Krungsri Research sees an improving outlook for the cassava industry through the period 2022 to 2024. Business conditions will brighten with stronger demand from both downstream domestic industries, especially from food processors and manufacturers of ethanol, and overseas markets, which absorb 67% of Thai output of cassava products. Growth in exports will be driven principally by a rise in sales into the main market of China, and in particular this will come from: (i) recovery in Chinese demand for cassava, most notably for use in the production of animal feed and ethanol; and (ii) the rising price of corn (an important substitute for cassava) and the 3-year rundown in Chinese corn stocks. Nevertheless, problems remain for the industry in the form of uncertain and variable outputs, which depend on favorable climatic conditions and the control of disease (e.g., of cassava mosaic disease), and the domestic industry’s heavy dependence on the Chinese market, access to which is increasingly contested by Thailand’s neighbors

Overview

Cassava is a carbohydrate-rich crop that has a wide range of uses in the so-called ‘4Fs’ of: (i) food (for human consumption), (ii) feed (for use in animal feed), (iii) fuel (for use in the production of ethanol), and (iv) factories (where it is used to make alcohol, citric acid, clothing, medicine, paper and chemicals).

For many years, global demand for cassava has been high thanks to its many industrial uses and the fact that it has often been cheaper than other starchy crops. This has then lifted it to the status of being the world’s 5th most important food crop, after corn, wheat, rice and potatoes.

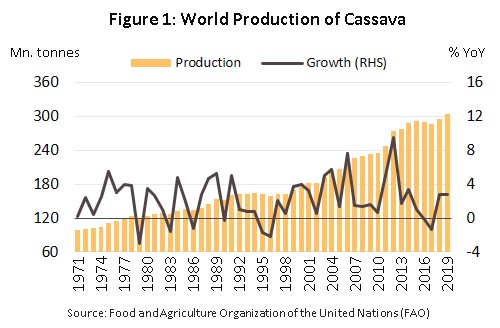

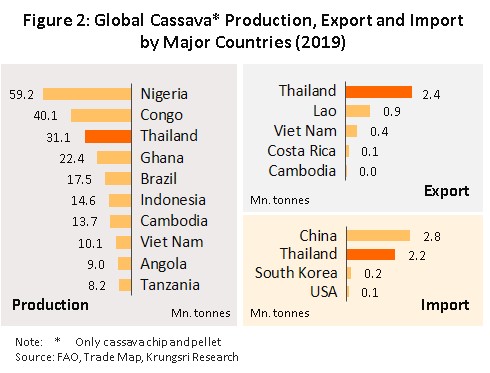

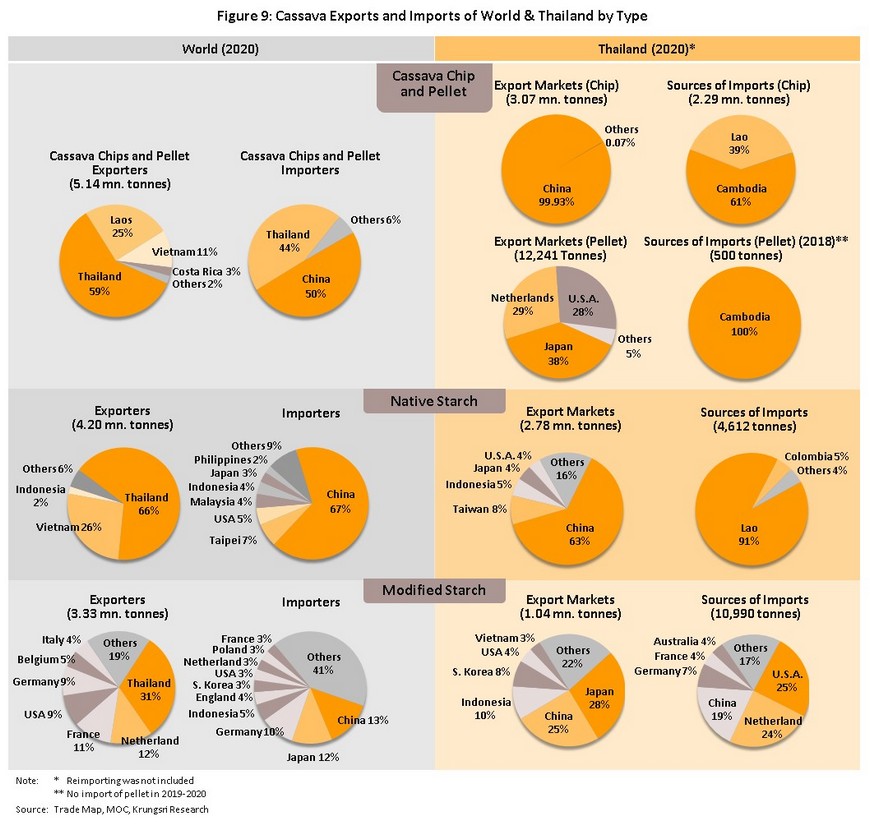

In 2019, a total of 304 million tonnes of cassava were produced globally (Figure 1). Contributing 63.3% of the total, Africa was the most important cassava-producing region, followed by Asia[1] (28.0%), the Americas (8.6%) and Oceania (0.1%). By individual country, Nigeria was the world’s biggest producer, with 19.5% of all outputs globally, followed by the DR Congo (13.2%), Thailand (10.2%), Ghana (7.4%), Brazil (5.8%) and Indonesia (4.8%) (Figure 2), although heavy investment by Thai and Chinese players in production in Vietnam and Cambodia has meant that outputs in these two countries have been rising rapidly over the past 10-15 years.

