Traditional Banking and DeFi: What Role will be Left for Banks if the Financial System is Disintermediated?

DeFi, or Decentralized Finance, refers to a newly emerging understanding of how decentralized financial services might be structured, with users themselves jointly responsible for maintaining the system and for managing and settling transactions. Proponents of DeFi argue that this ensures data transparency and the rapid processing of transactions, obviates the need for financial intermediaries, and reduces the risks that arise from the reliance on centrally stored data as per traditional financial systems. Given these clear attractions, interest in DeFi is rapidly building, both in financial circles and among the wider public.

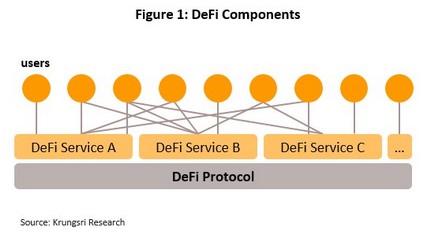

DeFi is composed of three main components: (i) DeFi protocols, which are essentially autonomous programs that are used to build, manage and operate DeFi systems, to check information, and to automatically convert real-world assets into digital form; (ii) DeFi services, which generally take the form of applications that make available financial services and other functions that expose the operation of backend systems to users; and (iii) DeFi users. DeFi has a short history and dates back not much more than a decade, though two events mark milestones in its development. The first of these was the creation of Bitcoin in 2009, while the second was the 2017 development of DAOs (decentralized autonomous organizations), smart decentralized organizations that operate independently and autonomously on a blockchain, for example as a smart contract.

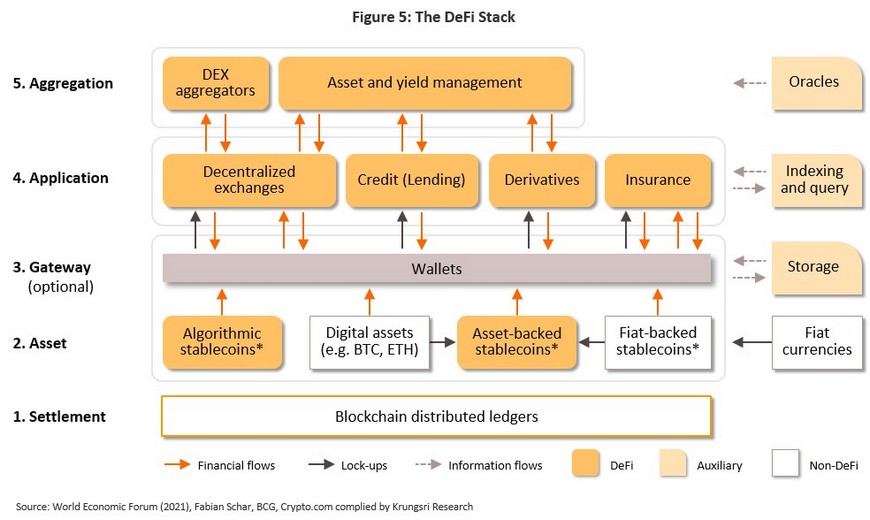

In terms of its operations, DeFi has five layers: (i) the settlement layer, which allows the network to safely exchange information on asset ownership via blockchains and other distributed ledger technologies (DLTs); (ii) the asset layer, which is composed of digital assets that act as a means of exchange when conducting transactions and includes for example tokens and stablecoins; (iii) the gateway layer, which may include a digital wallet that is used to store a user’s tokens; (iv) the application layer and the interface, which are particular to each application; and (v) the aggregation layer. In addition, further auxiliary components may be present within each layer to provide additional support.

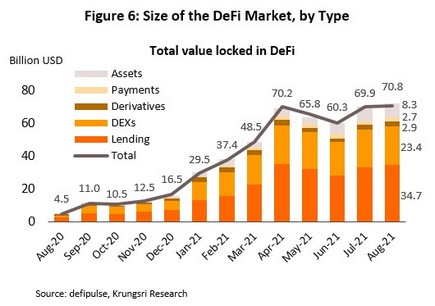

Over the recent past, the DeFi sector has grown rapidly and at present, the industry has an estimated global userbase of around 1.75 million individuals and a market value of USD 70.8 billion. Almost half of this is accounted for by loans, which are followed in importance by decentralized exchanges (DEXs). A portion of the DeFi market is also taken up by payments and insurance but currently, these are not significant contributors to DeFi’s total market value. However, although interest in the industry is rising among Thai investors, application developers, financial institutions, commercial banks, and regulatory bodies, the overall impact on the Thai banking sector of DeFi remains limited. This, though, is likely to change once members of generations Y, Z and Alpha reach maturity; by the time these age cohorts comprise the bulk of society, the role of DeFi in the Thai financial system will have become much clearer.

Krungsri Research’s assessment of these changes is that the emergence of DeFi is providing the commercial banking sector with a major opportunity to overhaul its operations. By taking advantage of a rapidly evolving situation to mix traditional centralized financial (CeFi) services with DeFi operations, banks will be able to offer financial solutions that are more finely tailored to individual market segments, and through this, better respond to the needs of their customers.

The Banking Crisis Sparks the DeFi Revolution

The subprime crisis of 2008-2009 marked a significant turning point in the history of the financial sector. In addition to triggering enormous global economic losses, the crisis has also left a lasting legacy, as a stark warning of the dangers that may lurk within the modern financial system.

In the wake of the events of 2008 and 2009, many regulators came to the conclusion that the crisis had its origin in financial institutions’ slow reaction to innovation and the serious miscalculation of risk that then flowed from this. In response, national and international bodies moved to tighten regulation of the financial sector, for example by introducing the Basel III reforms, which requires increase in reserves that commercial banks must hold, while broadening the definition and calculation of ‘risk’ itself.

However, technologists viewed the crisis rather differently. In the view of some, the source of the subprime crisis lay in the financial sector’s extreme reliance on centralized intermediaries like commercial banks. During the crisis, the collapse of a key node in this centralized, borderless and closely interconnected network thus swiftly and unavoidably generated systemic risk throughout the entire global financial system. Technologists thus looked to apply rapidly evolving information technology to the problem of reducing dependency on financial intermediation, or even to sidestep commercial banks altogether. This then gave birth to the developments that are now classified as ‘DeFi’. Given this history and its speed of development, many now believe that in the near future, DeFi may displace traditional commercial banking.

In a world where revolutionary change seems to be accelerating on an almost daily basis, the question then becomes, “How will commercial banks respond to the rapidly intensifying challenge posed by DeFi?”

Box 1: What are Blockchains and Smart Contracts?

