EXECUTIVE SUMMARY

The natural rubber industry from 2026-2028 is projected to expand in terms of both production and demand. In 2026, production is expected to grow as the La Niña phenomenon is anticipated to transition toward a neutral state during the first three quarters of 2026, creating favorable conditions for increased outputs. This growth is further supported by farmers' efforts to maintain and accelerate harvesting, driven by attractive market prices. However, production is likely to contract during 2027-2028 due to the expected return of El Niño conditions. Average domestic sales volume over three years is projected to increase, driven by 1) the automotive industry, tires, and electric vehicle components; 2) the construction sector, which is expected to gradually recover in line with government infrastructure development; and 3) ongoing government measures to absorb surplus production and promote domestic rubber consumption. While exports in 2026 will still benefit from accelerated stockpiling for automotive and parts manufacturing, they are expected to contract in 2027-2028 due to potential supply shortages and importers slowing orders to deplete existing inventories. Overall, the rubber industry continues to face risks from competition with rivals in CLMV countries, which are likely to expand their global market share following increased Chinese investment in cultivation. Additionally, international trade barriers, including both tariffs and Non-Tariff Barriers (NTBs), are expected to become more stringent, particularly impacting downstream products targeting the U.S. market, such as tires.

Krungsri Research view

From 2026-2028, the overall performance of midstream rubber product manufacturers in Thailand is expected to remain stable or expand modestly, amid intensifying competitive pressures, particularly from neighboring countries whose output is increasingly entering the market. This outlook is further shaped by uncertainty about domestic output, the gradual recovery of downstream manufacturing industries, and rising costs from more stringent trade protectionist measures.

-

Rubber growers: Incomes are projected to improve in line with higher expected outputs driven by favorable weather conditions in 2026, alongside rising price levels supported by demand from downstream industries. However, during 2027–2028, farmers face supply risks from anticipated drought conditions, cultivation costs remain elevated due to high labor and fertilizer prices, combined with the management costs of rubber leaf fall disease, which may still occur periodically, could impact overall profitability.

-

Rubber traders: The revenue is facing high uncertainty. As marketing channels narrow, industrial factories are increasingly tending to purchase rubber products directly from farmers, central markets, or cooperatives. Furthermore, traders may be impacted by Chinese entrepreneurs directly contacting and purchasing rubber from Thai farmer groups, which bypasses the raw material supply chain of Thai middlemen, alongside a shift in import markets, particularly China, which is increasingly importing from the CLMV countries.

-

Producers of intermediate products: Revenue is likely to expand, albeit at a modest rate, as follows.

-

Manufacturers of Ribbed Smoked Sheet (RSS) and Compound Rubber: Performance trends are expected to remain stable, as trading partners accelerated their stock accumulation during 2025-2026, leading importers to likely slow down orders between 2027-2028. This period coincides with a projected decline in supply due to the impact of El Niño, which will also drive-up raw material processing costs and potentially affect profitability.

-

Manufacturers of Technically Specified Rubber (TSR) and Mixed Rubber: Performance is trending toward improvement in line with demand from the automotive and parts sectors in China, particularly the electric vehicle industry.

-

Concentrated latex manufacturers: There is an opportunity for growth following the demand trends of downstream industries, specifically rubber gloves, medical rubber products, and general consumer goods, which are gradually recovering alongside the manufacturing sectors of key trading partners, such as Malaysia, India, the United States, and Europe.

However, midstream rubber manufacturers may face sustained high costs, particularly for chemicals and synthetic rubber used as production ingredients, following oil price trends amidst geopolitical tensions that continue to emerge periodically. Furthermore, China's expansion of investments in competing ASEAN countries to increase both upstream and midstream rubber production remains a constraint on the future export growth of Thai rubber products

