Industry Horizon (เมษายน 2569)

22 เมษายน 2569

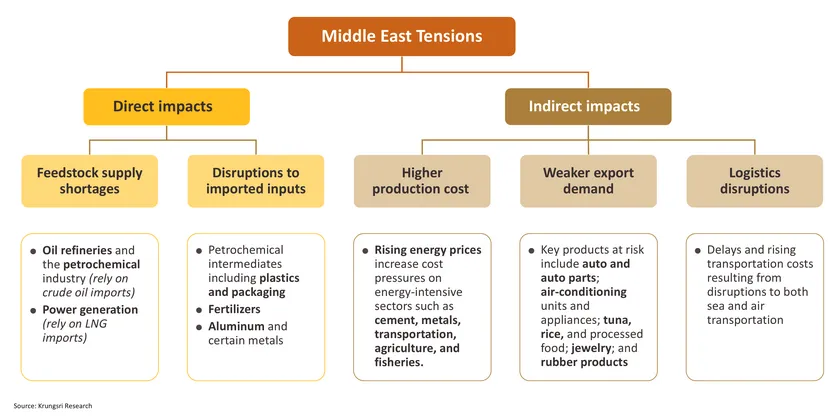

Middle East tensions are driving direct and indirect impacts across Thai industries.

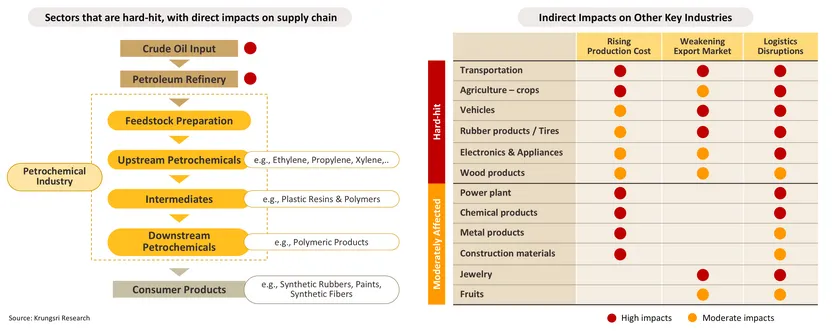

Sectoral Impact: Hard-Hit vs. Moderately Affected Industries

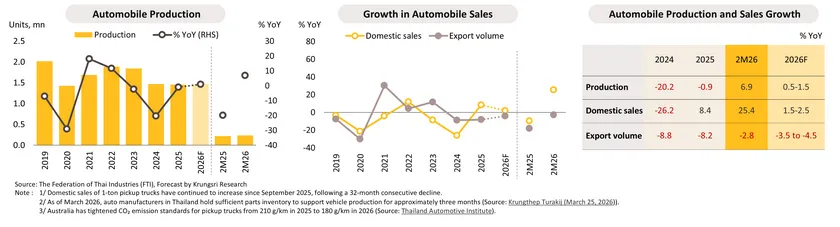

Automobile: Production and sales are expected to slow for the rest of the year, reflecting the Middle East conflict, U.S. tariff measures, and stricter environmental standards.

-

In 2M26, production rose by 6.9% YoY to 236,338 units, supported by a 41.6% YoY increase in BEV passenger car output to 5,533 units, driven by higher compensation production requirements under the EV 3.5 scheme (raised to 2–3 times). Domestic sales grew by 25.4% YoY to 122,178 units, underpinned by a surge in BEV passenger car registrations (+228.1% YoY in January 2026, the final month eligible for subsidies under the EV 3.0 scheme). Additional support came from a 5.0% YoY increase in 1-ton pickup sales, rebounding from a low base1/, partly due to improved hire-purchase loan approvals amid declining auto loan NPLs and SMLs. Meanwhile, exports declined by -2.8% YoY to 139,600 units, weighed down by softer global demand amid economic uncertainty, as well as stricter environmental and vehicle safety standards in some trading partners, which limited exports of certain models that do not meet regulatory requirements.

-

For full-year 2026, production is projected to grow by 0.5–1.5%, though growth is expected to moderate in the remainder of the year, due to a decline in ICE vehicle output amid the transition toward electric vehicles and rising global energy cost concerns among consumers. Additional risks include potential shortages of automotive components and rising parts costs2/, due to disruptions in the Strait of Hormuz. Domestic sales are projected to grow by 1.5–2.5%, partly supported by rising EV adoption driven by higher fuel costs and the planned vehicle trade-in scheme in 2026. However, overall growth is expected to moderate due to the impact of Middle East tensions on economic activity, a decline in tourist arrivals, and persistently high household debt weighing on purchasing power. Meanwhile, exports are projected to contract by -3.5% to -4.5%, pressured by weaker consumer demand in the Middle East—which accounted for 21% of Thailand’s total auto exports in 2025—as well as the impact of U.S. tariff measures and stricter environmental standards in Australia3/, Thailand’s largest pickup export market. Nevertheless, BEV exports are expected to benefit from revised BOI criteria allowing one EV produced for export to be counted as 1.5 units of compensation production.

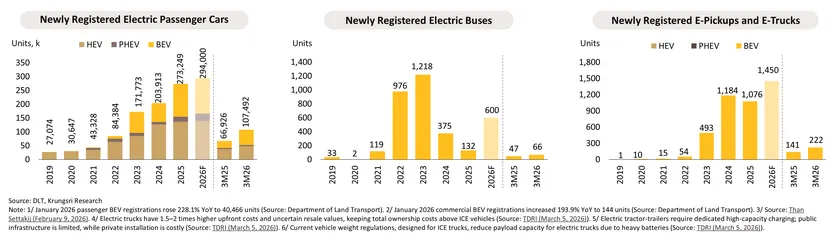

Electric Vehicles: BEVs are expected to gain from high fuel costs, while HEVs and MHEVs will be supported by reductions in excise tax rates.