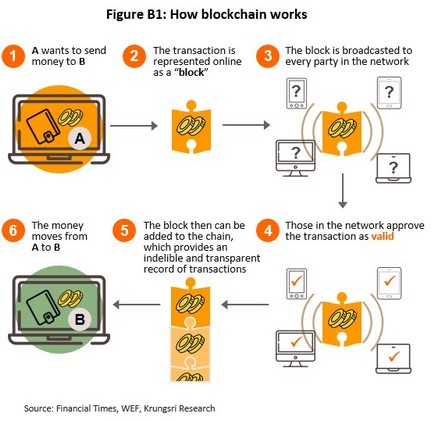

A blockchain is a digitally distributed, decentralized, public ledger that exists across a peer-to-peer network. When users join a blockchain, they will have access to a distributed shared database, and they will be able to read and record data in this. Because data is public, it is possible to easily confirm who has the right to access or who is the owner of particular chunks of data. This data is stored in blocks. As new data is added, new blocks will be formed and linked together in a chain of new-to-old data blocks, hence the name ‘blockchain’.

The most important feature of the blockchain is that when data is written into it, that data is both publicly visible and irrevocable. It is as if all participants in the blockchain are instantly sent a copy of the associated paperwork to file for reference. Whenever there are any additions, all members of the network receive new copies of the relevant paperwork to file alongside their existing records. The basic technology behind this is now mature, and blockchains and the data stored on them are regarded as stable, safe, and transparent. The added advantage is that blockchains store data entirely without the need for any centralized oversight.

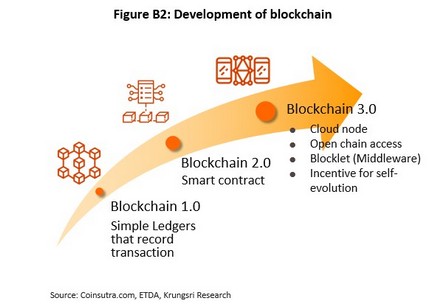

Blockchain technology has been used in a wide range of applications, the most widely known of which are cryptocurrencies[1] and especially bitcoin. However, blockchains are beginning to crop up in other areas, including in the manufacturing, logistics and real estate sectors, as well as in more localized applications, such as recording exam results, and even in elections.

However, at first, uses of the blockchain were limited. During the ‘Blockchain 1.0’ era, applications were restricted to recording transactions. The most famous example is Bitcoin, which is built directly on a blockchain. This situation changed in 2014, when Vitalik Buterin, a Russian-Canadian programmer, extended the blockchain’s functionality by adding the ability to run code on it with independent record keeping. These developments were incorporated into the next generation of blockchain, led by Ethereum, marking the start of the ‘Blockchain 2.0’ era.

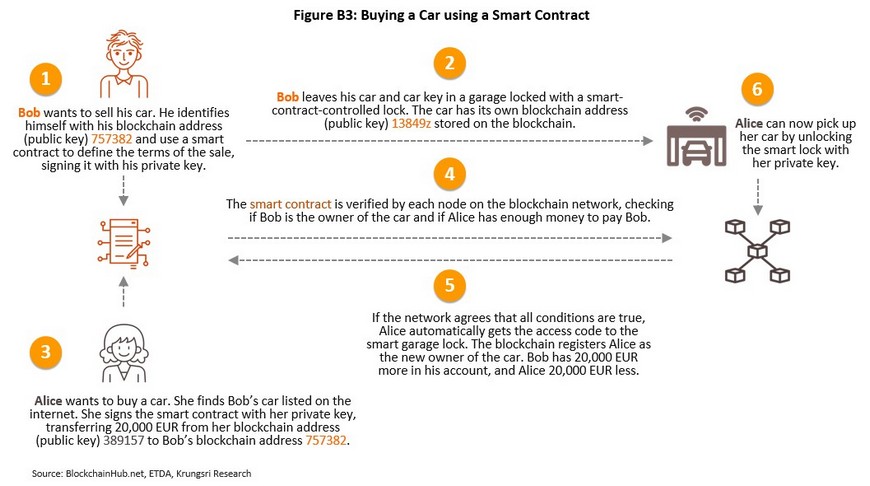

The code embedded on a blockchain is often called a ‘smart contract’ since these programs operate much like standard contracts agreed between a seller and a buyer. The major difference is that smart contracts are programed into the blockchain and operate autonomously while maintaining other aspects of the blockchain, i.e., public, checkable, distributed, and trustless (that is, their functions do not rely on the intervention of, or trust in, any third-parties.)

To illustrate, consider an example in which Alice wants to buy a secondhand car from Bob. In the pre-blockchain era, the two would have to use standard contracts that require third party (e.g., Department of Motor Vehicle, or perhaps a bank) confirming that money had passed in one direction and ownership of the car had gone in the other. However, if they were able to use a smart contract for this transaction, other participants on blockchain (i.e., nodes) would be able to verify that Bob is indeed the lawful owner of the car, and that Alice has sufficient money to meet Bob’s asking price. Moreover, if Bob leaves his car at a parking site connected to smart contracts, when the transaction is confirmed, the car will be released to Alice automatically, without Bob having to deliver it in person. In addition, because this transaction has been recorded on a blockchain, if the car is stolen from Alice in the future, it will be possible to check its ownership through vehicle identification number and confirm that Alice is still its legal owner (Figure B3).

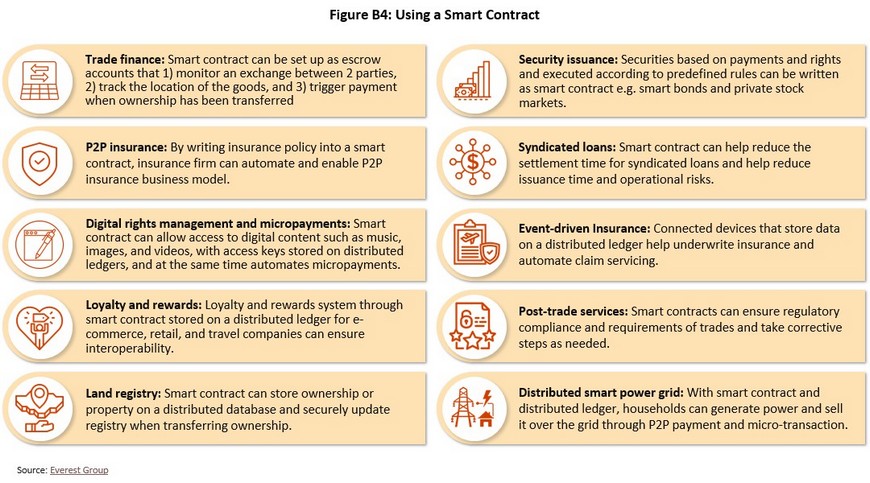

Smart contracts have a wide range of use-cases, from relatively simple applications such as transferring cryptocurrencies between individuals, to more complicated activities such as arranging insurance and land registry (Figure B4).

Following the introduction of smart contracts and the emergence of Blockchain 2.0, technological development has continued apace and decentralized applications (DApps) are now on the cutting edge of blockchain technology. These are an extension of smart contracts, though DApps allow the limited functionality of smart contracts to flower into full-blown applications, and because these now allow cross-chain interoperability, they mark a further significant step forward for blockchain functionality. In addition, distributed ledger technology (DLT) is being extended to increase the usability of blockchains across a much broader range of use-cases, including in insurance, logistics, real estate, education, healthcare, the arts, and a large number of other areas.

