Executive Summary

Since President Prabowo Subianto took office in 2024, Indonesia's increasing reliance on populist, state-interventionist, and nationalist policies has raised concerns over governance standards, fiscal discipline, and policy credibility. Meanwhile, the Middle East conflict and the government's continued commitment to fixed domestic energy prices further amplified concerns over fiscal sustainability. This ultimately contributed to what can be described as a "confidence crisis" by mid-2026, reflected in outlook downgrades by major credit rating agencies, MSCI's review of Indonesia's Emerging Market status, and a broad-based selloff across Indonesian financial markets.

On the horizon, trajectory of the crisis will depend on two key factors: the outcome of MSCI's market classification review in late June and the government's ability to restore policy credibility. Over the medium term, if investor confidence remains weak, the risk of spillovers from financial markets to the real economy will increase. Such spillovers could weigh on investment, employment, and economic growth, posing a significant challenge to Indonesia's long-term development objectives.

Introduction

During the administration of Joko Widodo (Jokowi), particularly between 2016 and 2023, Indonesia was widely regarded as one of the most promising emerging markets in the world. The country benefited from a large and youthful population, abundant natural resources, prudent macroeconomic management, and a series of structural reforms that strengthened investor confidence. Its large economic size also cemented its position as a founding member of the G20.

However, Indonesia's policy quality and credibility have increasingly come under scrutiny since President Prabowo Subianto took office in October 2024. Investors have raised concerns over governance standards, fiscal discipline, and the overall investment climate. These concerns were further amplified by the outbreak of conflict in the Middle East, which exposed Indonesia's vulnerability as a net oil importer. The external shock acted as a catalyst, intensifying existing concerns over the country's economic stability and policy direction. As a result, investor confidence deteriorated sharply, triggering broad-based selloffs across Indonesian financial markets and driving the rupiah to record lows.

This report aims to examine the evolution of economic policies under the Prabowo administration, which has been a key factor behind the erosion of investor confidence and the resulting pressures on Indonesia's financial markets. It also assesses the economic and financial implications of these developments, the policy measures adopted in response, and the key issues to watch going forward.

Key Policy Development under President Prabowo

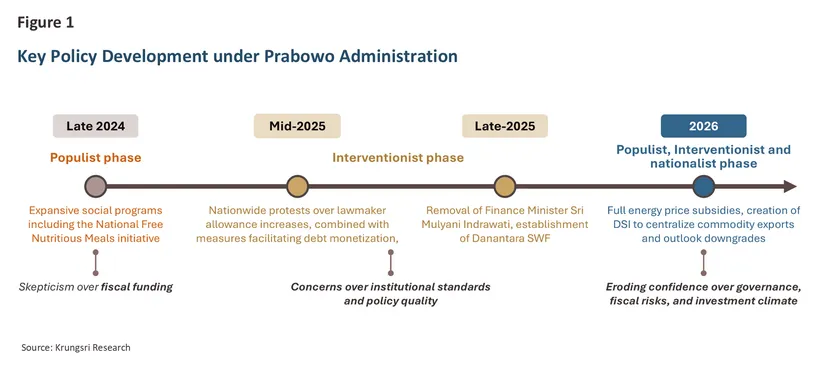

Since President Prabowo took office in 2024, Indonesia's policy direction has been characterized by three key themes: populism, state interventionism, and nationalism.

2024: The Populist Mandate

President Prabowo entered office with an ambitious goal of raising Indonesia's GDP growth to 8% by 2029. As part of this agenda, he launched the Free Nutritious Meals Program, one of his flagship campaign promises. However, concerns over fiscal sustainability quickly began to emerge. Questions arose over how the program would be financed, particularly given the government's commitment to maintaining the fiscal deficit within the legal ceiling of 3% of GDP.

2025: The Interventionist Turn

In the second year of President Prabowo's administration, several major economic policy initiatives reflected a growing role of the state in economic affairs. These developments marked a turning point that began to erode governance standards, institutional quality, and policy credibility, as reflected in the following developments:

-

February 2025: The establishment of Danantara, a new sovereign wealth fund with an ambitious investment mandate, marked the first major source of concern due to its opaque governance structure and the potential overlap between its investment activities and the state's fiscal liabilities.

