Global: Multi-speed recovery with crisis legacies

Global economy is on a gradual recovery path; COVID-19 crisis leaves permanent loss of supply potential

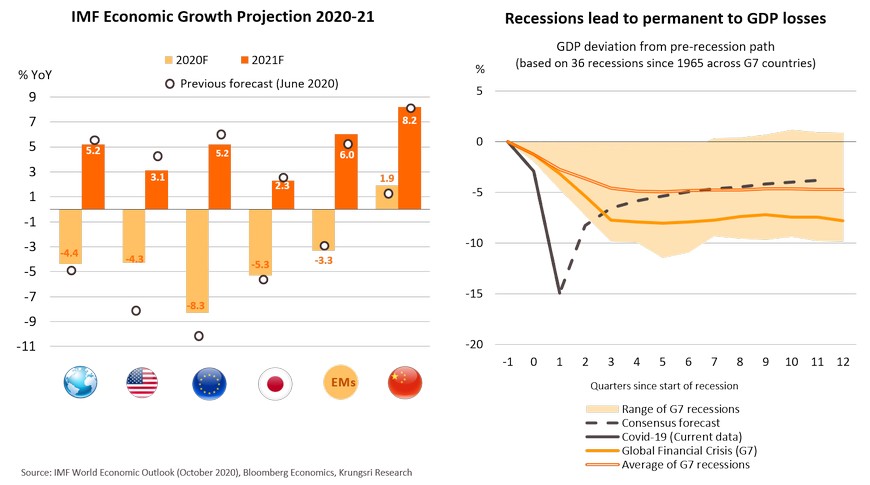

The IMF nudged up 2020 global growth forecast but revised down 2021 growth, citing “A Long and Difficult Ascent”. Historical data of G7 economies compiled by Bloomberg suggest that on average, a recession takes an economy 4.7% below its pre-downturn path and the gap persists for up to three years.

US: More solid economic recovery next year, but full-fledged recovery would take longer

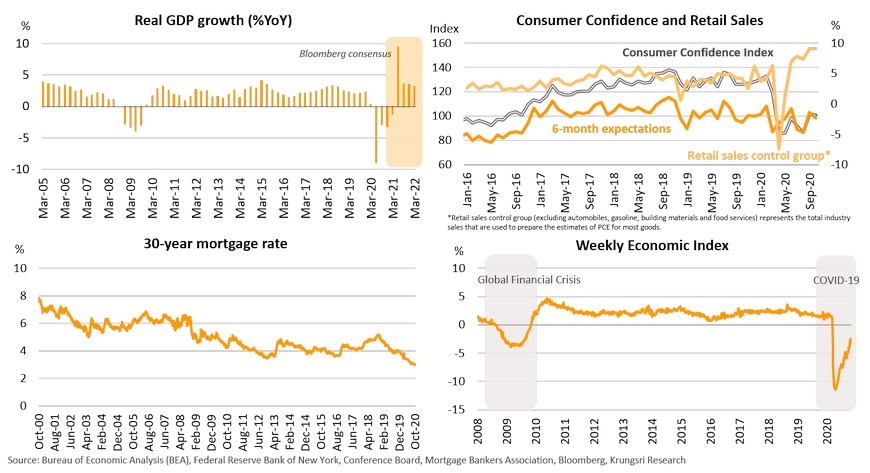

US Real GDP is projected to rebound strongly to 9.5% in 2H21 and return to potential growth of 3% in 2021. The massive stimulus would continue to help the economy to normalize gradually. Consumption and housing sector would be the major growth drivers. There are several positive signs, including a rebound in 6-month Consumer Expectation Index to pre-pandemic level. “Retail sales control group,” an indicator of personal consumption expenditure, has also exceeded its pre-outbreak level. And, supported by monetary stimulus, current record-low mortgage rate (3.0%) would continue to support the housing market which is a bright spot in the economy. The Weekly Economic Index, an indicator of overall economic activity, continued to recover. However, this crisis created a bigger slump than the Global Financial Crisis, suggesting it would take longer to return to normal. We expect the overall economy to recover at a more solid pace in 2021, but it could take two years to reach a full-fledged recovery due to elevated unemployment.

Extension of unemployment aid would support labor market and consumer spending

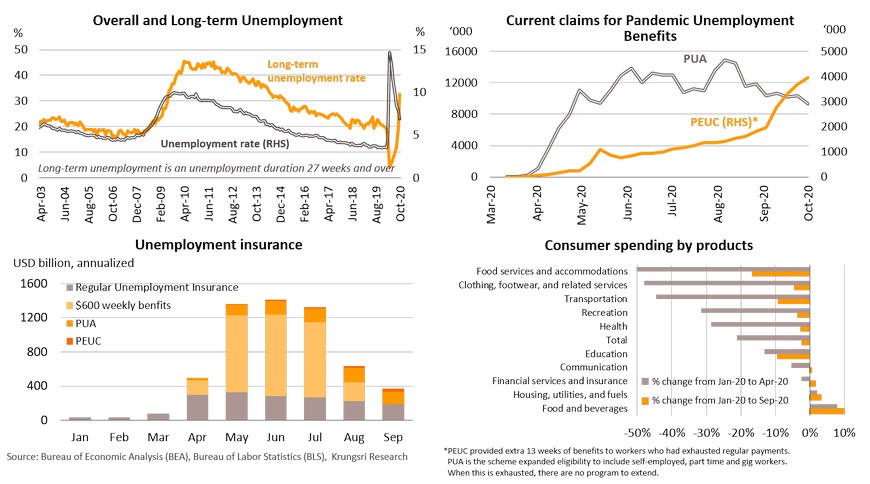

Although overall unemployment has gradually improved to 6.9%, long-term unemployment continued to rise to 32.5% in October 2020, indicating the crisis is leaving a scar on the labor market. Workers are currently receiving Pandemic Emergency Unemployment Compensation (PEUC) and Pandemic Unemployment Assistance (PUA) after the USD600 weekly payment ended in July. These programs will also end this year but they unlikely to pose a major risk on the economy. According to BEA estimates, the PEUC and PUA are worth USD175bn annualized in September or 1% of personal income, which is relatively low compared to USD900bn (4.5% of personal income) for the USD600 weekly benefits. The expiration of these two programs would have a mild impact on the labor market but that can be offset by extending the programs in early 2021. The extension would support consumer spending, especially since it has improved significantly compared to during the peak of the outbreak.

Additional fiscal stimulus would be sufficient to support recovery despite smaller aid than previous packages

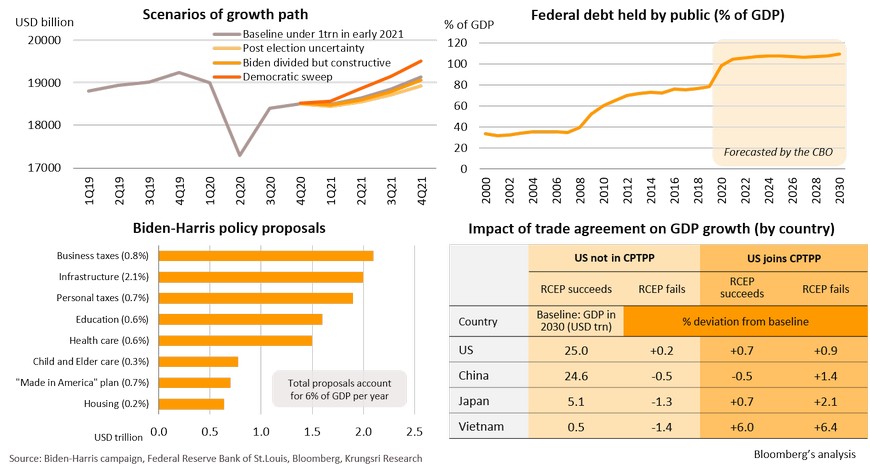

Fiscal policy and additional bills are back in the spotlight following Biden’s win with a split Congress. The split Congress might reduce the fiscal stimulus bill to USD 1trn from the proposed USD1.5-2trn as (i) the economy has rebounded strongly since 3Q20, leaving GDP at only 3.5% below pre-pandemic level, and (ii) public debt is expected to rise to 104% of GDP in 2021, which could limit policy room. Moreover, a Republican-majority Senate might hamper policy approval or new regulations. Then, Biden can partially implement his proposal to spend more infrastructure over 4 years, up to USD2trn (2.1% of GDP), due to concerns over higher tax rates during the nascent recovery. On trade policy, the US might return to the CPTPP rather than join RCEP, because of lingering US-China tension. Rejoining the trade agreement would benefit the US economy and lift GDP by 0.2-0.9% from baseline, and support growth of their trade partners’ economies.

