EXECUTIVE SUMMARY

The palm oil industry during 2026-2028 is expected to face supply volatility. In 2026, oil palm production is expanding due to favorable rainfall under the influence of La Niña during 1H/26, coupled with past plantation areas beginning to reach high-yield maturity. Subsequently, production is projected to contract during 2027-2028 following the return of the El Niño phenomenon and the onset of drought conditions. Regarding domestic demand, 2026 is set to see an acceleration driven by the biodiesel industry, which is increasing biodiesel blending proportions to mitigate the impact of oil prices amidst conflicts in the Middle East. Meanwhile, the refined palm oil industry will continue to expand at a low rate due to a slowdown in orders from downstream sectors amidst weak purchasing power. During 2027-2028, demand from the food and oleochemical industries is likely to gradually recover in line with economic activities and the tourism business, though tight supply will continue to limit growth. For exports over the three-year period, a contraction is anticipated due to government policies controlling exports to reserve crude palm oil for domestic demand during periods of supply tightness resulting from the Middle East war in 2026 and the 2027-2028 drought. This situation is expected to lead to a continuous decline in crude palm oil stock levels, supporting fresh fruit bunch and palm oil prices throughout 2026-2028 to remain higher than the average price level in 2025.

Krungsri Research view

Overall performance of the palm oil industry during 2026-2028 is expected to encounter volatility due to risks from climate variability leading to tight supply and Middle East conflicts impacting demand through a slowdown in orders from downstream industries. However, domestic demand will be supported by the biodiesel sector to accommodate government policies for balancing domestic oil management, alongside the recovery of the food and oleochemical industries in line with the gradual rebound of economic activities and the tourism business. While exporters may face risks from insufficient output, the upward trend in fresh fruit bunch prices may provide some support to the profitability of businesses within the supply chain. Competition for fresh palm raw materials among extraction mills is anticipated to intensify, causing the trend of excess production capacity to remain sustained at a high level.

-

Palm growers: Revenue is expected to fluctuate; although production is set to expand in 2026 due to favorable weather, production in 2027-2028 is trending toward a contraction from anticipated severe El Niño conditions, coupled with pressure from fertilizer shortages and costs expected to remain high due to the prolonged Middle East conflict, leading to a decline in yield per rai that may impact revenue despite the mitigating effect of rising palm prices.

-

Crude palm oil mills: Operating performance is projected to gradually grow, supported by selling prices influenced by the Middle East war situation and recovering domestic markets, the expansion of commercial transport, and government biodiesel support measures, as well as the gradual recovery of the tourism sector during 2027-2028. However, total production capacity of most extraction mills has historically exceeded the volume of fresh palm fruit entering the market. This results in competition for raw materials which impacts production costs and pressures profitability, particularly for small-scale crude palm oil mills lacking integrated networks with refineries or downstream industries such as refined palm oil, biodiesel, oleochemical products1/, or production by-products like refined glycerin2/, Phase Change Material (PCM)3/, and fatty alcohols4/.

-

Palm oil refiners: Business performance continues to trend toward a gradual recovery driven by the demand for crude palm oil to be refined into refined palm oil for the food industry, which is expected to recover in line with the tourism, hotel, and restaurant sectors, including the oleochemical industry where demand for crude palm oil and palm fats (derived from the refining process) is expected to increase following consumption recovery in downstream industries such as detergents, soap, pharmaceuticals, and cosmetics.

-

Traders in crops used in the production of vegetable oil (oil palm collection yards): Revenue is likely to expand following the volume of fresh palm fruit which will continue to increase in 2026 due to favorable weather conditions, while in 2027-2028, despite a downward trend in production from the returning El Niño. Support will come from higher prices due to the Middle East war and energy insecurity, combined with the high bargaining power of collection yard operators over palm oil farmers, most of whom are smallholders reliant on selling through these yards.

