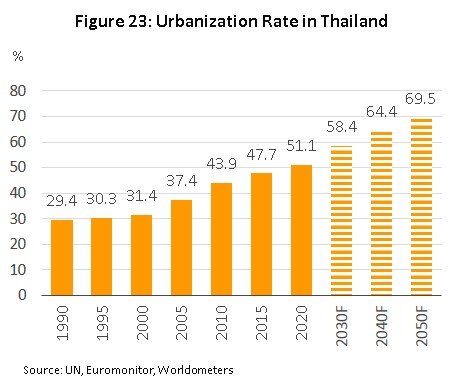

Over the three years from 2021 to 2023, the value of the domestic market for ready-to-eat food will gradually rise. In the coming period, many consumers will need to exercise greater care over their spending, and because instant noodles are a low-cost product, somewhat unfavorable economic conditions will feed into low levels of growth. Sales of chilled and frozen ready-to-eat food will also be helped by the continuing and rapid expansion in the number of modern retail outlets, which with over 90% of the market are these products’ principal distribution channel. In addition, increasing rates of urbanization are also precipitating changes in consumer behavior that favor greater speed and convenience in food preparation and consumption.

Exports (15-20% of the market) are also forecast to see solid rates of growth. As vaccination programs make greater progress and, exports of instant noodles will benefit from the steady relaxation of checks and controls on cross-border trade and travel and the reopening of border checkpoints. The market for chilled and frozen ready-to-eat foods will expand aligned with trading partner’s economic growth. Beyond this, consumers in world markets are increasingly accepting of Thai food with regard to both its safety and its taste, and because consumer perceptions are favorable and in accord with deepening concerns over personal health and wellness, this too will help to lift export sales.

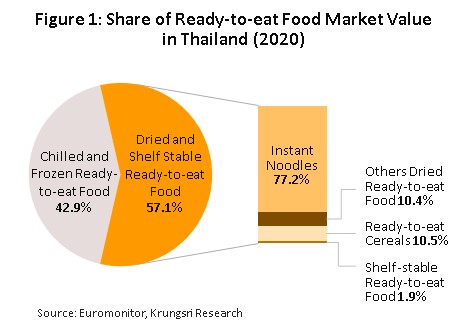

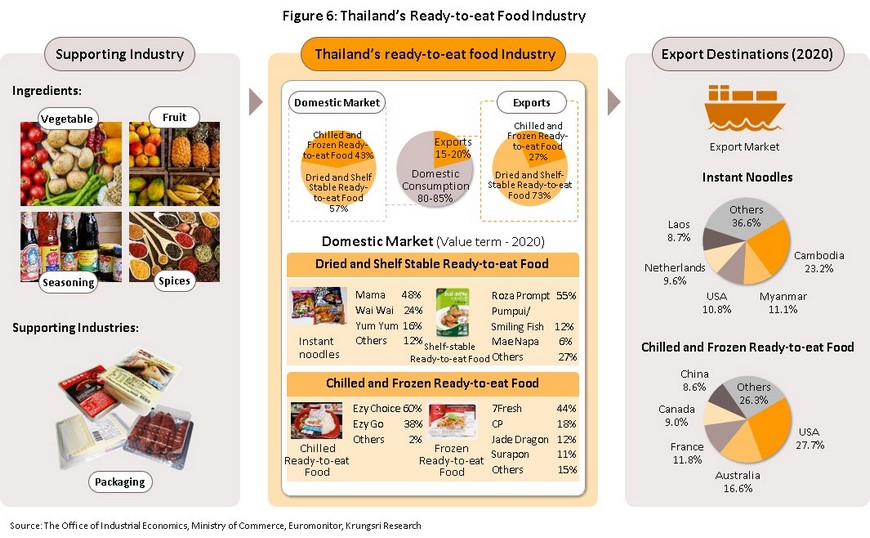

Ready-to-eat food is food that has been processed in such a way that it is both preserved or had its shelf life extended and has been put into a state that makes it easy to consume. Ready-to-eat food can be split into two main categories, according to the processing and preserving techniques that are used (Figure 1).