Overview

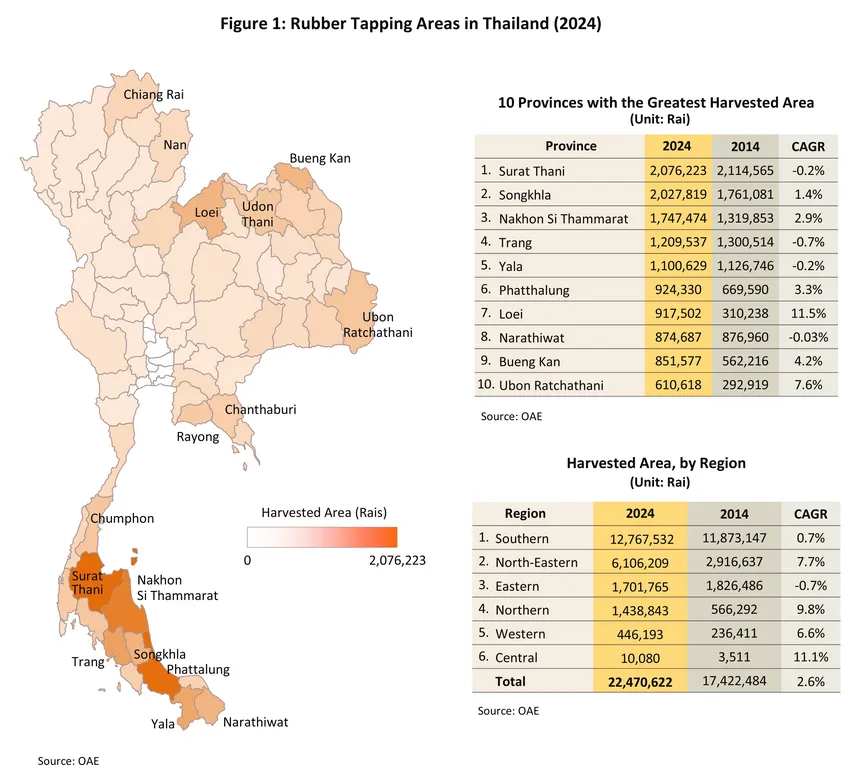

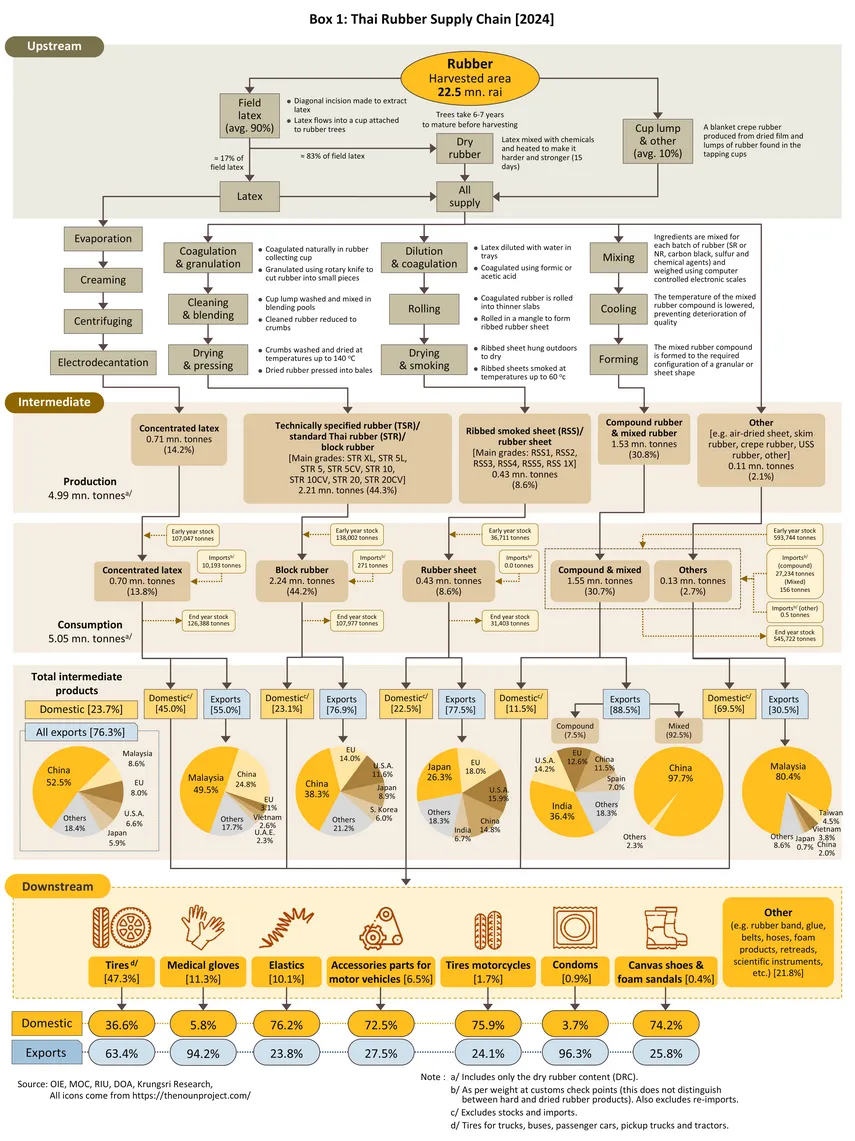

Regarding the Thai rubber industry1/, in 2024, Thailand possessed a total rubber planting area of 23.8 million rai, with approximately 22.5 million rai available for harvest. The majority of these areas are located in the Southern region (56.8% of Thailand's total rubber planting area), followed by the Northeast (27.2%), the East (7.6%), the North (6.4%), the West (1.9%), and the Central region (0.1%) (Figure 1). The production volume of midstream rubber stood at approximately 5.0 million tonnes of dry rubber content. Most of Thailand's midstream rubber output is exported for the manufacturing of downstream rubber products abroad, with exports accounting for 76.3% of total midstream rubber products as of 2024. Thailand's primary export market is China, representing 52.5% of the total export volume of Thai midstream rubber products, followed by Malaysia (8.6%), the European Union (8.0%), the United States (6.6%), and Japan (5.9%). The remaining midstream rubber output (23.7%) is utilized as raw material for domestic downstream rubber product manufacturing, primarily within the tire industry, which accounts for 47.3% of the total domestic demand for midstream rubber products. Other significant applications include medical rubber gloves (11.3%), elastic thread (10.1%), and various other products such as automotive spare parts, motorcycle tires, condoms, rubber hoses, and rubber bands (Box 1).

In 2024, Thailand's intermediate rubber industry had a market value (including exports and domestic consumption) of approximately THB 374.7bn.2/ Thailand is capable of producing a wide range of intermediate rubber products, comprising technically specified rubber (TSR), rubber sheets, concentrated latex, compound rubber, mixtures, and others. When considering individual products, it was found that TSR is the intermediate rubber product for which Thailand has the highest production volume, accounting for a proportion of approximately 44.2% of Thailand's total intermediate rubber product production volume, followed by compound rubber and mixtures (30.7%), concentrated latex (13.8%), rubber sheets (8.6%), and other types of rubber (2.7%) (Box 1), with each product having the following market values:

-

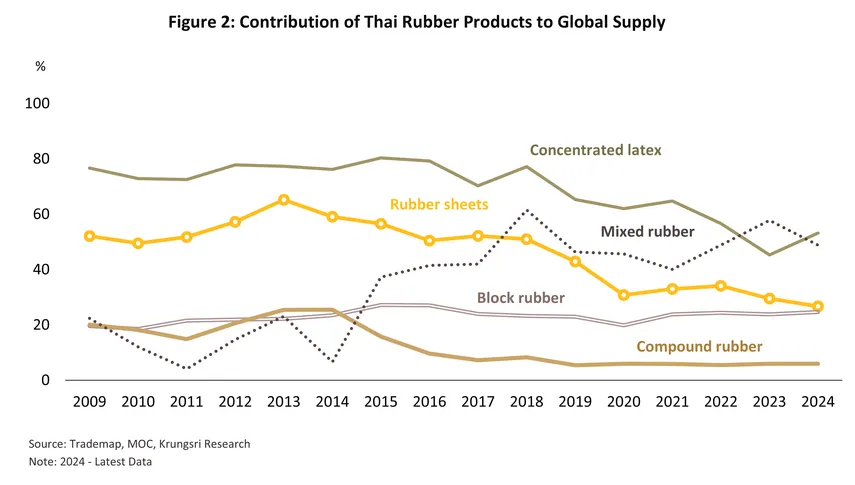

Thailand’s ribbed smoked sheet (RSS) industry had a market value (including exports and domestic consumption) of approximately THB 36.2bn in 2024. Furthermore, Thailand maintained the world’s number one market share, accounting for 26.7% of the global RSS export volume (Figure 2). Thailand exported approximately 77.5% of Thailand’s total RSS sales volume, with major export markets consisting of Japan, at a proportion of 26.3% of Thailand’s total RSS export volume, followed by the European Union (18.0%), the US (15.9%), China (14.8%), and India (6.7%) (Box 1). The remaining 22.5% represented domestic sales of ribbed smoked sheets for internal use.

-

Thailand’s technically specified rubber (TSR) industry had a market value of approximately THB 145.8bn in 2024, characterized by a high export concentration at 76.9% of Thailand’s total TSR sales volume. The primary export markets are China, accounting for 38.3% of Thailand’s TSR export volume, followed by the European Union (14.0%), the US (11.6%), Japan (8.9%), and South Korea (6.0%). Thailand holds the world’s second-largest market share at 24.7% of the global TSR export volume (Figure 2). The remaining 23.1% consists almost entirely of domestic sales, the majority of which is utilized within the tire industry (Box 1).