What is DeFi?

DeFi, an acronym formed from the first syllables of Decentralized and Finance, is a catch-all term for decentralized financial services that are carried out in the absence of financial intermediaries. At present, the most obvious manifestation of DeFi is found in DApps (decentralized applications) that are built on blockchains[2]. Most DeFi transactions are connected to the transfer of digital assets[3].

There are three main components of DeFi:

1) DeFi protocols[4] are essentially computer programs that are used to build, manage, and operate DeFi systems, to check information, and to automatically convert real-world assets into digital form. DeFi protocols form the basis of other DeFi services.

2) DeFi services are built on DeFi protocols to develop financial services or to offer other functions connected to backend operations, such as specifying risk parameters or interest rates. Services also include frontend offerings, such as providing users with digital wallets that can be used to store, manage, and transfer assets. DeFi services may also include processes that are connected to DeFi financial service regulations and conditions.

3) DeFi users are those who use DeFi services to carry out financial transaction.

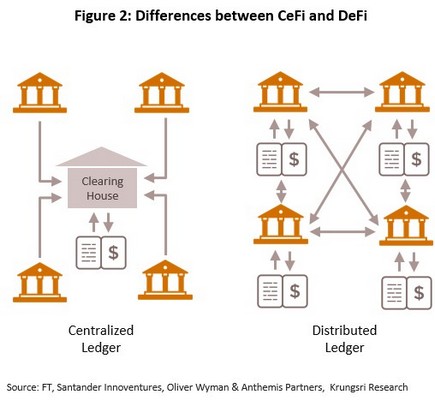

At present, settling transactions is usually carried out through a centralized financial (CeFi) system. That is, the power to manage financial transactions is centralized, most obviously in the case of the banking system, which has responsibility for confirming that valid and authorized transactions have occurred and then recording these. This system has the advantage of being generally very convenient for most people, but its weakness is that when the central financial body experiences problem, this may have significant effects on all system participants. On the other hand, in decentralized systems, all system participants (i.e., not just the bank) are responsible for jointly managing the system and for checking and confirming transactions (Figure 2), which is made possible by the structure of blockchain technology and the fact that this puts complete copies of all blockchain data in the hands of every user. The general working principle of decentralized systems is thus that when a transaction takes place, all blockchain participants will check the data that they have, which is recorded in each block of the blockchain, and when there are changes to an account, this new information will be written into a new block that is then digitally linked to the previous block on the blockchain. Because each new block is cryptographically tied to the preceding block, it is extremely difficult to alter data once it has been recorded, and this helps to prevent account data (either historical or current) being changed fraudulently.

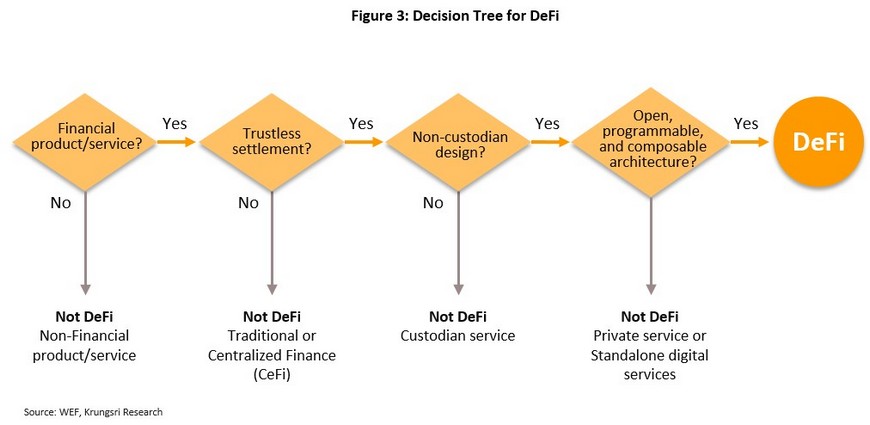

Figure 3 shows how to decide whether a particular service or product may be described as a DeFi. This involves four steps, as described below.

1. Is this a financial product or service? If it is not concerned principally with finance, it cannot be a DeFi good/service. If it is, move to the next question.

2. Does the operation of this product or service reduce or remove the need for trust in another individual, organization, middleman, or other third party in favor of a technological, algorithmic or other such solution that is based on ‘trustless’ settlement? If the answer is no, the item should be considered a traditional financial product or service; one of the key features of DeFi is that recording and processing transactions is carried out through the logic of pre-determined DeFi protocols (e.g., by settling payments on a blockchain). However, if the answer is yes, move to the next stage.

3. Is it possible for any outside party other than the account holder to influence, affect or alter the good or service? If the answer is yes, the item will be classified as ‘custodial’, that is a third party is responsible for its management, as is the case with stablecoins[5]. This consideration is important because it is not possible for third parties to alter assets that originate from or are managed by a DeFi system. Rather, within DeFi systems, assets are only managed under the conditions specified in a smart contract and a DeFi protocol. If this is the case for the item under consideration, move onto the last stage.

4. Is the product or service has an open, programmable, and composable architect? This refers to the ability of third parties to inspect source code (to check security and efficiency) and the extent to which the item exposes its services through a public API [6] in a manner similar to CeFi-type open banking[7]. Making a service open source helps stakeholders directly inspect and check its use of protocols, and also allows outsiders to use and extend the source code for their own purposes. If the answer to this question is no, this should be considered a private or standalone digital service.

Services that pass all four stages of this test may be regarded as DeFi services.

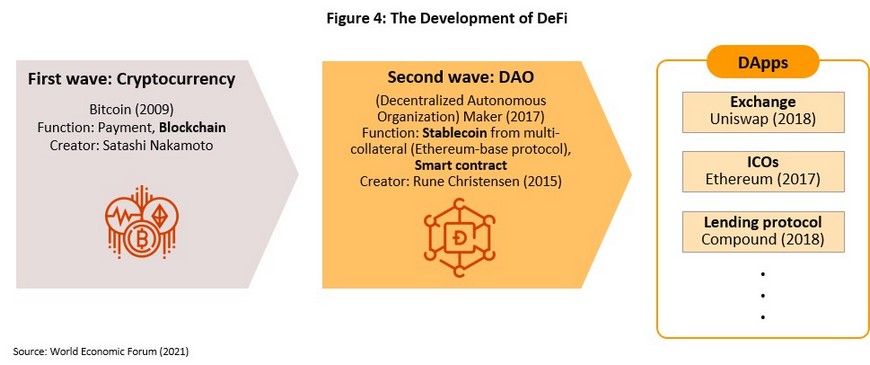

Although interest in DeFi has increased dramatically over the last one to two years, in reality the DeFi revolution did not emerge into the world fully formed, and trends that are now tied together under the heading ‘DeFi’ have been gathering pace for many years. Indeed, the emergence of DeFi can be traced back to two separate technological developments.