Overview

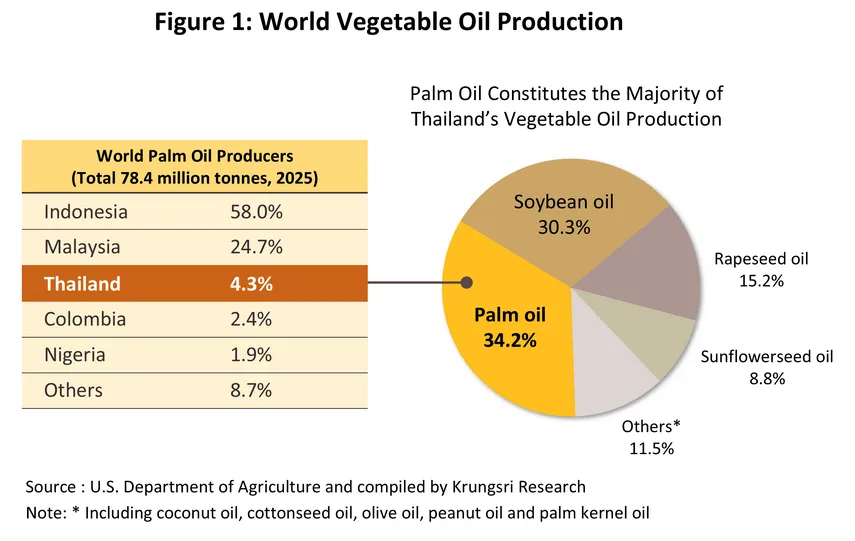

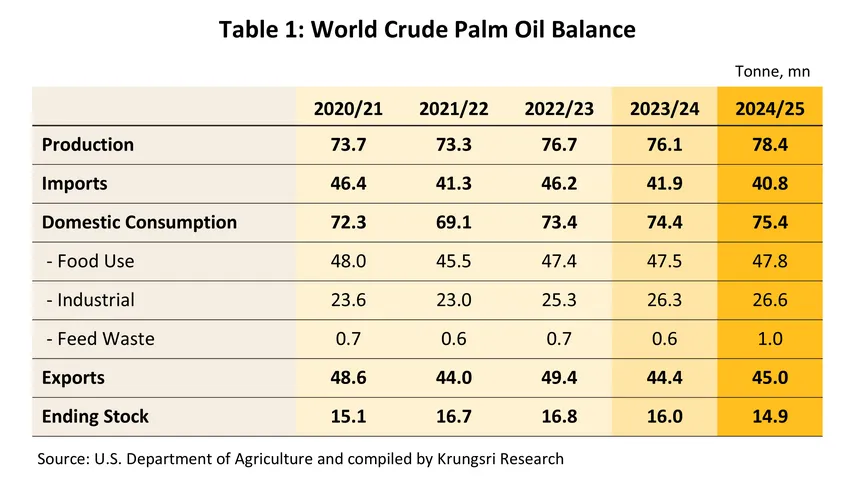

Palm oil5/ is a vegetable oil with a lower production cost than other types of vegetable oils such as soybean oil, rapeseed oil, sunflower seed oil, coconut oil, and olive oil, partly because the oil yield per rai of fresh palm fruit is 5-10 times6/ higher than other oil-bearing plants. In 2025, global palm oil production and consumption volumes reached 78.4 million tonnes and 75.4 million tonnes, accounting for 38.2% and 37.7% of the total production and consumption volume of all vegetable oils, respectively. Key palm oil production sources are located in the ASEAN region, where Indonesia and Malaysia serve as major producers and exporters that play a role in determining global market prices, producing 45.5 million tonnes and 19.4 million tonnes of crude palm oil, respectively. Together, they account for 82.8% of global production and 86.9% of the total crude palm oil export volume in the global market. Major crude palm oil importing countries include India (representing 19.1% of the total global import volume), Pakistan (8.1% ), China (7.9% ), and the European Union (7.7% ). Over the past five years (2021-2025), global production and demand for crude palm oil (for consumption and fuel production) increased at the same rate of 1.3% per year, while accumulated crude palm oil stocks at the end of 2025 decreased to 14.9 million tonnes from 16.0 million tonnes at the end of 2024 (Figure 1 and Table 1).

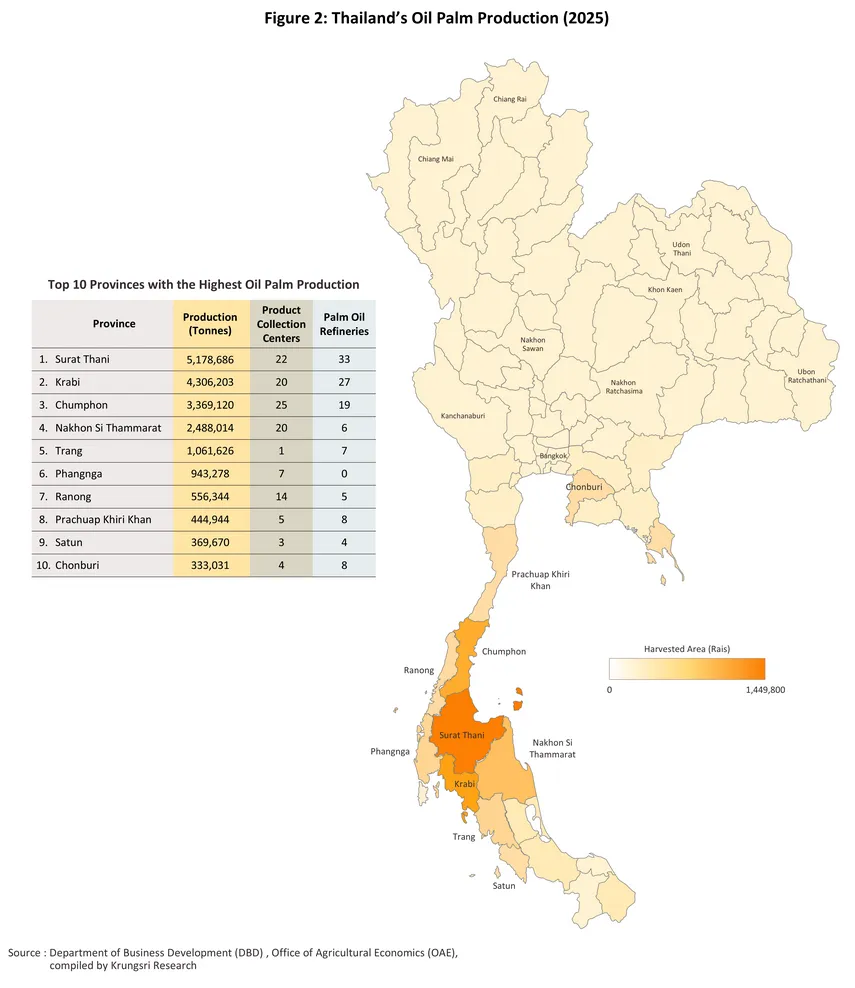

In 2025, although Thailand ranked as the third-largest producer of palm oil in the world, it accounted for a minor share of only 4.3% of global palm oil production, thereby playing no role in determining price directions. The harvested area ready for output was 6.4 million rai (+1.9%), yielding 21.1 million tonnes (+13.9%) of oil palm fruit7/, which allowed for the extraction of approximately 3.9 million tonnes (+17.7%) of crude palm oil. The majority of Thailand's oil palm cultivation areas and crude palm oil extraction mills are situated in the Southern region8/, accounting for 86.2% of the nation's total harvested area, particularly in Surat Thani, Krabi, and Chumphon provinces (with a combined share of nearly 56.8%), with the rest distributed across the Central, Northeastern, and Northern regions, respectively (Figure 2).