-

Thailand’s concentrated latex industry had a market value of approximately THB 48.4bn in 2024, with a focus on exports accounting for 55.0% of Thailand’s total concentrated latex sales volume. Thailand holds the world’s highest market share at approximately 53.2% of the global concentrated latex trade volume (Figure 2). The primary export markets are Malaysia, representing a significant proportion of 49.5% of the Thailand’s total concentrated latex export volume, and China (24.8%) (Box 1). The demand for concentrated latex in the downstream industries of these export markets primarily stems from the rubber glove and condom industries, while domestic consumption in Thailand is mostly directed toward the production of medical products and rubber gloves.

-

Other significant rubber industries include compound rubber and mixed rubber (mixture rubber). Thailand's compound rubber and mixed rubber industries had a market value of approximately THB 144.3bn in 2024, with the export market accounting for 88.5% of Thailand's total compound rubber and mixed rubber sales volume. The export markets can be categorized as follows:

-

Compound rubber: Thailand's global market share ranked 5th, following Germany, the US, Italy, and Canada, respectively, with Thailand's export volume accounting for an average of 5.7% of the global market in 2024 (Figure 2). India serves as the primary export market, representing a proportion of approximately 36.4% of Thailand’s total compound rubber export volume, followed by the US (14.2%) and the European Union (12.6%) (Box 1).

-

Mixed rubber: Thailand holds the world’s number one market share in export volume at 48.8% in 2024 (Figure 2), followed by Vietnam (24.5%) and Malaysia (15.4%), respectively. China is the world’s primary import market, accounting for a proportion of over 98.5%, and also serves as nearly the entirety of Thailand’s export market, representing approximately 97.7% of Thailand’s total mixed rubber export volume. However, the Chinese market imports mixed rubber from Thailand for only 41.1% of China’s total mixed rubber demand, with the remainder imported from Vietnam (35.2%) and Malaysia (13.6%).

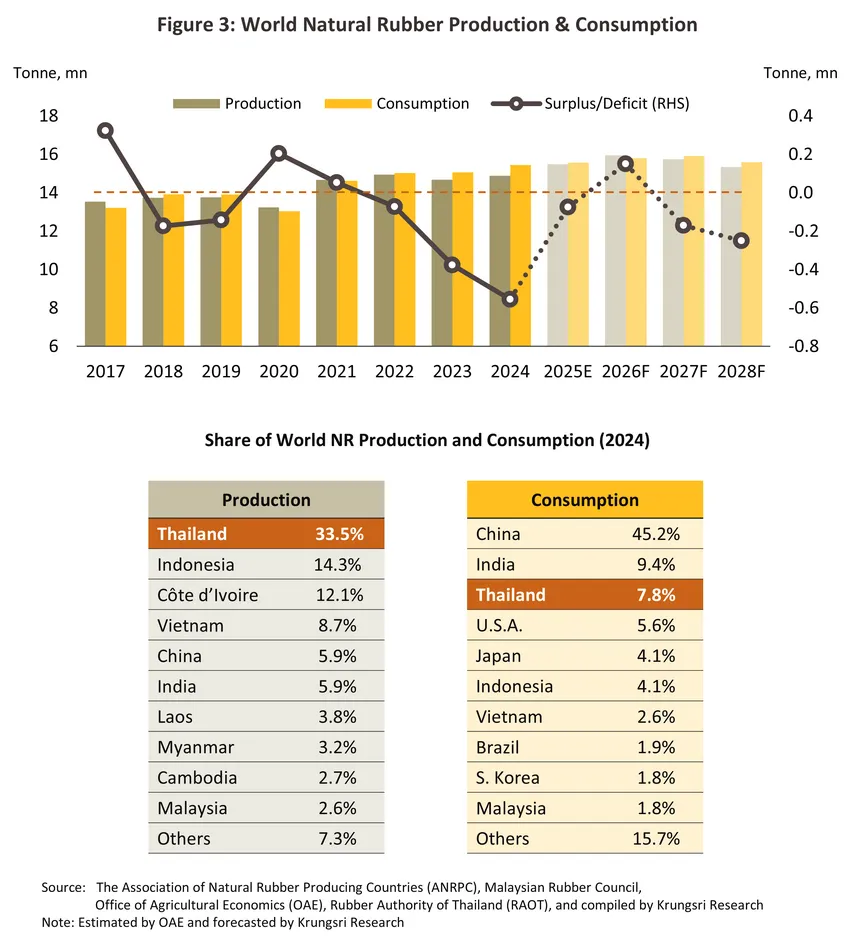

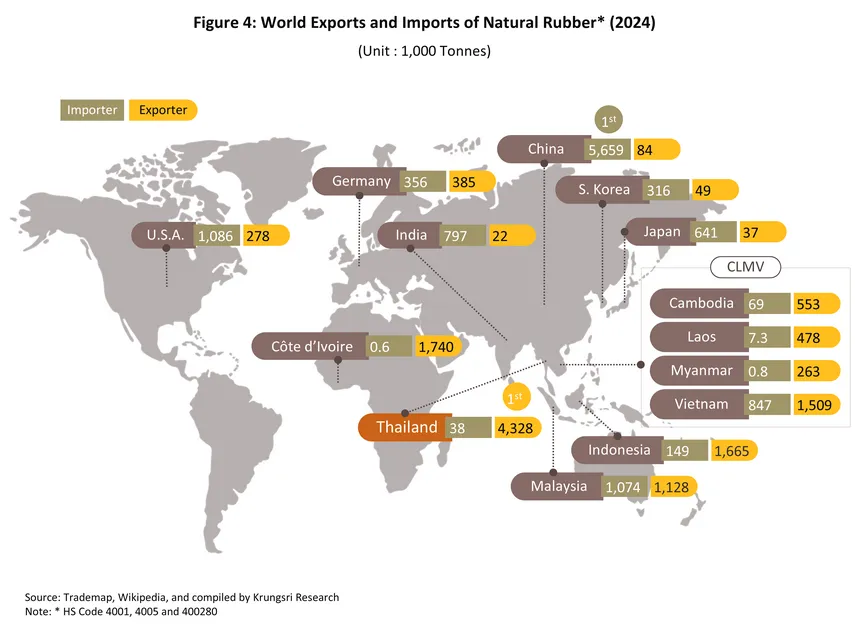

In 2024, global natural rubber production totaled 14.9 million tonnes, with Thailand ranking as the world’s number one producer, accounting for a proportion of approximately 33.5% of global output. This was followed by Indonesia, Côte d'Ivoire, Vietnam, China, and India, respectively, reflecting that the Asian region is the world's primary rubber production source (accounting for more than 82.0% of global rubber production). Thailand’s main competitors are therefore fellow ASEAN nations, particularly Indonesia, Malaysia, and the CLMV group (Cambodia, Laos, Myanmar, Vietnam) (Figure 3), which possess high levels of surplus rubber production and export similarly to Thailand. Nevertheless, Thailand currently maintains its status as a major global exporter of intermediate rubber products, including ribbed smoked sheets (RSS), technically specified rubber (TSR), concentrated latex, and mixed rubber, for which Thailand’s export volume ranks first in the world.

