ASEAN: On track for moderate growth, economies diverge in timing toward pre-pandemic norms based on domestic demand strength. Ongoing uncertainties highlight the need for policy buffers.

-

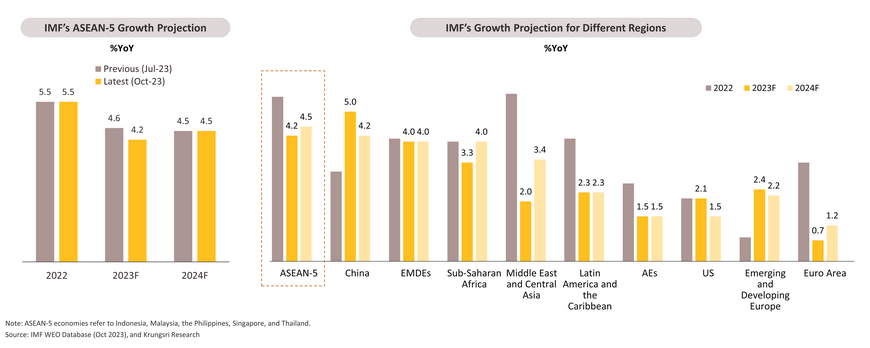

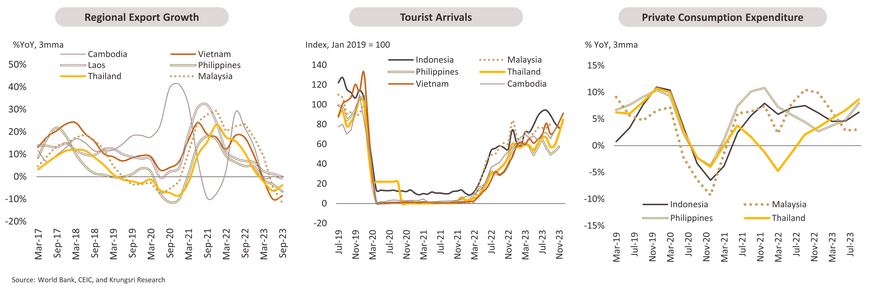

In 2023, ASEAN-5’s economy continues to expand, with growth projected to average 4.2 percent. The growth is at a slower pace compared to 2022 and earlier projections due to a fading reopening boost, the global growth slowdown, and tight domestic financial conditions. Varied economic fundamentals have resulted in different growth trajectories for each country in the region. In 2023, robust private consumption has been the key driver of regional growth. Domestic-demand-oriented economies like Indonesia and the Philippines have benefited the most in this regard compared to other export-oriented economies, particularly Vietnam and Cambodia.

-

Going into 2024, growth in the region is expected to slightly edge up to 4.5 percent in 2024, where domestic demand is expected to remain a key driver. Additionally, exports should modestly rebound due to supply chain loosening, easing inflation, and a diminishing drag from tightened financial conditions.

-

Major headwinds are external factors, including weaker external demand, geoeconomic fragmentation, and extreme climate events like El Niño. These factors are expected to increase uncertainties for the region's growth prospects through both the financial and trade channels. Countries heavily reliant on trade will be most adversely affected by weaker global demand, while those heavily dependent on external financing will be most vulnerable to financial market volatility.

-

In terms of monetary policy, the US decade-high policy rates and potential upside inflation risks from higher commodity prices could keep regional monetary policy stances neutral until late 2024. If necessary, monetary easing is also plausible, given easing inflation pressures, growth staying below pre-pandemic, coupled with improving external balances. Indonesia and the Philippines will likely be the first in ASEAN to cut policy rates as they have tightened the most to date.

-

With more obvious signs of economic slowdown and more frequent supply-driven headwinds, fiscal buffers are increasingly important. Countries with relatively ample fiscal space include Indonesia, the Philippines, and Cambodia.

Cyclical Outlook: Growth expected to moderate but remain robust.

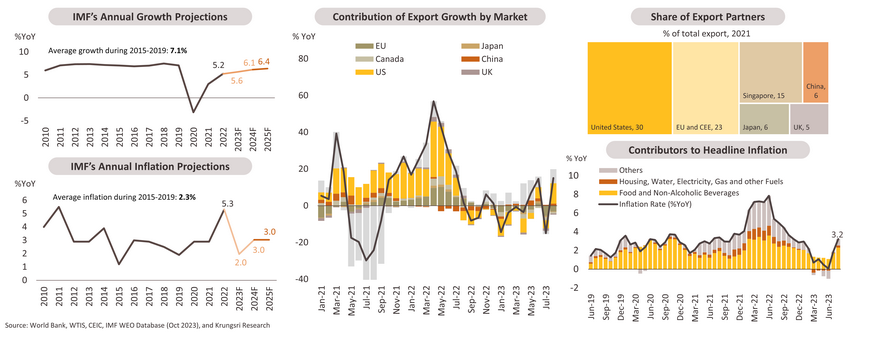

ASEAN-5’s economy continues expanding, with growth projected to average 4.2 percent in 2023. The growth is at a slower pace compared to 2022 and earlier projections amid a fading reopening boost, the global growth slowdown, and tight domestic financial conditions. Growth in the region is expected to marginally edge up to 4.5 percent in 2024, gradually converging to trend in most countries, where domestic demand and a modest rebound in global goods trade will be the drivers. While domestic fundamental is the main positive influence on growth, external factors will lead to higher uncertainties for the regional outlook. Key headwinds are weak external demand, geoeconomic fragmentations, and El Nino weather phenomenon. Despite slowing global growth and uncertainties, ASEAN-5 remains higher than the growth projected in other Emerging Market and Developing Countries (EMDEs).

Factors shaping the outlook: both structural and cyclical forces at play

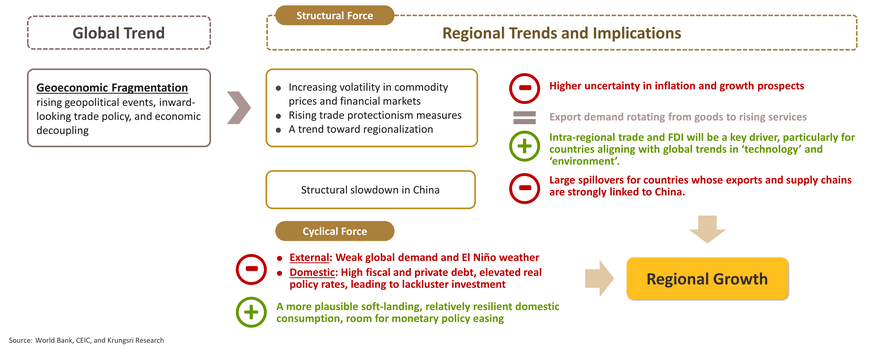

Economic performance in the region is being shaped by both structural forces and cyclical developments. Structural forces include geoeconomic fragmentations (arising tensions in geopolitics and trade) and structural slowdown in China. However, regionalization trend; investment shifting away from China, and several trade agreements particularly Regional Comprehensive Economic Partnership (RCEP), would keep ASEAN countries remain an attractive destination for FDI inflows. For cyclical matters, even though inflation shows signs of declining in major economies, high interest rates continued to pressure economic activities. Hence, weak external demand, coupled with the pandemic-legacy like high debts, and extreme climate pattern remains challenging for the region’s economic performance.

On a path of asynchronous recovery; monetary policy can be a support in 2H2024.

-

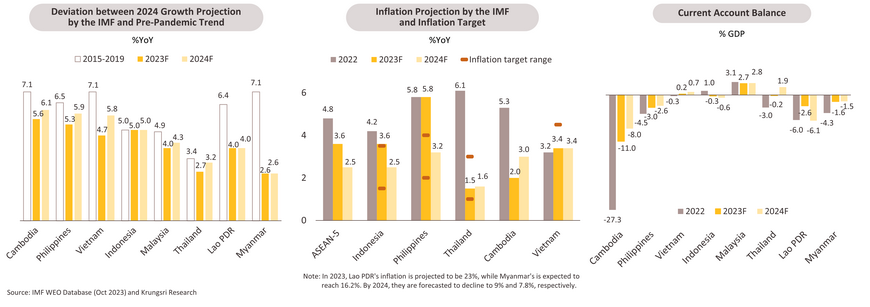

The post-pandemic economic recovery has been uneven across the region. Some countries are gradually converging towards the pre-pandemic trends, while countries with structural vulnerabilities, such as Lao PDR and Myanmar, are experiencing growth rates far below the trend. In the past, synchronous recoveries tended to be driven by strong trade cycles. This time around, the recovery has been asynchronous, driven by i) different economies fully reopened at different times; ii) when global goods demand deflated from late 2022, the support from domestic demand has led to a different evolution of growth, and iii) structural and idiosyncratic issue, like the coup in Myanmar.