-

In 3M26, new registrations of passenger XEVs rose by 60.6% YoY to 107,492 units, driven by passenger BEVs (+121.5% YoY), HEVs (+26.8% YoY), and PHEVs (+1.8% YoY). Growth was supported by a surge in BEV registrations in January 20261/, the final month for domestically produced BEVs to qualify for subsidies under the EV 3.0 scheme, as well as new model launches, particularly by leading Chinese and Japanese manufacturers in Thailand. New registrations of electric buses increased by 40.4% YoY to 66 units, partly reflecting a new procurement cycle by the Bangkok Mass Transit Authority following the 2022–2023 peak. Meanwhile, commercial BEV registrations rose by 57.5% YoY to 222 units, supported by a spike in pickup BEV registrations in January 20262/ to meet EV 3.0 requirements.

-

In 2026, new registrations of passenger XEVs are projected to reach 294,000 units, accounting for 69.0% of total passenger car sales, supported by (i) higher oil prices, prompting a shift from ICE vehicles to BEVs and larger-battery PHEVs; (ii) reduced excise tax rates for HEVs and mild hybrids (MHEVs) (6–9%); (iii) increased BEV supply driven by stricter compensation production requirements (2–3 times prior imports), alongside new model launches with improved technology and driving range; and (iv) intensified dealer promotions to clear inventories. However, rising BEV prices following the end of import incentives under the EV 3.5 scheme in 2025 may weigh on market growth. Electric bus registrations are expected to increase to 600 units, supported by a new procurement plan for 1,520 electric buses during 2026–20323/, aimed at replacing ICE buses amid higher fuel costs. Meanwhile, commercial BEV registrations are projected to reach 1,450 units, driven by logistics operators shifting to electric light trucks to reduce fuel costs. However, adoption of heavy-duty electric trucks remains constrained by unclear commercial viability4/, limited infrastructure readiness5/, and restrictive payload regulations6/.

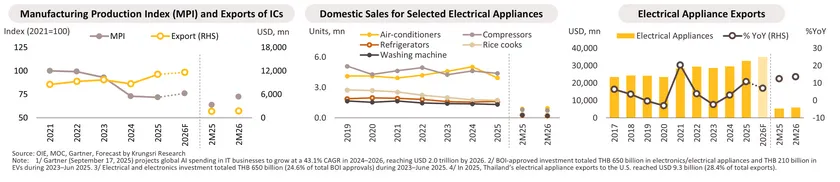

ICs and Electrical Appliances: Exports continue expanding, supported by the ongoing global upcycle, despite headwinds from Middle East tensions and U.S. tariff measures.

Situation in 2M26

-

Integrated Circuits (ICs): Production and exports grew by 13.6% YoY and 8.6% YoY, respectively, supported by sustained chip demand from electrical appliance manufacturing, EV production, and global AI infrastructure, alongside a -29.9% YoY decline in IC inventories. The rise in production was also partly driven by a low base effect in the previous year. However, domestic production growth remains pressured by imported chips, reflected in a sharp increase in chip imports from Taiwan (+282.3% YoY) and China (+28.9% YoY).

-

Electrical appliances: Domestic sales declined by -7.7% YoY, as consumers delayed appliance purchases due to weakened purchasing power and subdued spending confidence amid a still-fragile domestic economic recovery. This was partially offset by air conditioner sales (accounting for around 50% of total market value, the highest in the segment), which increased by 6.7% YoY from a low base in the previous year, supported in part by periods of elevated temperatures in Thailand. Meanwhile, export value rose by 13.6% YoY, supported by a new global replacement cycle for electrical appliances following the peak during the COVID-19 period.

2026 Outlook

-

ICs: MPI and export value are projected to grow by 5.5–6.5% and 4.0–5.0%, respectively, supported by (i) continued expansion of the global AI1/ and data center sectors, driving demand for processing and memory chips; and (ii) investment in domestic midstream and downstream industries that use ICs as key inputs2/, particularly XEV production, where OEMs are required to adopt locally produced key components starting from 2026 onward. However, IC production may face risks from supply chain disruptions stemming from Middle East tensions, tightening export controls on rare earths and critical minerals by China, and the impact of higher U.S. import tariffs.

-

Electrical appliances: Domestic sales are projected to decline by -7.0% to -8.0%, reflecting weak purchasing power, particularly among lower- to middle-income consumers. Key headwinds include Middle East tensions and U.S. tariff measures affecting business activity, high household debt, declining tourist arrivals, and rising living costs. This is partly offset by a shift toward energy-efficient air conditioner replacements among upper-middle-income consumers, driven by hotter weather linked to El Niño and rising electricity costs. Meanwhile, the export value is expected to grow by 6.5–7.5%, supported by the global upcycle in electrical appliances and continued investment in Thailand’s electrical and electronics sector3/, though growth may be tempered by U.S. tariff measures, given the U.S. remains Thailand’s largest trading partner4/.

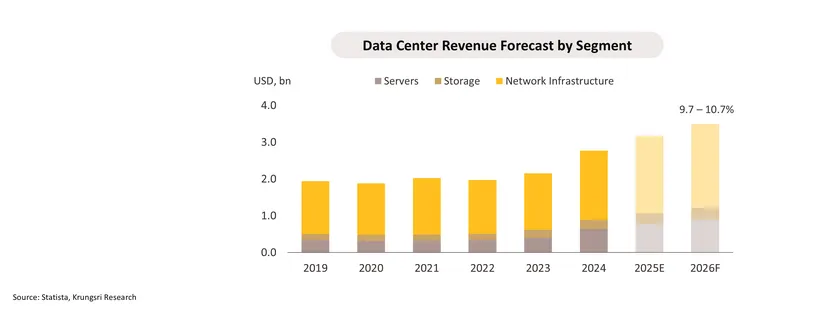

Data Center: Total revenue continues to grow strongly, supported by AI-driven demand for network infrastructure, and servers & data storage systems.