Regarding global intermediate rubber product consumption in 2024, the volume stood at 15.4 million tonnes, with the majority of rubber demand concentrated in the automotive and parts industries, followed by the medical rubber products and rubber gloves sector for disease prevention and general hygiene, and the general construction and infrastructure development sector. China remains both the world's largest rubber consumer and importer, accounting for high proportions of 45.2% and 41.2% of global consumption and import volumes, respectively, followed by India, Thailand, the US, Japan, Indonesia, and Vietnam (Figures 3 and 4). Consequently, Thailand's rubber product export markets are highly concentrated among major consuming nations. In 2024, Thailand relied on the Chinese market for 52.5% of Thailand’s total intermediate rubber product export volume, followed by the US at 6.6% and Malaysia at 5.9%. This concentration subjects the rubber industry to high risks from economic volatility within these primary export markets.

Situation

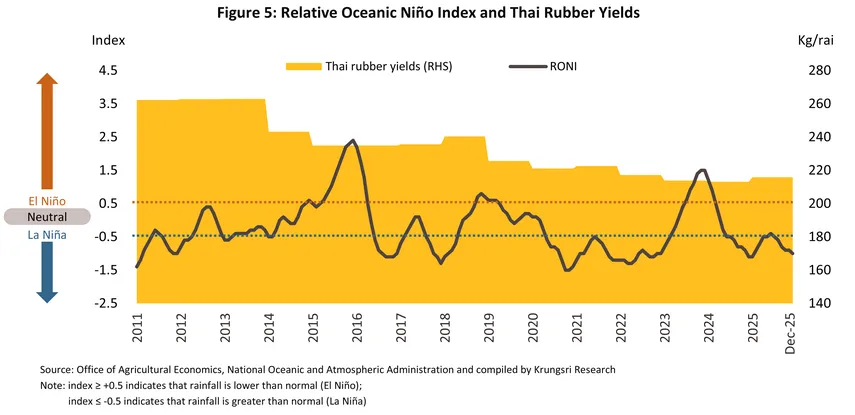

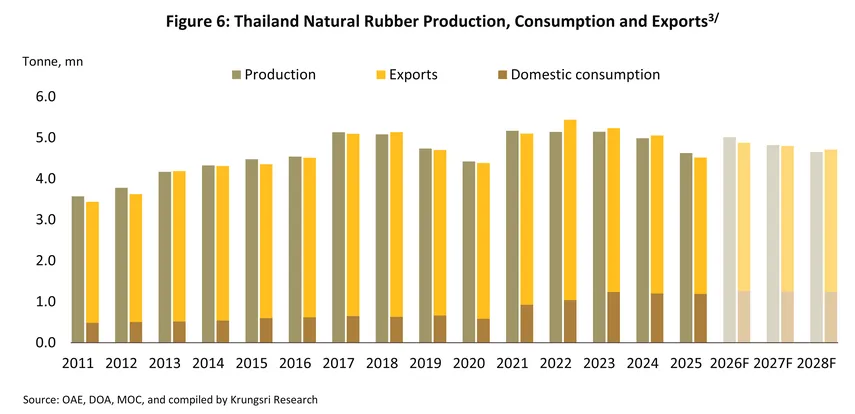

In 2025, Thailand's total harvested rubber area reached 22.4 million rai, a slight increase of 0.2%, following the acceleration of planting area expansion in 2019. The majority of the harvested area is located in the Southern region, accounting for approximately 57.0% of the country's total rubber planting area; however, this proportion has continuously declined from a high of 68.0% a decade ago due to increased planting in the Northeast (which rose to 27.0% of the total planting area from 17.0% in 2015). Upstream rubber production for 2025 is estimated at 4.9 million tonnes, an increase of 1.1%, resulting from 1) the return to normal climatic conditions and the La Niña phenomenon, which supported a yield per rai increase of approximately 1.2% (Figure 5), and 2) more efficient management of Circular Leaf Fall Disease by the majority of Thai farmers, allowing for higher tapping yields in many areas. Nevertheless, despite the increase in raw rubber production, the volume of processing into intermediate rubber in 2025 decreased to 4.6 million tonnes3/, contracting at -7.2%. This was due to softened demand from domestic downstream industries3/, coupled with an increased substitution of synthetic rubber for natural rubber in certain export products3/ following the downward trend in crude oil prices (Dubai crude oil prices decreased by an average of -14.2% in 2025) (Figure 6).