-

Although global financial conditions remain tight, potentially keeping regional monetary policy stances neutral until late 2024, there may be room for monetary easing to support economic growth if necessary. This is due to growth in most countries being below the pre-pandemic trend and with inflation rates projected to return to the central banks’ targets next year, along with improving external balances. On the external front, a soft-landing scenario after the monetary policy tightening cycle is now more plausible, featuring expected global disinflation. This scenario is expected to create more supportive external conditions, paving the way for a more accommodative monetary policy in the region as well. Indonesia and the Philippines will likely be the first in ASEAN to cut policy rates in 2H2024 as they have tightened the most, bringing elevated real interest rates that have been pressuring economic activities.

Private consumption is the main support for regional growth; a modest rebound in goods exports is possible in the near term.

-

Usually, the trade cycle would be a significant driver of the regional outlook. However, weak global demand for goods since late 2022 has been a drag, mainly due to slowing economic activity in major economies like the United States and Europe as a response to financial tightening to combat inflation. Going forward, goods exports are showing signs of stabilization, and should modestly rebound in 2024, mainly due to easing supply chain conditions, and easing inflation, coupled with a diminishing drag of tightened financial conditions. According to the World Trade Organization (WTO), global trade volume expansion is likely to be driven by trade in goods, which tend to recover when economic growth stabilizes. We are not expecting a strong, sustained export recovery as growth in major economies is projected to be below trend in 2024. On the positive side, the ongoing tourism revival has helped offset the decline of goods exports by boosting services exports. For most countries, the ongoing gradual recovery of international tourism, which has not yet fully returned to pre-Covid levels, will continue to be supportive.

-

Domestic demand has been the primary driver of regional growth. Falling inflation is also a support for real income. Domestic-demand-oriented economies like Indonesia and the Philippines have benefited the most in this regard compared to other small-open economies. Without significant support from exports, private consumption will remain the key driver into 2024, though some moderation is expected with higher real interest rates.

ASEAN FDI inflows remain resilient with rising opportunity in energy transition sectors.

-

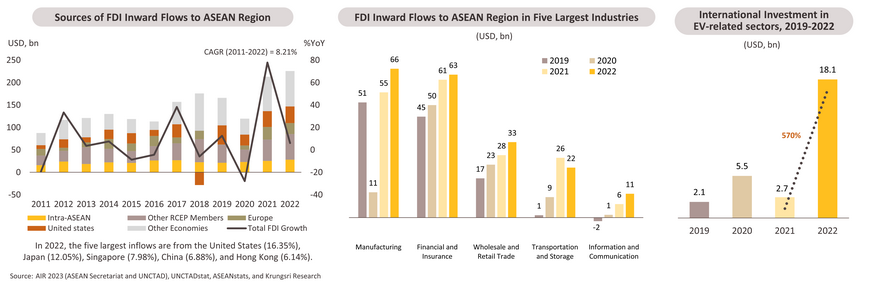

Amid the decline of global FDI, FDI inflows into ASEAN recorded a growth rate of 5.5 percent in 2022, after a remarkable rebound in 2021, when FDI rose 42 percent to greater than pre-pandemic levels. According to UNCTAD, the ASEAN FDI growth has surpassed the worldwide investment growth over the past decade, suggesting that the region remains and will likely continue to be appealing to foreign investment (Over 17 percent of global FDI went to ASEAN in 2022, up from 15 percent in 2021).

-

The RCEP integration, which took effect on 1 January 2022, shows some positive signs in attracting inward FDI into the ASEAN region. In 2022, RCEP members accounted for more than 37 percent of total inward investment in ASEAN, and that grew from its investment in 2021 at 16.8 percent. The future prospects for ASEAN investments will potentially be further supported by this regionalization trend.

-

According to a Special ASEAN Investment Report 2023, geopolitical tensions have prompted supply chain restructuring, favoring ASEAN. In addition, the region's commitment to energy transition will have a significant impact on attracting FDI, this extends to investments in renewable energy for electricity generation, transmission, and distribution, as well as technological solutions. In 2022, international investment in EV-related industries in ASEAN soared by 570 percent to USD 18 billion. Given that the top-ten global EV manufacturers are based in ASEAN and keep expanding there, this indicates to the region's attraction for investment in EVs. Furthermore, this will attract pertinent EV vendors to ASEAN.

External headwinds expected to increase uncertainties in the region's growth prospects

-

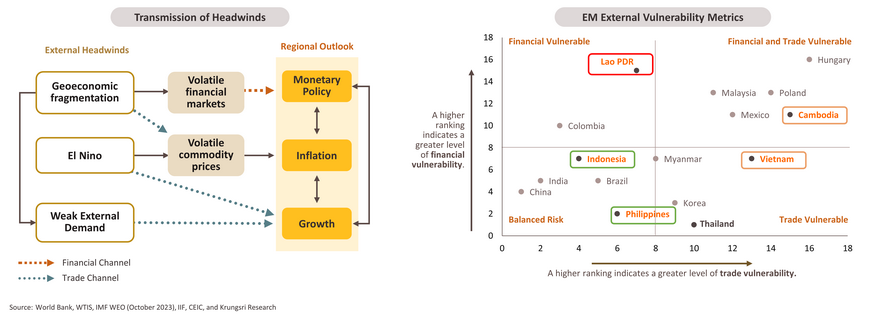

There are three main headwinds to consider in the upcoming period that could increase uncertainties for the region's growth outlook. On the demand side, the most significant one is the weaker growth in major economies. Supply-side headwinds include geoeconomic fragmentation and extreme climate events like El Niño. As major headwinds are external factors, they will impact regional growth through both the financial and trade channels. Countries heavily reliant on trade will be most adversely affected by weak external demand, while those heavily dependent on external financing will be most vulnerable to financial market volatility. We use external vulnerability metrics to assess which domain of vulnerability emerging and developing countries fall into.

-

Financial vulnerability metrics used in the analysis include twin deficit, FX reserves cover (months of imports), and share of short-term debt to total reserves. Trade vulnerability metric is each country’s export exposure to the US, China, and Europe relative to GDP. In the region, Indonesia and the Philippines have balanced risks, while Cambodia and Vietnam are vulnerable to weak external demand. Lao PDR is considered extremely financially vulnerable.

Demand-side headwind: weak external demand are a major headwind. Coupled with high private debt, it has held back investment recovery in most economies.

-

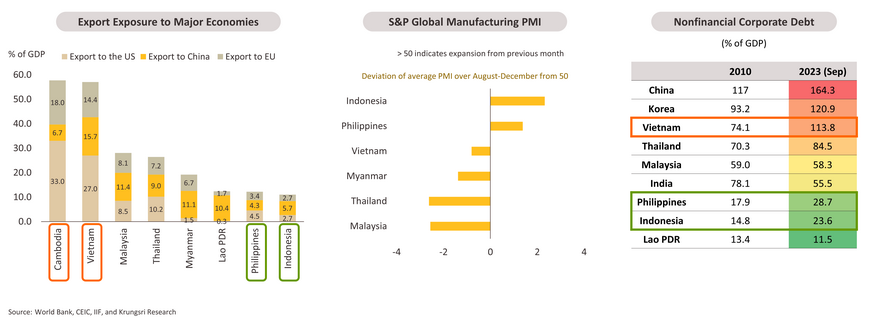

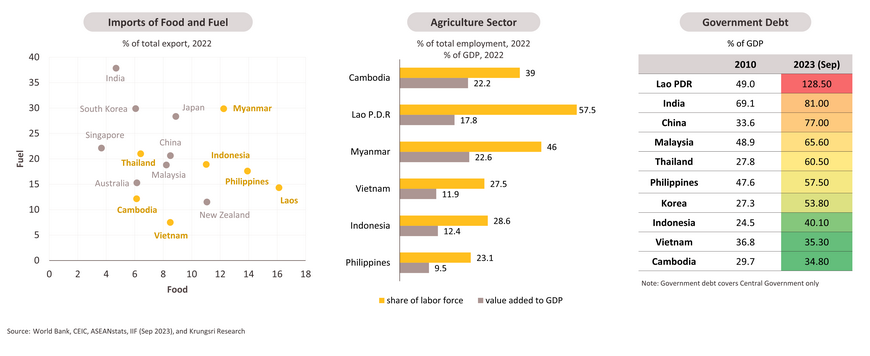

Despite the expected modest rebound in goods exports from depressed levels, expectations of a slowdown in major economies could be a headwind for the turnaround. Countries with high export exposure and low diversification in trade would be the most vulnerable. In this case, Cambodia and Vietnam are the most vulnerable, given their high export shares to the US, Europe, and China. More than half of Cambodia's total exports go to the US and Europe.

-

Soft external demand over the past year has provided a setback to the investment recovery in the region, as reflected in headline manufacturing PMI, though the indices have diverged. The indicators were relatively strong in the Philippines and Indonesia, largely attributed to their strong reliance on domestic demand. Coupled with high private debt, investments in the region have been further dragged. Nonfinancial corporate debt has increased significantly in most countries. Higher corporate debt amid high level of real interest rates can hurt private investment growth as firms are left with less money available to invest in new projects or expand its existing business.