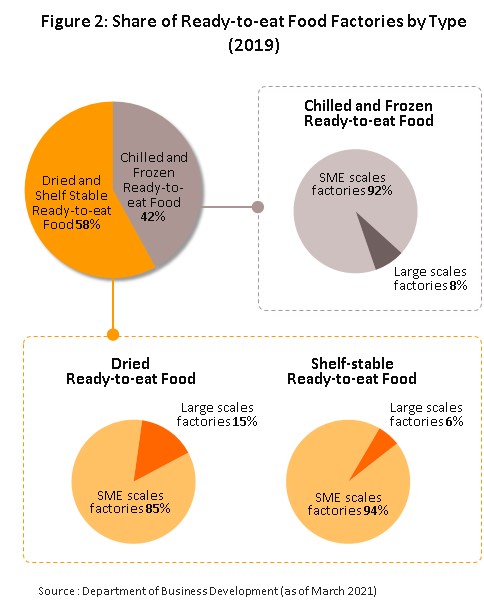

As of 2019, there were 229 facilities producing ready-to-eat foods that were registered with the Department of Business Development, the vast majority of which were SMEs. These may be split into two groups. (i) 96 (or 42%) produced dried and shelf-stable goods. 13 of these made dried foods, mainly instant noodles, and of these 11 (or 85%) were SMEs, the remainder being large-scale operations. 83 factories produced shelf-steady goods, and 78 of these (94%) were SMEs. (ii) 133 sites (58% of the total) produced chilled and frozen ready-to-eat food, with 122 of these (92%) being SMEs (Figure 2).

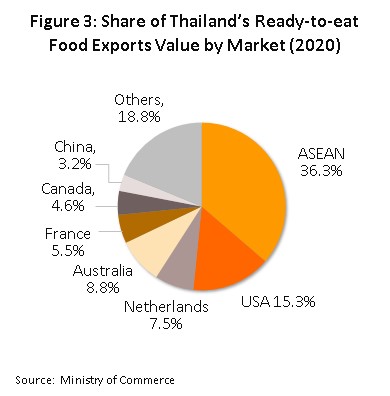

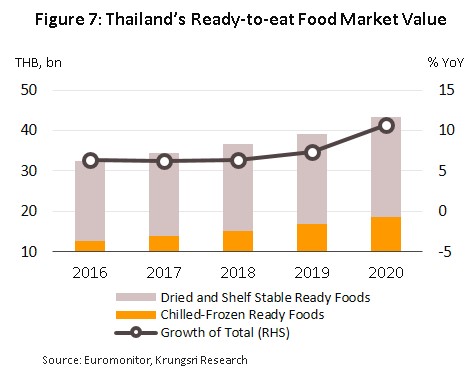

Thai producers of ready-to-eat food largely focus on the domestic market, and over 2016-2020, this absorbed 80-85% of the industry’s output. In 2020, the Thai market had a total value of THB 44 billion, split between THB 25 billion for dried and shelf-stable goods and THB 19 billion for chilled and frozen meals. The 15-20% of output that is bound for overseas markets generated USD 328.9 million in 2020, with Thailand enjoying an advantage in the production and export of instant noodles and chilled and frozen meals. The main export markets are the ASEAN region (36.3% of exports by value), followed by the United States (15.3%) and the Netherlands (7.5%) (Figure 3).

Within the dried and shelf-stable segment, instant noodles comprise the main product category. Here, Thai players benefits from the size of the domestic market, which has helped to generate significant economies of scale for manufacturers, and this then helps to support cheaper production and stronger exports. However, the market is approaching saturation and competition is intensifying, and as it becomes more difficult to maintain growth. Therefore, players are increasingly looking to expand into export markets, especially in the ASEAN region and the US. By contrast, the chilled and frozen ready-to-eat segment is largely still concentrated on the domestic market. These foods benefit from the fact that they are easy to consume, are sold at price points that are similar to those of freshly prepared foods, and are extremely easy to purchase since they are distributed through convenience stores that have very extensive national networks. At present, exports are not a major contributor to earnings but these have the potential to grow, given the widespread preference for Thai food and these products’ attractive prices. Details of these two main segments are given below.

Instant Noodles

- As of 2020, the market for instant noodles was worth around THB 20 billion. Within Thailand, sales are dominated by Thai President Foods (producers of Mama), Thai Preserved Food Factory (operators of the Waiwai brand) and Wan Thai Foods Industry (selling under the Yam Yam brand), which collectively enjoy an almost 90% market share. Because these players manufacture in such significant quantities, they also enjoy economies of scale, as well as having advantages in terms of access to raw materials and capital, their brand recognition, and their well-developed distribution networks.

- Consumer demand for instant noodles has increased steadily, helped by low prices and the ability of the product to meet buyers’ basic needs when spending power is low and access to fresh foods is limited. Instant noodles also benefit from being a favored product across most consumer groups, regardless of age or sex, and players are constantly expanding their markets by adding new and unusual flavors.