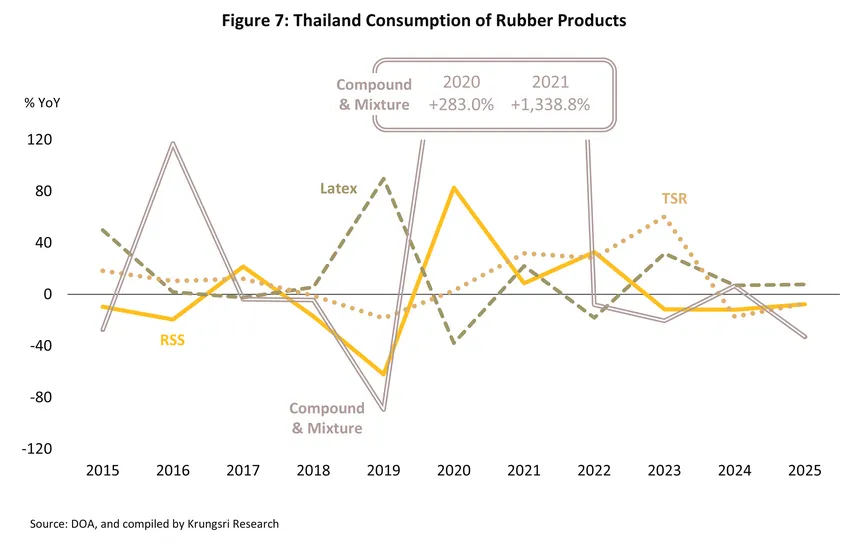

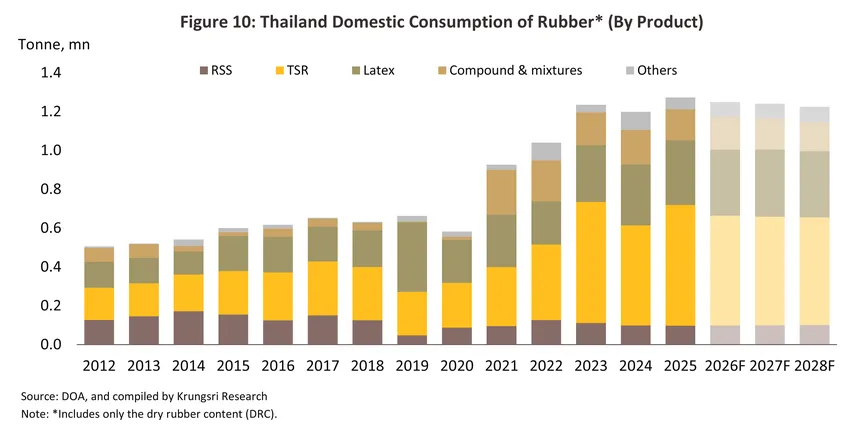

Domestic demand for intermediate rubber products contracted by -0.8% to 1.2 million tonnes3/ in 2025 (Figure 6). This was primarily driven by declining demand for RSS at 90.4 thousand tonnes (-7.6%), TSR at 479.3 thousand tonnes (-7.1%), and the compound and mixed rubber group, where combined demand fell to 120.0 thousand tonnes (-33.0%). This occurred despite growth in certain products, namely concentrated latex at 337.1 thousand tonnes (+7.7%) and other rubber types at 162.0 thousand tonnes (+74.3%) (Figure 7).The main drag resulted from severe contractions in other rubber product industries4/ (-37.8%), footwear (-21.3%), elastic thread5/ (-18.5%), and conveyor belts (-10.8%), with combined volume decreasing by 120.0 thousand tonnes from 2024. This aligns with the 2025 situation where the luxury goods manufacturing and textile sectors faced slowing global purchasing power alongside continuously rising production costs, leading to partial substitution with synthetic rubber for cost management. Although tire demand benefited from electric vehicle (EV) growth, the replacement tire market, and essential vehicle maintenance—such as vehicle tires (+2.7%), motorcycle tires (+7.5%), automotive spare parts (+19.7%), and retreaded tires (+51.8%)—this positive momentum was insufficient to offset the sharp contraction in traditional product groups sensitive to the economic slowdown.

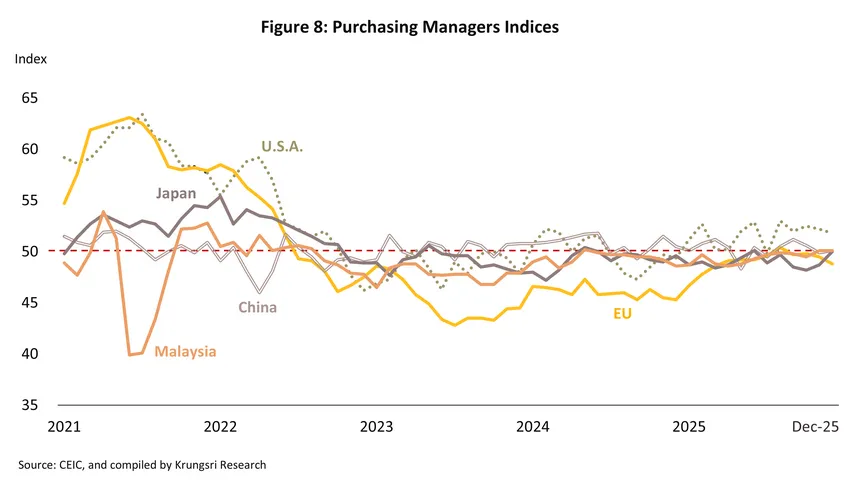

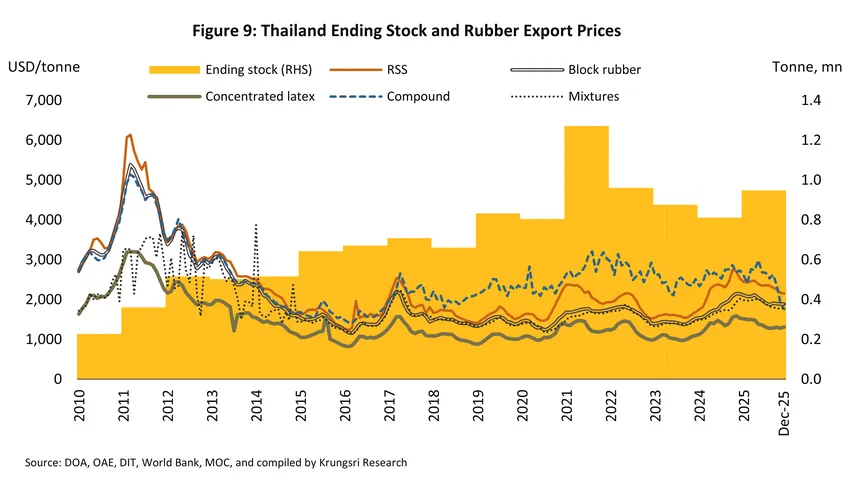

The movement of rubber prices was influenced by favorable weather conditions in Thailand during 2025, which led to higher yields per rai, supported the expansion of upstream rubber production, and pressured the average price of unsmoked Grade 3 raw rubber sheets (farm-gate price) in Thailand to contract by -13.7% to THB 60.3/kg. Similarly, export prices for concentrated latex and compound rubber decreased to averages of USD 1,377/tonne (-1.5%) and USD 2,503/tonne (-5.3%), respectively, due to intense price competition and demand from downstream industrial sectors being impacted by global economic uncertainty and manufacturing volatility. This is reflected by the manufacturing Purchasing Managers' Index (PMI) of key trading partners remaining below the 50.0 level (Figure 8). However, export prices for certain rubber product groups showed an upward trend, including mixed rubber at USD 1,900/tonne (+11.8%), TSR at USD 1,982/tonne (+7.9%), and RSS at USD 2,346/tonne (+1.7%) (Figure 9 and Table 1). Key supporting factors included 1) rising global rubber demand, particularly from the Chinese market as a major importer for the automotive and parts industries, and 2) supply-side issues, specifically disease outbreaks and droughts in some major competing countries (Indonesia and Malaysia) that have not yet returned to normal levels, resulting in limited rubber volume in the global market.

