EXECUTIVE SUMMARY

In 2026, the Thai sugar industry is projected to expand, supported by a favorable supply factor stemming from increased production due to the onset of the La Niña phenomenon since the 2025/2026 crop season. This production growth is also driven by farmers expanding cultivation areas due to attractive prices in the preceding year. However, domestic market expansion is expected to be modest, constrained by the slow recovery in the economy and the tourism sector. The supply increase is anticipated to drive strong export growth across several key markets, many of which are initiating a new sugar stock accumulation cycle to ensure food security and meet the expected gradual recovery in demand from downstream industries. Furthermore, this industry will benefit from market expansion to countries where Thailand secures new trade agreements.

However, in 2027-2028, sugar production is projected to decline due to the anticipated return of El Niño, which is expected to reduce yield per rai. Nonetheless, domestic consumption is likely to gradually recover, supported by improving economic activities and tourism, which continue to drive demand in the food, beverage, and restaurant industries. This will move against trends in export markets, where domestic supply constraints will make it difficult to meet overseas demand. This situation will likely be worsened by intensifying competition from other sugar-producing nations, most notably Brazil.

Krungsri Research view

Over 2026-2028, industry income will improve on stronger domestic sales, but receipts from exports will remain volatile.

-

Sugarcane growers: Revenue of sugarcane growers is projected to remain volatile, following the direction of global sugarcane and sugar prices, which is partly a consequence of uncertainty risks related to both climatic conditions and global sugar supply. Growers are also in a weak bargaining position relative to sugar mills, as production costs are rising due to higher energy, fertilizer, pesticides, herbicides, and labor costs, especially during the harvest of fresh sugarcane. This will then impact net profits and may negatively affect future planting decisions.

-

Traders: Exporters are expected to benefit from the gradual recovery in economic activities and related industries, including food, beverage, tourism, and restaurant sectors in trading partner countries. However, players may face risks from expected fluctuations in global sugar prices and supply conditions, which could affect inventory management costs.

-

Sugar mills: Revenue is expected to gradually improve, supported by rising domestic consumption driven by: (i) the recovery of purchasing power in line with the overall economic outlook; (ii) the rebound in tourism, which will stimulate demand in related industries, particularly food, beverage, and restaurant sectors; and (iii) the sale of by-products, especially molasses, which is expected to benefit from growing ethanol demand in the transport sector as economic activities and investments recover, alongside government measures promoting ethanol blending in gasohol. Furthermore, a strong supply chain, product diversification, and investment in high value-added downstream industries (utilizing by-products and waste materials as inputs) will help sugar mills maintain profitability. However, rising production costs due to higher cane procurement prices—above the initial reference rate—may pressure some mills into losses or liquidity constraints, particularly during 2027–2028.

Overview

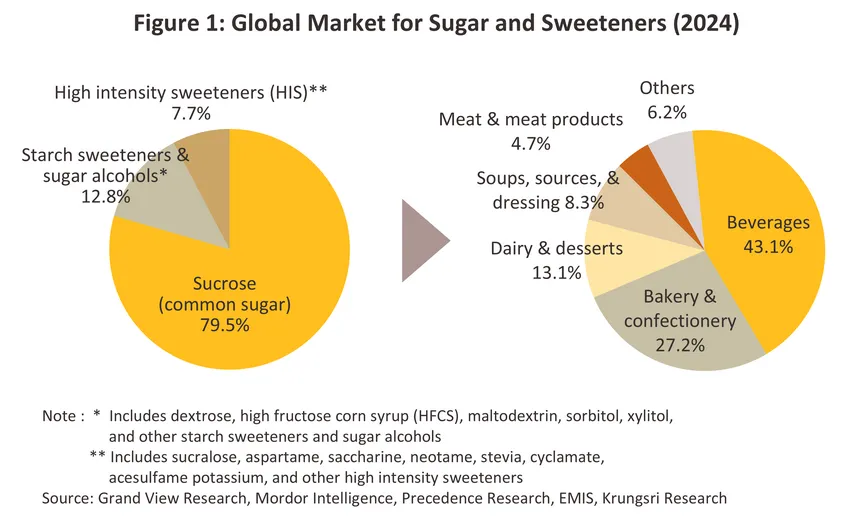

Sugar is a plant-derived product that is used to increase sweetness1/. Global demand for sugar remains strong, with sugar consumed both directly and indirectly, in the latter case as an additive or flavoring in a wide range of other products, including foods, beverages, processed dairy products (milk, butter, yoghurt, etc.), candy, baked goods and so on. In 2024, 79.5% of all sweeteners consumed globally2/ were sucrose-based, with the remainder being accounted for by a number of non-nutritive products. These include natural items such as honey, stevia and monkfruit (also called luohan guo), high intensity sweeteners such as aspartame cyclamate and neotame, and starch sweeteners and sugar alcohols (e.g., maltrodextrin, fructo-oligosaccharides and inulin) (Figure 1).

Products derived from sugar processing can be split into the following.

-

Raw sugar: This brown substance, though the color can range from light to dark, has moderate moisture and high molasses content, exhibits a tightly packed crystalline structure, and tends to contain large quantities of impurities and residues. Raw sugar is subject to further process, and this then results in white sugar, refined sugar and other sugar-derived products including ethanol, alcohol, and bioplastics. This refining process is what converts raw sugar into a product fit for human consumption.

-

White sugar: This is obtained by removing impurities from raw sugar. White sugar is crystalline, colored white to pale yellow, has a low molasses and moisture content, and is loosely aggregated and more friable than raw sugar. White sugar is an ingredient for domestic household use and is also used as a raw material in food and drinks processing.

-

Refined sugar: This goes through the same refining process as white sugar but the end product has fewer impurities and tends to be in the form of clear white granules. Refined sugar is very pure, with zero molasses content and very low or zero moisture. Refined sugar is generally produced for household consumption and for industrial processes that require very pure sugars, such as making carbonated and energy drinks, and producing pharmaceuticals.

-

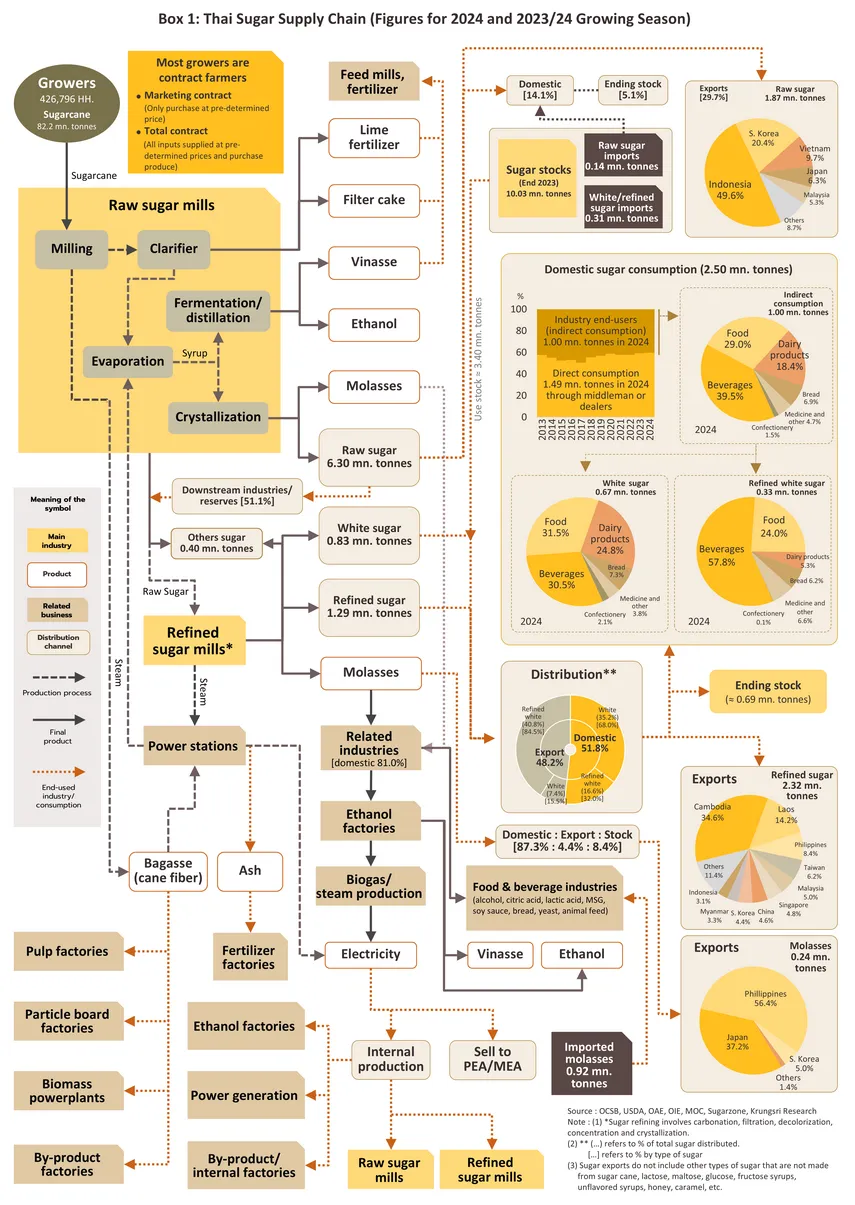

Byproducts of sugar refining: Byproducts or value-added products that arise from sugar refining include molasses3/, bagasse4/, filter cake5/, vinasse6/ and steam7/.