1. The first wave in the development of DeFi was the emergence of cryptocurrencies, specifically the mining of the first Bitcoin in 2009. The invention of bitcoin showed how blockchain technologies could find real world applications in the exchange of money, a development that potentially does away with the need to go through a financial intermediary. However, at this stage, use was limited by several factors, including the wild swings in value that tend to affect cryptocurrencies.

2. The second wave of the development of DeFi was ushered in with the 2017 creation of DAOs, or decentralized autonomous organizations. DAOs are distributed systems that live on blockchains and function as smart contracts. Similar to other aspects of the blockchain, it is possible for network participants to inspect DAOs and the network shares responsibility for their operation through the holding of governance tokens[8]. Also important was the development of stablecoins on the MakerDAO[9] platform, the first platform to successfully link DAOs with stablecoins. These breakthroughs then spawned further innovation in financial services that better addressed network user needs, including the creation of decentralized exchanges (DEXs) such as Uniswap, ICOs[10], and other lending protocols. DAOs and stablecoins were thus important contributory factors in the emergence of the DeFi phenomenon.

A Deep-dive into the Structure of DeFi

DeFi services are built in five distinct layers.

Layer 1: The settlement layer provides the basis for the whole system. This layer authorizes the network to safely process data on network participants’ ownership status and lays out the conditions under which changes to network data may be made, ensuring that this only happens in accordance with established protocols. This layer thus forms the foundation for other operations. For DeFi goods and services, layer 1 is principally composed of blockchain and distributed ledger technologies

Layer 2: The asset layer sits on top of the base, which is ready to process future transactions. The next important layer is thus comprised of assets that act as means of exchange and that therefore facilitate these transactions. This layer thus contains coins or tokens that are established on the settlement layer, the most well-known of which are Bitcoin (BTC), Ether (ETH) and stablecoins.

Layer 3: The gateway layer may or may not be present. If it is, it may consist of a digital wallet that can be used to store a user’s tokens. These will be held in a password-protected account.

Layer 4: The application layer is, from the user’s point of view, the most commonly seen aspect of the DeFi stack, and the rapid expansion of DeFi services in the recent past has largely been fueled by and focused on extending this layer. Developments in the application layer boost functionality and extend user interfaces according to the demands of each application, and these may involve smart contract functionality, for example DEX, loan, and insurance applications.

Level 5: The aggregation layer connects to and aggregates data from layer 4 platforms to develop tools that help with comparisons made between products and services. The aggregation layer may thus help with the development of user-centric platforms that allow users to more easily complete complex tasks.

As Figure 5 shows, in addition to the DeFi stack, running from the foundations up to its connections with the user, the DeFi ecosystem also contains other components that further support service functionality. This includes auxiliary units that assist with the functioning of each layer together with what are technically non-DeFi components, such as access to fiat currencies and blockchain distributed ledger technology. Beyond this, the system also has to deal with flows of money and data. Financial flows originate from users moving tokens and coins into and out of wallets as they engage in layer 4 financial transactions, whether that be from buying and selling or from borrowing. At the same time, information flows are generated by DeFi activities and the work of auxiliary functions in each of the layers of the DeFi stack. Within this system, services are also facilitated by establishing fixed relationships between digital and real-world assets, so for example, fiat-backed stablecoins are possible only by pegging the value of a platform-based currency to a currency used in the real economy at a 1-to-1 value. Thus, the value of USDT (tether) is set at USTD 1 to USD 1, meaning that the issuers of tether need to maintain dollar reserves to a value equal to the value of all issued tether, much as currency boards of central banks maintain foreign reserves to ensure that their national currency trades against other currencies at a pre-determined value[11]. Likewise, other types of asset-backed stablecoins have been developed that tie the value of the digital currency to outside assets, including Dai (MakerDAO), the value of which is pegged to the digital assets that the platform accepts, including bitcoin.

Why should Banks Pay Attention to DeFi?

Over the recent past, the DeFi sector has seen rapid growth in both its market value and its user base. The market value of DeFi activities can be judged by the total value of assets locked up in the DeFi ecosystem (the so-called ‘total value locked’, or TVL), which currently stands at USD 70.8 billion12/. Within this total, lending is the largest segment, which accounts for USD 34.7 billion, or 49% of DeFi TVL. Lending is followed in importance by decentralized exchanges, which have a TVL of USD 23.4 billion, or 33% of the total. The global DeFi user base now stands at over 1.75 million, with over half (50.7%) using the Ethereum protocol. This is followed in importance by Bitcoin (22.0%), Uniswap (12.3%) and others (15.0%).

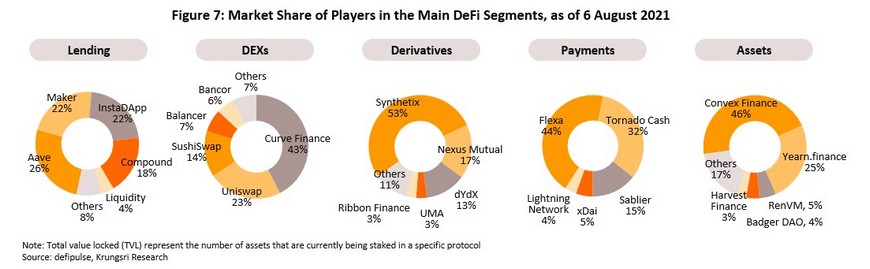

Within each segment of the DeFi industry, market leaders have emerged, some of which have established dominant positions that put them far in advance of their competitors. This is especially the case for derivatives, where the market leader enjoys a 53.0% market share. However, in the lending and DEX segments, market leaders regularly trade places. In the lending market, MakerDAO, the first DeFi lending operation, was overtaken by Compound in June 2020, but Compound was then itself overtaken by Aave at the start of 2021, and this remains the market leader, while in the DEX market, Uniswap had been the market leader from 2017 but has now been overhauled by Curve Finance. It is noteworthy that in both segments, service providers continue to compete against each other through the development of new technology as they try to outmatch the ability of other players to ease their clients’ pain-points, and thanks to this, no clear leader has emerged as yet. In the payments segment, competition remains relatively low, but in the asset group, competition is stiff, and currently Convex Finance is the market leader.

In Thailand, Thai-owned DeFi operations are now beginning to emerge. In the DEX segment, the KULAP platform was established in mid-2020 and was licensed by the Thai Securities and Exchange Commission in 2021, while in the lending segment, JREPO (part of the JMART group) began operating in February 2021.

As its userbase begins to expand and the value of transactions begins to rise, many external players are beginning to pay closer attention to the DeFi market. Naturally, those most directly affected by its expansion are most interested in developments within the DeFi ecosystem. Among these, traditional financial institutions are at the forefront. This research thus now turns to the 4 segments of the DeFi market that have the greatest potential to disrupt the global financial system.