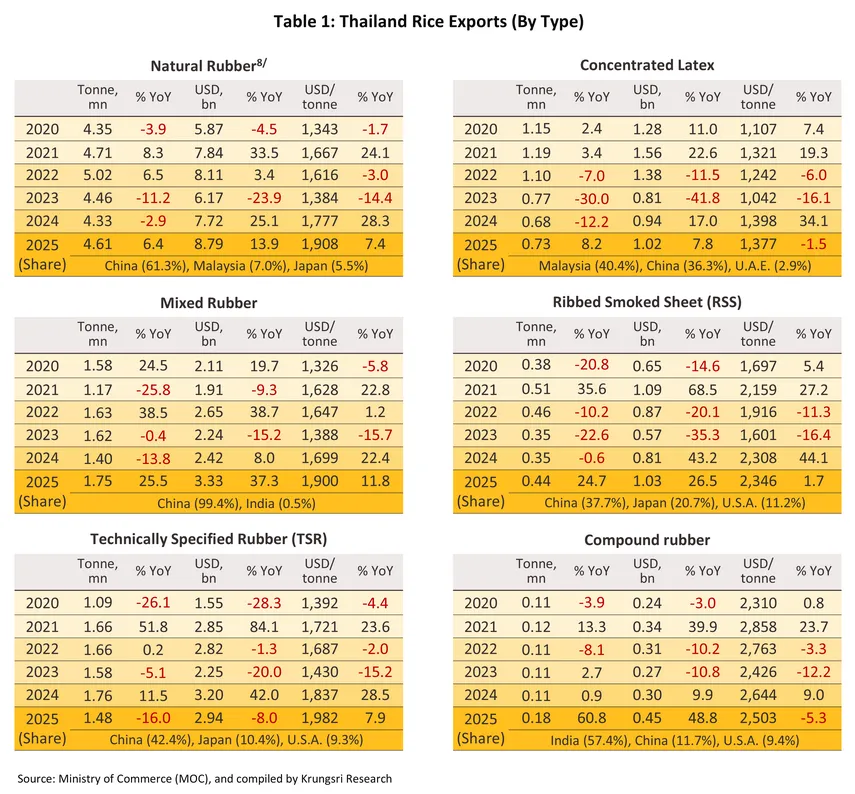

Thailand’s intermediate rubber export volume expanded by 6.4% to 4.6 million tonnes6/, valued at USD 8.8bn (+13.9%) in 2025. China remained the primary market, accounting for a proportion of 61.3% of Thailand’s total intermediate rubber export volume, followed by Malaysia (7.0%), Japan (5.5%), the US (4.6%), and India (4.0%), respectively (Table 1). The export volume expansion was primarily driven by mixed rubber products at 1.75 million tonnes (+25.5%), followed by concentrated latex at 0.73 million tonnes (+8.2%), RSS at 0.44 million tonnes (+24.7%), and compound rubber at 0.18 million tonnes (+60.8%). Products experiencing a contraction in export volume included TSR at 1.48 million tonnes (-16.0%) and crepe rubber and other types at 0.02 million tonnes (-32.6%). Overall, the export market expanded primarily due to China (+24.3%), totaling 2.8 million tonnes across rubber sheets (+217.0%), concentrated latex (+58.1%), compound rubber (+63.7%), and mixed rubber (+27.8%). This growth was supported by 1) the Rubber Authority of Thailand successfully negotiating with the Chinese government to exempt import duties on Thai natural rubber7/ exported via the Mekong River route to 0.0%; 2) tire demand from the electric vehicle (EV) manufacturing industry in China to serve both the original equipment manufacturer (OEM) and replacement markets; 3) the Chinese government’s economic stimulus measures in early 2025, which led the industrial sector to accelerate rubber restocking to support the recovery of China’s manufacturing and rubber product exports to new markets, such as the Middle East and Africa; 4) Concerns over European Union Deforestation Regulation (EUDR) enforcement led China to increase Thai imports, trusting Thailand's traceability systems for downstream production targeting European markets; and 5) Supply shortages persist in Indonesia and Malaysia due to leaf disease and aging trees, while Thai supply remains sufficient to meet Chinese importer demand.

Outlook

During the 2026-2028 period, Thailand’s rubber industry is projected to experience a gradual expansion in production, domestic sales volume, and exports, driven by the following factors:

-

Thailand's intermediate rubber production growth is projected to remain relatively flat at an average rate of -0.3% to +0.7% per year9/. In 2026, rubber production is likely to expand by an average of 7.9-8.9%, supported by 1) favorable weather conditions and temperatures in Thailand resulting from the La Niña phenomenon, which is expected to transition toward neutral conditions10/ during the first three quarters of the year, leading to higher yields per rai with upstream rubber production forecasted to increase by an average of 1.0-2.0%; 2) the expansion of planting areas during 2003-201311/, which are currently at an age that provides high latex yields per rai12/; and 3) incentives for farmers to maintain rubber trees to increase output and accelerate harvesting based on attractive rubber price trends following rising demand, particularly for tires. However, during 2027-2028, production is expected to decline at an average of -3.2% to -4.2% per year. This drag results from 1) hot weather conditions and reduced rainfall as the return of the El Niño phenomenon impacts outputs, and 2) the risk of both existing and emerging strains of rubber leaf fall disease13/, prompting some farmers to switch to other economic crops or livestock (such as durian, oil palm, or beef cattle).

-

Domestic sales volume is projected to expand by 0.8-1.8% per year (Figure 10). This growth is supported by 1) demand from downstream industries, particularly the automotive, tire, and electric vehicle (EV) parts sectors, benefiting from the EV 3.5 measure which requires local production to offset previous imports within 2026-2027, as well as policies supporting HEV and MHEV production through excise tax reductions during 2026-2032; 2) demand in the construction sector, expected to gradually recover following public infrastructure developments such as double-track railways, the Eastern Economic Corridor (EEC), and a recovery in private construction including factories, commercial buildings in the EEC, major hotel chains, and the repair of structures affected by flooding in the South; and 3) ongoing and potentially intensified government measures to absorb supply and enhance policy effectiveness, such as the domestic rubber consumption promotion policy, the establishment of the Southern Economic Corridor of Rubber Innovation (SECri), the development of carbon credit management projects, the implementation of the Thai Rubber Reference Price, rubber auctioning via the "Thai Rubber Trade" (TRT) digital platform, and the execution of measures to comply with the EUDR regulations.