In the medium term, inward-looking trade policies and a structural slowdown in China are also factors putting pressure on exports in the region.

-

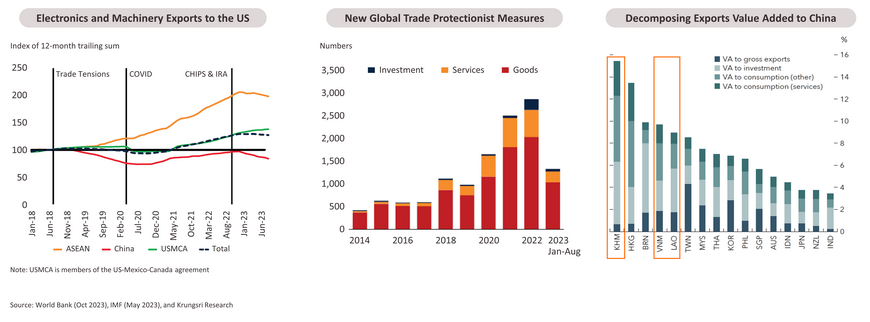

Trade protectionist measures are affecting exports in the region. The tariffs imposed by the US on China since 2018 shifted US imports towards other countries in the region. More recently, the US’s Inflation Reduction Act (IRA) and the CHIPS and Science Act of August 2022, introduced domestic content requirements linked to subsidies granted under the new laws. These Acts were followed by a decline in the exports of the affected products to the US from China and ASEAN countries. Furthermore, almost 3,000 new restrictions were imposed on global trade in 2022, three times as large as those in 2019.

-

Regarding structural China’s slowdown, spillover effects will differ across countries based on exposure to demand for China’s consumption and investment, as well as the degree of integration in global value chains (GVCs) through China. Looking at value-added exports, Cambodia, Vietnam, and Lao PDR could be the worst hit by slowing growth in China.

Supply-side headwinds will become more frequent, fiscal buffers matter

-

These supply-side headwinds from rising geopolitical tensions and El Niño weather will primarily lead to volatility in commodity prices. The impact of El Niño phase is projected to intensify in 2024. Severe droughts could reduce agricultural output and elevate food prices. Lao PDR, Indonesia, and the Philippines with high food imports are more vulnerable to price shocks. Furthermore, countries with relatively high reliance on the agricultural sector will be adversely affected by the possible reduction in output as well.

-

Supply shocks will become more frequent. Thus, fiscal buffers are increasingly important, not only due to constraints of monetary policy to address supply-side shocks but also from decade-high interest rates. General government debt as a share of GDP has increased significantly in most of the region’s economies, particularly Lao PDR. Countries with relatively ample fiscal space include Indonesia, the Philippines, Cambodia, and Vietnam.

Cambodia: Service sector remains a major support amid high uncertainties

-

The Cambodian economy grew slower than expected in 2023 with growth projected at 5.6 percent, marginally lower than 5.8 percent projected earlier, amid weaker exports. In 2024, growth is expected to gradually converge to the medium-term trend at 6.1 percent, with the support of ongoing recovery in tourism and improving exports of electrical components. Regarding inflation, after a period of decline, inflation rebounded in September due to higher food and fuel prices. For the full year 2023, inflation is expected to average 2 percent and pick up to 3 percent by 2024.

-

Uncertainties to the outlook include external risks and domestic financial stability. External risks include slower-than-expected growth in the US, Europe, and China, given its low diversifications on FDI source, type of export goods, and destinations. A renewed surge in global oil and food prices driven by geopolitical tensions and a severe El Nino weather pattern could cause inflation to spike given its significant share of food items in the CPI basket (around 40 percent) and heavy reliance on imported oil. Domestically, financial distress could arise with the high level of private debt and a prolonged slump in the real estate sector.

Weak goods exports and domestic headwinds have led to a sluggish manufacturing sector. A modest recovery in merchandise trade is expected.

-

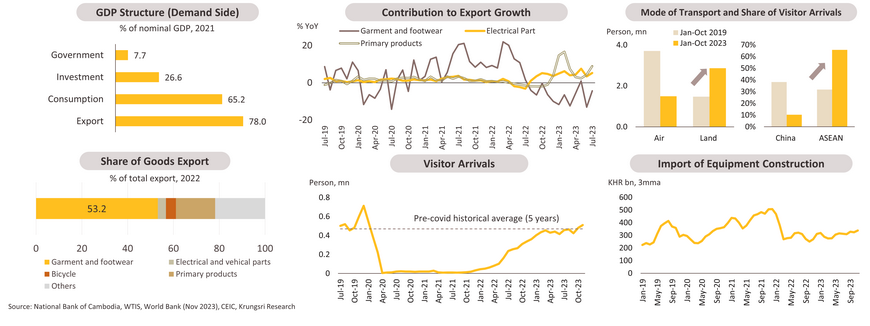

Cambodian economy is supported by the recovery in services amid a continued decline in goods exports. Exports of garments, footwear, and travel goods fell since mid-2022. The decline was partly offset by a rise in other exports of manufactures, notably electrical parts and primary products. Subdued goods exports have affected the real sector. Manufacturing jobs declined by -5 percent from July 2022 to May 2023, largely reflecting the impact of global demand slowdown in garment, travel goods, footwear, and textile industries, which provide as much as 83 percent of total employment in the manufacturing sector. In terms of the service sector, rapid recovery in tourist arrivals is observed, recovering to pre-covid average level. However, the structure of arrivals has changed. Rising land arrivals and ASEAN tourists (particularly Thai) reflect increased foreign tourists with relatively short lengths of stays and lower daily expenditures.

-

Going forward, the ongoing recovery in tourism and an expected recovery in exports, particularly electrical components following the normalization of supply chain conditions, would gradually support domestic employment and the economy. However, garment exports, comprising the highest share of total exports, will remain relatively weak given soft global demand. Due to the oversupply situation and tighter financial conditions, slower construction activity, reflected by sluggish imports of equipment construction, is also weighing on growth.

Close monitoring is needed for deteriorating asset quality and high private debt levels

-

Since the economy is highly dollarized, Cambodia imports the US’s monetary policy tightening, the National Bank of Cambodia (NBC) raised the reserve requirement (RRR) for foreign currencies from 7 to 9 percent in January 2023, and plan to normalize to the pre-pandemic level at 12.5 percent while maintaining the RRR for Cambodia’s riel at 7 percent. Banking regulatory forbearance measures introduced during the pandemic are also being withdrawn. As a result, broad money has declined, credit growth has sharply eased, and non-performing loans rose to 4.6 percent of total loans in August.

-

High level of private debt and the continued concentration of domestic credit in the real estate sector remain key risks to financial stability in Cambodia. The private credit-GDP ratio remains high for Cambodia’s level of development at around 170 percent. Further tightening in global financial conditions, particularly rising interest rates, could severely affect the leveraged banking system. Although the banking sector is well capitalized and profitable (commercial banks registered profit 1.4 percent of assets and 2 percent of loans by the end of 2022), the recent deterioration in asset quality and the high level of private sector debt require close monitoring.

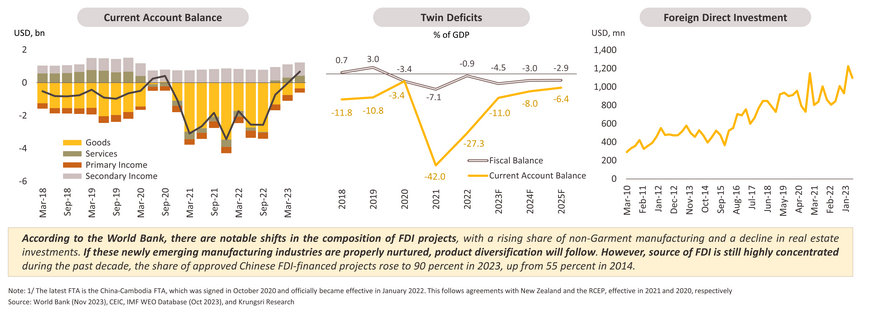

Narrower twin deficits expected, with FDI serving as the key driver of medium-term growth

-

Twin deficits are expected to narrow with a significantly improved current account, on the back of a sharp decline in capital goods imports, sustained inflows from remittances and tourism. Current account deficit is expected to fall further, mainly due to normalized merchandise trade and continued tourism recovery. Fiscal deficit should start to decline in 2024 with planned fiscal consolidation i.e., support measures for the pandemic and rising cost of living are being removed, and revenues improve owing to tax and customs administration reforms. However, external financing needs remain. To finance the gap, the country’s public debt (35 percent of GDP, as of Sep 2023) consists almost solely of external debt and China is the largest creditor (37.5 percent of total external debt). However, debt distress remains low as a significant share of external borrowing is concessional loan.