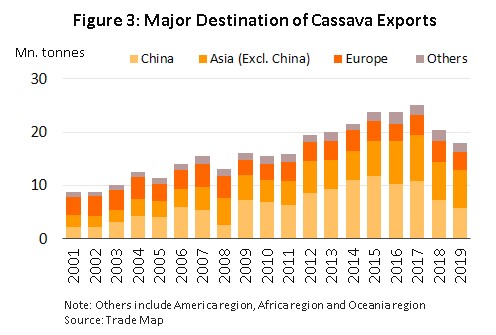

However, although Africa is the world’s most important cassava-producing nations, African production is largely for domestic consumption since in these countries, the crop plays an important role maintaining the quality of life and in supporting local food security and economic activity. African-produced cassava is therefore principally consumed as fresh and processed products. By contrast, in Thailand, production is oriented towards overseas markets and the country is thus among the world’s most important exporters (Figure 2). In terms of export destinations, global markets for cassava are largely supported by demand from Asia, especially China, which alone accounts for 50.0% of all cassava imports globally (Figure 3).

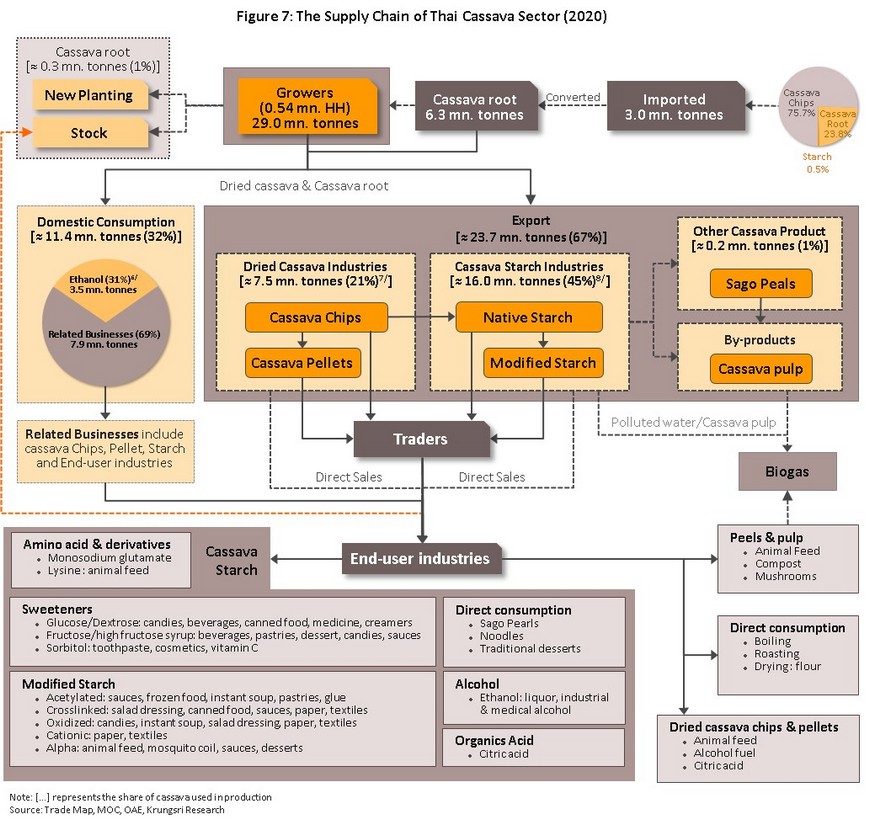

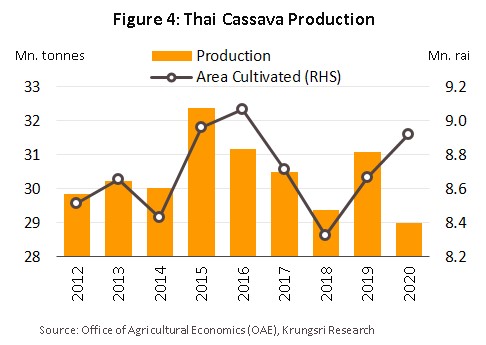

Over the past two decades, rising demand on export markets has fed into an expansion of Thai cassava processing capabilities and through this, to a steady rise in the size of the national cassava harvest; as of 2020, 8.9 million rai of Thai farmland was planted with cassava, and this produced roughly 29.0 million tonnes of raw product[2] (Figure 4). Cassava cultivation is clustered most heavily in Nakhon Ratchasima (16.0% of all Thai cassava farms by area), followed by Kamphaeng Phet (7.8%), Chaiyaphum (6.4%) and Kanchanaburi (5.7%).

In 2020, there are 1,210 cassava processing facilities[3] in Thailand but for convenience and to save on transportation costs, these are generally located close to cassava production, and so with 161 plants, Nakhon Ratchasima has the most of all of Thailand’s provinces, followed by Kamphaeng Phet (150), Nakhon Sawan (90), and Chaiyaphum (63). Thai players have also sited facilities in positions that allow them easy access to imports from neighboring countries, especially Lao PDR, Cambodia and Myanmar, where to ensure secure supplies of inputs, they have established basic processing facilities. Thus, there are 75 cassava plants in Ubon Ratchathani, 61 in Kanchanaburi and 33 in Sri Saket, while to make exports more convenient, there are a further 26 facilities in Chonburi, 16 in Rayong and 15 in Chachoengsao, these locations having the advantage of ready access to major ports (Figure 5).