-

Throughout 2025, a total of 36 data center investment promotion applications were submitted to the Board of Investment (BOI), with a combined value of THB 728 billion—more than double the level recorded in 2024. This surge, supported by the expansion of the digital economy and rising demand for AI infrastructure, is expected to sustain industry momentum, with data center revenue projected to grow by 14.0–15.0% in 2025. Reinforcing this positive outlook, the BOI approved seven additional data center projects in January 2026, with a total value exceeding THB 96 billion, highlighting the sector’s strong long-term growth potential.

-

Looking ahead to 2026, total data center industry revenue is forecast to grow by 9.7–10.7%, driven by three key segments: (i) Network Infrastructure — Revenue is projected to expand by 7.5–8.5%, supported by rising internet usage and the continued rollout of 5G networks by domestic service providers. Increased investment from foreign technology firms is also expected to accelerate digital infrastructure development. (ii) Server Systems — Revenue is expected to grow by 15.4–16.4%, underpinned by strong demand for AI and cloud computing from both consumers and enterprises. This is driving investment in high-performance servers capable of handling intensive workloads. (iii) Data Storage Systems — Revenue is anticipated to increase by 9.9–10.9%, fueled by rapid growth in data generation from AI adoption, as well as expanding e-commerce and e-payment platforms. This will intensify competition among operators to invest in greater storage capacity, enhanced data security, and faster data processing.

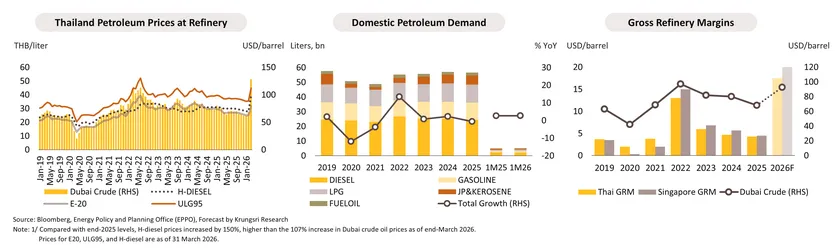

Refinery: Refining margins are expected to trend upward, driven by disruptions at several refined oil production facilities in the Middle East.

-

In 1Q26, gross refinery margins (GRMs) rose significantly above the 2025 average, despite higher crude costs driven by escalating Middle East tensions and the closure of the Strait of Hormuz—a key route for roughly one-third of global seaborne crude—tightening supply and pushing Dubai crude to USD 128.5 per barrel in late March. At the same time, disruptions to refined product supply from drone attacks on refining facilities in the UAE, Saudi Arabia, and Bahrain tightened market conditions. As a result, refined product prices in March increased at a faster pace than crude prices1/. These dynamics provided strong tailwinds for Thai refiners, boosting margins and generating inventory gains. Meanwhile, domestic demand for refined products continued to grow from 2.6% YoY (January 2025) and is expected to accelerate further in March, supported by precautionary stockpiling amid ongoing geopolitical tensions.

-

For the remainder of 2026, Thai refiners are expected to continue benefiting from elevated refining margins, supported by persistent supply tightness. This reflects prolonged disruptions to refining infrastructure in the Middle East, where repairs are likely to take 3–5 years, keeping regional refined product spreads above crude prices. As a result, Thailand’s GRMs are projected to average USD 15–20 per barrel in 2026, up significantly from USD 5.9 in 2025. However, should the situation escalate into a prolonged full-scale conflict, it could turn into a downside risk for Thai refiners. Production costs would rise sharply once lower-cost inventories are depleted, while increasing risks of global and domestic stagflation could constrain refined product prices amid weakening energy demand. This would likely compress refining margins over time.

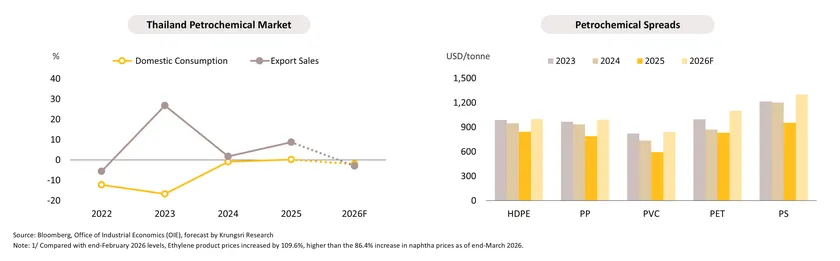

Petrochemical: Petrochemical product spreads broadly increased, supported by tighter supply following multiple plant shutdowns caused by the Middle East conflict.

-

In 1Q26, petrochemical spreads for products such as HDPE, PP, and PET widened in March. As the Hormuz Strait handles around 37% of global seaborne naphtha trade, petrochemical producers—particularly in Asia, which heavily relies on Middle Eastern feedstock—faced acute supply disruptions. This forced naphtha-based producers in Japan, Singapore, Indonesia, and Thailand to declare force majeure and temporarily halt operations, tightening regional supply and driving product prices to rise faster than feedstock costs1/. Gas-based olefin producers were the main beneficiaries, as they are less dependent on naphtha and could fully capture the upside from higher product prices.

-

For the remainder of 2026, the petrochemical sector is expected to benefit from sustained high spreads, driven by ongoing supply tightness after multiple plant disruptions in the Middle East (notably Iran, the UAE, and Bahrain). However, supply constraints are likely to persist even if tensions ease in 2H26. Under a base case of contained conflict, petrochemical demand and exports are projected to contract by -2% to -3% in 2026, amid a slowing global economy, feedstock shortages, and logistics disruptions. In a full-scale escalation scenario, rising feedstock costs and weak demand would limit cost pass-through, potentially triggering widespread shutdowns and pressuring profitability and supply chain stability. Structural challenges remain, including (i) stricter environmental policies (e.g., single-use plastic bans), (ii) ongoing oversupply from capacity expansions in China and the Middle East, and (iii) inflows of low-cost Chinese plastic products into Thailand.

Construction: Total construction investment in 2026 is expected to see modest growth, constrained by higher energy costs and delays in budget disbursement.