-

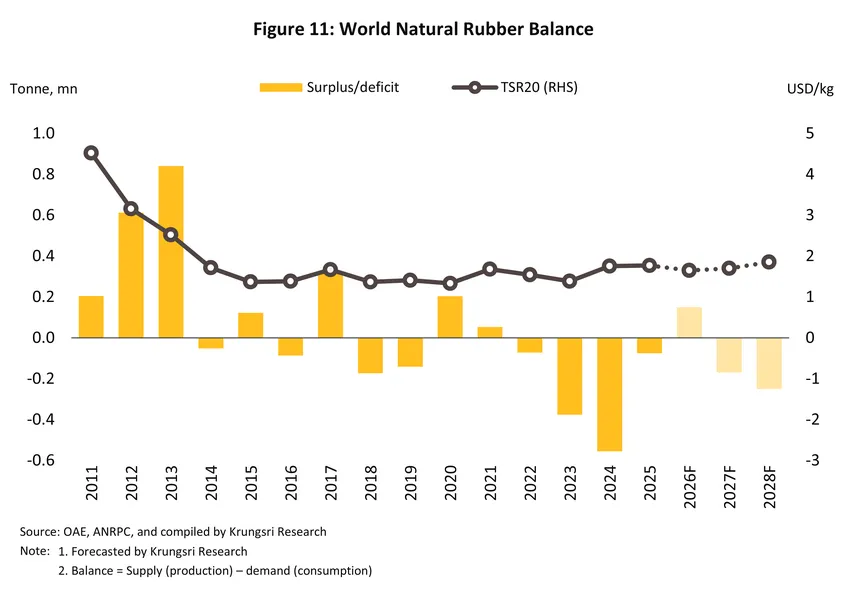

Global rubber prices are projected to increase by an average of 1.9-2.9% annually. In 2026, supply is expected to increase due to favorable weather conditions in 3Q/26, especially in Southeast Asia, the world’s major rubber‑growing region. At the same time, demand is climbing in the manufacturing sector. Tire production, in particular, is expanding as global electric‑vehicle output continues to grow. This will support higher demand for block rubber. Consequently, global block rubber prices are expected to range between USD 1.75-1.85/kg in 2026 (compared to USD 1.77/kg in 2026). For 2027-2028, the impact of droughts and rubber leaf fall disease in several countries, combined with expanding rubber demand to support global market needs, particularly within the automotive industry, will bolster global block rubber prices to continue rising to USD 1.85-1.95/kg (Figure 11).

-

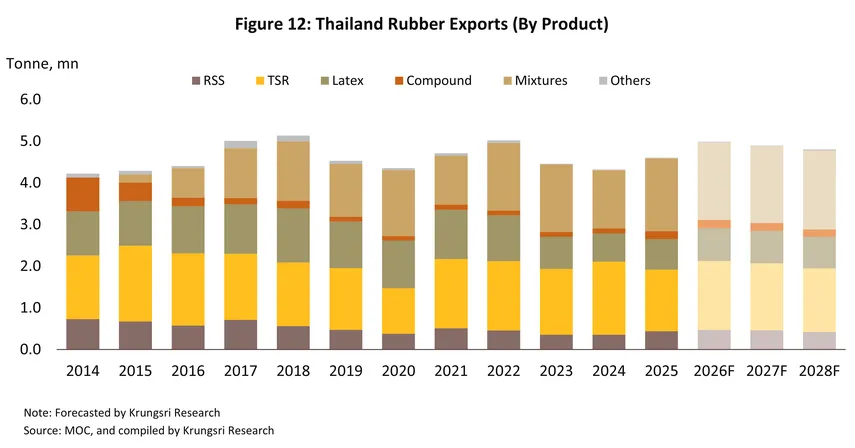

Export volumes for 2026-2028 are expected to expand by 1.0-2.0% annually, consistent with global demand for intermediate rubber which is projected to remain stable at an average of 0.1-1.1% per year. In 2026, export volumes are anticipated to grow by 8.3-9.3%, driven by key supporting factors including 1) restocking demand, particularly within the automotive, tire, and parts industries to ensure supply chain security and support future market recovery, the promotion of electric vehicle (EV) usage, urban expansion leading to increased travel, and stricter safety and environmental regulations in Europe and the US that accelerate the tire replacement rate; 2) demand for medical equipment, especially rubber gloves, medical rubber tools, and rubber products for hygiene, which is growing in line with healthcare megatrends and the transition toward an aging society; and 3) global supply still facing production issues in Indonesia and Malaysia due to the impact of rubber leaf fall disease, the shift toward other economic crops with more attractive returns and lower disease risks such as oil palm and durian, labor shortages, and increasingly volatile weather conditions, resulting in importers turning to Thailand to replace lost supply from other trading partners. For 2027-2028, Thai rubber export volumes are projected to contract by -1.5% to -2.5% annually due to 1) supply-side constraints, particularly the risk of weather volatility from El Niño which may return to reduce outputs and cause a supply shortage, and 2) importers in major markets potentially slowing orders to manage or discharge previously accumulated inventories (destocking). Regarding export trends categorized by product (Figure 12), the details are as follows:

-

RSS: Export volumes are projected to contract by -1.1% to -2.1% per year. Thai smoked rubber sheets remain recognized for their high standards and quality for use in manufacturing premium tires, specifically sidewalls and treads, as well as conveyor belts, rubber hoses, and automotive parts. However, due to the accelerated accumulation of high inventory levels during 2025-2026, smoked rubber sheet export volumes for 2027-2028 are expected to trend downward, compounded by Thailand's increasing loss of competitiveness and market share to neighboring countries (Cambodia, Lao PDR, Myanmar, and Vietnam).

-

TSR: Export volumes are projected to grow by 0.6-1.6% annually, following the recovery of downstream industries, particularly automotive, tires, and automotive parts, which represent key end-use sectors. Furthermore, the accelerating trend in electric vehicle production and adoption, especially in China as Thailand's primary trading partner, leads to expectations that the Chinese market will demand significantly higher quantities of block rubber for the production of electric vehicles, tires, and automotive components, as well as for the manufacturing of engineering parts in the construction sector, such as shock-absorbing rubber and bridge or railway bearing pads.

-

Concentrated latex: Export volumes are projected to expand by 0.8-1.8% annually, driven by growth in the medical industry, rubber gloves, various medical rubber products, and household goods (such as rubber mattresses, pillows, and elastic yarns) in trading partner countries. Supporting factors include population growth, more comprehensive medical services, the rise of various diseases, and the increasing use of hygiene products. Malaysia remains the primary market as the major importer of Thai concentrated latex and the world's leading rubber glove manufacturer. However, the business faces limited growth potential due to increasingly stringent trade barriers on downstream products in certain countries, particularly the United States, which has elevated restrictive measures into laws prohibiting the use of natural rubber gloves in the food service industry in some states and has begun enforcement in specific medical industry areas to avoid potential protein-coating allergies among consumers.

-

Compound rubber: Export volumes are projected to contract by -1.1% to -2.1% per year, resulting from the accelerated high inventory accumulation during 2025-2026 due to concerns over supply shortages and the upward trend of future prices. Furthermore, compounded rubber carries higher production costs and prices compared to other substitutable rubber types in downstream industries. This may cause importers in key trading partner countries, such as India, the US, China, and Europe, to delay orders while the manufacturing sector undergoes a gradual recovery, acting as a factor that continues to pressure the growth rate of foreign market demand.

-

Mixed rubber: Export volumes are projected to grow by 2.3-3.3% annually, following the expansion of demand in the automotive manufacturing and automotive parts industries, particularly vehicle tires. Furthermore, mixed rubber formulations can be customized as raw materials for a wide variety of other manufacturing industries, such as daily consumer goods, electronic equipment, and insulation for wires and cables. Consequently, demand for mixed rubber is expected to expand in line with the economic recovery of trading partner countries, especially China as the primary market.

Challenges facing the rubber industry include:

-

China increasingly turning to imports from the CLMV group after Chinese investors continuously expanded rubber cultivation in CLMV countries, with outputs now entering the market; this may lead to China, as Thailand’s major trading partner, reducing its demand for Thai rubber imports.