Thailand-made cassava products can be split into two main groups:

- Dried cassava products: The most important product is cassava chip, which is used as an input into the manufacture of animal feed, alcohol and citric acid. Thailand is currently home to 1,042 facilities that produce dried cassava chip (or 96% of all total processing plants). A further 29 (2.7%) process cassava pellets, 12 (1.1%) produce dried crushed cassava and 2 (0.2%) produce other types of dried cassava goods.

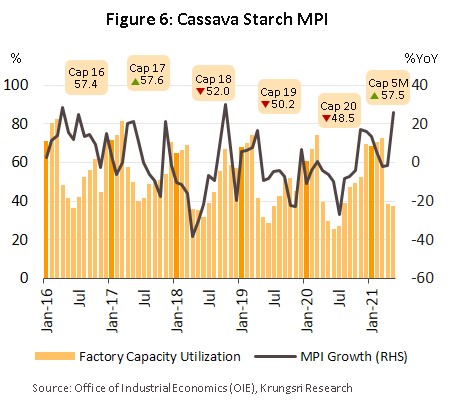

- Tapioca/cassava starch products: The initial output of cassava starch production is ‘native starch’, which can be consumed directly in households as a cooking ingredient or used in the manufacture of ‘modified starch’[4], a high value-added good that is then used as an input into a wide variety of downstream industries. Industrial processes then convert this into products including monosodium glutamate, sweeteners, sauces, cosmetics and medicines. At present, there are 104 cassava starch processing facilities in Thailand and a further 21 producing modified starch. Generally, the initial processing of cassava into starch occurs at the end of the year or the start of the next year because this follows on from the main harvest. Thus, both the cassava starch MPI and capacity utilization for the cassava industry typically peak between December and March (Figure 6).

These supplied 2.3 million tonnes of cassava chip[5] and 0.7 million tonnes of fresh cassava (together these accounted for 95% of all cassava imports by volume).

In total, 67% of Thai cassava output is used to supply export markets, with the remainder going to the domestic market, where it is either consumed directly or used as an input into downstream industries (Figure 7).

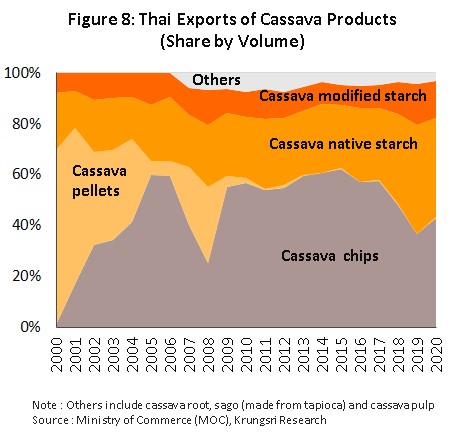

Because of its highly developed cassava industry, Thailand is the world’s leading exporter of cassava products, and the country now has a 66% share of global exports of native starch, 59% of exports of cassava chip, and 31% of modified starch. However, following the 2005 decision by the EU to stop imports of cassava pellets[9] (the EU had until then been a major importer) and to switch to the use of alternatives, Thai exports of these have dropped to very low levels (Figure 8). The change in EU policy also had the effect of profoundly altering the structure of Thai exports, which moved from a reliance on sales to Europe to an almost total dependency on Asian export markets, and in particular to China, which with a 72% share of all Thai exports of cassava products is by far Thailand’s most important market (Figure 9).

- Cassava chip: In 2020, 43.0% of exports of Thai cassava products by volume were of cassava chip (Figure 8), almost all of which went to China (the market for 99% of Thai exports of cassava chip), where it is used to manufacture alcohol, ethanol, animal feed[10], and citric acid. However, the structure of the export market and the extreme concentration of purchasing power means that Thai suppliers have only weak bargaining power, while they are also exposed to significant levels of risk should policies towards sourcing imports change. This is in fact what happened in 2018-2020, when China cut its imports of cassava chip and switched instead to using domestically-produced corn, and this then caused significant knock-on effects for Thai exporters.

- Native starch: This accounted for 39.0% by volume of all exports of cassava products from Thailand in 2020. The main markets for this are in China (which took 63% by value of all exports of native starch in 2020), followed by Taiwan (8%), Indonesia (5%), Japan (4%) and the US (4%) although the exact state of export markets depends to a large degree on the health of downstream industries, including food processing, paper production, beverages and textiles.

- Modified starch: This is a highly value-added product that accounts for another 14.6% by quantity of Thai cassava exports. Demand for modified starch generally moves in line with changes in the outlook for downstream industries, including producers of cosmetics and medicines. The main export markets for modified starch are Japan (which bought 28% of all 2020 exports of modified starch by volume), China (25%), Indonesia (10%) and South Korea (8%).

- Cassava pellets: The 2005 decision by the European Union[11] to cut imports of cassava pellets had profound impacts on producers, and pellets now contribute just 0.2% to total cassava exports.

- Other cassava products: The remaining 3.2% of exports come from a mixed bag of products, including cassava root, sago (made from tapioca) and cassava pulp. The principal markets for these goods are New Zealand (which took 37% of exports of this group in 2020), South Korea (36%), China (16%) and Bangladesh (3%).