-

Despite uncertainties in the global economy and financial conditions, foreign direct investment (FDI) inflows remained resilient, with 40 percent increase over the first half of 2023, compared to last year. With continued inflows, international reserves stay ample, covering 7 months of imports. In the medium term, FDI inflow is expected to be a major driver of growth, facilitated by the newly ratified free trade agreements1/, a substantial increase in private and public investment in key physical infrastructure, and structural reforms.

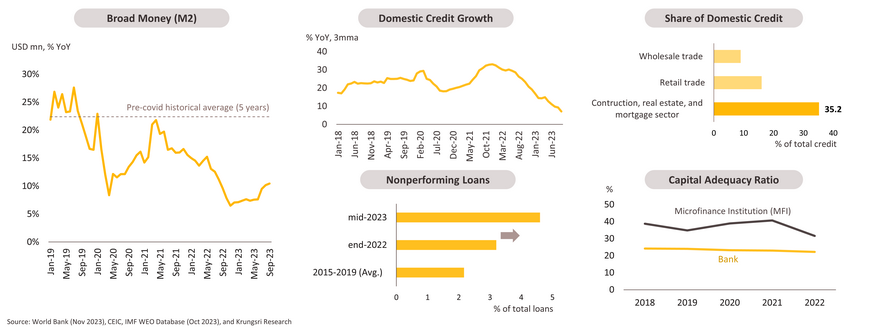

Lao PDR: Steady growth to remain at 4.0% in 2024 amid structural vulnerabilities.

-

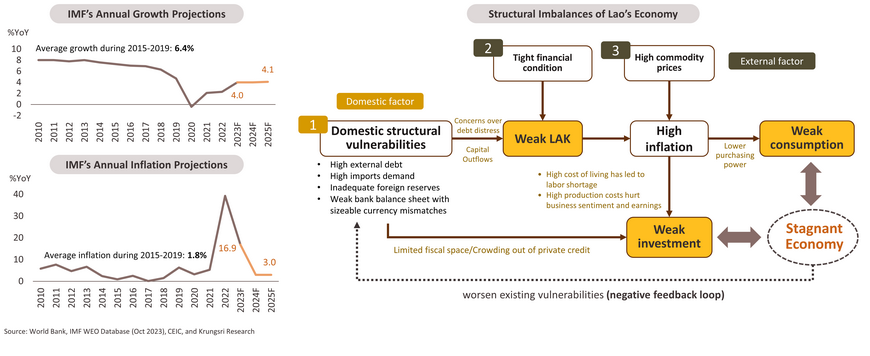

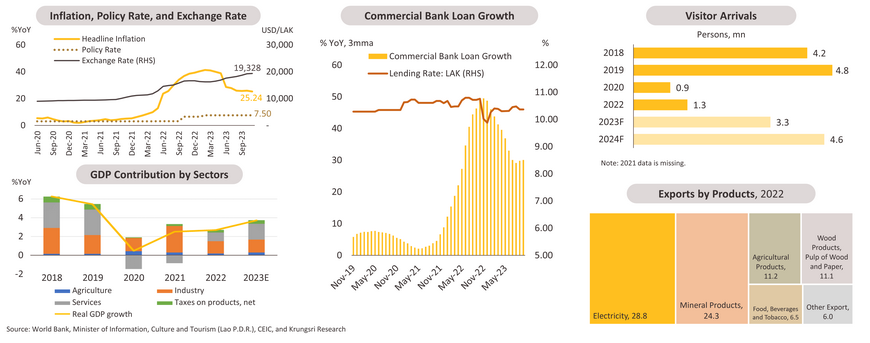

In the near term, the IMF maintains its 4 percent growth forecast for Laos in 2023, unchanged from the earlier projection. Despite a decline in domestic activities, service exports and foreign direct investment continue to support economic growth. In 2024, steady growth of 4 percent is predicted with continued support from the service sector. As weak local currency is likely to persist and keep inflationary pressures high, domestic activities will remain subdued. As a result, the Lao’s economy will have to continue relying on external forces.

-

Over the medium term, Lao’s structural vulnerabilities have capped economic growth. Domestic structural vulnerabilities have led to the depreciation of Lao kip. Since Laos heavily relies on imports, persistent depreciation has significantly increased inflation, which negatively impacts domestic consumption and slows down investment accordingly. Despite falling food and energy costs and alleviating global financial conditions, the country's economy will remain stagnant as long as structural imbalances persist, particularly high external debt.

The services sector and FDI are the main expansion engines in the near term.

-

An upsurge in inflation has dampened domestic activities. Private consumption has subdued from lower purchasing power. Furthermore, high cost of living has accordingly led to a labor migration issue, which is restricting the recovery prospects of labor-intensive sectors such as agriculture, manufacturing, and hospitality. Lower commercial bank loan growth indicated that private investment decreased in 2023. Furthermore, government spending is not supportive for the economy as the spending has been cut due to the fiscal consolidation scheme.

-

As a consequence, economic growth in recent years has relied more on external drivers such as exports and foreign direct investment. The services sector, which accounts for more than 30 percent of GDP, is a major economic contributor to growth in the near term. Only the first nine months of 2023 saw an extraordinary spike in tourism, with over 2.4 million foreign tourists, exceeding Lao tourism authorities' goal of 1.4 million. “Visit Laos Year 2024" aims to attract 4.6 million visitors and USD 712 million in revenue to stimulate the economy. In terms of other exports, electricity dominated total exports in 2022, followed by mineral products. In 2023, electricity exports fell slightly due to less rainfall, while mining exports rose substantially in the first nine months.

Despite substantial inflows, weak Kip is likely to persist with structural vulnerabilities

-

Another major driver of Lao’s economy is foreign direct investment. The inflows into Laos reached USD 1.25 billion in the first nine months of 2023, a growth of 191.5 percent from the same period in the previous year, as reported by the Lao Statistics Bureau. Over 60 percent of the inflows are from China, and most are invested in electricity, mining, and construction. The balance of payments thus turned to positive territory in the first nine months of 2023 following tourism receipts and substantial FDI inflows.

-

Despite a positive balance of payments, large debt repayment and concerns over debt distress have led to the Lao kip's significant depreciation in 2023. The government have introduced policies to curb currency depreciation pressure. To reduce outflows, the government restricted imports of luxury goods and increased excise taxes on non-essential products, such as fuel-powered vehicles, alcoholic beverages, and smoking products. Furthermore, an effort is being made to increase the proportion of export earnings entering the Lao banking system from 40 to 70 percent. To mitigate the public debt burden, the government enacted fiscal consolidation plans. This includes a reduction in government spending and an increase in revenue collection. The Lao Ministry of Finance is considering raising the value-added tax (VAT) rate from 7 to 10 percent, which is expected to be effective in early 2024. However, these policies have had limited effect on currency due to its structural issues. Thus, the kip could remain relatively weak, despite anticipated less negative effects from alleviating global financial conditions.

Low foreign exchange reserves, substantial public external debt, and concealed solvency strains in the banking sector remain key concerns

-

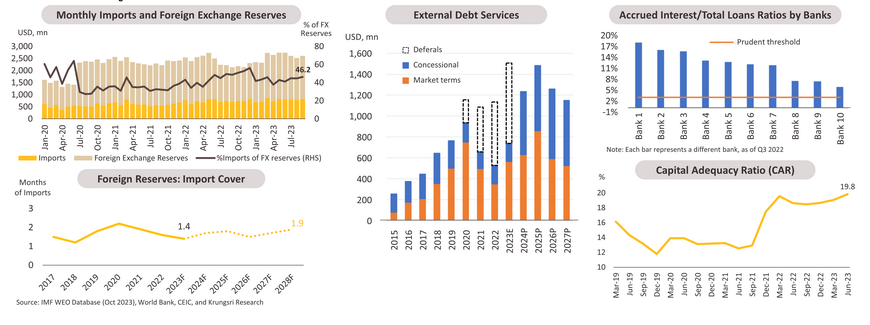

Despite improving foreign exchange reserves due to positive inflows, the reserves remain dangerously low by international standards. Gross reserves totaled USD 1.78 billion, covering only 1.4 months of goods and services imports in 2023 (monthly imports account for about 46 percent of gross reserves as of September 2023). This is owing to its heavy import dependence and huge external debt.

-

Currently, public debt exceeds 120 percent of GDP, the majority of which is external debt. This is subject to a tremendous depreciation of the currency. Despite China's deferrals in 2020-2023, total debt repayments have grown. In addition, the particular terms of these deferrals remain unidentified, and they are expected to total almost USD 2 billion (nearly 16 percent of GDP) by the end of 2023. Debt renegotiations for 2024-2027 repayments must thus be successful in order to assure debt sustainability and restore macroeconomic stability.