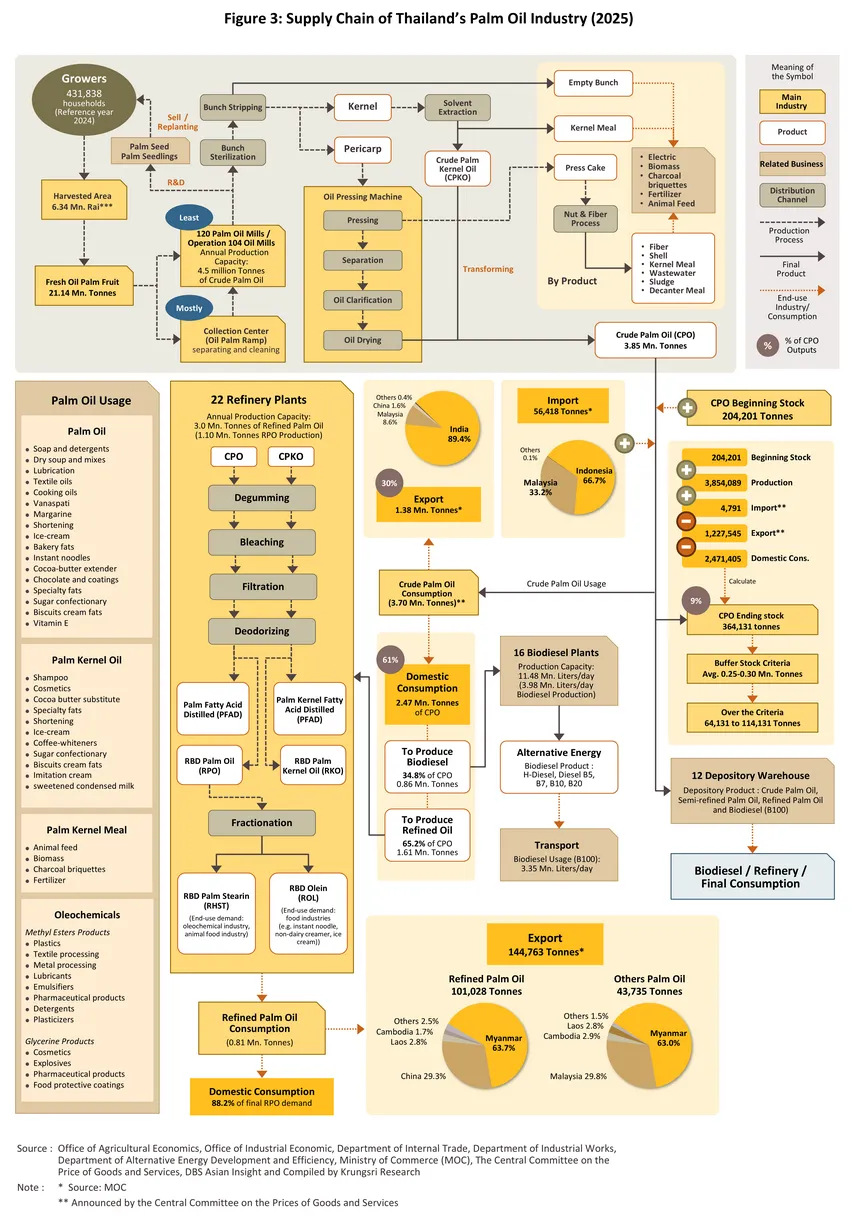

In 2025, the majority of crude palm oil production was utilized for domestic consumption, accounting for approximately 61% of total output (Figure 3),

-

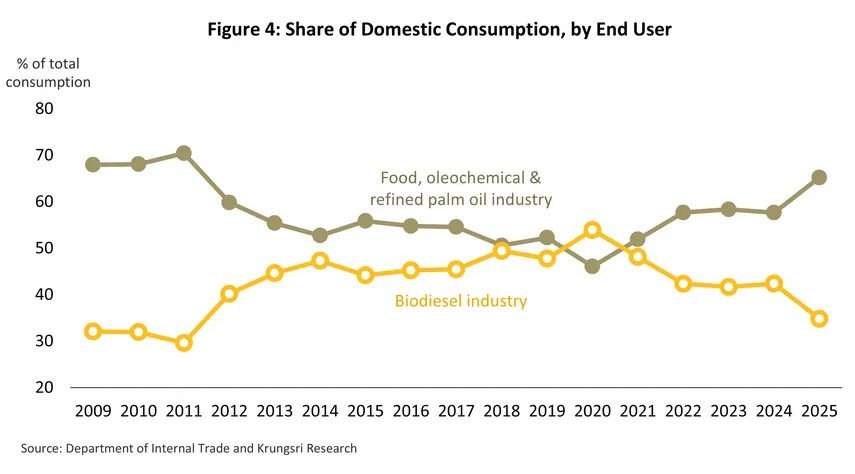

Crude palm oil was refined into refined palm oil (representing 65% of domestic crude palm oil consumption; Figure 4) for use in 1) the food industry, such as snacks, instant noodles, sweetened condensed milk, non-dairy creamer, margarine, shortening, ice cream, and food supplement products, as well as the chemical and oleochemical industries; and 2) the production of other goods such as soap, cosmetics, shampoo, and lubricants (Figure 3).

-

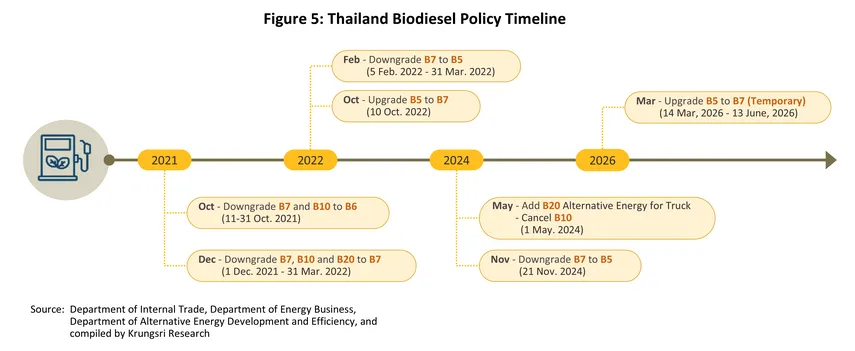

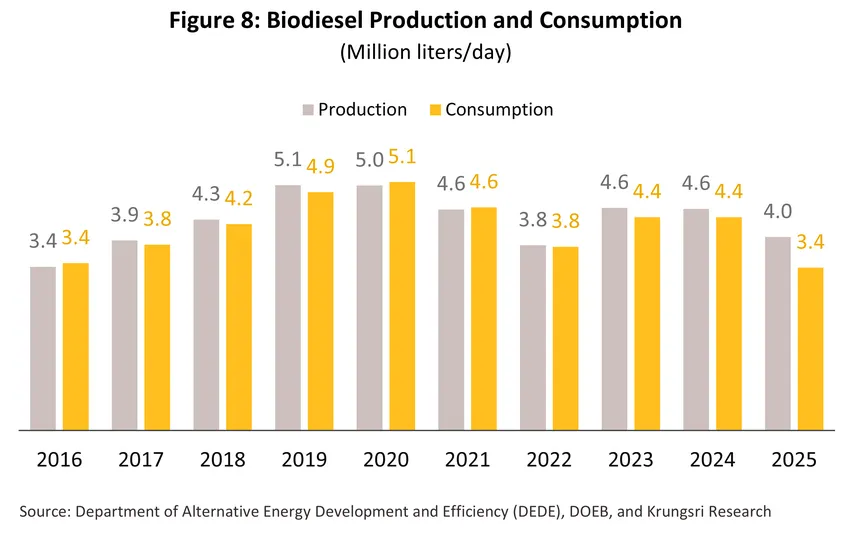

Crude palm oil was utilized as raw material in the biodiesel industry or B100 (representing 35%) for blending into motor vehicle fuel, with authorities adjusting the B100 blending ratio in diesel to align with crude palm oil production in each period (for instance, in 2022, the ratio was reduced from B7 to B59/ due to significantly higher domestic palm oil prices and declining domestic stocks; later in 2023, it was increased from B5 back to B7 due to a relatively high surplus of crude palm oil supply (Figure 5)).

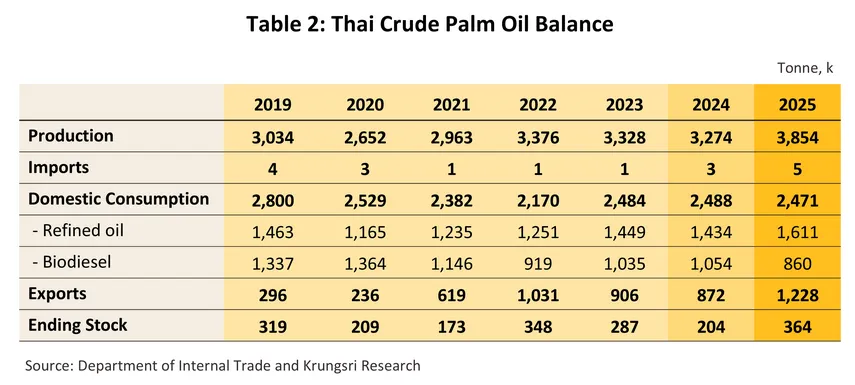

Thailand exports approximately 30% of total crude palm oil production, and the annual export volume depends on the surplus output in each period, with the government periodically implementing measures or projects to promote crude palm oil exports to alleviate domestic oversupply. Similarly, imports are only conducted during periods of supply shortages, such as when crude palm oil stocks fall below the buffer stock level, which authorities have set at 0.25-0.30 million tonnes10/; as of the end of 2025, Thailand held ending stocks of 0.36 million tonnes, representing 9% of total crude palm oil production, as domestic crude palm oil stock levels have a substantial impact on price levels.