-

In 2025, total construction investment grew 6.5% to THB 1.5 trillion, driven by an 11.7% increase in public construction (THB 920 billion), particularly infrastructure (+14.3%), amid accelerated disbursement for large pre-approved transport projects. In contrast, private construction declined -0.8% to THB 580 billion, weighed by a -2.5% contraction in residential construction (49% of private investment) due to weak purchasing power and tighter mortgage approvals. Non-residential construction (e.g., offices, commercial buildings, and industrial facilities) rose marginally by 0.9%, with activity concentrated in strategic locations, especially the EEC, supporting investment in target industries.

-

In 2026, total construction investment is projected to grow modestly at 1.0–1.5%, with public investment continuing to outpace private. Headwinds from the Middle East conflict are expected to push up energy prices—particularly oil and natural gas—raising construction material and transport costs. This will increase contractor costs amid still-uncertain demand, putting pressure on margins, especially for contracts signed before the rise in costs. Some projects may also face delays or postponements.

-

Public construction: Investment value is expected to grow modestly at 1.0–1.5%, partly due to delays in approvals and budget disbursement for new projects in the first half amid the formation of a new government. Nevertheless, some previously approved projects have already commenced construction, with accelerated disbursement supporting ongoing investment.

-

Private construction: Investment value is projected to grow by 0.5–1.0%, supported by non-residential construction. Residential construction is expected to continue contracting from the previous year, weighed by high household debt and rising energy and goods prices that constrain purchasing power. On the supply side, elevated inventory levels are likely to limit new project development.

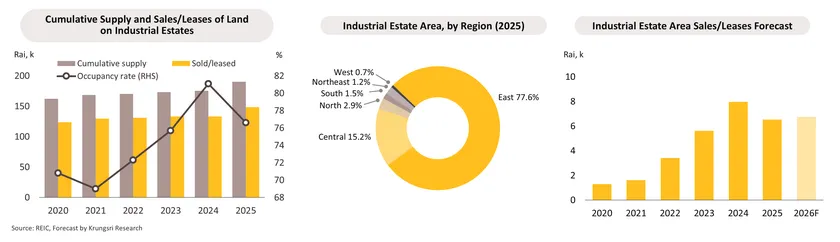

Industrial Estate: Sales and leases are expected to expand in line with investment relocation, though growth will remain concentrated in key strategic locations.

-

In 2025, 10 new industrial estates were established—8 in the Eastern region, 1 in the Central region (including Bangkok and its vicinity), and 1 in the North—adding a total of 13,819 rai. This brings the nationwide total to 82 estates, covering approximately 191,000 rai. The Eastern region remains dominant, accounting for around 78% of total industrial estate land (about 148,000 rai). Land sales and leases totaled 6,531 rai, declining by -18.0% amid economic uncertainty, U.S. tariff hikes weighing on investment sentiment, and a high base effect. Activity remained heavily concentrated in the Eastern region at 6,152 rai (94% of total), down -14.4%, bringing the occupancy rate to 76.6%, from 81.1% in 2024.

-

In 2026, industrial land sales and leases are expected to grow, supported by ongoing investment relocation to ASEAN, including Thailand, amid heightened global trade tensions. Thailand continues to benefit from its strategic location, well-connected logistics infrastructure, and progress in the Eastern Economic Corridor (EEC), alongside the development of smart industrial parks, which enhance long-term investment appeal. This is consistent with strong growth in investment promotion approvals and certificates in the Eastern region, rising by 60.3% and 57.2% in 2025, indicating continued investment momentum. However, growth is likely to remain constrained by prolonged Middle East tensions and elevated energy and logistics costs, which may delay investment decisions for some investors. Nevertheless, direct impacts from Middle Eastern investors remain limited, given their small share of total investment applications in 2025 (nine projects worth THB 1.6 billion, compared to 2,421 projects totaling THB 1.36 trillion). As a result, sales and leases are projected to recover to around 6,750-6,800 rai in 2026, expanding by approximately 3.0–4.0%, partly reflecting a high base in the previous year.

Housing (BMR): Demand is expected to remain subdued, pushing sales to a 23-year low.

-

In 2M26, newly launched residential supply declined by -8.8% YoY to 5,706 units. The contraction was primarily driven by a drop in condominium and townhouse launches, which fell by -16.4% YoY and -15.3% YoY, respectively. In contrast, detached house launches surged by 83.7% YoY, particularly in the mid- to high-end segment (THB 10 million and above), driven by developers’ focus on high-net-worth buyers who continue to exhibit strong purchasing power and maintain relatively better access to mortgage financing. Sales of newly launched units totaled 1,065 units, falling -51.1% YoY. This decline was attributed to the condominium segment, which dropped sharply by -59.7% YoY, particularly for units priced below THB 3 million. This segment remains constrained by elevated mortgage rejection rates, driven by persistently high household debt levels. In contrast, sales of townhouses and detached houses continued to expand, rising by 58.6% YoY and 14.3% YoY, respectively. This divergence highlights a market increasingly supported by real end-user demand, with buyers purchasing for owner-occupation remaining relatively resilient amid the ongoing economic slowdown.

-

For the remainder of 2026, housing demand in the BMR is expected to see limited growth, weighed down by: (i) a significant slowdown in domestic purchasing power amid economic uncertainty and rising living costs, particularly driven by surging energy prices; and (ii) a decline in foreign demand due to the Middle East conflict, coupled with a substantial increase in travel costs, which is likely to hinder site visits and property transfers. However, a segment of high-net-worth individuals (HNWIs), particularly from Israel and the Middle East, is expected to enter the market in search of safe-haven assets. This “safe-haven demand” is expected to provide increasing support to the luxury1/ condominium segment. Consequently, developers are expected to shift their focus toward mid- to high-end residential projects, while delaying new project launches to manage cash flow and existing inventory. In 2026, newly launched residential supply is projected to decline by -2.7% YoY to 36,000 units, marking a 23-year low and falling below the annual average of 60,000 units recorded during the pandemic period (2020–2021). Total residential sales are also forecast to decrease by -1.2% YoY to 46,000 units, likewise, reaching their lowest level in 23 years.