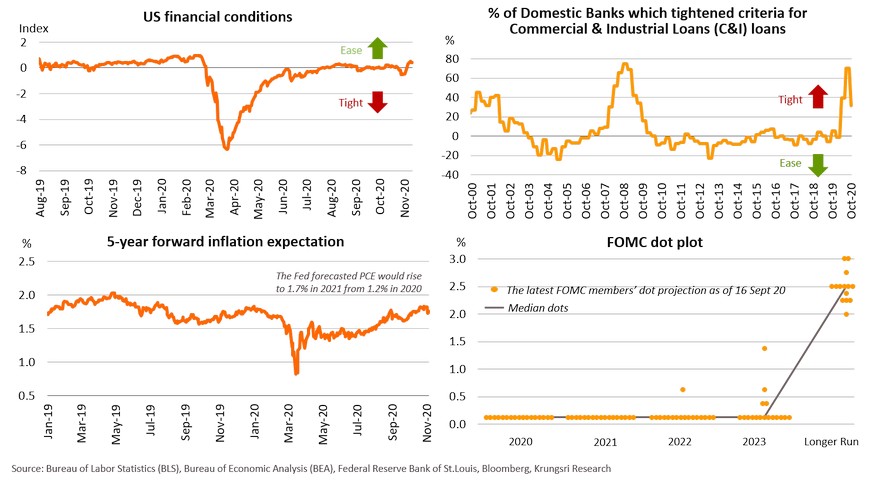

Crisis scars and low inflation imply record-low rates; still-tight credit standards suggest more alternative policy

Financial conditions have recovered since the sharpest tightening in 1Q20 and 2Q20, reflecting recent improvements in liquidity in financial markets. On credit standards, the net percentage of banks which have eased criteria for commercial and industrial loans has dropped from 70% in September to 31% in October. However, conditions remain tighter-than normal, implying businesses are still facing difficulty accessing credit. On price stability, we project inflation would converge towards the 2% target in 2H21 as a vaccine would unleash pent-up demand. However, the 5-year Forward Inflation Expectation suggests inflation would stay below the official target in 2021. Thus, the Federal Reserve would keep an accommodative policy and short-term borrowing rates anchored to 0%-0.25%. The FOMC Dot Plot suggests only 4 of the 17 members anticipate interest rates need to be raised before the end of 2023.

Unconventional policy to continue with a slightly more dovish stance

Europe: Growth trajectory differs markedly between countries; structural challenges weigh on recovery

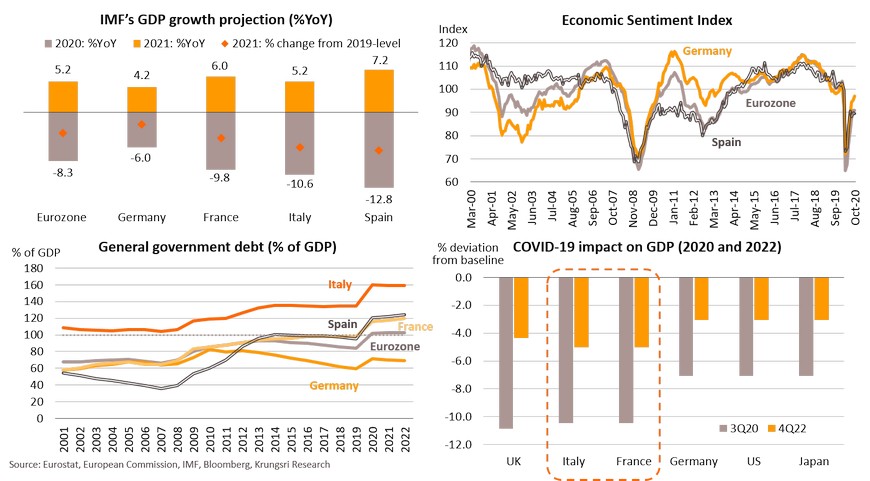

Eurozone GDP is projected to grow by 5.2% in 2021 compared to -8.3% in 2020. This leaves 3.5% far below the pre-pandemic level. Although Spain would see the strongest growth in 2021, it remains 6.5% below 2019 level. In 2021, each country would have a different recovery trajectory depending on national relief measures, a recovery in domestic demand, and structural challenges. Germany would lead the recovery because of effective stimulus and containment measures that support the Economic Sentiment Index to surge to 97, exceeding 90.9 for Eurozone and 89.5 for Spain. Moreover, the German government’s debt would rise only slightly to 70% of GDP in 2021 compared to more than 100% in several major countries. The current crisis could create long-term damage in this region’s economies, especially Italy and France, suggesting a difficult road to recovery in 2021 and beyond.

Second wave would delay recovery in the services sectors and slow down the labor market recovery

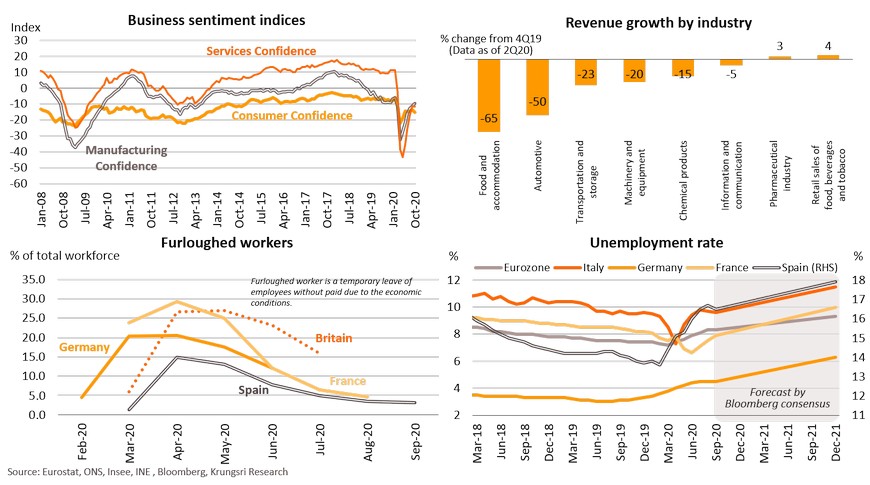

The second lockdown in Eurozone could affect the region’s recovery in 2021 particularly the services sectors and labor market. The Business Sentiment Index indicates confidence in the services sector remains far below pre-pandemic level. Revenue growth by industry also reveal the largest impact on food and accommodation sector, which lost 65% of revenues, reflecting a deeper hole to climb out of relative to manufacturing sectors. In addition, major industries showed widespread negative-revenue growth in 2020. This will continue to pressure the labor market. Although the number of furloughed workers have started to drop, 11 million workers or 9% of the Eurozone’s total workforce are still waiting to resume jobs. Besides, governments continue to struggle with the costs of extending this scheme. Eurozone unemployment rate could spike to 9.3% in 2021, led by Spain (17.9%), Italy (11.5%), France (10%) and Germany (6.3%).

Substantial targeted stimulus would support growth; recovery pace depends on size and speed of national aid

ECB stands ready to offer a mixed policy to empower the economy

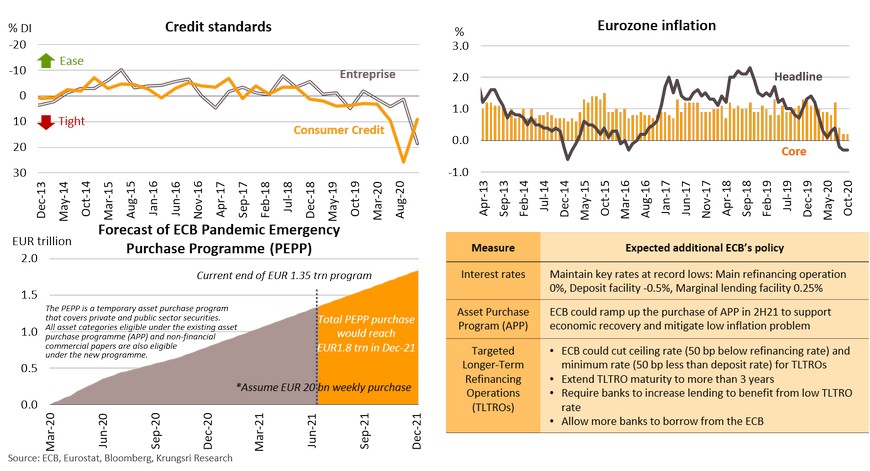

The ECB’s Bank Lending Survey in 3Q20 reveals tightening credit standards for both enterprises and consumers as banks see a worsening economic outlook and rising vulnerability. Eurozone 3-month reading for headline inflation was -0.3% YoY in October 2020. Looking ahead, inflation would remain subdued at least through 1Q21, before picking up when demand and energy prices recover. The subdued inflation and weak domestic demand might prompt the ECB to adjust its inflation target from “below, but close to 2%” to “symmetric at 2%” under 2021 policy review. The ECB could offer extra stimulus through various tools such as increase the ceiling of PEPP by at least EUR450bn by 1Q21 to EUR1.8trn and extend the purchase period to December 2021. The ECB could also apply a mixed policy in 2021 that could include cutting TLTRO interest rates and ramping up Asset Purchase Programs (APP) to meet inflation target and ensure bond yields stay at ultra-low levels.

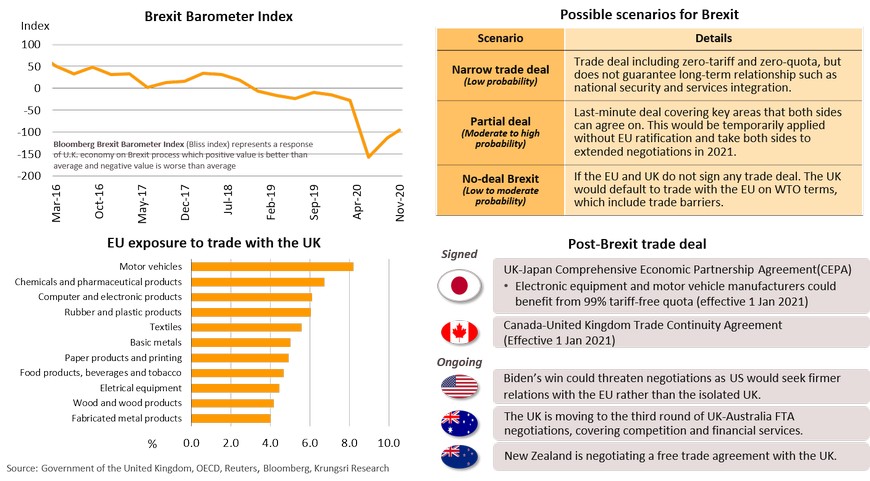

Brexit: UK’s departure could hit the EU but benefit the global economy

The Brexit Barometer Index indicates a slightly better situation, but still worse than the average in the past few years as the EU and UK have yet to agree in many areas. The possible scenarios now are mixed, ranging from No-deal Brexit (worst-case, low-to-moderate probability) to a Narrow trade deal which could be the best solution for the UK currently. Regardless of the scenario, Brexit would have negative impact on EU trade, especially in the most exposed sectors such as motor vehicles and chemical & pharmaceutical products. On the other hand, the UK departure could benefit the global economy as the UK would be free to pursue bilateral and multi-lateral trade agreements with several trade partners, including the US, Australia and New Zealand.