Situation

In 2025, Thai palm oil supply surged by 17.7% as production accelerated due to favorable weather conditions and plantation area expansion driven by attractive price levels. Overall sales accelerated by more than 10.1% , propelled by the export sector, while domestic sales contracted slightly following a decrease in biodiesel usage within the transport sector. However, the rise in oil palm fruit prices impacted production costs, leading to an upward trend in selling prices for crude palm oil, refined palm oil, and export prices accordingly.

-

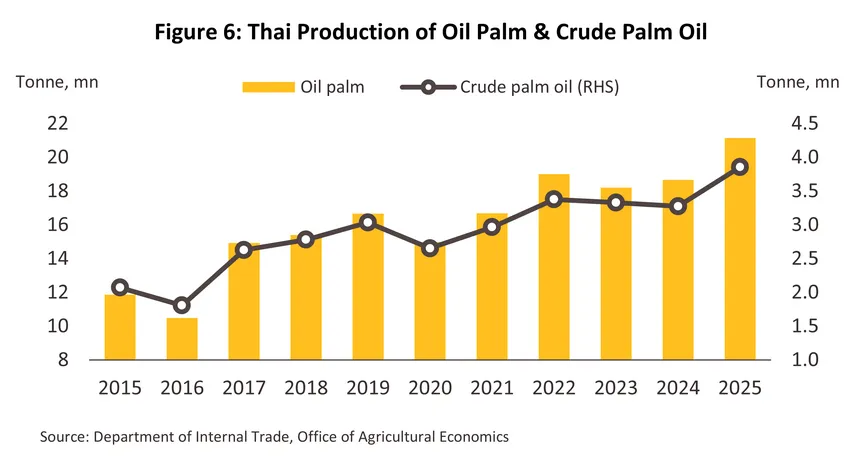

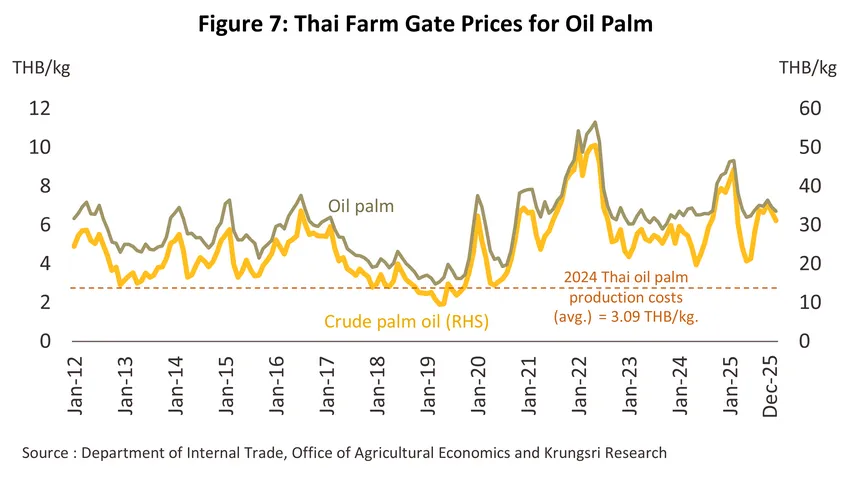

Fresh fruit bunch and crude palm oil production in Thailand reached a record high in 2025 (Figure 6). According to assessments by the Office of Agricultural Economics, the harvested area for oil palm expanded to 6.44 million rai (+1.9%), resulting in the volume of fresh fruit bunches entering the crude palm oil (CPO) production process reaching as high as 21.1 million tonnes (+13.3%) compared to 18.7 million tonnes in 2024. Key supporting factors included 1) more favorable weather conditions and rainfall patterns driven by the La Niña phenomenon; 2) the expansion of cultivation by farmers in response to high prices during 2021-2022 with yields beginning to enter the market in 2025; and 3) attractive government measures for minimum purchase prices11/ that pushed the average annual fresh fruit bunch price to THB 6.3/kg (+7.1%), which was higher than the average cost of THB 3.1/kg (Figure 7). This encouraged farmers to improve palm tree maintenance and elevate harvesting quality to meet standard criteria, consequently increasing the average annual oil extraction rate (OER) for palm bunches to 18.2% from the 17.7% level in the previous year. These factors collectively enabled Thailand to produce as much as 3.85 million tonnes (+17.7%) of crude palm oil, compared to 3.27 million tonnes in 2024 (Table 2).

-

In 2025, the export volume of palm oil products expanded 42.6% to 1.5 million tonnes, with a value of USD 1,762.8mn (+65.3%), driven by accelerating demand from major trading partners, the price advantage of palm oil compared to other types of vegetable oils, and government support measures, with details as follows:

-

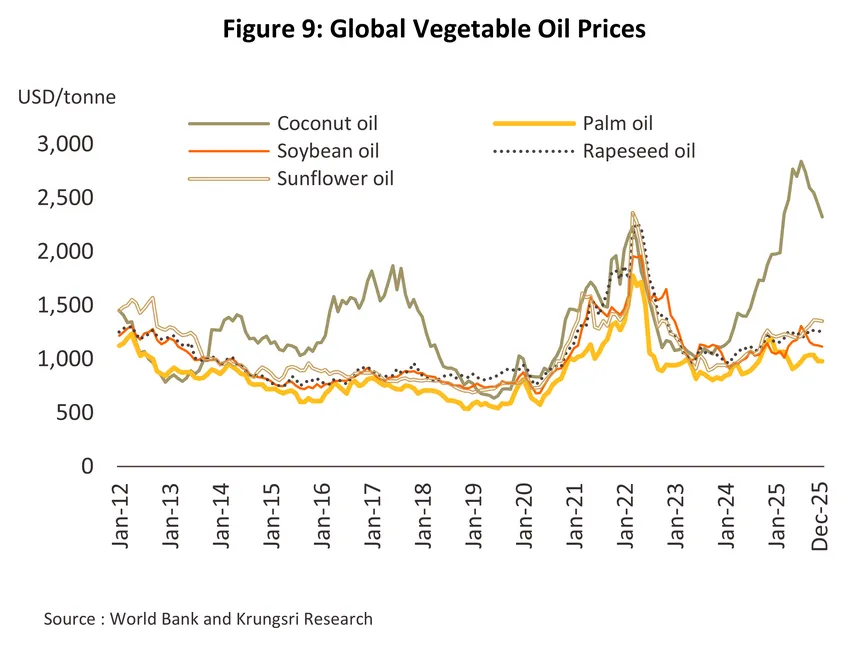

Crude palm oil: The export volume stood at 1.38 million tonnes (+50.0%), representing a value of USD 1,552.9mn (+75.7%), particularly driven by acceleration in major export markets, namely India with a volume reaching 1.23 million tonnes (+54.9%) and Malaysia with 0.12 million tonnes (+18.5%). Both countries accounting for a combined share as high as 98.0% of Thailand's total crude palm oil export volume. Key positive factors included 1) India's demand to accelerate stock accumulation to support domestic consumption and food and energy security, despite facing a weakening Rupee; 2) global palm oil prices remaining lower than other vegetable oil types (Figure 9), which stimulated overall export market demand; and 3) government support measures through export management subsidies at a rate of THB 2/kg, which enhanced the competitiveness of Thai exporters, resulting in the average crude palm oil export price rising to USD 1,252/tonne, or an increase of 22.3%, following the upward trend in raw material costs.

-

Refined palm oil: The export volume stood at 0.10 million tonnes (-12.1%) due to a contraction in demand from the primary market, Myanmar, which decreased to 0.06 million tonnes (-14.7%), and the secondary market, China, which decreased to 0.03 million tonnes (-4.3%); these two markets combined accounted for 93.0% of Thailand's total refined palm oil export volume. Key reasons included 1) Myanmar facing a US dollar shortage crisis, import license restrictions, and stringent international money transfer control measures, as well as logistical obstacles from the domestic unrest situation; and 2) the Chinese market turning to import palm oil from Indonesia, which is cheaper than Thailand, combined with a large supply of inexpensive domestically produced soybean oil in China being used as a substitute product. Nevertheless, the overall refined palm oil export value was still able to expand to USD 155.3mn (+6.9%) from the average export price, which accelerated to USD 1,542/tonne (+19.2%) in line with the upward trend of crude palm oil costs.

-

Crude palm oil stocks in both the global and Thai markets have trended downward continuously from 2024 through early 2025, primarily driven by expanded consumption in both the industrial (+0.9%) and food (+0.7%) sectors, particularly as demand in major producing countries such as Indonesia and Malaysia accelerated by 6.2% and 13.6% , respectively.

-

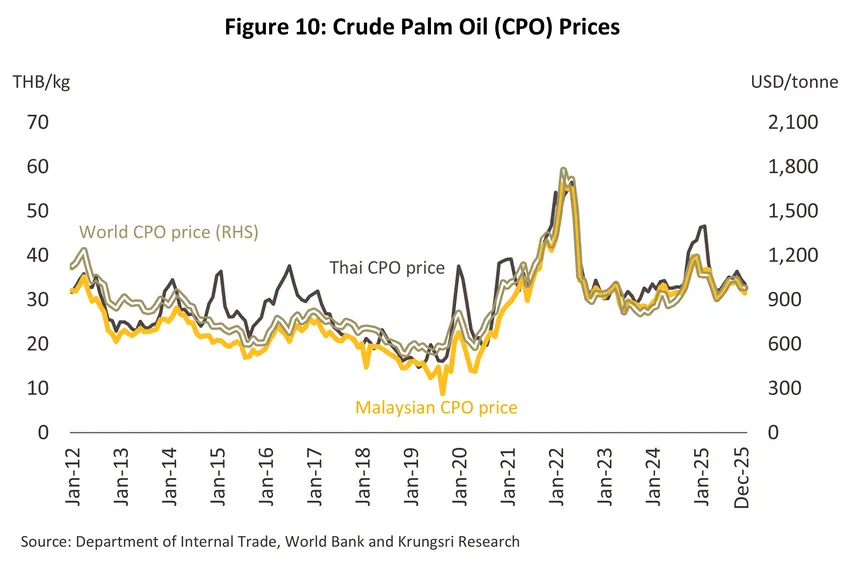

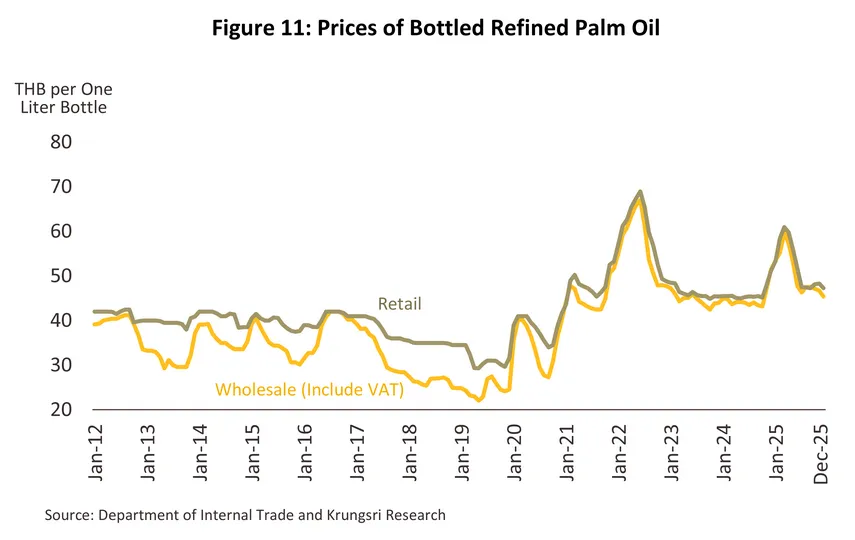

The result of the lower overall stocks in 2025 led to the average fresh fruit bunch price12/ increasing to THB 6.7/kg (+7.3%), in line with the minimum purchase price settings announced by the Energy Policy and Planning Office (EPPO) and the price competition for raw materials among palm oil extraction mills, causing the average annual crude palm oil (CPO) price to move up to THB 36.5/kg (+2.8%) compared to 2024 (Figure 10). Part of the increased cost was passed on to downstream industries, resulting in the increasing of average price of bottled refined palm oil (1 liter) to THB 52.2/bottle (+13.4%) (Figure 11), as well as the overall export price of palm oil products which rose 13.9% in alignment with the global palm oil price trend that increased to an average of USD 1,007/tonne (+4.5%).

-

However, during the second half of 2025, Thailand's crude palm oil stocks increased, standing at 0.36 million tonnes13/ as of the end of December 2025, an increase of 78.3% following the expansion of production supported by weather conditions, combined with pressure from the decrease in biodiesel consumption volume, which dragged down fresh fruit bunch and palm oil prices into a downward trend.

Outlook

During 2026-2028, fresh fruit bunch production is expected to stabilize at an average rate of -0.8% to +0.2% per year, while Thailand's crude palm oil is set to contract at -1.1% to -2.1% per year, respectively.