-

For the financial sector, continuing supervisory forbearance policies, such as loan classification freezes, restructuring, and capital improvements of banks, have made it more challenging to acknowledge losses in the financial system, as well as capital buffers and asset quality across banks. This is evident in low NPL levels and a higher aggregate capital adequacy ratio (CAR) in the banking sector, while several banks have large amounts of accrued interest receivable.

Myanmar: Trapped in political conflicts and policy errors.

-

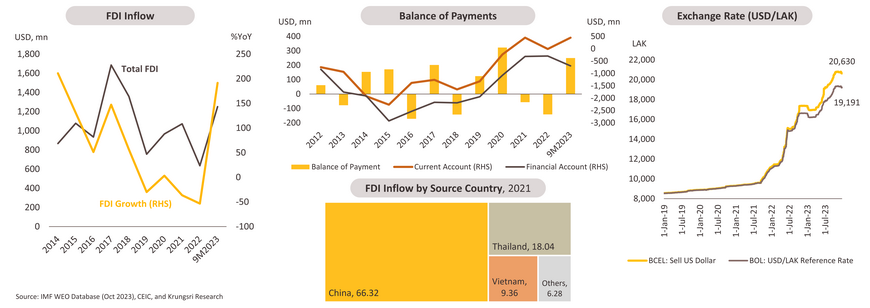

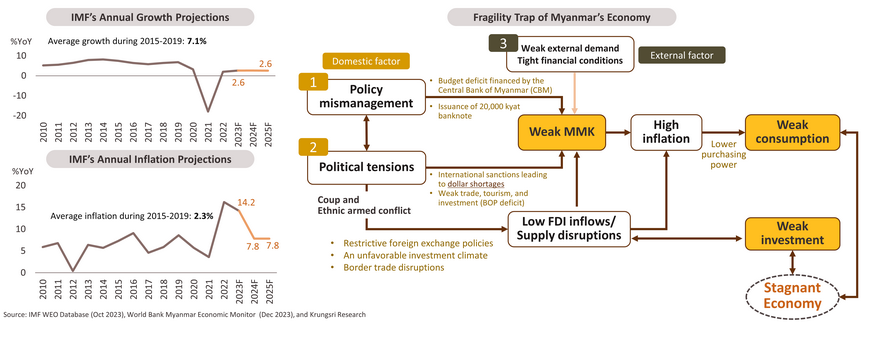

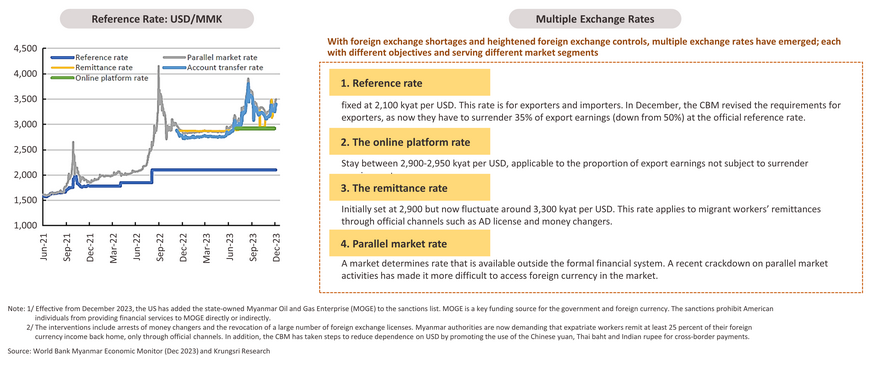

The signs of recovery observed in the first half of 2023 proved to be short-lived, given weak global demand, international sanctions, and continuing political tensions. There are significant dispersions in growth projections: while the IMF sees the economy growing by 2.6 percent in 2023, the World Bank estimates that growth for the year up to March 2024 will be 1 percent. Inflation is expected to persist at high levels due to the depreciation of the Myanmar kyat (MMK) and supply disruptions. The Central Statistical Organization reported an inflation rate of 28.58 percent for April-June 2023.

-

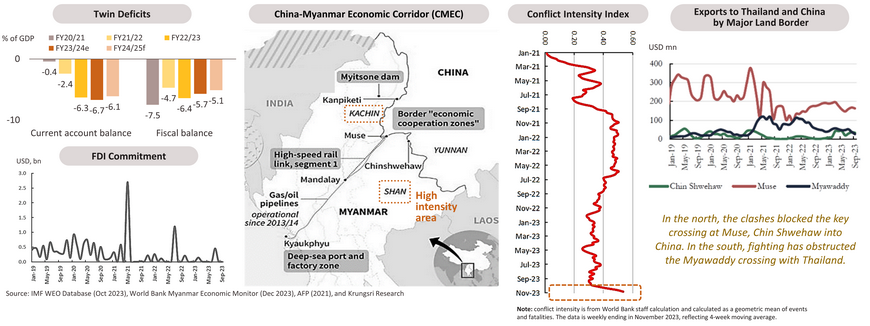

A fragility trap for Myanmar's economy is evident with the medium-term growth trajectory expected to remain well below pre-pandemic levels (2.6 percent vs. 7 percent). Domestically, policy mismanagement, particularly debt monetization, has resulted in a lack of confidence in the local currency. Following the coup, international sanctions have led to a shortage of dollars, complicating the imports of necessary goods. The inevitable unfavorable investment climate is compounded by widespread political opposition. Recent ethnic armed conflicts have further worsened the supply situation through border trade disruptions. These factors are major contributors to periods of high inflation and deteriorating consumption and investment, leading to a structural stagnation of the economy. In contrast to domestic structural factors, external factors like weak demand and a strong dollar appear to be cyclical but are not supportive of the economy either.

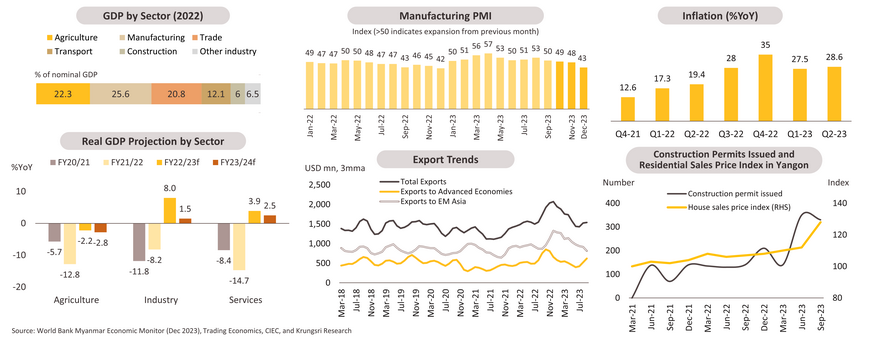

Broad-based slowdown is seen across productive sectors.

-

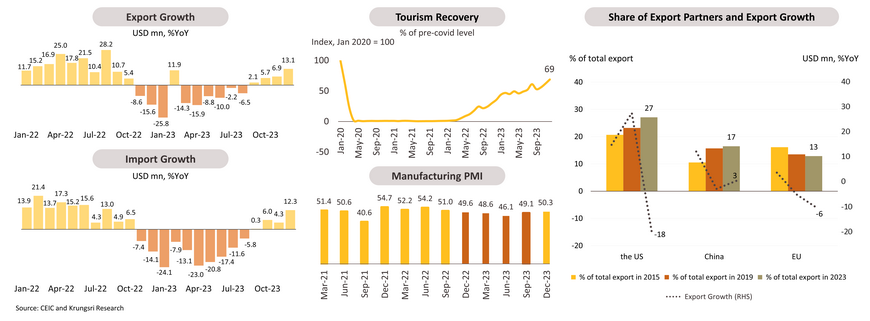

For the manufacturing sector, raw material shortages, power outages, and worsening logistic disruptions from the recent conflict continue to constrain activities. The contraction of manufacturing PMIs is also explained by stagnant domestic demand, primarily due to high inflation, which has squeezed real household income and led to subdued wholesale and retail trade. The agriculture sector is particularly vulnerable to border trade disruptions. Regarding international trade, weakness in the services sector continues as the recovery of tourism has been modest, with the return of international tourists at 17 percent in May 2023 compared to the pre-pandemic period. Goods exports weakened over the past year, consistent with a drop in manufacturing activities. Going forward, weak goods and services exports are expected to persist due to the escalation of political conflicts and increased logistics constraints.

-

On the contrary, the construction sector remains relatively strong, as safe-haven demand drove a pronounced increase in Yangon real estate prices. However, large-scale commercial real estate projects continue to stagnate with no approved FDI in the real estate sector since April 2023. Public infrastructure also slows due to budget constraints and severely constrained external borrowing.

Shortage of foreign exchanges continue, while measures have been ineffective.

After the stabilization of Kyat in the first half of 2023, the local currency saw sharp depreciation in July-August, following the introduction of US sanctions on two large state-owned banks, the announcement of restrictions on cross-border payments by international banks1/, and the launch of a higher denomination 20,000-kyat banknote that fueled devaluation expectations. Coupled with ongoing pressures on the balance of payments associated with a reduction in goods exports, insignificant return of international tourism, and lack of foreign direct investment, the local currency continued to be weak despite intervention to encourage foreign currency inflows, limit outflows, and tighten in limits on parallel market activity2/. According to the World Bank, the gap between the parallel market rate and the official reference rate stayed around 60-70 percent, reflecting persistent USD shortages.