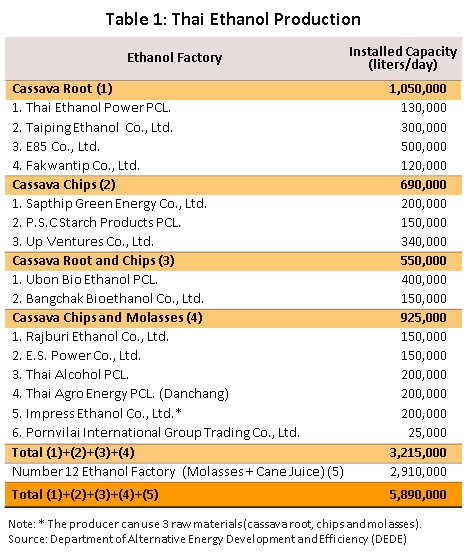

With regard to domestic uses of cassava, in addition to being consumed directly in households and in the manufacture of animal feed, it is also used as a raw material in other industries, including the processing and production of food and beverages, medicines, cosmetics, chemicals and alcohol. Large players have also invested in downstream industries, including ethanol production and the generation of bioenergy from cassava pulp and other waste products. The electricity that is produced from this may then be distributed commercially or used by the cassava processor itself (Table 1).

Situation

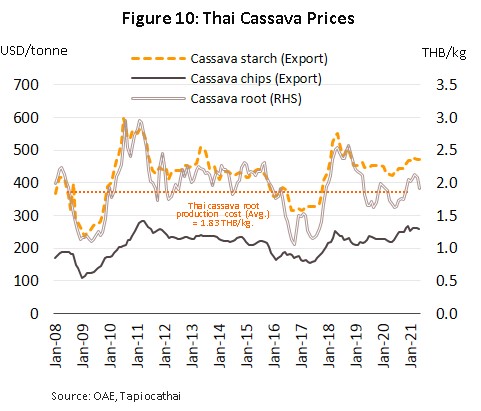

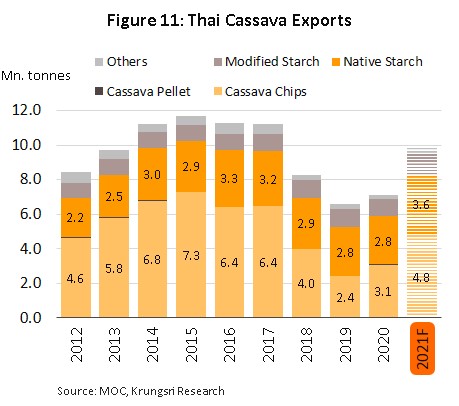

In 2020, cassava outputs dropped 6.7% to 29.0 million tonnes. The harvest was affected by (i) natural factors that included drought, the delayed onset of the rains, and outbreaks of cassava mosaic disease, and (ii) a decline in the total cultivated area of cassava, which was in turn driven by a fall in the price of fresh cassava from its 2019 level to just THB 1.80/kilogram (-4.9%) in 2020. At this price, income was insufficient to recoup production costs[12] (Figure 10) but despite this, the volume and value of total exports of cassava products climbed by respectively 8.1% and 2.7% to 7.1 million tonnes and USD 2.7 billion (Figure 11) as overseas sales of cassava chip (Thailand’s primary export product) rose, especially to China. Exports were boosted by the Covid-19 pandemic and the lift this gave to demand for energy crops (e.g., corn and cassava) for use in the production of alcohol and ethanol. By contrast, exports of cassava starch declined as China increased imports from the CLMV nations, most notably from Vietnam.

The outlook for the cassava industry should improve in 2021 on stronger supply that will be lifted by the incentive given by better prices, government support for the industry, and more favorable weather. The situation should also improve on the demand side, both domestically and internationally.

- Cassava outputs will tend to rise, and for 2021, these are forecast to be up 3.8% to 30.1 million tonnes. Tailwinds lifting the harvest will include: (i) an increase in the total cultivated area, which the Office of Agricultural Economics estimates will reach 9.16 million rai in 2021, up 2.8% from 2020 thanks to the incentives coming from: (i.i) the price rises that have been seen since 2H20 (Figure 10); and (i.ii) government support for the industry, coming in particular in the form of income guarantees; and (ii) heavy rainfall and a greater quantity of water available for irrigation, which should then bring yields up to 3,286 kilograms/rai (up 1.0%).

- Export orders are forecast to rise, with demand for cassava chip from China strengthening with the hike in corn prices and the rundown in corn stocks. The latter has come about as a result of the Covid-19 pandemic, which has then driven heavier demand for alcohol and ethanol, for which corn is an input. Given this, 2021 exports of cassava products from Thailand are expected to jump 39.0% to 9.9 million tonnes (compared to 7.1 million tonnes in 2020). These exports will be split between the following:

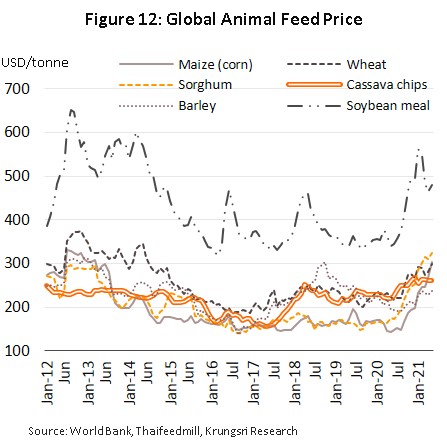

- Cassava starch: In 1H21, exports of cassava starch totaled 1.8 million tonnes (up 34.3% YoY), generating receipts of USD 831.7 million (up 47.4% YoY), caused by rising prices for other commercial crops, including millet (+82.4% YoY), corn (+69.0% YoY) and wheat (+26.0% YoY) (Figure 12), but prices for cassava tended to lag behind these and this then encouraged major importers including China, Taiwan, the Philippines and Malaysia to switch to an increasing reliance on cassava starch as a primary input in industries that use relatively straightforward processes (e.g., the processing and production of food and drinks, paper, adhesives, textiles, and particle/fiberboard). This then lifted export prices of Thai cassava starch by 10.0% YoY to USD 458/tonne, and it is expected that for 2021 overall, export volume will be up 28.3% to 3.6 million tonnes.