-

August 2025: Nationwide protests erupted after parliament approved new housing allowances for lawmakers, reportedly worth more than ten times Indonesia's minimum wage, while expenditure on social programs was being curtailed.

-

September 2025: Scrutiny intensified following the abrupt dismissal of Finance Minister Sri Mulyani Indrawati, who was widely respected by investors for her commitment to fiscal discipline and macroeconomic stability.

-

Late 2025: Questions surrounding the independence of Bank Indonesia began to emerge. The administration increasingly pushed for monetary accommodation, while Bank Indonesia revived a COVID-era burden-sharing arrangement by purchasing government bonds in the secondary market to support expansive state-led projects (Quasi-debt monetization).

2026: Rating Downgrade Risks and The Resource Nationalism

The policy developments since 2024 have been sufficient to prompt rating agencies to reassess Indonesia's credit outlook. In February 2026, Moody's revised the outlook on Indonesia's Baa2 sovereign rating from Stable to Negative, citing "reduced predictability in policymaking" and "weakening governance." Fitch subsequently followed with a similar outlook downgrade in March, highlighting concerns over the growing centralization of policymaking.

Concerns over governance have also materialized in the private sector. In early April 2026, MSCI (Morgan Stanley Capital International) removed six major Indonesian companies from its indices, citing issues related to concentrated ownership structures and corporate governance.

Most recently, in May 2026, President Prabowo announced the establishment of PT Danantara Sumberdaya Indonesia (DSI), which, beginning on June 1, would serve as the sole export intermediary for several key commodities, including coal and crude palm oil.

The measure represents another step in Indonesia's trend toward resource nationalism. These market distortions and increasingly investor-unfriendly policies have prompted MSCI to signal a potential reclassification of Indonesia from Emerging Market (EM) to Frontier Market status. Although no reclassification decision has been made, the warning has added to investor concerns and intensified capital outflows from Indonesian financial markets.

At the same time, populist policies have added to fiscal concerns. The conflicts in the Middle East since late-February has pushed global oil prices persistently higher, yet

the government has chosen to fully subsidize domestic energy prices to shield households from rising costs.

Taken together, these developments fueled concerns over governance standards, policy priorities, institutional independence, and the government's commitment to fiscal prudence. Each policy development added another layer of concern, gradually eroding investor confidence and ultimately contributing to the confidence crisis that emerged in 2026.