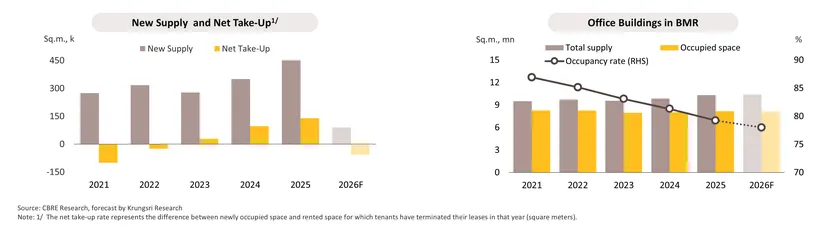

Office Building (BMR): Occupancy rates will decline further amid a weakening Thai economy and rising hybrid work adoption, driven by higher energy costs.

-

In 2025, office demand improved compared to 2024, as reflected in a 44.9% increase in net take-up to 140,000 sq.m. This growth was partly driven by relocation to higher-quality buildings, as well as the implementation of return-to-office policies. As a result, occupied space increased by 1.9% to 8.2 million sq.m. On the supply side, new office supply increased by 37.3% from 2024 to over 470,000 sq.m., driven by the completion of several new projects, the majority of which are Grade A and A+ buildings. This pushed total accumulated supply up by 4.6% to 10.3 million sq.m. However, as supply continued to outpace demand, the occupancy rate declined to 79.2%, down from 81.3% in 2024.

-

In 2026, the office rental market is expected to face continued pressure from a prolonged oversupply and spillover effects from the conflict in the Middle East. The Thai economy is projected to grow below 2.0%, slowing from 2025, amid ongoing uncertainties surrounding the conflict, which have continued to drive up energy prices. At the same time, weakening domestic purchasing power has led some business sectors to delay or postpone new investments. Combined with rising energy costs, companies are increasingly adopting hybrid work models to reduce operating expenses. As a result, occupied space is expected to remain flat or decline slightly by -0.7% from 2025. On the supply side, new office supply is expected to enter the market at a slower pace, in line with developers’ investment plans, with approximately 90,000 sq.m. scheduled for completion (+0.9% from 2025). As a result, the occupancy rate is projected to fall further to 78.0%, further strengthening tenants’ bargaining power. Close monitoring of the Middle East conflict remains essential, as it poses downside risks to both demand and supply. Businesses, including multinational corporations (MNCs), may delay leasing new space to control costs. At the same time, rising construction costs are likely to delay project timelines, affecting developers’ planned construction and project launches.

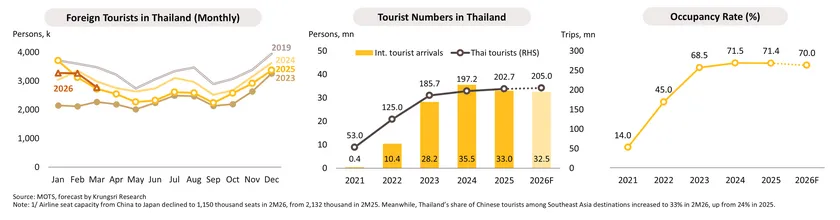

Hotel: International arrivals will decline slightly, constrained by Middle East tensions and high travel costs, with a partial China recovery weighing on occupancy.

-

In 1Q26, international tourist arrivals continued to decline by -2.4% YoY, totaling 9.5 million visitors. Chinese arrivals began to recover (+11.8% YoY), partly driven by a shift in travel preferences after China’s Ministry of Foreign Affairs advised its citizens to avoid travel to Japan (November 2025). This led some Chinese tourists to opt for Thailand instead in early 20261/ (with Chinese arrivals to Japan falling -37.8% YoY during December 2025–January 2026). The rebound was further supported by Thailand’s enhanced safety standards (Bangkokbiznews, Feb-26). Meanwhile, Malaysian arrivals continued to contract (-16.9% YoY), weighed down by weaker purchasing power amid Malaysia’s economic slowdown, higher travel costs, and flooding in southern Thailand, as well as a high base last year. In contrast, arrivals from India (+15.0% YoY) and Russia (+0.5% YoY) continued to expand. Domestic tourism during 2M26 increased by 2.2% YoY to 34.9 million trips, while the occupancy rate rose slightly to 76.9%, up 0.2 ppt YoY.

-

Throughout 2026, international tourist arrivals are expected to decline slightly from the previous year, driven by several headwinds: (i) prolonged geopolitical tensions in the Middle East, which constrain flight routes and frequencies, raise travel costs, and heighten safety concerns—particularly among long-haul travelers from Europe, Russia, and the Middle East, which collectively accounted for 27% of Thailand’s total international arrivals in 2025; (ii) the ongoing U.S.–China trade war, which continues to weigh on Chinese consumer confidence, thereby slowing the recovery of the Chinese outbound market; and (iii) intensifying competition from peer destinations, particularly Vietnam, which has been actively promoting tourism to attract Chinese visitors. Despite growth potential in certain markets, such as South Asia—especially India—total international arrivals in 2026 are projected to reach approximately 32.5 million, representing a -1.4% decline. Meanwhile, domestic tourism is expected to reach around 205 million trips, increasing modestly by 1.1%, supported by continued government stimulus measures. However, rising travel costs and weaker spending confidence remain key challenges. As a result, the nationwide hotel occupancy rate is expected to decline slightly to 70.0%, from 71.4% in 2025.

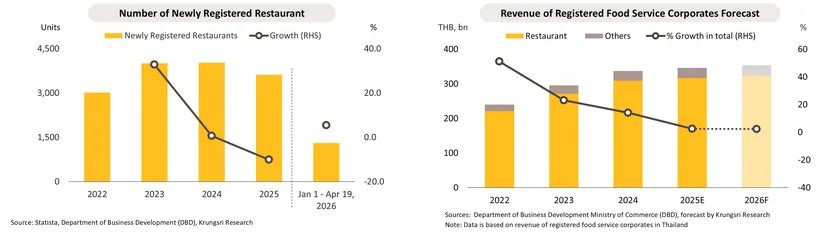

Restaurant: Revenue will grow slightly, as weak purchasing power, slow tourist recovery, intensifying competition, and elevated costs continue to weigh on the sector.