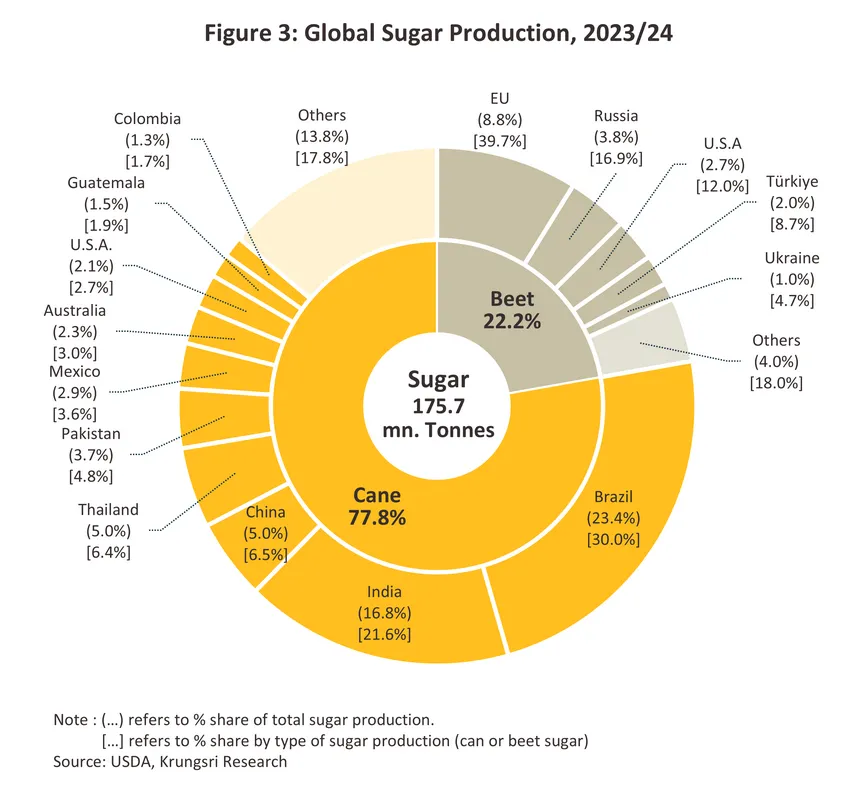

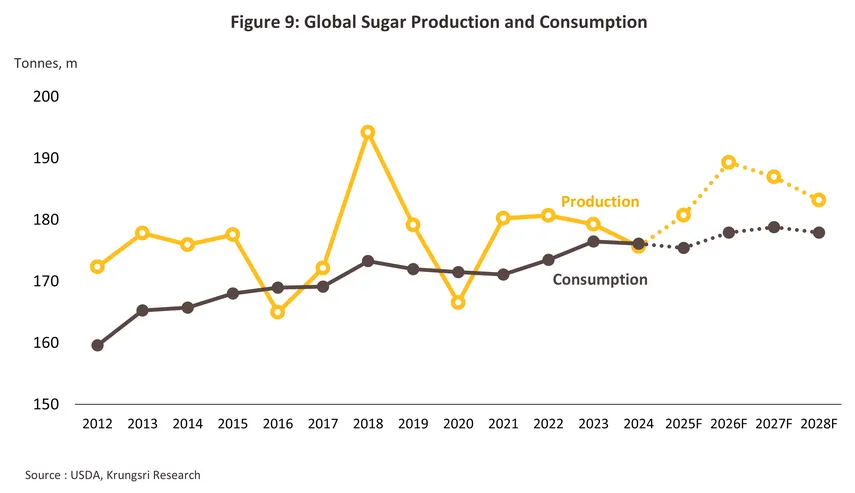

Over the two decades between 2004 and 2024, global output and consumption of sugar climbed steadily (Figure 2). This is supported by both the rising global per capita sugar consumption, which increased to 24.9 kilograms per person in 2024 from 21.2 kilograms per person in 20048/, as well as the expanding demand for sugar from downstream industries (such as food and beverages, and ethanol). In 2024, global sugar production thus hit 175.7 million tonnes (measured as raw sugar), with the biggest producers being Brazil (23.4% of global production), India (16.8%), the European Union (8.9%), China (5.7%), Thailand (5.0%), and the US (4.8%). Production can also be categorized according to the source of the sugar. (i) 77.8% of global output came from sugarcane, most of which was grown in countries in equatorial zones and in the Asia-Pacific region, including Brazil (the source of 30.0% of all sugarcane-produced sugar), India (21.6%), China (6.5%), Thailand (6.4%), and Pakistan (4.8%). (ii) The remaining 22.2% of the world’s supply of sugar came from sugar beet, 39.7% of which originated in the European Union. The EU was followed in importance by Russia (16.9%), the United States (12.0%), Türkiye (8.7%) and Ukraine (4.7%) (Figure 3).

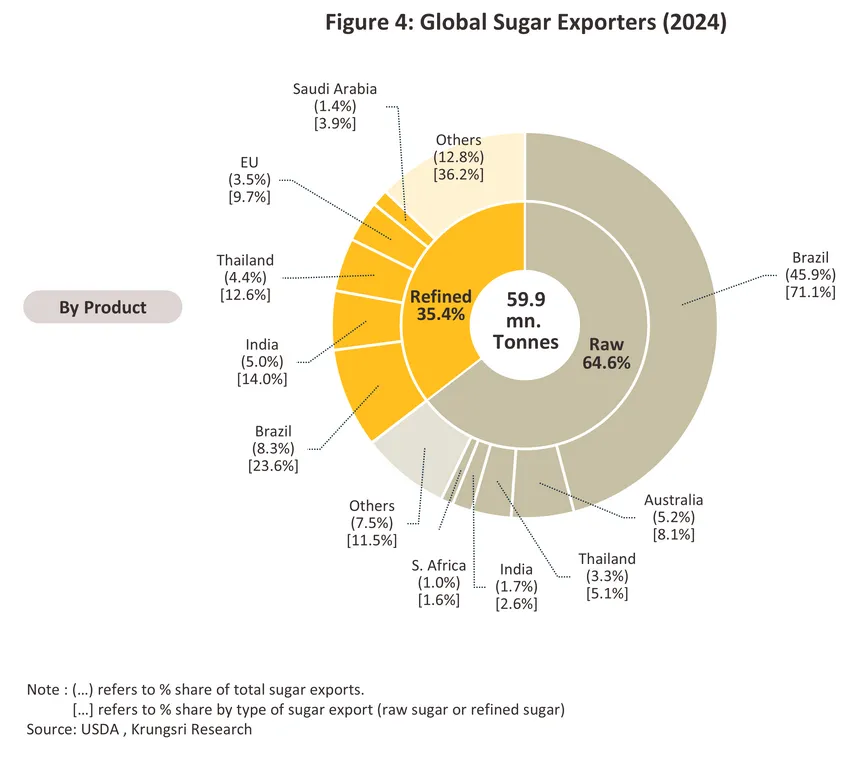

In 2024, a total of 59.9 million tonnes of sugar was traded on world markets, this thus representing 34.1% of global production. The largest exporter was Brazil, which was the source of 54.2% of supply to global markets, followed by Thailand (7.7%) and India (6.7%) (Figure 4). By product type, exports are split between: (i) raw sugar (64.6% of all exports globally), for which Brazil is the main originator (71.1% of all exports of raw sugar) and then in order of importance, Australia (8.1%), Thailand (5.1%), India (2.6%), and; and (ii) refined sugar (35.4% of exports), for which the main exporters are Brazil (23.6% of exports of refined sugar), India (14.0%), Thailand (12.6%), and the European Union (9.7%) (Figure 4).