- Cassava chip: By volume, 1H21 exports of cassava chip jumped by 55.9% YoY to 2.9 million tonnes, generating receipts of USD 712.5 million (up 85.0% YoY). Several factors lay behind these dramatic increases, including: (i) the Covid-19 pandemic, which drove stronger demand for cassava chip for use in the production of ethanol and alcohol in China; and (ii) the decline in Chinese stocks of corn (an alternative to cassava) in 2018 and 2019, which boosted export prices of cassava chip by 18.5% YoY to USD 250/tonne. For all of 2021, exports are forecast to reach 4.8 million tonnes (up 55.5%).

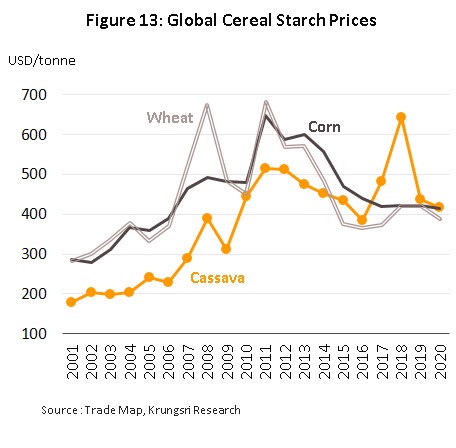

- Modified starch: Exports of modified starch rose 15.3% YoY to 0.6 million tonnes in 2021 (up 15.3%), generating income of USD 416.7 million (up 7.2% YoY). These increases are attributable to stronger demand from China, India, South Korea, Malaysia and Taiwan for modified starch for use in the production of medicines and cosmetics. However, sellers of modified starch are facing stiffer competition from starch produced from other inputs that have similar properties but which are more competitively priced (Figure 13), and this caused export prices to weaken by -4.3% YoY to an average of USD 698/tonne. For all of 2021, exports of modified starch are expected to reach 1.2 million tonnes (+12.0%).

- Cassava pellets: In the first half of 2021, exports of cassava pellets slid 12.6% to 7,459 tonnes, which then brought in earnings of USD 2.1 million (down -7.7% YoY). European buyers have switched to alternative crops grown in the region and as such, imports into the EU from Thailand are on a downward slide. This has been partially compensated for by continuing demand from Japan, the Netherlands and the US from use in animal feed and energy production, but for 2021, exports are forecast to fall another 11.0% to 11,000 tonnes.

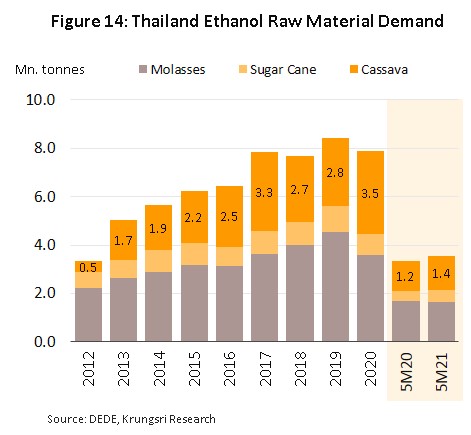

- Domestic consumption is expected to rise on greater demand from downstream industries, especially from food processors and ethanol distillers. As such, total demand for fresh cassava on the domestic market is expected to edge up 1.8% to 11.6 million tonnes in 2021, split between the following. (i) 8.0 million tonnes of cassava will be consumed by households and industry, most notably for the production of alcohol or products that contain alcohol (as a disinfectant), demand from which can be expected to continue to rise. (ii) 3.6 million tonnes will be used as an energy crop. The government is encouraging greater use of ethanol but the drought in 2019-2020 reduced the availability of sugarcane and molasses (with lower supply and higher price) and so manufacturers have switched to a greater dependency on cassava (Figure 14).

- Domestic prices for fresh cassava rose 12.7% YoY to THB 2.02/kilogram in 1H21 on stronger demand. In particular, domestic demand rose for cassava for processing into alcohol and ethanol, and to substitute the shortfalls of sugarcane and molasses in the production of energy from alternative sources, while on overseas markets (e.g., China), fresh cassava became more attractive and imports climbed as corn prices rose and stock holdings fell. For all of 2021, prices for fresh cassava are therefore forecast to average somewhere in the range of THB 2.1-2.2/kilogram.

Outlook

Through the years 2022 to 2024, demand for Thai cassava products is expected to strengthen relative to 2021 levels. Details of this are given below.