-

Revenue in the food and beverage service sector is expected to grow at a slower pace in 2025, expanding by only 2.0–3.0%, down sharply from 14.2% in 2024, largely due to a decline in foreign tourist arrivals. On the supply side, the number of registered and active restaurants rose by 6.0% to 29,579 outlets, although growth is moderating as new entrants declined by -10.2% to 3,616. According to the Department of Business Development (DBD), from January 1 to April 19, 2026, new registrations grew by 5.4% YoY, while registered capital declined by -10.9% YoY. This implies that these new entrepreneurs are smaller operators with limited registered capital, amid growing concerns among operators over weak purchasing power and high household debt, which continues to suppress per-visit spending. Intensifying competition and rising input costs—driven by the Middle East conflict—are further pressuring profitability.

-

2026 Outlook: Revenue is projected to grow at a slower pace of 1.8–2.8%, weighed down by (i) weakened consumer confidence and purchasing power amid economic uncertainty and elevated living costs linked to Middle East tensions, and (ii) lower-than-expected foreign tourist arrivals, constrained by high travel costs, limited flight capacity, and safety concerns. While the easing of alcohol sale time restrictions (a 180-day trial measure effective since early December 2025) is expected to provide some support, its overall impact on demand remains limited. Moreover, intensifying competition, coupled with increasingly value-conscious consumer behavior, will continue to exert downward pressure on prices and margins. The mid-tier segment is expected to be severely affected by (i) price reduction competition from high-end and hotel restaurants, (ii) value-based competition from mid-to-low tier markets, and (iii) investment expansion by new large-scale capital groups into the mid-tier market using pricing strategies to seize market share from existing players.

Private Hospital: Prolonged Middle East conflict poses downside risk to international patient revenue.

-

In 1Q26, revenue growth softened due to two main factors. (i) Domestic patients became more cautious in their spending, including spending on healthcare, as reflected by consumer confidence remaining around 50 amid a slowing Thai economy and rising living costs. This led some patients to shift to lower-cost public hospitals. (ii) International patient volumes declined due to the Ramadan period, which dampened travel by Muslim patients, compounded by the escalation of Middle East conflicts in early March. This particularly affected hospitals with a high reliance on Middle Eastern patients.

-

For the remainder of the year, revenue is expected to continue slowing, driven by fragile consumer purchasing power amid persistently high living costs and heightened uncertainty surrounding both the Thai and global economic outlook. At the same time, rising medical costs are likely to push up treatment expenses. Prolonged conflict in the Middle East could further pressure international patient revenue due to significantly higher travel costs and travel restrictions within the region. However, hospitals with a well-diversified revenue mix between self-pay patients and those covered by the social security scheme are expected to partially cushion the impact on performance, as social security income remains relatively stable and predictable, helping to mitigate earnings volatility during periods of economic weakness. In 2026, the business is expected to record revenue growth of around 2.0–3.0%.

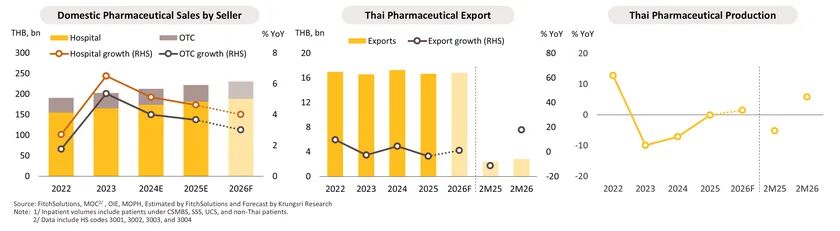

Pharmaceuticals: Production will grow modestly, supported by the domestic hospital market, amid the Middle East conflict which is driving up production costs.

-

In 2M26, domestic production rose by 5.8% YoY, driven by liquid formulations (+12.9% YoY) and tablets (+9.7% YoY), in line with stockpiling to meet anticipated growth in domestic pharmaceutical consumption. This was supported by continued drivers from 2025, including (i) seasonal disease outbreaks, such as influenza (+54.4%), and an increase in non-communicable disease (NCD) cases, namely hypertension (+4.9%) and diabetes (+4.8%), along with a rise in inpatient volumes across 13 health regions nationwide1/ (+3.4%); and (ii) government policies expanding healthcare coverage and access, enabling greater utilization of healthcare services and medicines. Export value also increased by 17.7% YoY, supported by demand from Asian markets such as Vietnam, the Philippines, and Japan, in line with ageing population trends.

-

In 2026, production is projected to grow modestly by 1.0–2.0%. Growth will be primarily driven by the domestic market, which is expected to expand by 3.0–4.0%, led by hospital demand (3.5–4.5%) and supported by over-the-counter (OTC) sales (2.5–3.5%). Key drivers include: (i) the continued rise in NCDs, particularly among the ageing population, and pollution-related illnesses; (ii) expanded healthcare coverage and improved access to medicines; and (iii) the wellness and longevity trend, supporting demand for preventive care and drugs for weight control, especially among middle- to high-income consumers. However, production may be affected by supply disruptions to petrochemical-based inputs due to ongoing Middle East tensions. In addition, domestic consumption is expected to slow slightly (from 3.5–4.5% in 2025) due to weakening purchasing power amid economic conditions and higher drug prices stemming from the Middle East conflict, which has raised import and input costs. This may lead consumers to cut back on non-essential medicines and expensive imports. Export value is expected to remain broadly flat from a low base, constrained by fragile global demand despite support from ageing demographics.