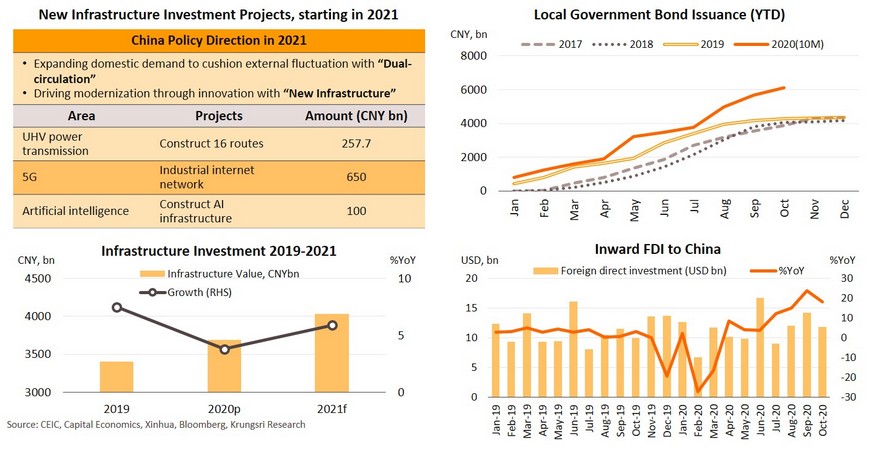

China: Effective policy responses and successful Covid-19 fight will keep recovery on track

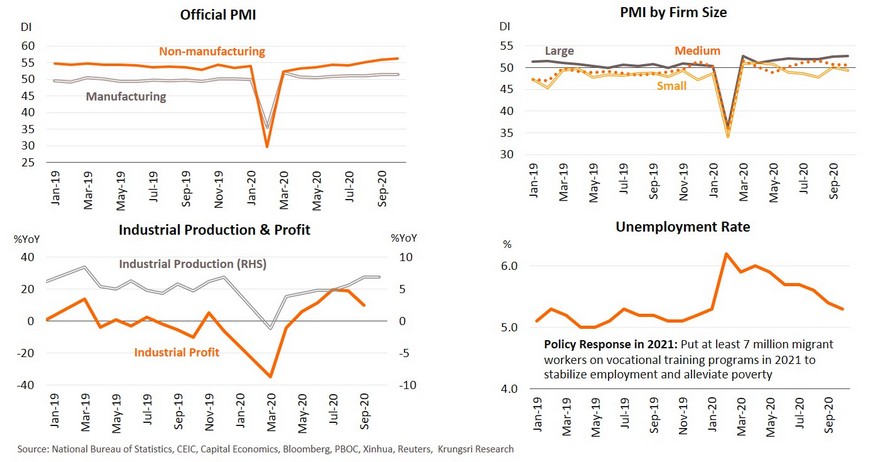

The ability to contain the spread of COVID-19 coupled with effective policy response, China is ahead in the race towards a global recovery. Both Manufacturing and Non-Manufacturing PMI data have recovered past pre-pandemic levels. Looking at the resumption of economic activities by firm size, recovery would be broader as PMI data for large firms have returned to levels prior to the outbreak, and data small and medium firms are close to pre-COVID levels. Industrial Production Index and industrial profits have risen gradually and has recently been growing faster before the pandemic. The gradual improvement in production also helped to reduce unemployment, which is also close to pre-pandemic level. The stronger recovery has been supported by prompt policy responses to contain infection, revitalize supply side, and boost domestic demand. However, there are several laggard sectors that remain weaker than pre-pandemic levels.

Demand-side recovery remains below pre-pandemic level, implying need for further stimulus measures

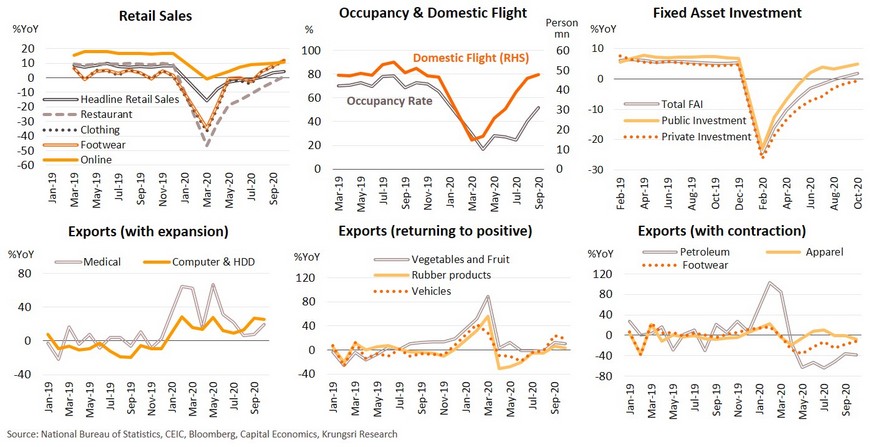

Despite the strong rebound in the supply-side, demand-side recovery has not returned to pre-pandemic level. Headline retail sales remained weak though sales of semi-durable goods such as clothing & footwear, are picking up, partly supported by discount vouchers and cash aid. Tourism incentives and residents replacing international travel with domestic trips helped to lift occupancy rates and air traffic, but the recovery in tourism-related activities remains below pre-pandemic levels. Most importantly, private investment is still sluggish and below pre-COVID level. On the external front, export demand for several products remain subdued although the pandemic helped to boost exports of medical products and computer & HDD products to support the pandemic-induced work-from-home policy. Therefore, the overall economic recovery towards pre-pandemic levels would be limited and require further stimulus support.

Despite tighter measures in some sectors, China still needs monetary easing

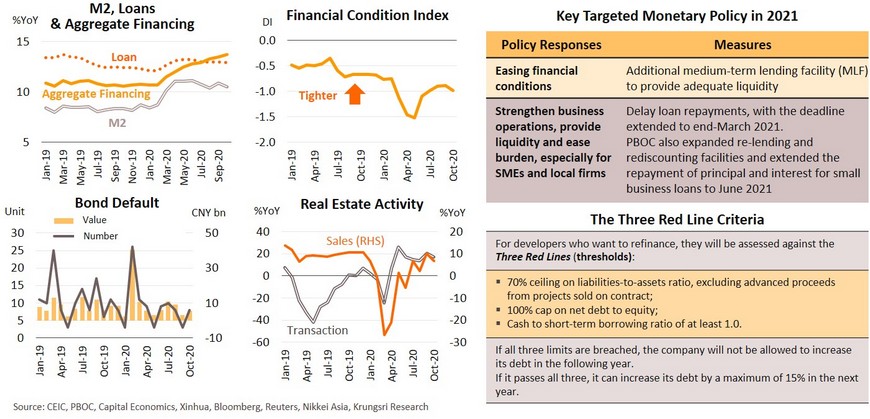

The economic recovery has been partly supported by quick policy responses and unprecedented stimulus measures. Bank loans and money supply have risen since the COVID-19 outbreak in 1Q20. Meanwhile, aggregate financing also increased, partly led by the issuance of bonds and equity to finance the fight against the crisis. Hence, financial conditions have been eased relative to pre-pandemic levels. Recently, the People’s Bank of China (PBOC) started to implement stricter supervision and regulations on sectors that are showing early signs of risks to financial stability. The PBOC and Ministry of Housing recently announced they were drafting the “Three Red Lines” regulation, where real estate developers who want to refinance will be required to pass a financial soundness assessment. This will be launched on 1st January 2021. The announcement has caused property loans to drop and slowed down real estate activity, which could reduce bubble risk. In addition, although some Chinese state-owned enterprises have defaulted on their bonds, the size is still considerably small compared to the total market size (only 0.46% of total SOE bonds). The PBOC is expected to implement targeted measures to curb specific risks. However, the central bank will keep interest rates unchanged and likely continue with monetary easing to support demand-side recovery.

Amid risk from US-China tension, public investment and FDI should play key roles in supporting domestic recovery

Infrastructure investment continues to play a leading role in stimulating China’s economy, given demand-side recovery remains below pre-pandemic level. Stimulus measures could strengthen the domestic economy and cushion the impact of external fluctuations, as indicated by the Dual Circulation Policy. This policy could also reduce the risk of US-China tension as president-elect Biden would push the the Made In America plan and improve multilateral relations with US allies to pressure China. Moreover, infrastructure investment would help to compensate for slower property investment due to tighter measures for property loan. The PBOC and the Ministry of Housing announced they will implement the Three Red Lines regulation, effective 1st January 2021. The infrastructure investment is aimed at developing capabilities in cutting-edge technology, especially 5G, artificial intelligence, big data, electric vehicle charging stations, and inter-city rail network. Rising foreign direct investment (FDI) would also support recovery of private investment ahead. Looking ahead, further growth in both infrastructure and foreign direct investment in the next period would strengthen economic recovery and mitigate external risks.