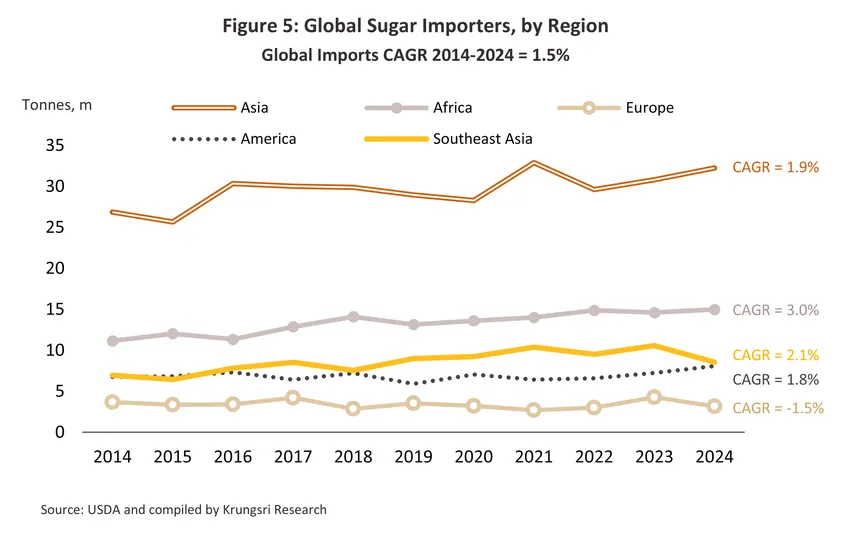

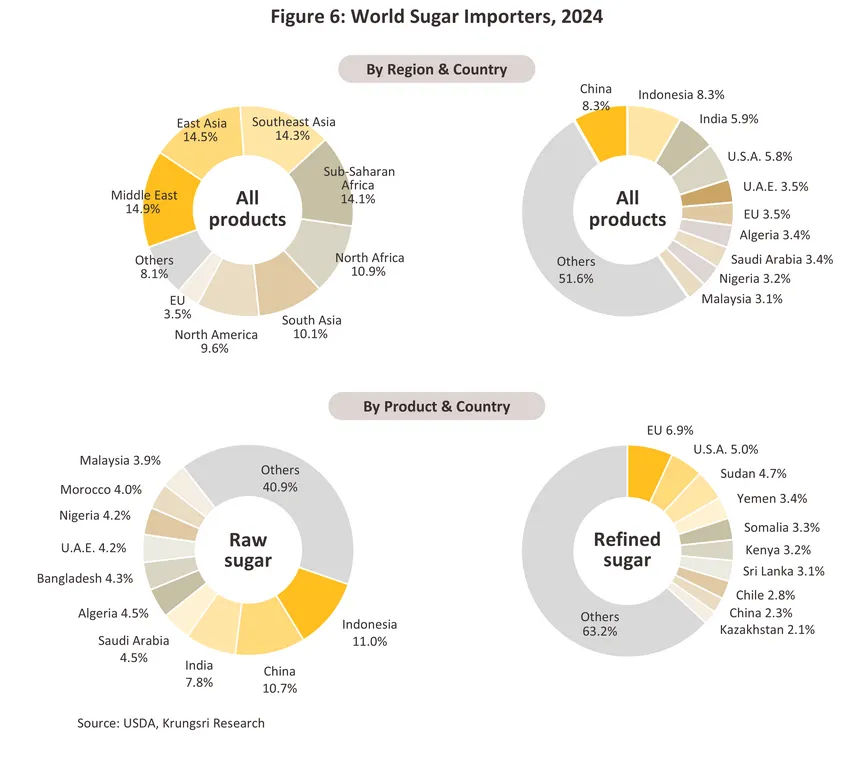

The world’s most important importers of sugar are in Asia, and with a 8.3% share by quantity, China is currently the world’s leading buyer of sugar traded on global exchanges (Figure 5 and Figure 6). Coming after China in order of importance are Indonesia (8.3%), India (5.9%), the United States (5.8%), and U.A.E. (3.5%). Considered by type, Indonesia is the world’s largest importer of raw sugar (11.0% of the world import quantity), followed by China (10.7%), India (7.8%), Saudi Arabia (4.5%), and Algeria (4.5%), while for refined sugar, the biggest importers are the European Union (6.9% of all global sales of refined sugar), the United States (5.0%), Sudan (4.7%), Yemen (3.4%), and Somalia (3.3%).

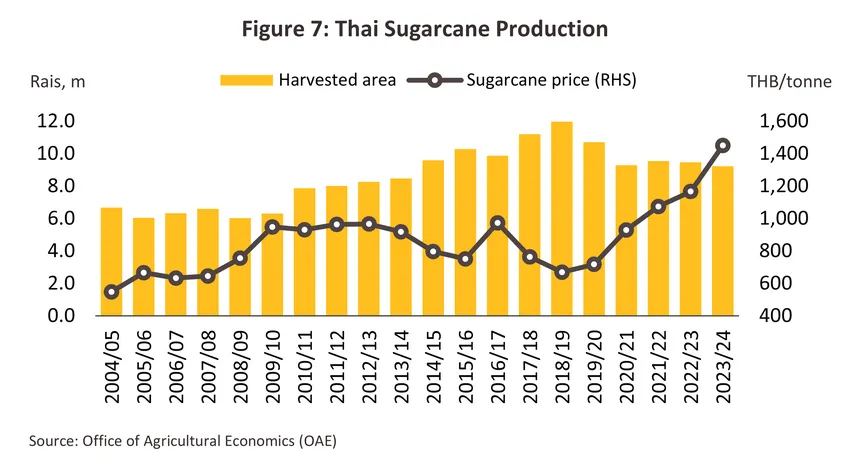

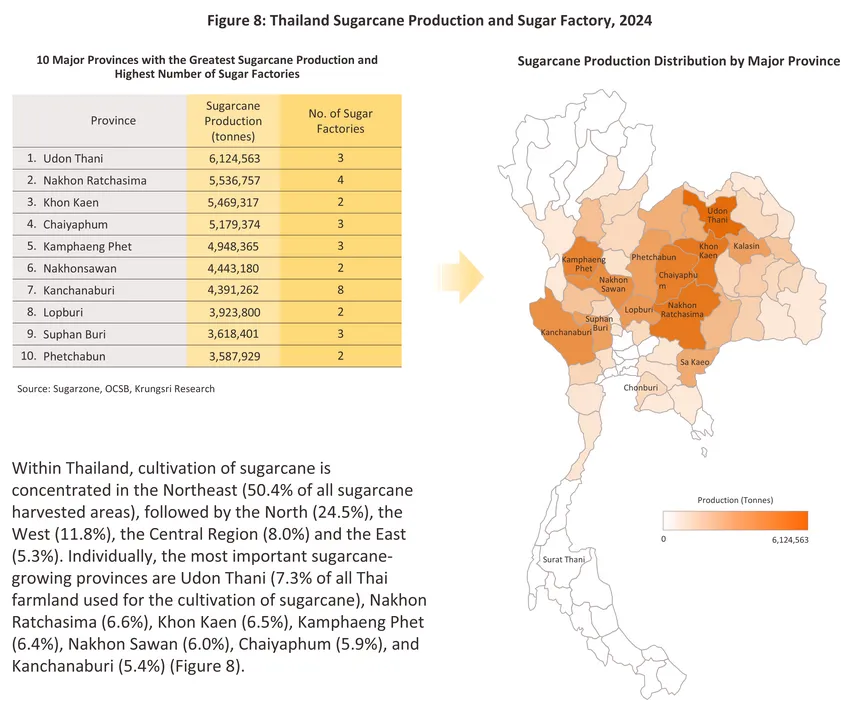

From 2010 to 2019, Thailand’s sugarcane harvested area expanded at a 7.4% CAGR, driven by steady sugar consumption growth across both domestic and export markets, stemming from end-consumers and downstream industries (food, beverage, dairy products). However, over the past five years, this area has progressively declined, contracting at a -5.1% CAGR from 12.0 million rai in 2019 to 9.2 million rai in 2024 (Figure 7). This reduction is largely attributed to highly volatile climate conditions, specifically escalating drought severity, combined with unpredictable sugar costs and prices. As a result, farmers are shifting to more drought-resistant economic crops, primarily cassava.

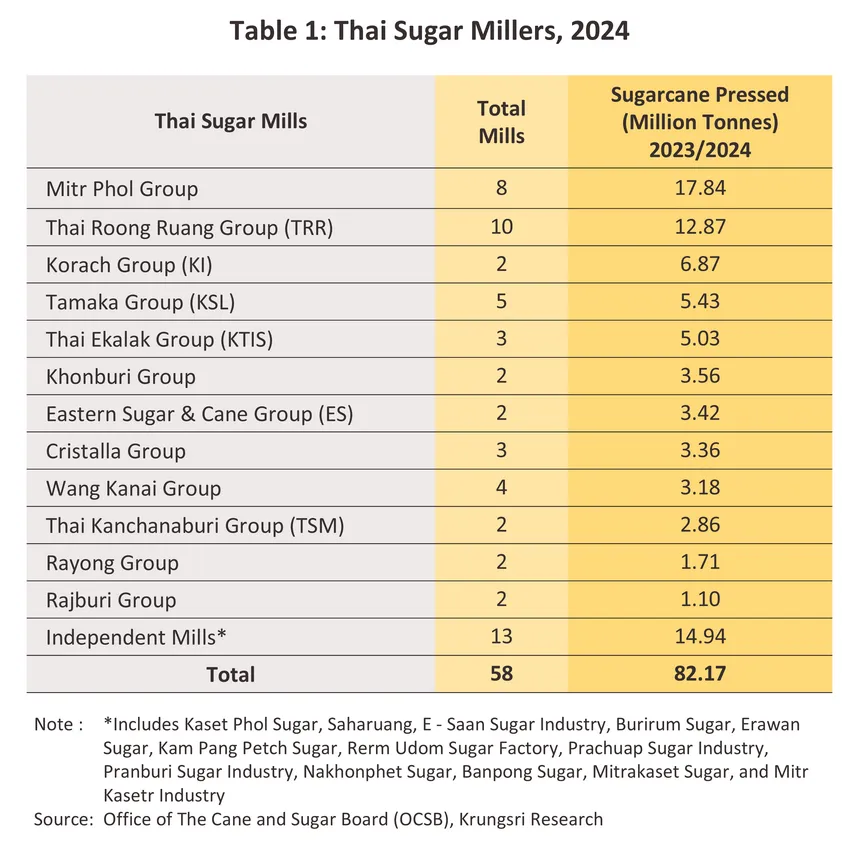

There are a total of 58 sugar mill operators in Thailand (Table 1). The majority are located in close proximity to cultivation areas due to: (i) The convenience of securing raw materials in line with production plans; (ii) Savings in transportation costs; and (iii) The ease of communication, promotion, or assistance provided to farmers. Furthermore, factory locations are typically selected near logistical facilities (such as major cities, ports, and trade hubs). Kanchanaburi holds the highest number of sugar mills with 8 factories, followed by Nakhon Ratchasima (4 factories), and Udon Thani, Kamphaeng Phet, Suphan Buri, Chaiyaphum, and Sa Kaeo (3 factories in each province).