The recent escalation of conflict has darkened the outlook.

-

Twin deficits are expected to persist over the medium term with a projected widening of current account deficits and fiscal balance, due mainly to a slowdown of goods and services exports and weak domestic revenue mobilization. Meanwhile, external borrowing to close the financing needs is severely constrained due to low foreign investment and international sanctions. In the financial sector, the NPL ratio stood at high levels; 20 percent in March 2023 (10 percent in 2020). This is partly explained by loans to the hotel and tourism sector, which continue to be weak after the pandemic

-

Currently, the political situation in Myanmar is highly uncertain. On October 27, the Three Brotherhood Alliance (3BA) – a coalition of three major ethnic armed groups in Myanmar – launched "Operation 1027" to seize territory from the junta in strategic areas of northern Myanmar (Shan and Kachin state). For economic implications, the conflict has disrupted several land trade routes to neighboring countries given the large share of goods exports that go through land borders (40 percent). Among land exports, agriculture commodities, which comprise about a third of land exports, are the most vulnerable. Disruptions to border trade have the potential to affect the availability and prices of some consumer imports, as well as firms’ access to key production inputs

-

The unrest has also disrupted infrastructure projects along the China-Myanmar Economic Corridor (CMEC), which seeks to connect China to the Indian Ocean through various roads, railways, and pipelines. Furthermore, there are broader implications for the political landscape. The general elections, initially scheduled for 2025, may face significant delays or possibly be accelerated, depending on the military's ability to contain the situation and manage internal conflicts within the government.

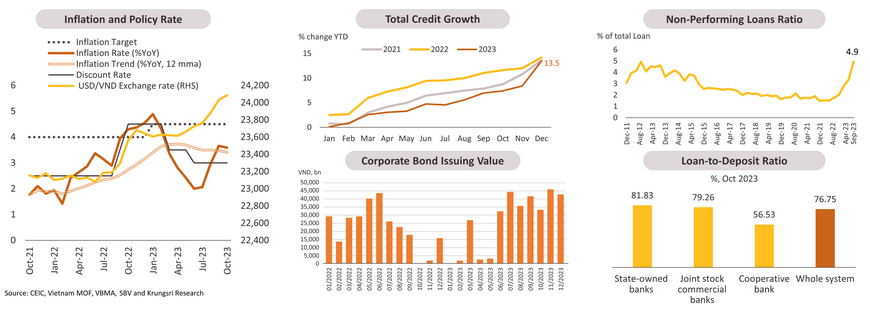

Vietnam: Modest growth projected ahead, contributed by countercyclical policies, improving domestic demand, and resilient FDI.

-

After a robust post-pandemic recovery, the economy has been hit by financial market turbulence and a sharp deterioration in export demand since late 2022. Thus, the 2023 growth slowed from a robust 8 percent in 2022 to 5.05 percent, mainly driven by domestic consumption and expansionary fiscal policies.

-

In 2024, Vietnam’s economy is expected to grow by a robust 5.8 percent, fueled by domestic demand, supported by ongoing fiscal stimulus measures including extended VAT cuts and accelerated public investment spending. More accommodative monetary policy is also expected to lend further support, as inflation remains within the target range and growth stays below pre-pandemic levels. Trade activities are expected to modestly rebound despite headwinds from soft global growth. Tourism receipts and resilient foreign direct investment (FDI) inflows are expected to support the trade balance.

Goods exports dip, tourism revives amid global economic uncertainty.

-

In 2023, total exports dropped -4.3 percent compared to the previous year, although gradual export growth picked up in the fourth quarter of 2023, led primarily by agricultural products. A drop in goods exports was mainly due to slowing economic growth in Vietnam's primary export destinations, particularly the US, China, and the EU. However, Vietnam’s services export was resilient with tourism growth of 34 percent in 2023. Trade surpluses reached record levels as imports fell. Given that raw and auxiliary materials and fuel account for 94 percent of total imports, a decline in imports is consistent with a slowing manufacturing, due to a dip in exports and domestic activities.

-

Going forward, a modest rebound in goods exports is expected. The tourism industry has expansive room to restore pre-pandemic levels. It ensures that the sector remains robust despite a moderate rate of expansion given the subsided reopening effect. In terms of imports, improving exports and domestic activities would increase import demand, particularly manufacturing materials. While soft global growth and geopolitical conflicts as the potential headwinds to the export recovery, enhancements in political relations with China and the US, along with various established FTAs, could potentially have upsides for its exports growth to meet the government's 6 percent target in 2024.

Domestic demand will be main economic driver in 2024.

-

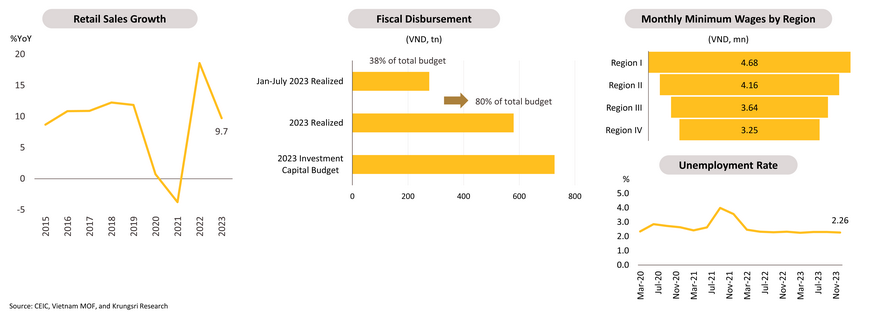

Domestic consumption was the only pillar to reach the target in 2023 with total retail sales of goods and consumer services revenue increased 9.7 percent. However, despite persistent efforts and measures to expedite the disbursement of public investments, the country had only accomplished approximately 80 percent by the end of 2023, falling short of its intended target of 95 percent.

-

Further recovery in domestic demand is expected in 2024, underpinned by government stimulus policies. The government has committed to continuing fiscal support through measures including the extension of VAT cut from 10 to 8 percent until June 2024 (introduced in July 2023) and the accelerated disbursement of public investment projects, which will further inflate domestic investment. Nevertheless, in 2024, public investment disbursement will still be burdened by overlapping laws and regulations unless there are significant changes.

-

The minimum wage in the business sector will rise by 6 percent in July 2024 as agreed by labor and business representatives in December 2023. This minimum wage hike will also apply to public officials during the same period. The wage increase plan was assessed in the wake of economic challenges and complicated trade barriers. Coupled with strong labor conditions (reflected by a low unemployment rate of 2.26 percent), this wage hike will likely be another driver boosting domestic consumption in the second half of 2024.

Regulators slowed the downward spiral in financial markets, but spillover risks persist.

-

During the first half of 2023, the State Bank of Vietnam (SBV) eased its monetary policy to support businesses and alleviate the real estate sector's liquidity crunch by lowering its benchmark rate by 150 basis points from 4.5 to 3 percent. However, the depreciation of VND, influenced by tightened external financial conditions, and elevated inflation amid higher oil and food prices, has prevented the SBV from adopting further rate cuts. Easing monetary policy has resulted in a rebound in credit growth. Though growth in the first 11 months was far below the annual target of 14–15 percent, banks accelerated lending in the final month of 2023 reaching annual credit growth at 13.5 percent due to the PM’s order. Going forward, the benign inflation outlook and stabilized credit growth should give the SBV to focus on another mandate: FX stability. We expect the SBV will resume rate cuts once see visible signs of easing global financial conditions, thus less pressure on VND, given growth staying below the trend.

-

While policymakers have managed to stabilize financial markets by easing liquidity pressures and restoring confidence in financial markets, particularly in the real estate and banking sector, risks in the financial sector remain. Corporate bond issuances have rebounded in the second half from a collapse since late 2022. In the aftermath of the real estate and Corporate Bond Markets (CBMs) turbulence, asset quality has been worsening, evident in the rise of NPLs to the 11-year high of 4.9 percent of total loans in September 2023. NPLs could rise further as payment rescheduling negotiations continue, especially if the payment rescheduling measure is not extended. This suggests that irregularities in CBMs and the real estate sector may have a higher risk of spillover into the banking sector. However, the banking sector is still relatively resilient with the Capital Adequacy Ratio (CAR) above the required level at 11.5 percent in September, and the loan-to-deposit ratio below the 85 percent threshold. Together with expected ongoing countercyclical measures, systemic risks, albeit rising, are perceived to be limited.