- Costs typically move with the price of wheat flour (70% of raw material costs) and palm oil (20% of costs, with the remaining 10% going to the manufacture of flavorings). Because wheat cannot be grown locally, raw materials must be imported, and this exposes players to risks arising from variations in exchange rates, while the sale price of instant noodles is also controlled by the authorities, limiting the room that players have to raise prices.

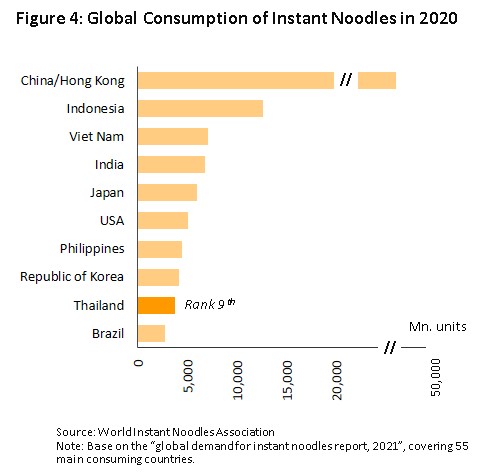

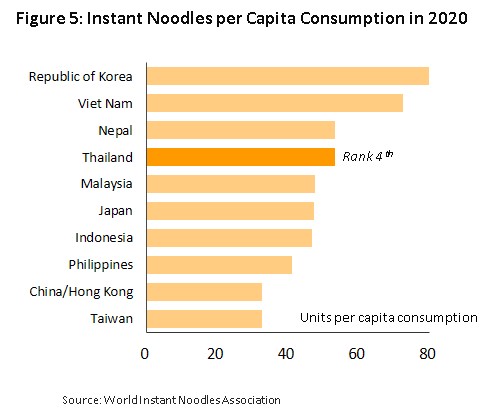

- Over the period 2016-2020, 80-85% of Thai instant noodle production was for distribution to the domestic market, which in 2020, consumed 3.71 billion packets of instant noodles, sufficient to rank the Thai market 9th in the world. However, in terms of per capita consumption, at 53.2 packets per person per year, Thai consumption is the 4th highest in the world, coming after only South Korea (79.8 packets/person/year), Nepal (72.4 packets/person/year) and Vietnam (53.4 packets/person/year). This compares to average global consumption of 15.3 packets per person per year (source: World Instant Noodles Association: WINA), indicating that the domestic market is close to saturation. At the same time, competition is building from the large range of alternative ready-to-eat products as well as from imported noodles, especially those from South Korea and Japan, which are gradually having a greater presence in the market. Manufacturers of instant noodles are thus having to develop new products and adopt new strategies as they fight more intensely for market share, including increasing investment in marketing and spending more heavily on television advertising and product promotions. Export markets soak up around 15-20% of output, though exports have been helped by the implementation of the AFTA free-trade agreement in the ASEAN zone. Because the latter is a large market with relatively low levels of instant noodle consumption, this now presents players with the opportunity for significant expansion, especially into markets in Cambodia, Myanmar, Vietnam and Lao PDR. These countries account for over 40% of the value of instant noodle exports, and consumers in these countries are generally positively inclined towards Thai products, being familiar with Thai flavors and having faith in the quality of Thai goods.

Chilled and frozen ready-to-eat food

- In 2020, the Thai market for chilled and frozen ready-to-eat foods was worth approximately THB 19 billion. These products are favored by consumers since they are easy to eat and the chilling or freezing process leaves the food’s flavors and nutritional values largely unaffected. To meet different tastes, manufacturers typically produce meals in a wide range of styles, but Thai dishes are the most widely consumed (45% of the market by value), followed by Chinese (29%), Italian (11%), Japanese (6%) and other (9%) (source: Euromonitor, December 2020).

- Producing chilled and frozen meals does not require large-scale investment or the mastery of complicated technology and so entry to and exit from the market is relatively straightforward. Given this, there is an abundance of suppliers in the market and thanks to their low levels of product differentiation, competition is stiff. In addition, producers have to contend with strong competition from a diverse range of alternative products that include tinned goods, instant noodles and freshly prepared food, such as fresh noodles and rice dishes. Consumers also face only very low brand switching costs, and so producers compete through marketing and the development of new products that have novel flavors or other innovations, hoping that new offerings will attract consumers. Major players active in the production of chilled and frozen meals have advantages with regard to their manufacturing capabilities and brand recognition, and these include CP All, Charoen Pokphand Foods, Prantalay Marketing, S & P Syndicate, Surapon Foods, and Ek-Chai Distribution System. These companies have a combined market share that covers over 90% of sales.