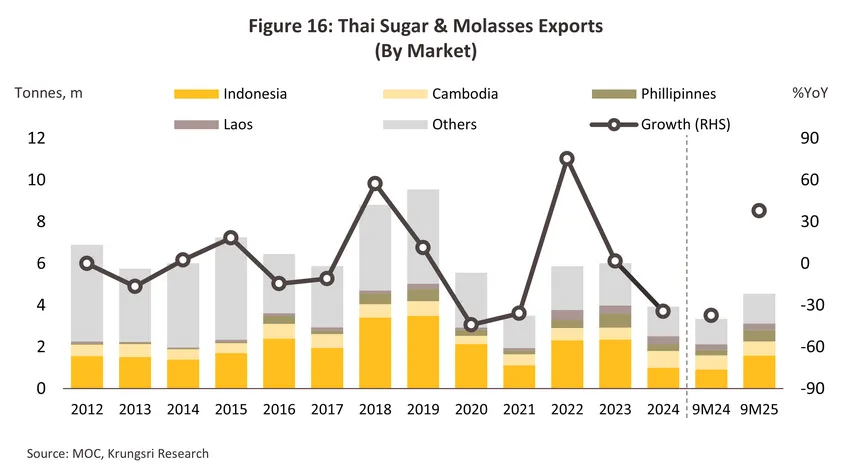

With 56% of output sold overseas, the Thai sugar industry relies primarily on export markets, of which the most important are Indonesia (buyers of 22.6% of all Thai sugar exports volume), Cambodia (18.2%), South Korea (11.2%), Lao PDR (8.4%) and the Philippines (7.5%). The state of export markets for the main product groups in 2024 is outlined below.

-

Raw sugar: Exports of raw sugar comprised 42.2% of all Thai sugar exports in 2024, or a total of 1.9 million tonnes. The main markets for this were in Indonesia (buyers of 49.6% of Thai exports volume of raw sugar), South Korea (20.4%), and Vietnam (9.7%).

-

White sugar: 2.3 million tonnes of white sugar were exported in 2024 (52.4% of Thai sugar exports volume), for which the biggest markets were Cambodia (34.6%), Lao PDR (14.2%), and the Philippines (8.4%).

-

Molasses: Molasses exports amounted to 5.4% of all Thai sugar exports in 2024, or 0.2 million tonnes. This was bought principally by the three countries of Philippines (56.4% of Thai molasses exports volume), Japan (37.2%), and South Korea (5.0%).

Domestic consumption absorbed 44% of the industry’s output9/, split between 59.8% that was sold to the consumer market for household consumption and 40.2% that went to industrial buyers for use in beverage production (39.5% of industrial consumption volume), food processing (29.0%), processing with milk products (18.4%), and other uses (13.1%).

In addition to receipts from the sale and distribution of sugar, companies also generate income from the commercial exploitation of byproducts arising from the sugar refining process. These include molasses, which is used to produce ethanol and indeed thanks to government promotion of this (mainly by specifying the proportion of ethanol that is mixed with gasoline to sell as gasohol)10/ demand is growing. Many sugar mills have also invested in downstream businesses that use byproducts of sugar milling as inputs, including biomass energy production11/ and the manufacturing and production of paper pulp, particle board, and fertilizer (Box 1).

Situation

The situation for the global sugar industry is described below.

-

Global sugar supply contracted -2.0% to 175.7 million tonnes in 2024 (Figure 9), largely as a result of an El Niño that impacted sugarcane outputs in Asia. As such, sugar production in the region dropped -4.9%, with falls particularly strong in India (-20.3%) and Thailand (-20.4%). However, bad weather in Asia was somewhat counterbalanced by better conditions in South America and Europe. Thus, the global market benefited from: (i) a 7.8% increase in supply from Brazil, the world’s most important producer and exporter, where a combination of gains in the price of sugar relative to ethanol and better weather helped to boost production of sugar from cane; and (ii) a 9.8% jump in the production of sugar from beet (up 13.6% in the EU, 8.2% in Russia, 17.2% in Turkey, and 36.8% in Ukraine) that came as a result of a more favorable climate and an expansion in the area under cultivation. 2025 global sugar supply is expected to have bounced back to growth of 2.9%, bringing this to a total of 180.8 million tonnes. The main driver of this will be more favorable weather across the majority of sugar-producing regions, especially in Asia. Production of sugar from sugarcane should therefore be up 2.1% on stronger supply from Brazil, Thailand, China and Mexico, while production from beet is forecast to rise 5.8% on better conditions in the EU, Egypt, China and the US.

-

Worldwide, sugar consumption slipped -0.2% in 2024, edging down to 176.1 million tonnes (Figure 9). Declines were driven by: (i) the rising cost of living and slowing economies that then undercut purchasing power and demand from downstream industrial consumers, and with even major producers such as Brazil and the EU seeing demand soften (down by respectively -7.4% and -0.6%), domestic supply gluts developed; (ii) rising public concern with sugar consumption and increased government action on public health12/ that then reduced consumer demand; and (iii) supply-side factors that included bad weather and a resulting shortage of inputs in some countries. As such, demand slackened in many countries, including Brazil (-7.4%), Indonesia (-3.9%), Mexico (-4.3%), the US (-1.1%) and the EU (-0.6%). Global sugar demand in 2025 is projected to reach 175.4 million tonnes, representing a marginal contraction of -0.4%. The primary pressure stems from the economic slowdown in key consuming nations, such as India, Thailand, the United States, and Russia, resulting in a decline in sugar demand from both direct consumption and usage in downstream industries.

-

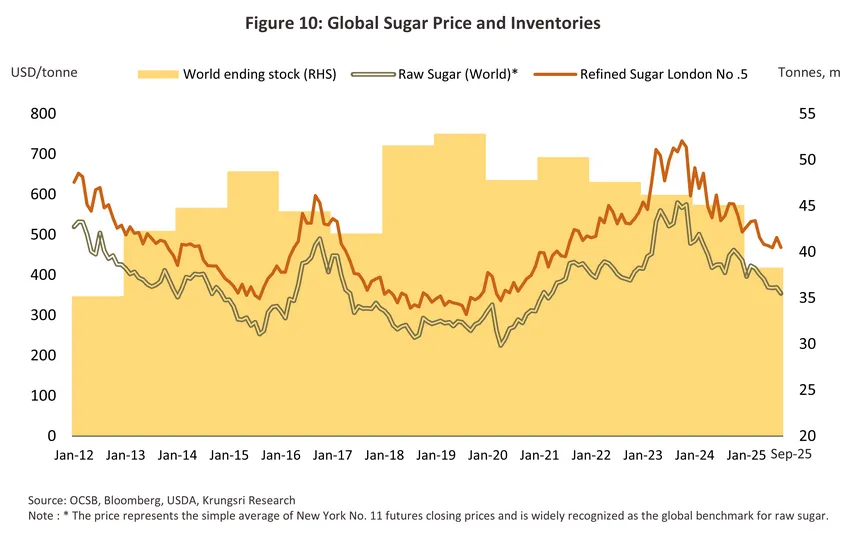

Exports also declined in 2024, falling -3.3% to 59.9 million tonnes on tightening supply to global markets from Asia. In particular, exports (excluding molasses) were down -52.2% from India and -32.5% from Thailand, where drought meant that insufficient inputs were available to supply overseas markets. As a result, global stocks shrunk -2.4% to 45.1 million tonnes (Figure 10). The decline in demand and the slowdown in the global economy indicated that a supply glut might emerge, particularly in Brazil since better climatic conditions meant that the oversupply to the market was significant. Global prices thus came under pressure, with average 2024 prices for New York No. 11 and London No. 5 dropping by respectively -13.1% and -13.0% to hit USD 448.6/tonne and USD 577.8/tonne.