Foreign direct investment remains a key engine over the medium-term

-

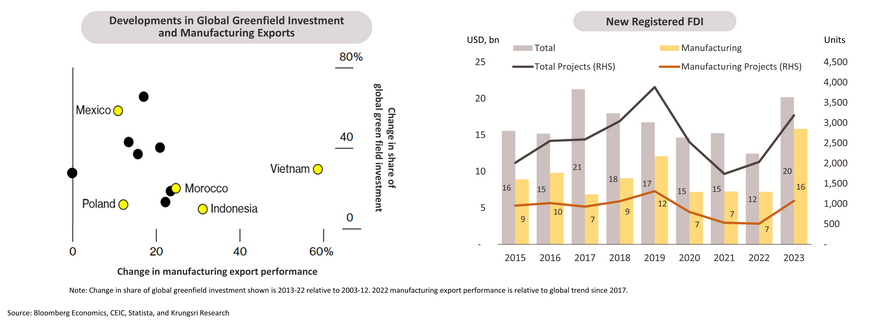

Vietnam will remain one of the brightest spots in the region with GDP growth averaging 6.7 percent over the next 5 years. Its competitive labor costs, sizeable domestic market, industrial park infrastructure readiness, a growing number of trade agreements, both bilateral and multilateral, along with a supply-chain diversification trend, will support a steady inflow of FDI, particularly manufacturing activities.

-

The developments in this regard have been promising. According to Bloomberg Economics, electronics manufacturers have relocated their factories from China to Vietnam after the US placed tariffs on Chinese goods in recent years. Since 2017, Vietnam has seen a 60 percent change in manufacturing export performance relative to the global trend. In comparison to 2003-2012, Vietnam’s share of global green field investment (a type of foreign direct investment where a company establishes new operations in a foreign country) increased by 29 percent between 2013 and 2022. It is also worth keeping an eye on their role in becoming a notable player in semiconductor supply chains. The seeking of opportunities and diversification in the global semiconductor industry by the US through the partnership, along with strong government support, is driving the rapid expansion of Vietnam's semiconductor industry, thus supporting the export of electronic goods.

-

In 2023, there has been a strong influx of Foreign Direct Investment (FDI) into manufacturing and processing which is expected to significantly contribute to boosting GDP growth over the medium term. The value of newly registered FDI in 2023 almost doubled that of the previous year, as well as the amount of newly registered FDI in manufacturing.

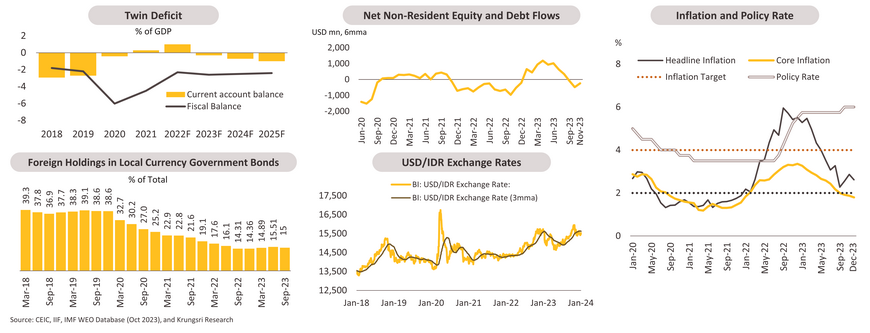

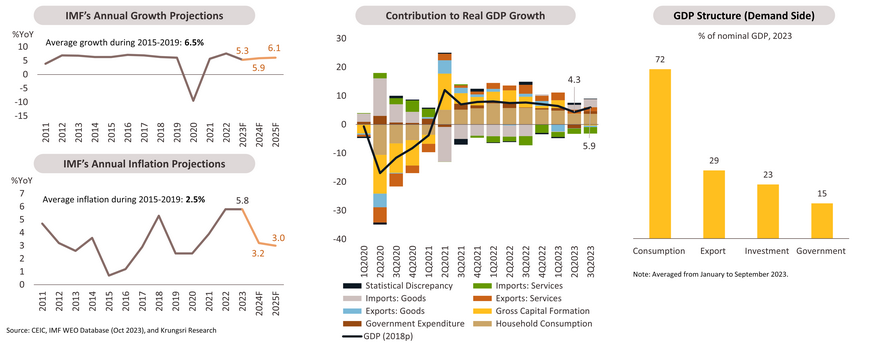

Indonesia: Cyclical outlook still intact with robust domestic demand

-

The Indonesian economy moderated slightly in 2023 with growth slowed from 5.3 percent in 2022 to 5 percent, amid normalization of commodity prices and tight monetary policy setting. Growth is projected to grow steadily at 5 percent in 2024 with relatively strong domestic demand and pre-election spending. Inflation returned to the target band in the second half of 2023 as a result of lower commodity prices and the government’s push to stabilize food prices. Inflation is expected to stay within Bank Indonesia (BI)’s revised target of 1.5-3.5 percent for 2024. The main source of inflationary pressure is likely to come from food prices, given lower domestic yields of rice from El Niño. The next move of BI would be to ease if external conditions turn more conducive to exchange rate stability.

-

Key near-term headwinds include heightened volatility in global financial conditions and uncertainties of policy direction related to the 2024 general election which might weigh on private investment momentum.

Resilient consumption to continue, while further private investment recovery is not expected until after the political transition.

-

Initially, Indonesia’s recovery was supported by a rise in commodity prices and improving terms of trade. In this stage, the growth drivers have been consumption- and capex-led recovery, rather than commodity exports, thanks to its high dependence on domestic demand. Private consumption has been resilient, and overall household fundamentals likely continue to improve as unemployment finally declined nearly to pre-Covid levels. The momentum is expected to remain relatively strong, but some moderation could be seen with elevated real interest rates.

-

Fixed investment has expanded, driven by construction spending, which hit a bottom in 1Q23 and has been increasing since then. A surge in capital goods imports reflects capex expansion. Construction growth has been supported by a last-mile run of government projects ahead of the election. Looking ahead, election-related spending, both from the government’s ramp-up of construction (basic infrastructure and buildings in the new capital city ‘Nusantara’), and political parties will also further lend support to the growth. Capacity utilization in manufacturing has returned to pre-covid level at 74.4 percent in 3Q23. The recovery has been mostly broad-based. However, a further private sector capex rebound is not yet pinned until post-political transition.

Sustaining growth momentum with prudent macroeconomic policies.

-

A prudent fiscal and conventional monetary policy mix has helped to anchor macro stability and created a conducive environment for growth momentum. Fiscal policy has been conservative with fiscal deficit hovering around 2.5 percent to GDP. Indonesia has ample fiscal policy space to respond to adverse supply-side shocks, with relatively low government debt at 40 percent to GDP. In terms of monetary policy, owing to its reliance on external funding (as reflected by the twin deficit and a moderate ratio of foreign holdings in government bonds, albeit a downward trend), the country is vulnerable to global financial conditions. Portfolio outflows in recent months, on the backdrop of global economic uncertainty and geopolitical tensions, have worsened the imbalance in the FX market, leading to an unexpected 25 bps policy rate hike in the October 2023 policy meeting after an extended pause since January 2023.

-

Recently, BI has employed a mix of monetary tools. They use the policy rate to stabilize financial markets while adopting a pro-growth macroprudential policy stance to support economic activity. The 2024 inflation target will be lowered to 1.5-3.5 percent, with inflation projected to fall within this range. If external financial conditions are constructive and domestic inflation remains manageable, BI could introduce rate cuts in late 2024 or when the Fed signals a rate cut.

Medium-term factors inducing foreign investments remain intact

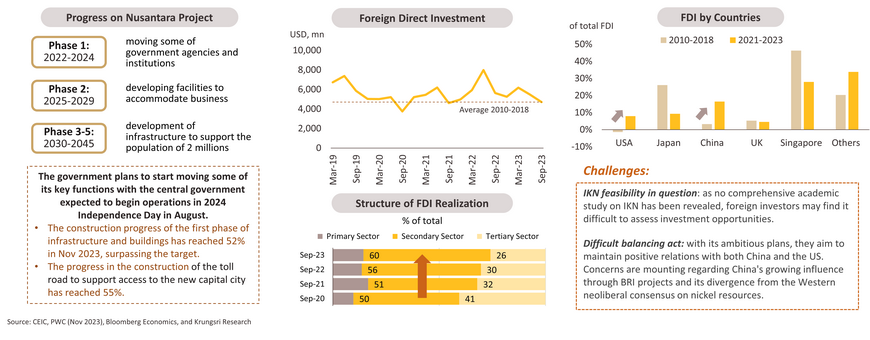

In the near term, FDI to Indonesia would benefit from the government’s focus on foreign investors to develop the new capital city ‘Nusantara’ and the trend of global economic fragmentation.

-

Nusantara (IKN project): The authority stated that 80 percent of government buildings and basic infrastructure will be handed over to the private sector to finance. The government is rolling out incentives to attract foreign investors to invest in the new capital. The incentives include up to 30 years of tax breaks for investment in targeted industries such as infrastructure and public services. The government claimed that they have collected 300 investment commitments from foreign investors, investment realization is thus expected to follow.