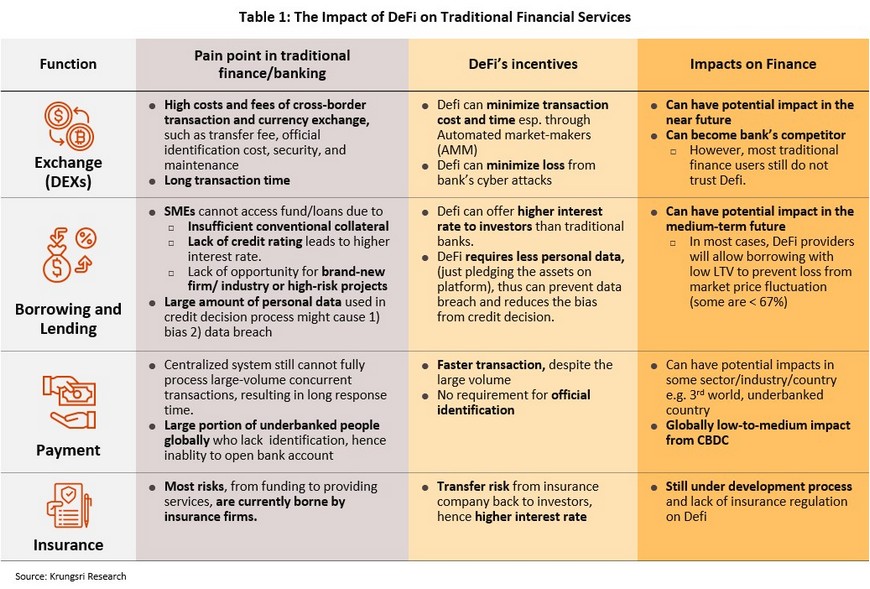

1) DeFi exchanges (DEXs): DEXs offer users the possibility of alleviating the pain points that they encounter when operating through traditional institutions, including the high administrative costs, stiff fees, and the lengthy times required when making international money transfers. These problems arise because at present services are mediated by a centralized financial body. On the other hand, as DeFi processes allow many parties to simultaneously authorize transactions, DeFi-based currency exchanges offer the possibility of lower transaction costs and faster processing times. In addition, because DeFi networks do not have a single chokepoint that handles all information flows, they are less at risk from disruption by cyber-attacks. The considerable advantages offered by DeFi therefore mean that in the coming period, DEXs are likely to be the first DeFi segment to expand in value and this will have potentially significant impacts on the banking sector in the near future. However, although DeFi exchanges are starting to see an expansion in their userbase, the majority of users of traditional banking services are unlikely to have complete confidence in DEXs, and it will take some time for these to prove themselves to the market at large.

2) Borrowing and lending: The ability to access credit through DeFi channels will have direct consequences for the banking sector, though this will be especially pronounced in the market for loans made to SMEs and new types of businesses (e.g., start-ups). These operations frequently encounter difficulties accessing loans and other financial services, because these operations often either lack sufficient collateral to secure a loan or their assets are in a form that the lender does not accept. In addition, the risk models that most banks use may be unsuitable in evaluating loans to these new types of business. Consequently, it can be hard for SMEs/start-ups to access credit, and even when they can they will often face high interest rates. Revealing the personal data for loan application also carries a certain amount of risk, either from the data being released (inadvertently or otherwise) or from bias among lenders. In instances such as this, there is clearly room for DeFi to enter the market and to better serve the interests of both borrowers and lenders. Because there are no middlemen taking a cut of the profits, using DeFi channels will make it possible for direct lenders to receive higher returns from the interest paid on their deposits, while potential borrowers are more likely to be able to secure funding through DeFi loans than from traditional sources. Given this, the impacts of DeFi loan-making are likely to be significant for the financial sector, including traditional banks.

Nonetheless, it will likely take some time for DeFi loans to be become commercially significant. This is because at present, DeFi loans are predominantly pawn-or pledge-type arrangements made to finance short-term speculative exchanges. Moreover, as risk is relatively high, DeFi loans tend to be overcollateralized. Platforms may ask for up to 150% of collateral against loans (e.g., MakerDao requires loan collateral at 1.5-times the loan value[13]), and this makes these loans unsuitable for most small businesses. However, some DeFi players are trying to extend their ability to make loans, especially to SMEs. An example of this is the Singaporean company ShutterOne, which has now made over 4,000 loans to SMEs in ASEAN.

3) Payments: This is another area with significant opportunities for DeFi, especially in this case to make available payment systems that can handle large numbers of concurrent transactions. Traditional systems also require that information flows through a central point when transactions are authorized, meaning that the whole payment network is at serious risk of collapse if this central point fails. In some countries, consumers may also be excluded from traditional financial services and hence the ability to make payments, as banks usually require official proof of identity to open a bank account and gain access to the system, and a great many people lack this. Some DeFi platforms are working to alleviate these two pain points, and through DeFi channels it may be possible to use payment systems without supplying state-approved identification. Moreover, by their design, the distributed, decentralized nature of DeFi platforms makes them considerably more immune to problems of centralized system outages.

For the banking and financial sector, the impact of DeFi payments may therefore be limited to some countries or to only some segments of society within those countries (i.e., those where large numbers of people have difficulty acquiring official identification.) Overall, the development of DeFi payment systems will likely have only low to mid-level impacts on traditional financial institutions. In addition, the authorities in many countries are investigating the feasibility of developing and deploying central bank digital currencies (CBDCs), thus further lessening the impact of DeFi payments.

4) Insurance: Insurance may also benefit strongly from the development of DeFi, and this prospect has spurred much research in the area. Currently, insurers must shoulder a considerable burden of risk, from customer acquisition to assessing their risk and making claim payments. Although some of this is shared with reinsurers, a portion of the risk will always remain as their ‘retention’. DeFi insurance platforms will enable insurers to share some of these risks to investors, who would then take on higher risk for higher returns. Nevertheless, DeFi insurance platforms are still being developed, and problems relating to their real-world deployment have yet to be resolved. Regulatory protection of investors is still also unclear. It is therefore not yet clear how these developments will affect the financial system.

DeFi in Thailand: Albeit still finding its feet, it might break into a sprint at any moment

The current state of the Thai DeFi ecosystem

Within Thailand, DeFi is beginning to attract growing interest from investors, developers, banks, and regulatory bodies. Developments among each of these groups are described below.

- Investors: Interest in DeFi among Thai investors is among the highest in the world, a fact that is reflected in Thailand’s third-placed position on the Chainalysis global DeFi Adoption Index[14], the country coming after only the US and Vietnam[15]. Thailand also consistently ranks very highly among users of DeFi apps and visitors to DeFi-related websites. Thus, in April 2021, Thailand ranked fourth globally for all users of Metamask, a crypto wallet and blockchain gateway, and in the month, 3.1% of all users came from Thailand, making this the most important national segment after the US, China, and Turkey. Pancakeswap, a DEX, also reported that 5.2% of its visitors are from Thailand, making Thailand its second most important market. These figures therefore indicate that compared to other countries, Thai investors are particularly interested in DeFi. Noteworthily, Thais may be familiar with the Thai owned and run digital exchange Bitkub or the foreign Binance platform, but these two cannot be regarded as entirely DeFi-based operations since these two are still structured around the provision of centralized services to offer the best possible service to their clients.