- Through the period 2016-2020, an average of around 80-90% of Thai-made chilled and frozen ready-to-eat food was consumed by the domestic market. Demand within Thailand is supported by continuing growth in rates of urbanization, which brings with it changes to consumer behavior that favor food that is easy and convenient to buy and consume. In addition, these products are distributed through convenience store networks that have a very extensive national reach and that are typically open 24 hours per day. 10-20% of output is bound for export markets, where Thai products have an advantage thanks to manufacturers’ access to a ready supply of raw materials and overseas consumers’ acceptance of Thai food with regard to both its flavor and quality. This is particularly so for frozen foods, since the freezing process keeps food fresh and flavors intact for up to 18 months, an important consideration given the long transit times to some destinations.

Situation

The Thai ready-to-eat food industry enjoyed average annual growth of 7.4% over the years 2016-2020, helped by increasing rates of urbanization in Thailand that in turn drove changes in lifestyle and supported greater demand for products that emphasize ease and convenience. Over the same period, exports also saw steady growth. Details of this are given below.

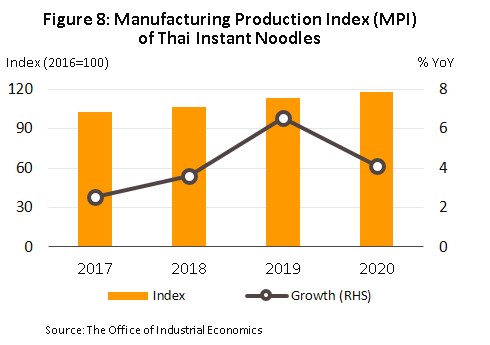

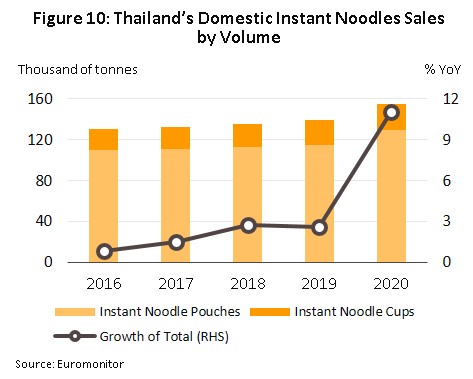

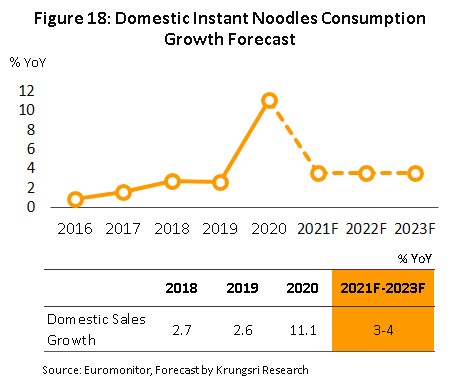

Instant noodles: Over 2016-2020, output rose constantly, as reflected in the 4.2% average annual climb in the industry’s manufacturing production index (MPI), at an average level of 107.9. These increases were driven by strength in the domestic market (where the bulk of sales are made), which expanded 3.8% annually in terms of volume and 4.9% in terms of value, Exports jumped 12.3% per year.

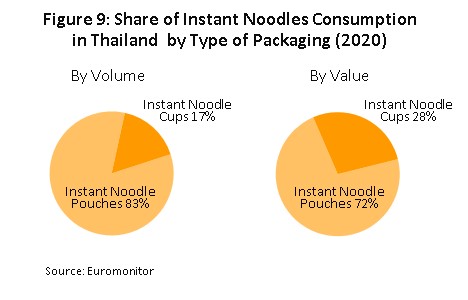

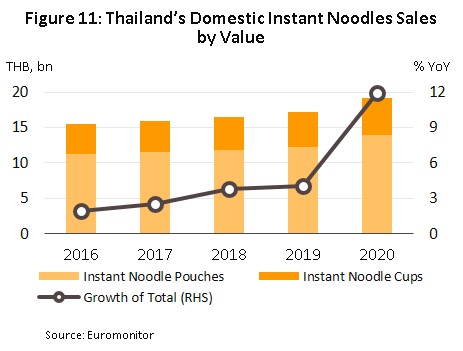

- In 2020, the domestic market recorded growth of 11.1% by volume (to 160,000 tonnes) and 11.9% by value (to THB 19 billion). Growth was seen in sales of both pouches (up 12.3% by volume and 13.9% by value) and cup/bowl-packaged noodles (up 5.9% by volume and 6.9% by value). Sales received a strong boost from the outbreak of Covid-19 and the decision by the government to introduce a lockdown and curfew in the second quarter of the year1/, which then encouraged consumers to stockpile long-lasting food at home.