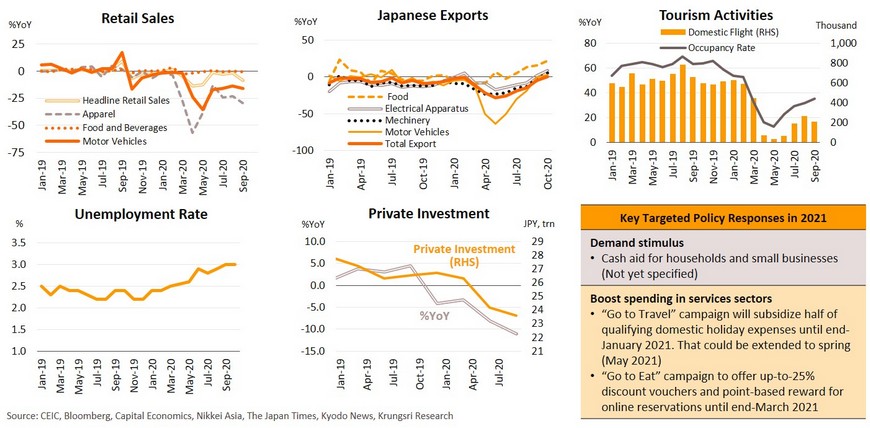

Japan: Some sectors are back to pre-pandemic levels but overall economic recovery remains weak and uneven

Economic stimulus measures helped to boost spending and supported the gradual economic recovery. Some economic indicators have returned to or exceeded pre-pandemic levels, including headline retail sales and total exports. However, looking at the sub-categories for retail sales and exports, several key items remain below pre-pandemic levels. Sales of apparel and motor vehicles remain in negative territory and exports of other major products, including vehicles and machinery, are still far below pre-pandemic levels. For tourism-related services, despite improvements driven by the “Go to Travel” and “Go to Eat” campaigns, domestic flights and occupancy rates are still far from normal. Unemployment rate has exceeded pre-pandemic levels and is rising. In addition, private investment remains weak and below pre-outbreak level. Looking ahead, since some components of economic activities remain below pre-pandemic levels and the new wave of infections could depress the economy, the additional stimulus would boost recovery. Being host of the Olympic Games next year should also help to improve domestic spending ahead.

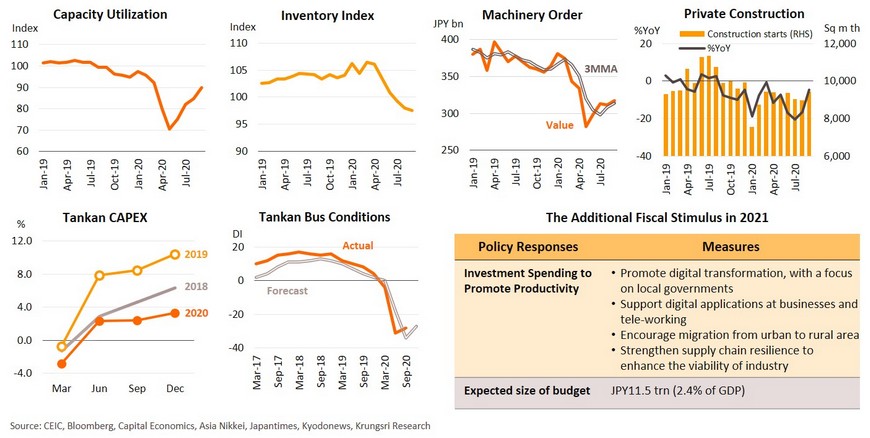

Additional fiscal stimulus could induce still-subdued private investment

There were positive signs from several investment indicators, such as capacity utilization rate picking up and running down of inventory. But private investment is still far below pre-pandemic level, reflected by weak machinery orders and private construction data. The Tankan capital expenditure survey claims capital expenditure in fiscal year 2020 is also lower than in 2019 and the Tankan business survey reflects still-weak business conditions. The lackluster improvement in private investment suggests a need for additional fiscal stimulus. The Japanese government is preparing to launch the third supplementary budget that would include a fresh economic stimulus package to enhance economic recovery. The supplementary budget is also expected to promote investment projects to support digital transformation, strengthen supply chains, support migration from urban to rural areas, and improve the country's disaster preparedness. Looking ahead, the gradual recovery of consumption and exports, as well as government stimulus to increase productivity, should boost private investment in the next period.

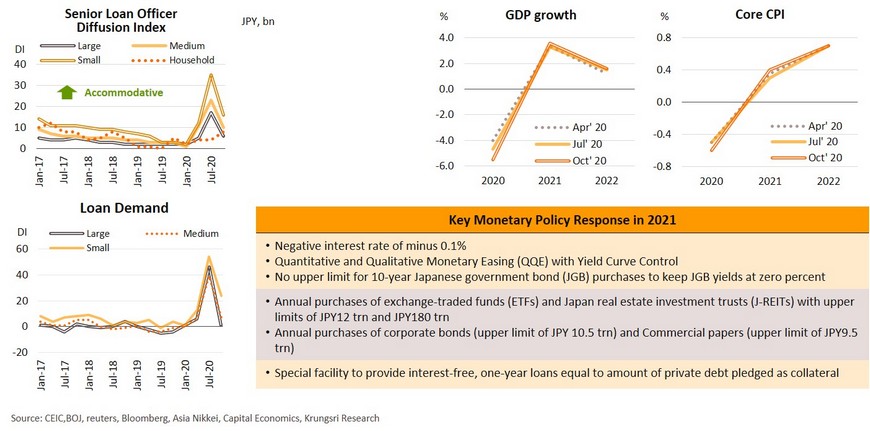

BOJ to implement very-loose monetary policy and maintain policy interest rates until 2023

The implementation of huge monetary stimulus during the pandemic has improved liquidity in the economic system, as reflected by easing credit conditions (or more accommodative lending by senior loan officers), slower purchases of ETF, and recent slowdown in loan demand from firms of all sizes. However, we expect the BOJ to continue to implement monetary stimulus measures, premised on the following: (i) although the BOJ projects the economy would grow by 3.6% in 2021, that is insufficient to cover the 5.6% GDP contraction in 2020; (ii) the BOJ projects inflation at only 0.4% in 2021 and 0.7% in 2022, far below the official target of 2%; and (iii) the economy has yet to see a firm recovery amid the new wave of infections. Hence, the BOJ would continue to implement very-loose monetary policy, by maintaining negative interest rate until 2023 and implementing quantitative and qualitative monetary easing (QQE) with yield curve control, unlimited asset purchases, and interest-free lending facilities. These measures should continue to improve liquidity in the financial system, along with fiscal stimulus to support further economic recovery.

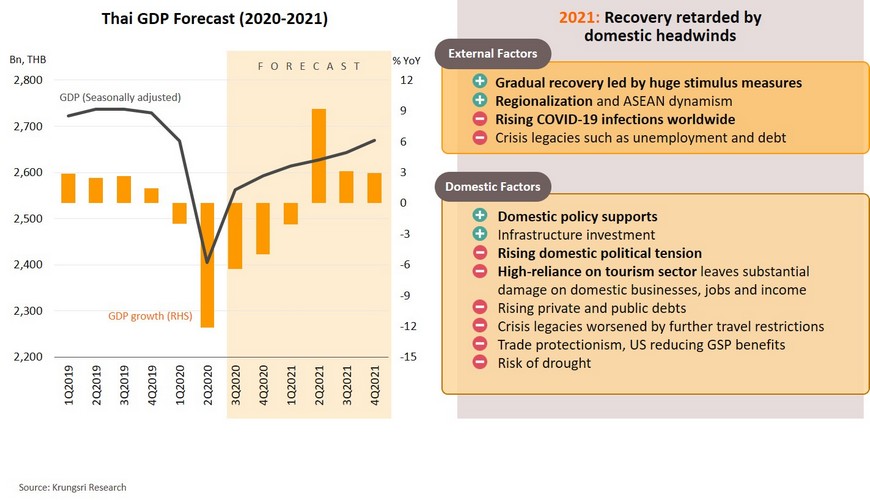

Thai economy in 2021: Gains from cyclical rebound in economic activity limited by domestic headwinds

Challenges and opportunities

Krungsri Research Forecast

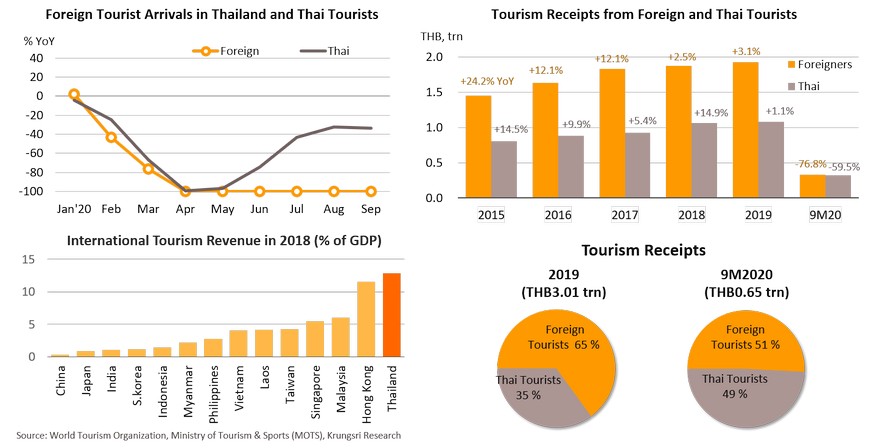

Tourism: Absence of foreign tourists hits overall economy because they are a major economic driver for Thailand