Impacts on Financial Markets, Real Economy, and Policy Responses

1. Financial Markets

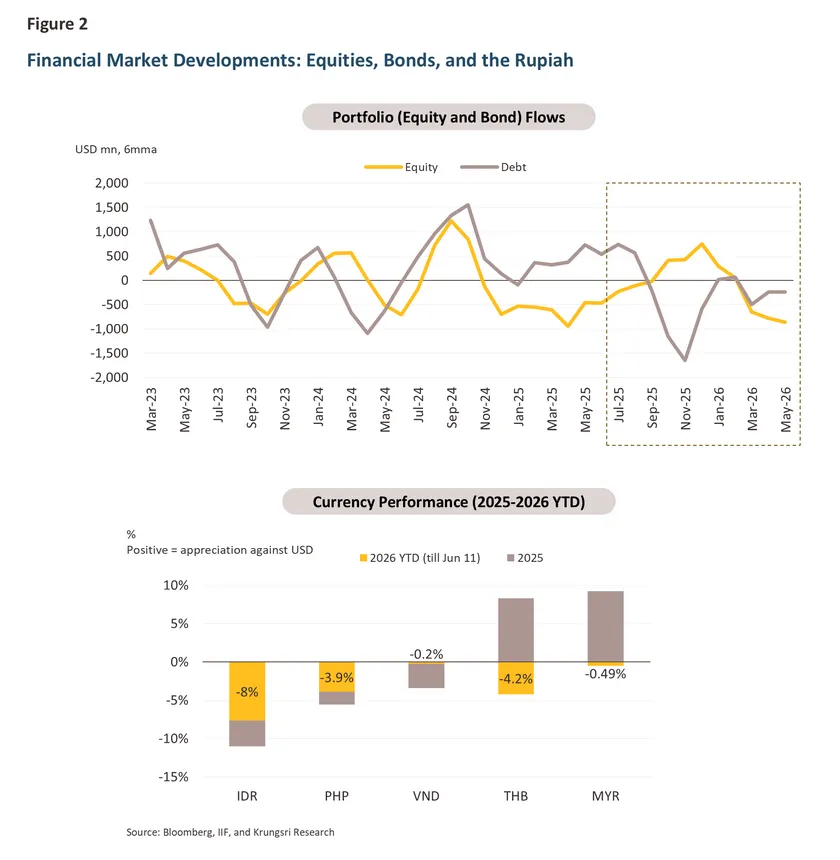

Indonesia is a twin-deficit economy, meaning that it relies on external financing to fund both its fiscal and external imbalances. As a result, investor confidence, fiscal discipline, and policy credibility are critical to maintaining macroeconomic and financial stability.

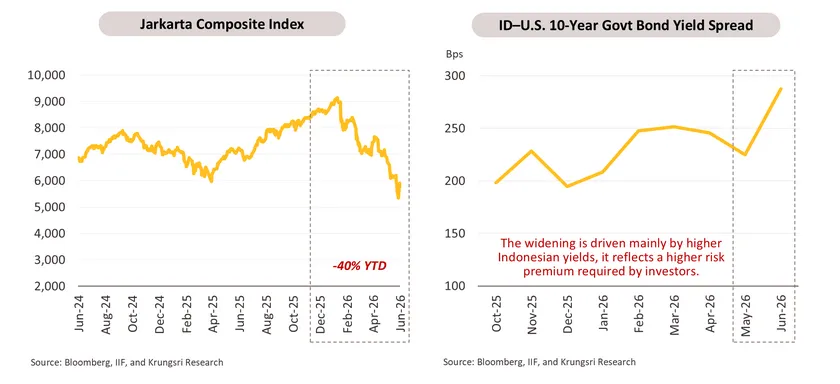

However, concerns over these policy developments have triggered broad-based selloffs across Indonesian financial markets. Equities have fallen sharply, the rupiah has repeatedly hit record lows despite continued intervention by Bank Indonesia, and government bond yields have risen as investors demand a higher risk premium for holding Indonesian assets (Figure 2).

2. Real Economy

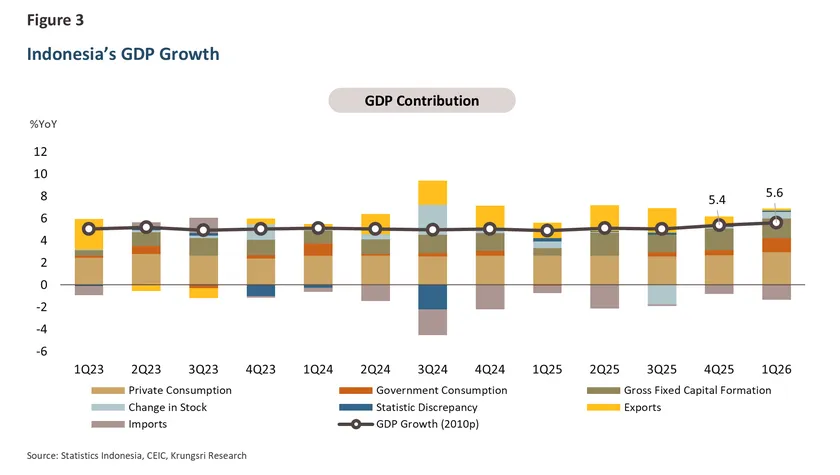

At first glance, Indonesia's real economy does not appear particularly concerning. Economic activity has remained resilient, with GDP growth reaching 5.6% in the first quarter of 2026 (Figure 3). However, a closer look at the composition of growth suggests that, beyond still-healthy private consumption, much of the recent momentum has been driven by fiscal stimulus measures and temporary factors. As such, the current pace of growth may prove difficult to sustain once these supporting factors fade.