- Application developers: The emergence of a homegrown DeFi development industry reflects growing interest and expertise in DeFi and underscores the likelihood that this will continue to grow in the future. Currently, there are two Thai companies that have developed DeFi products.

- KULAP is Thailand’s first financial platform to use blockchain technology to offer DEX services, and the first in the world to be officially licensed to offer services related to the trade in digital assets[16]. KULAP operates under the regulation of the Ministry of Finance and the Securities and Exchange Commission, which authorized its operations in respectively June and November 2020. The exchange then went live in January 2021.

- JREPO is a digital asset deposit and lending platform that began operations in February 2021, making it the country’s first venture into this area. The company is a joint venture between Tokenine, a consultancy, software developer and blockchain solutions provider, and JFIN, part of the JMART group, whose main business is the retail and wholesale of mobile phones and related equipment.

- Banks and the broader financial sector: Growth in the DeFi market and the broadening spread of DeFi applications is likely to have direct impacts on the traditional financial sector, and so banks and other bodies are beginning to step up their interest in and research into the industry. Within Thailand, two commercial banks have so far openly moved into the DeFi space, and by doing so, they hope to gain knowledge about DeFi for potential future application within the banking sector.

- KBTG (part of the Kasikorn banking group) has stated that it has entered the DeFi market to broaden its knowledge and investigate the possibilities offered by DeFi services[17]. As part of this, a new operation called Kubix has been added to the KBTG group as a pilot operation joining force with the Stock Exchange of Thailand to open an ICO portal[18]. This will provide advisory services and help companies raise funds through initial coin offerings (ICOs), which open the way for investors to convert real-world assets for digital tokens in return for a stake in the offering. KBTG thus believes that CeFi and DeFi can co-exist.

- SCB10X (part of the Siam Commercial Bank group) is also keen to investigate DeFi and to develop its DeFi-related operations[19]. As part of this, SCB10X joined with Band Protocol, a blockchain developer that provides backend services that gather the real-world data needed for the operation of blockchain-based smart contracts. SCB10X has also partnered with Alpha Finance Lab, a provider of DeFi services and builder of cross-chain DeFi product and service ecosystems[20], by sending its developers off to train and jointly-develop new DeFi products. The company has in addition agreed to take part in the running of a Band Protocol node, helping to manage data flows and checking and confirming financial transactions recorded on their blockchain and thus ensuring data integrity across the network[21]. At the start of 2021, SCB also established a new company called Token X that run an ICO portal[22]. In August 2021, Token X announced that it was ready to begin offering a comprehensive range of digital token services, from advisory to business planning and blockchain and technological development. At present, the company is in the process of applying for an operating license from the SEC that will permit it to offer digital tokens for sale, and this is expected to be granted at the end of 2021[23].

- Regulatory bodies: With interest in DeFi growing among Thai investors and the general public, and continuing growth in DeFi internationally, Thai regulatory bodies have begun to take a closer look at DeFi activities and digital assets generally.

- The Bank of Thailand (BOT): Since 2018, the BOT has been working on ‘Project Inthanon’, under which the BOT has partnered with eight commercial banks[24] to research and develop a central bank digital currency (CBDC). The scope of the project was extended in 2020, when the BOT joined with two companies (SCG and Digital Ventures) to start work on a CBDC for corporate users. BOT is also collaborating with the Hong Kong Monetary Authority to develop a CBDC for cross border transfers under the codename ‘Project Inthanon-Lionrock’. In 2021, the BOT further broadened its work on CBDCs to include research and development of a retail CBDC, and initial limited testing of this is expected to start in the second quarter of 2022. Work by the BOT on creating a CBDC involves the development of both blockchain technology and digital assets, which comprise two important layers of the DeFi stack. Many observers therefore believe that the CBDCs that are currently being developed by central banks around the world will help to accelerate change within the financial system, making access to financial services easier, spurring development of the market for cryptocurrencies, and helping to bridge the gap between the CeFi and DeFi worlds[25].

- The Securities and Exchange Commission of Thailand (SEC) and the Ministry of Finance: SEC has responsibility for licensing companies that deal with digital assets[26], as laid out in the Emergency Decree on Digital Asset Businesses, 2018. The latter regulates the raising of funds through the offering of digital tokens, the operation of businesses dealing in digital assets, and other matters related to these. Companies operating in this space thus need to be licensed to do so, and this is granted at the discretion of the Minister of Finance. Once licensed, companies must then operate strictly according to the regulations governing their registered activities. In the case of companies issuing digital tokens, they must first submit their registration documents and draft prospectuses to the SEC, and offers of sale should only be made to investors of the type and under the conditions specified by the SEC. Such offers must also only be made through SEC-approved ICO portals.

Future Growth in the Thai DeFi Sector: Opportunities and challenges

Although DeFi is attracting ever-more serious interest, at the moment, the Thai DeFi industry is still finding its feet. How the industry will develop remains to be seen, and while a range of factors are lined up that support its further expansion, challenges remain that Thai society will need to overcome if the industry is to develop.

Tailwinds boosting uptake of DeFi in Thailand: Because DeFi is a relatively new phenomenon that most people are either unfamiliar with or do not understand, the secure establishment of DeFi in Thailand will depend on an increase in user numbers and the work of agencies and other units that increase public understanding of the industry.

- Members of Generation Y or Millennials (currently 24-40 years old) and Generation Z (currently 13-23 years old) are generally interested in cryptocurrencies and DeFi. This is especially true for those in Generation Z, who may be more interested in investing through these channels than the traditional ways, partly because they are digital natives. Millennials, on the other hand, despite growing up through the transition from analogue to digital technologies, they have already completed their higher education and are more likely to have money to invest. These two groups are generally better in adopting DeFi than are earlier generations. This is not a feature unique to Thai society but rather a global phenomenon.

- The existence of individuals and companies that can give knowledge and advice on DeFi and DeFi-related investments in Thailand will help to boost uptake rates. Thailand already has a number of DeFi service providers, including DeFinix, a DeFi platform that allows users to invest in cryptocurrencies. Because they are able to give advice that is relevant to the local context, the presence in the market of companies established or staffed by Thais will help to diffuse knowledge about DeFi across the country and so increase public awareness and acceptance.

Significant challenges in the development of DeFi in Thailand: Both public bodies and the private sector will need to support each other’s work if DeFi is to make greater inroads into the Thai market.