-

Tariff barriers, particularly the U.S. customs duty hike measures; although natural rubber is currently exempt and not included under Section 232 of U.S. trade law, continuous monitoring of tariff policy uncertainty is required, especially regarding the impact on downstream export products centered on the U.S. market, such as tires.

-

Non-tariff import barriers, specifically the enforcement of environmental standards that must comply with the laws of importing countries, such as EUDR14/ and CSDDD15/; operators should increasingly adapt to handle these restrictive policies, particularly by upgrading product standards throughout the production chain to align with both Thai and trading partner standards. Besides reducing trade barriers, this will assist operators in accessing markets and securing capital from financial institutions that support green economies, ESG, or SDGs16/.

-

Supply shortage issues arising from both natural risk factors and industrial adjustments, such as volatile weather, outbreaks of both existing and new strains of rubber leaf fall disease, and a shortage of rubber tapping and factory labor due to geopolitical issues with Cambodia; furthermore, farmers switching to other crops has resulted in a decline in rubber output.

-

Escalating and persistent geopolitical tensions—particularly the intensifying U.S.–Israel–Iran conflict in 2026—could pose multidimensional risks to Thailand’s processed rubber industry. These include: 1) Rising volatility in global oil prices, likely trending upward, which may lead to: 1.1) Weaker demand, as downstream manufacturers may delay purchases while monitoring the situation; and 1.2) Greater pressure on profit management, due to higher and more volatile production costs (e.g., fertilizers, chemicals17/, and energy), which are embedded in transportation costs and chemical inputs used in processing. 2) Logistics disruptions and shipping route risks from the potential closure of the Strait of Hormuz, causing export delays for shipments to Middle Eastern markets. Although the Middle East is a relatively small market for Thai rubber compared with China and Malaysia, disruptions could still affect the liquidity of exporters that rely heavily on this market (in 2025, exports of Thai rubber products to Middle Eastern countries and Iran accounted for 1.8% and 0.2% of total export volume, respectively). 3) Payment and financial transaction risks for exporters dealing directly with Iranian counterparties.

1/ The Thai rubber industry consists of 1) the Upstream rubber industry, which refers to rubber farmers who cultivate natural rubber (NR), tap fresh latex, and in some cases, perform primary processing into dry rubber forms (such as cup lump, rubber scrap, unsmoked rubber sheet, and crepe rubber), where almost all of Thailand's upstream rubber output is used as raw material for the domestic intermediate rubber industry; 2) the Intermediate rubber industry, or processed rubber industry, which involves taking upstream rubber products from farmers and processing them into intermediate rubber products, such as ribbed smoked sheets (RSS), technically specified rubber (TSR), concentrated latex, compound rubber, and mixtures with characteristics and properties suitable as raw materials for downstream rubber product manufacturing; and 3) the Downstream rubber industry, or rubber product industry, such as tires, rubber gloves, condoms, and elastic thread, in which certain types of downstream rubber production may utilize synthetic rubber (SR), a petrochemical product, as a co-raw material to achieve properties appropriate for manufacturing each specific type of downstream rubber product.

2/ This comprises rubber sheets, technically specified rubber (TSR), concentrated latex, compound rubber, and mixtures, as assessed by the export value of natural rubber and the value of natural rubber consumed domestically.

3/ Calculated based on dry rubber content (DRC) only, excluding water and other chemical mixtures.

4/ Other products cover industrial rubber products, machine parts, and general consumer goods, which are categories characterized by high demand elasticity. When the global economy slows down, the manufacturing sector and purchasing power within the luxury and non-essential goods segments are the first to experience a decline.

5/ Elastic thread is primarily utilized within the apparel and textile industries.

6/ The rubber product weight measured at customs checkpoints, when calculated specifically for dry rubber content (DRC), totals 3.3 million tonnes. This is based on an average DRC for concentrated latex of 60.0%, while the average DRC for compound rubber and mixed rubber ranges between 80.0-95.0%.

7/The export of HS Codes 4001 and 4002 via the Mekong River route decreased from 20.0% to 0.0%, which enhanced Thailand's competitiveness to a level comparable with the CLMV group.

8/The HS Codes consist of 4001, 4005, and 400280.

9/Assuming no permanent felling of rubber trees and a lack of cooperation in supply reduction among major Asian rubber-producing nations.

10/ According to the National Oceanic and Atmospheric Administration (NOAA), the most recent El Niño occurred during 2023-2024, resulting in a relatively high probability of La Niña during 2025-2026. Krungsri Research expects this condition to persist for 1-2 years, after which weather conditions are likely to return to neutral, with a projected transition back to El Niño in 2027-2028.

11/ This is a result of government schemes that ran over 2003-2013 that had the goal of expanding the total area of rubber plantations by 1 million rai.

12/ Generally, rubber trees begin to provide high and consistent latex yields when they reach 10-20 years of age.

13/ Having first emerged in Thailand in 2019 and persisting through 2023, outbreaks of rubber leaf fall disease involve both existing and emerging strains and can be found across all cultivated rubber varieties. The disease is difficult to control and eradicate, with current strains identified as either Pestalotiopsis sp. or Colletotrichum sp. fungi. Transmission occurs via wind and rain, as well as through the movement of saplings or planting materials from infected plots. This results in stunted tree growth and leads to a significant reduction in production volume of approximately 30.0-50.0%.

14/ Thailand is currently categorized within the low-risk group of countries. Regarding enforcement, the implementation date has been rescheduled to December 30, 2026, while for small and medium-sized enterprises (SMEs), enforcement is expected to commence around June 2027.

15/ The European Union Corporate Sustainability Due Diligence Directive (CSDDD) will begin enforcement for large companies (with more than 5,000 employees and global revenue exceeding EUR 1,500mn) starting July 26, 2027, with full implementation expected by July 26, 2029.

16/ Adaptation guidelines following ESG and SDG trends in the Thai rubber industry include the Environmental pillar, where operators focus on

eco-friendly production by utilizing energy and water efficiently, maintaining standard wastewater treatment and odor filtration systems, and implementing waste segregation across the entire supply chain while restoring nature through reforestation and green space creation. Regarding the Social pillar, operators enhance quality of life and safety standards by complying with occupational health laws, emphasizing community engagement through local employment, supporting education, and providing disaster relief assistance. For the Governance pillar, operators establish policies rooted in procurement transparency and information disclosure, ensuring equal treatment of labor, fostering strong customer relationships, and instituting anti-corruption regulations in all forms within the organization.

17/ The rising prices of chemicals used in processing raw rubber and smoked rubber sheets have impacted farmers' costs, leading some to reduce fertilizer application for rubber trees. Consequently, the dry rubber content (DRC) of fresh latex has declined from 30-35% and may drop to 25-29%.

.webp.aspx)