-

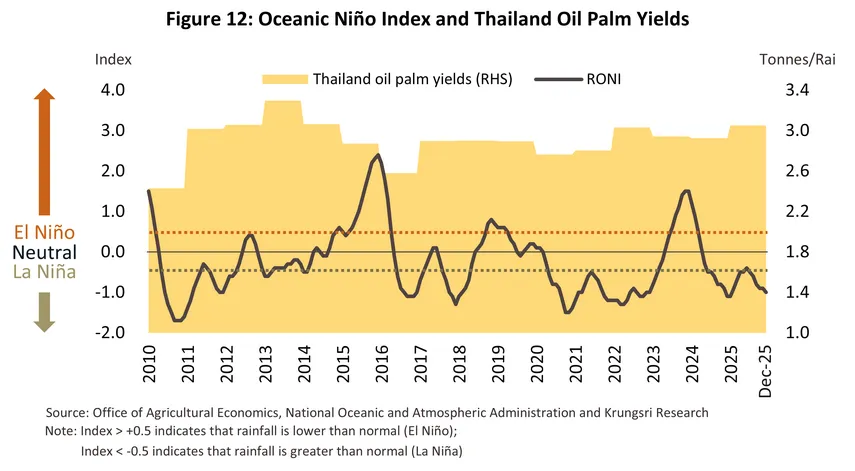

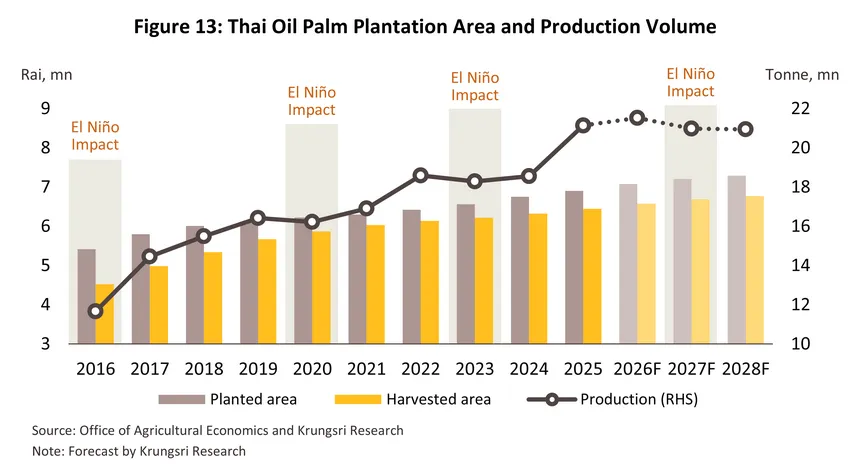

In 2026, oil palm production is trending toward an average expansion of 1.3-2.3%, supported by 1) favorable weather and temperatures in Thailand resulting from the La Niña phenomenon, which is expected to return to normal conditions14/ during 2Q/26 (Figure 12), leading to an increased yield per rai; 2) planted area is likely to increase by 1.5-2.5% per year, averaging 0.1-0.2 million rai annually, as oil palm trees planted in 2023 are currently beginning to produce, while an increasing number of previously planted batches are entering the high-yield per rai age criteria15/; and 3) overall prices remain attractive, encouraging farmers to maintain and harvest crops. Krungsri Research anticipates that the increase in fresh fruit bunch volume will cause the crude palm oil volume in 2026 to expand by an average of 1.1-2.1% . However, in 2027-2028, oil palm supply is likely to return to a contraction averaging -0.9% to -1.9% per year, dragged down by 1) hot weather and reduced rainfall from the return of El Niño conditions, causing damage to production, yield per rai, as well as the quality and extraction rate of oil from palm fruit; and 2) the ongoing prevalence of stem rot disease, resulting in Thailand's crude palm oil volume decreasing by an average of -2.6% to -3.6% per year (Figure 13).

-

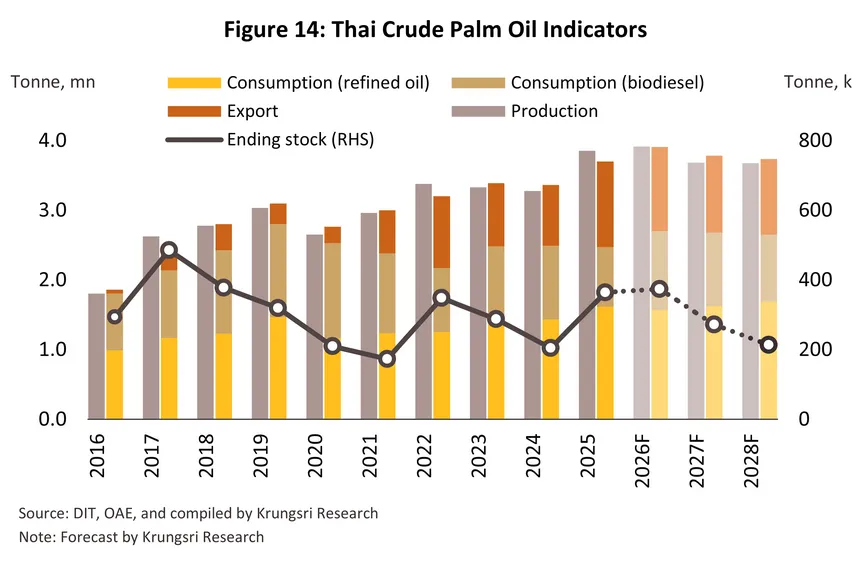

Domestic demand for crude palm oil during 2026-2028 is expected to grow at an average of 1.8-2.8% per year, accelerating significantly in 2026 driven by demand from the biodiesel industry as the mandatory biodiesel blending ratio is adjusted upward to mitigate pressure from the impact of rising oil prices amidst conflicts in the Middle East. While the refined palm oil industry will expand at a modest rate in 2026, partly due to a slowdown in orders from downstream industries during a period of weak purchasing power. During 2027–2028, overall growth is expected to moderate in line with tightening raw material supply. Nonetheless, the period will be partly supported by a gradual recovery in demand for refined palm products, in line with improving economic activity and tourism, which will drive demand in downstream industries—particularly food, chemicals, and oleochemicals (Figure 14), as follows.

-

Refined palm oil: Demand for crude palm oil for refining into refined palm oil is expected to trend toward growth of 1.1-2.1% per year, with the primary driver being the likelihood of accelerating growth during 2027-2028. This is supported by 1) the growth trajectory of the food industry, which is expanding in line with the gradual recovery of the tourism, hotel, and restaurant (HORECA) sectors; 2) demand in the oleochemical industry, which continues to trend upward following the gradual recovery in the consumption of downstream consumer goods such as detergents, soap, pharmaceuticals, and cosmetics, while the industry also directly benefits from the Oil Palm and Palm Oil Industry Reform Plan 2018-2037, aimed at upgrading toward advanced oleochemical industries to create added value and further broaden the domestic raw material utilization base; 3) the price competitiveness of palm oil compared to other types of vegetable oils, which provides incentives for substitution across various industrial groups; and 4) the expansion of production bases to accommodate the export of downstream products to regional markets with requirements for high standards and traceability.