- Thailand’s unbanked population is relatively small compared to countries that have seen a rapid uptake of DeFi services. The World Bank’s 2017 Global Finindex Database reveals that at that time, 18.4% of the Thai population did not have a bank account, which is significantly lower than countries with active cryptocurrency markets and high usage rates for DeFi services. For example, in Nigeria, around 60% of population do not have a bank account, while around 32% hold some cryptocurrency. In the Philippines, some 20% of the population hold cryptocurrency[27] but a full 65.5% lack a bank account. In these countries, connecting to banking services is thus both unusual and difficult, and this makes DeFi services much more attractive. In these contexts, using DeFi services can help to overcome an individual’s inability to open a bank account, whether that is caused by their not having an official identification or for another reason. In addition, the Thai economy has not seen a rapid expansion in new industries, in particular tech startups. As these are one of the main customers of DeFi loans, it is possible that more DeFi still cannot penetrate the broader Thai market.

- High income earners may be risk averse: This group has significant financial firepower but because they are familiar with traditional banking, members will tend to stick with it and avoid experimenting with innovations such as DeFi.

- The general public still lack the understanding of DeFi technology: As the co-founder and CEO of Dopple[28] said, “At the moment, the DeFi market is expanding faster than the understanding of it…but one of its most important sources of capital is exactly this knowledge.”[29]

- The regulations regulating DeFi and DeFi users remain largely unclear.

Given the considerations outlined above, Krungsri Research’s evaluation of the impacts of DeFi on the Thai banking sector is that it is having only a low impact across the areas of exchanges, loans and payments, but this may rise to a low-to-medium level impact in the future. Within the exchange segment, impacts will be clearest among Generation Y and Z consumers, but for the time being, the Bank of Thailand’s development of a retail CBDC is likely to be a more pressing issue. Nevertheless, looking out over the next 20 or so years[30], once society is dominated by generations Y, Z and Alpha[31], the impact of DeFi on Thailand will have become much clearer.

Krungsri Research View: How should Commercial Banks Prepare for the Rise of DeFi?

Interest in DeFi is building globally, and Thailand has not escaped this trend. The immediate impacts of this have so far been limited but in future, the distributed and decentralized nature of DeFi may pose a direct challenge to the traditional centralized financial systems. Both government-owned and private-sector banks are therefore rushing to better understand the structure, operations, and potential impacts of DeFi, hoping that this will better prepare them to meet these and then exploit any benefits that DeFi offers. The latter will include the ability to improve the customer experience for users accessing traditional banking services and this may then help banks maintain their central position in the financial system.

Many analysts believe that the rise of DeFi will erode the central place of banks within the financial system. However, Krungsri Research’s view is that the emergence of DeFi represents a unique opportunity for the commercial banking system to restructure its operations. Banks should therefore seize the moment and take the best of their traditional centralized services (their CeFi services) and combine these with newly developed DeFi activities. This might involve investing in existing DeFi platforms or setting up special units or subsidiary companies to exclusively look after DeFi-related operations. By mixing CeFi and DeFi in this way, banks could respond more precisely to individual market segments by offering each a range of financial services and products that better matched their particular needs. Banks should also perhaps view DeFi operations as allies that help them gain greater market insight. In light of this, banks should invest resources in researching DeFi and in improving their understanding of how new technology can be used to improve their own service offerings. This information should then be used to develop new business models that take account of the rapidly changing landscape within which banks are now operating.

However, if banks address the risks posed by the emergence of DeFi inappropriately, the situation may play out very differently. Although currently the DeFi sector may not be large, it could still present a significant threat to the banking sector. For example, it is possible that the rise of DeFi may rob banks of access to high-potential customers. Beyond this,

banks must also keep a close eye on developments in DeFi markets, and in particular on markets for digital assets, since booms and sell-offs on these markets have the potential to generate impacts on the financial system, with systemic risk potentially being spread by investors who play on both DeFi and CeFi markets.

Ultimately, DeFi will not be the last technological challenge that banks have to face. As long as humans walk the Earth, technological change will be a constant. Technological change is a tempest that constantly and ceaselessly beats at human institutions, and trying to stand rigid against this will be disastrous. If banks’ responses to the rise of DeFi draw exclusively from their traditional repertoire of business models, they are likely to experience a fate no different to the centuries-old tree that grows too stiff to bend with the storm, and instead ends broken on the ground. Much better to flex and turn, and faced with stiffening winds, banks need to adopt a policy of apprehend-accept-adjust-apply. By taking this more subtle approach, banks will be able to survive and prosper, even as the whirlwind of technological revolution accelerates by the day.

Reference

Adrian, Tobias (May 14, 2019) “Stablecoins, Central Bank Digital Currencies, and Cross-Border Payments: A New Look at the International Monetary System” Remarks at the IMF-Swiss National Bank Conference, Zurich, May 2019. Retrieved Sep 28, 2021 from

https://www.imf.org/en/News/Articles/2019/05/13/sp051419-stablecoins-central-bank-digital-currencies-and-cross-border-payments

Andrew Lisa (June 29, 2021) Which Countries Are Using Cryptocurrency the Most? Yahoo! Finance from

https://finance.yahoo.com/news/countries-using-cryptocurrency-most-210011742.html

Bitkom (2020) Decentralized Finance (DeFi) – A new Fintech Revolution?: The Blockchain Trend explained.

Consensys (2021) The Q1 2021DeFi Report: An analysis of Ethereum’s decentralized finance ecosystem in Q1 2021.

E.Napoletano and John Schmidt (April 2, 2021) Decentralized Finance Is Building A New Financial System. Forbes Advisor from https://www.forbes.com/advisor/investing/defi-decentralized-finance/

Fabian Schär (2021) Decentralized Finance: On Blockchain- and Smart Contract-Based Financial Markets. Economic Research Federal Reserve Bank of St.Louis Review. Second Quarter 2021, Vol.103, No.2

Igor Mikhalev (September 9, 2020). The Sudden Rise of DeFi: Opportunities and Risks for Financial Services. Linkedin from https://www.linkedin.com/pulse/sudden-rise-defi-opportunities-risks-financial-igor-mikhalev

Ivan Kot (January 18, 2021) 6 Use Cases for Smart Contract in Decentralized Finance. Finextra from

https://www.finextra.com/blogposting/19770/6-use-cases-for-smart-contracts-in-decentralized-finance

Phillipp Sandar (February 22, 2021) Decentralized Finance Will Change Your Understanding Of Financial Systems. Forbes from https://www.forbes.com/sites/philippsandner/2021/02/22/decentralized-finance-will-change-your-understanding-of-financial-systems/?sh=27e16db75b52

Polly Jean Harrison (March 25, 2021) ShuttleOne to Build DeFi Blockchain Solution for SME Lending and Remittance Market. The Financial Times

Rakesh Sharma (March 24, 2021) Decentralized Finance (DeFi) Definition. Investopedia from

https://www.investopedia.com/decentralized-finance-defi-5113835

Robert Farrington (March 23, 2021) Explainging DeFi And How It Will Revolutionize Financial Services. Forbes from https://www.forbes.com/sites/robertfarrington/2021/03/23/explaining-defi-and-how-it-will-revolutionize-financial-services/?sh=ca2506e1d080

World Economic Forum (June 2021). Decentrailzed Finance (DeFi) Policy-Maker Toolkit: White paper.