Competition on the domestic market is somewhat intense, with three players holding an 87.7% market share (as of 2020). These three are Thai President Foods, the producers of Mama (which has a 48.4% market share), Thai Preserved Food Factory, owners of the Waiwai brand (23.6% market share) and Wan Thai Foods Industry, which runs the Yam Yam brand (15.7% market share). Also active in the market is Nong Shim, an importer of instant noodles from South Korea that are sold under the Nong Shim brand (1.2% market share) and Nissin Food (Thailand), a Japanese brand that has a 0.7% market share. The remaining 10.4% of the market is shared between a number of less important brands.

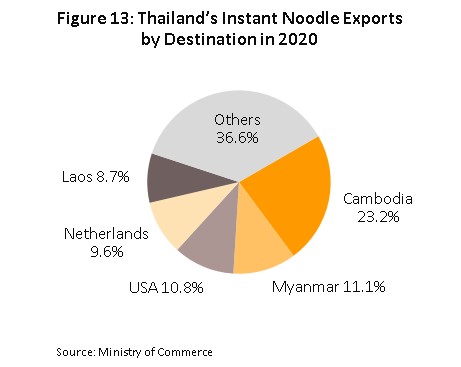

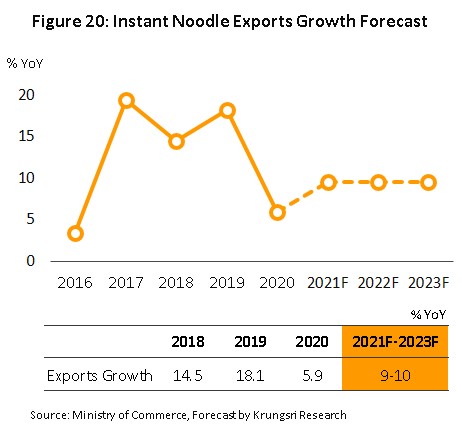

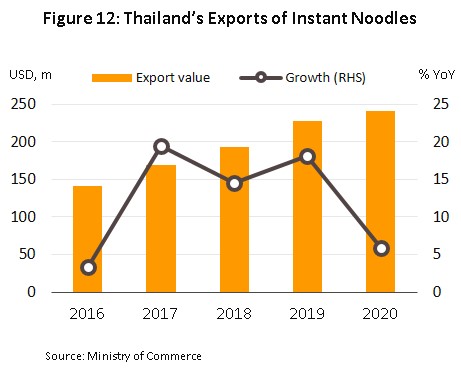

- In 2020, Thai producers exported USD 241.5 million worth of instant noodles. This represented an increase of 5.9%, though this was the lowest rate of growth recorded since 2017. (i) The global economy and trading partners’s economies all slowed in the year, including in Thailand’s major markets of Cambodia (23.2% of the value of all exports of Thai instant noodles), Myanmar (11.1%), the US (10.8%), the Netherlands (9.6%) and Lao PDR (8.7%). (ii) A large number of border crossings between Thailand and Cambodia, Myanmar and Lao PDR (which together buy 43% of Thai exports) closed in 2020, and indeed only 35 out of 97 checkpoints remained open through the year, while to help slow the spread of Covid-19, checks on goods in transit also became more onerous.

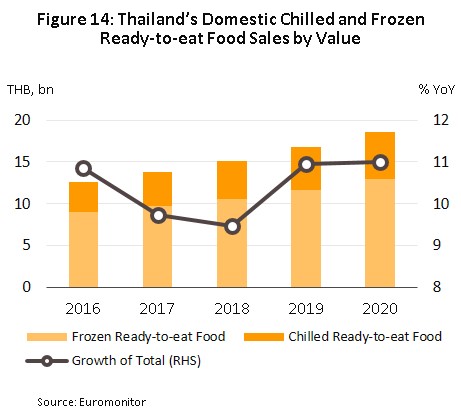

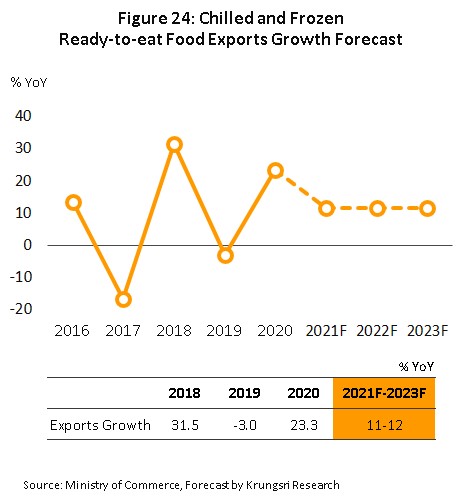

Chilled and frozen ready-to-eat food: This segment saw strong growth through 2016-2020, with sales into the domestic market (the main consumer of Thai products) expanding by 10.4% annually and generating some THB 15 billion per year. Over the same period, exports rose by an average of 9.7% per year, bringing in USD 70.8 million annually.