2025 exports are expected to reach 68.0 million tonnes worldwide, which would represent a jump of 13.4%. Global markets are benefitting from an increase in supply from the major producing nations of Brazil and Thailand, where better weather is boosting the sugarcane harvest. In addition, export markets are also being stimulated by deeper worries over food security and a perceived increased need to maintain greater domestic inventories as a hedge against the global trade war and worsening geopolitical tensions. Global stocks are thus dwindling and these are expected to have contracted -15.1% to 38.3 million tonnes (Figure 10). Moreover, the stumbling world economy and resulting weakness in demand is confronting an expansion in supply and this is depressing prices. Over the first 9 months of 2025, average prices for New York No. 11 and London No. 5 therefore contracted by respectively -13.6% and -15.9% to fall to USD 387.4/tonne and USD 495.3/tonne, and for all of 2025, these are expected to average USD 387-396/tonne and USD 485-491/tonne.

Conditions within the domestic sugar industry over 2024 and 2025 were as follows.

-

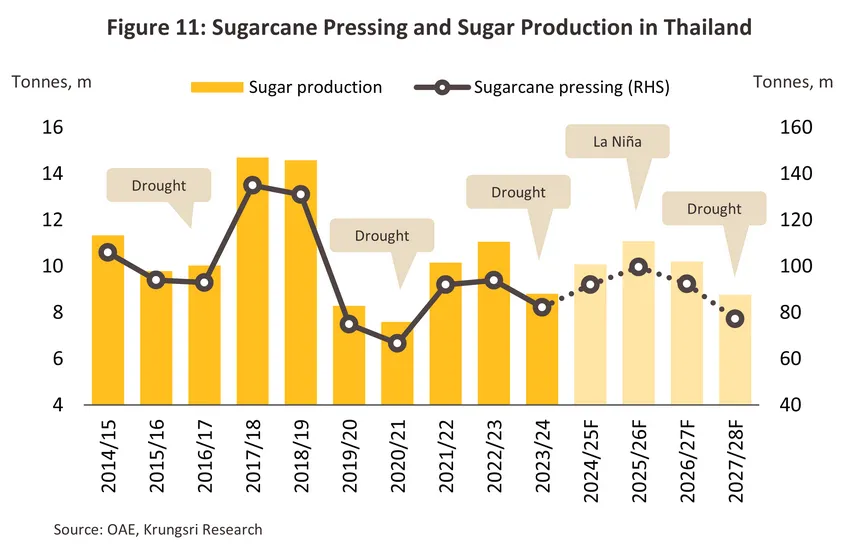

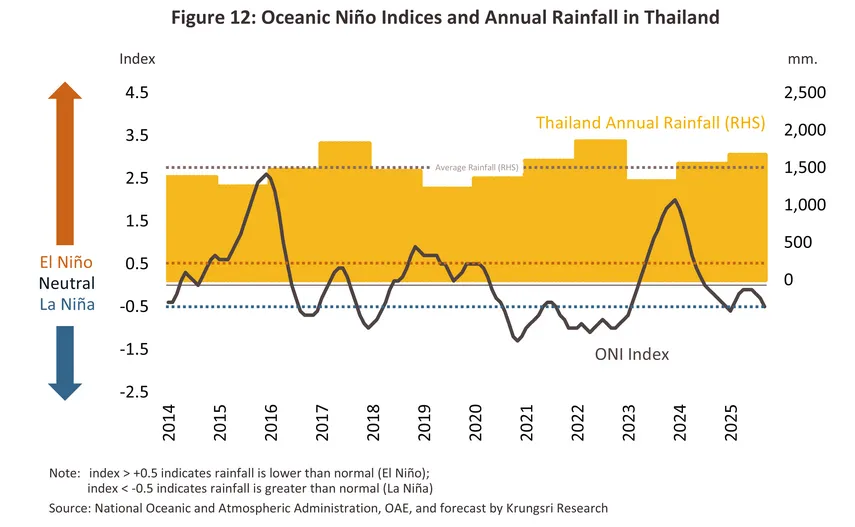

82.2 million tonnes of sugarcane were pressed in the 2023/2024 growing season (-12.5%), though the quantity of sugar produced from this fell at the faster rate of -20.4% to 8.8 million tonnes (Figure 11). Production was impacted by: (i) El Niño conditions that cut rainfall during the 2023 planting season (Figure 12), which then decreased outputs and reduced the average sugar content to 12.4 CCS13/ ; and (ii) worries among farmers that incomes would be adversely affected by measures allowing mills to cut payments to suppliers of burnt cane or to refuse this altogether that then encouraged some to switch to planting rice and cassava. However, tighter supply lifted sugarcane prices and so these jumped 24.4% to THB 1,450.5/tonne, ahead of production costs that averaged THB 1,203/tonne14/. The situation improved during the 2024/2025 growing season, and an estimated 92.0 million tonnes (+12.0%) of sugarcane production should be pressed this season. This will then yield 10.1 million tonnes of sugar, or a jump of 14.4%. These gains have come from: (i) better weather and heavier rainfall; and (ii) the stimulus effect on supply of the previous year’s rise in sugarcane prices to a historic high, financial support for farmers to assist with the harvest, and measures to help growers generate income from unused parts of the sugarcane plant. However, the flip side of stronger domestic and international supply is softer prices, and so for 2025, these will average THB 1,100-1,200/tonne.

-

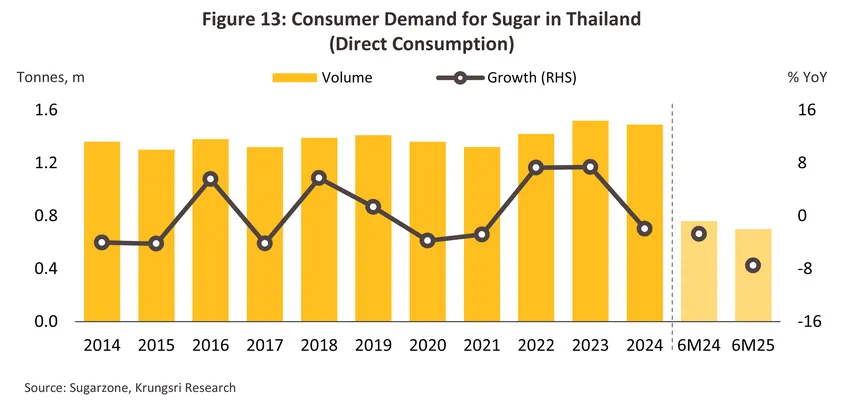

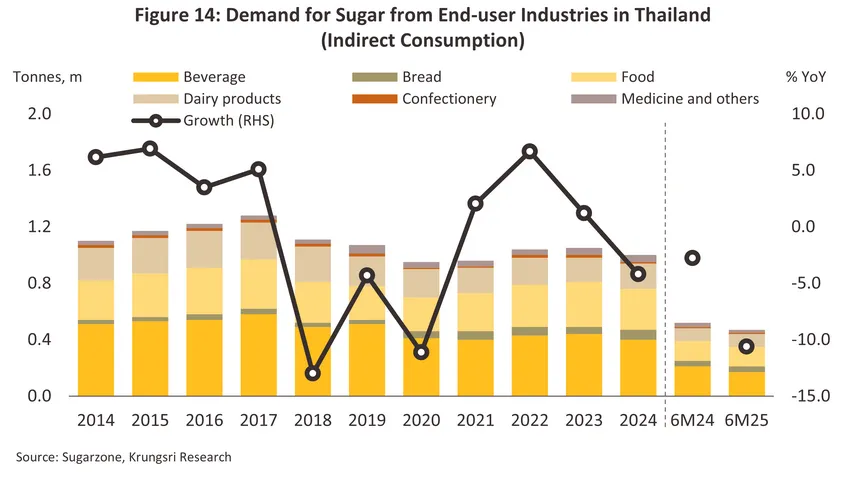

Consumption of white and refined sugar fell -2.9% to 2.50 million tonnes in 2024 on: (i) deepening health concerns and rising awareness of the dangers of sugar, which then translated into a -2.0% decline in direct consumption (down to 1.49 million tonnes); (ii) the increasing care shown by consumers over discretionary spending, including candy and sugary drinks, as the high cost of living and sluggish economic conditions took their toll on spending power; and (iii) the effects of the sugar tax, which in addition to encouraging beverage manufacturers to focus on low- or no-sugar drinks is also pushing manufacturers of other foods to cut the quantity of sugar in their products. Indirect consumption of sugar thus contracted -9.0% in the beverage industry, -7.8% in the food industry, -9.5% in the production of medicines and pharmaceuticals, and -6.6% in the manufacture of candy and sweets. These industries account for 75% of all indirect consumption of sugar and so overall, this fell -4.2% to 1.00 million tonnes (Figure 13-14). Over the first half of 2025, consumption of white and refined sugar slipped by another -8.8% YoY, this thus dropping to a total of 1.17 million tonnes. Direct consumption was down -7.5% YoY to 0.70 million tonnes, with declines again being driven by a combination of weak economic conditions (especially in the tourism, restaurant, and beverage industries) and worries over health that are eroding direct and indirect demand for sugar. Purchases by downstream industrial users thus fell back -10.6% YoY overall, though the introduction of the 4th and final phase of the sugar tax15/ helped to slash demand from beverage manufacturers by -21.1% YoY. Consumption also dropped for use in the production of medicines (-45.4% YoY) and bread, beer, and spirits (-3.0% YoY). Through the remainder of 2025, a worsening economic outlook will add to preexisting headwinds to cut overall domestic demand by between -8.5% and -10.5%, or to just 2.23-2.28 million tonnes.