World Economic Forum (19 July 2021). How decentralized finance will transform business financial services – especially for SMEs. From https://www.weforum.org/agenda/2021/07/decentralized-finance-transaction-banking-smes/

Bitkub.com (March 16, 2021) องค์กรอัตโนมัติ DAO คืออะไร?. Finnomena from https://www.finnomena.com/bitkub/what-is-dao/

Blockchain Review (July 9, 2021) "มารู้จัก Stablecoin ประเภทต่าง ๆ ในโลกของ Cryptocurrency" Finnomena Web. Retrieved Sep 3, 2021 from https://www.finnomena.com/blockchainreview/what-is-stablecoin/

Charoenvit Sierra (September 6, 2021) สินทรัพย์ดิจิทัล (Digital Asset) คืออะไร,ซื้อขาย,เสียภาษียังไง? Livewithoutpay from https://www.livewithoutpay.com/cryptocurrenc/digital-asset/

eFinancethai (June 5, 2020) KULAP ได้รับใบอนุญาตประกอบธุรกิจสินทรัพย์ดิจิทัล (Digital Asset) from http://www.efinancethai.com/LastestNews/app.index.aspx?id=RXFGNmY0TEplVUE9&year=2020&month=6&lang=T&v=2018&security=

eFinancethai (July 31, 2020) Decentralized Finance (DeFi) คืออะไร? From https://www.efinancethai.com/advertorial/AdvertorialMain.aspx?name=ad_202007311854

eFinancethai (June 1, 2021) “DeFi” ศึกชิงอำนาจระหว่างโค้ดคอมพิวเตอร์ Vs น้ำหมึกปากกา from https://www.efinancethai.com/LastestNews/LatestNewsMain.aspx?id=Z1hzNWtjWFgvb0U9

[1] Cryptocurrencies are digital currencies that are encrypted, allowing transactions to be protected and verified through blockchains.

[2] Details are given in Box 1.

[3] Digital assets are units of digital data that serve as a medium of exchange, or to buy and sell goods and services. These are of two main types: (i) cryptocurrencies, and (ii) digital tokens, or units of digital data that represent an underlying investment in the token issuer (i.e., an investment token) or the right to acquire goods, services or other products (i.e., a utility token) as agreed by the token issuer.

[4] A protocol is an agreement that governs how equipment, machinery, programs or other structured data interact. Protocols are thus like languages that are shared by computers and that allow these to communicate with one another. For example, everyone who uses the internet makes use of TCP/IP (Transfer Control Protocol/Internet Protocol), which makes it possible for computers to share data via the internet. Thus, TCP/IP manages and organizes data to be transmitted and then checks for mistakes in communication when that data has been sent over IP networks. Another example is HTTP (Hypertext Transfer Protocol) that happens whenever a user requests data through a web browser.

[5] Stablecoins are particular types of cryptocurrency that are backed at a fixed rate by other assets. These may be other cryptocurrencies or assets in the real world (e.g., the value of 1 Dai is fixed at USD 1)

[6] APIs, or Application Programming Interfaces, provide a means by which computer applications can communicate with one another. In some ways, APIs are like telephones that programs or applications use to contact each other and then to exchange data from each database.

[7] For more information, please see “นโยบายส่งเสริม Open Banking: สิ่งที่เป็น สิ่งที่คาด และสิ่งที่หวัง” (September 2020)

[8] Governance tokens are tokens distributed by the network to users who participate in the overall management and governance of the system.

[9] MakerDAO, the first DAO to be built on the Ethereum blockchain, was created with the goal of facilitating loans. Bitkub explains DApps and DAOs with this analogy: “If you think of a DApp as a vending machine, a DAO is a vending machine that will use money put into it to make as many purchases as it can and then calculate the profit that could be generated by selling all of this back to investors.”

[10] ICOs, or initial coin offerings, are a way of raising capital by selling digital tokens to the public via a blockchain. Those looking to raise funds through an ICO will issue digital tokens in return for funding in one of the main cryptocurrencies, such as Bitcoin or Ether.

[11] Tobias Adrian (2019) “Stablecoins, Central Bank Digital Currencies, and Cross-Border Payments: A New Look at the International Monetary System”

[12] As of August 6, 2021

[13] eFinancethai (July 31, 2020) “Decentralized Finance (DeFi) คืออะไร?”

[14] The DeFi Adoption Index is developed from three components: (i) the value of on-chain cryptocurrency received by DeFi platforms, weighted according to per capita PPP (a measure of the country’s wealth per resident); (ii) the total retail value received by DeFi platforms; and (iii) the value of individual deposits to DeFi platforms.

[15] https://blog.chainalysis.com/reports/2021-global-defi-adoption-index

[16] eFinancethai (June 5, 2020) “KULAP ได้รับใบอนุญาตประกอบธุรกิจสินทรัพย์ดิจิทัล (Digital Asset)”

[17] https://techsauce.co/pr-news/kbtg-company-establishment-kubix-run-business-digital-assets

[18] ICO portals provide electronic services related to the offering of newly issued digital tokens, which includes screening these for quality. They therefore assess the originator’s standing and the accuracy and completeness of their registration statement.

[19] https://www.scb.co.th/th/about-us/news/mar-2564/scb10x-band-protocol.html

[20] Cross-chain functionality allows blockchains that are built on different systems (e.g. on bitcoin and ethereum blockchains) to be interoperable.

[21] https://www.scb.co.th/th/about-us/news/mar-2564/scb10x-band-protocol.html

[22] https://www.brandbuffet.in.th/2021/01/scb-token-x-ico-portal-service/

[23] https://www.prachachat.net/finance/news-732821

[24] The eight commercial banks are: Krungsri, Bangkok Bank, Kasikorn, SCB, Krungthai, Thanachart, Standard Chartered, and HSBC.

[25] Techsauce (June 17, 2021) “นักวิเคราะห์มอง CBDC ของธนาคารกลางเกิดมาเพื่อเสริม Crypto และอุดช่องโหว่ DeFi”

[26] This includes the services provided by digital asset exchanges, digital asset brokers, digital asset dealers, digital asset fund managers, and investment advisors.

[27] yahoo!finance (June 29, 2021) “Which Countries Are Using Cryptocurrency the Most?”

[28] This is a DeFi platform for stablecoins trading.

[29] eFinancethai (June 1, 2021) ”DeFi” ศึกชิงอำนาจระหว่างโค้ดคอมพิวเตอร์ Vs น้ำหมึกปากกา

[30] The Office of the National Economic and Social Development Council estimates that by 2040, 31.28% of the population will be aged over 60. In the same year, the oldest members of Generation Y (born between 1980 and 1996) will be exactly 60.

[31] Generation Alpha is defined as those born between 2010 and 2024. Members of this generation will grow up immersed in new technology and so will be proficient users of this and will likely be able to adapt quickly to future technological change.