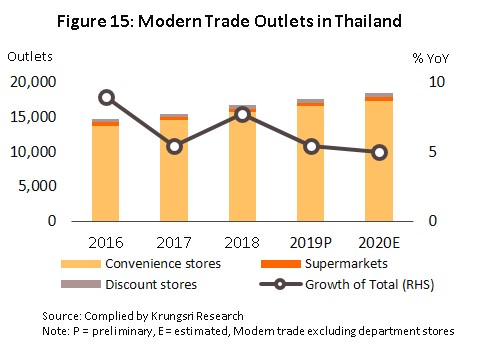

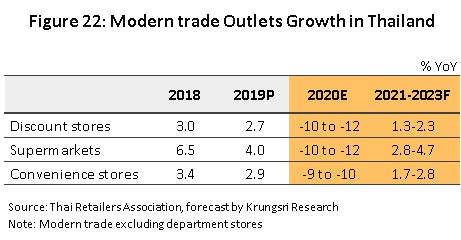

- In 2020, the Thai market for chilled and frozen ready-to-eat food expanded by 11.0% to a value of THB 19 billion, split between THB 5.6 billion from chilled foods (10.3%) and THB 13 billion from frozen foods (11.3%). Growth was driven by (i) worries over the spread of Covid-19 and with consumers stuck at home, many chose to stockpile food; (ii) continuing expansion in the number of modern trade outlets, especially of convenience stores, supermarkets, and discount stores (sales through these three types of retail outlets represent a full 92% of all sales of chilled and frozen meals in Thailand); (iii) ongoing urbanization, which is encouraging a greater number of Thais to adopt lifestyles that favor speed and convenience; (iv) moves by producers to develop new flavors and to expand the range of dishes on offer; and (v) the relatively low cost of most frozen and chilled foods, which, because manufacturers produce in bulk, are priced at a level that makes them competitive with freshly prepared meals.

Competition is somewhat stiff within this segment, and the market is dominated by a few large players that are able to draw on their advantages with regard to access to raw materials and distribution channels. CP All occupies a monopoly position in the market for chilled ready-to-eat foods, and operating under the brands Ezy Go and Ezy Choice, the company holds a 98.0% market share by value (as of 2020), partly thanks to the company’s ability to distribute through the large number of convenience stores that are operated by companies in the same commercial group. Sales of frozen meals are controlled by CP All, which sells under the brand Seven Fresh and has a 44.5% market share, and Charoen Pokphand Foods. The latter has a 17.8% market share under its CP brand and another 11.6% under the Jade Dragon brand, though both CP All and Charoen Pokphand Foods are part of the same commercial group, and so they have a combined 73.9% market share. Against this, other players have only a relatively slight presence in the market. These include Surapon Foods (Surapon brand, 11.2%), S&P Syndicate (Quick Meal, 5.2%), Thai Agri Foods (Little Chef, 2.8%), Prantalay Marketing (Prantalay, 0.9%, and Pranprai, 0.7%) and Ek-Chai Distribution System (Tesco, 0.7%). A number of other smaller companies account for the remaining 4.6% of the market.