-

Biodiesel production: Demand is expected to trend toward a gradual expansion averaging approximately 3.2-4.2% per year (around 3.7-4.4 million liters/day), stemming from two primary factors, namely

-

Demand from economic activities is driven by 1) economic and tourism conditions that are likely to gradually recover in 2027-2028 after facing a slowdown in 2026 due to the impact of the widespread Middle East conflict, with the number of foreign tourist arrivals likely to gradually increase to 35.5 million people in 2028 from 33.0 million people in 2025; 2) infrastructure investment under government transportation system development plans which is expected to see more progress, especially during 2027-2028; and 3) the continued expansion of the e-commerce business. These factors will help stimulate the demand for commercial vehicles, including both trucks and pickup trucks, for transportation and travel, resulting in an increase relative to 2025.

-

Government support measures to balance the domestic palm oil market include 1) a temporary increase in the mandatory biodiesel blending ratio from B5 to B716/ to manage domestic palm oil stocks and accommodate energy price volatility resulting from the potential prolonged Middle East conflict; 2) the enforcement of the Oil Fuel Management Plan 2024-2037 (Oil Plan 2024), which sets the biodiesel blending ratio in diesel fuel at 6.6-7.0%, a level consistent with the Euro 5 standard certified by automakers, and (3) the transition to the Euro 6 standard17/ for diesel vehicles starting from 2029 onwards, which will increase the potential for using diesel with higher biodiesel proportions; these are all key factors that will support long-term biodiesel demand as it is a low-sulfur fuel with notable properties for effectively reducing pollutant emissions, including carbon monoxide (CO), hydrocarbons (HC), and particulate matter (PM) efficiently.

-

Export volumes are projected to contract by -3.5% to -4.5% annually, as domestic raw material supply faces risks from weather volatility associated with a potential return of El Niño. This is expected to reduce output and lead to raw material shortages during 2027–2028. In addition, crude palm oil export control measures18/ aimed at securing domestic supply—amid rising demand driven by 1) the energy sector in response to the Middle East conflict and 2) the gradual recovery of tourism and the food industry—will further constrain export availability. This aligns with the global supply outlook, which is also expected to tighten due to 1) Indonesia’s increase in palm oil export tax to 12.5%19/ under commodity stockpiling policies for domestic use20/, along with land reclamation of palm plantations in forest overlap areas and a plan to raise the biodiesel blending mandate to B50 by 1 July 202621/; and 2) Malaysia’s constraints on plantation expansion due to anti-deforestation policies, coupled with disease outbreaks that have placed fresh palm output on a downward trend22/. Meanwhile, Malaysia’s domestic demand is expected to grow, supported by higher value-added downstream industries under policies promoting oleochemicals, food, and cosmetics, further limiting its capacity to expand export supply.

-

Year-end crude palm oil stocks during 2026-2028 are projected to decrease to 0.21-0.37 million tonnes (from 0.36 million tonnes at the end of 2025). Dragging factors include: 1) the impact of the El Niño phenomenon expected to return during 2027-2028, which will reduce oil palm production; and 2) domestic demand trending toward acceleration, particularly from the enforcement of the B7 biodiesel ratio, which still has the potential for further increases to accommodate energy prices that remain volatile in an upward direction due to the prolonged Middle East conflict, the expansion of high-value oleochemical industries23/, and the gradual recovery of the tourism and transport sectors during 2027-2028.

-

Regarding price trends, tight global and Thai supply amidst increasing global demand, coupled with the tendency to increase Thailand's biodiesel blending ratio to gradually absorb output exceeding the minimum reserve threshold, is expected to cause Thai oil palm and palm oil prices to trend upward continuously from 2025, with fresh fruit bunch prices expected to range between THB 7.5-8.5/kg (compared to the average price level of THB 6.3/kg in 2025).

Risk factors for the palm oil industry that may affect operators include

-

Geopolitical tensions which are broadening and likely to persist, particularly the US-Israel-Iran war crisis that intensified in 2026, cause the oil palm industry to face risks in several dimensions: 1) global oil price trends are likely to fluctuate on an upward trajectory, which subsequently impacts 1.1) purchasing demand that may slow down as downstream industrial plants tend to gradually delay orders to monitor the situation and 1.2) business profit management that may become more difficult due to production cost issues such as fertilizer, chemicals, and energy; and 2) logistics and maritime route crises from the closure of the Strait of Hormuz causing delays in exporting goods to Middle Eastern countries, although the average proportion of direct palm oil product exports from Thailand to Middle Eastern countries in 2025 was only 0.05%, downstream industry operators, especially for food and commodity products, may face logistics disruption.

-

Government policy changes are also a factor as oil palm industry production from upstream to downstream is under government management through both direct and indirect measures via various ministries such as the Ministry of Agriculture and Cooperatives, the Ministry of Industry, the Ministry of Energy, and the Ministry of Commerce, which may change according to the political situation.

-

Competition also trends toward intensity from substitute products, the entry of new operators, and existing players expanding production capacity. In addition, the average capacity utilization rate of the palm oil industry during 2023-2025 standing at only 48.7%, which is a low level compared to soybean oil (85.9%) and rice bran oil (61.4%), which are substitute products.

-

Thailand's overall palm oil production costs remain higher than Indonesia and Malaysia, coupled with the low-capacity utilization rate of Thai crude palm oil extraction mills, resulting in a disadvantage regarding unit costs and price competitiveness compared to global market competitors.

-

Non-tariff barriers, particularly the enactment of environmental conservation laws or measures by the European Union, which is one of the world's primary palm oil consumers, such as the EU Deforestation-free Regulation (EUDR)24/, requirements for European member states to gradually reduce the use of biofuels produced from oil palm—a crop at risk of high carbon generation—with a target to end usage or "Zero Palm Oil" by 203025/, and compliance with the Roundtable on Sustainable Palm Oil (RSPO) standards26/ to achieve international organizational acceptance.

-

The government's electric vehicle (EV) promotion trend, which aims to produce ZEV (Zero Emission Vehicle) at a rate of at least 30% by 2030, may result in a decrease in overall fuel consumption volume.

Regarding the future adaptation of the oil palm and palm oil industry, operators are likely to adjust by focusing on 1) elevating product standards such as producing to meet EUDR or RSPO standards; 2) expanding the business chain to increase efficiency and reduce production costs, such as producing biodiesel as an alternative fuel to reduce fossil fuel reliance, generating electricity from palm waste remaining from the palm oil production process for internal factory use, and producing Sustainable Aviation Fuel (SAF)27/, and 3) adjusting corporate strategies by emphasizing support for ESG (Environmental, Social, and Governance) and SDGs (Sustainable Development Goals) to build confidence among the environment, communities, and stakeholders.