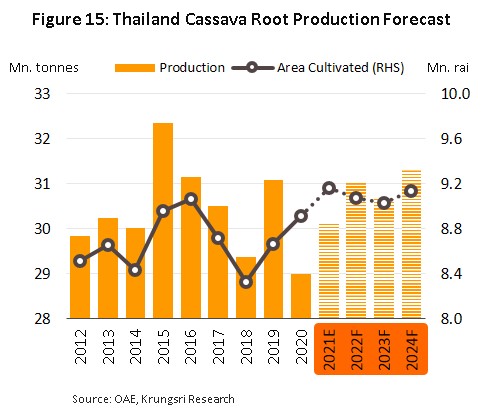

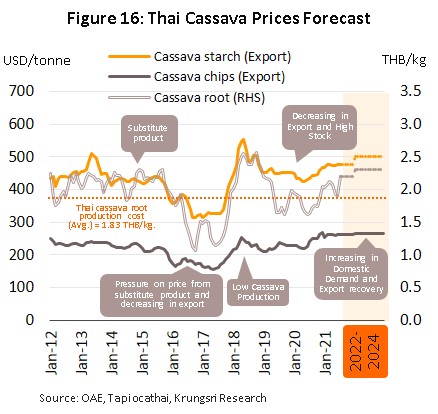

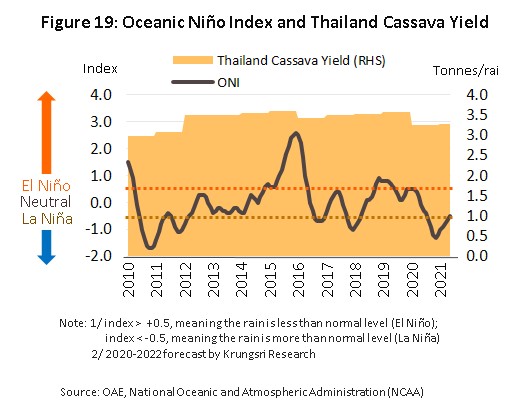

Production: Outputs of fresh cassava are forecast to increase by an average of 1.0-2.0% annually, helped by an expansion in the total area cultivated, better water management, control of outbreaks of leaf mosaic disease, and a more favorable long-term weather forecast (Figure 15). In addition, farmers will be incentivized to increase their plantings by positive price signals, themselves boosted by recovery in export markets and the world economy generally, and by government support for the industry, most obviously in the form of income guarantees. Given this, over the next 3 years, prices for fresh cassava are likely to climb to THB 2.2-2.4/kilogram compared to average production costs of THB 1.9/kilogram (Figure 16).

Domestic market: The forecast is for domestic demand for cassava products to strengthen by an average of 3.0-4.0% per year through the coming period on: (i) 3.5-4.0% annual growth in the food processing industry over 2022 to 2024 as the economy rebounds in the post-Covid-19 environment (source: Euromonitor); (ii) government policy that will drive stronger sales of ethanol (included in the E20 and E85 gasohol mixes), and rising demand for alcohol and alcohol-based disinfectant products; and (iii) the tight supply and higher prices for sugarcane and molasses, which has encouraged ethanol producers to increasingly switch to using fresh cassava, cassava chips and cassava starch as their primary inputs.

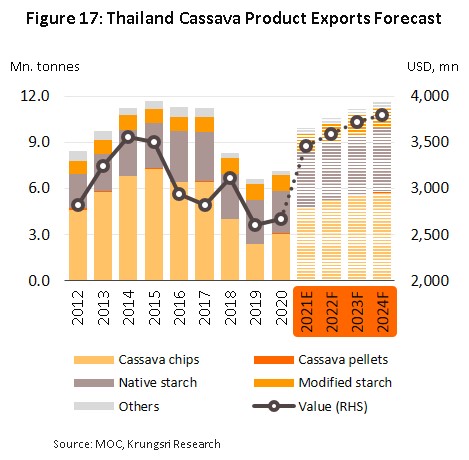

Export markets: Total exports are expected to expand by 5.0-6.0% annually (Figure 17). Details of individual product groups follow.

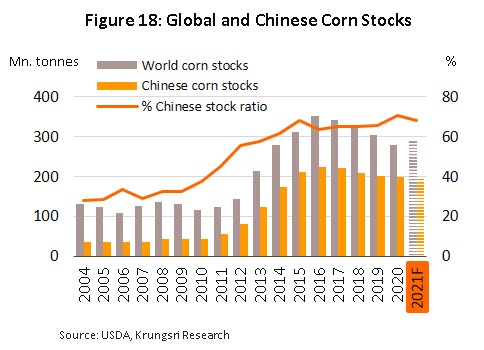

- Cassava starch: Exports should improve at a rate of approximately 5.0-5.5% per annum, moving in step with the better outlook for downstream industries, most especially in the food and beverage sector. However, exporters will have to contend with challenges in the form of: (i) competition on price from alternative starches (i.e., those made from corn and wheat), prices for which are expected to be close to those of cassava; (ii) the likely improvement in China’s ability to substitute corn for cassava or to use these alternately (Figure 18); and (iii) greater competition from exports from the CLMV countries[13] thanks to investments made there by Chinese players in Cassava supply chains, including both cassava farms and basic processing plants.

- Cassava chip: Exports of cassava chip are expected to rise by 6.0-7.0% annually on: (i) stronger demand from China (the main export market) due to increased output of disinfectant alcohol, ethanol for use in construction and as an energy source , and animal feed (now that the outbreak of African swine fever is abating); (ii) the stockpiling of agricultural goods and increased worries about food security that have followed the Covid-19 pandemic; and (iii) the rebound in the global economy that the easing of the Covid-19 crisis is bringing, and the stimulus effect of this on downstream industries worldwide.

- Modified starch: Recovery in the global economy and expansion in industries including the production of cosmetics, food and medicines will feed into average yearly growth in exports of 3.0-3.5%.

- Cassava pellets: The expectation is that overseas sales will grow by some 4.0-5.0% annually on greater demand for use as a biofuel and as an animal feed, but despite this more positive outlook, exports will remain weak and uncertain, and stronger demand will be limited to periods when alternative goods are in short supply.