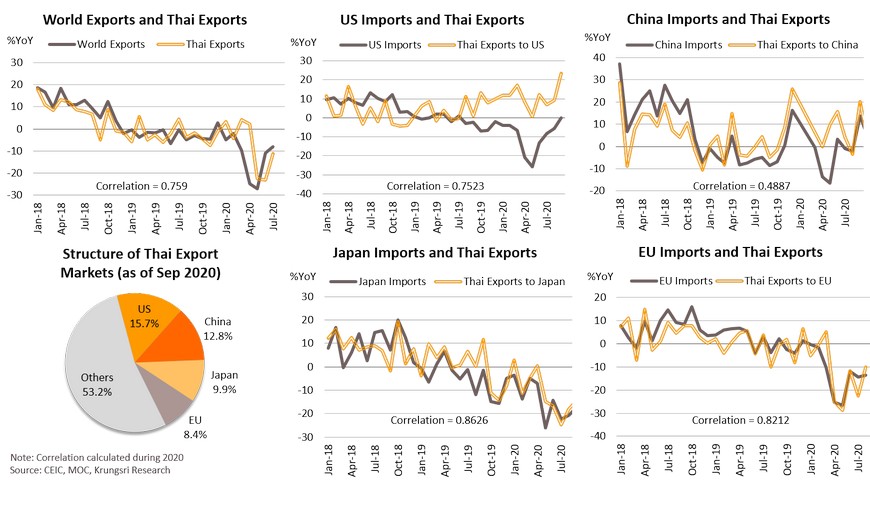

In 9M20, tourism receipts reached THB0.65mn (-70.6% YoY), of which THB0.33 mn (-76.8%) was generated by foreign tourists and THB0.32 mn (-59.5%) from Thai tourist. In 3Q20, there was no almost foreign tourist arrivals, like in 2Q20. In 4Q20, Thailand has reopened for selected foreign tourists under the Special Tourist Visa (STV) scheme, but that is expected to attract less than 1,000 tourists per month compared to 3.4mn per month in 4Q19. We estimate full-year number for 2020 at 6.7 mn. For domestic tourism, the number of Thai tourists have risen since June, supported by easing lockdown restrictions and the government’s stimulus program, known as ‘We travel together’ (effective July 2020-January 2021). Despite this, the absence of foreign tourists hurt the broad economy, including employment, tourism-related businesses, and income, because foreign tourist receipts normally account for about 13% of GDP, more than in other Asian countries.

Mass vaccination may boost foreign tourism in 4Q21, but it could take at least 2-3 years to return to pre-crisis level

While Thailand has allowed selected tourists to enter the country, the global situation remains risky with several nations re-imposing lockdown measures due to a resurgence of infections. Looking ahead, further travel restrictions, concerns over infections, and weaker incomes since the crisis, would lead to a slow recovery in tourism. It would take at least 2-3 years for foreign tourist arrivals to reach pre-pandemic level (39.8 mn in 2019). For 2021, Krungsri Research forecasts foreign tourist arrivals would reach 4 mn premised on the availability of effective vaccines worldwide by the fourth quarter of 2021. Domestic tourism would be buoyed by government measures to boost spending by Thai tourists who are not allowed to travel abroad. However, tourism receipts from Thai tourists is insufficient to offset lost revenues from foreign tourists (which accounted for 65% of total tourism receipts pre-Covid). The uncertainty in Thai politics could also be a risk factor that could dampen a recovery in tourism in the next period.

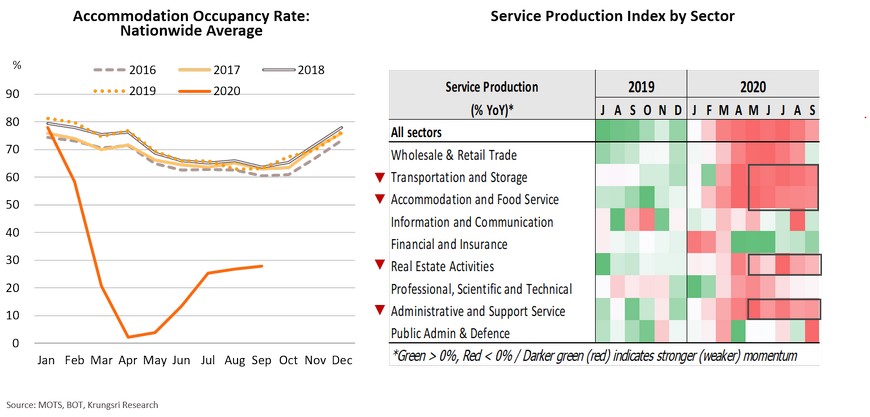

Ample idle capacity implies slow growth in major services sectors

Private consumption: Job losses continue to weigh on income and consumer spending

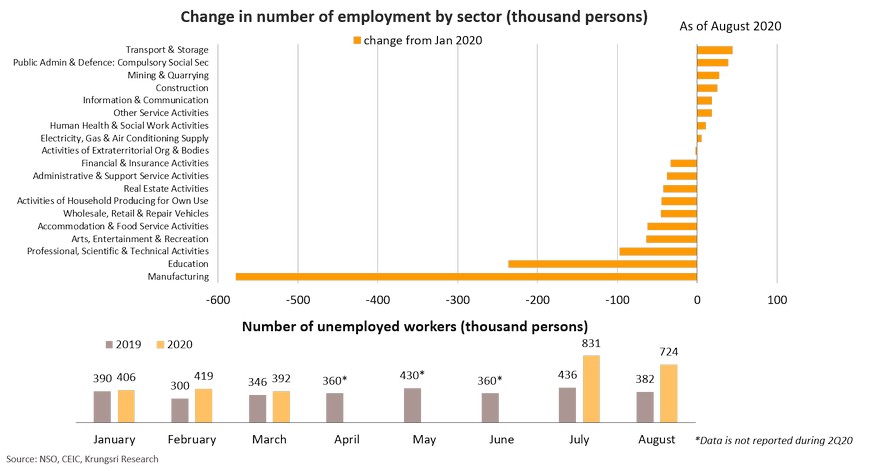

The labor market was directly hit by the COVID-19 pandemic in 2020. Thai domestic workers have experienced reduced working hours or lost the job. The largest drop was seen in non-agricultural sectors, where more than 1 million jobs have been lost this year led by Manufacturing (578k job losses) and Education (236k). There were also job losses in the tourism-related sector such as Arts & Entertainment (63k), Accommodation and Food Services (62k). The number of unemployed has doubled to 724k in August from 382k a year ago. This suggests rising unemployment and income loss would continue to dampen the labor market and undermine household purchasing power ahead.

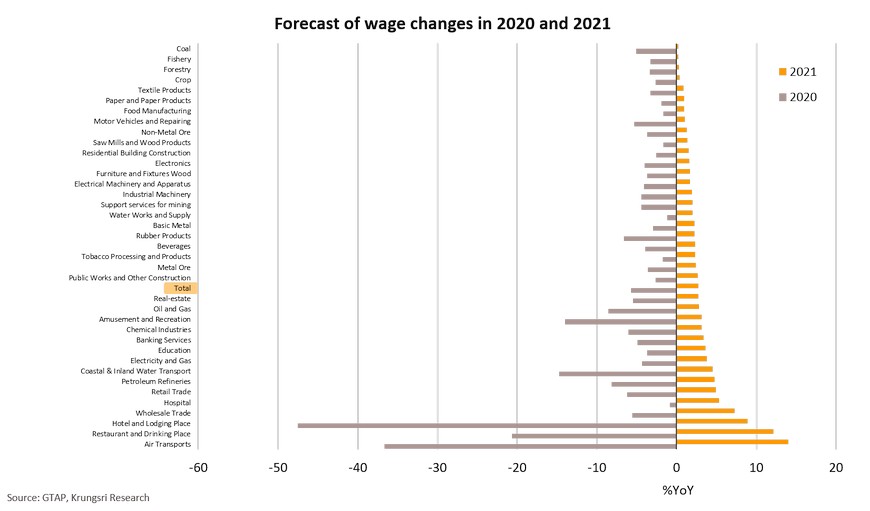

Average wage would pick up by 2.7% in 2021 but remain weak because it has dropped dramatically in 2020

We estimate average wage would rise by 2.7% in 2021, compared to -5.7% in 2020 due to the COVID-19 impact. Tourism-related sectors would see the largest wage increases, such as Air Transport (+14.0% in 2021 vs -36.6% in 2020), Restaurants & Bars (+12.2% vs -20.6%), Hotel & Lodging (+8.9% vs -47.6%), reflecting a moderate recovery in economic activities. Wages in the Agricultural sector and Primary Manufacturing would see mild increases in 2021 after a small drop in 2020. However, overall wage increases would be limited by the persistent impact of COVID-19 on the Thai economy and rising number of infections worldwide.