-

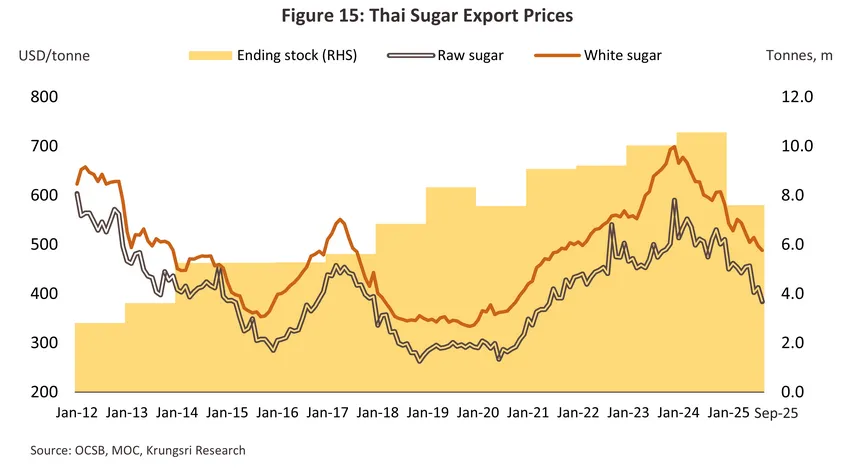

Exports of sugar and molasses slumped -34.4% to 4.43 million tonnes in 2024. This was a consequence of: (i) the El Niño and the subsequent shortage of sugarcane; and (ii) the resulting measures put in place by the Ministry of Commerce and the Office of the Cane and Sugar Board, which cut sugar export quotas as the authorities looked to ensure that supply was sufficient to meet domestic demand (forecast to grow on the strength of the tourism and food and beverage industries). Major markets that saw the sharpest declines included Indonesia (-57.6%), the Philippines (-50.6%), Malaysia (-60.7%) and South Korea (-33.4%). Export prices were also impacted by movements in global markets and with the latter fearful about a supply glut in Brazil, these softened. Prices for exports of sugar and molasses from Thailand thus crashed -29.8%, with receipts from overseas sales falling at the same rate to hit THB 2.5 billion (Figure 15 and Figure 16).

Exports of sugar and molasses bounced back strongly over the first three quarters of 2025, surging 37.8% YoY to 5.2 million tonnes and generating receipts worth USD 2.4 billion (+12.3% YoY). The market benefited from: (i) the ending of the drought and the return of a more favorable climate that then boosted sugarcane outputs; and (ii) the rundown in previously substantial sugar stocks. The strongest gains were seen in Indonesia (+72.0% YoY), the Philippines (+110.9% YoY), South Korea (+48.3% YoY) and China (+147.3% YoY). For all of 2025, exports are forecast to reach 5.95-6.04 million tonnes, or a rise of 34.3-36.3%. However, export prices are expected to slide by -18.5% YoY on worries over rising global supply.

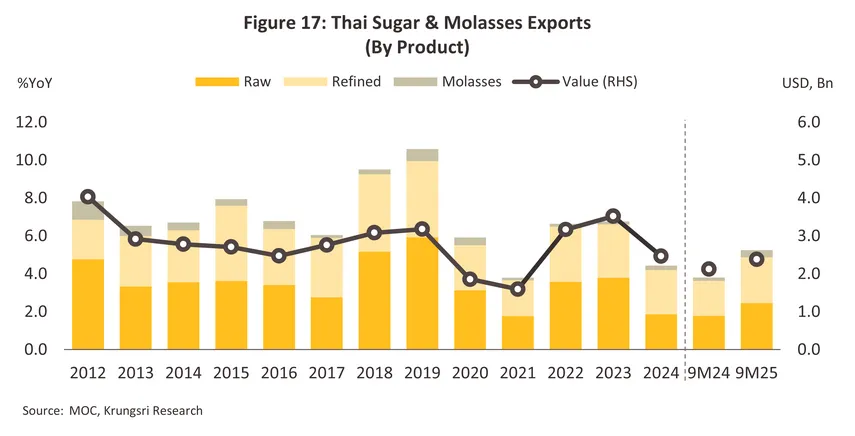

Details of export volume and earnings by product category are given below (Figure 17).

-

Raw sugar: By volume and value, 2024 exports slumped -50.7% and -45.3% to totals of respectively 1.9 million tonnes and USD 1.0 billion. The sharpest falls were seen in sales to Indonesia (-58.5% to 0.9 million tonnes), South Korea (-40.8% to 0.4 million tonnes) and Malaysia (-79.3% to 0.1 million tonnes). As described above, the emergence of an El Niño ate into the supply of inputs and diverted what was available to domestic industries, and so although global demand remained strong, Thai players were not able to respond effectively to this. As might be expected, this discrepancy fed through into stronger prices, which climbed 6.3% to USD 514.8/tonne. The situation improved over the first 9 months of 2025, and thanks to an increase in outputs and a rise in stocks, exports jumped 37.3% YoY to 2.5 million tonnes, with earnings up at the somewhat slower rate of 16.7% YoY to reach USD 1.1 billion. Sales into major markets thus bounced back to growth, surging 76.6% YoY in Indonesia and 32.2% YoY in South Korea. Over the remainder of the year, exports should continue to perform well and so for 2025 overall, these are expected to total 2.55-2.59 million tonnes (+36.5-38.5%). However, persistent fears over an oversupply to the market will continue to weigh on prices, and so these are forecast to contract -15.5% YoY to USD 435.3/tonne.

-

White sugar: In 2024, exports of white sugar fell -17.4% to 2.3 million tonnes, though earnings from this declined at the slightly slower rate of -15.7% to generate income worth USD 1.5 billion. As with the raw sugar segment, exports were hurt by a shortage of inputs and so declines were seen across the major markets of the Philippines (-67.5% to 195.4 kilo tonnes), Indonesia (-40.1% to 71.9 kilo tonnes), Singapore (-26.8% to 111,4 kilo tonnes), Taiwan (-15.4% to 145.0 kilo tonnes) and Lao PDR (-8.6% to 330.2 kilo tonnes). In response, export prices inched up 0.7% to an average of USD 624.5/tonne. Through the first 9 months of 2025, exports returned to growth, rising 31.1% YoY by volume and 7.7% by value to respectively 2.4 million tonnes and USD 1.2 billion. Among the most important markets, strong growth was seen in sales to the Philippines (+132.8% YoY), China (+116.6% YoY), and Malaysia (+58.3% YoY) as well as to the regional markets of Cambodia (+1.3% YoY), Lao PDR (+21.3% YoY), Vietnam (+90.9% YoY) and Myanmar (+11.8% YoY). Growth rates will likely slow through the remainder of the year and so for 2025, exports should total 2.89-2.94 million tonnes (+24.6-26.6%). However, with prices weakening on global exchanges, average Thai export prices for 2025 are forecast to slip -17.6% YoY to USD 521.6/tonne.

-

Molasses: Exports jumped 55.6% to 0.24 million tonnes in 2024, with income from these sales up at the even faster rate of 88.9% to reach USD 46.3 million. This was largely explained by the strength of the Philippine market (the source of 56% of all export orders by volume), where increasing demand for molasses for use in the production of animal feed, alcohol, ethanol and biomass energy drove a 130.2% jump in sales (to 135.0 kilo tonnes). By contrast, exports to Thailand’s second-most important market of Japan, where molasses is used to manufacture alcohol, ethanol and amino acids, slipped -4.2% to 88.9 kilo tonnes. More generally, demand for molasses to use in a broader range of applications helped to lift prices, which thus surged 60.3% to USD 286.6/tonne. Conditions improved further over the first 9 months of 2025, with exports up another 111.5% YoY to 378.5 kilo tonnes and income from this rising 50.1% YoY to USD 51.5 million. The Philippine market continued to perform well, with sales expanding by another 81.3% YoY to 188.4 kilo tonnes. However, the country’s share of total exports of molasses from Thailand slipped to 49.8% as exports to South Korea (for use in the alcohol, animal feed, and food and beverage industries) climbed to 117.6 kilo tonnes, sufficient to give the country a 31.1% market share. 2025 exports are on target to reach 505.6 to 510,3 kilo tonnes (a rise of between 111.2% and 113.2%), but with the cost of inputs falling globally, export prices are expected to slump -46.4% YoY to USD 169.3/tonne.

