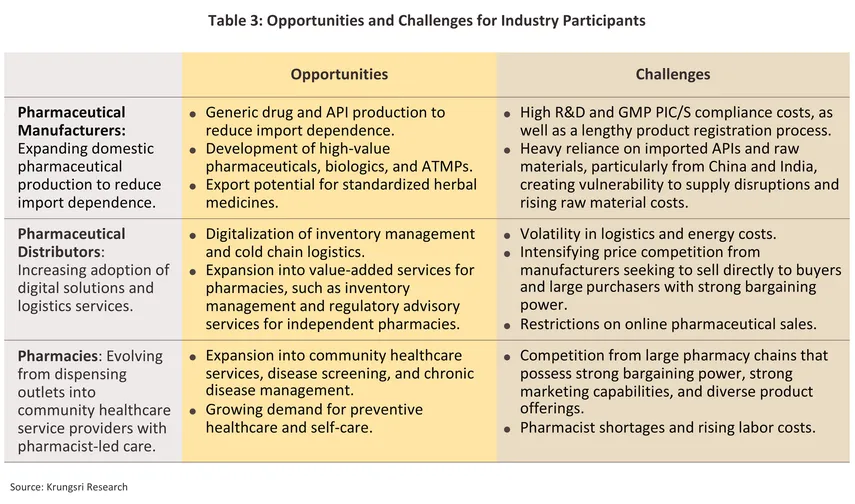

Heavy reliance on imported pharmaceutical ingredients and medicines. Thailand depends on imports for approximately 80%24/ of its pharmaceutical supply, while most domestically manufactured medicines also rely on imported raw materials. As a result, global supply chain disruptions or shortages of key inputs in source countries could increase the risk of drug shortages and higher pharmaceutical costs in Thailand. However, the impact of these risks varies across different segments of the pharmaceutical value chain (Table 3).

-

Intensifying competition from both foreign and domestic investors. The value of FDI applications in healthcare projects grew by an average of 67.0% per year during 2022–2025, with a cumulative proposed investment value exceeding THB 25.5 billion, covering both generic drug and API manufacturing projects. In addition, major Thai business groups from industries such as energy, chemicals, and food have increasingly expanded into the pharmaceutical and healthcare sectors, intensifying competition in the generic drug and OTC markets.

-

Constraints in R&D and high-value pharmaceutical manufacturing. Although Thailand has made progress in developing biologics and advanced medical products, the industry still faces limitations in the availability of specialized talent in biopharmaceuticals and advanced biotechnology. This is particularly relevant to the development and production of biologics and Advanced Therapy Medicinal Products (ATMPs), resulting in continued reliance on imports of high-value pharmaceuticals and biopharmaceutical products.

-

Rising cost pressures on domestic manufacturers. Pharmaceutical producers face increasing costs from upgrading facilities and quality control systems to comply with GMP PIC/S standards and meet regulatory requirements for both domestic and export markets. Additional cost pressures stem from ESG-related investments, including the adoption of clean energy and technologies to reduce PM2.5 emissions. At the same time, prices of medicines listed on Thailand’s National List of Essential Medicines (NLEM) remain subject to government price controls, limiting manufacturers’ pricing flexibility.

1/ In accordance with the World Trade Organization (WTO) Agreement on Trade-Related Aspects of Intellectual Property Rights (TRIPS)

2/ Source: Government Pharmaceutical Organization (GPO), “API Production to Reduce Imports and Strengthen Thailand’s Pharmaceutical Security,” Bangkok Biz News, 21 April 2026.

3/ Source: Thailand Drug System Development Action Plan (2023–2027).

4/ Upstream vaccine production includes BCG (tuberculosis), aP (acellular pertussis), Tdap (tetanus, diphtheria and pertussis), and COVID-19 vaccines. Downstream vaccine production includes rabies, Japanese encephalitis (JE), and influenza vaccines. Source: National Vaccine Institute.

5/ Thailand’s national immunization program currently covers 13 vaccine-preventable diseases: tuberculosis, diphtheria, pertussis, tetanus, hepatitis B, Haemophilus influenzae type b (Hib) disease, polio, measles, rubella, mumps, Japanese encephalitis, cervical cancer (HPV), and rotavirus gastroenteritis. Source: National Vaccine Institute.

6/ The Drug Act has been Thailand’s primary pharmaceutical legislation since 1967 and was most recently amended under the Drug Act (No. 6) B.E. 2562 (2019)

7/ Source: Office of Industrial Economics (OIE) and Krungsri Research, 2024.

8/ Source: National Health Accounts 2020–2021 and Health Expenditure Projections 2022–2024.

9/ Source: National Health Security Office (NHSO), 2024.

10/ Source: BMI/Fitch Solutions, Q4 2024.

11/ Includes (i) modern pharmacies, (ii) pharmacies specializing in the sale of prepackaged drugs that are not subject to controls on their sale, (iii) wholesalers of pharmaceuticals, (iv) importers of pharmaceuticals, and (v) manufacturers of pharmaceuticals. Source: Thai FDA.

12/ The import and export of goods with HS codes HS 3001 3002 3003 3004

13/ HS 3002

14/ PIC/S was established to harmonize GMP inspection standards among member authorities.Thailand became the 49th member on 1 August 2016.

15/ Source: Office of Industrial Economics (OIE). Refers to the production of finished pharmaceutical products, including liquid medicines, tablets, capsules, creams, powders, and injectables.

16/ PM2.5 concentrations were approximately 3.8 times higher than the WHO recommended guideline. Source: 2025 World Air Quality Report.

17/ In fiscal year 2025, the number of inpatients receiving treatment through public healthcare services across Thailand’s 13 health regions reached 8.3 million, up 3.4% from fiscal year 2024.

18/ The 32 covered minor ailments include dizziness, headache, joint and muscle pain, toothache, menstrual pain, abdominal pain, diarrhea, and constipation/hemorrhoids, among others.

19/ Targeted medicines are medicines designed to act on specific cells or molecular pathways associated with a disease. Thailand has begun investing in domestic production of targeted therapies, including joint initiatives between the Government Pharmaceutical Organization (GPO) and private-sector partners under the BCG Economy policy, with a focus on treatments for cancer and immunodeficiency disorders.

20/ GLP-1 Receptor Agonists (GLP-1RAs) are incretin-mimetic drugs used to improve blood glucose control and reduce appetite. Originally developed for type 2 diabetes, they are increasingly prescribed for obesity management.

21/ "Overview of the Thai Life Insurance Industry in the First Half of 2025," Thai Life Assurance Association, 1 August 2025.

22/ “ABeam Consulting shares insight on Thailand’s pharmaceutical sectors’ opportunities, challenges, and entry approaches for New Entrants”, ABeam Consulting 1 เมษายน 2568

23/ The global market for AI applications in drug discovery and development is projected to expand at a compound annual growth rate (CAGR) of 29.7% during 2026–2028.

24/ Source: Health Systems Research Institute (HSRI), “Thailand Imports More Than 80% of Its Medicines; Clinical Research Expansion to 30 Centers Proposed Amid Hospital Drug Dispensing Constraints”.

25/ Ministerial Notification of the Ministry of Public Health on the Designation of Substances as Drugs under the Drug Act B.E. 2510 (1967),

dated 15 May 2026, classifies products containing genes, cells, or tissues derived from living organisms, intended for the diagnosis, treatment, alleviation, cure, or prevention of human diseases or illnesses, or intended to affect the health, structure, or any function of the human body, as drugs under the Drug Act B.E. 2510 (1967).

26/ Cabinet Policy Statement, 9 April 2026

.webp.aspx)