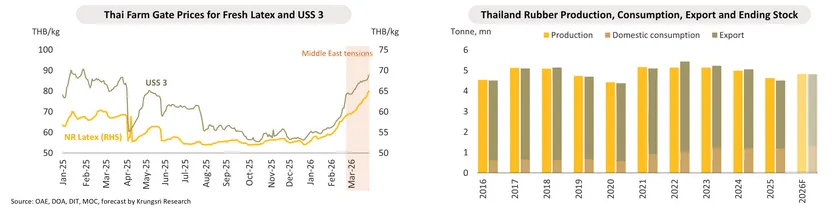

Rubber: Production and exports will expand on favorable weather and stockpiling demand, while Middle East conflicts remain a key headwind to demand, costs, and logistics.

-

Over 2M26, the natural rubber output index grew 1.3% YoY, primarily supported by favorable weather conditions that improved overall yields. However, weak economic conditions in overseas markets weighed on purchasing power and downstream industrial demand, resulting in export volumes declining to 0.8 million tonnes (-5.1% YoY). The contraction was mainly driven by Technically Specified Rubber (TSR), which fell to 239.0 thousand tonnes (-22.3% YoY), and concentrated latex, which declined to 122.6 thousand tonnes (-15.1% YoY). Meanwhile, other intermediate rubber products continued to expand, supported by demand from the automotive and auto parts industries, particularly in China and Japan.

-

Full-year natural rubber production is projected to expand by 3.9-4.9%, supported by: (i) generally favorable weather conditions despite sooner-than-expected El Niño; (ii) the gradual output contribution from newly planted areas expanded during 2003-2013; and (iii) stronger incentives for farmers to accelerate harvesting in line with rising rubber prices, consistent with the upward trend in global crude oil prices. Export volumes are likewise expected to increase by 4.5-5.5%, driven by: (i) restocking demand for raw materials in downstream industries, including automotive, tires, components, and medical equipment; and (ii) tight global supply conditions, as key competitors such as Indonesia and Malaysia continue to face persistent leaf fall disease affecting output. Nevertheless, Thailand’s processed rubber industry remains exposed to multi-dimensional risks from prolonged geopolitical tensions, particularly in the Middle East. Key risks include: (i) potential weakening of purchasing power in key trading partner markets, which may dampen downstream industry growth; (ii) an upward trend in global crude oil prices, adding pressure to production costs despite higher rubber prices in line with oil prices; (iii) disruptions to logistics and maritime transport, particularly from a potential closure of the Strait of Hormuz, leading to delays in shipments to Middle Eastern markets, although Thailand’s direct rubber product exports to the region remain limited (accounting for 1.8% of total export volume in 2025); and (iv) payment and financial transaction risks for exporters with direct exposure to Iranian counterparties.

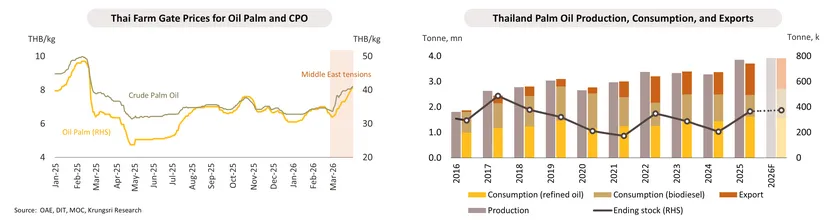

Palm Oil: Domestic sales are expected to grow on higher biodiesel blending, while exports may decline due to restrictions prioritizing domestic energy demand.

-

In 2M26, the volume of fresh fruit bunches (FFB) increased to 2.8 million tonnes (+76.3% YoY), primarily driven by favorable weather conditions. This resulted in a crude palm oil (CPO) output of 530.8 thousand tonnes (+92.6% YoY). Meanwhile, distribution accelerated significantly as domestic consumption rose to 391.2 thousand tonnes (+19.1% YoY), following utilization in the biodiesel production sector of approximately 135.7 thousand tonnes (+6.5% YoY) and the production of refined palm oil at around 255.5 thousand tonnes (+27.0% YoY). Exports surged to 133.4 thousand tonnes (+651.2% YoY), driven by stronger demand from key trading partners, palm oil’s price competitiveness relative to other vegetable oils, and government measures to reduce domestic stockpiles.

-

In 2026, oil palm production is projected to expand by 1.3-2.3%, supported by: (i) favorable weather conditions and temperatures, (ii) continued expansion of cultivated areas, together with the maturing of oil palm trees planted in 2023, and (iii) relatively attractive price levels, which continue to incentivize farmers to maintain plantations and sustain harvesting activities. The increase in fresh fruit bunch output is expected to drive crude palm oil (CPO) production growth of 1.1-2.1%. Meanwhile, domestic CPO demand is projected to grow by 8.9-9.9%, supported by the biodiesel blend increase from B5 to B7 to reduce excess stockpiles and mitigate the impact of higher oil prices amid the Middle East conflict. Export volumes are expected to contract by -1.3% to -2.3% due mainly to government measures to control CPO exports to accommodate domestic energy demand, which is likely to increase as a result of Middle East tensions. However, the palm oil industry remains exposed to geopolitical risks, particularly the ongoing conflict in the Middle East, including (i) heightened volatility and upward pressure on global oil prices, which may increase energy costs, weigh on domestic consumption, and lead downstream industries to delay orders, and (ii) potential disruptions to logistics and shipping—particularly from a possible closure of the Strait of Hormuz—which could delay exports to Middle Eastern markets.

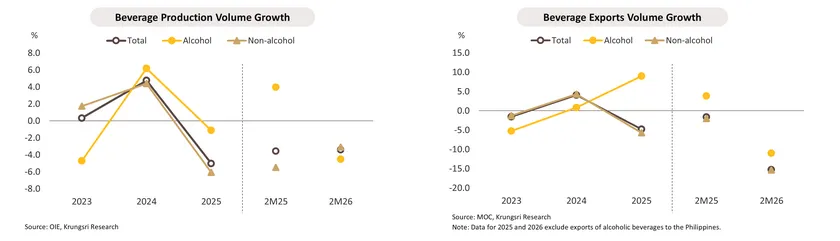

Beverage: Modest recovery is expected across the board, though Middle East-driven cost pressures and Cambodia trade disruptions pose key risks.