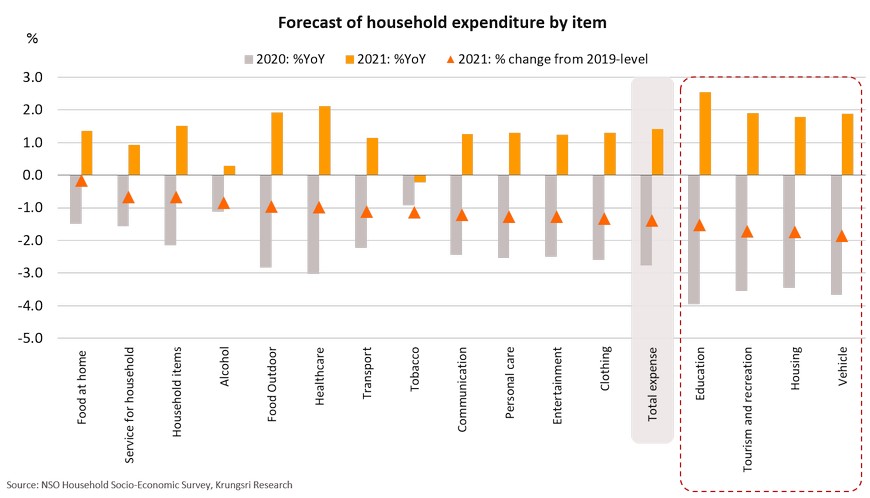

Household expenditure would rebound moderately but spending on all items remains below pre-pandemic level

Consumers have responded to smaller incomes by reducing spending. In this crisis, they cut spending on education, tourism and housing when the pandemic started. The COVID-19 impact has reduced household expenditure by 2.8% YoY in 2020. In 2021, expenditure on education, healthcare and outdoor food consumption would register the largest increases of 2.5%, 2.1% and 1.9%, respectively. Total household expenditure would rise by a moderate 1.4%. Even so, consumption spending would remain far below pre-pandemic level, especially on vehicle, housing and tourism & recreation.

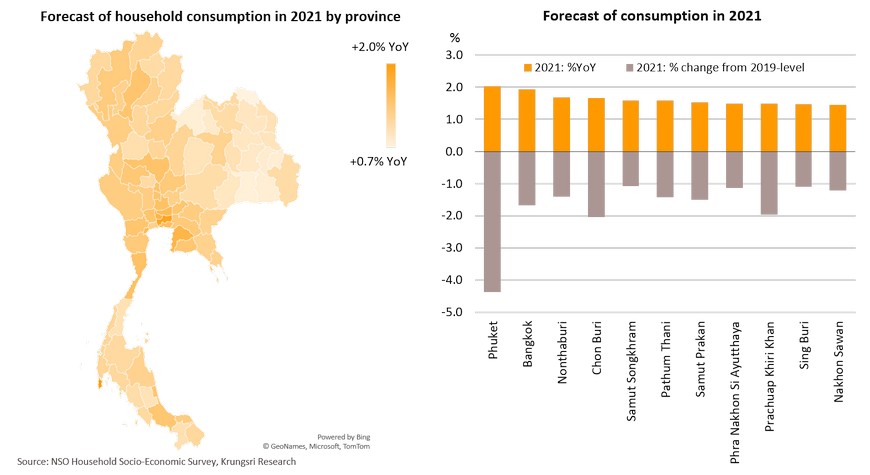

BMR shows largest rise in consumption; tourism-dependent provinces see nascent recovery

National consumption would increase moderately, led by Bangkok Metropolitan Region (+1.6% in 2021 vs -2.9% in 2020), followed by Western region (+1.4% vs -2.7%), Eastern (+1.4% vs -2.7%), Southern (+1.2% vs -2.7%) and Northern (+1.2% vs -2.4%). The northeastern region would see the smallest rise in consumption of only 0.9% in 2021 (vs -2.0% in 2020). Consumption in tourism-dependent provinces such as Phuket, Bangkok and Chon Buri should soar because of the low-base effect in 2020 due to travel restrictions. Despite the anticipated improvement in 2021, consumption in major provinces would remain weak at 2-4% below pre-pandemic levels.

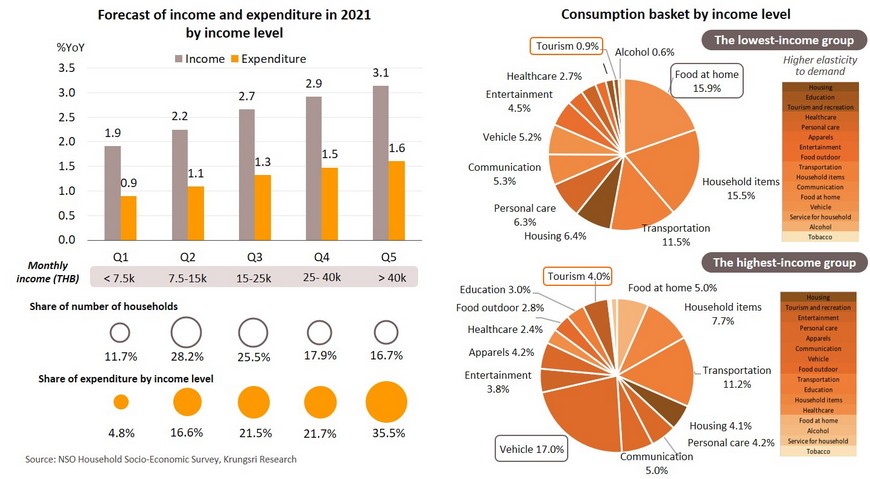

High-income group could be major growth driver of private consumption

We estimate expenditure in the low-income group would rise by only 0.9% in 2021, but the high-income group (earn more than THB40,000 per month) would see a larger increase in expenditure of 1.6%, which would be the major growth driver of private consumption in the country. Spending by the high-income group accounts for 35.5% of total household spending in the country. Considering the consumption basket, we expect businesses in the vehicle and transportation sectors would continue to recover in the coming period supported by recovering purchasing power in high-income households. In contrast, spending on tourism will remain weak because that is normally considered non-essential.

Farmers benefit from rising prices for major crops and farm price guarantee scheme

Farm income could rise moderately, backed by anticipated higher agricultural output and favorable farm prices

Exports: Under Biden, US policy would have mild benefits for Thailand because trade protectionism will remain

Gradual recovery of global manufacturing activities to trigger modest rebound in Thailand merchandise exports

Global exports have improved since bottoming-out in May though the year-on-year growth remained in negative territory. Thai exports are also recovering along with global exports. Recently, the WTO projected world merchandise exports would grow 7.2% YoY in 2021, after experiencing a sharp drop of 9.2% in 2020. In fact, Thai exports to major economies - the US, China, Japan and the EU - contributed 46.8% or half of total Thai exports. Imports by these countries are also improving and would boost demand for Thai export goods. Data show imports by major economies have strong positive correlation with Thai exports to these countries, specifically with Japan (correlation 0.86), EU (0.82), the US (0.75), and China (0.49). Therefore, economic recovery in these countries and the anticipated pick-up in global trade would drive Thai exports to expand in 2021.

Private investment in the export sector would rise

Parts of private investment are likely to expand following a rebound in exports. The strong correlation between exports and investment in plant & machinery suggests an export recovery would encourage investment in export-related items. In addition, several industries may expand investment after production capacity utilization rises substantially, particularly in automotive, chemicals & chemical products, IC & semiconductor, HDD and electrical & appliances sectors.

Capacity utilization of manufacturing production has almost returned to pre-pandemic level

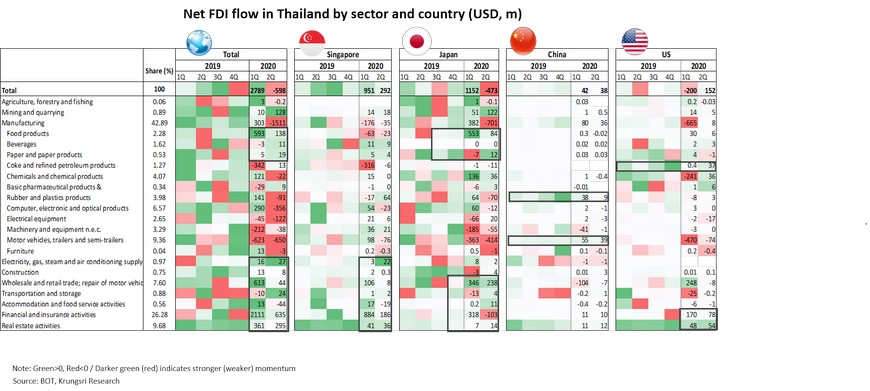

Despite virus impact, there was net FDI inflow in 1H20, close to 1H19 level, led by Financial and Food sectors

Net Foreign Direct Investment (FDI) totaled USD4.4bn in 2019, down from USD8.5bn per year during 2015-2018. In 1H20, despite the global economic meltdown triggered by the COVID-19 pandemic, there were net FDI inflows of USD2.19bn, close to USD2.37bn in 1H19. FDI from most key countries still posted net inflows, led by Japan, China, and Singapore -- a financial hub in ASEAN region. FDI from Singapore was impressive, led by financial and insurance activities. FDI inflows also benefited several industries such as from Japan (food products), China (rubber and plastic products, motor vehicle industries), and the US (petroleum products).