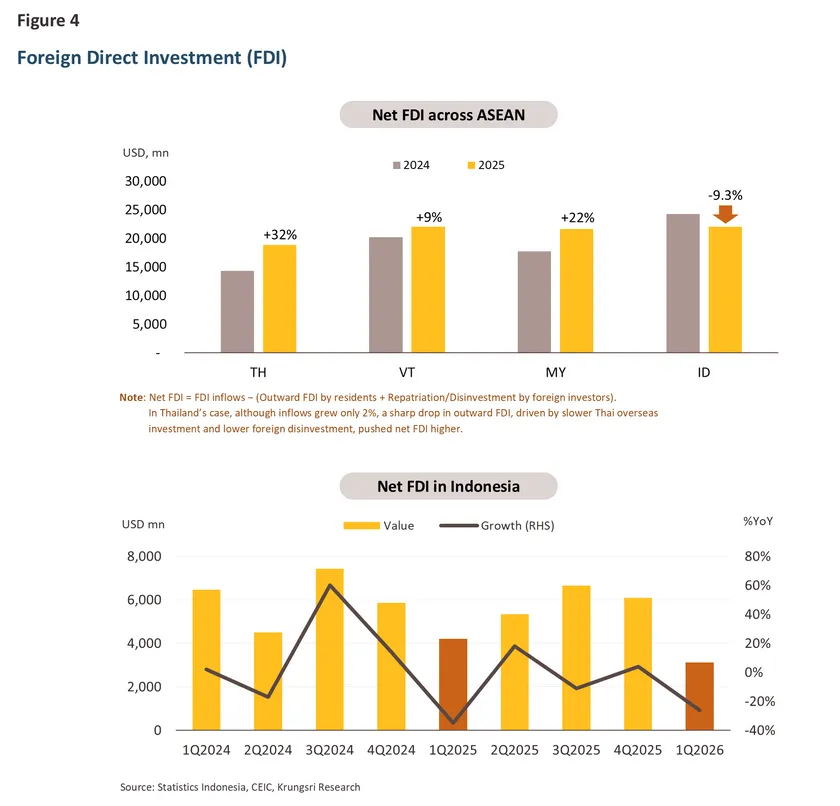

In contrast, foreign direct investment (FDI) presents a less encouraging picture. Following the first wave of confidence concerns in 2025, FDI inflows into Indonesia began to slow, particularly relative to several ASEAN peers. As investor sentiment continued to deteriorate this year, net FDI contracted by 26% year-on-year in the first quarter of 2026 (Figure 4). This suggests that the confidence shock is no longer confined to financial markets and has begun to affect investment decisions in the real economy.

Overall, recent developments suggest that the confidence crisis has already had a clear impact on both financial markets and foreign direct investment. However, the effects on domestic economic activity remain relatively contained for now. If investor confidence fails to recover in the near term, the impact could gradually spill over into employment, household consumption, and broader economic growth in the periods ahead.

3. Policy Responses

So far, the government's policy response has been concentrated on the external stability front. In response to the weakening rupiah, Bank Indonesia raised its policy rate by 50 bps in May, followed by an emergency 25-bps hike on June 9, bringing the policy rate to 5.50%. Despite the so-called "unanticipated moves," the rupiah has remained broadly stable at around 18,000 against the U.S. dollar (as of June 15, 2026). In addition, the government and Bank Indonesia announced a coordinated fiscal-monetary package on June 6, including measures to raise government bond yields and attract foreign capital inflows, with the aim of preserving the attractiveness of Indonesian assets and stabilizing the rupiah.

However, investors are not attracted solely by higher returns; they are also drawn by confidence in the credibility and predictability of the policy environment. As such, market pressures are likely to persist if the underlying concerns that triggered the confidence crisis remain unaddressed.