Outlook

-

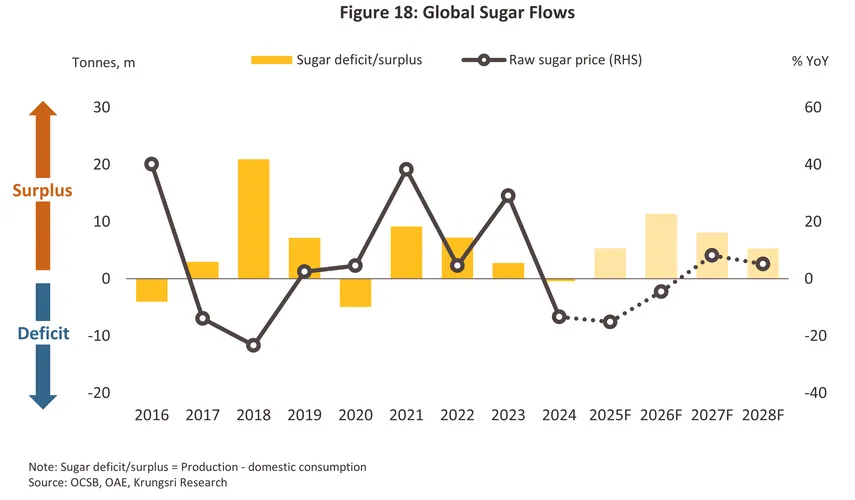

The USDA sees global sugar production rising 4.7% to 189.3 million tonnes in 2026 on: (i) La Niña and better weather conditions, which will lift Indian production (the world’s second most important supplier of sugar) by 25.9% to 35.3 million tonnes; and (ii) the increased need to build sugar stocks to offset worries over food security and to meet anticipated future demand from downstream industries. However, if, as expected, the climate flips to El Niño conditions, Krungsri Research forecasts global sugar output sliding by between -0.6% and -2.6% CAGR over 2027 and 2028 since this would cut rainfall and suppress outputs in Asia, especially in India and Thailand. Nevertheless, world markets will be supported by better climate conditions and rising outputs in Brazil that will counterbalance the worse weather in Asia. In addition, sugar prices are expected to rise strongly in 2027-2028, and this will further encourage Brazilian manufacturers to focus on sugar production at the expense of ethanol.

-

Growth in global demand will remain flat through 2026 as US tariffs drag on the world economy and weaken spending power, although this will be somewhat offset by the pressure to shore up food security and to build domestic stocks. The situation should improve slightly in 2027 and 2028 as global economic activity picks up and demand revives, especially from the food and beverage, tourism, and other downstream industries. Global demand is anticipated to commence its recovery phase during 2027–2028, albeit at a low average annual growth rate of 0.1–1.1%. This momentum will be driven by the gradual revival of global economic activities and the upward trajectory of the food, beverage, and related downstream industries, along with a mild rebound in the global tourism sector. However, the expansion of global sugar demand will remain constrained due to the countervailing pressure from the worldwide health-conscious trend to reduce sugar consumption, coupled with related regulatory control policies. These policies include measures that directly and indirectly impact sugar consumption demand, such as sugar taxes, mandatory nutritional labeling systems, restrictions on the marketing and advertising of high-sugar food or beverages, and the mandatory reformulation of food and beverage products to meet specified sugar content standards.

-

Prices for raw sugar set on world markets should average USD 363-370/tonne (16.5-16.8¢/lb) in 2026, down from USD 384/tonne (17.4¢/lb) in 2025. Prices have been suppressed by an extension in supply that has outrun growth in demand (Figure 18). However, the situation will shift in the coming years, and supply will tighten again as: (i) drier conditions return in 2027-2028; and (ii) farmers switch to planting drought-resistant crops, such as cassava. In addition, returns have fallen below the five-year average for 2021-2025, further suppressing supply. Consequently, prices are forecast to climb to USD 397-417/tonne (18.0-18.9¢/lb) in 2027 and 2028.

Domestically, output from the 2026-2027 growing season is likely to be affected by a worsening climate that will limit the quantity of sugarcane available for pressing. However, even as supply tightens, domestic sugar demand is likely to improve in line with the gradual recovery of the Thai economy and tourism sector. This will contrast with a potential decline in exports due to intensified competition from major global producers. Details are given below.

-

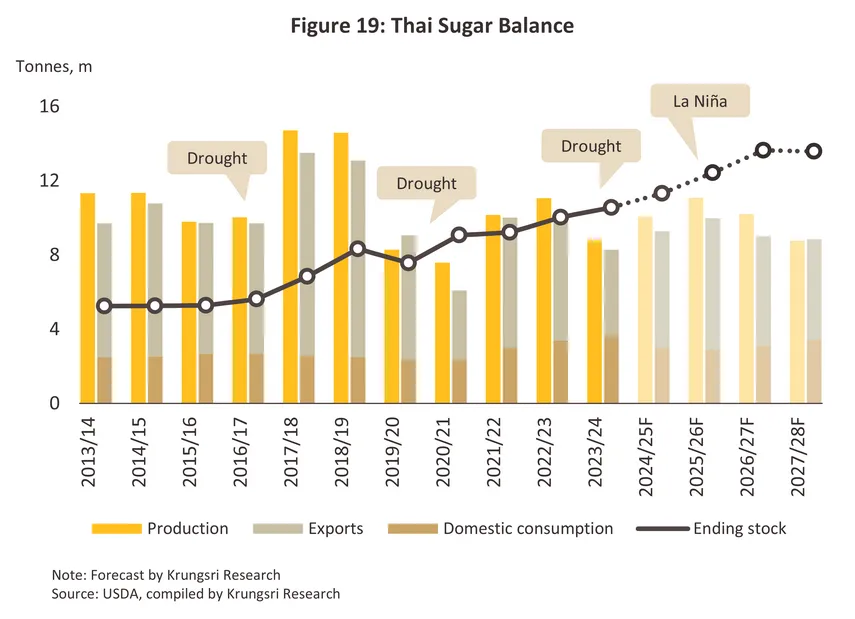

98.8-100.6 million tonnes of sugarcane are expected to be pressed during 2026, and this should then yield 11.0-11.2 million tonnes of sugar (+9.0-11.0%) (Figure 19). Supply will be boosted by: (i) heavier rainfall thanks to the onset of neutral and then La Niña16/ conditions in 2025, which is especially important for sugarcane growers since this is mostly planted in areas that are beyond the reach of irrigation systems; and (ii) higher prices in the previous season that will then incentivize farmers to expand the area under cultivation. However, increased output by the major producing nations of Brazil, India, and Thailand will suppress prices on both global and Thai markets. As such, the price paid for domestic sugarcane is expected to soften by between -3.5% and -5.5% to an average of THB 1,070-1,095/tonne. However, total outputs from the 2027-2028 growing season are forecast to slide to 77.2-92.3 million tonnes per year, which would then result in a fall in sugar output of between -10.1% and -12.1%, or to just 8.8-10.2 million tonnes per year. This will be caused by: (i) the possible return of an El Niño and the effects of this on crop losses and per-unit yields; (ii) the switch by farmers to more drought tolerant and easier to harvest crops; and (iii) high production costs, especially for fertilizer and energy, which will then encourage farmers to cut back on applications, further lowering outputs. Lower supply to the Thai and global markets will tend to lift sugarcane prices, and so these are expected to rally by 5.7-7.7% to reach an average of THB 1,173-1,234/tonne.

-

Annual domestic sugar consumption is projected to expand by 3.5-5.4% per year over 2026-2028 to reach 2.9-3.4 million tonnes per year (Figure 19). However, sluggishness in the tourism sector and in the economy generally will combine with more cautious consumer spending (especially on non-essential food and drinks that typically have a high sugar content and are bad for health) to restrict 2026 growth. The outlook will improve in 2027 and 2028 thanks to: (i) gradual growth in tourism and the economy, which will drive greater direct consumption via restaurants and beverage outlets and lift sales to industrial consumers, especially manufacturers of food and drinks, which should rebound in line with stronger household and service-sector spending, most notably in restaurants and hotels; and (ii) low-base effects in 2025. Nevertheless, the impacts of the sugar tax on sweetened drinks will continue to drag on growth.