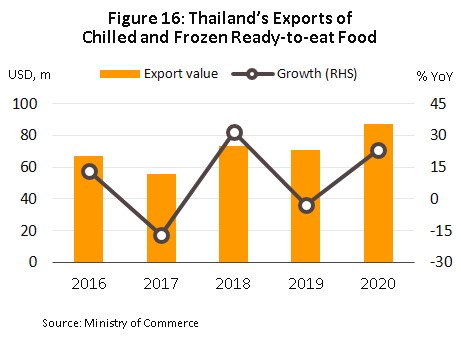

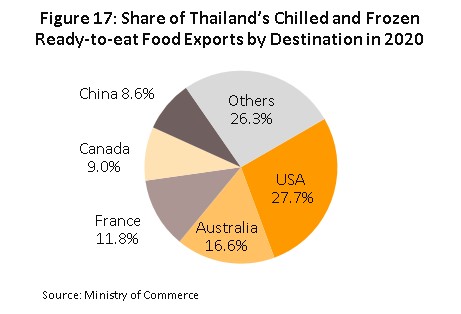

- In 2020, income from exports jumped 23.3% to USD 87.4 million. Sales were lifted by the outbreak of the Covid-19 pandemic, which forced governments around the world to introduce lockdowns as they tried to slow the spread of the disease, and in response many consumers stockpiled goods at home, especially food with a longer shelf life. In addition, markets are increasingly accepting of Thai chilled and frozen meals and consumers (especially in the US and Europe) are turning to Asian, and in particular Thai, food as a healthy, novel and tasty alternative, while the development of the new generation of refrigerators which have larger freezer compartments is also encouraging consumers to stock up on chilled and frozen meals2/. Export markets reporting the greatest rates of growth in 2020 were China (up 655.1%), the US (36.6%), Canada (36.3%), Australia (26.4%) and France (7.2%).

Outlook

Overall, the ready-to-eat food industry should see continuing growth through the years from 2021 to 2023. Domestic demand for instant noodles will strengthen, but only to a limited degree and competition will likely worsen, though because the economic outlook remains uncertain, consumers will tend to be more careful about their spending and as they try to keep their expenses under control. Exports are also expected to strengthen. Sales of chilled and frozen ready-to-eat foods to both domestic and export markets are forecast to see stronger growth, helped by expansion in the modern trade sector at home and increasing consumer preference for Thai food in some overseas markets. Factors that will have a significant impact on the market for each category of ready-to-eat food are outlined below.

- Instant noodles: Domestic demand is forecast to strengthen by an average of 3-4% per year. The uncertain outlook for the economy will tend to encourage consumers to be more careful about their expenditure and because instant noodles are a low-cost food, economic weakness will likely stimulate stronger sales. However, in 2020, Thai consumption of instant noodles averaged 53.2 packets per person per year against a global average of 15.3 packets per person per year, which tends to indicate that the domestic market is close to saturation (Figure 5). Competition is also strong from alternative products, including shelf-stable ready-to-eat food, chilled and frozen read-to-eat foods, and freshly prepared food, as well as from goods such as bakery products, snacks, cereals and ready-to-drink milk products, and increasing sales of these may help to raise competitive pressure within the segment. In response, manufacturers will tend to develop new products as they try to extend their appeal to consumers. The latter will include producing noodles with new and different tastes and textures, packaging these in new ways (pouches, cups and bowls) and releasing higher-end products to counter the challenge posed by Japanese and Korean imports. Challenges may also arise from government policy in the form of the proposed tax based on sodium content (the ‘salt tax’3/), which may then add to players’ manufacturing costs.

Over 2021-2023, the value of exports is forecast to rise by an average of 9-10% per year, lifted by recovery in trade partners’ economies. In particular, the rollout of vaccination programs will help to suppress the impacts of Covid-19, and this will ease restrictions and checks on cross-border trade and help to encourage the authorities to reopen border crossings that have been temporarily shut. Over the longer term, rates of consumption of instant noodles are currently rather low in many ASEAN nations, especially in Cambodia (7.3 packages per person per year) and Myanmar (12.4 packages per person per year) (Figure 19), and this will thus present an opportunity to Thai players to increase sales. Nevertheless, Myanmar’s deep political problems and uncertainty over the rules governing cross-border trade4/ present a significant risk to the future of Thailand’s second most important export market for instant noodles (in 2020, sales to Myanmar contributed 11.1% of all receipts from the export of instant noodles, second only to Cambodia, with 23.2%).

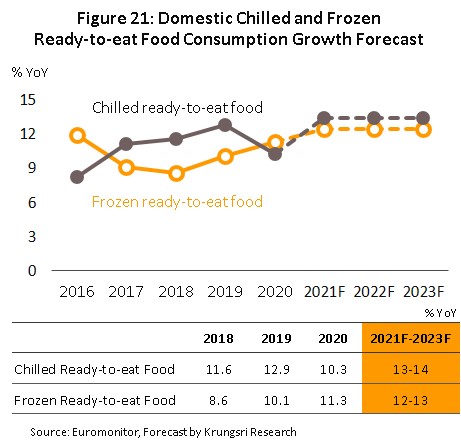

- Chilled and frozen ready-to-eat food: Over the next 3 years, the value of sales of these is expected to climb by 12-14% per year, split between annual average growth of 13-14% for sales of chilled food and of 12-13% for frozen meals. This outlook will be supported by: (i) an extension in the already large number of modern trade outlets, and in particular of convenience stores, which will then provide consumers with even easier access to prepared foods; (ii) increasing urbanization and with this, a growing desire for convenience; (iii) the development of new product lines and national cuisines, including Chinese, Japanese and Italian dishes; (iv) the fact that chilled and frozen meals are generally more nutritious than dried ready-to-eat foods; (v) the spread of new refrigerators with freezer compartments and the falling price of microwaves, which allows consumers to better store and prepare chilled and frozen food at home; and (vi) ongoing price cuts and other promotional campaigns laid on by modern trade outlets. However, the development of new products of other ready-to-eat foods (i.e., shelf-stable goods and freshly prepared foods) together with an increasing range of alternative products including bakery goods, snacks, and cereals may also help to stoke an increase in competitive pressures.