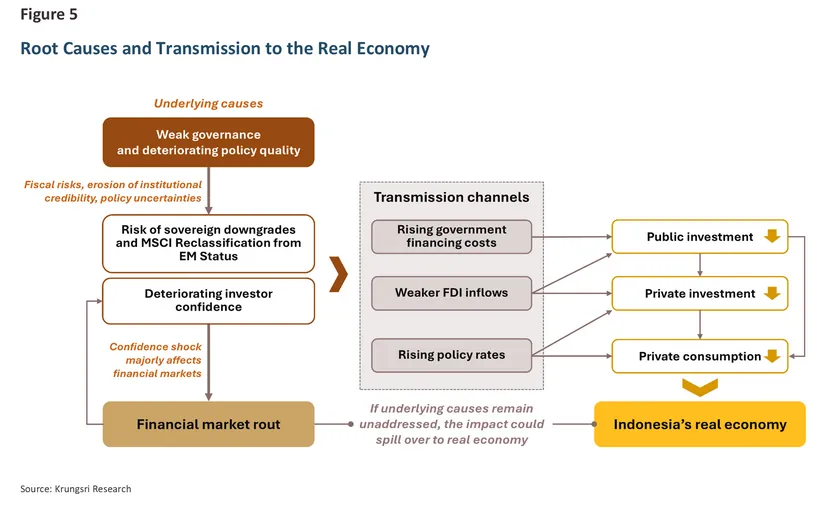

Root Causes and Economic Implications

The outlook downgrades, rupiah depreciation, and market selloffs are symptoms, not causes, of a deeper problem. At the core lies a deterioration in governance quality and policy credibility under the Prabowo administration, eroding investor confidence in Indonesia's economic management. While the Middle East conflict is not a root cause of Indonesia's confidence crisis, it has exposed the fragility of the country's fiscal prudence regarding the government's decision to fully subsidize domestic energy prices amid rising global oil prices (Figure 5).

For economic implication, if these core issues remain unaddressed, the confidence issue could gradually be transmitted to the real economy through several channels. First, higher government financing costs would reduce fiscal space and may force the government to delay or scale back major public investment projects, including strategic infrastructure developments such as Nusantara (IKN). Second, weaker investor confidence could discourage foreign direct investment (FDI), reducing private investment and job creation. Third, tighter financial conditions and higher policy rates could dampen credit growth, weighing on both business investment and household spending.

Krungsri Research View

On the horizon, the trajectory of Indonesia's confidence crisis will be determined by two key factors: the outcome of upcoming rating and market classification reviews, and the government's ability to restore policy credibility. On the market classification front, MSCI is expected to announce the outcome of its market status review by the end of June. Whether Indonesia retains its Emerging Market status or is reclassified to Frontier Market could have significant implications for capital flows and investor sentiment.

On the policy front, investors will be closely monitoring the evolution of populist policies, increasing state intervention, and resource nationalism, all of which have raised concerns over fiscal discipline and the broader private investment climate.

Over the medium term, if concerns over governance standards and policy quality persist, the risk of spillovers from financial markets to the real economy will continue to increase. At the same time, the growing allocation of public resources toward populist programs may crowd out investment in projects that enhance long-term productivity. The Nusantara Capital City (IKN) project illustrates this challenge. Faced with mounting fiscal constraints, the Indonesian government has repeatedly scaled back budget allocations for the project, increasing its reliance on private-sector financing.

However, attracting private investment will require stronger governance, greater transparency, and a clearer development roadmap. Without meaningful progress in these areas, it may prove difficult to secure sufficient private capital to complete the project as planned.

- Is Indonesia in a crisis?

By definition, Indonesia is not currently facing a full-blown economic crisis of the kind experienced in the past, such as a balance-of-payments crisis, a banking crisis, or a severe economic contraction.

Rather, what the country is experiencing is better described as a "confidence crisis," rooted in concerns over governance quality and policy credibility. Such weaknesses have long been recognized as key obstacles preventing many emerging economies from escaping the middle-income trap. Ironically, overcoming this very challenge has been one of the central objectives of President Prabowo's administration since taking office.

While investor confidence can be restored, doing so will require acknowledging the root causes of the problem and rebuilding policy credibility through transparent, predictable, and well-governed policymaking. Without such efforts, Indonesia risks facing further rating pressures and prolonged financial market volatility, which could eventually spill over into the real economy. This, in turn, would make it increasingly difficult for the country to achieve its long-term development objectives.