-

Exports of sugar and molasses will do well in 2026, expanding by 11.9-13.9% to a total of 6.7-6.8 million tonnes. Growth will come despite the impacts of US tariffs on global trade and the world economy, in part because of: (i) better weather and an expansion in the area under cultivation, which will ease problems with a shortage of inputs and so allow players to better respond to overseas demand for Thai molasses and sugar; (ii) the onset of a new round of restocking that will be driven by the need to shore up feed security and to build reserves to meet strengthening demand from downstream industries; and (iii) a broadening of distribution channels, especially with countries with which Thailand should conclude free trade agreements since at present, progress continues to be made on these17/. Unfortunately, exports will likely contract again through 2027-2028. By volume, overseas sales of sugar and molasses will drop by between -11.4% and -13.4% in each of these years to hit 5.2-5.6 million tonnes per year. This will be caused principally by supply-side problems, including: (i) the possible return of El Niño conditions, which will cut outputs and restrict access to inputs, thereby potentially resulting in a lack of goods to fill export orders; and (ii) increased competition from other major sugar-producing nations, especially Brazil

Players in the Thai sugar industry will need to face additional challenges in the coming period. (i) Companies within the industry may have to deal with a drop in supply that will be caused by: (a) sugarcane production costs that remain higher than the cane price, particularly due to elevated costs of fresh cane harvesting and persistently high labor expenses stemming from labor shortages; and (b) pressure on supply as growers switch to planting crops that are easier to harvest, are more drought- and pest-resistant, and that realize higher prices. (ii) Growth in direct sugar consumption is being undercut by rising global consumer concerns over personal health and wellness, while the introduction of sugar taxes both in Thailand and in export markets is reducing indirect demand from downstream manufacturers, especially of drinks. (iii) Uncertainty over the outlook for the regulatory environment is rising. (a) Both financial and non-financial regulations governing purchases of burnt sugarcane change annually. (b) The new Sugar and Sugarcane Act is currently under consideration by the Office of the Cane and Sugar Board, and as part of this, farmers have proposed that bagasse be included in a byproduct resulting from the manufacturing process. However, doing so would have an impact on the profit-sharing scheme18/. (c) The recent hike in US tariffs will impact the market, although limited, as the US is not a major market for Thai sugar producers 19/. Risks of excess global sugar supply flowing into Thailand also remain contained, given Thailand’s import control measures. Any slowdown in the global economy, however, will result in weaker purchasing power in export markets overall, and this will thus generate indirect impacts.

Adoption strategies for the sugar industry

-

The industry will focus on ensuring security of supply. This will involve: growers cooperating to make the SDG goals20/ a reality, in particular those relating to water resources and the environment; managing costs to better generate economies of scale; supporting greater technology transfer from sugar mills and government agencies; and expanding the reach of irrigation systems, thus cutting the risk of future supply shortfalls. In addition, the BCG model21/ will be used to support the development of the industry and its supply chains, thereby raising farmers’ profits and ensuring that inputs are secured for the sugar industry as a whole.

-

Growing interest in environmental issues and in the ESG (environmental, social and governance) framework is influencing the strategic decision-making processes of both government agencies and private-sector players. These are thus pivoting towards a greater focus on reducing pollution, particularly air pollution, by the sugar and sugarcane industry, and to this end, a wide range of policies are being considered. These include: agreeing a memorandum of understanding with relevant agencies to support monitoring, enforcement, and appropriate punishments in areas where sugarcane burning occurs; using unburnt sugarcane ahead of burnt cane, with the latter only accessed once supplies of unburnt products are not available; and agreeing deductions to the price paid for burnt sugarcane, while to further discourage openair burning, sales of cane leaves will be encouraged. Farmers will be educated on how best to harvest sugarcane so that post-harvest CCS levels can be maintained, and more broadly, the greening of the industry and the transition to carbon neutrality will be facilitated by the use of modern smart farming technology and innovation that extends across the production lifespan, from initial planting to the transport of harvested products to mills. On-farm processes will therefore be increasingly automated.

1/Sugars are found in low quantities in most plant tissues but sugarcane and beet have sufficiently high concentrations that they can be cultivated for the commercial production of sugar.

2/Considering only sugar.

3/Molasses is produced from boiling down sugarcane or beet during the sugar refining process. This results in a viscous, dark brown liquid that is used as an input into ethanol production (which is then mixed into gasohol) or in the food and drinks industry to make products including alcohol, yeast, monosodium glutamate, pet food, vinegar, and a range of different sauces.

4/Although bagasse is a waste product resulting from the pressing of sugarcane, it is one of the main inputs into biomass energy production. Bagasse is also used to produce packaging and various construction materials including fiber board, particle board, melamine faced chipboard, medium-density fiber board (MDF), synchronous MDF, lacquer high gloss MDF, and pure cellulose.

5/As its name suggests, filter cake is produced from the filtering of liquid sugarcane extracts. The residue left behind by the filtering processing contains nutrients and minerals that can be used to make fertilizer or animal feed, or processed into biogas.

6/Vinasse is used to make organic fertilizer and animal feed.

7/Surplus steam can be used to power machinery or to generate electricity for use within the sugar mill.

8/Source: OECD-FAO Agricultural Outlook 2016-2025

9/This does not include imports of raw sugar that are used to make white sugar or stocks of raw sugar held in the country.

10/In 2024, installed production capacity for the manufacture of ethanol from sugarcane and molasses came to 3.63 million liters per day

(this does not include another 1.07 million liters per day of capacity in facilities that use both cassava chip and molasses). This then generated annual demand that totalled over 3.0 million tonnes for molasses (-8.5%) and 0.9 million tonnes for pressed sugarcane (-10.7%).

11/Energy produced from bagasse-powered biomass facilities is generally consumed within the sugar mill itself or sold to nearby consumers.

12/These include sugar taxes on drinks, nutri-score/nutri-grade labeling, restrictions on advertising food and drink with

a high sugar content, and enforcing standards for maximum sugar content for consumable items. These regulations

are reducing demand both directly and indirectly (i.e., via the food and beverage industry).

13/CCS is short for ‘commercial cane sugar’, a system for measuring sugarcane quality. The scoring reflects the quantity of sugar in the cane

that can be extracted and used to make pure refined sugar. High scores thus indicate a high sugar content, with 10 CCS indicating that

1 tonne (or 1,000 kilograms) of sugarcane will produce 100 kilograms of pure refined sugar (or a ratio of 10%).

14/From the Office of the Cane and Sugar Board and the Office of Agricultural Economics.

15/Taxes are levied on drinks with a sugar content greater than 6 grams per 100 milliliters. With effect from 1 April, 2025, the sugar tax is now at phase 4 of its implementation, with the tax set at four rates: (i) A sweetness level of 0-6 grams per 100 milliliters is tax exempt; (ii) a sweetness level of 6-8 grams per 100 milliliters incurs a duty of THB 1/liter; (iii) a sweetness level of 8-10 grams per 100 milliliters incurs a duty of THB 3.0/liter; and (iv) a sweetness level of more than 10 grams per 100 milliliters incurs a duty of THB 5.0/liter. The introduction of the tax has had the effect of prompting manufacturers to cut the quantity of sugar in their drinks.

16/The National Oceanic and Atmospheric Administration (NOAA) predicts that there is a greater than 50% chance that over October-December 2025, the Pacific will switch to La Niña conditions (i.e., rainfall is likely to be above average) (source: Weekly ENSO Evolution, Status, and Prediction Presentation, NOAA, 29 September, 2025).

17/The Department of Trade Negotiations is currently in discussion over a number of free trade agreements (FTAs). These include the Thailand-South Korea, Thailand-Peru, Thailand-EU, ASEAN-Canada, ASEAN-India, and ASEAN-South Korea FTAs. The Thailand-EFTA (the European Free Trade Area, which includes Iceland, Lichtenstein, Norway, and Switzerland) and Thailand-Sri Lanka FTAs have been agreed and are now in the process of being enforced.

18/A revenue-sharing system (the ‘70:30 system’) has been established by law to split revenue between sugarcane growers and sugar millers. In each growing season, the system divides net profits from domestic and export sales between farmers, who receive 70% of net profits as ‘compensation for the sugarcane price’, and processors, who receive 30% as ‘compensation for production’. These proportions are set by the 1984 Sugarcane and Sugar Act.

19/The direct impacts of the imposition of US Section 232 or ‘reciprocal’ tariffs will be limited by the fact that: (i) the US is not a major market for Thai sugar exporters; and (ii) exports of sugar to the US are covered by the Tariff Rate Quotas (TRQs), which give Thailand a limited annual quota. Likewise, the risk of excess global supply flooding markets is relatively slight thanks to: (i) the lower prices in global markets relative to the US; (ii) Thailand’s position as a leading global supplier and exporter of sugar; and (iii) the continuation of the domestic cane and sugar system, which despite the enforcement of WTO rules and the signing of a number of FTAs still determines pricing and allows for import controls, thereby restricting access to the domestic market by overseas companies.

20/There are 17 Sustainable Development Goals (SDGs), organized into 169 SDG Targets that are regarded as universal, interconnected, and mutually supportive. Progress towards meeting the SDGs is assessed through 247 indicators. Overall, the SDGs are grouped into the 5 primary areas (the ‘5 Ps’) of: (i) people; (ii) planet; (iii) prosperity; (iv) peace; and (v) partnership (source: Office of the National Economic and Social Development Council).

21/The BCG model has three components. The ‘B’ is for the bioeconomy, which attempts to ensure that bio-resources are used with maximum efficiency by raising outputs, maximizing value added, and emphasizing biodiversity. This is linked to the circular economy, the ‘C’, which closes the economic loop to ensure the greatest possible reuse of resources. This thus includes making full use of products across their entire lifecycle and then reusing or recycling these. Both of these are then subsumed into the ‘G’, that is, the green economy. This aims to address problems with pollution and to sustainably reduce human impacts on the world (source: the National Science and Technology Development Agency).

.webp.aspx)