-

Global economic fragmentation: With an abundance of natural resources, an immense domestic market, and government initiatives, Indonesia has welcomed companies from both the US and China to build onshore value-added in the downstream commodity sector, particularly in the entire EV supply chain. During 2013-2022, Indonesia had a 10 percent increase in the share of global greenfield investment (new plants and other facilities by a foreign company establishing operations in another country), compared to 2003-2012. Investment trend in the manufacturing sector is expected to be resilient, driven by global trends in technology and environment, along with the anticipated continuation of government support.

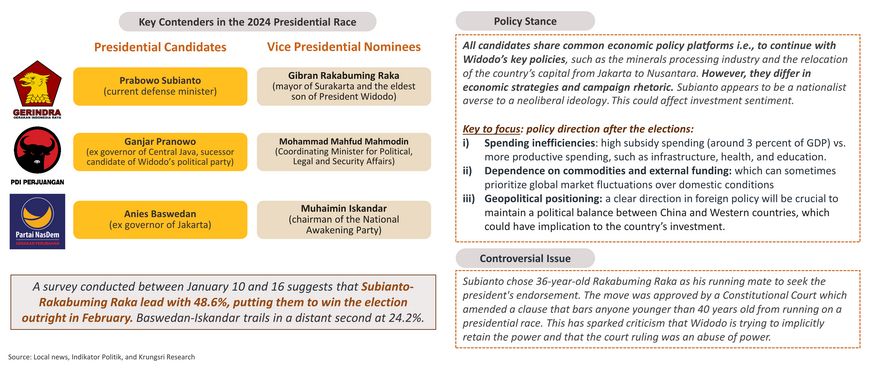

Issues to watch in 2024: General and presidential election

As the constitution caps each president from being elected for more than two terms, incumbent President Joko Widodo will step down. Presidential elections will be held on February 14, 2024. The leading candidate has to win a nationwide majority of votes and at least 20 percent of the votes in over half of Indonesia’s provinces—otherwise, the top two candidate pairs will face-off in a second electoral round on June 26, 2024. An inconclusive outcome in the first round of voting may lead to increased uncertainty around the macro policy environment. It could dampen private sector confidence and weigh on domestic demand.

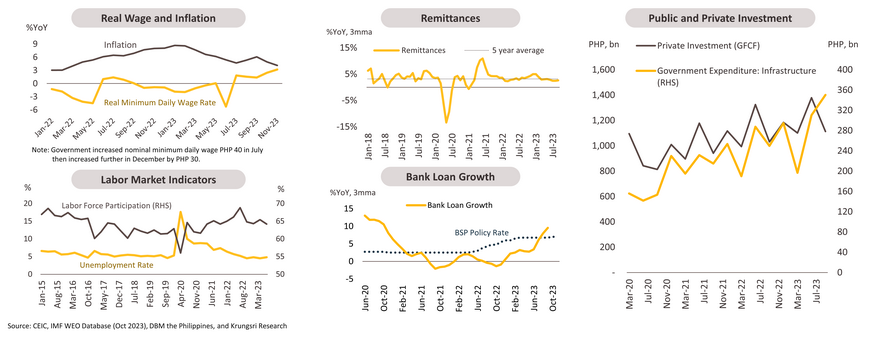

Philippines: Strong economic expansion in the region is driven by robust domestic consumption.

-

In 2023, the economic expansion is forecast to slow down to 5.3 percent from 7.6 percent in the previous year, due to moderating domestic consumption resulting from a positive real interest rate and the post-pandemic’s momentum waning. Private investment also slowed due to uncertainties in private consumption and shrinking exports.

-

Growth is predicted to rebound to 5.9 percent in 2024, with major support from domestic demand, including private consumption and government spending. Private investment is also expected to recover, driven by infrastructure spending by the public sector. Despite the projection that inflation will fall below the central bank (BSP)'s target range in 2024, the BSP will likely maintain the policy rate at a constant high level until there is a clear signal of price stability, especially considering potential upside inflationary pressure from El Niño and the Fed’s monetary policy stance.

Private consumption and government spending on public infrastructure will be major contributors to resilient domestic demand

-

Domestic consumption, accounting for more than 70 percent of GDP, is expected to remain robust in 2024, supported by easing inflation, a higher real wage, strong employment (unemployment rate at the lowest in 18 years), and minimum wage hikes. Following moderate loan growth in the first half of 2023, the expansion in bank loan growth reflects that the momentum of relatively resilient private consumption should continue. Positive growth in overseas workers’ income remittances, constituting nearly 10 percent of GDP, is also expected to continue supporting private consumption, despite a moderate slowdown against the backdrop of a more challenging global economy.

-

Government consumption will be another key growth engine in 2024 following its announcement of a 6.6 percent increase in infrastructure expenditure (or approximately PHP 1.42 trillion) through the Build-Better-More Program in 2024, or equivalently 5.3 percent of GDP, with almost half allocated for the construction of accessible road networks and railways.

Spillover from public investment is expected to support a recovery in private investment, while the impact of geopolitical tensions is anticipated to be insignificant.

-

Private investment has remained subdued due to moderated domestic consumption and the impact of monetary policy tightening. In 2024, spillover effects from public infrastructure investment, along with a modest recovery in goods exports, particularly electronic products (accounting for 57 percent of total exports), are expected to support the recovery of private investment.

-

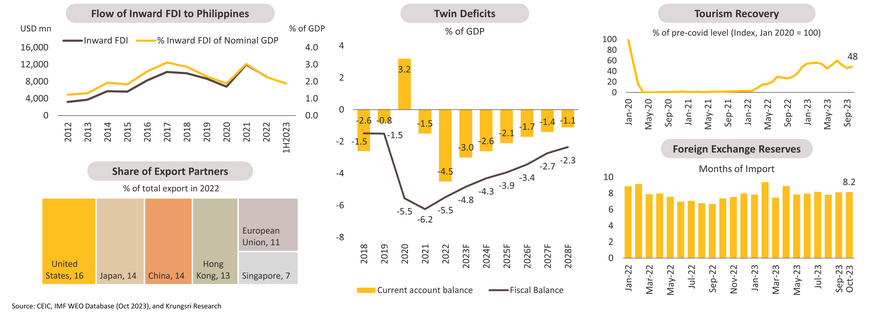

The impact of geopolitical tensions, particularly in the South China Sea conflict with China, so far there are no signs of aggressive economic pressure from China or supply chain disruption. However, if the tensions continue to escalate, it will accordingly affect private sentiments in the country. Noteworthily, China is the Philippines' third-largest export destination, and out of the total FDI, which accounts for roughly 10% of the Philippines' GDP, 14% originates from China.

-

External stability appears robust, with the twin deficit exhibiting a narrower gap as the government continues to increase revenues following the budget consolidation plan. Additionally, the trade deficit is decreasing due to the modest growth of imports and further support from tourism recovery. Foreign exchange reserves are ample, covering about 8 months of imports (October 2023).

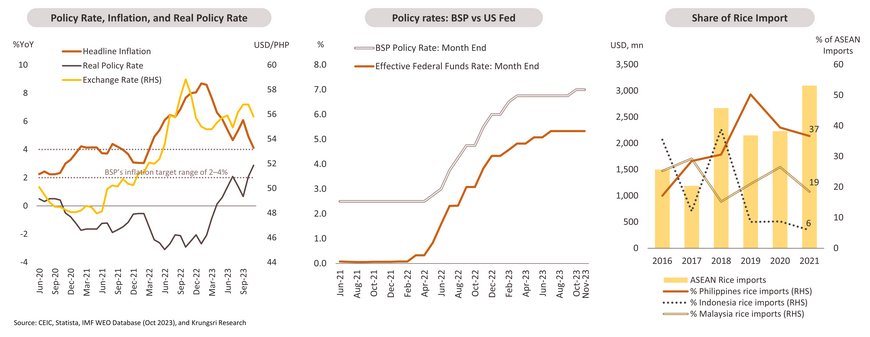

BSP to manage risks amid global and domestic pressures, maintaining the policy rate at a high level with a potential cut in the second half.

On price stability, inflation is expected to stay within the BSP's target range of 2–4 percent in 2024. However, upside risk arises from El Niño, which may keep global rice prices elevated and supply tight among regional exporters. The weaker local currency (PHP) could still add to the overall impact of costly imported key food products, particularly since the Philippines has a high share of rice imports in ASEAN, accounting for more than 35 percent of the total rice imports in ASEAN. Currently, the BSP’s stance is hawkish, trying to ensure inflation expectations remain well anchored (to curb the second-round effect from cost-push factors) and stabilize its currency. Going forward, we expect the BSP to maintain an unchanged policy rate through the first half of 2024. Given signs of constant disinflation, growth staying subpar, and the Fed’s easing stance, the BSP could deliver rate cuts in the second half.