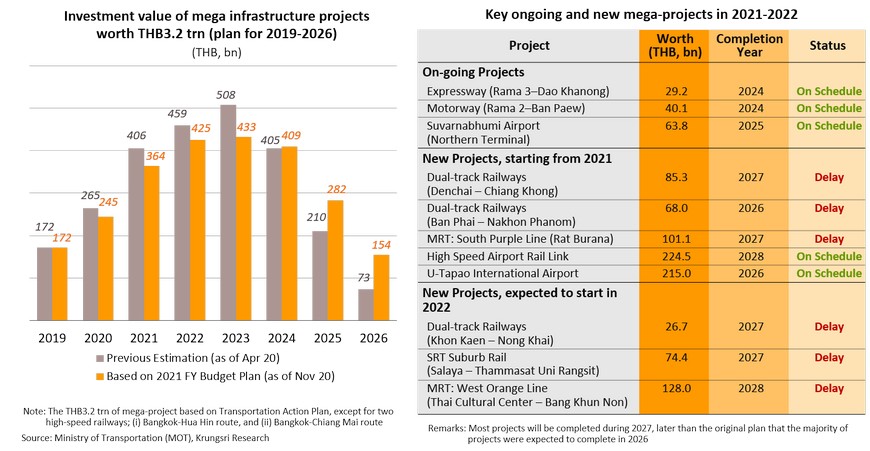

Infrastructure investment would rise in 2021 despite a delay due to budget reallocation after COVID-19 crisis

The need for budget reallocation in response to COVID-19 impact caused some mega-infrastructure projects to start later than scheduled. The Dual-Track Railway project Phase 2 is now under PPP funding instead of solely by fiscal budget, and hence, it will start with only two new routes in 2021 (instead of 7 in 2020). The MRT West Orange Line (Thai Cultural Center – Bang Khun Non) project has been postponed by two years to start in 2022. Nonetheless, several mega-projects are expected to start in 2021, including MRT South Purple Line (Rat Burana), High Speed Airport Rail Link, and U-Tapao International Airport. The overall investment value of mega-infrastructure projects in 2021 would rise by 48.5% YoY, relative to 53.2% under the previous plan. Despite rising infrastructure investment, it would be slower than the original plan estimated in April. Domestic political uncertainty could also delay investments.

Public spending: Focus is on short-term stimulus, especially to boost consumption by early 2021

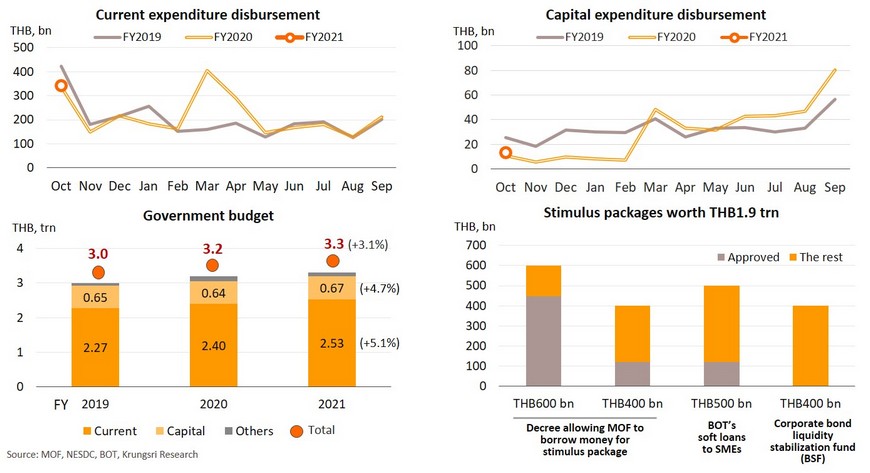

THB200bn extra-budget left for new stimulus in 2021; still lacks plan to generate multiplier effect in economy

The regular budget expenditure for fiscal year 2021 (Oct 2020-Sep2021) is almost THB3.3 trn (+3.1% YoY), including current budget of THB2.53 trn (+5.1%) and capital budget of THB0.67 trn (+4.7%). The delay in budget disbursement in FY2021 should be temporary as the 2021 Budget Act was published in the Royal Gazette on 7 October 2020. The government also plans to set up a committee to speed up budget disbursement in FY2021. In addition, under the THB400bn extra budget, THB200bn is kept for further stimulus, aimed at (i) revitalizing economic activity; (ii) supporting the recovery of local and community businesses; (iii) increasing household consumption and private investment; and (iv) developing infrastructure projects. However, most of the budget has been utilized via measures to stimulate consumption in the short-term. There are no firm measures to generate a multiplier effect in the economy, such as programs to support business expansion and employment.

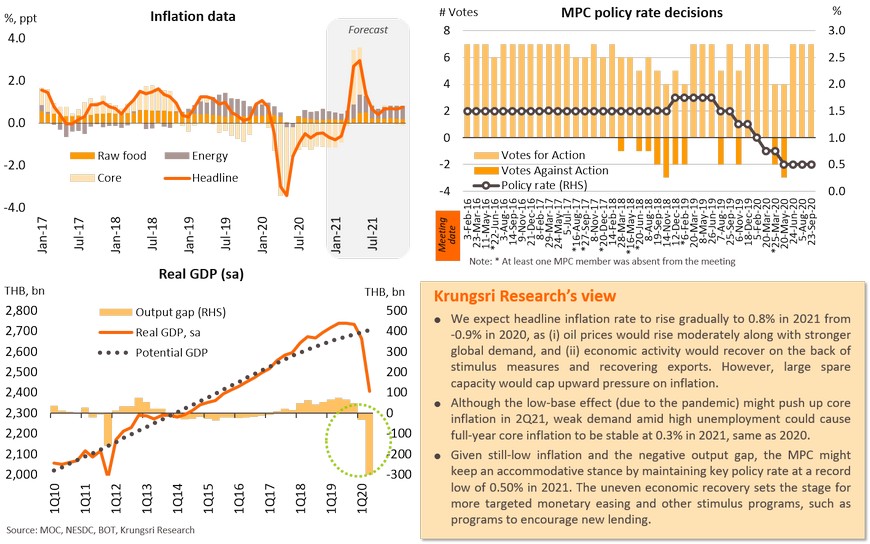

Monetary policy: MPC likely to keep rate at record low amid negative output gap and still-low inflation

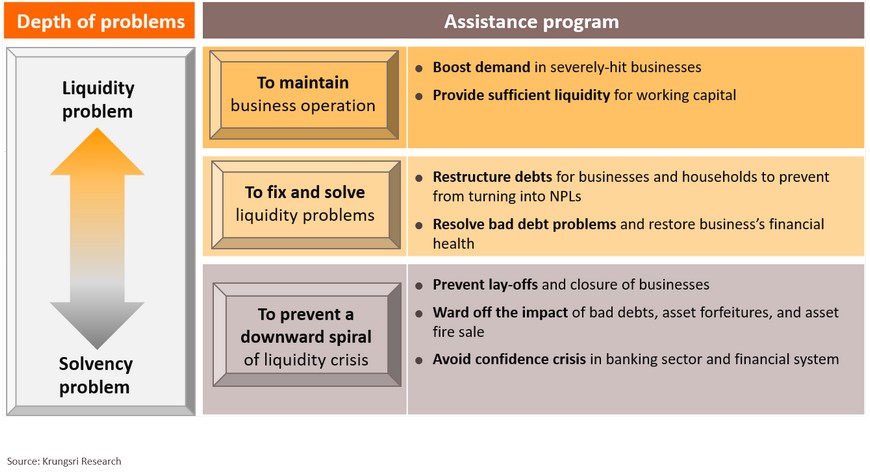

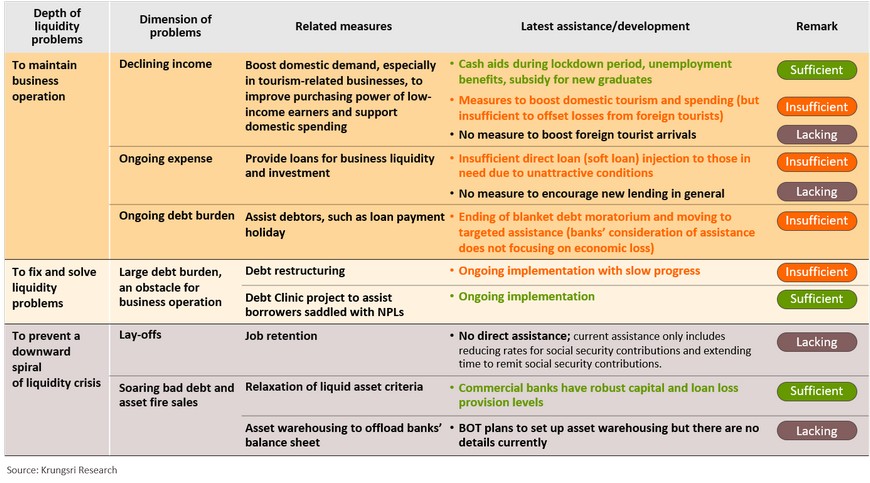

Aid programs should be immediate and appropriate, depending on depth of liquidity problems

Most of the recent aid programs are inadequate, with few measures to encourage new lending

Risk aversion behavior amid concerns over rising bad debt and falling liquidity might lead to a lockdown in new lending for firms’ working capital and business expansion. This could have spillover to the overall economy, postponing economic recovery and reducing potential growth. To avoid permanent negative impacts, such as job losses and business closures, there should be measures that are able to create collective action in the banking system, such as measures to encourage new lending and debt restructuring, to improve businesses’ liquidity in order to maintain their operations, to solve their liquidity problems, and to prevent solvency.