In light of the trends described above, players involved in upstream cassava production will likely increase the scale of their investments in related industries (e.g., ethanol refineries and bioenergy facilities), switch their output to focus on products that have greater added value, and cut production costs by generating their own electricity. However, while these moves will help to increase players’ ability to generate profits overall, manufacturers of cassava pellets are likely to face ongoing problems with depressed and uncertain demand in export markets.

Major factors influencing the market in the coming period

Tailwinds

- Short-term (i.e., affecting the market over 2022-2023) positive factors affecting the cassava market will come from the impact of the Covid-19 crisis on demand. Demand will rise: (i) for use in the production of alcohol directly or as a component in other products; (ii) for use in the manufacture of ethanol, now that other inputs (e.g., sugarcane and molasses) are in short supply and prices are increasing; and (iii) from the food processing industry as worries over food security rise

- Long-term (i.e., affecting the market from 2023 onwards) drivers of higher demand for cassava will include: (i) the Thai government’s encouragement of greater use of ethanol as an alternative energy source; and (ii) heavier demand from downstream industrial consumers in China, which will see growth in step with the expansion of the Chinese middle class.

Headwinds

- Short-term headwinds affecting the market will comprise: (i) uncertainty over outputs, which are determined by (a) variations in the weather (Figure 19) and (b) the risk of outbreaks of cassava mosaic disease; (ii) price variability; and (iii) a fall in orders from China, as industries there switch to alternative inputs.

- Longer-term headwinds include: (i) competition for supplies of fresh cassava to use in industrial applications, especially for use in high value-added biotech industries and in other sectors that enjoy government support; (ii) the heavy dependence on the Chinese market, which makes Thai operators highly exposed to changes in Chinese government policy; and (iii) rising competition on world markets, especially from Vietnam and Cambodia, which may put downward pressure on export prices and reduce operators’ profitability.

Programs and measures affecting the cassava industry, 2020-2021

1) Guaranteed income scheme for cassava growers, 2020-2021: A cabinet resolution passed on 18 August, 2020 approved the earmarking of THB 9.79 billion to be used to support the income of farmers growing cassava. 0.52 million people are eligible for this help, details of which are as follows:

- Access, prices and limits of the scheme: The program is open to farmers planting cassava in crop year 2020/21, for which it sets a target price of THB 2.50/kilogram with 25% starch content. Participants in the scheme are limited to 100 tonnes of cassava per household.

- Claiming top-up payments on the difference between market and target cassava prices: All farmers registering as cassava growers must record the date of their harvest with the Department of Agriculture Extension (operating under the Ministry of Agriculture and Cooperatives), and this should be at least 8 months after planting. Applicants must be also growing the cassava themselves and have legal claim to the final crop.

- Payment conditions: Assistance is limited to 100 tons of cassava per household, and applications may be made only once for each location.

- Making top-up payments: The Bank for Agriculture and Agricultural Cooperatives will transfer funds equal to the difference between the target price and the market price (the central reference price) directly to farmers’ accounts. The reference prices will be announced on the 1st day of each month for a period of 12 months.

- Duration of the scheme: Farmers who registered as cassava growers with the Department of Agriculture Extension between 1 April, 2020 and 31 March, 2021 have received payments from the government starting on 1 December, 2020. Payments will be made on the first day of each month and will cover the period from 1 December, 2020 to 30 November, 2021.

2) Other measures to assist cassava growers, 2020-2021

- Improving the efficiency of cassava growing: The Bank for Agriculture and Agricultural Cooperatives has been tasked with allocating credit to be used to invest in the development of cassava growing and to find ways to use technology to improve the efficiency and reduce the costs of this. To this end, 5,000 loans of up to THB 230,000 have been made available (with a total value of THB 1.15 billion) at an annual interest rate of 6.50% and to be repaid over not longer than 5 years. However, growers will be responsible for paying interest rates of only 3.50% per year, with the government contributing the additional 3% for a period of up to 24 months (this ending no later than 30 September, 2023). The project will run from 1 October, 2020 to 31 October, 2023. Budget allocations for this total THB 69 million.

- Providing credit to farming associations that are collecting and adding value to cassava stocks: The Bank for Agriculture and Agricultural Cooperatives is also providing loans to farming groups (farming cooperatives, groups and community enterprises) that are active in the cassava industry and that intend to use these funds as working capital to pay for the building of stocks of fresh cassava or cassava chip that will then be distributed or processed. This plan has been put in place to try to soak up the excess supplies of cassava that are currently weighing on the market, and provides for total funding of THB 1.5 billion, with loans repayable at an annual interest rate of 4%. Of this, the borrower will be responsible for 1%, with the government paying the additional 3% interest for up to 12 months (no later than 31 May, 2022). The program will run from 1 October, 2020 to 30 June, 2022 at a cost of THB 45 million.

- Interest compensation for holders of cassava stock: This scheme will support the extension of credit to cassava processors (operators of collection yards and processing plants) that hold stocks of fresh cassava or cassava chip for a period of 60-180 days. The government will pay interest compensation to these players at a rate of 3% per year at a total cost of THB 225 million, drawn from the farmers assistance fund.

- Managing imports and exports: The Department of Foreign Trade should put in place measures to ensure that the quality of goods meet established standards and that there is strict enforcement of these rules.

Joint Standing Committee on Commerce, Industry and Banking (JSCCIB) guidelines that are relevant to the cassava industry

1) Declaring cassava holdings: Business operators, owners and individuals who have monthly cassava holdings of more than 15 tonnes are required to report their purchases (the type of goods bought and the prices paid), the distribution prices, their current holdings, the quantities bought, distributed, received, used and remaining and the storage location of these, and to keep full inventory records.