-

In 2M26, domestic beverage consumption contracted across both alcoholic and non-alcoholic segments, weighed down by higher living costs amid a sluggish economy and slower foreign tourist arrivals, despite relaxed alcohol trading hours. Total beverage production declined by -3.4% YoY, with alcoholic beverages falling -4.5% YoY due to production cuts aimed at destocking elevated inventory levels, alongside softer domestic and external demand. Non-alcoholic beverages decreased by -3.1% YoY, primarily driven by contractions in the energy drink and ready-to-drink tea segments. Total exports contracted by -15.3% YoY, with alcoholic beverages declining -11.0% YoY and non-alcoholic beverages down -15.4% YoY, largely due to a halt in shipments to Cambodia (Thailand’s key beverage export market) following prolonged border closures amid ongoing border tensions.

-

2026 Outlook: Domestic consumption is forecast to grow modestly by 1.0–2.0% (lower than 2.0% growth in 2025), constrained by rising living costs amid the Middle East conflict and lower-than-expected foreign tourist arrivals. Compared with a low base in 2025 due to destocking and maintenance shutdowns by some major producers, production is projected to grow by 1.0–2.0%, supported by both domestic and export demand, albeit at a slower pace. However, production costs are expected to rise significantly, driven by higher oil prices and shortages of plastic resin—a key packaging material—due to the Middle East conflict. Exports are forecast to remain stable or expand by up to 1.0% (following a low base of a -4.8% contraction in 2025), led by modest gains in juice, energy drinks, and beer, despite ongoing headwinds, particularly from global economic uncertainty and weak purchasing power. Nonetheless, exports to Cambodia will remain a drag throughout the year, as prolonged border closures and ongoing tensions continue to disrupt trade.

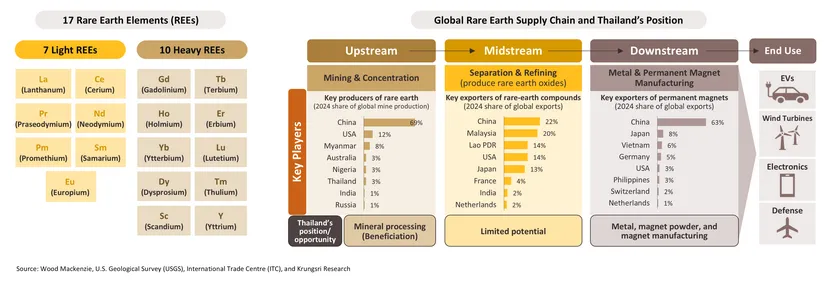

Rare Earths: Rising global demand creates opportunities for Thailand, while highlighting the need to address environmental challenges.

-

In 2025, U.S.–China trade tensions have expanded into strategic competition over access to rare earth elements (REEs). China continues to dominate the global REE supply chain, spanning mining, refining, and magnet production, and retains the ability to impose export controls. In response, the U.S. is accelerating efforts to diversify supply chains by strengthening partnerships with resource-rich and processing-capable countries, including Australia, Malaysia, Vietnam, and Thailand.

-

Thailand’s opportunities span both upstream and downstream activities within the rare earth value chain. In upstream industries, Thailand could add value by importing minerals, processing them, and re‑exporting rare earth concentrates. In downstream segments, the country could benefit from increased investment, particularly in the production of rare earth alloys, magnet powders, and permanent magnets. Going forward, developing a domestic rare earth industry would allow Thailand to benefit from rising global demand for REEs while strengthening its high-tech supply chains. However, this advantage comes with trade-offs, as it may increase environmental and social risks, particularly from greater exposure to hazardous waste affecting communities and ecosystems.

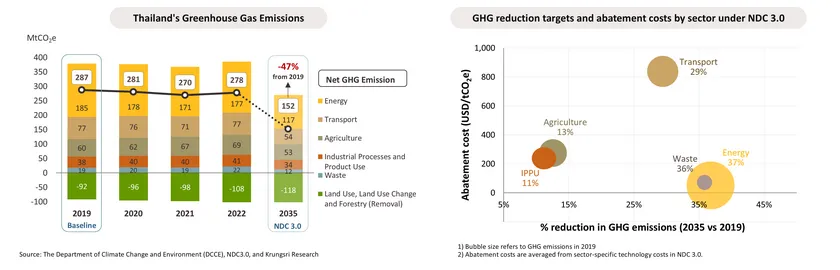

Net Zero 2050: The new target creates challenges while unlocking business opportunities in renewables, ZEVs, and low-carbon technologies.

-

Thailand has pledged to achieve Net Zero emissions by 2050, bringing the timeline forward by 15 years from its previous goal. Under its latest Nationally Determined Contribution (NDC 3.0), the country aims to reduce net greenhouse gas (GHG) emissions by -47% by 2035 compared to 2019 levels. This compels businesses to accelerate their transition toward a low-carbon future, creating both challenges and opportunities, particularly in the following sectors.

-

Energy: The largest emitter is required to cut emissions by -37% by 2035. Challenges remain due to its heavy reliance on fossil fuels (70% of power generation). However, opportunities lie in renewables, Carbon Capture and Storage (CCS), and alternative fuels like hydrogen and sustainable aviation fuel (SAF).

-

Transport: The sector is set to cut GHG emissions by -29%. While EV adoption is expanding in Thailand, shipping, trucking, and aviation still face high decarbonization costs.

-

Industrial: Despite the relatively smaller reduction target of -11%, the transition in this sector remains challenging, particularly for hard-to-abate sectors such as cement, chemicals, and steel, which depend on costly CCS and hydrogen. Opportunities exist in green manufacturing like low-carbon steel and cement, bioplastics, and energy-efficient appliances.

ย้อนกลับ

.webp.aspx)