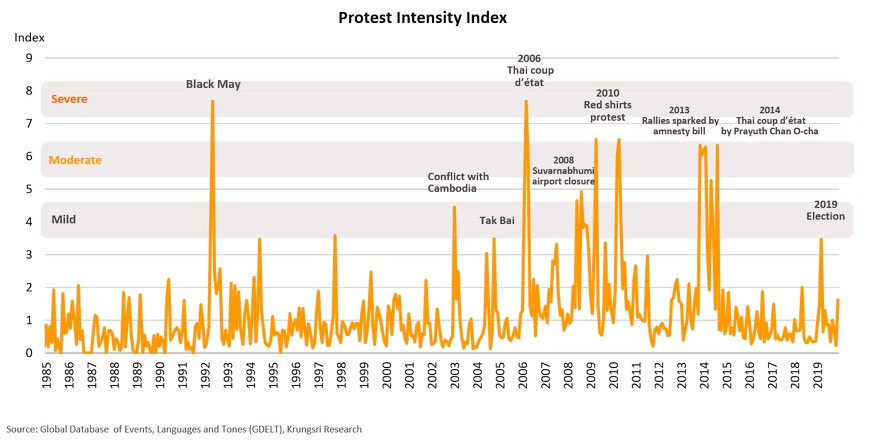

Domestic political risk: Economic growth was hurt in protest years and there are long-term effects

The impact of political protests is different depending on the duration, degree of violence, and overall economic conditions at that time. In 2010, the impacts were limited as the economy had registered impressive growth before protest started, and private consumption and investment fell for only 3 months. In 2013-2014, the political crisis had extended to about 7 months, and had gradually dampened investor and consumer confidence. Tourism was directly affected by the protests and tourist arrivals fell immediately. Extended period of protests could continue to dampen the tourism sector, and it took about one year to recover. Overall GDP growth fell in that period and potential (long-term) growth was adversely affected by weaker investment growth.

Impact depends on protest duration; tourism takes direct hit; there is long-term impact on investment

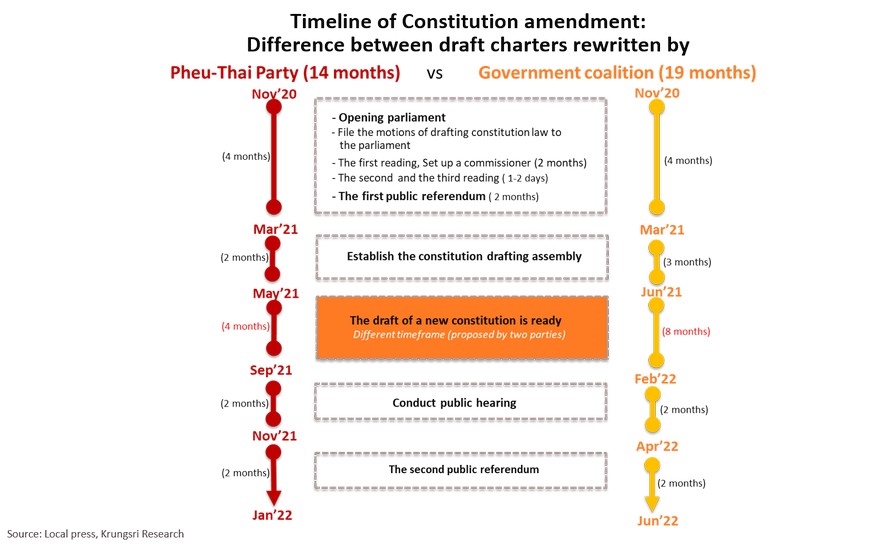

Constitution amendment will take more than one year, implying political protests will continue

The process of amending the constitution proposed by the government coalition parties and opposition political parties is anticipated to take more than a year. There is a significant difference between the timelines proposed by both camps (Pheu-Thai: 120 days vs Government Coalition: 240 days). No matter which option is accepted, the political protests will persist.

Intensity of current protests seems close to previous periods of unrest

The Protest Intensity Index was constructed by collecting and tracking news about political uncertainty. This captured the political instability followed by mass civil protests. The highest intensity was 7.7 during Black May in 1992. The index for the past decade illustrate the intensity of major political events such as the Coup d’état in 2006 (7.6) and Red and Yellow shirts protests which marked 6.5 intensity. Political uncertainty can hurt economic performance but the degree of impact is influenced by the intensity of protests. Looking at periods of past political unrest, current intensity scenarios for mild and moderate cases would be similar to previous events (marking 4.0-6.0) but the worst case would be more severe than previous events (marking 8.0).

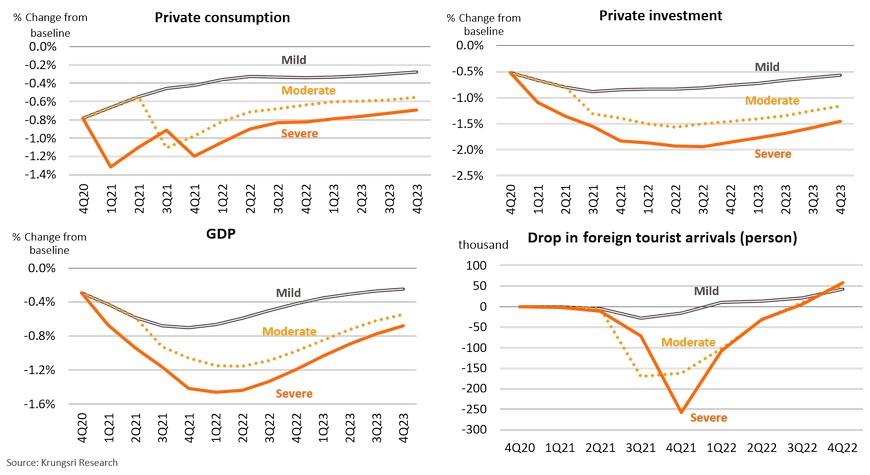

Economic impact: Political unrest would reduce GDP by 0.6% to 1.1% in 2021 and have long-term effects

This is based on our Mild, Moderate and Severe scenarios for protest intensity. The political turmoil could drag 2021 Thai GDP by -0.6% from baseline under the Mild case, -0.8% in the Moderate case, and -1.1% in the Severe case. Similarly, private investment could fall by -0.8% next year under Mild case and -1.5% under Severe case. This means investor confidence is damaged by domestic uncertainty. Consumption would drop sharply when protests start, but the impact is relatively small compared to other indicators. Foreign tourist arrivals could drop by 50k (from baseline) to 340k in 2021. Overall, indicators would drop for more than two years, reflecting existing impact along the path to recovery. Hence, we anticipate the current political protests could have negative short- and medium-term impact on Thailand’s already-crippled economy.

Opportunity: ASEAN is expanding economic ties through new free trade deals, shifting to greater regionalization

Stronger regional trade ties support higher participation of ASEAN in the global value chain

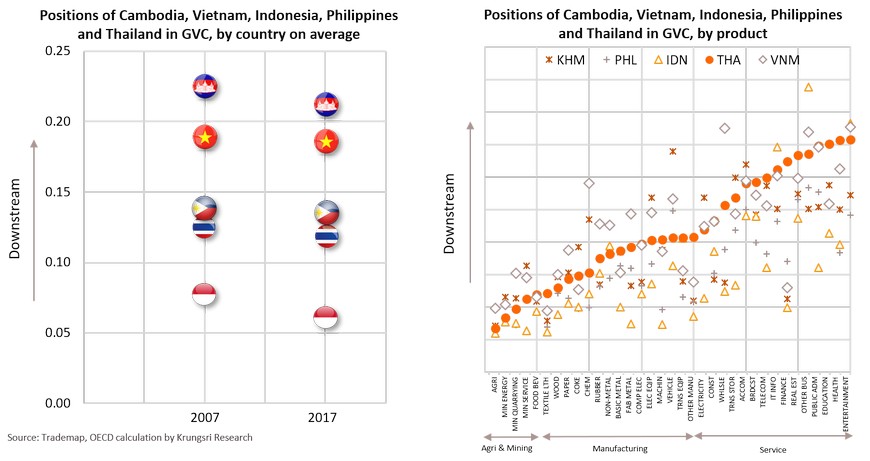

Most ASEAN countries have different positions in supply chains, representing more opportunities to complement each other

We observe three key points about positions in the Global Value Chain (GVC) of selected ASEAN countries, including Thailand, Cambodia, Vietnam, Indonesia and the Philippines. First, in terms of relative positions, they rarely change. Cambodia remains in relative downstream position while Indonesia is relatively in upstream. Cambodia focuses on labor-intensive manufacturing. In contract, Indonesia’s production involved processing raw materials at the beginning of the process. Second, in terms of products, different products manufactured by each country are on different positions in the GVC and they reflect complementary opportunities among ASEAN countries. Third, Thailand’s relative position is in the middle of the GVC. Most of our manufacturing products are in the middle of the GVC – which is generally considered intermediate inputs for final products. This would allow Thailand to connect with other ASEAN members in the regional supply chains.

RCEP would benefit the ASEAN economy, fostered by harmonizing and liberalizing trade and investment

Regional economy: The way forward through regionalization

ASEAN recovery would be relatively stronger than other regions, mainly driven by FDI and public investment

International tourism would remain subdued but progress in vaccines could support recovery

Exports would improve gradually; Vietnam would outpace peers driven by its competitive products and privileges

Investment would start to rise again in 2021, geared by public investment and new regional & bilateral FTAs

Private consumption would improve moderately; Vietnam would see strongest rebound

Monetary policy would remain accommodative; Indonesia and Myanmar have room for more easing