2) The transportation of cassava: The transportation of loads of cassava or cassava chip weighing over 10 tonnes into or out of 12 specified provinces is prohibited without the permission of the chair of that province’s JSCCIB or of an authorized representative.

3) Regulations for making purchases of cassava and for displaying purchase prices for goods with a particular starch content: If operators of collection yards, starch processors and ethanol distillers discover that cassava being sold has a lower starch content than specified, they are permitted to reduce their purchase price by up to THB 0.05/kilogram/1% of lower starch content. Conversely, if the cassava has a starch content that is higher than that specified, they may increase their purchase price at the same rate.

4) Adding cassava varieties to the list of controlled goods: To prevent or halt the spread of cassava mosaic disease, the transportation of cassava into and out of areas affected by the disease is strictly controlled. The relevant authorities will be responsible for either requiring that permission be sought by those wishing to move cassava in and out of affected locations or of banning this entirely.

Krungsri Research’s view

Overall, players in cassava supply chains will benefit from favorable business conditions in downstream industries on domestic and overseas markets, and this will then support increases in income for many in the industry.

- Producers of cassava chip: Turnover will tend to rise on stronger sales in China, where cassava chip is used as an input (among others) into ethanol production and consumption remains strong and stable in downstream industries. At the same time, outputs and stockholdings weakened substantially in the recent past, and this presents operators with much better opportunities for profits. However, exporters remain highly dependent on the Chinese market, leaving them exposed to any changes in demand or purchases there, while competition for Chinese market share is also rising from the CLMV region.

- Producers of cassava pellets: Uncertain demand and the continuing sluggishness in export markets (especially in Europe, which used to be the main purchaser of cassava pellets) means that manufacturers are exposed to significant risk.

- Producers of native starch: Turnover will tend to rise with stronger consumption on domestic and overseas markets. This will be thanks to an improving outlook for food and drinks processors and ethanol distillers.

- Producers of modified starch: Turnover should rise on an expansion in downstream industries in Asia, including cosmetics, food and medicine, together with a broadening of exports into new markets. On the downside, producers may also face stronger competition from starches produced from other sources that have a wider range of desirable qualities.

- Traders in cassava products: Traders will be able to maintain turnover at normal levels. It is expected that demand for cassava from domestic and export markets will grow steadily and this will allow operators to remain in profit.

- Cassava growers: Income are expected to rise with higher purchase prices for fresh cassava, while production costs will tend to hold steady and demand from industrial consumers will strengthen. Farmers are also being supported by the government, which is attempting to preserve stability in the cassava industry by establishing a guaranteed income scheme, low-interest loans and measures to absorb excess supply. As such, cassava growers will have the opportunity of earning rising profits over the coming period.

[1]In Asia, cassava is used principally as an input to downstream industries, rather than for consumption. However, many countries have been moving to strengthen their food security, especially India, Indonesia and the Philippines, and in these countries, cassava has been promoted as an alternative to rice, while in Latin America, governments have pushed the commercial cultivation of cassava mainly for use as an input to industry.

[2]Data is from the Office of Agricultural Economics. Cassava can be grown in poor soils and is drought tolerant so it can be planted year-round, although in Thailand planting usually occurs between March and May for harvest in the period from January to March the following year.

[3]Data correct as of 2 July 2021, though this does not include unregistered businesses, those that may have suspended or ceased operations, or those that have a size as determined by the Factory Act (No. 2). The data includes cassava processing facilities that output products including pellets, chips, starch, pulp and other goods (source: Department of Industrial Works).

[4]Modified starch is made from native starch that has its physical and chemical properties altered through the application of heat, enzymes and/or chemicals. This gives the modified starch particularly desirable qualities that then make it more useful in industrial applications, such as making its viscosity less variable, increasing its stability at a wider range of temperatures, and altering its acidity and shear strength.

[5]Equivalent to 5.5 million tonnes of fresh cassava root.

[6]Producing 1 liter of ethanol requires 6.25 kilograms of fresh cassava root.

[7]Producing 1 kilogram of cassava chips or pellets requires 2.42 kilograms of fresh cassava root.

[8]Producing 1 kilogram of cassava starch requires 4.20 kilograms of fresh cassava root.

[9]The reform of the Common Agricultural Policy (CAP) that was carried out in 2005 encouraged member states to increase the area given over to crops that could be used as alternatives to imported cassava. In addition, prices for these were also low, and as such, EU-based producers of animal feed switched from using cassava pellets to different products, most notably potatoes.

[10]To produce a nutrient profile similar to corn, animal feed is made by mixing cassava chip and soy pulp at a ratio of 87:13.

[11]The result of reform of the EU Common Agricultural Policy was to encourage Thai exporters of cassava pellets to switch to the manufacture of cassava chip.

[12]In 2020, cassava production costs came to THB 1.83 per kilogram.

[13]Chinese players have invested in cash crop growing and basic processing facilities in countries including Cambodia (rubber, acacia, cassava and sugarcane), Lao PDR (rubber, sugarcane, corn for animal feed, bananas, cassava, teak and eucalyptus, with most investments being made in the north of the country in areas close to the Chinese border) and Myanmar (rubber, cassava, sugarcane, bananas and watermelons). Source: Chinese Agriculture in Southeast Asia: Investment, Aid and Trade in Cambodia, Laos and Myanmar.

.webp.aspx)