The value of exports is forecast to climb at an annual average rate of 11-12% over the period 2021-2023, helped by: (i) an improving economic outlook in export markets, especially once vaccination programs make greater headway; (ii) improvements in food technology that will allow food processors to release chilled and frozen foods that better match the flavor and quality of freshly made food; (iii) the development of a broader and more interesting range of dishes that appeals to a wider range of buyers; and (iv) the increasing popularity of Thai food in many countries, where it is now accepted as a safe and healthy. Nevertheless, despite these tailwinds, the industry will face challenges in the form of stricter checks on food exports, including the necessity of meeting HACCP, GMP, and ISO 9001-2000 standards, as well as in some cases having to conform to halal traditions. Stricter rules over labelling and requirements for supply chain tracking and traceability may also add to operators’ manufacturing costs.

Krungsri Research’s view:

Overall, players in the ready-to-eat food industry will see solid rates of growth in income over the three years from 2021 to 2023. The domestic and export markets for frozen ready-to-eat foods will benefit from the continuing expansion in the number of modern trade retail outlets as well as from the steady increase in rates of urbanization. Exports of instant noodles are also expected to grow well, but domestic sales will be limited by the fact that the Thai market for instant noodles is reaching its limits. Players will also have to contend with the possibility that the Thai government may impose a salt tax on their products, which would then increase costs and erode profitability.

Manufacturers of instant noodles: Players’ income will rise with what is likely to be an only slow economic recovery, though this will help sellers of instant noodles since while the economic outlook remains uncertain, consumers will likely try to cut their expenses by increasing purchases of instant noodles. Unfortunately, since the domestic market is close to saturation, the extent to which this will help producers will be limited, while worsening competition will force manufacturers to develop and release a steady stream of new products. In addition, other types of ready-to-eat products and alternative foods will also threaten to steal market share, while the government is actively considering introducing a tax on the sodium content of processed food (likely to be implemented in 2022 or 2023), which would then add to production costs and so erode the ability of manufacturers to generate profits. On the other hand, exports should see stronger rates of growth thanks to economic recovery in export markets and the current low levels of consumption of instant noodles in many countries, though in particular in the major export targets of Cambodia and Myanmar (respectively the 1st and 2nd most important export markets for Thailand, with a 23.2% and 11.1% share each of Thai exports). The latter thus represents a clear opportunity for Thai manufacturers to expand their markets.

Manufacturers of frozen ready-to-eat food: Income is expected to rise moderately, supported by strength in the domestic market that will come from the continuing expansion in the number of modern trade outlets, increasing rates of urbanization, a diversification of the food types on sale, and the impact of sales promotions and price discounts organized by modern trade retailers as they look to attract customers. The outlook is also positive for exports, which should rise with economic growth in trading partner countries, boosted further by the fact that in many countries, Thai food is now viewed favorably in terms of flavor and safety. Nevertheless, challenges will persist, in particular from a tightening of controls and checks on food imports, including the need to meet HACCP, GMP, ISO 9001-2000 and halal standards, and additional requirements for food labeling and supply chain tracing and accountability, which may then add to manufacturing costs.

[1] The government imposed a curfew from 22.00-04.00 that ran from 3 April to 17 May, when it was shortened to 23.00-04.00. The curfew was shortened again (to 23.00-03.00) on 1 June, and was then lifted entirely on 30 June.

[2] Source: Utsahagamsan, the journal of the Department of Industrial Promotion.

[3] The Excise Department is currently assessing the potential impacts of this tax, which is expected to be implemented in 2022-2023.

[4] From 1 May, 2021, officials in Myanmar have banned the import of non-alcoholic drinks (including energy drinks, carbonated and other sugary drinks, ready-to-drink coffee, mixed coffee and tea drinks, fruit juices and milk drinks) through land crossings with Thailand. Importers are instead now required to ship goods via boat, extending transit times from just 1 day (for shipments to Yangon and some other provinces) to 1 week. This has then added to transport costs and pushed up prices for Thai-made soft drinks.

.webp.aspx)