1/ Oleochemicals are biochemicals produced from vegetable oils and animal fats. These include fatty acids, glycerin, fatty acid esters, and fatty alcohols, and these are typically used in the food processing and consumer goods industries, where they are found in products such as cosmetics, pharmaceuticals, soap, shampoo, detergents, lubricants, and insecticides.

2/ This is a precursor utilized in the production of chemicals and is often used in food processing and the manufacture of pharmaceuticals, personal healthcare products, cosmetics, and soap.

3/ Phase change materials are used to absorb and control temperatures. These are used in construction materials, textiles, goods transport, and packaging.

4/ Fatty alcohols are a type of basic oleochemical used in the manufacture of products across a range of industries including fragrancies, cosmetics, shampoo, surfactants, solvents, flavorings, detergents, lubricants, colorings and coatings, plasticizers, foam stabilizers, and additives used in the production of fibers and paper.

5/ Palm oil may be extracted either from the oil palm fruit and from the oil palm seeds, although as of the 2024/2025 season, extraction of oil from palm fruit accounted for 89.7% of global palm oil production.

6/ The oil yield per rai of various oil-producing crops is as follows: oil palm yields 500-600 liters per rai, rapeseed 100-150 liters per rai, sunflower seed 80-120 liters per rai, coconut 80-100 liters per rai, peanut 90-130 liters per rai, and soybean 50-70 liters per rai. (Note: The actual oil yield depends on the extraction efficiency of processing facilities, the quality of agricultural produce, and farm management practices.)

7/ Typically, harvesting can begin when oil palms are 3.5-4 years old. Yields peak when palms are 6-16 years old and then decline, although production can continue until trees are 25-28 years old. At this point, the palms are usually cut down and replaced.

8/ CPO mills are generally located close to plantations since to guarantee high-quality oil, the palm fruits need to be processed within 24 hours of harvesting.

9/ B5, B7, and B10 refer to mineral diesel mixed with respectively 5%, 7% and 10% biodiesel.

10/ Safety stock or buffer stock refers to the volume of inventory (in this context, the volume of crude palm oil) that the Public Warehouse Organization (PWO) reserves to prevent raw material shortages during the production or consumption of related domestic industries, enabling manufacturers to maintain continuous production.

11/ The Prices of Goods and Services Act set a minimum price of THB 4.5/kg to be paid by mills purchasing oil palms. As per article 7, traders are also required to pay minimum prices set by the Energy Policy and Planning Office when purchasing oil palm and derivative products.

12/ As per the announcement by the Central Committee on the Price of Goods and Services, palm fruits are a controlled product (the most recent announcement was made on July 29, 2025).

13/ Higher than the minimum reserve level of 0.25-0.30 million tonnes.

14/ According to data from the National Oceanic and Atmospheric Administration (NOAA), El Niño most recently occurred during 2023-2024, resulting in a relatively high probability of La Niña conditions occurring in 2025-2026, which Krungsri Research expects to persist for 1-2 years. Subsequently, weather patterns are likely to enter a neutral state and are projected to transition into El Niño in second half of 2026.

15/ Palm trees planted in response to government incentives that ran from 2008-2012 are now 13-17 years old, and so these are within their peak producing age range of 7-16 years (source: Office of Agricultural Economics).

16/ The resolution of the National Palm Oil Policy Committee (NPOPC) on May 8, 2025, to adjust the blending ratio from B5 back to B7 was not implemented immediately until November 17, 2025, when the NPOPC (Meeting No. 2/2025) reaffirmed the resolution requesting the Ministry of Energy to expedite the adjustment from B5 to B7. Ultimately, the Department of Energy Business issued a notification for the temporary implementation of B7 for a three-month period, which became effective from March 14, 2026, and is scheduled to expire on June 13, 2026.

17/ Regarding the Euro 6 standard, the timeline has been adjusted to align with economic conditions and the adaptation of operators, under which small diesel vehicles will begin enforcement starting January 1, 2029, while large diesel vehicles will be considered for enforcement with at least two years' prior notice, but no later than January 1, 2032.

18/ Initially effective for one year starting from April 7, 2026, onwards.

19/ Regarding the increase in export levies, since March 1, 2026, Indonesia has raised the CPO export levy rate to 12.5% (from the previous 10.0% ) to contribute funds to the Palm Oil Fund and control the volume of outflowing goods.

20/ Indonesia implemented strict export control measures for commodities including palm oil in mid-March 2026, requiring producers to allocate sufficient crude palm oil (CPO) to meet domestic demand before being granted export permits.

21/ Indonesia supports palm oil utilization through initiatives such as the development of sustainable aviation fuel and the increase of the biodiesel blend in diesel fuel to B50 on July 1, 2026, aims to reduce reliance on imported fuels and mitigate impacts from geopolitical tensions, similar to Malaysia, which supports bioenergy use through the approval of B30 biodiesel for heavy vehicles or trucks by 2030 (Source: Malaysian Palm Oil Board).

22/ The palm oil industry in Indonesia and Malaysia faces supply issues, including 1) disease outbreaks, particularly from Ganoderma fungi that cause damage; 2) aging oil palm trees among smallholders that produce low outputs; despite government budget support for replanting, it remains insufficient to cover costs, causing replanting rates to fall below targets and leading to a downward trend in palm oil export volumes from both countries, with production from 2030 onwards expected to decline by approximately 20%; and 3) Indonesia's crackdown on illegal natural resource use, which has already resulted in the reclamation of 19.4 million rai of oil palm plantation area with another 31.3 million rai under investigation (Source: Office of Agricultural Economics).

23/ Thailand has implemented measures to drive value addition in the oil palm and palm oil industry by designating eight target products, which include base oil lubricants, bio-transformer oil, environmentally friendly detergents (Methyl Ester Sulfonate: MES precursor), bio-lubricants and greases, paraffin, pesticides and insecticides, bio-hydrogenated diesel (BHD), and biojet fuels.

24/ The EU Deforestation-free Regulation (EUDR) is a law aimed at limiting cultivation derived from deforestation, covering seven categories of agricultural products: rubber, oil palm, cattle, cocoa, coffee, peanuts, wood and wood products, as well as products developed from these commodities. The law will be effective from December 30, 2025, for large enterprises and from June 30, 2026, for small and medium-sized enterprises (SMEs).

25/ The European Union is striving to reduce palm oil usage, with the European Parliament issuing the "Renewable Energy Directive, Directive (EU) 2018/2001 (RED II)," which stipulates that Europe must use alternative energy and reduce energy consumption from palm oil to "Zero Palm Oil" by 2030.

26/ The Roundtable on Sustainable Palm Oil (RSPO) standard has been in effect since 2004 through the collaboration of farmers and oil palm and palm oil production operators, with the objective of promoting the growth and use of palm oil products that meet international standards, covering economic, social, and environmental sustainability dimensions.

27/ Aviation fuel produced from renewable raw materials that can be regenerated, whereby this fuel must comply with sustainability standards as defined by the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) of the International Civil Aviation Organization (ICAO).

.webp.aspx)